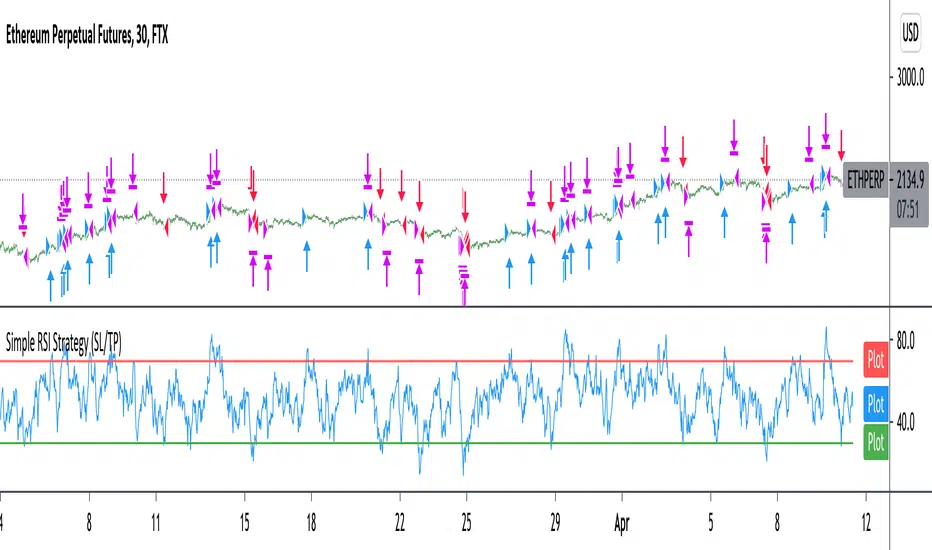

Improved simple RSI Buy/Sell at a level (SL/TP)Improved Simple Strategy based on RSI, using overbought or oversold levels.

Backtest: ETHPERP (FTX) - 30m

Set STOP LOSS and GET PROFIT as a percentage (2% and 10% by default).

If strategy.position_size != 0 algorithm convert percentages into points and set stop loss and take profit limit orders.

Pine Script™ 전략