Fury by Tetrad Fury by Tetrad

What it is:

A rules-based Bollinger+RSI strategy that fades extremes: it looks for price stretching beyond Bollinger Bands while RSI confirms exhaustion, enters countertrend, then exits at predefined profit multipliers or optional stoploss. “Ultra Glow” visuals are purely cosmetic.

How it works — logic at a glance

Framework: Classic Bollinger Bands (SMA basis; configurable length & multiplier) + RSI (configurable length).

Long entries:

Price closes below the lower band and RSI < Long RSI threshold (default 28.3) → open LONG (subject to your “Market Direction” setting).

Short entries:

Price closes above the upper band and RSI > Short RSI threshold (default 88.4) → open SHORT.

Profit exits (price targets):

Uses simple multipliers of the strategy’s average entry price:

Long exit = `entry × Long Exit Multiplier` (default 1.14).

Short exit = `entry × Short Exit Multiplier` (default 0.915).

Risk controls:

Optional pricebased stoploss (disabled by default) via:

Long stop = `entry × Long Stop Factor` (default 0.73).

Short stop = `entry × Short Stop Factor` (default 1.05).

Directional filter:

“Market Direction” input lets you constrain entries to Market Neutral, Long Only, or Short Only.

Visuals:

“Ultra Glow” draws thin layered bands around upper/basis/lower; these do not affect signals.

> Note: Inputs exist for a timebased stop tracker in code, but this version exits via targets and (optional) price stop only.

Why it’s different / original

Explicit extreme + momentum pairing: Entries require simultaneous band breach and RSI exhaustion, aiming to avoid entries on gardenvariety volatility pokes.

Deterministic exits: Multiplier-based targets keep results auditable and reproducible across datasets and assets.

Minimal, unobtrusive visuals: Thin, layered glow preserves chart readability while communicating regime around the Bollinger structure.

Inputs you can tune

Bollinger: Length (default 205), Multiplier (default 2.2).

RSI: Length (default 23), Long/Short thresholds (28.3 / 88.4).

Targets: Long Exit Mult (1.14), Short Exit Mult (0.915).

Stops (optional): Enable/disable; Long/Short Stop Factors (0.73 / 1.05).

Market Direction: Market Neutral / Long Only / Short Only.

Visuals: Ultra Glow on/off, light bar tint, trade labels on/off.

How to use it

1. Timeframe & assets: Works on any symbol/timeframe; start with liquid majors and 60m–1D to establish baseline behavior, then adapt.

2. Calibrate thresholds:

Narrow/meanreverting markets often tolerate tighter RSI thresholds.

Fast/volatile markets may need wider RSI thresholds and stronger stop factors.

3. Pick realistic targets: The default multipliers are illustrative; tune them to reflect typical mean reversion distance for your instrument/timeframe (e.g., ATRinformed profiling).

4. Risk: If enabling stops, size positions so risk per trade ≤ 1–2% of equity (max 5–10% is a commonly cited upper bound).

5. Mode: Use Long Only or Short Only when your discretionary bias or higher timeframe model favors one side; otherwise Market Neutral.

Recommended publication properties (for backtests that don’t mislead)

When you publish, set your strategy’s Properties to realistic values and keep them consistent with this description:

Initial capital: 10,000 (typical retail baseline).

Commission: ≥ 0.05% (adjust for your venue).

Slippage: ≥ 2–3 ticks (or a conservative pertrade value).

Position sizing: Avoid risking > 5–10% equity per trade; fixedfractional sizing ≤ 10% or fixedcash sizing is recommended.

Dataset / sample size: Prefer symbols/timeframes yielding 100+ trades over the tested period for statistical relevance. If you deviate, say why.

> If you choose different defaults (e.g., capital, commission, slippage, sizing), explain and justify them here, and use the same settings in your publication.

Interpreting results & limitations

This is a countertrend approach; it can struggle in strong trends where band breaches compound.

Parameter sensitivity is real: thresholds and multipliers materially change trade frequency and expectancy.

No predictive claims: Past performance is not indicative of future results. The future is unknowable; treat outputs as decision support, not guarantees.

Suggested validation workflow

Try different assets. (TSLA, AAPL, BTC, SOL, XRP)

Run a walkforward across multiple years and market regimes.

Test several timeframes and multiple instruments. (30m Suggested)

Compare different commission/slippage assumptions.

Inspect distribution of returns, max drawdown, win/loss expectancy, and exposure.

Confirm behavior during trend vs. range segments.

Alerts & automation

This release focuses on chart execution and visualization. If you plan to automate, create alerts at your entry/exit conditions and ensure your broker/venue fills reflect your slippage/fees assumptions.

Disclaimer

This script is provided for educational and research purposes. It is not investment advice. Trading involves risk, including the possible loss of principal. © Tetrad Protocol.

