The Oracle: Dip & Top Adaptive Sniper [Hakan Yorganci]█ OVERVIEW

The Oracle: Dip & Top Adaptive Sniper is a precision-focused trend trading strategy designed to solve the biggest problem in swing trading: Timing.

Most trend-following strategies chase price ("FOMO"), buying when the asset is already overextended. The Oracle takes a different approach. It adopts a "Sniper" mentality: it identifies a strong macro trend but patiently waits for a Mean Reversion (pullback) to execute an entry at a discounted price.

By combining the structural strength of Moving Averages (SMA 50/200) with the momentum precision of RSI and the volatility filtering of ADX, this script filters out noise and targets high-probability setups.

█ HOW IT WORKS

This strategy operates on a strictly algorithmic protocol known as "The Yorganci Protocol," which involves three distinct phases: Filter, Target, and Execute.

1. The Macro Filter (Trend Identification)

* SMA 200 Rule: By default, the strategy only scans for buy signals when the price is trading above the 200-period Simple Moving Average. This ensures we are always trading in the direction of the long-term bull market.

* Adaptive Switch: A new feature allows users to toggle the Only Buy Above SMA 200? filter OFF. This enables the strategy to hunt for oversold bounces (dead cat bounces) even during bearish or neutral market structures.

2. The Volatility Filter (ADX Integration)

* Sideways Protection: One of the main weaknesses of moving average strategies is "whipsaw" losses during choppy, ranging markets.

* Solution: The Oracle utilizes the ADX (Average Directional Index). It will BLOCK any trade entry if the ADX is below the threshold (Default: 20). This ensures capital is only deployed when a genuine trend is present.

3. The Sniper Entry (Buying the Dip)

* Instead of buying on breakout strength (e.g., RSI > 60), The Oracle waits for the RSI Moving Average to dip into the "Value Zone" (Default: 45) and cross back up. This technique allows for tighter stops and higher Risk/Reward ratios compared to traditional breakout systems.

█ EXIT STRATEGY

The Oracle employs a dynamic dual-exit mechanism to maximize gains and protect capital:

* Take Profit (The Peak): The strategy monitors RSI heat. When the RSI Moving Average breaches the Overbought Threshold (Default: 75), it signals a "Take Profit", securing gains near the local top before a potential reversal.

* Stop Loss (Trend Invalidated): If the market structure fails and the price closes below the 50-period SMA, the position is immediately closed to prevent deep drawdowns.

█ SETTINGS & CONFIGURATION

* Moving Averages: Fully customizable lengths for Support (SMA 50) and Trend (SMA 200).

* Trend Filter: Checkbox to enable/disable the "Bull Market Only" rule.

* RSI Thresholds:

* Sniper Buy Level: Adjustable (Default: 45). Lower values = Deeper dips, fewer trades.

* Peak Sell Level: Adjustable (Default: 75). Higher values = Longer holds, potentially higher profit.

* ADX Filter: Checkbox to enable/disable volatility filtering.

█ BEST PRACTICES

* Timeframe: Designed primarily for 4H (4-Hour) charts for swing trading. It can also be used on 1H for more frequent signals.

* Assets: Highly effective on trending assets such as Bitcoin (BTC), Ethereum (ETH), and high-volume Altcoins.

* Risk Warning: This strategy is designed for "Long Only" spot or leverage trading. Always use proper risk management.

█ CREDITS

* Original Concept: Inspired by the foundational work of Murat Besiroglu (@muratkbesiroglu).

* Algorithm Development & Enhancements: Developed by Hakan Yorganci (@hknyrgnc).

* Modifications include: Integration of ADX filters, Mean Reversion entry logic (RSI Dip), and Dynamic Peak Profit taking.

Swingtrading

Universal Breakout Strategy [KedArc Quant]Description:

A flexible breakout framework where you can test different logics (Prev Day, Bollinger, Volume, ATR, EMA Trend, RSI Confirm, Candle Confirm, Time Filter) under one system.

Choose your breakout mode, and the strategy will handle entries, exits, and optional risk management (ATR stops, take-profits, daily loss guard, cooldowns).

An on-chart info table shows live mode values (like Prev High/Low, Bollinger levels, RSI, etc.) plus P&L stats for quick analysis.

Use it to compare which breakout style works best on your instrument and timeframe, whether intraday, swing, or positional trading

🔑 Why it’s useful

* Flexibility: Switch between breakout strategies without loading different indicators.

* Clarity: On-chart info table displays current mode, relevant indicator levels, and live strategy P&L stats.

* Testing efficiency: Quickly A/B test different breakout styles under the same backtest environment.

* Transparency: Every trade is rule-based and displayed with entry/exit markers.

🚀 How it helps traders

* Lets you experiment with breakout strategies quickly without loading multiple scripts.

* Helps identify which breakout method fits your instrument & timeframe.

* Gives clear on-chart visual + statistical feedback for confident decision-making.

⚙️ Input Configuration

* Breakout Mode → choose which strategy to test:

* *Prev Day* → breakouts of yesterday’s High/Low.

* *Bollinger* → Upper/Lower BB pierce.

* *Volume* → Breakout confirmed with volume above average.

* *ATR Stop* → Wide range breakout using ATR filter.

* *Time Filter* → Breakouts inside defined session hours.

* *EMA Trend* → Breakouts only in EMA fast > slow alignment.

* *RSI Confirm* → Breakouts with RSI confirmation (e.g. >55 for longs).

* *Candle Confirm* → Breakouts validated by bullish/bearish candle.

* Lookback / ATR / Bollinger inputs → adjust sensitivity.

* Intrabar mode → option to evaluate breakouts using bar highs/lows instead of closes.

* Table options → show/hide info table, show/hide P&L stats, choose corner placement.

📈 Entry & Exit Logic

* Entry → occurs when breakout condition of chosen mode is met.

* Exit → default exits via opposite signals or optional stop/target if enabled.

* Session filter → optional auto-flat at session end.

* P&L management → optional daily loss guard, cooldown between trades, and ATR-based stop/take profit.

❓ FAQ — Choosing the best setup

Q: Which strategy should I use for which chart?

* *Prev Day Breakouts*: Best on indices, FX, and liquid futures with strong daily levels.

* *Bollinger*: Works well in range-bound environments, or crypto pairs with volatility compression.

* *Volume*: Good on equities where breakout strength is tied to volume spikes.

* *ATR Stop*: Suits volatile instruments (commodities, crypto).

* *EMA Trend*: Useful in trending markets (stocks, indices).

* *RSI Confirm*: Adds momentum filter, better for swing trades.

* *Candle Confirm*: Ideal for scalpers needing visual confirmation.

* *Time Filter*: For intraday traders who want signals only in high-liquidity sessions.

Q: What timeframe should I use?

* Intraday traders → 5m to 15m (Time Filter, Candle Confirm).

* Swing traders → 1H to 4H (EMA Trend, RSI Confirm, ATR Stop).

* Position traders → Daily (Prev Day, Bollinger).

* Breakout

A trade entry condition triggered when price crosses above a resistance level (for longs) or below a support level (for shorts).

* Prev Day High/Low

Formula:

Prev High = High of (Day )

Prev Low = Low of (Day )

* Bollinger Bands

Formula:

Basis = SMA(Close, Length)

Upper Band = Basis + (Multiplier × StdDev(Close, Length))

Lower Band = Basis – (Multiplier × StdDev(Close, Length))

* Volume Confirmation

A breakout is only valid if:

Volume > SMA(Volume, Length)

* ATR (Average True Range)

Measures volatility.

Formula:

ATR = SMA(True Range, Length)

where True Range = max(High–Low, |High–Close |, |Low–Close |)

* EMA (Exponential Moving Average)

Weighted moving average giving more weight to recent prices.

Formula:

EMA = (Price × α) + (EMA × (1–α))

with α = 2 / (Length + 1)

* RSI (Relative Strength Index)

Momentum oscillator scaled 0–100.

