Period Range AnalyzerThis indicator analyzes a specific periodic range, which can start from a fixed date or a defined lookback period. It draws percentage levels and colored zones between the highest and lowest price. It also displays a detailed information table, which shows the price's position within the range in "Trend" mode, and the relative strength of currency pairs in "Forex" mode. The current price position is also indicated by a label with a percentage value and the name of the corresponding zone.

User Guide

Calculation Method

This setting determines how the indicator defines the range used for the calculation.

Lookback Period: In this mode, the indicator uses the last N candles (the number can be specified in the "Lookback Period (bars)" field). The range (the highest and lowest price) is "floating," meaning it is recalculated with each new candle based on the last N candles.

Date Based: In this mode, the calculation starts from a fixed date and time you select. The indicator finds the opening price of the start date and continuously tracks the highest and lowest price from that point on. This mode is ideal for measuring performance from a specific event (e.g., start of a week/month/year, news).

Data Handling Note: If you select a date in "Date Based" mode for which no data is available on the current timeframe (e.g., switching to a very low timeframe), the indicator will automatically use the earliest available candle as the starting point. All calculations (Open, Max, Min, Range, Percentage, Change, Trend) are based on this actual start date.

Start Date & Time

This setting is only active in "Date Based" mode.

Here you can specify the fixed starting point for the calculation.

The specified time is in the Exchange timezone.

Important limitation: Due to TradingView platform limits, visual elements (levels, zones) are only drawn for a maximum of 250 candles back. If the set date is older than this, the calculation still applies to the entire period (from the set date), but the drawing only covers the last 250 candles. The table always displays accurate data for the entire period.

When switching to a higher timeframe, the range may restart from a slightly later bar due to TradingView's bar alignment. For best accuracy, set your timeframe first, then select the start date.

Table Mode

This setting controls what data the information table displays.

Trend: This is the default mode, which works on any symbol (stock, index, crypto, etc.). It displays information related to the trend and the range.

Forex: This is a special mode used to measure the strength of currency and crypto pairs. It only works on symbols with exactly 6 characters (e.g., "EURUSD", "BTCUSD"). It treats the first 3 characters as the base currency (e.g., EUR) and the last 3 as the quote currency (e.g., USD). If the symbol does not have 6 characters, the table will automatically display in "Trend" mode.

Trend

This trend determination operates based on the formation order of the high and low within the analyzed range:

Its switch is located in the “Table Additional Rows” menu.

Bullish: Indicated if the low was formed before the high (on different candles). Or if they formed on the same candle, it was a bullish candle.

Bearish: Indicated if the high was formed before the low (on different candles). Or if they formed on the same candle, it was a bearish candle.

Neutral: Indicated if the high and low formed on the same candle, and it was a "doji" candle (close = open).

Upper & Lower Threshold

These settings (Upper Threshold (%) and Lower Threshold (%) in the "Label Coloring" section) primarily determine the state (Bullish/Bearish/Neutral) of the top row of the table.

The logic is not based on the percentage change of the price movement, but on the current price's position within the range, where the bottom of the range is 0% and the top is 100%.

Upper Threshold (%): The percentage level (e.g., 60.0) above which the indicator considers the price position "Bullish" (or "Strong").

Lower Threshold (%): The percentage level (e.g., 40.0) below which the indicator considers the price position "Bearish" (or "Weak").

If the price is between the two (e.g., between 40% and 60%), the signal is Neutral.

Secondary function: These thresholds also control the color of the label next to the price, provided the "Dynamic Label Coloring" option is enabled.

스크립트에서 "Table"에 대해 찾기

Range Percentage Analyzer This indicator is a tool for analyzing the market range and trend. It calculates the extent of price movement between a specified starting point and the current price, displaying it as a percentage.

The calculation can be based on a fixed lookback period (e.g., the last 30 candles) or from a fixed start date. It also provides a clear table that shows the general trend in "Trend" mode, and the relative strength of the base and quote currencies of forex pairs (e.g., EURUSD) in "Forex" mode.

User Guide

Calculation Method

This setting determines how the indicator defines the starting point for the calculation.

Lookback Period: In this mode, the indicator uses the last N candles (the number can be specified in the "Lookback Period (bars)" field, maximum 250).

The starting point is "floating," meaning it shifts with each new candle. For example, with a setting of 30, the 30th candle from the current one will always be the starting point.

Date Based: In this mode, the calculation starts from a fixed date and time you select.

This mode is ideal for measuring performance from a specific event (e.g., news, start of a week/month).

Note: If you select a date in "Date Based" mode for which no data is available on the current timeframe (e.g., switching to a very low timeframe), the indicator will automatically use the earliest available candle as the starting point.

Start Date & Time

This setting is only active in "Date Based" mode.

Here you can specify the fixed starting point for the calculation.

The specified time is in the Exchange timezone.

Important limitation: Due to TradingView platform limits, visual elements (box, line) are only drawn for a maximum of 250 candles back.