지표 및 전략

Solana 4H RSI->MACD — Counter-Trend By TetradTetrad RSI→RSI Cross→MACD (Sequenced) — Counter-Trend (SL-Only)

Category: Market-neutral, counter-trend, sequenced entries

Timeframe default: Works on any TF; designed around 4H On Solana

Markets: Any (spot, perp, futures); parameterize to your asset

What it does

This strategy hunts reversals using a 3-step sequence on RSI and MACD, then optionally restricts entries by market regime and a price gate. It shows stop-loss lines only when hit (clean chart), and paints a Donchian glow for quick read of backdrop conditions.

Entry logic (sequenced)

1. RSI Extreme:

Long path activates when RSI < Oversold (default 27.5).

Short path activates when RSI > Overbought (default 74).

2. RSI Cross confirmation:

Long path: RSI crosses up back above the oversold level.

Short path: RSI crosses down back below the overbought level.

Each step has a max bar lookback so stale signals time out.

3. MACD Cross trigger:

Long: MACD line crosses above Signal.

Short: MACD line crosses below Signal.

→ When step 3 fires and gates are satisfied, a trade is entered.

Optional gates & filters

Regime Filter (Counter-Trend):

Longs allowed in **Range / Short Trend / Short Parabolic** regimes.

Shorts allowed in **Range / Long Trend / Long Parabolic** regimes.

Based on ADX/DI and ATR% intensity.

* Price Gate (Long Ceiling):

Toggle to **disable new longs above a chosen price (default 209.0 For SOL).

Useful for assets like SOL where you want longs only below a cap.

Exits / Risk

* Stop-Loss (% of entry):** default **14%**, toggleable.

* SL visualization:** plots a **thin dashed red line only on the bar it’s hit**.

* (No take-profit or time-based exit in this version—keep it pure to the sequence and regime. Add TP/time exits if desired.)

Visuals

* Donchian Glow (50): background band only (upper/lower lines hidden).

* Regime HUD: compact table (top-right) highlighting the active regime.

* Minimal marks: no entry/exit “arms” clutter; only SL-hit lines render.

Inputs (key)

* Core: RSI Length, Oversold/Overbought, MACD Fast/Slow/Signal.

* Sequence: Max bars from Extreme→RSI Cross and RSI Cross→MACD Cross.

* Regime: ADX Length, Trend/Parabolic thresholds, ATR length & floor.

* Stops: Enable/disable; SL %.

* Price Gate: Enable; Long ceiling price.

Alerts

Sequenced Long (CT): RSIhigh → RSI cross down → MACD bear cross.

## Notes & Tips

Designed for counter-trend fades that become trend rides. The regime filter helps avoid fading true parabolics and aligns entries with safer contexts.

The sequence is stateful (steps must occur in order). If a step times out, the path resets.

Works on lower TFs, but the 4H baseline reduces noise and over-trading.

Consider pairing with volume or structure filters if you want fewer but higher-conviction entries.

Past performance ≠ future results. **Educational use only. Not financial advice.

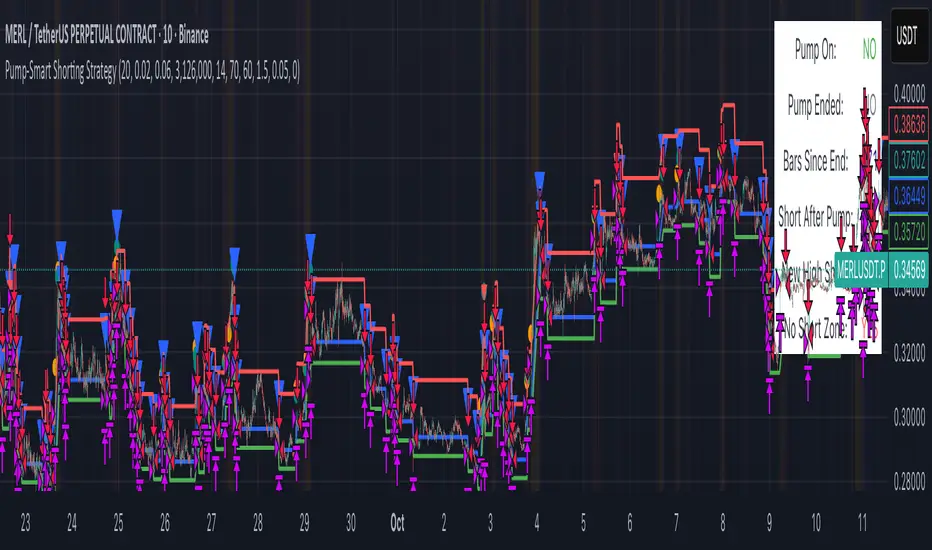

Pump-Smart Shorting StrategyThis strategy is built to keep your portfolio hedged as much as possible while maximizing profitability. Shorts are opened after pumps cool off and on new highs (when safe), and closed quickly during strong upward moves or if stop loss/profit targets are hit. It uses visual overlays to clearly show when hedging is on, off, or blocked due to momentum, ensuring you’re protected in most market conditions but never short against the pump. Fast re-entry keeps the hedge active with minimal downtime.

