Bar Count Per SessionCount K bars based on sessions, supporting at most 3 sessions

- Customize the session's timezone and period

- Set the steps between each number

- Use with the built-in `Trading Session` is a great convenience

Statistics

STRATEGY 1 │ Red Dragon │ Model 1 │ [Titans_Invest]The Red Dragon Model 1 is a fully automated trading strategy designed to operate BTC/USDT.P on the 4-hour chart with precision, stability, and consistency. It was built to deliver reliable behavior even during strong market movements, maintaining operational discipline and avoiding abrupt variations that could interfere with the trader’s decision-making.

Its core is based on a professionally engineered logical structure that combines trend filters, confirmation criteria, and balanced risk management. Every component was designed to work in an integrated way, eliminating noise, avoiding unnecessary trades, and protecting capital in critical moments. There are no secret mechanisms or hidden logic: everything is built to be objective, clean, and efficient.

Even though it is based on professional quantitative engineering, Red Dragon Model 1 remains extremely simple to operate. All logic is clearly displayed and fully accessible within TradingView itself, making it easy to understand for both beginners and experienced traders. The structure is organized so that any user can quickly view entry conditions, exit criteria, additional filters, adjustable parameters, and the full mechanics behind the strategy’s behavior.

In addition, the architecture was built to minimize unnecessary complexity. Parameters are straightforward, intuitive, and operate in a balanced way without requiring deep adjustments or advanced knowledge. Traders have full freedom to analyze the strategy, understand the logic, and make personal adaptations if desired—always with total transparency inside TradingView.

The strategy was also designed to deliver consistent operational behavior over the long term. Its confirmation criteria reduce impulsive trades; its filters isolate noise; and its overall logic prioritizes high-quality entries in structured market movements. The goal is to provide a stable, clear, and repeatable flow—essential characteristics for any medium-term quantitative approach.

Combining clarity, professional structure, and ease of use, Red Dragon Model 1 offers a solid foundation both for users who want a ready-to-use automated strategy and for those looking to study quantitative models in greater depth.

This entire project was built with extreme dedication, backed by more than 14,000 hours of hands-on experience in Pine Script, continuously refining patterns, techniques, and structures until reaching its current level of maturity. Every line of code reflects this long process of improvement, resulting in a strategy that unites professional engineering, transparency, accessibility, and reliable execution.

🔶 MAIN FEATURES

• Fully automated and robust: Operates without manual intervention, ideal for traders seeking consistency and stability. It delivers reliable performance even in volatile markets thanks to the solid quantitative engineering behind the system.

• Multiple layers of confirmation: Combines 10 key technical indicators with 15 adaptive filters to avoid false signals. It only triggers entries when all trend, market strength, and contextual criteria align.

• Configurable and adaptable filters: Each of the 15 filters can be enabled, disabled, or adjusted by the user, allowing the creation of personalized statistical models for different assets and timeframes. This flexibility gives full freedom to optimize the strategy according to individual preferences.

• Clear and accessible logic: All entry and exit conditions are explicitly shown within the TradingView parameters. The strategy has no hidden components—any user can quickly analyze and understand each part of the system.

• Integrated exclusive tools: Includes complete backtest tables (desktop and mobile versions) with annualized statistics, along with real-time entry conditions displayed directly on the chart. These tools help monitor the strategy across devices and track performance and risk metrics.

• No repaint: All signals are static and do not change after being plotted. This ensures the trader can trust every entry shown without worrying about indicators rewriting past values.

🔷 ENTRY CONDITIONS & RISK MANAGEMENT

Red Dragon Model 1 triggers buy (long) or sell (short) signals only when all configured conditions are satisfied. For example:

• Volume:

• The system only trades when current volume exceeds the volume moving average multiplied by a user-defined factor, indicating meaningful market participation.

• RSI:

• Confirms bullish bias when RSI crosses above its moving average, and bearish bias when crossing below.

• ADX:

• Enters long when +DI is above –DI with ADX above a defined threshold, indicating directional strength to the upside (and the opposite conditions for shorts).

• Other indicators (MACD, SAR, Ichimoku, Support/Resistance, etc.)

Each one must confirm the expected direction before a final signal is allowed.

When all bullish criteria are met simultaneously, the system enters Long; when all criteria indicate a bearish environment, the system enters Short.

In addition, the strategy uses fixed Take Profit and Stop Loss targets for risk control:

Currently: TP around 1.5% and SL around 2.0% per trade, ensuring consistent and transparent risk management on every position.

⚙️ INDICATORS

__________________________________________________________

1) 🔊 Volume: Avoids trading on flat charts.

2) 🍟 MACD: Tracks momentum through moving averages.

3) 🧲 RSI: Indicates overbought or oversold conditions.

4) 🅰️ ADX: Measures trend strength and potential entry points.

5) 🥊 SAR: Identifies changes in price direction.

6) ☁️ Cloud: Accurately detects changes in market trends.

7) 🌡️ R/F: Improves trend visualization and helps avoid pitfalls.

8) 📐 S/R: Fixed support and resistance levels.

9)╭╯MA: Moving Averages.

10) 🔮 LR: Forecasting using Linear Regression.

