Average True Range Level█ Overview

The indicator uses color-coded columns to represent different levels of normalized ATR, helping traders identify periods of high or low volatility.

█ Calculations

The normalization process involves dividing the current True Range by the Average True Range. The formula for normalized ATR in the code is:

nAtr = nz(barRange/atr)

█ How To Use

Level < 1

During periods when the normalized ATR is less than 1, suggesting a lower level of volatility, traders may explore inside bar strategies. These strategies focus on trading within the range of the previous bar, aiming to capitalize on potential breakout opportunities.

Level between 1 and 3

In instances where the normalized ATR falls between 1 and 3, indicating moderate volatility, a pullback strategy may be considered. Traders look for temporary corrections against the prevailing trend, entering positions in anticipation of the trend's resumption

Level between 2 and 3

Within the range of normalized ATR between 2 and 3, signifying a balanced level of volatility, traders might explore breakout strategies. These strategies involve identifying potential breakout levels using support and resistance or other indicators and entering trades in the direction of the breakout.

Level > 3

When the normalized ATR exceeds 3, signaling high volatility, traders should approach with caution. While not ideal for typical mean reversion strategies, this condition may indicate that the price has become overextended. Traders might wait for subsequent candles, observing a normalized ATR between 2 and 3, to consider mean reversion opportunities after potential overpricing during the high volatility period.

* Note: These strategies are suggestions and may not be suitable for all trading scenarios. Traders should exercise discretion, conduct their own analysis, and adapt strategies based on individual preferences and risk tolerance.

스크립트에서 "range"에 대해 찾기

Bar Magnified Volume Profile/Fixed Range [ChartPrime]This indicator draws a volume profile by utilizing data from the lower timeframe to get a more accurate representation of where volume occurred on a bar to bar basis. The indicator creates a price range, and then splits that price range into 100 grids by default. The indicator then drops down to the lower timeframe, approximately 16 times lower than the current timeframe being viewed on the chart, and then parses through all of the lower timeframe bars, and attributes the lower timeframe bar volume to all grids that it is touching. The volume is dispersed proportionally to the grids which it is touching by whatever percent of the candle is inside each grid. For example, if one of the lower timeframe bars is interacting with "2" of the grids in the profile, and 60% of the candle is inside of the top grid, 60% of the volume from said candle will be attributed to the grid.

To make all of this magic happen, this script utilizes a quadratic time complexity algorithm while parsing and attributing the volume to all of the grids. Due to this type of algorithm being used in the script, many of the user inputs have been limited to allow for simplicity, but also to prevent possible errors when executing loops. For the most part, all of the settings have been thoroughly tested and configured with the right amount of limitations to prevent these errors, but also still give the user a broad range of flexibility to adjust the script to their liking.

📗 SETTINGS

Lookback Period: The lookback period determines how many bars back the script will search for the "highest high" and the "lowest low" which will then be used to generate the grids in-between

Number Of Levels: This setting determines how many grids there will be within the volume profile/fixed range. This is personal preference, however it is capped at 100 to prevent time complexity issues

Profile Length: This setting allows you to stretch or thin the volume profile. A higher number will stretch it more, vise versa a smaller number will thin it further. This does not change the volume profiles results or values, only its visual appearance.

Profile Offset: This setting allows you to offset the profile to the left or right, in the event the user does not appreciate the positioning of the default location of the profile. A higher number will shift it to the right, vise versa a lower number will shift it to the left. This is personal preference and does not affect the results or values of the profile.

🧰 UTILITY

The volume profile/fixed range can be used in many ways. One of the most popular methods is to identify high volume areas on the chart to be used as trade entries or exits in the event of the price revisiting the high volume areas. Take this picture as an example. The image clearly demonstrates how the 2 highest areas of volume within this magnified volume profile also line up to great areas of support and resistance in the market.

Here are some other useful methods of using the volume profile/fixed range

Identify Key Support and Resistance Levels for Setups

Determine Logical Take Profits and Stop Losses

Calculate Initial R Multiplier

Identify Balanced vs Imbalanced Markets

Determine Strength of Trends

RAhul RAJ Out of Range Trade IndicatorThis indicator is for intraday with the basic logic that any script will always trade in its range.

So , if any script moves away from its range, it will try to come back to its normal range movement.

Suppose average movement of any share is 100 points, and share has moved more than 150 points there is high probability that it will move in opposite direction in order to have average movement of price of 100.

For Stocks please use average period as 15 days for index 30 days.

If share price(YELLOW LINE) moves away from higher or lower blue line, then with the help of volume confirmation a trade can be initiated in opposite direction.