Formula:

RSI = 100 – (100 / (1 + RS))

where RS = Avg(Gain, Length) ÷ Avg(Loss, Length)

* Candle Confirmation

Bullish candle: Close > Open AND Close > Close

Bearish candle: Close < Open AND Close < Close

Win Rate (%)

Formula:

Win Rate = (Winning Trades ÷ Total Trades) × 100

* Average Trade P&L

Formula:

Avg Trade = Net Profit ÷ Total Trades

📊 Performance Notes

The Universal Breakout Strategy is designed as a framework rather than a single-asset optimized system. Results will vary depending on the chart, timeframe, and asset chosen.

On the current defaults (15-minute, INR-denominated example), the backtest produced 132 trades over the selected period. This provides a statistically sufficient sample size.

Win rate (~35%) is relatively low, but this is balanced by a positive reward-to-risk ratio (~1.8). In practice, a lower win rate with larger wins versus smaller losses is sustainable.

The average P&L per trade is close to breakeven under default settings. This is expected, as the strategy is not tuned for a single symbol but offered as a universal breakout framework.

Commissions (0.1%) and slippage (1 tick) are included in the simulation, ensuring realistic conditions.

Risk management is conservative, with order sizing set at 1 unit per trade. This avoids over-leveraging and keeps exposure well under the 5-10% equity risk guideline.

👉 Traders are encouraged to:

Experiment with inputs such as ATR period, breakout length, or Bollinger parameters.

Test across different timeframes and instruments (equities, futures, forex, crypto) to find optimal setups.

Combine with filters (trend direction, volatility regimes, or volume conditions) for further refinement.

⚠️ Disclaimer This script is provided for educational purposes only.

Past performance does not guarantee future results.

Trading involves risk, and users should exercise caution and use proper risk management when applying this strategy.

Trendline Breakout Strategy [KedArc Quant] Description

A single, rule-based system that builds two trendlines from confirmed swing pivots and trades their breakouts, with optional retest, trend-regime gates (EMA / HTF EMA), and ATR-based risk. All parts serve one decision flow: structure → breakout → gated entry → managed risk.

What it does (for traders)

Draws Up line (teal) through the last two Higher Lows and Down line (red) through the last two Lower Highs, then extends them forward.

Long when price breaks above red; Short when price breaks below teal.

Optional Retest entry: after a break, wait for a pullback toward the broken line within an ATR-scaled buffer.

Uses ATR stop and R-multiple target so risk is consistent across symbols/timeframes.

Labels HL1/HL2/LH1/LH2 so non-coders can verify which pivots built each line.

Why these components are combined

Pure breakout systems on trendlines suffer from three practical issues:

False breaks in chop → solved by trend-regime gates (EMA / HTF EMA) that only allow trades aligned with the prevailing trend.

Uneven volatility across markets/timeframes → solved by ATR-based stop/target, normalizing distance so R-multiples are comparable.

First break whipsaws near wedge apices → mitigated by the optional retest rule that demands a pullback/hold before entry.

These modules are not separate indicators with their own signals. They are support roles inside one method.

The pivot engine defines structure, the breakout detector defines signal, the regime gates decide if we’re allowed to take that signal, and the ATR module sizes risk.

Together they make the trendline breakout usable, testable, and explainable.

How it works (mechanism; each component explained)

1) Pivot engine (structure, non-repainting)

Swings are confirmed with ta.pivotlow/high(L, R). A pivot only exists after R bars (no look-ahead), so once plotted, the line built from those pivots will not repaint.

2) Trendline builder (geometry)

Teal line updates when two consecutive pivot lows satisfy HL2.price > HL1.price (and HL2 occurs after HL1).

Red line updates when two consecutive pivot highs satisfy LH2.price < LH1.price.

Lines are extended right and their current value is read every bar via line.get_price().

3) Breakout detector (signal)

On every bar, compute:

crossover(close, redLine) ⇒ Long breakout

crossunder(close, tealLine) ⇒ Short breakdown

4) Regime gates (trend filters, not separate signals)

EMA gate: allow longs only if close > EMA(len), shorts only if close < EMA(len).

HTF EMA gate (optional): same rule on a higher timeframe to avoid fighting the larger trend.

These do not create entries; they simply permit or block the breakout signal.

5) Retest module (optional confirmation)

After a breakout, record the line price. A valid retest occurs if price pulls back within an ATR-scaled buffer toward that broken line and then closes back in the breakout direction.

This reduces first-tick fakeouts.

6) Risk module (position exit)

Initial stop = ATR(len) × atrMult from entry.

Target = tpR × (ATR × atrMult) (e.g., 2R).

This keeps results consistent across instruments/timeframes.

Entries & exits

Long entry

Base: close breaks above red and passes EMA/HTF gates.

Retest (if enabled): after the break, price pulls back near the broken red line (within the ATR buffer) and holds; then enter.

Short entry

Mirror logic with teal (break below & gates), optionally with a retest.

Exit

strategy.exit places ATR stop & R-multiple target automatically.

Optional “flip”: close if the opposite base signal triggers.

How to use it (step-by-step)

Timeframe: 1–15m for intraday, 1–4h for swing.

Start defaults: Pivot L/R = 5, EMA len = 200, ATR len = 14, ATR mult = 2, TP = 2R, Retest = ON.

Tune sensitivity:

Faster lines (more trades): set L/R = 3–4.

Fewer counter-trend trades: enable HTF EMA (e.g., 60-min or Daily).

Visual audit: labels HL1/HL2 & LH1/LH2 show which pivots built each line—verify by eye.

Alerts: use Long breakout, Short breakdown, and Retest alerts to automate.

Originality (why it merits publication)

Trades the visualization: many “auto-trendline” tools only draw lines; this one turns them into testable, alertable rules.

Integrated design: each component has a defined role in the same pipeline—no unrelated indicators bolted together.

Transparent & non-repainting: pivot confirmation removes look-ahead; labels let non-coders understand the setup that produced each signal.

Notes & limitations

Lines update only after pivot confirmation; that lag is intentional to avoid repainting.

Breakouts near an apex can whipsaw; prefer Retest and/or HTF gate in choppy regimes.

Backtests are idealized; forward-test and size risk appropriately.

⚠️ Disclaimer

This script is provided for educational purposes only.

Past performance does not guarantee future results.

Trading involves risk, and users should exercise caution and use proper risk management when applying this strategy.

Hazel nut BB Strategy, volume base- lite versionHazel nut BB Strategy, volume base — lite version

Having knowledge and information in financial markets is only useful when a trader operates with a well-defined trading strategy. Trading strategies assist in capital management, profit-taking, and reducing potential losses.

This strategy is built upon the core principle of supply and demand dynamics. Alongside this foundation, one of the widely used technical tools — the Bollinger Bands — is employed to structure a framework for profit management and risk control.

In this strategy, the interaction of these tools is explained in detail. A key point to note is that for calculating buy and sell volumes, a lower timeframe function is used. When applied with a tick-level resolution, this provides the most precise measurement of buyer/seller flows. However, this comes with a limitation of reduced historical depth. Users should be aware of this trade-off: if precise tick-level data is required, shorter timeframes should be considered to extend historical coverage .

The strategy offers multiple configuration options. Nevertheless, it should be treated strictly as a supportive tool rather than a standalone trading system. Decisions must integrate personal analysis and other instruments. For example, in highly volatile assets with narrow ranges, it is recommended to adjust profit-taking and stop-loss percentages to smaller values.

◉ Volume Settings

• Buyer and seller volume (up/down volume) are requested from a lower timeframe, with an option to override the automatic resolution.

• A global lookback period is applied to calculate moving averages and cumulative sums of buy/sell/delta volumes.

• Ratios of buyers/sellers to total volume are derived both on the current bar and across the lookback window.

◉ Bollinger Band

• Bands are computed using configurable moving averages (SMA, EMA, RMA, WMA, VWMA).

• Inputs allow control of length, standard deviation multiplier, and offset.

• The basis, upper, and lower bands are plotted, with a shaded background between them.