__________________________________________________________

🟢 ENTRY CONDITIONS 🔴

__________________________________________________________

IF all conditions are 🟢 = 📈 Long

IF all conditions are 🔴 = 📉 Short

__________________________________________________________

🚨 CURRENT TRIGGER SIGNAL 🚨

__________________________________________________________

🔊 Volume

🟢 LONG = (volume) > (MA_volume) * (Volume Mult)

🔴 SHORT = (volume) > (MA_volume) * (Volume Mult)

🧲 RSI

🟢 LONG = (RSI) > (RSI_MA)

🔴 SHORT = (RSI) < (RSI_MA)

🟢 ALL ENTRY CONDITIONS AVAILABLE 🔴

__________________________________________________________

🔊 Volume

🟢 LONG = (volume) > (MA_volume) * (Volume Mult)

🔴 SHORT = (volume) > (MA_volume) * (Volume Mult)

🔊 Volume

🟢 LONG = (volume) > (MA_volume) * (Volume Mult) and (close) > (open)

🔴 SHORT = (volume) > (MA_volume) * (Volume Mult) and (close) < (open)

🍟 MACD

🟢 LONG = (MACD) > (Signal Smoothing)

🔴 SHORT = (MACD) < (Signal Smoothing)

🧲 RSI

🟢 LONG = (RSI) < (Upper)

🔴 SHORT = (RSI) > (Lower)

🧲 RSI

🟢 LONG = (RSI) > (RSI_MA)

🔴 SHORT = (RSI) < (RSI_MA)

🅰️ ADX

🟢 LONG = (+DI) > (-DI) and (ADX) > (Treshold)

🔴 SHORT = (+DI) < (-DI) and (ADX) > (Treshold)

🥊 SAR

🟢 LONG = (close) > (SAR)

🔴 SHORT = (close) < (SAR)

☁️ Cloud

🟢 LONG = (Cloud A) > (Cloud B)

🔴 SHORT = (Cloud A) < (Cloud B)

☁️ Cloud

🟢 LONG = (Kama) > (Kama )

🔴 SHORT = (Kama) < (Kama )

🌡️ R/F

🟢 LONG = (high) > (UP Range) and (upward) > (0)

🔴 SHORT = (low) < (DOWN Range) and (downward) > (0)

🌡️ R/F

🟢 LONG = (high) > (UP Range)

🔴 SHORT = (low) < (DOWN Range)

📐 S/R

🟢 LONG = (close) > (Resistance)

🔴 SHORT = (close) < (Support)

╭╯MA2️⃣

🟢 LONG = (Cyan Bar MA2️⃣)

🔴 SHORT = (Red Bar MA2️⃣)

╭╯MA2️⃣

🟢 LONG = (close) > (MA2️⃣)

🔴 SHORT = (close) < (MA2️⃣)

╭╯MA2️⃣

🟢 LONG = (Positive MA2️⃣)

🔴 SHORT = (Negative MA2️⃣)

__________________________________________________________

🎯 TP / SL 🛑

__________________________________________________________

🎯 TP: 1.5 %

🛑 SL: 2.0 %

__________________________________________________________

🪄 UNIQUE FEATURES OF THIS STRATEGY

____________________________________

1) 𝄜 Table Backtest for Mobile.

2) 𝄜 Table Backtest for Computer.

3) 𝄜 Table Backtest for Computer & Annual Performance.

4) 𝄜 Live Entry Conditions.

1) 𝄜 Table Backtest for Mobile.

2) 𝄜 Table Backtest for Computer.

3) 𝄜 Table Backtest for Computer & Annual Performance.

4) 𝄜 Live Entry Conditions.

_____________________________

𝄜 BACKTEST / PERFORMANCE 𝄜

_____________________________

• Net Profit: +634.47%, Maximum Drawdown: -18.44%.

🪙 PAIR / TIMEFRAME ⏳

🪙 PAIR: BINANCE:BTCUSDT.P

⏳ TIME: 4 hours (240m)

✅ ON ☑️ OFF

✅ LONG

✅ SHORT

🎯 TP / SL 🛑

🎯 TP: 1.5 (%)

🛑 SL: 2.0 (%)

⚙️ CAPITAL MANAGEMENT

💸 Initial Capital: 10000 $ (TradingView)

💲 Order Size: 10 % (Of Equity)

🚀 Leverage: 10 x (Exchange)

💩 Commission: 0.03 % (Exchange)

📆 BACKTEST

🗓️ Start: Setember 24, 2019

🗓️ End: November 21, 2025

🗓️ Days: 2250

🗓️ Yers: 6.17

🗓️ Bars: 13502

📊 PERFORMANCE

💲 Net Profit: + 63446.89 $

🟢 Net Profit: + 634.47 %

💲 DrawDown Maximum: - 10727.48 $

🔴 DrawDown Maximum: - 18.44 %

🟢 Total Closed Trades: 1042

🟡 Percent Profitable: 63.92 %

🟡 Profit Factor: 1.247

💲 Avg Trade: + 60.89 $

⏱️ Avg # Bars in Trades

🕯️ Avg # Bars: 4

⏳ Avg # Hrs: 15

✔️ Trades Winning: 666

❌ Trades Losing: 376

✔️ Maximum Consecutive Wins: 11

❌ Maximum Consecutive Losses: 7

📺 Live Performance : br.tradingview.com

• Use this strategy on the recommended pair and timeframe above to replicate the tested results.

• Feel free to experiment and explore other settings, assets, and timeframes.

MTF Scalper - alemicihanMulti-Timeframe Scalper Strategy: Aligning the Big Picture for Quick Gains

This article presents a robust futures trading strategy designed for high-frequency scalping in the crypto market. It’s built on the principle of minimizing risk by ensuring that short-term entries are always aligned with the dominant, higher-timeframe trend.

The Core Concept: Alignment is Key

A Balanced Trend Follower approach, now refined for rapid scalping, uses a Multi-Timeframe (MTF) confirmation system to filter out market noise and increase the probability of a successful trade.

The strategy operates on a Low Timeframe (LTF) chart (e.g., 3m, 5m, or 15m) but only executes trades if the direction is validated by three Higher Timeframes (HTF).

ComponentPurposeFunctionHTF (D, 4h, 1h) EMA => Trend Confirmation =>Checks if the current price is above/below all three Exponential Moving Averages (EMA 20). This provides a strong directional bias.

LTF (5m) Stochastic RSI => Momentum Entry => Generates the actual buy/sell signal by spotting a swift crossover, indicating fresh momentum in the direction of the confirmed HTF trend.

