Breaks and Retests - Free990Strategy Description: "Breaks and Retests - Free990"

The "Breaks and Retests - Free990" strategy is based on identifying breakout and retest opportunities for potential entries in both long and short trades. The idea is to detect price breakouts above resistance levels or below support levels, and subsequently identify retests that confirm the breakout levels. The strategy offers an automated approach to enter trades after a breakout followed by a retest, which serves as a confirmation of trend continuation.

Key Components:

Support and Resistance Detection:

The strategy calculates pivot levels based on historical price movements to define support and resistance areas. A lookback range is used to determine these key levels.

Breakouts and Retests:

The system identifies when a breakout occurs above a resistance level or below a support level.

It then waits for a retest of the previously broken level as confirmation, which is often a better entry opportunity.

Trade Direction Selection:

Users can choose between "Long Only," "Short Only," or "Both" directions for trading based on their market view.

Stop Loss and Trailing Stop:

An initial stop loss is placed at a defined percentage away from the entry.

The trailing stop loss is activated after the position gains a specified percentage in profit.

Long Entry:

A long entry is triggered if the price breaks above a resistance level and subsequently retests that level successfully.

The entry condition checks if the breakout was confirmed and if a retest was valid.

The long entry is only executed if the user-selected direction is either "Long Only" or "Both."

Short Entry:

A short entry is triggered if the price breaks below a support level and subsequently retests that level.

The short entry is only executed if the user-selected direction is either "Short Only" or "Both."

sell_condition checks whether the support has been broken and whether the retest condition is valid.

An initial stop loss is placed when the trade is opened to limit the risk if the trade moves against the position.

The stop loss is calculated based on a user-defined percentage (stop_loss_percent) of the entry price.

pinescript

Copy code

stop_loss_price := strategy.position_avg_price * (1 - stop_loss_percent / 100)

For long positions, the stop loss is placed below the entry price.

For short positions, the stop loss is placed above the entry price.

Trailing Stop:

When a position achieves a certain profit threshold (profit_threshold_percent), the trailing stop mechanism is activated.

For long positions, the trailing stop follows the highest price reached, ensuring that some profit is locked in if the price reverses.

For short positions, the trailing stop follows the lowest price reached.

Code Logic for Trailing Stop:

Exit Execution:

The strategy exits the position when the price hits the calculated stop loss level.

This includes both the initial stop loss and the trailing stop that adjusts as the trade progresses.

Code Logic for Exit:

Summary:

Breaks and Retests - Free990 uses support and resistance levels to identify breakouts, followed by retests for confirmation.

Entry Points: Triggered when a breakout is confirmed and a retest occurs, for both long and short trades.

Exit Points:

Initial Stop Loss: Limits risk for both long and short trades.

Trailing Stop Loss: Locks in profits as the price moves in favor of the position.

This strategy aims to capture the momentum after breakouts and minimize losses through effective use of stop loss and trailing stops. It gives the flexibility of selecting trade direction and ensures trades are taken with confirmation through the retest, which helps to reduce false breakouts.

Original Code by @HoanGhetti

스크립트에서 "stop loss"에 대해 찾기

Dual Strategy Selector V2 - CryptogyaniOverview:

This script provides traders with a dual-strategy system that they can toggle between using a simple dropdown menu in the input settings. It is designed to cater to different trading styles and needs, offering both simplicity and advanced filtering techniques. The strategies are built around moving average crossovers, enhanced by configurable risk management tools like take profit levels, trailing stops, and ATR-based stop-loss.

Key Features:

Two Strategies in One Script:

Strategy 1: A classic moving average crossover strategy for identifying entry signals based on trend reversals. Includes user-defined take profit and trailing stop-loss options for profit locking.

Strategy 2: An advanced trend-following system that incorporates:

A higher timeframe trend filter to confirm entry signals.

ATR-based stop-loss for dynamic risk management.

Configurable partial take profit to secure gains while letting the trade run.

Highly Customizable:

All key parameters such as SMA lengths, take profit levels, ATR multiplier, and timeframe for the trend filter are adjustable via the input settings.

Dynamic Toggle:

Traders can switch between Strategy 1 and Strategy 2 with a single dropdown, allowing them to adapt the strategy to market conditions.

How It Works:

Strategy 1:

Entry Logic: A long trade is triggered when the fast SMA crosses above the slow SMA.

Exit Logic: The trade exits at either a user-defined take profit level (percentage or pips) or via an optional trailing stop that dynamically adjusts based on price movement.

Strategy 2:

Entry Logic: Builds on the SMA crossover logic but adds a higher timeframe trend filter to align trades with the broader market direction.

Risk Management:

ATR-Based Stop-Loss: Protects against adverse moves with a volatility-adjusted stop-loss.

Partial Take Profit: Allows traders to secure a percentage of gains while keeping some exposure for extended trends.

How to Use:

Select Your Strategy:

Use the dropdown in the input settings to choose Strategy 1 or Strategy 2.

Configure Parameters:

Adjust SMA lengths, take profit, and risk management settings to align with your trading style.

For Strategy 2, specify the higher timeframe for trend filtering.

Deploy and Monitor:

Apply the script to your preferred asset and timeframe.

Use the backtest results to fine-tune settings for optimal performance.

Why Choose This Script?:

This script stands out due to its dual-strategy flexibility and enhanced features:

For beginners: Strategy 1 provides a simple yet effective trend-following system with minimal setup.

For advanced traders: Strategy 2 includes powerful tools like trend filters and ATR-based stop-loss, making it ideal for challenging market conditions.

By combining simplicity with advanced features, this script offers something for everyone while maintaining full transparency and user customization.

Default Settings:

Strategy 1:

Fast SMA: 21, Slow SMA: 49

Take Profit: 7% or 50 pips

Trailing Stop: Optional (disabled by default)

Strategy 2:

Fast SMA: 20, Slow SMA: 50

ATR Multiplier: 1.5

Partial Take Profit: 50%

Higher Timeframe: 1 Day (1D)

Crypto Volatility Bitcoin Correlation Strategy Description:

The Crypto Volatility Bitcoin Correlation Strategy is designed to leverage market volatility specifically in Bitcoin (BTC) using a combination of volatility indicators and trend-following techniques. This strategy utilizes the VIXFix (a volatility indicator adapted for crypto markets) and the BVOL7D (Bitcoin 7-Day Volatility Index from BitMEX) to identify periods of high volatility, while confirming trends with the Exponential Moving Average (EMA). These components work together to offer a comprehensive system that traders can use to enter positions when volatility and trends are aligned in their favor.

Key Features:

VIXFix (Volatility Index for Crypto Markets): This indicator measures the highest price of Bitcoin over a set period and compares it with the current low price to gauge market volatility. A rise in VIXFix indicates increasing market volatility, signaling that large price movements could occur.

BVOL7D (Bitcoin 7-Day Volatility Index): This volatility index, provided by BitMEX, measures the volatility of Bitcoin over the past 7 days. It helps traders monitor the recent volatility trend in the market, particularly useful when making short-term trading decisions.

Exponential Moving Average (EMA): The 50-period EMA acts as a trend indicator. When the price is above the EMA, it suggests the market is in an uptrend, and when the price is below the EMA, it suggests a downtrend.

How It Works:

Long Entry: A long position is triggered when both the VIXFix and BVOL7D indicators are rising, signaling increased volatility, and the price is above the 50-period EMA, confirming that the market is trending upward.

Exit: The strategy exits the position when the price crosses below the 50-period EMA, which signals a potential weakening of the uptrend and a decrease in volatility.

This strategy ensures that traders only enter positions when the volatility aligns with a clear trend, minimizing the risk of entering trades during periods of market uncertainty.

Testing and Timeframe:

This strategy has been tested on Bitcoin using the daily timeframe, which provides a longer-term perspective on market trends and volatility. However, users can adjust the timeframe according to their trading preferences. It is crucial to note that this strategy does not include comprehensive risk management, aside from the exit condition when the price crosses below the EMA. Users are strongly advised to implement their own risk management techniques, such as setting appropriate stop-loss levels, to safeguard their positions during high volatility periods.

Utility:

The Crypto Volatility Bitcoin Correlation Strategy is particularly well-suited for traders who aim to capitalize on the high volatility often seen in the Bitcoin market. By combining volatility measurements (VIXFix and BVOL7D) with a trend-following mechanism (EMA), this strategy helps identify optimal moments for entering and exiting trades. This approach ensures that traders participate in potentially profitable market moves while minimizing exposure during times of uncertainty.