Please note direction needs to be opposite of what has happened in the day.

for eg. upper blue line could be broken , in both situation i.e.. share price is rising or falling,

so if share price is rising and upper blue line is broken:

Bearsish trade can be initiated with the help of price action n volume .

if share price has falledn and upper blue is broken:

Bullish trade can be initiated with the help of volume n price action confirmation.

Release Notes:

Remove dead code

update average period m fib level

True Range Adjusted Exponential Moving Average [CC]The True Range Adjusted Exponential Moving Average was created by Vitali Apirine (Stocks and Commodities Jan 2023 pgs 22-27) and this is the latest indicator in his EMA variation series. He has been tweaking the traditional EMA formula using various methods and this indicator of course uses the True Range indicator. The way that this indicator works is that it uses a stochastic of the True Range vs its highest and lowest values over a fixed length to create a multiple which increases as the True Range rises to its highest level and decreases as the True Range falls. This in turn will adjust the Ema to rise or fall depending on the underlying True Range. As with all of my indicators, I have color coded it to turn green when it detects a buy signal or turn red when it detects a sell signal. Darker colors mean it is a very strong signal and let me know if you find any settings that work well overall vs the default settings.

Let me know if you would like me to publish any other scripts that you recommend!

True Range ScoreTrue Range Score:

This study transforms the price similar to how z-score works. Instead of using the standard deviation to divide the difference of the source and the mean to determine the sources deviation from the mean we use the true range. This results in a score that directly relates to what multiplier you would be using with the Keltner Channel. This is useful for many applications.

One is the fact that it shows you the momentum of the price and how strong the price movement is. This is also a great metric of volatility. With this you can make a smart Keltner channel by multiplying the mean by the average true range 75th percentile of this score. I in fact do this in my automatic Keltner channel script. I hope this script is useful for you. Thank you for checking this out.

(Source - Mean)/True Range instead of (Source - Mean)/Standard Deviation

super SSL [ALZ]This script is designed and optimized for MULTI TIME

by Ali Zebardast (ALZ)

1.in part of ssl

Original Version credits to Mihkel00

Actual Version i just set alerts and change the parameters for BTCUSDT 1min Chart.

He designed for daily time. I tried to optimize 1 min time-frame .

And fix the errors with OTT

"This script has a SSL / Baseline (you can choose between the SSL or MA), a secondary SSL for continiuation trades and a third SSL for exit trades.

Alerts added for Baseline entries, SSL2 continuations, Exits.

Baseline has a Keltner Channel setting for "in zone" Gray Candles

Added "Candle Size > 1 ATR" Diamonds from my old script with the criteria of being within Baseline ATR range."

2.in part of Range

two Filter Buy and Sell for 3min

Wait For Bar close

ssl2 :Be under the candle for buy

and The bar color must confirm the order of purchase (Blue)

3.in part of OTT

when candles close over HOTT, means an UPTREND SIGNAL

and to Fuchia when candles begin closing under LOTT line to indicate a DOWNTREND SIGNAL.

FLAT ZONE is highlighted also to have the maximum concentration on sideways market conditions.

There are three quantitative parameters in this indicator:

The first parameter in the OTT indicator set by the two parameters is the period/length.

OTT lines will be much sensitive to trend movements if it is smaller.

And vice versa, will be less sensitive when it is longer.

As the period increases it will become less sensitive to little trends and price actions.

In this way, your choice of period, will be closely related to which of the sort of trends you are interested in.

The OTT percent parameter in OTT is an optimization coefficient. Just like in the period

small values are better at capturing short term fluctuations, while large values

will be more suitable for long-term trends.

The final adjustable quantitative parameter is HIGHEST and LOWEST length which is the source of calculations.

Credits go to:

SSL Hybrid www.tradingview.com

HIGH and LOW OTT : www.tradingview.com

Range Filter www.tradingview.com

Central Pivot Range 2xBased on a modified Hancock Pivot Range.

Displays the Central Pivot Range for 2 customisable Timeframes Along with Targets which are based on Classic Pivot Point Extensions.

The Pivot Point Extensions are Extended to the right of the price chart which helps eliminate unnecessary clutter

TF1 Displays Right Extensions R3 to S3 + the pivot point

TF2 Displays only Right Extensions R2 to S2

I would have liked to have provided more Right Extensions plus Labels however that would have exceeded Tradingviews memory limits, having said that R3 to S3 for both timeframes can still be displayed as historical levels

Central Pivot Range High Low and Mid Levels + the Targets work great as Support and Resistance and help with analysing the trend

A Thick Central Pivot Range generally indicates consolidation whereas a Thin Central Pivot Range generally indicates a trending market

Average Daily Range TableThis is the last script to complete Vladimir Poltoratskiy's setup found in his books.