How The Signal Is Generated

Trend Alignment: The system first confirms the trend. If the price is trading above the Daily, 4-Hour, and 1-Hour EMAs, the market is deemed to be in a Strong LONG Trend. Only LONG signals are permitted.

Momentum Trigger: Once the trend is confirmed, a Long Signal is generated only when the Stochastic K-Line crosses above the D-Line, indicating a momentum shift (a pullback ending) towards the main trend direction.

Short Signal: The inverse logic applies to the Short Trend confirmation and entry signal.

Mandatory Risk Management: ATR-Based Exit

Given the high leverage nature of futures and scalping, static Stop-Loss (SL) and Take-Profit (TP) levels are inefficient. This strategy uses the Average True Range (ATR) indicator to dynamically set profit and loss targets based on current market volatility.

Stop Loss (SL): Set dynamically at 1.5 x ATR below (for long) or above (for short) the entry price. This gives the trade enough room to breathe without risking excessive capital.

Take Profit (TP): Set dynamically at 3.0 x ATR, establishing a robust Risk-to-Reward Ratio of 1:2.

Final Thoughts on Testing

This sophisticated approach combines the reliability of MTF analysis with the speed of momentum indicators. However, data analysis is key. Backtesting these parameters (EMA, ATR Multipliers, RSI/Stochastic lengths) on your chosen asset (like BTC/USDT or ETH/USDT) and timeframe is crucial to achieving optimal performance.

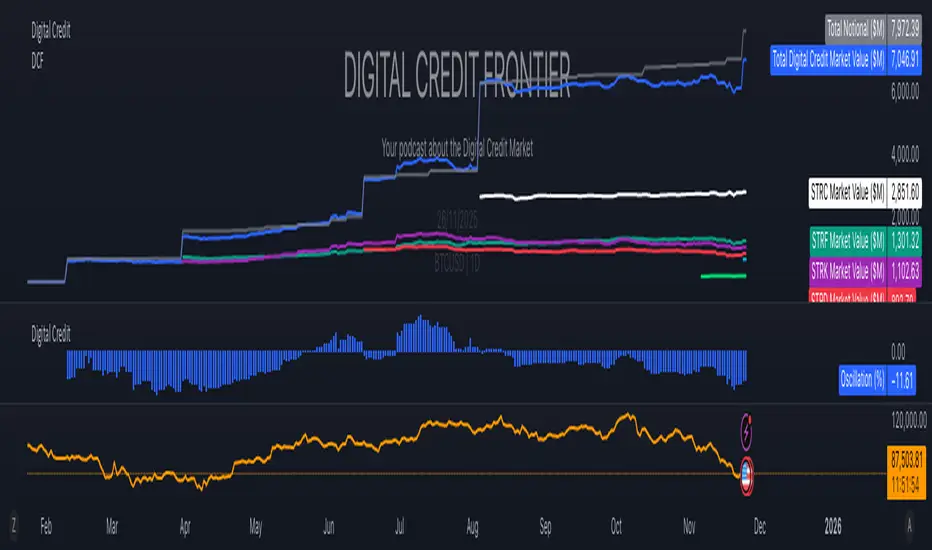

Digital Credit Market ValueDigital Credit Frontier

Script for tracking total notional value and total market value for the Digital Credit Market. Needs be manually updated. You can open it twice to get the total value in one pane and the oscillator in the other pane.

Uptrick: Dynamic Z-Score DivergenceIntroduction

Uptrick: Dynamic Z-Score Divergence is an oscillator that combines multiple momentum sources within a Z-Score framework, allowing for the detection of statistically significant mean-reversion setups, directional shifts, and divergence signals. It integrates a multi-source normalized oscillator, a slope-based signal engine, structured divergence logic, a slope-adaptive EMA with dynamic bands, and a modular bar coloring system. This script is designed to help traders identify statistically stretched conditions, evolving trend dynamics, and classical divergence behavior using a unified statistical approach.

Overview

At its core, this script calculates the Z-Score of three momentum sources—RSI, Stochastic RSI, and MACD—using a user-defined lookback period. These are averaged and smoothed to form the main oscillator line. This normalized oscillator reflects how far short-term momentum deviates from its mean, highlighting statistically extreme areas.

Signals are triggered when the oscillator reverses slope within defined inner zones, indicating a shift in direction while the signal remains in a statistically stretched state. These mean-reversion flips (referred to as TP signals) help identify turning points when price momentum begins to revert from extended zones.

In addition, the script includes a divergence detection engine that compares oscillator pivot points with price pivot points. It confirms regular bullish and bearish divergence by validating spacing between pivots and visualizes both the oscillator-side and chart-side divergences clearly.

A dynamic trend overlay system is included using a Slope Adaptive EMA (SA-EMA). This trend line becomes more responsive when Z-Score deviation increases, allowing the trend line to adapt to market conditions. It is paired with ATR-based bands that are slope-sensitive and selectively visible—offering context for dynamic support and resistance.

The script includes configurable bar coloring logic, allowing users to color candles based on oscillator slope, last confirmed divergence, or the most recent signal of any type. A full alert system is also built-in for key signals.

Originality

The script is based on the well-known concept of Z-Score valuation, which is a standard statistical method for identifying how far a signal deviates from its mean. This foundation—normalizing momentum values such as RSI or MACD to measure relative strength or weakness—is not unique to this script and is widely used in quantitative analysis.

What makes this implementation original is how it expands the Z-Score foundation into a fully featured, signal-producing system. First, it introduces a multi-source composite oscillator by combining three momentum inputs—RSI, Stochastic RSI, and MACD—into a unified Z-Score stream. Second, it builds on that stream with a directional slope logic that identifies turning points inside statistical zones.

The most distinctive additions are the layered features placed on top of this normalized oscillator:

A structured divergence detection engine that compares oscillator pivots with price pivots to validate regular bullish and bearish divergence using precise spacing and timing filters.