Pump Detection:

RSI (Relative Strength Index): Calculated over a custom period (default 14 bars). If RSI rises above a threshold (default 70), the strategy considers the market to be in a pump (strong upward momentum).

Volume Spike: The current volume is compared to a 20-bar simple moving average of volume. If it exceeds the average by 1.5× and price increases at least 5% in one bar, pump conditions are triggered.

Price Jump: Measured by (close - close ) / close . A single-bar change > 5% helps confirm rapid momentum.

Pump Zone (No Short): If any of these conditions is true, an orange or red background is shown and shorts are blocked.

Cooldown and Re-Entry:

Cooldown Detection: After the pump ends, RSI must fall below a set value (default ≤ 60), and either volume returns towards average or price momentum is less than half the original spike (oneBarUp <= pctUp/2).

barsWait Parameter: You can specify a waiting period after cooldown before a short is allowed.

Short Entry After Pump/Cooldown: When these cooldown conditions are met, and no short is active, a blue background is shown and a short position is opened at the next signal.

New High Entry:

Lookback New High: If the current high is greater than the highest high in the last N bars (default 20), and pump is NOT active, a short can be opened.

Take Profit (TP) & Stop Loss (SL):

Take Profit: Short is closed if price falls to a threshold below the entry (minProfitPerc, default 2%).

Stop Loss: Short is closed if price rises to a threshold above the entry (stopLossPerc, default 6%).

Preemptive Exit:

Any time a pump is detected while a short position is open, the strategy closes the short immediately to avoid losses.

Visual Feedback:

Orange Background: Market is pumping, do not short.

Red Background: Other conditions block shorts (cooldown or waiting).

Blue Background: Shorts allowed.

Triangles/Circles: Mark entries, pump start/end, for clear trading signals.

Moon Phases Long/Short StrategyThis is an experiment of Moon Phases, likely buy when full moon and sell when new moon with few changes, like it would buy a day ahead or sometimes sell a day post these events, with Stop loss and take profits, 50% profitable so sounds good to me

Long only good for bitcoin gold, both modes(L+S) better for stocks and alt coins

SPY200SMA (+4%/-3%) TQQQ/QQQ STRATEGYSummary of the Improved Strategy: When the price of AMEX:SPY is +4% above the 200SMA BUY NASDAQ:TQQQ and when the price of SPY drops to -3% under the SPY 200SMA SELL everything and slowly DCA into NASDAQ:QQQ over the next 6-12 months or until price returns to +4% above the SPY 200SMA at which point you will go back into 100% TQQQ.

Note: (if the price of QQQ goes 30% above the 200SMA of QQQ deleverage to QQQ or Sell to protect yourself from dot com level event)

More info and stats -https://www.reddit.com/r/LETFs/comments/1nhye66/spy_200sma_43_tqqqqqq_long_term_investment/

超趨勢策略 (中文)-Caelusif ta.change(direction) < 0

strategy.entry("My Long Entry Id", strategy.long)

if ta.change(direction) > 0

strategy.entry("My Short Entry Id", strategy.short)

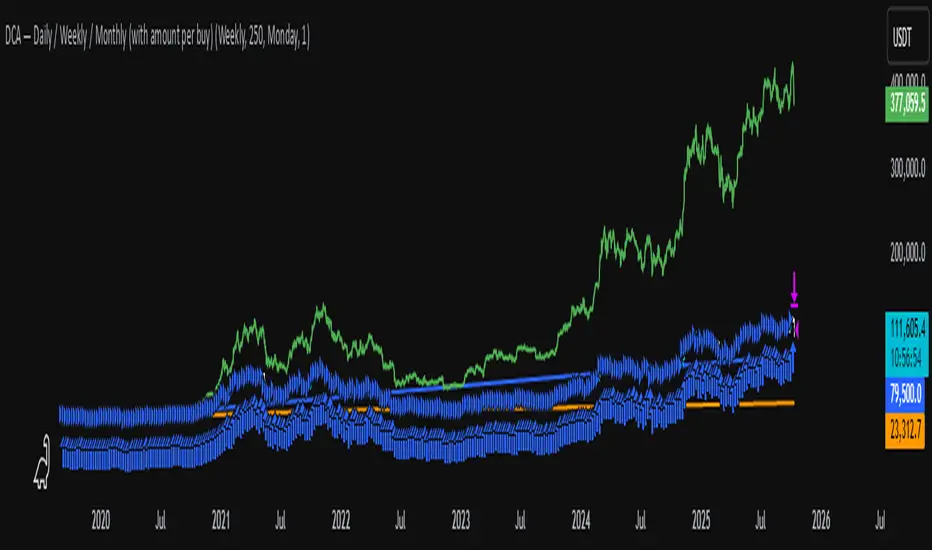

DCA Test Daily / Weekly / Monthly1.Input daily, weekly or monthly preferance of DCA

2.Select how much to DCA

3.Use the slider on the indicator down to select from where to DCA

Important: Don't use a higher timeframe chart than the desired DCA frequency, or all the DCA buys won't get executed.