If the set date is older than this, the calculation still applies to the entire period (from the set date), but the drawing only covers the last 250 candles.

When switching to a higher timeframe, the range may restart from a slightly later bar due to TradingView's bar alignment. For best accuracy, set your timeframe first, then select the start date.

Table Mode

This setting controls what data the information table displays.

Trend: This is the default mode, which works on any symbol (stock, index, crypto, etc.). It displays information related to the trend.

Forex: This is a special mode used to measure the strength of currency pairs.

It only works on symbols with exactly 6 characters (e.g., "EURUSD", "BTCUSD"). It treats the first 3 characters as the base currency (e.g., EUR) and the last 3 as the quote currency (e.g., USD).

If the symbol does not have 6 characters, the table will automatically display in "Trend" mode.

Extremes Trend Row

If this is enabled, the table displays an additional row that determines the trend based on the formation order of the high and low within the analyzed range.

The logic is as follows:

Bullish: Indicated if the low was formed before the high.

(Or if they formed on the same candle, which was a bullish candle).

Bearish: Indicated if the high was formed before the low.

(Or if they formed on the same candle, which was a bearish candle).

Neutral: Indicated if the high and low formed on the same candle, and it was a "doji" candle (close = open).

Upper & Lower Threshold

These settings control the logic for the "Change Trend" and "Forex Display" rows at the top of the table.

They determine when the total percentage change for the entire period is considered "Bullish/Strong", "Bearish/Weak", or "Neutral".

Upper Threshold (%): The percentage value (default 0.1%) above which the indicator considers the change "Bullish/Strong".

Lower Threshold (%): The percentage value (default -0.1%) below which the indicator considers the change "Bearish/Weak".

If the change is between the two, the signal is Neutral.

SECTOR ROTATION Sector Rotation Indicator with Auto Chart Symbol

This indicator helps traders track relative performance across multiple indices/sectors simultaneously, making it easy to identify sector rotation and market leadership.

Key Features:

✅ 21 Symbols Tracking: Monitor 20 customizable symbols + your current chart symbol automatically(DIVIDEND SYMBOL)

✅ Percentage Performance: All moving averages show percentage gain/loss from 1 timeframe period ago

✅ Color-Coded Visualization: Heat map coloring (red to green) based on relative performance ranking

✅ Flexible Timeframes: Works on any timeframe from 1-minute to 12-month charts

✅ Performance Table: Quick-view table showing candle performance with inside/outside bar detection

✅ Indian Market Ready: Pre-configured with NSE indices (NIFTY, BANKNIFTY, and sectoral indices)

Default Symbols (Customizable):

NIFTY, CNXSMALLCAP, CNXMIDCAP, BANKNIFTY

Sector indices: IT, AUTO, PHARMA, METAL, ENERGY, FMCG, etc.

Plus your current chart symbol (automatically added)

How It Works:

Select your preferred timeframe (1D, 1W, 1M, etc.)

The indicator calculates percentage performance from given period ago

Moving averages show smoothed performance trends

Colors indicate relative strength: Green = outperformers, Red = underperformers

Perfect For:

Sector rotation analysis

Relative strength comparison

Market breadth assessment

Index/ETF traders

Swing and position traders

Settings:

Adjustable MA length (default: 20)

Customizable colors and table position

Show/hide percentage labels

Horizontal or vertical table layout

This is not any buy or sell signal or recommendation, consult with your advisor first.

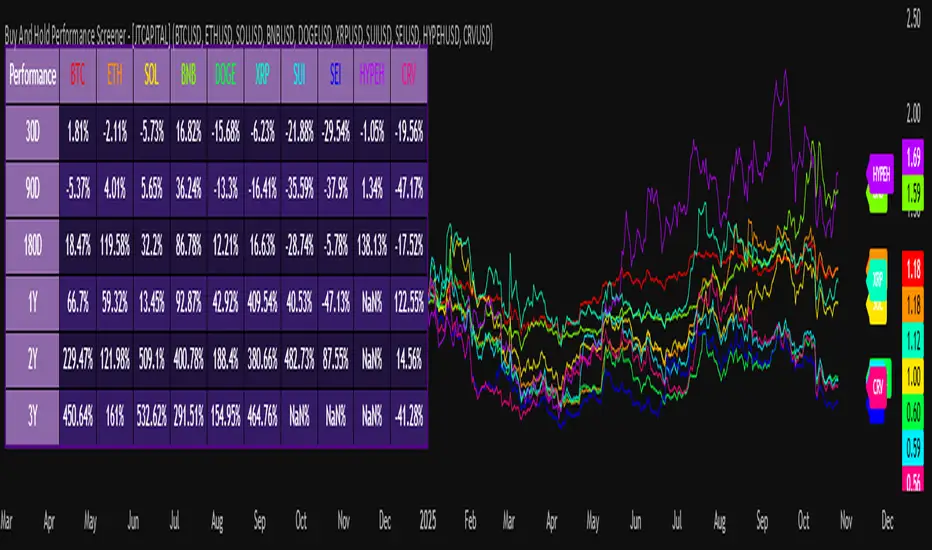

Buy And Hold Performance Screener - [JTCAPITAL]Buy And Hold Performance Screener – is a script designed to track and display multi-asset “buy and hold” performance curves and performance statistics over defined timeframes for selected symbols. It doesn’t attempt to time entries or exits; rather, it shows what would happen if one simply bought the asset at the defined start date and held it.