Use Cases:

Volatility-Based Entries: Traders looking to take advantage of market volatility spikes will find this strategy useful for timing entry points during market swings.

Trend Confirmation: By using the EMA as a confirmation tool, traders can avoid entering trades that go against the trend, which can result in significant losses during volatile market conditions.

Risk Management: While the strategy exits when price falls below the EMA, it is important to recognize that this is not a full risk management system. Traders should use caution and integrate additional risk measures, such as stop-losses and position sizing, to better manage potential losses.

How to Use:

Step 1: Monitor the VIXFix and BVOL7D indicators. When both are rising and the Bitcoin price is above the EMA, the strategy will trigger a long entry, indicating that the market is experiencing increased volatility with a confirmed uptrend.

Step 2: Exit the position when the price drops below the 50-period EMA, signaling that the trend may be reversing or weakening, reducing the likelihood of continued upward price movement.

This strategy is open-source and is intended to help traders navigate volatile market conditions, particularly in Bitcoin, using proven indicators for volatility and trend confirmation.

Risk Disclaimer:

This strategy has been tested on the daily timeframe of Bitcoin, but users should be aware that it does not include built-in risk management except for the below-EMA exit condition. Users should be extremely cautious when using this strategy and are encouraged to implement their own risk management, such as using stop-losses, position sizing, and setting appropriate limits. Trading involves significant risk, and this strategy does not guarantee profits or prevent losses. Past performance is not indicative of future results. Always test any strategy in a demo environment before applying it to live markets.

Fractal Breakout Trend Following StrategyOverview

The Fractal Breakout Trend Following Strategy is a trend-following system which utilizes the Willams Fractals and Alligator to execute the long trades on the fractal's breakouts which have a high probability to be the new uptrend phase beginning. This system also uses the normalized Average True Range indicator to filter trades after a large moves, because it's more likely to see the trend continuation after a consolidation period. Strategy can execute only long trades.

Unique Features

Trend and volatility filtering system: Strategy uses Williams Alligator to filter the counter-trend fractals breakouts and normalized Average True Range to avoid the trades after large moves, when volatility is high

Configurable Trading Periods: Users can tailor the strategy to specific market windows, adapting to different market conditions.

Flexible Risk Management: Users can choose the stop-loss percent (by default = 3%) for trades, but strategy also has the dynamic stop-loss level using down fractals.

Methodology

The strategy places stop order at the last valid fractal breakout level. Validity of this fractal is defined by the Williams Alligator indicator. If at the moment of time when price breaking the last fractal price is higher than Alligator's teeth line (8 period SMA shifted 5 bars in the future) this is a valid breakout. Moreover strategy has the additional volatility filtering system using normalized ATR. It calculates the average normalized ATR for last user-defined number of bars and if this value lower than the user-defined threshold value the long trade is executed.

When trade is opened, script places the stop loss at the price higher of two levels: user defined stop-loss from the position entry price or down fractal validation level. The down fractal is valid with the rule, opposite as the up fractal validation. Price shall break to the downside the last down fractal below the Willians Alligator's teeth line.

Strategy has no fixed take profit. Exit level changes with the down fractal validation level. If price is in strong uptrend trade is going to be active until last down fractal is not valid. Strategy closes trade when price hits the down fractal validation level.

Risk Management

The strategy employs a combined approach to risk management:

It allows positions to ride the trend as long as the price continues to move favorably, aiming to capture significant price movements. It features a user-defined stop-loss parameter to mitigate risks based on individual risk tolerance. By default, this stop-loss is set to a 3% drop from the entry point, but it can be adjusted according to the trader's preferences.

Justification of Methodology

This strategy leverages Williams Fractals to open long trade when price has broken the key resistance level to the upside. This resistance level is the last up fractal and is shall be broken above the Williams Alligator's teeth line to be qualified as the valid breakout according to this strategy. The Alligator filtering increases the probability to avoid the false breakouts against the current trend.

Moreover strategy has an additional filter using Average True Range(ATR) indicator. If average value of ATR for the last user-defined number of bars is lower than user-defined threshold strategy can open the long trade according to open trade condition above. The logic here is following: we want to open trades after period of price consolidation inside the range because before and after a big move price is more likely to be in sideways, but we need a trend move to have a profit.

Another one important feature is how the exit condition is defined. On the one hand, strategy has the user-defined stop-loss (3% below the entry price by default). It's made to give users the opportunity to restrict their losses according to their risk-tolerance. On the other hand, strategy utilizes the dynamic exit level which is defined by down fractal activation. If we assume the breaking up fractal is the beginning of the uptrend, breaking down fractal can be the start of downtrend phase. We don't want to be in long trade if there is a high probability of reversal to the downside. This approach helps to not keep open trade if trend is not developing and hold it if price continues going up.

Backtest Results

Operating window: Date range of backtests is 2023.01.01 - 2024.05.01. It is chosen to let the strategy to close all opened positions.

Commission and Slippage: Includes a standard Binance commission of 0.1% and accounts for possible slippage over 5 ticks.

Initial capital: 10000 USDT

Percent of capital used in every trade: 30%

Maximum Single Position Loss: -3.19%

Maximum Single Profit: +24.97%

Net Profit: +3036.90 USDT (+30.37%)

Total Trades: 83 (28.92% win rate)

Profit Factor: 1.953

Maximum Accumulated Loss: 963.98 USDT (-8.29%)

Average Profit per Trade: 36.59 USDT (+1.12%)

Average Trade Duration: 72 hours

These results are obtained with realistic parameters representing trading conditions observed at major exchanges such as Binance and with realistic trading portfolio usage parameters.

How to Use

Add the script to favorites for easy access.

Apply to the desired timeframe and chart (optimal performance observed on 4h and higher time frames and the BTC/USDT).

Configure settings using the dropdown choice list in the built-in menu.

Set up alerts to automate strategy positions through web hook with the text: {{strategy.order.alert_message}}

Disclaimer:

Educational and informational tool reflecting Skyrex commitment to informed trading. Past performance does not guarantee future results. Test strategies in a simulated environment before live implementation

IsAlgo - Support & Resistance Strategy► Overview:

The Support & Resistance Strategy is designed to identify critical support and resistance levels and execute trades when the price crosses these levels. Utilizing a combination of a moving average, ATR indicator, and the highest and lowest prices, this strategy aims to accurately pinpoint entry and exit points for trades based on market movements.

► Description:

The Support & Resistance Strategy leverages the ATR (Average True Range) and a moving average to identify key support and resistance levels. The strategy calculates these levels by measuring the distance between the current market price and the moving average. This distance is continuously compared with each new candle to provide an estimate of the support and resistance levels.

The ATR is utilized to determine the width of these levels, ensuring they adjust to market volatility. To validate these levels, the strategy counts how often a candle’s low or high touches the estimated support or resistance and then bounces back. A higher frequency of such touches indicates a stronger, more reliable level.

Once the levels are confirmed, the strategy waits for a candle to close above the resistance level or below the support level. A candle closing above the resistance triggers a long entry, while a candle closing below the support triggers a short entry.

The strategy incorporates multiple stop-loss options to manage risk effectively. These options include setting stop-loss levels based on fixed pips, ATR calculations, or the highest/lowest prices of previous candles. Up to three take-profit levels can be set using fixed pips, ATR, or risk-to-reward ratios. A trailing stop feature adjusts the stop loss as the trade moves into profit, and a break-even feature moves the stop loss to the entry price once a certain profit level is reached.

Additionally, the strategy can close trades if the price crosses the opposite support or resistance level or if a candle moves significantly against the trade direction.

↑ Long Entry Example:

↓ Short Entry Example:

► Features & Settings:

⚙︎ Levels: Configure the length, width, and ATR period for support and resistance levels.

⚙︎ Moving Average: Use an Exponential Moving Average (EMA) to confirm trend direction. This can be enabled or disabled.

⚙︎ Entry Candle: Define the minimum and maximum body size and the body-to-candle size ratio for entry candles.

⚙︎ Trading Session: Specify the trading hours during which the strategy operates.

⚙︎ Trading Days: Select which days of the week the strategy is active.

⚙︎ Backtesting: Set a backtesting period with start and end dates. This feature can be deactivated.

⚙︎ Trades: Customize trade direction (long, short, or both), position sizing (fixed or percentage-based), maximum open trades, and daily trade limits.