Confluence Dashboard + Strategy [Daily + Weekly Adaptive]Removed duplicate strategy() declarations

Scoped getWeeklyBias() safely with correct request.security() usage

Ensured all variables are declared before use

Aligned background shading with bias logic

Streamlined signal tier logic to avoid overlap

Integrated strategy entries/exits cleanly

ALMASTO – Pro Trend & Momentum (v1.1)ALMASTO — Pro Trend & Momentum Strategy

Description:

This strategy is designed for precision trading in both Forex (FX) and Crypto markets.

It combines multi-timeframe trend confirmation (EMA200), momentum filters (RSI, MACD, ADX), and ATR-based dynamic risk management.

ALMASTO — Pro Trend & Momentum Strategy automatically manages take-profit levels, stop-loss, and breakeven adjustments once TP1 is reached — providing a structured and emotion-free trading approach.

Optimal Use

Works best on lower timeframes (5m–15m) with strong liquidity sessions.

Optimized for pairs like EURUSD, XAUUSD, and BTCUSDT.

Built for trend-following setups and momentum reversals with high volatility confirmation.

Recommended Settings

🔹 Forex – 5m

EMA Fast = 34, EMA Slow = 200, HTF = 1H

RSI (14): Long ≥ 55 / Short ≤ 45

MACD (8 / 21 / 5), ADX Len 10 / Min 27

ATR Len 7, Stop Loss = ATR × 2.1

TP1 = 1.1 RR, TP2 = 2.3 RR

Session = 07:00–11:00 & 12:30–16:00 (Exchange Time)

Risk = 0.8% per trade

🔹 Forex – 15m

EMA Fast = 50, EMA Slow = 200, HTF = 4H

RSI (14): Long ≥ 53 / Short ≤ 47

MACD (12 / 26 / 9), ADX Min 24

ATR Len 10, SL = ATR × 1.9

TP1 = 1.2 RR, TP2 = 2.6 RR

Risk = 1.0% per trade

🔹 Crypto – 5m (BTC/USDT)

EMA Fast = 34, EMA Slow = 200, HTF = 4H

RSI (14): Long ≥ 56 / Short ≤ 44

MACD (8 / 21 / 5), ADX Min 30

ATR Len 7, SL = ATR × 2.2

TP1 = 1.0 RR, TP2 = 2.5 RR

Session = 00:00–06:00 & 12:00–22:00 (UTC)

Risk = 0.5% per trade

Core Features

✅ Auto breakeven after TP1

✅ Dual take-profit system (1:1 & 1:2 RR)

✅ ATR-based stop & trailing logic

✅ Filters for session time, volume, and volatility

✅ Candle-body vs ATR size filter to avoid noise

✅ Optional cooldown between trades

Important Notes

Use bar close confirmation only (barstate.isconfirmed) to avoid repainting on lower timeframes.

Adjust commission (0.01–0.03%) and slippage (1–2 ticks) in Strategy Tester for realistic results.

Avoid low-liquidity hours (after 21:00 UTC for FX / after midnight for crypto).

Backtest using realistic broker data (e.g., BlackBull Markets / Bybit / Binance Futures).

Best results occur during London & New York sessions with moderate volatility.

⚠️ Disclaimer

This script is for educational and research purposes only.

It does not constitute financial advice.

Use proper risk management and test thoroughly before using on live accounts.

Developed by KING FX Labs

Built and optimized by Yousef Almasto — combining advanced price-action logic, multi-timeframe EMA structure, and volatility-adaptive ATR management.

Tested across Forex, Gold, and Crypto markets to ensure consistent performance and minimal drawdown.

📈 “Precision Trading. Zero Emotion. Pure Momentum.”

Strategy with Reference Lines📊 Strategy with Reference Lines

Description:

This strategy uses a contrarian approach based on the analysis of the previous candle to identify entry and exit points. The strategy draws horizontal reference lines at important levels of the previous candle and generates buy/sell signals based on the candle's direction.