A fully integrated slope-adaptive EMA overlay, where the smoothing dynamically adjusts based on real-time Z-Score movement of RSI, allowing the trend line to become more reactive during high-momentum environments and slower during consolidation.

ATR-based dynamic bands that adapt to slope direction and offer real-time visual zones for support and resistance within trend structures.

These features are not typically found in standard Z-Score indicators and collectively provide a unique approach that bridges statistical normalization, structure detection, and adaptive trend modeling within one script.

Features

Z-Score-based oscillator combining RSI, StochRSI, and MACD

Configurable smoothing for stable composite signal output

Buy/Sell TP signals based on slope flips in defined zones

Background highlighting for extreme outer bands

Inner and outer zones with fill logic for statistical context

Pivot-based divergence detection (regular bullish/bearish)

Divergence markers on oscillator and price chart

Slope-Adaptive EMA (SA-EMA) with real-time adaptivity based on RSI Z-Score

ATR-based upper and lower bands around the SA-EMA, visibility tied to slope direction

Configurable bar coloring (oscillator slope, divergence, or most recent signal)

Alerts for TP signals and confirmed divergences

Optional fixed Y-axis scaling for consistent oscillator view

The full setup mode can be seen below:

Input Parameters

General Settings

Full Setup: Enables rendering of the full visual system (lines, bands, signals)

Z-Score Lookback: Lookback period for normalization (mean and standard deviation)

Main Line Smoothing: EMA length applied to the averaged Z-Score

Slope Detection Index: Used to calculate directional flips for signal logic

Enable Background Highlighting: Enables visual region coloring in

overbought/oversold areas

Force Visible Y-Axis Scale: Forces max/min bounds for a consistent oscillator range

Divergence Settings

Enable Divergence Detection: Toggles divergence logic

Pivot Lookback Left / Right: Defines the structure of oscillator pivot points

Minimum / Maximum Bars Between Pivots: Controls the allowed spacing range for divergence validation

Bar Coloring Settings

Bar Coloring Mode:

➜ Line Color: Colors bars based on oscillator slope

➜ Latest Confirmed Signal: Colors bars based on the most recent confirmed divergence

➜ Any Latest Signal: Colors based on the most recent signal (TP or divergence)

SA-EMA Settings

RSI Length: RSI period used to determine adaptivity

Z-Score Length: Lookback for normalizing RSI in adaptive logic

Base EMA Length: Base length for smoothing before adaptivity

Adaptivity Intensity: Scales the smoothing responsiveness based on RSI deviation

Slope Index: Determines slope direction for coloring and band logic

Band ATR Length / Band Multiplier: Controls the width and responsiveness of the trend-following bands

Alerts

The script includes the following alert conditions:

Buy Signal (TP reversal detected in oversold zone)

Sell Signal (TP reversal detected in overbought zone)

Confirmed Bullish Divergence (oscillator HL, price LL)

Confirmed Bearish Divergence (oscillator LH, price HH)

These alerts allow integration into automation systems or signal monitoring setups.

Summary

Uptrick: Dynamic Z-Score Divergence is a statistically grounded trading indicator that merges normalized multi-momentum analysis with real-time slope logic, divergence detection, and adaptive trend overlays. It helps traders identify mean-reversion conditions, divergence structures, and evolving trend zones using a modular system of statistical and structural tools. Its alert system, layered visuals, and flexible input design make it suitable for discretionary traders seeking to combine quantitative momentum logic with structural pattern recognition.

Disclaimer

This script is for educational and informational purposes only. No indicator can guarantee future performance, and trading involves risk. Always use risk management and test strategies in a simulated environment before deploying with live capital.

Now PDC ±0.5% & ±0.7% Levels (Custom Lines)Net Change of Instrument movement for the day. Enhances perception of price action

Pair Cointegration & Static Beta Analyzer (v6)Pair Cointegration & Static Beta Analyzer (v6)

This indicator evaluates whether two instruments exhibit statistical properties consistent with cointegration and tradable mean reversion.

It uses long-term beta estimation, spread standardization, AR(1) dynamics, drift stability, tail distribution analysis, and a multi-factor scoring model.

1. Static Beta and Spread Construction

A long-horizon static beta is estimated using covariance and variance of log-returns.

This beta does not update on every bar and is used throughout the entire model.

Beta = Cov(r1, r2) / Var(r2)

Spread = PriceA - Beta * PriceB

This “frozen” beta provides structural stability and avoids rolling noise in spread construction.

2. Correlation Check

Log-price correlation ensures the instruments move together over time.

Correlation ≥ 0.85 is required before deeper cointegration diagnostics are considered meaningful.

3. Z-Score Normalization and Distribution Behavior

The spread is standardized:

Z = (Spread - MA(Spread)) / Std(Spread)

The following statistical properties are examined:

Z-Mean: Should be close to zero in a stationary process

Z-Variance: Measures amplitude of deviations

Tail Probability: Frequency of |Z| being larger than a threshold (e.g. 2)

These metrics reveal whether the spread behaves like a mean-reverting equilibrium.

4. Mean Drift Stability

A rolling mean of the spread is examined.

If the rolling mean drifts excessively, the spread may not represent a stable long-term equilibrium.

A normalized drift ratio is used:

Mean Drift Ratio = Range( RollingMean(Spread) ) / Std(Spread)

Low drift indicates stable long-run equilibrium behavior.

5. AR(1) Dynamics and Half-Life

An AR(1) model approximates mean reversion:

Spread(t) = Phi * Spread(t-1) + error

Mean reversion requires:

0 < Phi < 1

Half-life of reversion:

Half-life = -ln(2) / ln(Phi)

Valid half-life for 10-minute bars typically falls between 3 and 80 bars.