⚙︎ Trades Exit: Choose from various exit methods, including profit/loss limits, trade duration, or crossing the opposite support/resistance level.

⚙︎ Stop Loss: Set stop-loss levels using fixed pips, ATR-based calculations, or the highest/lowest price within a specified number of previous candles.

⚙︎ Break Even: Adjust the stop loss to break-even once certain profit conditions are met.

⚙︎ Trailing Stop: Automatically adjust the stop loss as the trade moves into profit.

⚙︎ Take Profit: Define up to three take-profit levels using fixed pips, ATR, or risk-to-reward ratios based on the stop loss.

⚙︎ Alerts: Receive alerts for significant actions such as trade openings and closings, with support for dynamic values.

⚙︎ Dashboard: A visual display on the chart providing detailed information about ongoing and past trades.

► Backtesting Details:

Timeframe: 1-hour US30 chart

Initial Balance: $10,000

Order Size: 5 Units

Commission: $0.5 per contract

Slippage: 5 ticks

Stop Loss: Based on the opposite support/resistance level or break-even adjustments

Momentum Alligator 4h Bitcoin StrategyOverview

The Momentum Alligator 4h Bitcoin Strategy is a trend-following trading system that operates on dual time frames. It utilizes the 1D Williams Alligator indicator to identify the prevailing major price trend and seeks trading opportunities on the 4-hour (4h) time frame when the momentum is turning up. The strategy is designed to close trades if the trend fails to develop or holding position if price continues increasing without any significant correction. Note that this strategy is specifically tailored for the 4-hour time frame.

Unique Features

2-layers market noise filtering system: Trades are only initiated in the direction of the 1D trend, determined by the Williams Alligator indicator. This higher time frame confirmation filters out minor trade signals, focusing on more substantial opportunities. At the same time, strategy has additional filter on 4h time frame with Awesome Oscillator which is showing the current price momentum.

Flexible Risk Management: The strategy exclusively opens long positions, resulting in fewer trades during bear markets. It incorporates a dynamic stop-loss mechanism, which can either follow the jaw line of the 4h Alligator or a user-defined fixed stop-loss. This flexibility helps manage risk and avoid non-trending markets.

Methodology

The strategy initiates a long position when the d-line of Stochastic RSI crosses up it's k-line. It means that there is a high probability that price momentum reversed from down to up. To avoid overtrading in potentially choppy markets, it skips the next two trades following a winning trade, anticipating sideways movement after a significant price surge.

This strategy has two layers trades filtering system: 4h and 1D time frames. The first one is awesome oscillator. It shall be increasing and value has to be higher than it's 5-period SMA. This is an additional confirmation that long trade is opened in the direction of the current momentum. As it was mentioned above, all entry signals are validated against the 1D Williams Alligator indicator. A trade is only opened if the price is above all three lines of the 1D Alligator, ensuring alignment with the major trend.

A trade is closed if the price hits the 4h jaw line of the Alligator or reaches the user-defined stop-loss level.

Risk Management

The strategy employs a combined approach to risk management:

It allows positions to ride the trend as long as the price continues to move favorably, aiming to capture significant price movements. It features a user-defined stop-loss parameter to mitigate risks based on individual risk tolerance. By default, this stop-loss is set to a 2% drop from the entry point, but it can be adjusted according to the trader's preferences.

Justification of Methodology

This strategy leverages Stochastic RSI on 4h time frame to open long trade when momentum started reversing to the upside. On the one hand, Stochastic RSI is one of the most sensitive indicator, which allows to react fast on the potential trend reversal. On the other hand, this indicator can be too sensitive and provide a lot of false trend changing signals. To eliminate this weakness we use two-layers trades filtering system.

The first layer is the 4h Awesome oscillator. This is less sensitive momentum indicator. Usually it starts increasing when price has already passed significant distance from the actual reversal point. The strategy opens long trade only is Awesome oscillator is increasing and above it's 5-period SMA. This approach increases the probability to filter the false signals during the choppy market or if the reversal is false.

The second layer filter is the Williams Alligator indicator on 1D time frame. The 1D Alligator serves as a filter for identifying the primary trend and increases probability to avoid the trades with low potential because trading against major trend usually is more risky. It's much better to catch the trend continuation than local bounce.

Last but not least feature of this strategy is close trades condition. It uses the flexible approach. First of all, user can set up the fixed stop-loss according to his own risk-tolerance, by default this value is 2% of price movement. It restricts the potential loss at the moment when trade has just been opened. Moreover strategy utilizes the 4h Williams Alligator's jaw line to exit the trade. If price fell below it trade is closed. This approach helps to not keep open trade if trend is not developing and hold it if price continues going up.

Backtest Results:

Operating window: Date range of backtests is 2021.01.01 - 2024.05.01. It is chosen to let the strategy to close all opened positions.

Commission and Slippage: Includes a standard Binance commission of 0.1% and accounts for possible slippage over 5 ticks.

Initial capital: 10000 USDT

Percent of capital used in every trade: 50%

Maximum Single Position Loss: -3.04%

Maximum Single Profit: +29.67%

Net Profit: +6228.01 USDT (+62.28%)

Total Trades: 118 (24.58% win rate)

Profit Factor: 1.71

Maximum Accumulated Loss: 1527.69 USDT (-11.52%)

Average Profit per Trade: 52.78 USDT (+0.89%)

Average Trade Duration: 60 hours

These results are obtained with realistic parameters representing trading conditions observed at major exchanges such as Binance and with realistic trading portfolio usage parameters.

How to Use:

Add the script to favorites for easy access.

Apply to the 4h timeframe desired chart (optimal performance observed on the BTC/USDT).

Configure settings using the dropdown choice list in the built-in menu.

Set up alerts to automate strategy positions through web hook with the text: {{strategy.order.alert_message}}

Disclaimer:

Educational and informational tool reflecting Skyrex commitment to informed trading. Past performance does not guarantee future results. Test strategies in a simulated environment before live implementation

Range Average Retest Model [LuxAlgo]The Range Average Retest Model tool highlights setups from the range average retest entry model, a model using the retest of the average between two opposite swing points as an entry.

This tool uses long-term volatility coupled with user-defined multipliers to filter out swing areas and set take profit and stop loss levels for all trades.

Key features include:

Draw up to 165 swing areas and their associated trades

Filter out swing areas using Pivot Length , Selection Mode and Threshold parameters

Filter out trades with Maximum Distance and Minimum Distance parameters

Enable or disable swing areas and select default colors

Enable or disable overlapping trades and change the default colors for Take Profit and Stop Loss zones

🔶 USAGE

The "Range Average Retest Model" is an entry model that enters a position when the price retests the average made between two swing points. Users can determine the period of the detected swing points from the "Pivot Length" setting.

The conditions for long or short trades, regardless of whether the swing area is bullish or bearish, are as follows:

Long positions: the current bar close is below the swing area average and the last bar close was above it.

Short positions: the current bar close is above the swing area average price and the last bar close was below it.

Each trade is displayed on the chart with a line connecting it to its swing area highlighting the range average, a green area for the take profit, and a red area for the stop loss.

Both the Take Profit and Stop Loss levels are calculated by applying your own multiplier in the settings panel to the long-term volatility measure, in this case, the average true range over the last 200 bars.

Trades will remain open until they reach either the Stop Loss or Take Profit price levels.

🔹 Filtering Swing Areas

The daily chart of the Nasdaq-100 futures (NQ) with pivot length 2 and bullish selection mode: it only detects bullish swing areas, but they are smaller and more numerous.

Traders can manipulate the behavior of the swing areas from the settings panel.

The Selection mode will filter areas by bias: it will detect bullish areas, bearish areas, or both.

The Threshold parameter is applied to the long-term volatility to filter out areas where the average prices are too close together; the higher the value, the greater the difference between the average prices must be.

🔹 Trades

3-minute chart of the Nasdaq-100 futures (NQ) with pivot length 5, bearish selection mode maximum distance 4, and stop loss 2: many trades detected with very asymmetric risk/reward.

The behavior of the trades is also manipulated from the settings panel.

The maximum and minimum distance parameters specify the number of bars a trade must be away from a swing area.

The Take Profit and Stop Loss parameters are applied to the long-term volatility to obtain their respective price levels.

🔹 Overlapping Trades

Same chart as before, but with overlapping trades: messy, right?

By default the tool does not show overlapping trades, this allows for a cleaner chart.

In the settings panel traders can enable overlapping mode, in which case the tool will show all available trades.

Traders must be aware that the chart can be very crowded.