Key Features:

🔹 Multi-Timeframe Analysis: Configurable for 1H, 2H, 3H, 4H, 6H, 12H, and 1D

🔹 Reference Lines: High, low, close, and midpoint (50%) of the previous candle

🔹 Visual Signals: Labels with prices and actions (BUY/SELL/TP)

🔹 Optional Trading: Enable/disable automatic order execution

🔹 Complete System: Automatic entry, Take Profit, and Stop Loss

🔹 Alerts: Notifications when a new candle is detected

Strategy Logic:

When the previous candle is POSITIVE:

Signal: 🔴 SELL at the previous candle's close

Take Profit: 🎯 Midpoint (50%) of the previous candle

Stop Loss: 🔴 High of the previous candle

When the previous candle is NEGATIVE:

Signal: 🟢 BUY at the previous candle's close

Take Profit: 🎯 Midpoint (50%) of the previous candle

Stop Loss: 🟢 Low of the previous candle

Visual Elements:

Green Line: High of the previous candle (when positive)

Red Line: Low of the previous candle (when negative)

Yellow Line: Close of the previous candle (always present)

Blue Line: Midpoint (50%) of the previous candle (always present)

Labels: Prices and actions with emojis for easy identification

Settings:

Timeframe: Default 4H (configurable)

Auto Trading: Disabled by default (safety)

Alerts: Include entry prices, TP, and SL

Recommended Usage:

✅ Visual Analysis: Use with trading disabled for analysis

✅ Backtesting: Enable trading to test historically

✅ Swing Trading: Ideal for 4H or higher timeframes

✅ Risk Management: Automatic SL and TP for protection

Risk Disclaimer:

This strategy is for educational and analysis purposes only. Always test in a simulation environment before using with real capital. Trading involves significant risks and may result in losses.

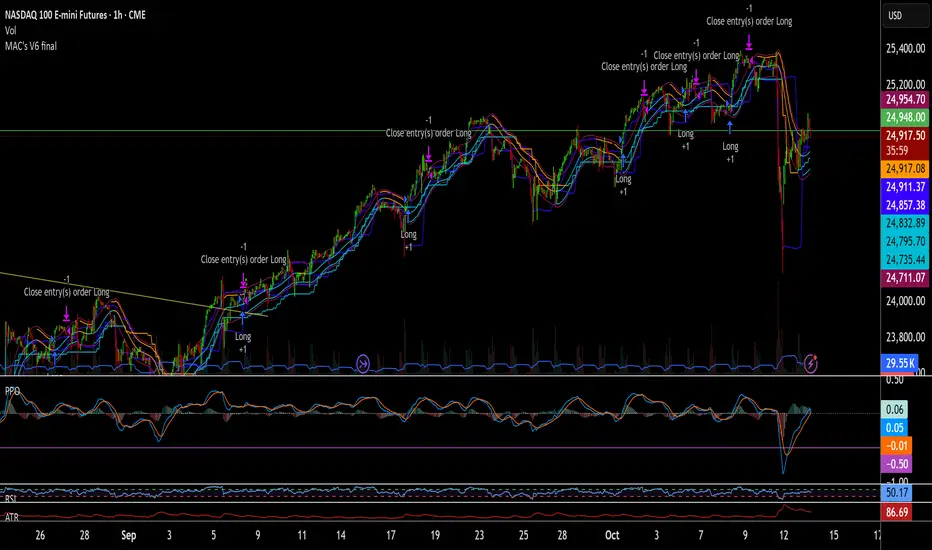

MAC's V6 finalBreakout retest strategy

Works best on a NQ 1 hour chart

Also works on other futures charts

Adjust the initial capital to 100000

and the margin requirement percent to 0

Supertrend + MACD + EMA200 (Pro) V2 — Strict & TrailingThis strategy uses Supertrend, MACD and EMA 200 as indicators. When all three indicators shows the sema direction, you enter the trade.

LW Outside Day Strategy[SpeculationLab]This strategy is inspired by the “Outside Day” concept introduced by Larry Williams in Long-Term Secrets to Short-Term Trading, and has been extended with configurable risk management tools and realistic backtesting parameters.

Concept

The “Outside Day” is a classic price action pattern that reflects strong market rejection or continuation pressure.

An Outside Bar occurs when the current bar’s high exceeds the previous high and the low falls below the previous low.

A body-size filter ensures only significant candles are included.

Entry Logic

Buy setup: Price closes below the previous low (bullish rejection).

Sell setup: Price closes above the previous high (bearish rejection).

Only confirmed bars are used (no intrabar signals).

Stop-Loss Modes

Prev Low/High: Uses the previous swing point ± ATR-based buffer.

ATR: Dynamic stop based on Average True Range × multiplier.

Fixed Pips: User-defined fixed distance (for forex testing).

Take-Profit Modes

Prev High/Low (PHL): Exits near the opposite swing.

Risk-Reward (RR): Targets a user-defined multiple of the stop distance (default = 2 : 1).

Following Price Open (FPO): Exits on the next bar’s open if price opens in profit (used to test overnight price continuation).

Risk Management & Backtest Settings

Default risk per trade is set at 10% of account equity (user-adjustable).

Commission = 0.1% and slippage = 2 ticks are applied to simulate realistic conditions.

For reliable statistics, test on data that yields over 100 trades.

Suitable for daily and 4-hour timeframes across stocks, forex, and crypto markets.

Visual Elements

Green and red triangles show entry signals.