The indicator works by calculating in the following steps:

Start Date Definition

The script begins by reading an input for the start date. This defines the bar from which the equity curves begin.

Symbol Definitions & Close Price Retrieval

The script allows the user to specify up to ten tickers. For each ticker it uses request.security() on the “1D” timeframe to retrieve the daily close price of that symbol.

Plot Enable Inputs

For each ticker there is an input boolean controlling whether the equity curve for that ticker should be plotted.

Asset Name Cleaning

The helper function clean_name(string asset) => … takes the asset string (e.g., “CRYPTO:SOLUSD”) and manipulates it (via string splitting and replacements) to derive a cleaned short name (e.g., “SOL”). This name is used for visuals (labels, table headers).

Equity Curve Calculation (“HODL”)

The helper function f_HODL(closez) defines a variable equity that assumes a starting equity of 1 unit at the start date and then multiplies by the ratio of each bar’s close to the prior bar’s close: i.e. daily compounding of returns.

Performance Metrics Calculation

The helper function f_performance(closez) calculates, for each symbol’s close series, the percentage change of the current close relative to its close 30 days ago, 90 days ago, 180 days ago, 1 year ago (365 days), 2 years ago (730 days) and 3 years ago (1095 days).

Equity Curve Plots

For each ticker, if the corresponding plot input is true, the script assigns a plotted variable equal to the equity curve value. Its then drawing each selected equity curve on the chart, each in a distinct color.

Table Construction

If the plottable input is true, the script constructs a table and populates it with rows and column corresponding to the assigned tickers and the set 6 timeframes used for display.

Buy and Sell Conditions:

Since this is strictly a “buy-and-hold” performance screener, there are no explicit buy or sell signals generated or plotted. The script assumes: buy at the defined start_date, hold continuously to present. There are no filters, no exit logic, no take-profit or stop-loss. The benefit of this approach is to provide a clean benchmark of how selected assets would have performed if one simply adopted a passive “buy & hold” approach from a given start date.

Features and Parameters:

start_date (input.time) : Defines the date from which performance and equity curves begin.

ticker1 … ticker10 (input.symbol) : User-selectable asset symbols to include in the screener.

plot1 … plot10 (input.bool) : Boolean flags to enable/disable plotting of each asset’s equity curve.

plottable (input.bool) : Flag to enable/disable drawing the performance table.

Colored plotting + Labels for identifying each asset curve on the chart.

Specifications:

Here is a detailed breakdown of every calculation/variable/function used in the script and what each part means:

start_date

This is defined via input.time(timestamp("1 Jan 2025"), title = "Start Date"). It allows the user to pick a specific calendar date from which the equity curves and performance calculations will start.

ticker1 … ticker10

These inputs allow the user to select up to ten different assets (symbols) to monitor. The script uses each of these to fetch daily close prices.

plot1 … plot10

Boolean inputs controlling which of the ten asset equity curves are plotted. If plotX is true, the equity curve for ticker X will be visible; otherwise it will be not plotted. This gives the user flexibility to include or exclude specific assets on the chart.

Returns the cleaned asset short name.

This provides friendly text labels like “BTC”, “ETH”, “SOL”, etc., instead of full symbol codes.

The choice of distinct colours for each asset helps differentiate curves visually when multiple assets are overlaid.

Colour definitions

Variables color1…color10 are explicitly defined via color.rgb(r,g,b) to give each asset a unique colour (e.g., red, orange, yellow, green, cyan, blue, purple, pink, etc.).

What are the benefits of combining these calculations?

By computing equity curves for multiple assets from the same start date and overlaying them, you can visualise comparative performance of different assets under a uniform “buy & hold” assumption.

The performance table adds multi-horizon returns (30 D, 90 D, 180 D, 1 Y, 2 Y, 3 Y) which helps the user see both short-term and longer-term performance without having to manually compute returns.

The use of daily close data via request.security(..., "1D") removes dependency on the chart’s timeframe, thereby standardising the comparison across assets.

The equity curve and table together provide both visual (curve) and numerical (table) summaries of performance, making it easier to spot trends, divergences, and cross-asset comparisons at a glance.

Because it uses compounding (equity := equity * (closez / closez )), the curves reflect the real growth of a 1-unit investment held over time, rather than only simple returns.

The labelling of curves and the color-coding make the multi-asset overlay easier to interpret.

Using a clean start date ensures that all curves begin at the same point (1 unit at start_date), making relative performance intuitive.