🔶 SETTINGS

🔹 Swings

Pivot Length: How many bars are used to confirm a swing point. The larger this parameter is, the larger and fewer swing areas will be detected.

Selection Mode: Swing area detection mode, detect only bullish swings, only bearish swings, or both.

Threshold: Swing area comparator. This threshold is multiplied by a measure of volatility (average true range over the last 200 bars), for a new swing area to be detected it must have an average level that is sufficiently distant from the average level of any untouched swing area, this parameter controls that distance.

🔹 Trades

Maximum distance: Maximum distance allowed between a swing area and a trade.

Minimum distance: Minimum distance allowed between a swing area and a trade.

Take profit: The size of the take profit - this threshold is multiplied by a measure of volatility (the average true range over the last 200 bars).

Stop loss: The size of the stop-loss: this threshold is multiplied by a measure of volatility (the average true range over the last 200 bars).

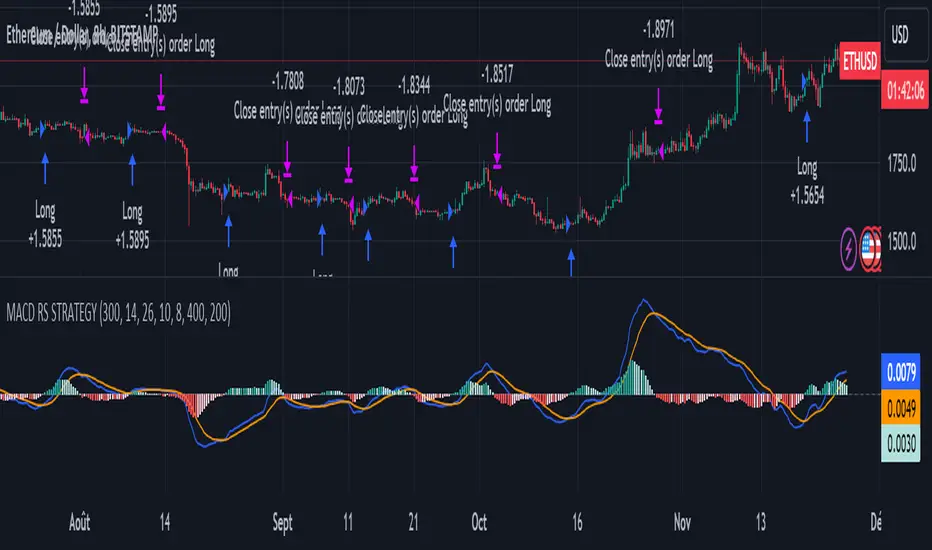

MACD of Relative Strenght StrategyMACD Relative Strenght Strategy :

INTRODUCTION :

This strategy is based on two well-known indicators: MACD and Relative Strenght (RS). By coupling them, we obtain powerful buy signals. In fact, the special feature of this strategy is that it creates an indicator from an indicator. Thus, we construct a MACD whose source is the value of the RS. The strategy only takes buy signals, ignoring SHORT signals as they are mostly losers. There's also a money management method enabling us to reinvest part of the profits or reduce the size of orders in the event of substantial losses.

RELATIVE STRENGHT :

RS is an indicator that measures the anomaly between momentum and the assumption of market efficiency. It is used by professionals and is one of the most robust indicators. The idea is to own assets that do better than average, based on their past performance. We calculate RS using this formula :

RS = close/highest_high(RS_Length)

Where highest_high(RS_Length) = highest value of the high over a user-defined time period (which is the RS_Length).

We can thus situate the current price in relation to its highest price over this user-defined period.

MACD (Moving Average Convergence - Divergence) :

This is one of the best-known indicators, measuring the distance between two exponential moving averages : one fast and one slower. A wide distance indicates fast momentum and vice versa. We'll plot the value of this distance and call this line macdline. The MACD uses a third moving average with a lower period than the first two. This last moving average will give a signal when it crosses the macdline. It is therefore constructed using the values of the macdline as its source.

It's important to note that the first two MAs are constructed using RS values as their source. So we've just built an indicator of an indicator. This kind of method is very powerful because it is rarely used and brings value to the strategy.

PARAMETERS :

RS Length : Relative Strength length i.e. the number of candles back to find the highest high and compare the current price with this high. Default is 300.

MACD Fast Length : Relative Strength fast EMA length used to plot the MACD. Default is 14.

MACD Slow Length : Relative Strength slow EMA length used to plot the MACD. Default is 26.

MACD Signal Smoothing : Macdline SMA length used to plot the MACD. Default is 10.

Max risk per trade (in %) : The maximum loss a trade can incur (in percentage of the trade value). Default is 8%.

Fixed Ratio : This is the amount of gain or loss at which the order quantity is changed. Default is 400, meaning that for each $400 gain or loss, the order size is increased or decreased by a user-selected amount.

Increasing Order Amount : This is the amount to be added to or subtracted from orders when the fixed ratio is reached. The default is $200, which means that for every $400 gain, $200 is reinvested in the strategy. On the other hand, for every $400 loss, the order size is reduced by $200.

Initial capital : $1000

Fees : Interactive Broker fees apply to this strategy. They are set at 0.18% of the trade value.

Slippage : 3 ticks or $0.03 per trade. Corresponds to the latency time between the moment the signal is received and the moment the order is executed by the broker.

Important : A bot has been used to test the different parameters and determine which ones maximize return while limiting drawdown. This strategy is the most optimal on BITSTAMP:ETHUSD in 8h timeframe with the parameters set by default.

ENTER RULES :

The entry rules are very simple : we open a long position when the MACD value turns positive. You are therefore LONG when the MACD is green.

EXIT RULES :

We exit a position (whether losing or winning) when the MACD becomes negative, i.e. turns red.

RISK MANAGEMENT :

This strategy can incur losses, so it's important to manage our risks well. If the position is losing and has incurred a loss of -8%, our stop loss is activated to limit losses.

MONEY MANAGEMENT :

The fixed ratio method was used to manage our gains and losses. For each gain of an amount equal to the value of the fixed ratio, we increase the order size by a value defined by the user in the "Increasing order amount" parameter. Similarly, each time we lose an amount equal to the value of the fixed ratio, we decrease the order size by the same user-defined value. This strategy increases both performance and drawdown.

Enjoy the strategy and don't forget to take the trade :)

MFR RangeHello Traders!

You requested it for many months, we are finally making our proprietary Range available to all.

First of all, how should a trader consider a Range in general:

In trading, a "range" refers to a specific price interval or zone within which an asset's price moves or consolidates for a period of time. Ranges are characterized by relatively horizontal or sideways price movements, where the price oscillates between a defined upper and lower boundary. Traders often use ranges to identify potential trading opportunities, manage risk, and make trading decisions.

Here's how ranges are used in trading:

1. Range Identification:

Traders identify ranges by observing price charts and looking for periods where the price appears to be moving horizontally with clear upper and lower boundaries.

Common range patterns include rectangles, channels, and horizontal consolidations.

2. Range Trading Strategies:

Range trading strategies aim to profit from price movements within the established range. Traders typically use two main approaches within a range:

Buying near the range's lower boundary: Traders buy when the price approaches the lower end of the range, anticipating a bounce or reversal towards the upper boundary. This is often referred to as "buying support."

Selling near the range's upper boundary: Traders sell when the price approaches the upper end of the range, anticipating a pullback or reversal towards the lower boundary. This is known as "selling resistance."

3. Risk Management:

Stop-loss orders are crucial when trading ranges. Traders set stop-loss orders just outside the range's boundaries to limit potential losses if the price breaks out of the range unpredictably.

4. Range Breakouts:

Ranges do not last indefinitely, and eventually, the price may break out of the range, leading to a significant price movement.

Traders often look for breakout patterns and use breakout trading strategies to capitalize on the potential for a strong price movement after the range is broken.

5. Volatility Consideration:

Some traders may assess the volatility within the range. If the price oscillates within the range with high volatility, they may consider trading shorter timeframes for smaller, quicker profits.

Lower volatility may prompt longer-term traders to take positions within the range, expecting a slower, more controlled price movement.

6. Time Frame Analysis:

Traders may analyze the time frame in which the range has developed, in our case MFR range are based solely on the Daily timeframe.

7. Confirmation Indicators:

Traders often use technical indicators like Relative Strength Index (RSI), Moving Averages, or Bollinger Bands to confirm range trading signals and assess overbought or oversold conditions.