Stop-loss (red) and take-profit (green) reference lines are drawn for clarity.

Optional alerts notify when a valid setup forms.

Disclaimer

This script is for educational and research purposes only.

It does not constitute financial advice or guarantee profits.

Always backtest thoroughly and manage your own risk.

Enhancements over Classic Outside Bar Models

Adjustable stop and target logic with ATR and buffer multipliers.

“Following Price Open” exit logic for realistic day-end management.

Optimized to avoid repainting and bar-confirmation issues.

Built with realistic trading costs and position sizing.

策略逻辑

外包线识别

当日最高价高于前一日最高价,且当日最低价低于前一日最低价,即形成外包线。

同时过滤掉较小实体的 K 线,仅保留实体显著大于前一根的形态。

方向过滤

收盘价低于前一日最低价 → 视为买入信号。

收盘价高于前一日最高价 → 视为卖出信号。

止损设置(可选参数)

前低/高止损:以形态前低/前高为止损,带有缓冲倍数。

ATR 止损:根据平均波动率(ATR)动态调整。

固定点数止损:按照用户设定的点数作为止损范围。

止盈设置(可选参数)

前高/低止盈(PHL):以前高/前低为目标。

固定盈亏比(RR):根据用户设定的风险回报比自动计算。

隔夜开盘(FPO):若次日开盘价高于进场价(多单)或低于进场价(空单),则平仓。

信号标记

在图表中标注买入/卖出信号(三角形标记)。

绘制止损与目标位参考线。

使用说明

适用周期:建议用于 日线图(Daily)。

适用市场:股票、外汇、加密货币等各类市场均可。

提示:此策略为历史研究与学习用途,不构成投资建议。实际交易请结合自身风险管理。

Larry Williams Oops StrategyThis strategy is a modern take on Larry Williams’ classic Oops setup. It trades intraday while referencing daily bars to detect opening gaps and align entries with the prior day’s direction. Risk is managed with day-based stops, and—unlike the original—all positions are closed at the end of the session (or at the last bar’s close), not at a fixed profit target or the first profitable open.

Entry Rules

Long setup (bullish reversion): Today opens below yesterday’s low (down gap) and yesterday’s candle was bearish. Place a buy stop at yesterday’s low + Filter (ticks).

Short setup (bearish reversion): Today opens above yesterday’s high (up gap) and yesterday’s candle was bullish. Place a sell stop at yesterday’s high − Filter (ticks).

Longs are only taken on down-gap days; shorts only on up-gap days.

Protective Stop

If long, stop loss trails the current day’s low.

If short, stop loss trails the current day’s high.

Exit Logic

Positions are force-closed at the end of the session (in the last bar), ensuring no overnight exposure. There is no take-profit; only stop loss or end-of-day flat.

Notes

This strategy is designed for intraday charts (minutes/seconds) using daily data for gaps and prior-day direction.

Longs/shorts can be enabled or disabled independently.

Larry Williams Bonus Track PatternThis strategy trades the day immediately following an Inside Day, under specific directional and timing conditions. It is designed for daily-based setups but executed on intraday charts to ensure orders are placed exactly at the open of the following day, rather than at the daily bar close.

Entry Conditions

Only trades on Monday, Thursday, or Friday.

The previous day must be an Inside Day (its high is lower than the prior high and its low is higher than the prior low).

The bar before the Inside Day must be bullish (close > open).

On the following day (t):

The daily open must be below both the Inside Day’s high and the highest high of the two days before that.

A buy stop is placed at the highest high of the three previous days (Inside Day and the two days before it).

If the new day’s open is already above that level (gap up), the strategy enters long immediately at the open.

Exit Rules

Stop Loss: Fixed, defined in points or percentage (user input).

FPO (First Profitable Open): the position is closed at the first daily open after the entry day where the open price is above the average entry price (the first profitable open).

Notes

The script must be applied on an intraday timeframe (e.g., 15-minute or 1-hour) so that the strategy can:

Detect the Inside Day pattern using daily data (request.security).

Execute orders in real time at the next day’s open.

Running it directly on the daily timeframe will delay executions by one bar due to Pine Script’s evaluation model.

ORDER BLCOK custom strategy# OB Matrix Strategy - Documentation

**Version:** 1.0

**Author:** HPotter

**Date:** 31/07/2017

The **OB Matrix Strategy** is based on the identification of **bullish and bearish Order Blocks** and the management of conditional orders with multiple Take Profit (TP) and Stop Loss (SL) levels. It uses trend filters, ATR, and percentage-based risk management.