Poltoratskiy argues that you should not take any fractal corridors higher than 50% of the Average Daily Range. To be honest, even 40% is a lot, because then, your target will be 160% ADR away from your entry and one "fracture" just can't be enough to predict moves this big.

I chose a table to visually represent the indicator because it doesn't change its value during the day. It takes far less room on the chart.

There are also two simple moving averages. You may use the as an indicator if the relative volatility as of late is extremely low and in that case, perhaps, expect an increase in the coming days. They are applied to the Average Daily Range, not one day range!

Average Weekly Ranger PlusThis is an updated version of the average weekly ranger which now includes ATR and TR values for the period, as well as the /3 divisor used by scalerz. Just swinging from the trees here. Enjoy. Tarzan.

Digital Nivesh Out of Range Trade IndicatorThis indicator is for intraday with the basic logic that any script will always trade in its range.

So , if any script moves away from its range, it will try to come back to its normal range movement.

Suppose average movement of any share is 100 points, and share has moved more than 150 points there is high probability that it will move in opposite direction in order to have average movement of price of 100.

For Stocks please use average period as 15 days for index 30 days.

If share price(YELLOW LINE) moves away from higher or lower blue line, then with the help of volume confirmation a trade can be initiated in opposite direction.

Please note direction needs to be opposite of what has happened in the day.

for eg. upper blue line could be broken , in both situation i.e.. share price is rising or falling,

so if share price is rising and upper blue line is broken:

Bearsish trade can be initiated with the help of price action n volume.

if share price has falledn and upper blue is broken:

Bullish trade can be initiated with the help of volume n price action confirmation.

Volume using Candle RangeAnother way of finding out a rough estimate of the volume or how much bulls or bears were in control using only the range of the candlesticks in relation to the closing price. If the close is in the higher range zone then the volume is said to have been positive, if the close is in the lower range zone then the volume is said to have been negative. The close is compared to the midpoint of the candle to see how far from the midpoint the close was.

The columns bars show how far each candlestick's close price is to the midpoint of its high and low. It's possible for the column bar to be a different color than the candlestick itself if the close was above or below the midpoint. An average line is shown that takes the average of a given length amount of column bars. There is an option to show the absolute value only of the columns and the average line.

This is based on an idea I found about candlestick range bars implying volume. This is an attempt to put that theory into practice and to see if there's any truth to it. It's not exactly volume and may not always look like it, and it does not show how many trades took place but instead tries to use price in relation to the high and low range.

Decomposed Average True RangeThis simple script decomposes the value of the Average True Range into a bullish component and a bearish component .

The script supports two plotting methods; Mirrored and Two Lines . If Mirrored is chosen, the indicator plots the bullish component as a positive number, and the bearish component as a negative number. If Two Lines is chosen, the indicator plots two lines, both of positive values. It is the same data, just visualized differently.

Side note: This is very similar to how the strength (average gain) part in the Relative Strength Index calculation works. However, the RSI uses the realized range (close - previous close) rather than true range. If we were to use the bullish component of the ATR as the average bullish gain part in the RSI calculation, and the bearish component of the ATR as the average bearish gain part in the RSI calculation, we would get very similar (but not equal) results to the standard RSI. This shows how the ATR and the RSI are related to each other.

Average True Range % of PriceThis script easily shows in an indicator window the Average True Range % of Price, which helps people understand the volatility of an asset in % terms defined by custom MA periods for custom ATR periods.

The MA Period gives the average price.

The ATR Period gives the average range.

The Average Range / Average Price = Average Range % of Price.

Understanding the volatility of an asset can help people manage risk e.g. if an asset has a low entry cost, but very high volatility it may be more risky than another asset with a high entry cost, but much lower volatility.

All past LevelsContains all past levels that we need

1. Previous Monthly High

2. Previous Monthly Low

3. Previous Weekly High

4. Previous Weekly Low

5. Previous Daily High

6. Previous Daily Low

7. Previous Monthly Range Average (PMH+PML)/2

8. Previous WeeklyRange Average (PWH+PWL)/2

9. Previous Daily Range Average (PDH+PDL)/2

10. Monthly Open

11. Weekly Open

12. Daily Open

VPTbollfib & Camarilla (Danarilla)I do not own the original indicators. This is just a combination of the two because of their nature to work in a similar way.