Because of this, the script is useful as a benchmarking tool: rather than trying to pick entries or exit points, you can simply compare “what if I had held these assets since Jan 1 2025” (or your chosen date), and see which assets out-/under-performed in that period. It helps an investor or trader evaluate the long-term benefits of passive vs. active management, or of allocation decisions.

Please note:

The script assumes continuous daily data and does not account for dividends, fees, slippage, or tax implications.

It does not attempt to optimise timing or provide trading signals.

Returns prior to the start date are ignored (equity only begins once time >= start_date).

For newly listed assets with fewer than 365 or 730 or 1095 days of history, the longer-horizon returns may return na or misleading values.

Because it uses request.security() without specifying lookahead, and on “1D” timeframe, it complies with standard usage but you should verify there is no look-ahead bias in your particular setup.

ENJOY!

Multi-Timeframe EMA (5 Configurable)Here's a comprehensive description you can use for your indicator:

Multi-Timeframe EMA Indicator (5 Configurable Slots)

Description

This indicator displays up to 5 Exponential Moving Averages (EMAs) from different timeframes simultaneously on a single chart. Perfect for multi-timeframe analysis, it allows traders to visualize key EMAs from intraday to higher timeframes without switching charts.

Key Features

5 Independent EMA Slots: Each slot can be configured with its own timeframe, EMA length, and color

Flexible Configuration: Mix any timeframes and EMA lengths (e.g., 1m EMA 50, 15m EMA 200, 4h EMA 100)

Smart Label Formatting: Automatically displays timeframes in readable format (minutes, hours, or days)

Optional Data Table: Toggle a compact table showing EMA values and price distance percentages

Individual Toggle Controls: Enable/disable each EMA independently without losing settings

Customizable Styling: Adjust colors and line width to match your chart theme

Default Configuration

EMA 1: 1-minute timeframe, EMA 200 (Red)

EMA 2: 5-minute timeframe, EMA 200 (Purple)

EMA 3: 15-minute timeframe, EMA 200 (Yellow)

EMA 4: 1-hour timeframe, EMA 200 (Blue)

EMA 5: 4-hour timeframe, EMA 200 (Orange)

How to Use

Add the indicator to any chart

Configure each EMA slot in the settings:

Timeframe: Choose from 1m, 5m, 15m, 1h, 4h, D, W, M, or custom

Length: Set the EMA period (default 200)

Color: Select a color for easy identification

Enable "Show Line Labels" to see EMA identifiers on the right side

Enable "Show Values Table" for a detailed view of current values and distances

Use Cases

Trend Analysis: Identify alignment across multiple timeframes

Support/Resistance: Use higher timeframe EMAs as dynamic S/R levels

Entry/Exit Timing: Enter on lower timeframe signals near higher timeframe EMAs

Multi-Timeframe Confirmation: Validate setups when price is above/below key EMAs

Scalping: Monitor 1m/5m EMAs while respecting 1h/4h trend direction

Tips

All EMAs update in real-time and move with the chart

Use contrasting colors for easier visual distinction

Disable unused slots to declutter your chart

The table shows percentage distance from current price to each EMA

Works on any symbol and any chart timeframe

TradeVision Pro - Multi-Factor Analysis System═══════════════════════════════════════════════════════════════════

TRADEVISION PRO - MULTI-FACTOR ANALYSIS SYSTEM

Created by Zakaria Safri

═══════════════════════════════════════════════════════════════════

A comprehensive technical analysis tool combining multiple factors for

signal generation, trend analysis, and dynamic risk management visualization.

Designed for educational purposes to study multi-factor convergence trading

strategies across all markets and timeframes.

⚠️ IMPORTANT DISCLAIMER:

This indicator is provided for EDUCATIONAL and INFORMATIONAL purposes only.

It does NOT constitute financial advice, investment advice, or trading advice.

Past performance does not guarantee future results. Trading involves

substantial risk of loss. Always do your own research and consult a

financial advisor before making trading decisions.

🎯 KEY FEATURES

═══════════════════════════════════════════════════════════════════

✅ MULTI-FACTOR SIGNAL GENERATION

• Price Volume Trend (PVT) analysis

• Rate of Change (ROC) momentum confirmation

• Volume-Weighted Moving Average (VWMA) trend filter

• Simple Moving Average (SMA) price smoothing

• Signals only when all factors align

✅ DYNAMIC RISK VISUALIZATION (Educational Only)

• ATR-based stop loss calculation

• Risk-reward based take profit levels (1-5 targets)

• Visual lines and labels showing entry, SL, and TPs

• Automatically adapts to market volatility

• ⚠️ VISUAL REFERENCE ONLY - Does not execute trades

✅ SUPPORT & RESISTANCE DETECTION

• Automatic pivot-based level identification

• Red dashed lines for resistance zones

• Green dashed lines for support areas

• Helps identify key price levels

✅ VWMA TREND BANDS

• Volume-weighted moving average with standard deviation

• Color-changing bands (Green = Uptrend, Red = Downtrend)