---

## 1. Main Parameters

### Strategy

- `initial_capital`: 50

- `default_qty_type`: percentage of capital

- `default_qty_value`: 10

### Money Management

- `rr_threshold`: minimum Risk/Reward threshold to open a trade

- `risk_percent`: percentage of capital to risk per trade (default 2%)

- `maxPendingBars`: maximum number of bars for a pending order

- `maxBarsOpen`: maximum number of bars for an open position

- `qty_tp1`, `qty_tp2`, `qty_tp3`: quantity percentages for multiple TPs

---

## 2. Order Block Identification

### Order Block Parameters

- `obLookback`: number of bars to identify an Order Block

- `obmode`: method to calculate the block (`Full` or `Breadth`)

- `obmiti`: method to determine block mitigation (`Close`, `Wick`, `Avg`)

- `obMaxBlocks`: maximum number of Order Blocks displayed

### Main Variables

- `bullBlocks`: array of bullish blocks

- `bearBlocks`: array of bearish blocks

- `last_bull_volume`, `last_bear_volume`: volume of the last block

- `dom_block`: dominant block type (Bullish/Bearish/None)

- `block_strength`: block strength (normalized volume)

- `price_distance`: distance between current price and nearest block

---

## 3. Visual Parameters

- `Width`: line thickness for swing high/low

- `amountOfBoxes`: block grid segments

- `showBorder`: show block borders

- `borderWidth`: width of block borders

- `showVolume`: display volume inside blocks

- `volumePosition`: vertical position of volume text

Customizable colors:

- `obHighVolumeColor`, `obLowVolumeColor`, `obBearHighVolumeColor`, `obBearLowVolumeColor`

- `obBullBorderColor`, `obBearBorderColor`

- `obBullFillColor`, `obBearFillColor`

- `volumeTextColor`

---

## 4. Screener Table

- `showScreener`: display the screener table

- `tablePosition`: table position (`Top Left`, `Top Right`, `Bottom Left`, `Bottom Right`)

- `tableSize`: table size (`Small`, `Normal`, `Large`)

The table shows:

- Symbol, Timeframe

- Type and status of Order Block

- Number of retests

- Bullish and bearish volumes

---

## 5. Trend Filters

- EMA as a trend filter (`emaPeriod`, default 223)

- `bullishTrend` if close > EMA

- `bearishTrend` if close < EMA

---

## 6. ATR and Swing Points

- ATR calculated with a customizable period (`atrLength`)

- Swing High/Low for SL/TP calculation

- `f_getSwingTargets` function to calculate SL and TP based on direction

---

## 7. Trade Logic

### Buy Limit on Bullish OB

- Conditions:

- New bullish block

- Uptrend

- RR > threshold (`rr_threshold`)

- SL: `bullishOBPrice * (1 - atr * atrMultiplier)`

- Multiple TPs: TP1 (50%), TP2 (80%), TP3 (100% max)

- Quantity calculation based on percentage risk

### Sell Limit on Bearish OB

- Conditions:

- New bearish block

- Downtrend

- RR > threshold (`rr_threshold`)

- SL: `bearishOBPrice * (1 + atr * atrMultiplier)`

- Multiple TPs: TP1 (50%), TP2 (80%), TP3 (100% max)

- Quantity calculation based on percentage risk

---

## 8. Order Management and Timeout

- Close pending orders after `maxPendingBars` bars

- Close open positions after `maxBarsOpen` bars

- Label management for open orders

---

## 9. Alert Conditions

- `bull_touch`: price inside maximum bullish volume zone

- `bear_touch`: price inside maximum bearish volume zone

- `bull_reject`: confirmation of bullish zone rejection

- `bear_reject`: confirmation of bearish zone rejection

- `new_bull`: new bullish block

- `new_bear`: new bearish block

---

## 10. Level Calculation

- Swing levels based on selected timeframe (`SelectPeriod`)

- `xHigh` and `xLow` for S1 and R1 calculation

- Levels plotted on chart

---

## 11. Take Profit / Stop Loss

- Extended horizontal lines (`extendBars`) to visualize TP and SL

- Customizable colors (`tpColor`, `slColor`)

---

## 12. Notes

- Complete script based on Pine Script v5

- Advanced graphical management with boxes, lines, labels

- Dynamically displays volumes and Order Blocks

- Integrated internal screener

---

### End of Documentation

Larry Williams - Smash Day (SL/TP in %)This strategy implements Larry Williams’ “Smash Day” reversal concept on any symbol and timeframe (daily is the classic). A Smash Day is a bar that closes beyond a recent extreme and then potentially reverses on the next session.

Short Only Bot (3Commas Webhook Uyumlu)Short işlem açmaya ce 3commans ile uyumlu hacim odaklı indikatör. halka açık herkes kullanabilir.

the Father, the Son, and the Holy SpiritThis is a tool used to find great trades! It's the Father, the Son, and the Holy Spirit.

Camarilla Pivots + 20 EMA StrategyThis is an intraday volatility and trend-following system for commodities like Natural Gas, combining dynamic pivot levels (Camarilla) with a trend filter (20-period EMA) to improve risk-reward and reduce false breakouts.

Core Components

1. Camarilla Pivots:

These are special support and resistance levels (H3, H4, L3, L4) calculated each day based on the previous day's high, low, and close.