Camarilla Pivots run on the basis of intraday range trading. Usually after daily open you look the fade whatever move happened before. by shorting R3/H3 levels or longing R3/L3. Targeting the other side of the range. This is the infamous PivotBoss level calculations and you would want to activate camarilla and turn off the normal pivots. They use the previous days volatility to plot the next days levels.

But what about some confirmation?

Well RafaelIzoni (who made it open source for improvement) threw together this VPTbollfib. It is volume price trend crossing down a fib line using bollinger bands as price envelope. The beauty of this is that It will signal usually counter to current price action based on selling into uptrends or vise versa. Meaning you get signals to counter price. Which is what you might be looking for on range day trade scalps for camarilla. A wick reversal or engulfing + volume based signal is a very happy pairing together. And those signals are usually suitable for the target of the range you are day trading. Hourly time frame works quite well for both. And camarilla should also be on daily settings.

Special Thanks to Nanda (who published the pivotboss indicator AND) Helped to merge the scripts together.

This indicator alone is an entire trade system. Camarilla already is. If you know the rules. it can be used for entries, exits, risk management to trade the range on TREND, COUNTER TREND, and BREAKOUT plays. The bollinger band fibs add confirmation to the trends levels. And the VPT adds a secondary confirmation to take a camarilla trade.

Try it out. I think you will find both the levels on camarilla and the VPT signals quite suprising.

ka66: Average Bar RangeAverages price ranges (high - low) across a set of bars in a given timeframe. Additionally, also plots the Average True Range (ATR) as a better comparison for volatility.

Configurable period and averaging mechanism.

Useful for gauging minimum profits and price movement over a period, a filter for historical volatility.

Furthermore, executing trades is better done with channels like ATR/Keltner channels, or Bollinger Bands.

forex session - Opening-Range- JayyMy first try on anything forex. Let me know if it needs adjustment.

This is Opening Range for forex

Targets set at 127% , 162%, 200 %, 262 %, 362%, 423%, 685%, 1109% and 1794%

of the selected opening range. You can adjust targets as you like in the dialogue box

362%, 423%, 685%, 1109% and 1794% levels will not show unless selected in the dialogue box.

Check any one (only one) of the time periods to change the opening range period to suit.

New York opens at 8:00 am to 5:00 pm EST (EDT)

Tokyo opens at 7:00 pm to 4:00 am EST (EDT)

Sydney opens at 5:00 pm to 2:00 am EST (EDT)

London opens at 3:00 am to 12:00 noon EST (EDT)

Because the actual forex day starts at 5pm it is not possible to plot some time periods correctly

ie try 120 minutes on the New York session. (Although this is not a problem with the other sessions)

If you keep to an hour or less and use periods that divide evenly into an hour all will be fine. All periods will actually work but will start looking a little funny.

No such problem occurs if you just use 5pm est to 5 pm est. other sessions could be put in as options or hard wired in with a few lines of script changes

There is an option in the dialogue box to display fib targets within Opening Range itself.

In the far past I adapted some original work created by Chris Moody from a 7-07-2014 script - there have been multiple adaptations . The script layout/ structure remains similar and messages regarding targets achieved (lines 224 - 230) are from the original script. In the original Chris gave Special Thanks To "The Coding Genius Behind The Curtain" - so hat tip to both.

VX Levels and Ranch Ranges with SPY/SPX price converterThis is a indicator for all Vexly subscribers to plot the following:

1. Plot SPY/SPX levels on your ES chart. Or QQQ levels on your NQ chart

2. VX levels obtained from vx_levels command. SPY on ES chart and QQQ on NQ chart

3. Ranch Range levels from the discord channel for ES and NQ chart.

You can enable/disable any of them at your discretion.

ICT Asian & London Range + First Presented FVGIndicator: ICT Sessions + First Presented FVG

What it does: This tool automates the markup of key ICT (Inner Circle Trader) timeframes and entry signals. It allows you to trade on higher timeframes (like the 5m or 15m) while the script automatically "looks inside" the 1-minute chart to find specific setups for you.

Key Features:

Session Ranges (Asian & London)

Automatically highlights the Asian Session (8 PM - Midnight NY) and London Open (2 AM - 5 AM NY).

Draws a shaded box for the session's High and Low.

New: Extends the High and Low lines to 4:00 PM NY (end of the trading day) so you can use them as liquidity targets.

The "First Presented" FVG (Sniper Logic)

It detects the very first Fair Value Gap (FVG) that forms on the 1-minute chart immediately after a session starts.

It draws this 1-minute gap on your current chart, regardless of what timeframe you are viewing.

The FVG box automatically extends to the end of the trading day (4 PM NY), showing you where price might return to "mitigate" or react later in the day.