• Filled band area for easy visualization

• Volume-confirmed trend strength

✅ TREND DETECTION SYSTEM

• Counting-based trend confirmation

• Three states: Up Trend, Down Trend, Ranging

• Requires threshold of consecutive bars

• Independent trend validation

✅ PRICE RANGE VISUALIZATION

• High/Low range lines showing market structure

• Filled area highlighting price volatility

• Helps identify breakout zones

✅ COMPREHENSIVE INFO TABLE

• Real-time trend status

• Last signal type (BUY/SELL)

• Entry price display

• Stop loss level

• All active take profit levels

• Clean, professional layout

✅ OPTIONAL FEATURES

• Bar coloring by trend direction

• Customizable alert notifications

• Toggle visibility for all components

• Fully configurable parameters

📊 HOW IT WORKS

═══════════════════════════════════════════════════════════════════

SIGNAL METHODOLOGY:

BUY SIGNAL generates when ALL conditions are met:

• Smoothed price > Moving Average (upward price trend)

• PVT > PVT Average (volume supporting uptrend)

• ROC > 0 (positive momentum)

• Close > VWMA (above volume-weighted average)

SELL SIGNAL generates when ALL conditions are met:

• Smoothed price < Moving Average (downward price trend)

• PVT < PVT Average (volume supporting downtrend)

• ROC < 0 (negative momentum)

• Close < VWMA (below volume-weighted average)

This multi-factor approach filters out weak signals and waits for

strong convergence before generating alerts.

RISK CALCULATION:

Stop Loss = Entry ± (ATR × SL Multiplier)

• Uses Average True Range for volatility measurement

• Automatically adjusts to market conditions

Take Profit Levels = Entry ± (Risk Distance × TP Multiplier × Level)

• Risk Distance = |Entry - Stop Loss|

• Creates risk-reward based targets

• Example: TP Multiplier 1.0 = 1:1, 2:2, 3:3 risk-reward

⚠️ NOTE: All risk levels are VISUAL REFERENCES for educational study.

They do not execute trades automatically.

⚙️ SETTINGS GUIDE

═══════════════════════════════════════════════════════════════════

SIGNAL SETTINGS:

• Signal Length (14): Main calculation period for averages

• Smooth Length (8): Price data smoothing period

• PVT Length (14): Price Volume Trend calculation period

• ROC Length (9): Rate of Change momentum period

RISK MANAGEMENT (Visual Only):

• ATR Length (14): Volatility measurement lookback

• SL Multiplier (2.2): Stop loss distance (× ATR)

• TP Multiplier (1.0): Risk-reward ratio per TP level

• TP Levels (1-5): Number of take profit targets to display

• Show TP/SL Lines: Toggle visual reference lines

SUPPORT & RESISTANCE:

• Pivot Lookback (10): Sensitivity for S/R detection

• Show SR: Toggle support/resistance lines

VWMA BANDS:

• VWMA Length (20): Volume-weighted average period

• Show Bands: Toggle band visibility

TREND DETECTION:

• Trend Threshold (5): Consecutive bars required for trend

PRICE LINES:

• Period (20): High/low calculation lookback

• Show: Toggle price range visualization

DISPLAY OPTIONS:

• Signals: Show/hide BUY/SELL labels

• Table: Show/hide information panel

• Color Bars: Enable trend-based bar coloring

ALERTS:

• Enable: Activate alert notifications for signals

💡 USAGE INSTRUCTIONS

═══════════════════════════════════════════════════════════════════

RECOMMENDED APPROACH:

• Works on all timeframes (1m to Monthly)

• Suitable for all markets (Stocks, Forex, Crypto, etc.)

• Best used with additional analysis and confirmation

• Always practice proper risk management

ENTRY STRATEGY:

1. Wait for BUY or SELL signal to appear

2. Check trend table for trend confirmation

3. Verify VWMA band color matches signal direction

4. Look for nearby support/resistance confluence

5. Consider entering on next candle open

6. Use visual SL level for risk management

EXIT STRATEGY:

1. Use TP levels as potential exit zones

2. Consider scaling out at multiple TP levels

3. Exit on opposite signal

4. Adjust stops as trade progresses

5. Account for spread and slippage

TREND TRADING:

• "Up Trend" → Focus on BUY signals

• "Down Trend" → Focus on SELL signals

• "Ranging" → Wait for clear trend or use range strategies

🎨 VISUAL ELEMENTS

═══════════════════════════════════════════════════════════════════

• GREEN VWMA BANDS → Bullish trend indication

• RED VWMA BANDS → Bearish trend indication

• ORANGE DASHED LINE → Entry price reference

• RED SOLID LINE → Stop loss level

• GREEN DOTTED LINES → Take profit targets

• RED DASHED LINES → Resistance levels

• GREEN DASHED LINES → Support levels

• GREY FILLED AREA → Price high/low range

• GREEN BUY LABEL → Long signal

• RED SELL LABEL → Short signal

• BLUE INFO TABLE → Current trade details

• GREEN/RED BARS → Trend direction (optional)