The pivots adapt to daily volatility, giving more relevant breakout and bounce zones than static lines.

H4: Aggressive resistance (used for breakout LONG entry)

H3: Moderate resistance/support (used for bounce or stoploss)

L4: Aggressive support (used for breakout SHORT entry)

L3: Moderate support/resistance (used for bounce or stoploss)

2. 20 EMA (Exponential Moving Average):

Plotted on the 30-minute chart, this acts as a trend filter.

If the price is above 20 EMA: Only look for long trades (bullish bias).

If below 20 EMA: Only look for short trades (bearish bias).

How the Strategy Works

Setup (30-Min Chart):

Camarilla pivots for the day are drawn on the chart.

20 EMA is also plotted.

Trade Filter:

Bullish: Trade ONLY if price is above 20 EMA.

Bearish: Trade ONLY if price is below 20 EMA.

Entry:

LONG: Enter when price breaks and closes above the H4 pivot AND is above 20 EMA.

SHORT: Enter when price breaks and closes below the L4 pivot AND is below 20 EMA.

Stop Loss:

LONG: Place stoploss at H3 (the next lower Camarilla resistance).

SHORT: Place stoploss at L3 (the next higher Camarilla support).

Target:

Always set a profit target at 2x the distance (risk) between entry and stoploss (strict R:R 2).

For example, if your entry is at H4 and stoploss at H3, your target is entry + 2*(entry - stoploss).

Alerts & Visuals:

The strategy plots entry arrows, stoploss and target lines for immediate visual reference.

Alerts trigger on breakout signals so you never miss a trade.

Why This Works Well for Natural Gas

Adapts to volatility: The pivots change daily, handling wide-ranging and choppy price moves better than fixed breakouts.

Trend filter: EMA prevents counter-trend whipsaws, only trades with market momentum.

Risk control: Every trade must meet strict risk-reward criteria, so losses are contained and winners can outweigh losers.

Ajay R5.41🔻 Ajay Gold 3H Power Indicator 🔻

Precision-Based Smart Sell System for Gold (XAU/USD)

💡 Overview

This indicator is specifically designed for Gold (XAU/USD) and delivers best results on the 3-Hour Timeframe (3H TF).

It is a Smart Money Logic-based Sell Confirmation System, combining institutional structure and candle behavior to generate highly accurate bearish signals.

⚙️ Technical Foundation

The indicator uses multiple advanced confirmations:

📉 EMA Trend Filter → Confirms downtrend

💪 RSI Overbought Rejection → Momentum reversal signal

📊 MACD Bearish Cross → Confirms trend strength

🕯️ Bearish Candle Structure → Price action validation

When all conditions align, a clear 🔻 Sell Signal is plotted on the chart.

💎 Hidden Feature

This indicator includes a hidden feature that activates only when the correct market structure forms.

It helps reduce false signals and increases accuracy without being visible on the chart — fully automated internal logic.

📆 Recommended Settings

Symbol: XAU/USD (Gold)

Timeframe: 3-Hour (3H)

Market: Forex / Commodity

Mode: Sell-Only Confirmation Indicator

Performance: Best precision and consistency on 3H TF

📈 How to Use

Select XAU/USD on chart and set 3H timeframe.

Add the indicator to the chart.

Wait for the 🔻 Sell Signal and confirm the market structure after candle close.

Take entry according to your risk management.

⚠️ Disclaimer

This indicator is for educational and analytical purposes only.

No system is 100% accurate — always backtest and demo trade before using in real trading.

💬 Credits

Developed by Ajay Sahu (India)

Based on Institutional & Smart Money Logic

Best results on 3H TF

Hidden Algorithm for XAU/USD traders

EMA Trend Buy sell strategyThis strategy is built to help investors get into a trend safely and smartly — without rushing and without getting in and out too often.

When to Buy:

First Signal – Small Step In (50% Buy)

When the short-term trend (EMA 18) turns positive and goes above the medium trend (EMA 33),

👉 we buy half of our planned position.

This is an early warning that a new upward trend might be starting.

Second Signal – Full Confidence (Buy other 50%)

If the medium-term trend (EMA 33) also crosses above the long-term (EMA 50),

👉 we buy the other half of the position.

Now we’re more confident that the trend is real.

When to Sell:

First Warning – Reduce Position (Sell 50%)

If EMA 33 falls below EMA 50,

👉 we sell half of the position to reduce risk.

Trend Reversal – Exit Completely (Sell the rest)

If EMA 18 also falls below EMA 33,

👉 we sell the remaining half and leave the trade fully.

Why This Strategy?

📉 We don’t jump in all at once.

→ We wait for confirmation before going full in.

⏳ We stay in the trade as long as the trend is healthy.

→ No overtrading or reacting to small moves.

📊 We get out slowly, not suddenly.

→ This helps protect profits and avoid emotional decisions.