◉ Progress & Proximity

• Relative position of the price to the Bollinger basis is expressed as percentages (qPlus/qMinus).

• “Near band” conditions are triggered when price progress toward the upper or lower band exceeds a user-defined threshold (%).

• A signed score (sScore) represents how far the close has moved above or below the basis relative to band width.

◉ Info Table

• Optional compact table summarizing:

• - Upper/lower band margins

• - Buyer/seller volumes with moving averages

• - Delta and cumulative delta

• - Buyer/seller ratios per bar and across the window

• - Money flow values (buy/sell/delta × price) for bar-level and summed periods

• The table is neutral-colored and resizable for different chart layouts.

◉ Zone Event Gate

• Tracks entry into and exit from “near band” zones.

• Arming logic: a side is armed when price enters a band proximity zone.

• Trigger logic: on exit, a trade event is generated if cumulative buyer or seller volume dominates over a configurable window.

◉ Trading Logic

• Orders are placed only on zone-exit events, conditional on volume dominance.

• Position sizing is defined as a fixed percentage of strategy equity.

• Long entries occur when leaving the lower zone with buyer dominance; short entries occur when leaving the upper zone with seller dominance.

◉ Exit Rules

• Open positions are managed by a strict priority sequence:

• 1. Stop-loss (% of entry price)

• 2. Take-profit (% of entry price)

• 3. Opposite-side event (zone exit with dominance in the other direction)

• Stop-loss and take-profit levels are configurable

◉ Notes

• This lite version is intended to demonstrate the interaction of Bollinger Bands and volume-based dominance logic.

• It provides a framework to observe how price reacts at band boundaries under varying buy/sell pressure, and how zone exits can be systematically converted into entry/exit signals.

When configuring this strategy, it is essential to carefully review the settings within the Strategy Tester. Ensure that the chosen parameters and historical data options are correctly aligned with the intended use. Accurate back testing depends on applying proper configurations for historical reference. The figure below illustrates sample result and configuration type.

Gann Fan Strategy [KedarArc Quant]Description

A single-concept, rule-based strategy that trades around a programmatic Gann Fan.

It anchors to a swing (or a manual point), builds 1×1 and related fan lines numerically, and triggers entries when price interacts with the 1×1 (breakout or bounce). Management is done entirely with the fan structure (next/previous line) plus optional ATR trailing.

What TV indicators are used

* Pivots: `ta.pivothigh/ta.pivotlow` to confirm swing highs/lows for anchor selection.

* ATR: `ta.atr` only to scale the 1×1 slope (optional) and for an optional trailing stop.

* EMA: `ta.ema` as a trend filter (e.g., only long above the EMA, short below).

No RSI/MACD/Stoch/Heikin/etc. The logic is one coherent framework: Gann price–time geometry, with ATR as a scale and EMA as a risk filter.

How it works

1. Anchor

* Auto: chooses the most recent *confirmed* pivot (you control Left/Right).

* Manual: set a price and bar index and the fan will hold that point (no re-anchoring).

* Optional Re-anchor when a newer pivot confirms.

2. 1×1 Slope (numeric, not cosmetic)

* ATR mode: `1×1 = ATR(Length) × Multiplier` (adapts to volatility).

* Fixed mode: `ticks per bar` (constant slope).

Because slope is numeric, it doesn’t change with chart zoom, unlike the drawing tool.

3. Fan Lines

Builds classic ratios around the 1×1: 1/8, 1/4, 1/3, 1/2, 1/1, 2/1, 3/1, 4/1, 8/1.

4. Signals

* Breakout: cross of price over/under the 1×1 in the EMA-aligned direction.

* Bounce (optional): touch + reversal across the 1×1 to reduce whipsaw.

5. Exits & Risk

* Take-profit at the next fan line; Stop at the previous fan line.

* If a level is missing (right after re-anchor), a fallback Risk-Reward (RR) is used.

* Optional ATR trailing stop.

Why this is unique

* True numeric fan: The 1×1 slope is calculated from ATR or fixed ticks—not from screen geometry—so it is scale-invariant and reproducible across users/timeframes.

* Deterministic anchor logic: Uses confirmed pivots (with your L/R settings). No look-ahead; anchors update only when the right bars complete.

* Fan-native trade management: Both entries and exits come from the fan structure itself (with a minimal ATR/EMA assist), keeping the method pure.

* Two entry archetypes: Breakout for momentum days; Bounce for range days—switchable without changing the core model.

* Manual mode: Lock a session’s bias by anchoring to a chosen swing (e.g., day’s first major low/high) and keep the fan constant all day.

Inputs (quick guide)

* Auto Anchor (Left/Right): pivot sensitivity. Higher values = fewer, stronger anchors.

* Re-anchor: refresh to newer pivots as they confirm.

* Manual Anchor Price / Bar Index: fixes the fan (turn Auto off).

* Scale 1×1 by ATR: on = adaptive; off = use ticks per bar.

* ATR Length / ATR Multiplier: controls adaptive slope; start around 14 / 0.25–0.35.

* Ticks per bar: exact fixed slope (match a hand-drawn fan by computing slope ÷ mintick).

* EMA Trend Filter: e.g., 50–100; trades only in EMA direction.

* Use Bounce: require touch + reverse across 1×1 (helps in chop).

* TP/SL at fan lines; Fallback RR for missing levels; ATR Trailing Stop optional.

* Transparency/Plot EMA: visual preferences.

Tips

* Range days: larger pivots (L/R 8–12), Bounce ON, ATR Multiplier \~0.30–0.40, EMA 100.

* Trend days: L/R 5–6, Breakout, Multiplier \~0.20–0.30, EMA 50, ATR trail 1.0–1.5.

* Match the TV Gann Fan drawing: turn ATR scale OFF, set ticks per bar = `(Δprice between anchor and 1×1 target) / (bars) / mintick`.

Repainting & testing notes

* Pivots require Right bars to confirm; anchors are set after confirmation (no look-ahead).

* Signals use the current bar close with TradingView strategy mechanics; real-time vs. bar-close can differ slightly, as with any strategy.

* Re-anchoring legitimately moves the structure when new pivots confirm—by design.

⚠️ Disclaimer

This script is provided for educational purposes only.

Past performance does not guarantee future results.

Trading involves risk, and users should exercise caution and use proper risk management when applying this strategy.

Liquidity Sweep Breakout - LSBLiquidity Sweep Breakout - LSB

A professional session-based breakout system designed for OANDA:USDJPY and other JPY pairs.

Not guesswork, but precision - built on detailed observation of institutional moves to capture clear trade direction daily.

Master the Market’s Daily Bank Flow.

---

Strategy Detail:

I discovered this strategy after carefully studying how Japanese banks influence the forex market during their daily settlement period. Banks are some of the biggest players in the financial world, and when they adjust or settle their accounts in the morning, it often creates a push in the market. From years of observation, I noticed a consistent pattern, once banks finish their settlements, the market usually continues moving in the same direction that was formed right after those actions. This daily banking flow often sets the tone for the entire trading session, especially for JPY pairs like USDJPY.

To capture this move, I built the indicator so that it follows the bank-driven trend with clear rules for entries, stop-loss (SL), and take-profit (TP). The system is designed with professional risk management in mind. By default, it assumes a $10,000 account size, risks only 1% of that balance per trade, and targets a 1:1.5 reward-to-risk ratio. This means for every $100 risked, the potential profit is $150. Such controlled risk makes the system safer and more sustainable for long-term traders. At the same time, users are not limited to this setup, they can adjust the account balance in the settings, and the indicator will automatically recalculate the lot size and risk levels based on their own capital. This ensures the strategy works for small accounts and larger accounts alike.

🌍 Why It Works

Fundamentally driven: Based on **daily Japanese banking settlement flows**.

Session-specific precision: Targets the exact window when USDJPY liquidity reshapes.

Risk-managed: Always calculates lot size based on account and risk preferences.

Automatable: With webhook + MT5 EA, it can be fully hands-free.

---

✅ Recommended

Pair: USDJPY (best observed behavior).

Timeframe: 3-Minute chart.