6. Composite Scoring Model (0–100)

A multi-factor weighted scoring system is applied:

Component Score

Correlation 0–20

Z-Mean 0–15

Z-Variance 0–10

Tail Probability 0–10

Mean Drift 0–15

AR(1) Phi 0–15

Half-Life 0–15

Score interpretation:

70–100: Strong Cointegration Quality

40–70: Moderate

0–40: Weak

A pair is classified as cointegrated when:

Total Score ≥ Threshold (default = 70)

7. Main Cointegration Panel

Displays:

Static beta

Log-price correlation

Z-Mean, Z-Variance, Tail Probability

Drift Ratio

AR(1) Phi and Half-life

Composite score

Overall cointegration assessment

8. Beta Hedge Position Sizing (Average-Price Based)

To provide a more stable hedge ratio, hedge sizing is computed using average prices, not instantaneous prices:

AvgPriceA = SMA(PriceA, N)

AvgPriceB = SMA(PriceB, N)

Required B per 1 A = Beta * (AvgPriceA / AvgPriceB)

Using averaged prices results in a smoother, more reliable hedge ratio, reducing noise from bar-to-bar volatility.

The panel displays:

Required B security for 1 A security (average)

This represents the beta-neutral quantity of B required to hedge one unit of A.

Overview of Classical Stationarity & Cointegration Methods

The principal econometric tools commonly used in assessing stationarity and cointegration include:

Augmented Dickey–Fuller (ADF) Test

Phillips–Perron (PP) Test

KPSS Test

Engle–Granger Cointegration Test

Phillips–Ouliaris Cointegration Test

Johansen Cointegration Test

Since these procedures rely on regression residuals, matrix operations, and distribution-based critical values that are not supported in TradingView Pine Script, a practical multi-criteria scoring approach is employed instead. This framework leverages metrics that are fully computable in Pine and offers an operational proxy for evaluating cointegration-like behavior under platform constraints.

References

Engle & Granger (1987), Co-integration and Error Correction

Poterba & Summers (1988), Mean Reversion in Stock Prices

Vidyamurthy (2004), Pairs Trading

Explanation structured with assistance from OpenAI’s ChatGPT

Regards.

GVI – Guendogan Valuation IndexGlobalization-adjusted valuation indicator modeling rising international revenue exposure since 1990. Includes a long-term fair-value framework.

Prob Stats PPIBW Prob Stats PPIBW - Data-Driven Trading Decisions

Transform historical price patterns into actionable probabilities. This indicator analyzes thousands of periods to show you the real odds behind pivot hits, range

expansions, inside bars, and weekend breakouts.

What It Tracks

Pivot Hit Rates (D/W/M/Q/6M/Y)

What percentage of pivot points get touched during their period? Includes recent period comparison to spot regime changes.

Example: "Daily: 82.3% (450/547) | L30: 76.7% (23/30)"

Previous Period Levels (D/W/M)

How often does current period break previous period's high or low? Only counts actual range expansion, not equilibrium crossings. Helps gauge breakout probability.

Inside Bar Analysis (D/W/M)

When price consolidates inside previous period's range, what are the odds of a breakout? Only appears when currently in an inside bar.

Weekend Breakdown

When Sat/Sun breaks Mon-Fri range, does the following week continue? Critical for crypto traders and weekend gap analysis.

Key Features

- Recent Period Comparison: See if recent behavior differs from historical averages

- Self-Documenting: Hover over any header for instant explanations

- Color-Coded Sections: Yellow (Pivots), Orange (Prev Period), Pink (Inside Bar), Green (Weekend)

- Blue Background: Recent stats highlighted for easy identification

- Dynamic Layout: Adapts based on market conditions

- Real-Time Updates: Includes current period for live probability tracking

How To Use

1. Add to any chart (best on Daily+ for maximum historical data)

2. Hover over column headers to understand each statistic

3. Compare historical vs recent probabilities

4. Use probabilities to inform position sizing and expectations

Example: Weekly pivot shows 78% historical hit rate but only 60% in last 30 weeks. Recent regime change suggests lower probability of test.

Technical Details

- Pine Script v6

- Rolling window arrays track last 30/30/12 periods for D/W/M

- Previous Period excludes EQ crossings for accurate stats

- Works on all timeframes, optimized for Daily+

- Configurable table position

Perfect For

Traders seeking data-driven confirmation, those wanting to quantify probability vs guessing, regime change detection, and crypto traders analyzing weekend patterns.

Note: Past performance doesn't guarantee future results. Use these statistics as one input in your overall trading strategy.

FVG – (auto close + age) GR V1.0FVG – Fair Value Gaps (auto close + age counter)

Short Description

Automatically detects Fair Value Gaps (FVGs) on the current timeframe, keeps them open until price fully fills the gap or a maximum bar age is reached, and shows how many candles have passed since each FVG was created.

Full Description

This indicator automatically finds and visualizes Fair Value Gaps (FVGs) using the classic 3-candle ICT logic on any timeframe.

It works on whatever timeframe you apply it to (M1, M5, H1, H4, etc.) and adapts to the current chart.

FVG detection logic

The script uses a 3-candle pattern:

Bullish FVG

Condition:

low > high

Gap zone:

Lower boundary: high

Upper boundary: low

Bearish FVG

Condition:

high < low

Gap zone:

Lower boundary: high

Upper boundary: low

Each detected FVG is drawn as a colored box (green for bullish, red for bearish in this version, but you can adjust colors in the inputs).

Auto-close rules

An FVG remains on the chart until one of the following happens:

Full fill / mitigation

A bullish FVG closes when any candle’s low goes down to or below the lower boundary of the gap.

A bearish FVG closes when any candle’s high goes up to or above the upper boundary of the gap.

Maximum bar age reached

Each FVG has a maximum lifetime measured in candles.

When the number of candles since its creation reaches the configured maximum (default: 200 bars), the FVG is automatically removed even if it has not been fully filled.

This keeps the chart cleaner and prevents very old gaps from cluttering the view.