⚠️ IMPORTANT NOTES

═══════════════════════════════════════════════════════════════════

RISK WARNING:

• Trading involves substantial risk of loss

• You can lose more than your initial investment

• Past performance does not guarantee future results

• No indicator is 100% accurate

• Always use proper position sizing

• Never risk more than you can afford to lose

EDUCATIONAL PURPOSE:

• This tool is for learning and research

• Not a complete trading system

• Should be combined with other analysis

• Requires interpretation and context

• Test thoroughly before live use

• Consider consulting a financial advisor

TECHNICAL LIMITATIONS:

• Signals lag price action (all indicators lag)

• False signals occur in choppy markets

• Works better in trending conditions

• Support/resistance levels are approximate

• TP/SL levels are suggestions, not guarantees

📚 METHODOLOGY

═══════════════════════════════════════════════════════════════════

This indicator combines established technical analysis concepts:

• Price Volume Trend (PVT): Volume-weighted price momentum

• Rate of Change (ROC): Momentum measurement

• Volume-Weighted Moving Average (VWMA): Trend identification

• Average True Range (ATR): Volatility measurement (J. Welles Wilder)

• Pivot Points: Support/resistance detection

All methods are based on publicly available technical analysis

principles. No proprietary or "secret" algorithms are used.

⚖️ FULL DISCLAIMER

═══════════════════════════════════════════════════════════════════

LIABILITY:

The creator (Zakaria Safri) assumes NO liability for:

• Trading losses or damages of any kind

• Loss of capital or profits

• Incorrect signal interpretation

• Technical issues, bugs, or errors

• Any consequences of using this tool

USER RESPONSIBILITY:

By using this indicator, you acknowledge that:

• You are solely responsible for your trading decisions

• You understand the substantial risks involved

• You will not hold the creator liable for losses

• You will conduct your own research and analysis

• You may consult a licensed financial professional

• You are using this tool entirely at your own risk

AS-IS PROVISION:

This indicator is provided "AS IS" without warranty of any kind,

express or implied, including but not limited to warranties of

merchantability, fitness for a particular purpose, or non-infringement.

The creator is not a registered investment advisor, financial planner,

or broker-dealer. This tool is not approved or endorsed by any

financial authority.

📞 ABOUT THE CREATOR

═══════════════════════════════════════════════════════════════════

Created by: Zakaria Safri

Specialization: Technical analysis indicator development

Focus: Multi-factor analysis, risk visualization, trend detection

This is an educational tool designed to demonstrate technical

analysis concepts and multi-factor signal generation methods.

📋 VERSION INFO

═══════════════════════════════════════════════════════════════════

Version: 1.0

Platform: TradingView Pine Script v5

License: Mozilla Public License 2.0

Creator: Zakaria Safri

Year: 2024

═══════════════════════════════════════════════════════════════════

Study Carefully, Trade Wisely, Manage Risk Properly

TradeVision Pro - Educational Trading Tool

Created by Zakaria Safri

═══════════════════════════════════════════════════════════════════

Seasonality Heatmap [QuantAlgo]🟢 Overview

The Seasonality Heatmap analyzes years of historical data to reveal which months and weekdays have consistently produced gains or losses, displaying results through color-coded tables with statistical metrics like consistency scores (1-10 rating) and positive occurrence rates. By calculating average returns for each calendar month and day-of-week combination, it identifies recognizable seasonal patterns (such as which months or weekdays tend to rally versus decline) and synthesizes this into actionable buy low/sell high timing possibilities for strategic entries and exits. This helps traders and investors spot high-probability seasonal windows where assets have historically shown strength or weakness, enabling them to align positions with recurring bull and bear market patterns.

🟢 How It Works

1. Monthly Heatmap

How % Return is Calculated:

The indicator fetches monthly closing prices (or Open/High/Low based on user selection) and calculates the percentage change from the previous month:

(Current Month Price - Previous Month Price) / Previous Month Price × 100

Each cell in the heatmap represents one month's return in a specific year, creating a multi-year historical view

Colors indicate performance intensity: greener/brighter shades for higher positive returns, redder/brighter shades for larger negative returns

What Averages Mean:

The "Avg %" row displays the arithmetic mean of all historical returns for each calendar month (e.g., averaging all Januaries together, all Februaries together, etc.)