Platform: TradingView Premium (for webhooks).

Execution: MT5 via EA.

---

🔎 Strategy Concept

The Tokyo Magic Breakout (TMB) is built on years of session observation and the unique daily rhythm of the Japanese banking system.

Every morning between 5:50 AM – 6:10 AM PKT (09:50 – 10:10 JST), Japanese banks perform daily reconciliation and settlement. This often sets the tone for the USDJPY direction of the day.

This strategy isolates that critical moment of liquidity adjustment and waits for a clean breakout confirmation. Instead of chasing noise, it executes only when price action is aligned with the Tokyo market’s hidden flows.

---

🕒 Timing Logic

Session Start: 5:00 AM PKT (Tokyo market open range).

Magic Candle: The 5:54 AM PKT candle is marked as the reference “breakout selector.”

Checkpoints: First confirmation at 6:30 AM PKT, then every 15 minutes until 8:30 AM PKT.

* If price stays inside the magic range → wait.

* If a breakout happens but the candle wick touches the range → wait for the next checkpoint.

* If by 8:30 AM PKT no clean breakout occurs → the day is marked as No Trade Day (NTD).

👉 Recommended timeframe: 3-Minute chart (3M) for precise signals.

---

📈 Trade Execution

Entry: Clean break above/below the magic candle’s range.

Stop-Loss: Opposite side of the Tokyo session high/low.

Take-Profit: Calculated by Reward\:Risk ratio (default 1.5:1).

Lot Size: Auto-calculated based on your risk model:

* Fixed Dollar

* % of Equity

* Conservative (minimum of both).

Visuals include:

✅ Entry/SL/TP lines

✅ Shaded risk (red) and reward (green) zones

✅ Trade labels (Buy/Sell with lot size & levels)

✅ TP/SL hit markers

---

🔔 Alerts & Automation (AutoTMB)

This strategy is fully automation-ready with EA + MT5:

1. Enable alerts in TMB settings.

2. Insert your PineConnector License Key.

3. Configure your risk management preferences.

4. Create a TradingView alert → in the message box simply type:

Pine Script®

{{alert_message}}

and set the EA webhook.

Now, every breakout trade (with exact entry, SL, TP, and lot size) is sent instantly.

👉 On your MT5:

* Install the EA.

* Use the same license key.

* Run it on a VPS or local MT5 terminal.

You now have a hands-free trading system: AutoTMB.

Nifty Power -> Nifty 50 chart + EMA of RSI + avg volume strategyThis strategy works in 1 hour candle in Nifty 50 chart. In this strategy, upward trade takes place when there is a crossover of RSI 15 on EMA50 of RSI 15 and volume is greater than volume based EMA21. On the other hand, lower trade takes place when RSI 15 is less than EMA50 of RSI 15. Please note that there is no stop loss given and also that the trade will reverse as per the trend. Sometimes on somedays, there will be no trades. Also please note that this is an Intraday strategy. The trade if taken closes on 15:15 in Nifty 50. This strategy can be used for swing trading. Some pine script code such as supertrend and ema21 of close is redundant. Try not to get confused as only EMA50 of RSI 15 is used and EMA21 of volume is used. I am using built-in pinescript indicators and there is no special calculation done in the pine script code. I have taken numbars variable to count number of candles. For example, if you have 30 minuite chart then numbars variable will count the intraday candles accordingly and the same for 1 hour candles.

SwingTrade ADX Strategy v6This is a swing trading strategy that combines VWAP (Volume Weighted Average Price), ADX (Average Directional Index) for trend strength, and volume ratios to generate long/short entry and exit signals. It's designed for daily charts but can be adapted.

#### Key Features:

- **Entries**: Based on VWAP crossovers, rising/falling delta (price deviation from VWAP), ADX trend confirmation, and volume ratios.

- **Exits**: Dynamic exits when VWAP delta reverses after a peak.

- **Filters**: Optional toggles for VWAP signals, ADX, and volume. Backtest date range for custom periods.

- **Visuals**: VWAP line, signal shapes/labels, and an info panel showing key metrics (VWAP Delta %, ADX, Volume Ratio).

- **Alerts**: Built-in alerts for buy/sell entries and exits.

#### How to Use:

1. Apply to your chart (e.g., stocks, forex, crypto).

2. Adjust parameters in the settings (e.g., ADX threshold, volume period).

3. Enable/disable indicators as needed.

4. Backtest using the date filters and review equity curve.

**Disclaimer**: This is for educational purposes only. Past performance is not indicative of future results. Not financial advice—trade at your own risk. Backtest thoroughly and use with proper risk management.

Feedback welcome! If you find it useful, give it a like.

SOXL Trend Surge v3.0.2 – Profit-Only RunnerSOXL Trend Surge v3.0.2 – Profit-Only Runner

This is a trend-following strategy built for leveraged ETFs like SOXL, designed to ride high-momentum waves with minimal interference. Unlike most short-term scalping scripts, this model allows trades to develop over multiple days to even several months, capitalizing on the full power of extended directional moves — all without using a stop-loss.

🔍 How It Works

Entry Logic:

Price is above the 200 EMA (long-term trend confirmation)

Supertrend is bullish (momentum confirmation)

ATR is rising (volatility expansion)

Volume is above its 20-bar average (liquidity filter)

Price is outside a small buffer zone from the 200 EMA (to avoid whipsaws)

Trades are restricted to market hours only (9 AM to 2 PM EST)

Cooldown of 15 bars after each exit to prevent overtrading

Exit Strategy:

Takes partial profit at +2× ATR if held for at least 2 bars

Rides the remaining position with a trailing stop at 1.5× ATR

No hard stop-loss — giving space for volatile pullbacks

⚙️ Strategy Settings

Initial Capital: $500

Risk per Trade: 100% of equity (fully allocated per entry)

Commission: 0.1%

Slippage: 1 tick

Recalculate after order is filled

Fill orders on bar close

Timeframe Optimized For: 45-minute chart

These parameters simulate an aggressive, high-volatility trading model meant for forward-testing compounding potential under realistic trading costs.

✅ What Makes This Unique

No stop-loss = fewer premature exits

Partial profit-taking helps lock in early wins

Trailing logic gives room to ride large multi-week moves

Uses strict filters (volume, ATR, EMA bias) to enter only during high-probability windows

Ideal for leveraged ETF swing or position traders looking to hold longer than the typical intraday or 2–3 day strategies

⚠️ Important Note

This is a high-risk, high-reward strategy meant for educational and testing purposes. Without a stop-loss, trades can experience deep drawdowns that may take weeks or even months to recover. Always test thoroughly and adjust position sizing to suit your risk tolerance. Past results do not guarantee future returns. Backtest range: May 8, 2020 – May 23, 2025

Multi-Indicator Swing [TIAMATCRYPTO]v6# Strategy Description:

## Multi-Indicator Swing

This strategy is designed for swing trading across various markets by combining multiple technical indicators to identify high-probability trading opportunities. The system focuses on trend strength confirmation and volume analysis to generate precise entry and exit signals.

### Core Components:

- **Supertrend Indicator**: Acts as the primary trend direction filter with optimized settings (Factor: 3.0, ATR Period: 10) to balance responsiveness and reliability.

- **ADX (Average Directional Index)**: Confirms the strength of the prevailing trend, filtering out sideways or choppy market conditions where the strategy avoids taking positions.

- **Liquidity Delta**: A volume-based indicator that analyzes buying and selling pressure imbalances to validate trend direction and potential reversals.

- **PSAR (Optional)**: Can be enabled to add additional confirmation for trend changes, turned off by default to reduce signal filtering.

### Key Features:

- **Flexible Direction Trading**: Choose between long-only, short-only, or bidirectional trading to adapt to market conditions or account restrictions.

- **Conservative Risk Management**: Implements fixed percentage-based stop losses (default 2%) and take profits (default 4%) for a positive risk-reward ratio.

- **Realistic Backtesting Parameters**: Includes commission (0.1%) and slippage (2 points) to reflect real-world trading conditions.