Age counter (labels inside the boxes)

Inside every FVG box there is a small label that:

Shows how many bars have passed since the FVG was created.

Moves together with the right edge of the box and stays vertically centered in the gap.

This makes it easy to distinguish fresh gaps from older ones and prioritize which zones you want to pay attention to.

Inputs

FVG color – Main fill color for all FVG boxes.

Show bullish FVGs – Turn bullish gaps on/off.

Show bearish FVGs – Turn bearish gaps on/off.

Max bar age – Maximum number of candles an FVG is allowed to stay on the chart before it is removed.

Usage

Works on any symbol and any timeframe.

Can be combined with your own ICT / SMC concepts, order blocks, session ranges, market structure, etc.

You can also choose to only display bullish or only bearish FVGs depending on your directional bias.

Disclaimer

This script is for educational and informational purposes only and is not financial advice. Always do your own research and use proper risk management when trading.

HPAS mean reversion strategy testerTakes Krown HPAS values hardcoded and simulates longs and short with configurable standard deviation multiplier TP/SL. Best used on lower timeframes

Intraday Close Price VariationShows in the graph the intraday variation, being useful when using the replay feature.

PIP BOOSTER (Desktop) DemoversionThe PIP BOOSTER from underground-traders.com is a very intelligent indicator with integrated win-rate tracking (%), which can be used on all markets and timeframes. Thanks to its two fundamentally different algorithms, the PIP BOOSTER is able to find a profitable setup in over 80% of all charts. The win-rate tracking (%) is highly detailed and can be applied to up to 5,000 candles.

It updates after every single signal, ensuring that performance monitoring is always up to date. Additionally, PIP BOOSTER users can apply different time filters, which can further optimize performance.

There is both a desktop version and a mobile version, which can be used with the TradingView mobile app. All signals are displayed clearly in the mobile app, making it possible to trade directly from your smartphone.

Please note that the demo version does not include any live signals. The demo version is only for you to evaluate the performance (win-rate %) of the two algorithms.

We guarantee that there are no repaint signals, and the signals in the demo version are 100% identical to those in the full version.

For any questions, please visit:

underground-traders.com

Or contact us at:

help@underground-traders.com

PIP BOOSTER (Mobile) DemoversionThe PIP BOOSTER from underground-traders.com is a very intelligent indicator with integrated win-rate tracking (%), which can be used on all markets and timeframes. Thanks to its two fundamentally different algorithms, the PIP BOOSTER is able to find a profitable setup in over 80% of all charts. The win-rate tracking (%) is highly detailed and can be applied to up to 5,000 candles.

It updates after every single signal, ensuring that performance monitoring is always up to date. Additionally, PIP BOOSTER users can apply different time filters, which can further optimize performance.

There is both a desktop version and a mobile version, which can be used with the TradingView mobile app. All signals are displayed clearly in the mobile app, making it possible to trade directly from your smartphone.

Please note that the demo version does not include any live signals. The demo version is only for you to evaluate the performance (win-rate %) of the two algorithms.

We guarantee that there are no repaint signals, and the signals in the demo version are 100% identical to those in the full version.

For any questions, please visit:

underground-traders.com

Or contact us at:

help@underground-traders.com

PIP BOOSTER (Desktop) FullversionThe PIP BOOSTER from underground-traders.com is a very intelligent indicator with integrated win-rate tracking (%), which can be used on all markets and timeframes. Thanks to its two fundamentally different algorithms, the PIP BOOSTER is able to find a profitable setup in over 80% of all charts. The win-rate tracking (%) is highly detailed and can be applied to up to 5,000 candles.

It updates after every single signal, ensuring that performance monitoring is always up to date. Additionally, PIP BOOSTER users can apply different time filters, which can further optimize performance.

There is both a desktop version and a mobile version, which can be used with the TradingView mobile app. All signals are displayed clearly in the mobile app, making it possible to trade directly from your smartphone.

Please note that the demo version does not include any live signals. The demo version is only for you to evaluate the performance (win-rate %) of the two algorithms.

We guarantee that there are no repaint signals, and the signals in the demo version are 100% identical to those in the full version.

For any questions, please visit:

underground-traders.com

Or contact us at:

help@underground-traders.com

PIP BOOSTER (Mobile) FullversionThe PIP BOOSTER from underground-traders.com is a very intelligent indicator with integrated win-rate tracking (%), which can be used on all markets and timeframes. Thanks to its two fundamentally different algorithms, the PIP BOOSTER is able to find a profitable setup in over 80% of all charts. The win-rate tracking (%) is highly detailed and can be applied to up to 5,000 candles.

It updates after every single signal, ensuring that performance monitoring is always up to date. Additionally, PIP BOOSTER users can apply different time filters, which can further optimize performance.

There is both a desktop version and a mobile version, which can be used with the TradingView mobile app. All signals are displayed clearly in the mobile app, making it possible to trade directly from your smartphone.

Please note that the demo version does not include any live signals. The demo version is only for you to evaluate the performance (win-rate %) of the two algorithms.

We guarantee that there are no repaint signals, and the signals in the demo version are 100% identical to those in the full version.

For any questions, please visit:

underground-traders.com

Or contact us at:

help@underground-traders.com

VWAP ±2σ Entry Signals (volume Weighted)This indicator builds a session based VWAP and plots the upper and lower 2nd standard deviation bands around it. These bands act as dynamic volatility edges for the session. When price reaches these outer bands, it often represents an extreme stretch away from fair value a place where mean reversion or exhaustion can occur.

The indicator generates trade signals only when price approaches the band from the correct direction, which filters out a lot of noise and reduces false touches.

How It Works

VWAP is calculated from the start of each session.

Standard deviation is computed using volume weighted prices, so the bands expand and contract with real market activity.

The upper and lower 2σ bands form natural "overextended" zones around VWAP.

Most VWAP band strategies fire signals every time price touches a band which produces a lot of junk signals.