8. Range Boundaries as Support and Resistance:

Once a range is identified, its upper and lower boundaries can serve as key support and resistance levels even after the range is broken. Traders pay attention to these levels for future trading decisions.

9. Range Expansion:

Some traders look for signs of range expansion, where the price starts to break out or trend strongly. This can signal the end of a range-bound market and a transition to a trending market.

It's important to note that while range trading can be profitable, it requires careful analysis and risk management. Traders must be prepared for the possibility of a breakout that can result in significant losses if they are on the wrong side of the trade. Additionally, market conditions can change, and ranges can evolve into trends or other patterns, so traders need to adapt their strategies accordingly.

What is specific to MFR range?

This script calculates and plots a trading range on a daily timeframe based on historical price data. Based on Benoit Mandelbrot and Edgar E. Peters publications on Range, we run a set of calculations over a defined period. The script will define those to generate the "Range High" and "Range Low". These values are used to define the upper and lower bounds of the trading range.

In short, how could I use this script?

A trader could use the Range to find overbought or oversold points to enter a position. The Lower Range being the price to buy an asset and the Upper Range being the place to sell an asset. This is recommended to be implemented only when our other indication called Trend matches the strategy: buy when the trend is bullish or short when the trend is bearish.

It's important to note that while Range is a useful tool, it should not be relied upon solely for making trading decisions. It's recommended to use it in conjunction with other technical analysis tools and consider other factors such as market conditions, risk management, and fundamental analysis. Remember that the Range indicator is just one tool among many, and it's important to consider other factors such as volume, momentum, volatility, and overall market conditions when making trading decisions. Additionally, using stop-loss orders and proper risk management techniques is crucial to mitigate potential losses.

We hope that you will find these explanations useful, please contact us by private message for access.

Enjoy!

DISCLAIMER: No sharing, copying, reselling, modifying, or any other forms of use are authorised. This script is strictly for individual use and educational purposes only. This is not financial or investment advice. Investments are always made at your own risk and are based on your personal judgement. Myfractalrange is not responsible for any losses you may incur. Please invest wisely.

Myfractalrange TrendHello Traders!

This is our main addition to MFR TradingView account: Myfractalrange Trend.

Many Trend signals exist out there, each trader has at some point created its own.

At Myfractalrange, we have developed a proprietary formula based on Price, Volume and Volatility.

Before going into how subscribers can use the Trend script, let't have a look at the different data point provided one by one:

- Bullish Trend: If the price of the asset is above this value, the asset is considered to be Bullish Trend. Default colour is green

- Bearish Trend : If the price of the asset is below this value, the asset is considered to be Bearish Trend. Default colour is red

- Neutral Trend: If the price of the asset is between the value of the Bullish Trend and the value of the Bearish Trend, the asset is considered to be Neutral Trend. Default colour is yellow

How does the script work?

The provided script is proprietary, so while the specific calculations and data sources cannot be disclosed, here is a broad explanation on how it works:

- It will retrieve the relevant data from the asset, could be volume, close, high, low, etc.

- The script will then check the length for the trend calculation of this specific asset and compute the Trend line

- From the value of this Trend line, we will then generate the "bullish" and "bearish" values

- The script will then plot the Bullish and Bearish values on the chart, the area between both being set as the Neutral area

How to use trend when trading?

When trading, understanding and utilising trends can be valuable for making informed trading decisions. Here are some key ways to use trends in trading:

- Trend Identification: Identifying the presence and direction of a trend is crucial

- Trend Following: One common trading strategy is trend following, which involves trading in the direction of the prevailing trend. In an uptrend, traders may look for opportunities to buy or go long, while in a downtrend, they may seek opportunities to sell or go short. Trend following strategies assume that trends are more likely to continue than reverse, and traders aim to capitalise on sustained price movements

- Trend Reversals: Identifying potential trend reversals is another approach. Traders may look for signs that a trend is losing momentum or showing signs of exhaustion. Traders may then consider taking contrarian positions or closing existing trades.

- Timing Entries and Exits: Trends can help with timing entry and exit points. Traders often aim to enter trades at favourable points within a trend, such as during pullbacks in an uptrend or rallies in a downtrend. This allows them to potentially capture favourable risk-to-reward ratios

- Risk Management: Incorporating trend analysis into risk management is crucial. Traders can set stop-loss orders or trailing stops based on the trend, aiming to protect profits or limit losses if the trend reverses. Position sizing can also be adjusted based on the strength or duration of a trend, with larger positions taken in strong, well-established trends

- Multiple Time Frame Analysis: Examining trends across different time frames can provide a broader perspective. Traders can look for alignment in trends across shorter-term and longer-term charts to gain confidence in their trading decisions. For example, a Trend on a daily chart may align with a Trend on a hourly chart, reinforcing the potential trading opportunity

The Myfractalrange Trend signal can be used for all the possibilities listed above

Here is an example of a Bullish Trend pattern: BTFD set up

Here is an example of a Bearish Trend pattern: STFR set up

Why use Trend in combination with other indicators, such as Hurst and probable Range?

Using Trend in combination with Hurst exponent and probable Range can provide traders with a more comprehensive view of market dynamics and potential trading opportunities. Here's how the three concepts can complement each other:

- Trend Analysis: Trend analysis helps identify the prevailing direction of the market. It provides insights into whether the market is in an uptrend (Bullish), downtrend (Bearish), or sideways consolidation (Neutral). Trend analysis helps traders align their positions with the dominant market direction, increasing the likelihood of successful trades

- Hurst exponent: Hurst exponent is a measure of the persistence or mean reversion characteristics of a time series. It provides insights into the strength and sustainability of price movements. Hurst momentum analysis helps traders understand whether the market is exhibiting trending behaviour or mean-reverting behaviour. It can help identify potential reversals or continuation patterns in the price action.

- Probable Range: The Range refers to the expected price range within which an asset is likely to fluctuate, in our case the MFR Ranges (normal and longer-term). It helps traders set realistic profit targets and stop-loss levels. By combining the probable range with the trend and the Hurst Exponent, traders can better gauge the potential extent of price movements and make more informed decisions regarding entry and exit points.

How to use these tools together?

- Confirmation and Confluence: Combining Trend with Hurst & Range can provide confirmation and confluence signals. For instance, when the trend analysis indicates an uptrend, Hurst confirms strong positive momentum and Range confirms the upside potential, it provides a stronger signal for potential bullish trades

- Timing Entries and Exits: The combination of trend analysis, Hurst and Range can assist in timing entry and exit points. For example, when trend analysis indicates an uptrend, traders can look for bullish signals from Hurst value and low of the MFR Range to identify potential entry points during pullbacks or periods of consolidation. Conversely, in a downtrend, bearish signals from Hurst at the top of the MFR Range can guide traders in identifying potential short-selling opportunities during corrective rallies

- Risk Management: The integration of trend analysis with Hurst and Range can also aid in risk management. Traders can adjust their stop-loss levels and profit targets based on the strength of the trend, its strength and its Range. Tighter stop-loss levels can be set when both trend analysis, Hurst value and Range are aligned, indicating a higher probability of trend continuation. Conversely, wider stop-loss levels may be used when conflicting signals or weakening trends are observed

By combining Trend analysis, Hurst exponent and MFR probable Range, traders can gain a more comprehensive understanding of the market's behaviour and make more informed trading decisions.

It's important to note that while Trend is a useful tool, it should not be relied upon solely for making trading decisions. It's recommended to use it in conjunction with other technical analysis tools and consider other factors such as market conditions, risk management, and fundamental analysis. Remember that the momentum indicator is just one tool among many, and it's important to consider other factors such as volume, momentum, volatility, and overall market conditions when making trading decisions. Additionally, using stop-loss orders and proper risk management techniques is crucial to mitigate potential losses.

We hope that you will find these explanations useful, please contact us by private message for access.

Enjoy!

DISCLAIMER: No sharing, copying, reselling, modifying, or any other forms of use are authorised. This script is strictly for individual use and educational purposes only. This is not financial or investment advice. Investments are always made at your own risk and are based on your personal judgement. Myfractalrange is not responsible for any losses you may incur. Please invest wisely.

Portfolio Backtester Engine█ OVERVIEW

Portfolio Backtester Engine (PBTE). This tool will allow you to backtest strategies across multiple securities at once. Allowing you to easier understand if your strategy is robust. If you are familiar with the PineCoders backtesting engine , then you will find this indicator pleasant to work with as it is an adaptation based on that work. Much of the functionality has been kept the same, or enhanced, with some minor adjustments I made on the account of creating a more subjectively intuitive tool.