- **Visual Signals**: Clear buy/sell arrows with customizable sizes for easy identification on the chart.

- **Information Panel**: Dynamic display showing active indicators and current risk settings.

### Best Used On:

Daily timeframes for cryptocurrencies, forex, or stock indices. The strategy performs optimally on assets with clear trending behavior and sufficient volatility.

### Default Settings:

Optimized for conservative position sizing (5% of equity per trade) with an initial capital of $10,000. The backtesting period (2021-2023) provides a statistically significant sample of varied market conditions.

PEAD strategy█ OVERVIEW

This strategy trades the classic post-earnings announcement drift (PEAD).

It goes long only when the market gaps up after a positive EPS surprise.

█ LOGIC

1 — Earnings filter — EPS surprise > epsSprThresh %

2 — Gap filter — first regular 5-minute bar gaps ≥ gapThresh % above yesterday’s close

3 — Timing — only the first qualifying gap within one trading day of the earnings bar

4 — Momentum filter — last perfDays trading-day performance is positive

5 — Risk management

• Fixed stop-loss: stopPct % below entry

• Trailing exit: price < Daily EMA( emaLen )

█ INPUTS

• Gap up threshold (%) — 1 (gap size for entry)

• EPS surprise threshold (%) — 5 (min positive surprise)

• Past price performance — 20 (look-back bars for trend check)

• Fixed stop-loss (%) — 8 (hard stop distance)

• Daily EMA length — 30 (trailing exit length)

Note — Back-tests fill on the second 5-minute bar (Pine limitation).

Live trading: enable calc_on_every_tick=true for first-tick entries.

────────────────────────────────────────────

█ 概要(日本語)

本ストラテジーは決算後の PEAD を狙い、

EPS サプライズがプラス かつ 寄付きギャップアップ が発生した銘柄をスイングで買い持ちします。

█ ロジック

1 — 決算フィルター — EPS サプライズ > epsSprThresh %

2 — ギャップフィルター — レギュラー時間最初の 5 分足が前日終値+ gapThresh %以上

3 — タイミング — 決算当日または翌営業日の最初のギャップのみエントリー

4 — モメンタムフィルター — 過去 perfDays 営業日の騰落率がプラス

5 — リスク管理

• 固定ストップ:エントリー − stopPct %

• 利確:終値が日足 EMA( emaLen ) を下抜け

█ 入力パラメータ

• Gap up threshold (%) — 1 (ギャップ条件)

• EPS surprise threshold (%) — 5 (EPS サプライズ最小値)

• Past price performance — 20 (パフォーマンス判定日数)

• Fixed stop-loss (%) — 8 (固定ストップ幅)

• Daily EMA length — 30 (利確用 EMA 期間)

注意 — Pine の仕様上、バックテストでは寄付き 5 分足の次バーで約定します。

実運用で寄付き成行に合わせたい場合は calc_on_every_tick=true を有効にしてください。

────

ご意見や質問があればお気軽にコメントください。

Happy trading!

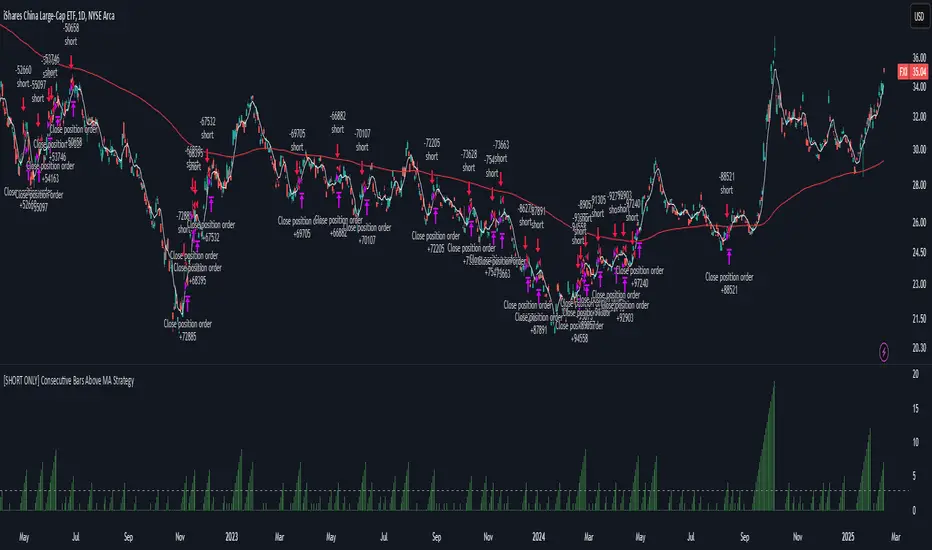

[SHORT ONLY] Consecutive Bars Above MA Strategy█ STRATEGY DESCRIPTION

The "Consecutive Bars Above MA Strategy" is a contrarian trading system aimed at exploiting overextended bullish moves in stocks and ETFs. It monitors the number of consecutive bars that close above a chosen short-term moving average (which can be either a Simple Moving Average or an Exponential Moving Average). Once the count reaches a preset threshold and the current bar’s close exceeds the previous bar’s high within a designated trading window, a short entry is initiated. An optional EMA filter further refines entries by requiring that the current close is below the 200-period EMA, helping to ensure that trades are taken in a bearish environment.

█ HOW ARE THE CONSECUTIVE BULLISH COUNTS CALCULATED?

The strategy utilizes a counter variable, `bullCount`, to track consecutive bullish bars based on their relation to the short-term moving average. Here’s how the count is determined:

Initialize the Counter

The counter is initialized at the start:

var int bullCount = na

Bullish Bar Detection

For each bar, if the close is above the selected moving average (either SMA or EMA, based on user input), the counter is incremented:

bullCount := close > signalMa ? (na(bullCount) ? 1 : bullCount + 1) : 0

Reset on Non-Bullish Condition

If the close does not exceed the moving average, the counter resets to zero, indicating a break in the consecutive bullish streak.

█ SIGNAL GENERATION

1. SHORT ENTRY

A short signal is generated when:

The number of consecutive bullish bars (i.e., bars closing above the short-term MA) meets or exceeds the defined threshold (default: 3).

The current bar’s close is higher than the previous bar’s high.

The signal occurs within the specified trading window (between Start Time and End Time).

Additionally, if the EMA filter is enabled, the entry is only executed when the current close is below the 200-period EMA.

2. EXIT CONDITION

An exit signal is triggered when the current close falls below the previous bar’s low, prompting the strategy to close the short position.

█ ADDITIONAL SETTINGS

Threshold: The number of consecutive bullish bars required to trigger a short entry (default is 3).

Trading Window: The Start Time and End Time inputs define when the strategy is active.

Moving Average Settings: Choose between SMA and EMA, and set the MA length (default is 5), which is used to assess each bar’s bullish condition.

EMA Filter (Optional): When enabled, this filter requires that the current close is below the 200-period EMA, supporting entries in a downtrend.

█ PERFORMANCE OVERVIEW

This strategy is designed for stocks and ETFs and can be applied across various timeframes.

It seeks to capture mean reversion by shorting after a series of bullish bars suggests an overextended move.

The approach employs a contrarian short entry by waiting for a breakout (close > previous high) following consecutive bullish bars.

The adjustable moving average settings and optional EMA filter allow for further optimization based on market conditions.

Comprehensive backtesting is recommended to fine-tune the threshold, moving average parameters, and filter settings for optimal performance.

Bearish Wick Reversal█ STRATEGY OVERVIEW

The "Bearish Wick Reversal Strategy" identifies potential bullish reversals following significant bearish price rejection (long lower wicks). This counter-trend approach enters long positions when bearish candles show exaggerated downside wicks relative to closing prices, then exits on bullish confirmation signals. Includes optional EMA trend filtering for improved reliability.

█ What is a Bearish Wick?