This version avoids that by requiring direction based touches, meaning:

If price is already above the band, no sell signal appears.

If price is already below the band, no buy signal appears.

BTC Macro Heatmap (Fed Cuts & Hikes)🔴 1. Red line – Fed Funds Rate (policy trend)

This line tells you what stage of the monetary cycle we’re in.

Rising red line = the Fed is hiking → liquidity is tightening → money leaves risk assets like BTC.

Flat = pause → markets start pricing in the next move (often sideways BTC).

Falling = easing / cutting → liquidity returns → bullish environment builds.

The rate of change matters more than the level. When the slope turns down, capital starts seeking yield again — BTC benefits first because it’s the most volatile asset.

💚 2. Dim green zones – detected cuts

These are data-based easing events pulled directly from FRED.

They show when the actual effective rate began moving down, not necessarily the exact meeting day.

Think of them as the Fed’s “foot off the brake” — that’s when risk markets begin responding.

🟩 3. Bright green lines – official FOMC cuts

These are the real policy shifts — the Fed formally changed direction.

After these appear, BTC historically transitions from accumulation → markup phase.

Look at 2020: the bright green lines came right before BTC’s full reversal.

You’re seeing the same thing now with the 2025 lines — early-stage liquidity return.

🟠 4. Orange line – DXY (US Dollar Index)

DXY is your “risk-off” gauge.

When DXY rises, global investors flock to dollars → BTC usually weakens.

When DXY peaks and starts dropping, it means risk appetite is coming back → BTC rallies.

BTC and DXY are inversely correlated about 70–80% of the time.

Watch for DXY lower highs after rate cuts — that’s your macro confirmation of a BTC-friendly environment.

🟦 5. Aqua line – BTC (normalized)

You’re not looking for the price itself here, but its shape relative to DXY and the Fed line.

When BTC curls up as the red line flattens and DXY rolls over → that’s historically the start of a major bull phase.

BTC tends to bottom before the first cut and explode once DXY decisively breaks down.

🧠 Putting it together

Here’s the rhythm this chart shows over and over:

Fed hikes (red line rising) → BTC weakens, DXY climbs.

Fed pauses (red line flat) → BTC stops falling, DXY tops.

Fed cuts (dim + bright green) → DXY turns down → BTC begins long recovery → bull cycle starts.

RLSR logreg_support_libLibrary "logreg_support_lib"

sigmoid(z)

Parameters:

z (float)

prng01(seed1, seed2)

Parameters:

seed1 (float)

seed2 (float)

normalize(value, minval, maxval)

Parameters:

value (float)

minval (float)

maxval (float)

calcpercentilefast(arr, percentile)

Parameters:

arr (array)

percentile (float)

calcpercentile_series_sampled(s, length, percentile, stride)

Parameters:

s (float)

length (int)

percentile (float)

stride (int)

calcRangeWithLog(value, minval, maxval, uselog)

Parameters:

value (float)

minval (float)

maxval (float)

uselog (bool)

calcMomentumAdvanced(src, length, momType)

Parameters:

src (float)

length (simple int)

momType (string)

normalizeMomentumByType(rawMom, momType, momMin, momMax, momNorm)

Parameters:

rawMom (float)

momType (string)

momMin (float)

momMax (float)

momNorm (float)

normalizeMomentumByTypeExt(rawMom, momType, momMin, momMax, momNorm, bouncingdecay)

Parameters:

rawMom (float)

momType (string)

momMin (float)

momMax (float)

momNorm (float)

bouncingdecay (float)

calcrollingstddev(src, length)

Parameters:

src (float)

length (int)

addlog(buffer, level, msg)

Parameters:

buffer (string)

level (string)

msg (string)

calcfeaturecorrelation(x1, x2)

Parameters:

x1 (array)

x2 (array)

calcnoiseratio(src, lookback)

Parameters:

src (float)

lookback (int)

calccompatibilityscore(x1, x2)

Parameters:

x1 (array)

x2 (array)

getfuturereturn(offset, returnlookback)

Parameters:

offset (int)

returnlookback (int)

calculatema(source, length, matype)

Parameters:

source (float)

length (simple int)

matype (string)

adaptive_trigger_for_source(src, enabled, freeze, lookback, threshold, volahistory)

Parameters:

src (float)

enabled (bool)

freeze (bool)

lookback (int)

threshold (float)

volahistory (array)

checkadaptivetrigger5(s1, enabled1, freeze1, hist1, s2, enabled2, freeze2, hist2, s3, enabled3, freeze3, hist3, s4, enabled4, freeze4, hist4, s5, enabled5, freeze5, hist5, lookback, threshold)

Parameters:

s1 (float)

enabled1 (bool)

freeze1 (bool)

hist1 (array)

s2 (float)

enabled2 (bool)

freeze2 (bool)

hist2 (array)

s3 (float)

enabled3 (bool)

freeze3 (bool)

hist3 (array)

s4 (float)

enabled4 (bool)

freeze4 (bool)

hist4 (array)

s5 (float)

enabled5 (bool)

freeze5 (bool)

hist5 (array)

lookback (int)

threshold (float)

ring_start_index(rb_write_idx, rb_count, rb_cap)

Parameters:

rb_write_idx (int)

rb_count (int)

rb_cap (int)

reversalLibrary "reversals"

psar(af_start, af_increment, af_max)

Calculates Parabolic Stop And Reverse (SAR)

Parameters:

af_start (simple float) : Initial acceleration factor (Wilder's original: 0.02)

af_increment (simple float) : Acceleration factor increment per new extreme (Wilder's original: 0.02)

af_max (simple float) : Maximum acceleration factor (Wilder's original: 0.20)

Returns: SAR value (stop level for current trend)

fractals()

Detects Williams Fractal patterns (5-bar pattern)

Returns: Tuple with fractal values (na if no fractal)

swings(lookback, source_high, source_low)