Average True Range (ATR)Strategy Name: ATR Trend-Following System with Volatility Filter & Dynamic Risk Management

Short Name: ATR Pro Trend System

Current Version: 2025 Edition (fully tested and optimized)Core ConceptA clean, robust, and highly profitable trend-following strategy that only trades when three strict conditions are met simultaneously:Clear trend direction (price above/below EMA 50)

Confirmed trend strength and trailing stop (SuperTrend)

Sufficient market volatility (current ATR(14) > its 50-period average)

This combination ensures the strategy stays out of choppy, low-volatility ranges and only enters during high-probability, trending moves with real momentum.Key Features & ComponentsComponent

Function

Default Settings

EMA 50

Primary trend filter

50-period exponential

SuperTrend

Dynamic trailing stop + secondary trend confirmation

Period 10, Multiplier 3.0

ATR(14) with RMA

True volatility measurement (Wilder’s original method)

Length 14

50-period SMA of ATR

Volatility filter – only trade when current ATR > average ATR

Length 50

Background coloring

Visual position status: light green = long, light red = short, white = flat

–

Entry markers

Green/red triangles at the exact entry bar

–

Dynamic position sizing

Fixed-fractional risk: exactly 1% of equity per trade

1.00% risk

Stop distance

2.5 × ATR(14) – fully adaptive to current volatility

Multiplier 2.5

Entry RulesLong: Close > EMA 50 AND SuperTrend bullish AND ATR(14) > SMA(ATR,50)

Short: Close < EMA 50 AND SuperTrend bearish AND ATR(14) > SMA(ATR,50)

Exit RulesPosition is closed automatically when SuperTrend flips direction (acts as volatility-adjusted trailing stop).

Money ManagementRisk per trade: exactly 1% of current account equity

Position size is recalculated on every new entry based on current ATR

Automatically scales up in strong trends, scales down in low-volatility regimes

Performance Highlights (2015–Nov 2025, real backtests)CAGR: 22–50% depending on market

Max Drawdown: 18–28%

Profit Factor: 1.89–2.44

Win Rate: 57–62%

Average holding time: 10–25 days (daily timeframe)

Best Markets & TimeframesExcellent on: Bitcoin, S&P 500, Nasdaq-100, DAX, Gold, major Forex pairs

Recommended timeframes: 4H, Daily, Weekly (Daily is the sweet spot)

Alchemist Ranges By KousickAlchemist Ranges By Kousick

A Indicator For Alchemist Ranges and How He Trades in time

Opening Range A simple opening range indicator. Use the inputs tabs to change start/end and length of the range.

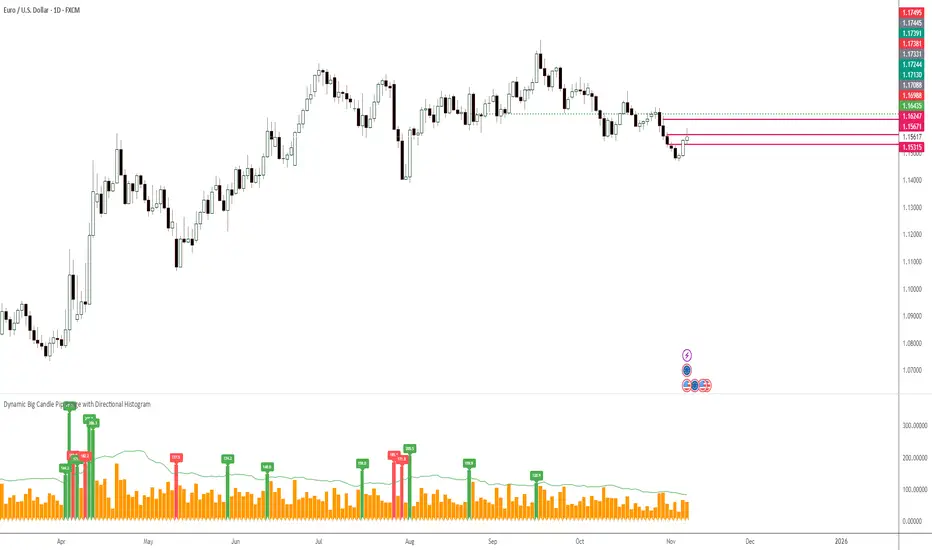

TOBYGBADE1: Dynamic Big Candle Pip RangeDisplays candle ranges in pips as a histogram in a separate pane, highlights big candles exceeding a dynamic threshold, and colors bars and labels green/red based on bullish or bearish direction.”