A price rejection pattern where:

Bearish candle (close < open) forms with extended lower wick

Wick represents failed selloff: Low drops significantly below close

Measured as: (Low - Close)/Close × 100 (Negative percentage indicates downward extension)

█ SIGNAL GENERATION

1. LONG ENTRY CONDITION

Bearish candle forms with close < open

Lower wick exceeds user-defined threshold (Default: -1% of close price)

The signal occurs within the specified time window

If enabled, the close price must also be above the 200-period EMA (Exponential Moving Average)

2. EXIT CONDITION

A Sell Signal is generated when the current closing price exceeds the highest high of the previous seven bars (`close > _highest `). This indicates that the price has shown strength, potentially confirming the reversal and prompting the strategy to exit the position.

█ PERFORMANCE OVERVIEW

Ideal Market: Volatile instruments with frequent price rejections

Key Risk: False signals in sustained bearish trends

Optimization Tip: Test various thresholds

Filter Impact: EMA reduces trades but improves win rate and reduces drawdown

Gap Down Reversal Strategy█ STRATEGY OVERVIEW

The "Gap Down Reversal Strategy" capitalizes on price recovery patterns following bearish gap-down openings. This mean-reversion approach enters long positions on confirmed intraday recoveries and exits when prices breach previous session highs. This strategy is NOT optimized.

█ What is a Gap Down Reversal?

A gap down reversal occurs when:

An instrument opens significantly below its prior session's low (price gap)

Selling pressure exhausts itself during the session

Buyers regain control, pushing price back above the opening level

Creates a candlestick with:

• Open < Prior Session Low (true gap)

• Close > Open (bullish reversal candle)

█ SIGNAL GENERATION

1. LONG ENTRY CONDITION

Previous candle closes BELOW its opening price (bearish candle)

Current session opens BELOW prior candle's low (gap down)

Current candle closes ABOVE its opening price (bullish reversal)

Executes market order at session close

2. EXIT CONDITION

A Sell Signal is generated when the current closing price exceeds the highest high of the previous seven bars (`close > _highest `). This indicates that the price has shown strength, potentially confirming the reversal and prompting the strategy to exit the position.

█ PERFORMANCE OVERVIEW

Ideal Market: High volatility instruments with frequent gaps

Key Risk: False reversals in sustained downtrends

Optimization Tip: Test varying gap thresholds (1-3% ranges)

SPY/TLT Strategy█ STRATEGY OVERVIEW

The "SPY/TLT Strategy" is a trend-following crossover strategy designed to trade the relationship between TLT and its Simple Moving Average (SMA). The default configuration uses TLT (iShares 20+ Year Treasury Bond ETF) with a 20-period SMA, entering long positions on bullish crossovers and exiting on bearish crossunders. **This strategy is NOT optimized and performs best in trending markets.**

█ KEY FEATURES

SMA Crossover System: Uses price/SMA relationship for signal generation (Default: 20-period)

Dynamic Time Window: Configurable backtesting period (Default: 2014-2099)

Equity-Based Position Sizing: Default 100% equity allocation per trade

Real-Time Visual Feedback: Price/SMA plot with trend-state background coloring

Event-Driven Execution: Processes orders at bar close for accurate backtesting

█ SIGNAL GENERATION

1. LONG ENTRY CONDITION

TLT closing price crosses ABOVE SMA

Occurs within specified time window

Generates market order at next bar open

2. EXIT CONDITION

TLT closing price crosses BELOW SMA

Closes all open positions immediately

█ ADDITIONAL SETTINGS

SMA Period: Simple Moving Average length (Default: 20)

Start Time and End Time: The time window for trade execution (Default: 1 Jan 2014 - 1 Jan 2099)

Security Symbol: Ticker for analysis (Default: TLT)

█ PERFORMANCE OVERVIEW

Ideal Market Conditions: Strong trending environments

Potential Drawbacks: Whipsaws in range-bound markets

Backtesting results should be analyzed to optimize the MA Period and EMA Filter settings for specific instruments

3 Down, 3 Up Strategy█ STRATEGY DESCRIPTION

The "3 Down, 3 Up Strategy" is a mean-reversion strategy designed to capitalize on short-term price reversals. It enters a long position after consecutive bearish closes and exits after consecutive bullish closes. This strategy is NOT optimized and can be used on any timeframes.

█ WHAT ARE CONSECUTIVE DOWN/UP CLOSES?

- Consecutive Down Closes: A sequence of trading bars where each close is lower than the previous close.

- Consecutive Up Closes: A sequence of trading bars where each close is higher than the previous close.

█ SIGNAL GENERATION

1. LONG ENTRY

A Buy Signal is triggered when:

The price closes lower than the previous close for Consecutive Down Closes for Entry (default: 3) consecutive bars.

The signal occurs within the specified time window (between Start Time and End Time).

If enabled, the close price must also be above the 200-period EMA (Exponential Moving Average).

2. EXIT CONDITION

A Sell Signal is generated when the price closes higher than the previous close for Consecutive Up Closes for Exit (default: 3) consecutive bars.

█ ADDITIONAL SETTINGS

Consecutive Down Closes for Entry: Number of consecutive lower closes required to trigger a buy. Default = 3.

Consecutive Up Closes for Exit: Number of consecutive higher closes required to exit. Default = 3.

EMA Filter: Optional 200-period EMA filter to confirm long entries in bullish trends. Default = disabled.

Start Time and End Time: Restrict trading to specific dates (default: 2014-2099).

█ PERFORMANCE OVERVIEW

Designed for volatile markets with frequent short-term reversals.

Performs best when price oscillates between clear support/resistance levels.

The EMA filter improves reliability in trending markets but may reduce trade frequency.

Backtest to optimize consecutive close thresholds and EMA period for specific instruments.

Internal Bar Strength (IBS) Strategy█ STRATEGY DESCRIPTION

The "Internal Bar Strength (IBS) Strategy" is a mean-reversion strategy designed to identify trading opportunities based on the closing price's position within the daily price range. It enters a long position when the IBS indicates oversold conditions and exits when the IBS reaches overbought levels. This strategy was designed to be used on the daily timeframe.

█ WHAT IS INTERNAL BAR STRENGTH (IBS)?

Internal Bar Strength (IBS) measures where the closing price falls within the high-low range of a bar. It is calculated as:

IBS = (Close - Low) / (High - Low)

- **Low IBS (≤ 0.2)**: Indicates the close is near the bar's low, suggesting oversold conditions.

- **High IBS (≥ 0.8)**: Indicates the close is near the bar's high, suggesting overbought conditions.

█ SIGNAL GENERATION

1. LONG ENTRY

A Buy Signal is triggered when:

The IBS value drops below the Lower Threshold (default: 0.2).

The signal occurs within the specified time window (between `Start Time` and `End Time`).

2. EXIT CONDITION

A Sell Signal is generated when the IBS value rises to or above the Upper Threshold (default: 0.8). This prompts the strategy to exit the position.

█ ADDITIONAL SETTINGS

Upper Threshold: The IBS level at which the strategy exits trades. Default is 0.8.

Lower Threshold: The IBS level at which the strategy enters long positions. Default is 0.2.

Start Time and End Time: The time window during which the strategy is allowed to execute trades.

█ PERFORMANCE OVERVIEW

This strategy is designed for ranging markets and performs best when prices frequently revert to the mean.

It is sensitive to extreme IBS values, which help identify potential reversals.

Backtesting results should be analyzed to optimize the Upper/Lower Thresholds for specific instruments and market conditions.

Buy on 5 day low Strategy█ STRATEGY DESCRIPTION

The "Buy on 5 Day Low Strategy" is a mean-reversion strategy designed to identify potential buying opportunities when the price drops below the lowest low of the previous five days. It enters a long position when specific conditions are met and exits when the price exceeds the high of the previous day. This strategy is optimized for use on daily or higher timeframes.

█ WHAT IS THE 5-DAY LOW?

The 5-Day Low is the lowest price observed over the last five days. This level is used as a reference to identify potential oversold conditions and reversal points.

█ SIGNAL GENERATION

1. LONG ENTRY

A Buy Signal is triggered when:

The close price is below the lowest low of the previous five days (`close < _lowest `).