█ HISTORY

The original purpose of the backtesting engine (`BTE`) was to bridge the gap between strategies and studies . Previously, strategies did not contain the ability to send alerts, but were necessary for backtesting. Studies on the other hand were necessary for sending alerts, but could not provide backtesting results . Often, traders would have to manage two separate Pine scripts to take advantage of each feature, this was less than ideal.

The `BTE` published by PineCoders offered a solution to this issue by generating backtesting results under the context of a study(). This allowed traders to backtest their strategy and simultaneously generate alerts for automated trading, thus eliminating the need for a separate strategy() script (though, even converting the engine to a strategy was made simple by the PineCoders!).

Fast forward a couple years and PineScript evolved beyond these issues and alerts were introduced into strategies. The BTE was not quite as necessary anymore, but is still extremely useful as it contains extra features and data not found under the strategy() context. Below is an excerpt of features contained by the BTE:

"""

More than `40` built-in strategies,

Customizable components,

Coupling with your own external indicator,

Simple conversion from Study to Strategy modes,

Post-Exit analysis to search for alternate trade outcomes,

Use of the Data Window to show detailed bar by bar trade information and global statistics, including some not provided by TV backtesting,

Plotting of reminders and generation of alerts on in-trade events.

"""

Before I go any further, I want to be clear that the BTE is STILL a good tool and it is STILL very useful. The Portfolio Backtesting Engine I am introducing is only a tangental advancement and not to be confused as a replacement, this tool would not have been possible without the `BTE`.

█ THE PROBLEM

Most strategies built in Pine are limited by one thing. Data. Backtesting should be a rigorous process and researchers should examine the performance of their strategy across all market regimes; that includes, bullish and bearish markets, ranging markets, low volatility and high volatility. Depending on your TV subscription The Pine Engine is limited to 5k-20k historical bars available for backtesting, which can often leave the strategy results wanting. As a general rule of thumb, strategies should be tested across a quantity of historical bars which will allow for at least 100 trades. In many cases, the lack of historical bars available for backtesting and frequency of the strategy signals produces less than 100 trades, rendering your strategy results inconclusive.

█ THE SOLUTION

In order to be confident that we have a robust strategy we must test it across all market regimes and we must have over 100 trades. To do this effectively, researchers can use the Portfolio Backtesting Engine (PBTE).

By testing a strategy across a carefully selected portfolio of securities, researchers can now gather 5k-20k historical bars per security! Currently, the PTBE allows up to 5 securities, which amounts to 25k-100k historical bars.

█ HOW TO USE

1 — Add the indicator to your chart.

• Confirm inputs. These will be the most important initial values which you can change later by clicking the gear icon ⚙ and opening up the settings of the indicator.

2 — Select a portfolio.

• You will want to spend some time carefully selecting a portfolio of securities.

• Each security should be uncorrelated.

• The entire portfolio should contain a mix of different market regimes.

You should understand that strategies generally take advantage of one particular type of market regime. (trending, ranging, low/high volatility)

For example, the default RSI strategy is typically advantageous during ranging markets, whereas a typical moving average crossover strategy is advantageous in trending markets.

If you were to use the standard RSI strategy during a trending market, you might be selling when you should be buying.

Similarily, if you use an SMA crossover during a ranging market, you will find that the MA's may produce many false signals.

Even if you build a strategy that is designed to be used only in a trending market, it is still best to select a portfolio of all market regimes

as you will be able to test how your strategy will perform when the market does something unexpected.

3 — Test a built-in strategy or add your own.

• Navigate to gear icon ⚙ (settings) of strategy.

• Choose your options.

• Select a Main Entry Strat and Alternate Entry Strat .

• If you want to add your own strategy, you will need to modify the source code and follow the built-in example.

• You will only need to generate (buy 1 / sell -1/ neutral 0) signals.

• Select a Filter , by default these are all off.

• Select an Entry Stop - This will be your stop loss placed at the trade entry.

• Select Pyamiding - This will allow you to stack positions. By default this is off.

• Select Hard Exits - You can also think of these as Take Profits.

• Let the strategy run and take note of the display tables results.

• Portfolio - Shows each security.

• The strategy runs on each asset in your portfolio.

• The initial capital is equally distributed across each security.

So if you have 5 securities and a starting capital of 100,000$ then each security will run the strategy starting with 20,000$

The total row will aggregate the results on a bar by bar basis showing the total results of your initial capital.

• Net Profit (NP) - Shows profitability.

• Number of Trades (#T) - Shows # of trades taken during backtesting period.

• Typically will want to see this number greater than 100 on the "Total" row.

• Average Trade Length (ATL) - Shows average # of days in a trade.

• Maximum Drawdown (MD ) - Max peak-to-valley equity drawdown during backtesting period.

• This number defines the minimum amount of capital required to trade the system.

• Typically, this shouldn’t be lower than 34% and we will want to allow for at least 50% beyond this number.

• Maximum Loss (ML) - Shows largest loss experienced on a per-trade basis.

• Normally, don’t want to exceed more than 1-2 % of equity.

• Maximum Drawdown Duration (MDD) - The longest duration of a drawdown in equity prior to a new equity peak.

• This number is important to help us psychologically understand how long we can expect to wait for a new peak in account equity.

• Maximum Consecutive Losses (MCL) - The max consecutive losses endured throughout the backtesting period.

• Another important metric for trader psychology, this will help you understand how many losses you should be prepared to handle.

• Profit to Maximum Drawdown (P:MD) - A ratio for the average profit to the maximum drawdown.

• The higher the ratio is, the better. Large profits and small losses contribute to a good PMD.

• This metric allows us to examine the profit with respect to risk.

• Profit Loss Ratio (P:L) - Average profit over the average loss.

• Typically this number should be higher in trend following systems.

• Mean reversion systems show lower values, but compensate with a better win %.

• Percent Winners (% W) - The percentage of winning trades.

• Trend systems will usually have lower win percentages, since statistically the market is only trending roughly 30% of the time.

• Mean reversion systems typically should have a high % W.

• Time Percentage (Time %) - The amount of time that the system has an open position.

• The more time you are in the market, the more you are exposed to market risk, not to mention you could be using that money for something else right?

• Return on Investment (ROI) - Your Net Profit over your initial investment, represented as a percentage.

• You want this number to be positive and high.

• Open Profit (OP) - If the strategy has any open positions, the floating value will be represented here.

• Trading Days (TD) - An important metric showing how many days the strategy was active.

• This is good to know and will be valuable in understanding how long you will need to run this strategy in order to achieve results.

█ FEATURES

These are additional features that extend the original `BTE` features.

- Portfolio backtesting.

- Color coded performance results.

- Circuit Breakers that will stop trading.

- Position reversals on exit. (Simulating the function of always in the market. Similar to strategy.entry functionality)

- Whipsaw Filter

- Moving Average Filter

- Minimum Change Filter

- % Gain Equity Exit

- Popular strategies, (MACD, MA cross, supertrend)

Below are features that were excluded from the original `BTE`

- 2 stage in-trade stops with kick-in rules (This was a subjective decision to remove. I found it to be complex and thwarted my use of the `BTE` for some time.)

- Simple conversion from Study to Strategy modes. (Not possible with multiple securities)

- Coupling with your own external indicator (Not really practical to use with multiple securities, but could be used if signals were generated based on some indicator which was not based on the current chart)

- Use of the Data Window to show detailed bar by bar trade information and global statistics.

- Post Exit Analysis.

- Plotting of reminders and generation of alerts on in-trade events.

- Alerts (These may be added in the future by request when I find the time.)

█ THANKS

The whole PineCoders team for all their shared knowledge and original publication of the BTE and Richard Weismann for his ideas on building robust strategies.

═════════════════════════════════════════════════════════════════════════

[ADOL_]Trend BreakENG)

Trend Break trend break+

It automatically draws a trend line and generates signals based on elaborate standards.

It is a secretary who plays an excellent role as an auxiliary tool in the sale and sale.

Trend lines are an important tool in determining the direction of trading.

These indicators are automatic trend line construction and trading signal generation indicators.

The background informs the trend section. The key function is the notation of signals.

principle)

It reflects the concept of HH and LL.

What is HH? Abbreviation of Higher High, which means to increase the high point.

What is LL? It stands for Lower Low, which means to lower the low point.

The trend line is created by the basic construction method that connects the highs and the highs, and the lows and the lows.