Detects swing highs and swing lows using lookback period

Parameters:

lookback (simple int) : Number of bars on each side to confirm swing point

source_high (float) : Price series for swing high detection (typically high)

source_low (float) : Price series for swing low detection (typically low)

Returns: Tuple with swing point values (na if no swing)

pivot(tf)

Calculates classic/standard/floor pivot points

Parameters:

tf (simple string) : Timeframe for pivot calculation ("D", "W", "M")

Returns: Tuple with pivot levels

pivotcam(tf)

Calculates Camarilla pivot points with 8 levels for short-term trading

Parameters:

tf (simple string) : Timeframe for pivot calculation ("D", "W", "M")

Returns: Tuple with pivot levels

pivotdem(tf)

Calculates d-mark pivot points with conditional open/close logic

Parameters:

tf (simple string) : Timeframe for pivot calculation ("D", "W", "M")

Returns: Tuple with pivot levels (only 3 levels)

pivotext(tf)

Calculates extended traditional pivot points with R4-R5 and S4-S5 levels

Parameters:

tf (simple string) : Timeframe for pivot calculation ("D", "W", "M")

Returns: Tuple with pivot levels

pivotfib(tf)

Calculates Fibonacci pivot points using Fibonacci ratios

Parameters:

tf (simple string) : Timeframe for pivot calculation ("D", "W", "M")

Returns: Tuple with pivot levels

pivotwood(tf)

Calculates Woodie's pivot points with weighted closing price

Parameters:

tf (simple string) : Timeframe for pivot calculation ("D", "W", "M")

Returns: Tuple with pivot levels

Weekday Close vs Open — Last N (per weekday)# Weekday Close vs Open - Last N Occurrences

This indicator distills every weekday's historical open-to-close behavior into a compact table so you can see how "typical" the current session is before the day even closes. It runs independently of your chart timeframe by pulling daily OHLCV data under the hood, tracking the last **N** completed occurrences for each weekday, and refreshing only when a daily bar closes. On daily charts you can also shade every past bar that matches today's weekday (excluding the in-progress session) to reinforce the pattern visually while the table remains non-repainting.

## What It Shows

- **Win/Loss/Tie counts** - how many of the last `N` occurrences closed above the open (wins), below (losses), or inside the tie threshold you define as "flat".

- **Win % heatmap** - the win column is color-coded (deep green > deep red) so you immediately recognize strong or weak weekdays.

- **Advanced metrics (optional)** - average daily volume plus the average percentage excursion above/below the open (`AvgUp%`, `AvgDn%`) for that weekday.

- **Totals row** - aggregates every weekday into one row to estimate overall hit rate and average stats across the entire data set.

- **Weekday shading (optional)** - on daily charts you can tint every bar that matches today's weekday (all Mondays, all Fridays, etc.) for instant pattern recognition.

## How It Works

1. The script requests daily OHLCV data (non-repainting) regardless of the chart timeframe.

2. When a new daily bar confirms, it packs that day's data into one of seven arrays (one per weekday). Each day contributes five floats (O/H/L/C/V) so trimming and statistics stay in lockstep.

3. A helper function (`f_dayMetrics`) scans daily history to compute average volume, average excursion above/below the open, and win/loss/tie counts for the requested weekday.

4. The table populates on the last bar of the chart session, respecting your advanced/totals toggles and keeping text at `size.normal`.

## Reading the Table

- **Win/Loss/Tie columns**: raw counts taken from your chosen `N`.

- **Win %***: excludes ties from the denominator so it reflects only decisive closes.

- **AvgUp% / AvgDn%**: typical intraday extension (high vs open, open vs low) in percent.

- **Avg Vol**: arithmetic mean of daily volume for that weekday.

- **TOTAL row**: provides a global win rate plus volume/up/down averages weighted by how many samples each weekday contributed.

## Practical Uses

- Spot weekdays that historically trend higher or lower before entering a trade.

- Compare current price action against the typical intraday range (`AvgUp%` vs today's move).

- Filter mean-reversion vs breakout setups based on the most reliable weekday patterns.

- Quickly gauge whether today is behaving "in character" by referencing the highlighted row or the optional whole-chart weekday shading.

> **Tip:** Use smaller `N` values (e.g., 10-20) for adaptive, recent behavior and larger values (50+) to capture longer-term seasonality. Tighten the tie threshold if you want almost every candle to register as win/loss, or widen it to focus only on meaningful moves.

Forward Returns – (Next Month Start)This indicator calculates 1-month, 3-month, 6-month, and 12-month forward returns starting from the first trading day of the month following a defined price event.

A price event occurs when the selected asset drops below a user-defined threshold over a chosen timeframe (Day, Week, or Month).

For monthly conditions, the script evaluates the entire performance of the previous calendar month and triggers the event only at the first trading session of the next month, ensuring accurate forward-return alignment with historical monthly cycles.

The forward returns for each detected event are displayed in a paginated performance table, allowing users to navigate through large datasets using a page selector. Each page includes:

Entry Date

Forward returns (1M, 3M, 6M, 12M)

Average forward return

Win rate (percentage of positive outcomes)

This tool is useful for studying historical performance after major drawdowns, identifying seasonal patterns, and building evidence-based risk-management or timing models.

Frank Strategy V2.06 Quantum FilterThe Frank Strategy indicator version 2.06 is designed to:

Identify high-probability entries

Filter out false signals typical of XAUUSD (especially M1–M5)

Enter only when trend + momentum + market coherence are aligned

Provide automatic TP/SL based on volatility

Get additional confirmation with the quant filter

It is a strategy for short and medium-term trends, not for impulsive scalping or excessively long cycles.

The Frank Strategy aims to:

Do not chase the price

Do not enter sideways

Do not trade without momentum

Do not trade without coherence between trend + strength + volatility

Avoid impulsive and noisy entries

It is a strategy designed to be:

selective

precise

repeatable

disciplined