The signal occurs within the specified time window (between `Start Time` and `End Time`).

2. EXIT CONDITION

A Sell Signal is generated when the current closing price exceeds the high of the previous day (`close > high `). This indicates that the price has shown strength, potentially confirming the reversal and prompting the strategy to exit the position.

█ ADDITIONAL SETTINGS

Start Time and End Time: The time window during which the strategy is allowed to execute trades.

█ PERFORMANCE OVERVIEW

This strategy is designed for mean-reverting markets and performs best when the price frequently oscillates around key support levels.

It is sensitive to oversold conditions, as indicated by the 5-Day Low, and overbought conditions, as indicated by the previous day's high.

Backtesting results should be analyzed to optimize the strategy for specific instruments and market conditions.

3-Bar Low Strategy█ STRATEGY DESCRIPTION

The "3-Bar Low Strategy" is a mean-reversion strategy designed to identify potential buying opportunities when the price drops below the lowest low of the previous three bars. It enters a long position when specific conditions are met and exits when the price exceeds the highest high of the previous seven bars. This strategy is suitable for use on various timeframes.

█ WHAT IS THE 3-BAR LOW?

The 3-Bar Low is the lowest price observed over the last three bars. This level is used as a reference to identify potential oversold conditions and reversal points.

█ WHAT IS THE 7-BAR HIGH?

The 7-Bar High is the highest price observed over the last seven bars. This level is used as a reference to identify potential overbought conditions and exit points.

█ SIGNAL GENERATION

1. LONG ENTRY

A Buy Signal is triggered when:

The close price is below the lowest low of the previous three bars (`close < _lowest `).

The signal occurs within the specified time window (between `Start Time` and `End Time`).

If the EMA Filter is enabled, the close price must also be above the 200-period Exponential Moving Average (EMA).

2. EXIT CONDITION

A Sell Signal is generated when the current closing price exceeds the highest high of the previous seven bars (`close > _highest `). This indicates that the price has shown strength, potentially confirming the reversal and prompting the strategy to exit the position.

█ ADDITIONAL SETTINGS

MA Period: The lookback period for the 200-period EMA used in the EMA Filter. Default is 200.

Use EMA Filter: Enables or disables the EMA Filter for long entries. Default is disabled.

Start Time and End Time: The time window during which the strategy is allowed to execute trades.

█ PERFORMANCE OVERVIEW

This strategy is designed for mean-reverting markets and performs best when the price frequently oscillates around key support and resistance levels.

It is sensitive to oversold conditions, as indicated by the 3-Bar Low, and overbought conditions, as indicated by the 7-Bar High.

Backtesting results should be analyzed to optimize the MA Period and EMA Filter settings for specific instruments.

Bollinger Bands Reversal + IBS Strategy█ STRATEGY DESCRIPTION

The "Bollinger Bands Reversal Strategy" is a mean-reversion strategy designed to identify potential buying opportunities when the price deviates below the lower Bollinger Band and the Internal Bar Strength (IBS) indicates oversold conditions. It enters a long position when specific conditions are met and exits when the IBS indicates overbought conditions. This strategy is suitable for use on various timeframes.

█ WHAT ARE BOLLINGER BANDS?

Bollinger Bands consist of three lines:

- **Basis**: A Simple Moving Average (SMA) of the price over a specified period.

- **Upper Band**: The basis plus a multiple of the standard deviation of the price.

- **Lower Band**: The basis minus a multiple of the standard deviation of the price.

Bollinger Bands help identify periods of high volatility and potential reversal points.

█ WHAT IS INTERNAL BAR STRENGTH (IBS)?

Internal Bar Strength (IBS) is a measure of where the closing price is relative to the high and low of the bar. It is calculated as:

IBS = (Close - Low) / (High - Low)

A low IBS value (e.g., below 0.2) indicates that the close is near the low of the bar, suggesting oversold conditions. A high IBS value (e.g., above 0.8) indicates that the close is near the high of the bar, suggesting overbought conditions.

█ SIGNAL GENERATION

1. LONG ENTRY

A Buy Signal is triggered when:

The IBS value is below 0.2, indicating oversold conditions.

The close price is below the lower Bollinger Band.

The signal occurs within the specified time window (between `Start Time` and `End Time`).

2. EXIT CONDITION

A Sell Signal is generated when the IBS value exceeds 0.8, indicating overbought conditions. This prompts the strategy to exit the position.

█ ADDITIONAL SETTINGS

Length: The lookback period for calculating the Bollinger Bands. Default is 20.

Multiplier: The number of standard deviations used to calculate the upper and lower Bollinger Bands. Default is 2.0.

Start Time and End Time: The time window during which the strategy is allowed to execute trades.

█ PERFORMANCE OVERVIEW

This strategy is designed for mean-reverting markets and performs best when the price frequently deviates from the Bollinger Bands.

It is sensitive to oversold and overbought conditions, as indicated by the IBS, which helps to identify potential reversals.

Backtesting results should be analyzed to optimize the Length and Multiplier parameters for specific instruments.

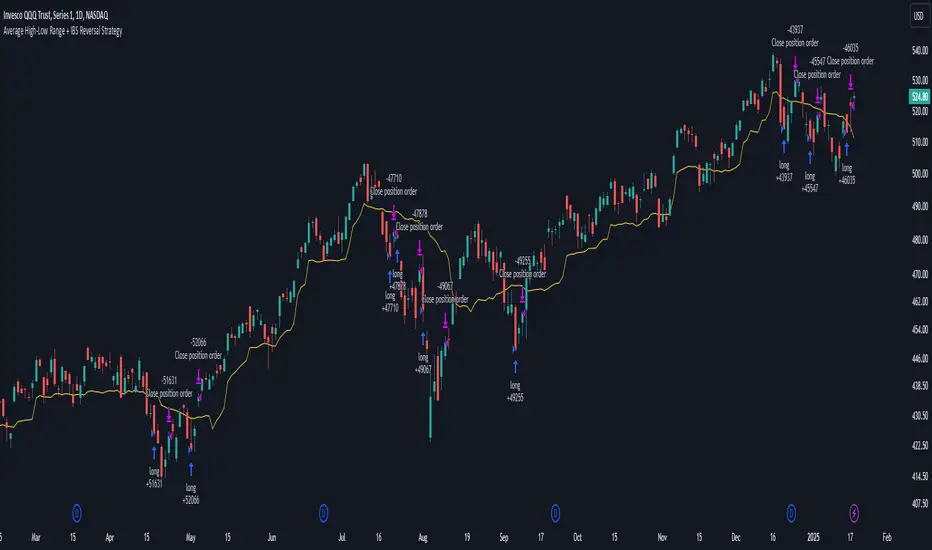

Average High-Low Range + IBS Reversal Strategy█ STRATEGY DESCRIPTION

The "Average High-Low Range + IBS Reversal Strategy" is a mean-reversion strategy designed to identify potential buying opportunities when the price deviates significantly from its average high-low range and the Internal Bar Strength (IBS) indicates oversold conditions. It enters a long position when specific conditions are met and exits when the price shows strength by exceeding the previous bar's high. This strategy is suitable for use on various timeframes.

█ WHAT IS THE AVERAGE HIGH-LOW RANGE?

The Average High-Low Range is calculated as the Simple Moving Average (SMA) of the difference between the high and low prices over a specified period. It helps identify periods of increased volatility and potential reversal points.

█ WHAT IS INTERNAL BAR STRENGTH (IBS)?

Internal Bar Strength (IBS) is a measure of where the closing price is relative to the high and low of the bar. It is calculated as:

IBS = (Close - Low) / (High - Low)

A low IBS value (e.g., below 0.2) indicates that the close is near the low of the bar, suggesting oversold conditions.

█ SIGNAL GENERATION

1. LONG ENTRY

A Buy Signal is triggered when:

The close price has been below the buy threshold (calculated as `upper - (2.5 * hl_avg)`) for a specified number of consecutive bars (`bars_below_threshold`).