The basic signal is prepared by generating a signal from the 3 previous candles of the breakthrough of the trend line.

Basic signal; L for long, S for short

When the flow continues in one direction by reflecting the candle flow in ascending and descending order

Create a filtered signal.

Filtering signal; Filtering signals are marked with ★.

The background is the output through direction matching filtering of the double weighted moving average.

Green Background: Uptrend Progress

Red background: downtrend progress

Gray background: neutral zone (rebound, retracement, crossing)

Principle example)

This is an example of a signal with no filtering applied.

This is an example of a filtered signal.

option)

Line color, line shape, whether or not to include a tail when drawing a trend, line thickness

You can choose options such as.

Time frame)

Applicable to all time frames.

Scalping: 1 minute bar, 3 minute bar

Single hit: 3 minutes, 15 minutes, 1 hour

Swing: 1 hour salary, 4 hour salary, daily salary

Applicable market)

Applicable to all markets.

Examples of market application)

NASDAQ

Korean stocks (ex: Samsung Electronics)

alert)

You can use the alert function.

-Background alert for trend direction

-Alert to break through downtrend line and alert to break through uptrend line

-Filtering applied alert to break through the downtrend line

-Filtering applied alert to break through the uptrend line

Trading method)

1. The trend line refers to the concept of support/resistance touch. Through the concept of touch

You can set a standard once more to see if the signal output is adequate.

One touch of support/resistance line: On the first touch, see long at the support line and short at the resistance line.

Touch the support/resistance line 2: Check the position once more in the step of building (consolidating) the support/resistance line. Long at the support level and short at the resistance level.

3 touches of the ground/resistance line: This is the section with high possibility in both directions.

Support/resistance line 4 (or higher) touch: Use as a breakthrough reference line. When breaking through, hit short at the support line and long at the resistance line.

If the support/resistance line breaks through to the closing price, support becomes resistance and resistance becomes support."

Trading method)

1. The trend line refers to the concept of support/resistance touch. Through the concept of touch

You can set a standard once more to see if the signal output is adequate.

One touch of support/resistance line: On the first touch, see long at the support line and short at the resistance line.

Touch the support/resistance line 2: Check the position once more in the step of building (consolidating) the support/resistance line. Long at the support level and short at the resistance level.

3 touches of the ground/resistance line: This is the section with high possibility in both directions.

Support/resistance line 4 (or higher) touch: Use as a breakthrough reference line. When breaking through, hit short at the support line and long at the resistance line.

If the support/resistance line breaks through to the closing price, support becomes resistance and resistance becomes support."

2. Entry Criteria/Stop Loss Criteria

-Entry criteria; Follow the signal.

-Stop loss criteria;

Using Fixed Stop Loss: Set the 1% fixed stop loss interval from signal generation (% is set individually).

Use of Candle Stop: When the low or high point of the signal generating rod collapses, set the stop loss.

Use of flow stop loss: Set the stop loss by considering the flow of the wave.

3. Note

All trading decisions you make are your sole responsibility.

If the indicators were helpful, please support us. Help in developing the following metrics.

4. How to use

Tap Add Indicator to Favorites. Click on the indicator at the top of the chart screen and look at the left tab

Indicators have been added. Press to use. Anyone can use it.

KOR)

Trend Break 추세돌파+

추세선을 자동으로 작도해주며, 정교화된 기준으로 시그널을

발생시켜 매매에 보조도구로써 훌륭한 역할을 수행해내는 비서입니다.

추세선은 매매의 방향성을 결정하는데 중요한 도구입니다.

해당 지표는 자동 추세선 작도와 매매 시그널 발생 지표입니다.

배경은 추세구간을 알려줍니다. 핵심기능은 시그널의 표기입니다.

원리)

HH와 LL의 개념을 반영합니다.

HH란 ? Higher High의 약자로 고점을 높인다는 의미입니다.

LL란? Lower Low의 약자로 저점을 낮춘다는 의미입니다.

추세선은 고점과 고점, 저점과 저점을 잇는 기본 작도 방법으로 만들어집니다.

추세선 돌파의 3개 이전 캔들부터 신호발생으로 준비를 기본 시그널을 만듭니다.

기본 시그널 ; 롱의 경우 L 표기, 숏의 경우 S표기

오름차순과 내림차순의 캔들 흐름을 반영하여, 한 방향으로 흐름이 지속될때

필터링된 시그널을 만듭니다.

필터링 시그널 ; 필터링 시그널은 ★ 표기가 붙습니다.

배경은 이중 가중이동 평균의 방향일치 필터링을 통한 출력입니다.

초록색 배경 : 상승추세 진행

빨간색 배경 : 하락추세 진행

회색 배경 : 중립구역(반등, 되돌림, 교차)

원리 예시)

필터링이 적용되지 않은 시그널의 예시입니다.

필터링이 적용된 시그널의 예시입니다.

옵션)

선색상, 선모양, 추세선작도시 꼬리포함여부, 선굵기

등의 옵션을 선택할 수 있습니다.

타임프레임)

모든 시간프레임에 적용 가능합니다.

스캘핑 : 1분봉, 3분봉

단타 : 3분봉, 15분봉, 1시간봉

스윙 : 1시간봉, 4시간봉, 일봉

적용시장)

모든 시장에 적용 가능합니다.

시장 적용의 예시)

나스닥

한국주식(예 : 삼성전자)

알람)

얼러트 기능을 사용할 수 있습니다.

- 추세방향성에 대한 배경의 얼러트

- 하락추세선 돌파 얼러트, 상승추세선 돌파 얼러트

- 필터링을 적용한 하락추세선 돌파 얼러트

- 필터링을 적용한 상승추세선 돌파 얼러트

매매방법)

1. 추세선은 지지/저항의 터치 개념을 참고합니다. 터치의 개념을 통해

시그널 출력이 적절한지 한번 더 기준을 잡을 수 있습니다.

지지/저항선 1터치 : 첫번째 터치에는 지지선에서 롱을, 저항선에서 숏을 봅니다.

지지/저항선 2터치 : 지지/저항선 구축(다지기)의 단계로 한번 더 자리를 확인합니다. 지지선에서 롱을, 저항선에서 숏을 봅니다.

지/저항선의 3터치 : 양방향의 가능성이 높은 구간입니다.

지지/저항선4(이상)터치 : 돌파기준선으로 사용합니다. 돌파할 때, 지지선에서 숏을, 저항선에서 롱을 칩니다.

지지/저항선이 종가로 뚫리면 지지는 저항이 되고, 저항은 지지가 됩니다."

2. 진입기준/손절기준

- 진입기준; 시그널을 따릅니다.

- 손절기준;

고정손절가 이용 : 시그널 발생으로부터 1% 고정 손절가 구간을 설정합니다.(%는 개별로 설정)

캔들손절가 이용 : 시그널 발생봉의 저점이나 고점이 무너지면 손절을 설정합니다.

흐름손절가 이용 : 파동의 흐름을 고려하여 손절을 설정합니다.

3. 참고

귀하가 내리는 모든 거래 결정은 전적으로 귀하의 책임입니다.

지표가 도움이 되었다면 응원 부탁드립니다. 다음 지표 개발에 도움이 됩니다.

4. 사용방법

즐겨찾기에 인디케이터 넣기를 누릅니다. 차트화면 상단에 지표를 눌러서 왼쪽탭에 보면

지표가 추가되어 있습니다. 눌러서 사용합니다. 누구나 사용할 수 있습니다.

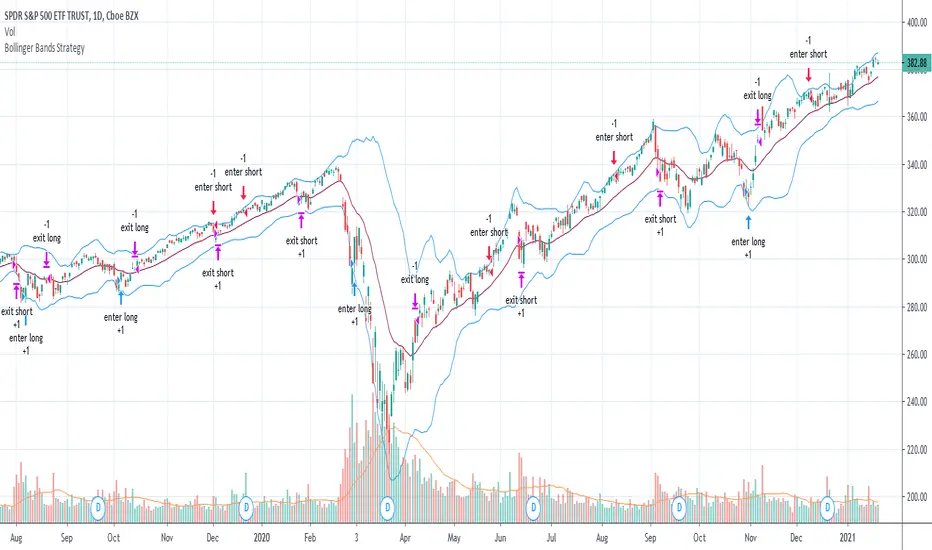

Bollinger Bands Strategy with Intraday Intensity IndexFor Educational Purposes. Results can differ on different markets and can fail at any time. Profit is not guaranteed.