This metric identifies historically recurring patterns by showing which months have tended to rise or fall on average

Positive averages indicate months that have typically trended upward; negative averages indicate historically weaker months

Example: If April shows +18.56% average, it means April has averaged a 18.56% gain across all years analyzed

What Months Up % Mean:

Shows the percentage of historical occurrences where that month had a positive return (closed higher than the previous month)

Calculated as:

(Number of Months with Positive Returns / Total Months) × 100

Values above 50% indicate the month has been positive more often than negative; below 50% indicates more frequent negative months

Example: If October shows "64%", then 64% of all historical Octobers had positive returns

What Consistency Score Means:

A 1-10 rating that measures how predictable and stable a month's returns have been

Calculated using the coefficient of variation (standard deviation / mean) - lower variation = higher consistency

High scores (8-10, green): The month has shown relatively stable behavior with similar outcomes year-to-year

Medium scores (5-7, gray): Moderate consistency with some variability

Low scores (1-4, red): High variability with unpredictable behavior across different years

Example: A consistency score of 8/10 indicates the month has exhibited recognizable patterns with relatively low deviation

What Best Means:

Shows the highest percentage return achieved for that specific month, along with the year it occurred

Reveals the maximum observed upside and identifies outlier years with exceptional performance

Useful for understanding the range of possible outcomes beyond the average

Example: "Best: 2016: +131.90%" means the strongest January in the dataset was in 2016 with an 131.90% gain

What Worst Means:

Shows the most negative percentage return for that specific month, along with the year it occurred

Reveals maximum observed downside and helps understand the range of historical outcomes

Important for risk assessment even in months with positive averages

Example: "Worst: 2022: -26.86%" means the weakest January in the dataset was in 2022 with a 26.86% loss

2. Day-of-Week Heatmap

How % Return is Calculated:

Calculates the percentage change from the previous day's close to the current day's price (based on user's price source selection)

Returns are aggregated by day of the week within each calendar month (e.g., all Mondays in January, all Tuesdays in January, etc.)

Each cell shows the average performance for that specific day-month combination across all historical data

Formula:

(Current Day Price - Previous Day Close) / Previous Day Close × 100

What Averages Mean:

The "Avg %" row at the bottom aggregates all months together to show the overall average return for each weekday

Identifies broad weekly patterns across the entire dataset

Calculated by summing all daily returns for that weekday across all months and dividing by total observations

Example: If Monday shows +0.04%, Mondays have averaged a 0.04% change across all months in the dataset

What Days Up % Mean:

Shows the percentage of historical occurrences where that weekday had a positive return

Calculated as:

(Number of Positive Days / Total Days Observed) × 100

Values above 50% indicate the day has been positive more often than negative; below 50% indicates more frequent negative days

Example: If Fridays show "54%", then 54% of all Fridays in the dataset had positive returns

What Consistency Score Means:

A 1-10 rating measuring how stable that weekday's performance has been across different months

Based on the coefficient of variation of daily returns for that weekday across all 12 months

High scores (8-10, green): The weekday has shown relatively consistent behavior month-to-month

Medium scores (5-7, gray): Moderate consistency with some month-to-month variation

Low scores (1-4, red): High variability across months, with behavior differing significantly by calendar month

Example: A consistency score of 7/10 for Wednesdays means they have performed with moderate consistency throughout the year

What Best Means:

Shows which calendar month had the strongest average performance for that specific weekday

Identifies favorable day-month combinations based on historical data

Format shows the month abbreviation and the average return achieved

Example: "Best: Oct: +0.20%" means Mondays averaged +0.20% during October months in the dataset

What Worst Means:

Shows which calendar month had the weakest average performance for that specific weekday

Identifies historically challenging day-month combinations

Useful for understanding which month-weekday pairings have shown weaker performance

Example: "Worst: Sep: -0.35%" means Tuesdays averaged -0.35% during September months in the dataset

3. Optimal Timing Table/Summary Table

→ Best Month to BUY: Identifies the month with the lowest average return (most negative or least positive historically), representing periods where prices have historically been relatively lower

Based on the observation that buying during historically weaker months may position for subsequent recovery

Shows the month name, its average return, and color-coded performance

Example: If May shows -0.86% as "Best Month to BUY", it means May has historically averaged -0.86% in the analyzed period

→ Best Month to SELL: Identifies the month with the highest average return (most positive historically), representing periods where prices have historically been relatively higher

Based on historical strength patterns in that month

Example: If July shows +1.42% as "Best Month to SELL", it means July has historically averaged +1.42% gains

→ 2nd Best Month to BUY: The second-lowest performing month based on average returns

Provides an alternative timing option based on historical patterns

Offers flexibility for staged entries or when the primary month doesn't align with strategy

Example: Identifies the next-most favorable historical buying period

→ 2nd Best Month to SELL: The second-highest performing month based on average returns

Provides an alternative exit timing based on historical data

Useful for staged profit-taking or multiple exit opportunities

Identifies the secondary historical strength period

Note: The same logic applies to "Best Day to BUY/SELL" and "2nd Best Day to BUY/SELL" rows, which identify weekdays based on average daily performance across all months. Days with lowest averages are marked as buying opportunities (historically weaker days), while days with highest averages are marked for selling (historically stronger days).