The IBS value is below the specified buy threshold (`ibs_buy_treshold`).

The signal occurs within the specified time window (between `Start Time` and `End Time`).

2. EXIT CONDITION

A Sell Signal is generated when the current closing price exceeds the high of the previous bar (`close > high `). This indicates that the price has shown strength, potentially confirming the reversal and prompting the strategy to exit the position.

█ ADDITIONAL SETTINGS

Length: The lookback period for calculating the average high-low range. Default is 20.

Bars Below Threshold: The number of consecutive bars the price must remain below the buy threshold to trigger a Buy Signal. Default is 2.

IBS Buy Threshold: The IBS value below which a Buy Signal is triggered. Default is 0.2.

Start Time and End Time: The time window during which the strategy is allowed to execute trades.

█ PERFORMANCE OVERVIEW

This strategy is designed for mean-reverting markets and performs best when the price frequently deviates from its average high-low range.

It is sensitive to oversold conditions, as indicated by the IBS, which helps to identify potential reversals.

Backtesting results should be analyzed to optimize the Length, Bars Below Threshold, and IBS Buy Threshold parameters for specific instruments.

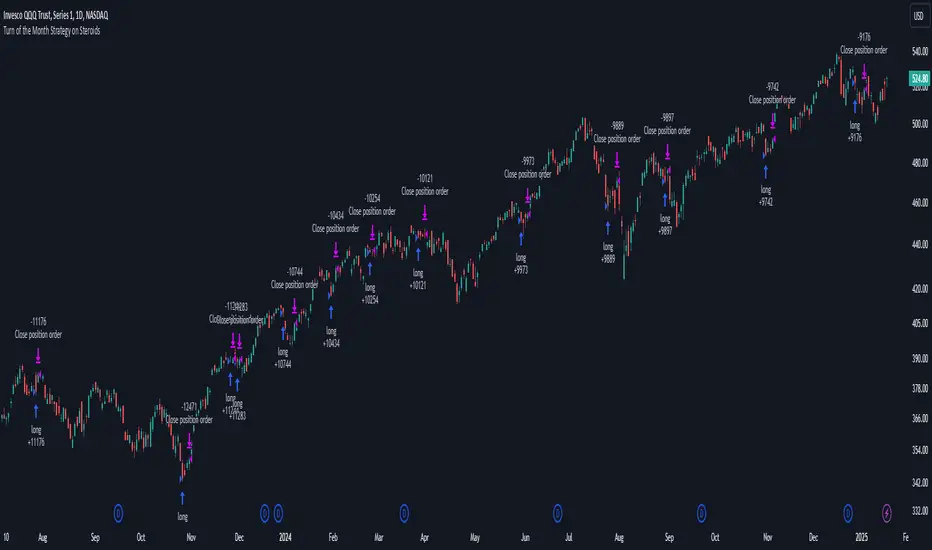

Turn of the Month Strategy on Steroids█ STRATEGY DESCRIPTION

The "Turn of the Month Strategy on Steroids" is a seasonal mean-reversion strategy designed to capitalize on price movements around the end of the month. It enters a long position when specific conditions are met and exits when the Relative Strength Index (RSI) indicates overbought conditions. This strategy is optimized for use on daily or higher timeframes.

█ WHAT IS THE TURN OF THE MONTH EFFECT?

The Turn of the Month effect refers to the observed tendency of stock prices to rise around the end of the month. This strategy leverages this phenomenon by entering long positions when the price shows signs of a reversal during this period.

█ SIGNAL GENERATION

1. LONG ENTRY

A Buy Signal is triggered when:

The current day of the month is greater than or equal to the specified `dayOfMonth` threshold (default is 25).

The close price is lower than the previous day's close (`close < close `).

The previous day's close is also lower than the close two days ago (`close < close `).

The signal occurs within the specified time window (between `Start Time` and `End Time`).

There is no existing open position (`strategy.position_size == 0`).

2. EXIT CONDITION

A Sell Signal is generated when the 2-period RSI exceeds 65, indicating overbought conditions. This prompts the strategy to exit the position.

█ ADDITIONAL SETTINGS

Day of Month: The day of the month threshold for triggering a Buy Signal. Default is 25.

Start Time and End Time: The time window during which the strategy is allowed to execute trades.

█ PERFORMANCE OVERVIEW

This strategy is designed to exploit seasonal price patterns around the end of the month.

It performs best in markets where the Turn of the Month effect is pronounced.

Backtesting results should be analyzed to optimize the `dayOfMonth` threshold and RSI parameters for specific instruments.

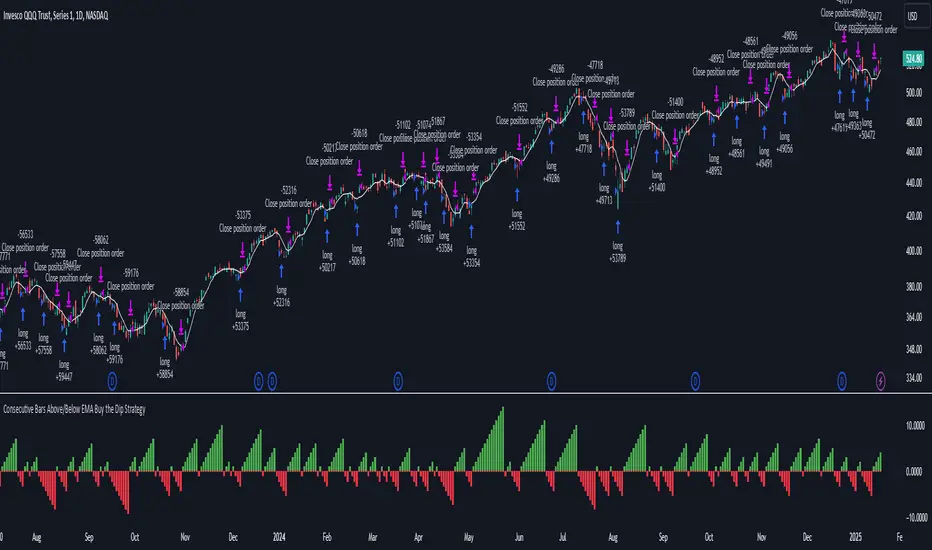

Consecutive Bars Above/Below EMA Buy the Dip Strategy█ STRATEGY DESCRIPTION

The "Consecutive Bars Above/Below EMA Buy the Dip Strategy" is a mean-reversion strategy designed to identify potential buying opportunities when the price dips below a moving average for a specified number of consecutive bars. It enters a long position when the dip condition is met and exits when the price shows strength by exceeding the previous bar's high. This strategy is suitable for use on various timeframes.

█ WHAT IS THE MOVING AVERAGE?

The strategy uses either a Simple Moving Average (SMA) or an Exponential Moving Average (EMA) as a reference for identifying dips. The type and length of the moving average can be customized in the settings.

█ SIGNAL GENERATION

1. LONG ENTRY

A Buy Signal is triggered when:

The close price is below the selected moving average for a specified number of consecutive bars (`consecutiveBarsTreshold`).

The signal occurs within the specified time window (between `Start Time` and `End Time`).

2. EXIT CONDITION

A Sell Signal is generated when the current closing price exceeds the high of the previous bar (`close > high `). This indicates that the price has shown strength, potentially confirming the reversal and prompting the strategy to exit the position.

█ ADDITIONAL SETTINGS

Consecutive Bars Threshold: The number of consecutive bars the price must remain below the moving average to trigger a Buy Signal. Default is 3.

MA Type: The type of moving average used (SMA or EMA). Default is SMA.

MA Length: The length of the moving average. Default is 5.

Start Time and End Time: The time window during which the strategy is allowed to execute trades.

█ PERFORMANCE OVERVIEW

This strategy is designed for mean-reverting markets and performs best when the price frequently oscillates around the moving average.

It is sensitive to the number of consecutive bars below the moving average, which helps to identify potential dips.

Backtesting results should be analysed to optimize the Consecutive Bars Threshold, MA Type, and MA Length for specific instruments.