This only works in a few markets and in certain situations. Changing the settings can give better or worse results for other markets.

This is a mean reversion strategy based on Bollinger Bands and the Intraday Intensity Index (a volume indicator). John Bollinger mentions that the Intraday Intensity Index can be used with Bollinger Bands and is one of the top indicators he recommends in his book. It seems he prefers it over the other volume indicators that he compares to for some reason. III looks a lot like Chaikin Money Flow but without the denominator in that calculation. On the default settings of the BBs, the III helps give off better entry signals. John Bollinger however is vague on how to use the BBs and it's hard to say if one should enter when it is below/above the bands or when the price crosses them. I find that with many indicators and strategies it's best to wait for a confirmation of some sort, in this case by waiting for some crossover of a band. Like most mean reversion strategies, the exit is very loose if using BBs alone. Usually the plan to exit is when the price finally reverts back to the mean or in this case the middle band. This can potentially lead to huge drawdowns and/or losses. Mean reversion strategies can have high win/loss ratios but can still end up unprofitable because of the huge losses that can occur. These drawdowns/losses that mean reversion strategies suffer from can potentially eat away at a large chunk of all that was previously made or perhaps up to all of it in the worst cases, can occur weeks or perhaps up to months after being profitable trading such a strategy, and will take a while and several trades to make it all back or keep a profitable track record. It is important to have a stop loss, trailing stop, or some sort of stop plan with these types of strategies. For this one, in addition to exiting the trade when price reverts to the middle band, I included a time-based stop plan that exits with a gain or with a loss to avoid potentially large losses, and to exit after only a few periods after taking the trade if in profit instead of waiting for the price to revert back to the mean.

AltS Swing [Backtester]

PLEASE READ THIS DESCRIPTION TO SAVE TIME AND UNDERSTAND WHAT THIS INDICATOR DOES

This is the backtesting version for this script

In this back tested version I have shown it to be used on regular candles with realistic calculations in regards to positions sizes, slippage, fees and more

Kind Regards

This is a official version of AltSignals Long/Short Reverse Indicator

Description:

This indicator uses various indicators in combination with each other, some of the key ones to mention is Hulls, EMA , MA. Along with that it uses EMA crossovers to get the precise entries and exits.

The recommended time frames with this indictor are shorter ones, for example 5m,10m,15m work well, along with that I have found that some of the more unique time frames also work well such as 20m,45m,2hr and so on.

This indicator is not super advanced but it's still very powerful, with only 130 lines of code.

This indicator works on every chart, time, and candle type but you must play with the settings to find what is best, the same setting will not work on every pair etc.

With AltSignals Swing Indicator it trades one way, that means it gives 3 pieces of information. BUY/TakeProfit/StopLoss.

Unlike most indicators which Buy and Sell both ways this one focuses on one direction of trading so please take into account when using this.

I have added in a reverse strategy which basically shows the opposite values of of the buy, so if you select the box in the settings and un-tick it, then it will show opposite directions so sells only.

This feature is very useful especially in general bear markets when buying is difficult.

I have also added in the option for no stop losses to be used, if you set the stop loss value = 100 then it will show no stop losses.

I suggest a stop loss somewhere in the region of 1-2-3%, please note that you can use decimal stop losses too so for example 0.1 or 0.5.

This indicator is NOT a once size fits all, every chart is different, time frame and candles also, so i would suggest spending some time going through and playing with the channel length settings, which will change the EMA numbers.

Using this along with the back script to find the ideal settings is the best way to use this script, once you have done that make sure to save those values somewhere.

Its important to remember that the Regular script and the back testing script values should be the same for them to match up on the chart, so the channel lengths, stop losses and so on values should be the same.

Side note

This is not financial advice.

We will continue making updates as time goes on.

If you would like to try this script for free please visit our website or message us on Tradingview live chat.

AltS Swing [Backtester]

PLEASE READ THIS DESCRIPTION TO SAVE TIME AND UNDERSTAND WHAT THIS INDICATOR DOES

This is the backtesting version for this script

In this back tested version I have shown it to be used on regular candles with realistic calculations in regards to positions sizes, slippage, fees and more

Kind Regards

This is a official version of AltSignals Long/Short Reverse Indicator

Description:

This indicator uses various indicators in combination with each other, some of the key ones to mention is Hulls, EMA , MA. Along with that it uses EMA crossovers to get the precise entries and exits.

The recommended time frames with this indictor are shorter ones, for example 5m,10m,15m work well, along with that I have found that some of the more unique time frames also work well such as 20m,45m,2hr and so on.

This indicator is not super advanced but it's still very powerful, with only 130 lines of code.

This indicator works on every chart, time, and candle type but you must play with the settings to find what is best, the same setting will not work on every pair etc.

With AltSignals Swing Indicator it trades one way, that means it gives 3 pieces of information. BUY/TakeProfit/StopLoss.

Unlike most indicators which Buy and Sell both ways this one focuses on one direction of trading so please take into account when using this.

I have added in a reverse strategy which basically shows the opposite values of of the buy, so if you select the box in the settings and un-tick it, then it will show opposite directions so sells only.

This feature is very useful especially in general bear markets when buying is difficult.

I have also added in the option for no stop losses to be used, if you set the stop loss value = 100 then it will show no stop losses.

I suggest a stop loss somewhere in the region of 1-2-3%, please note that you can use decimal stop losses too so for example 0.1 or 0.5.

This indicator is NOT a once size fits all, every chart is different, time frame and candles also, so i would suggest spending some time going through and playing with the channel length settings, which will change the EMA numbers.

Using this along with the back script to find the ideal settings is the best way to use this script, once you have done that make sure to save those values somewhere.

Its important to remember that the Regular script and the back testing script values should be the same for them to match up on the chart, so the channel lengths, stop losses and so on values should be the same.

Side note

This is not financial advice.

We will continue making updates as time goes on.

If you would like to try this script for free please visit our website or message us on Tradingview live chat.

AltS Swing (INV)

PLEASE READ THIS DESCRIPTION TO SAVE TIME AND UNDERSTAND WHAT THIS INDICATOR DOES

This is a official version of AltSignals Long/Short Reverse Indicator

Description:

This indicator uses various indicators in combination with each other, some of the key ones to mention is Hulls, EMA , MA. Along with that it uses EMA crossovers to get the precise entries and exits.

The recommended time frames with this indictor are shorter ones, for example 5m,10m,15m work well, along with that I have found that some of the more unique time frames also work well such as 20m,45m,2hr and so on.

This indicator is not super advanced but it's still very powerful, with only 130 lines of code.

This indicator works on every chart, time, and candle type but you must play with the settings to find what is best, the same setting will not work on every pair etc.

With AltSignals Swing Indicator it trades one way, that means it gives 3 pieces of information. BUY/TakeProfit/StopLoss.

Unlike most indicators which Buy and Sell both ways this one focuses on one direction of trading so please take into account when using this.

I have added in a reverse strategy which basically shows the opposite values of of the buy, so if you select the box in the settings and un-tick it, then it will show opposite directions so sells only.

This feature is very useful especially in general bear markets when buying is difficult.

I have also added in the option for no stop losses to be used, if you set the stop loss value = 100 then it will show no stop losses.

I suggest a stop loss somewhere in the region of 1-2-3%, please note that you can use decimal stop losses too so for example 0.1 or 0.5.

This indicator is NOT a once size fits all, every chart is different, time frame and candles also, so i would suggest spending some time going through and playing with the channel length settings, which will change the EMA numbers.

Using this along with the back script to find the ideal settings is the best way to use this script, once you have done that make sure to save those values somewhere.