🟢 Examples

Example 1: NVIDIA NASDAQ:NVDA - Strong May Pattern with High Consistency

Analyzing NVIDIA from 2015 onwards, the Monthly Heatmap reveals May averaging +15.84% with 82% of months being positive and a consistency score of 8/10 (green). December shows -1.69% average with only 40% of months positive and a low 1/10 consistency score (red). The Optimal Timing table identifies December as "Best Month to BUY" and May as "Best Month to SELL." A trader recognizes this high-probability May strength pattern and considers entering positions in late December when prices have historically been weaker, then taking profits in May when the seasonal tailwind typically peaks. The high consistency score in May (8/10) provides additional confidence that this pattern has been relatively stable year-over-year.

Example 2: Crypto Market Cap CRYPTOCAP:TOTALES - October Rally Pattern

An investor examining total crypto market capitalization notices September averaging -2.42% with 45% of months positive and 5/10 consistency, while October shows a dramatic shift with +16.69% average, 90% of months positive, and an exceptional 9/10 consistency score (blue). The Day-of-Week heatmap reveals Mondays averaging +0.40% with 54% positive days and 9/10 consistency (blue), while Thursdays show only +0.08% with 1/10 consistency (yellow). The investor uses this multi-layered analysis to develop a strategy: enter crypto positions on Thursdays during late September (combining the historically weak month with the less consistent weekday), then hold through October's historically strong period, considering exits on Mondays when intraweek strength has been most consistent.

Example 3: Solana BINANCE:SOLUSDT - Extreme January Seasonality

A cryptocurrency trader analyzing Solana observes an extraordinary January pattern: +59.57% average return with 60% of months positive and 8/10 consistency (teal), while May shows -9.75% average with only 33% of months positive and 6/10 consistency. August also displays strength at +59.50% average with 7/10 consistency. The Optimal Timing table confirms May as "Best Month to BUY" and January as "Best Month to SELL." The Day-of-Week data shows Sundays averaging +0.77% with 8/10 consistency (teal). The trader develops a seasonal rotation strategy: accumulate SOL positions during May weakness, hold through the historically strong January period (which has shown this extreme pattern with reasonable consistency), and specifically target Sunday exits when the weekday data shows the most recognizable strength pattern.

Candle Body Break (M/W/D/4H/1H)v5# Candle Body Break (M/W/D/4H/1H) Multi-Timeframe Indicator

This indicator identifies and plots **Candle Body Breaks** across five key timeframes: Monthly (M), Weekly (W), Daily (D), 4-Hour (4H), and 1-Hour (1H).

## Core Logic: Candle Body Break

The core concept is a break in the swing high/low defined by the body of the previous counter-trend candle(s). It focuses purely on **closing price breaks** of remembered highs/lows established by full candle bodies (close > open or close < open).

1. **Remembering the Swing:**

* After a bullish break (upward trend), the indicator waits for the first **bearish (close < open) candle** to appear. This bearish candle's high (`rememberedHigh`) and low (`rememberedLow`) are saved as the **breakout level**.

* Subsequent bearish candles that make a new low update this saved level, continuously adjusting the level to the most significant recent resistance/support established by the body's range.

2. **Executing the Break:**

* **Bull Break (Long signal):** Occurs when a **bullish candle's closing price** exceeds the last remembered bearish high (`rememberedHigh`).

* **Bear Break (Short signal):** Occurs when a **bearish candle's closing price** falls below the last remembered bullish low (`rememberedLow_Bull`).

Once a break occurs, the memory is cleared, and the indicator waits for the next counter-trend candle to establish a new level.

## Features

* **Multi-Timeframe Analysis:** Displays break lines and labels for M, W, D, 4H, and 1H timeframes on any chart.

* **Timeframe Filtering:** Break lines are only shown for timeframes **equal to or higher** than the current chart timeframe (e.g., on a 4H chart, only 4H, D, W, and M breaks are displayed).

* **Candidate Lines (Dotted Green):** Plots the current potential breakout level (the remembered high/low) that must be broken to trigger the next signal.

* **Direction Table:** A table in the top right corner summarizes the latest break direction (⇧ Up / ⇩ Down) for all five timeframes. This can be optionally limited to the 4H chart only.

* **1H Alert:** Triggers an alert when a 1-Hour break is detected.

## Input Settings Translation (for Mod Compliance)

| English Input Text | Original Japanese Text |

| :--- | :--- |

| **Show Monthly Break Lines** | 月足ブレイクを描画する |

| **Show Weekly Break Lines** | 週足ブレイクを描画する |

| **Show Daily Break Lines** | 日足ブレイクを描画する |

| **Show 4-Hour Break Lines** | 4時間足ブレイクを描画する |

| **Show 1-Hour Break Lines** | 1時間足ブレイクを描画する |

| **Show Monthly Candidate Lines** | 月足ブレイク候補ラインを描画する |

| **Show Weekly Candidate Lines** | 週足ブレイク候補ラインを描画する |

| **Show Daily Candidate Lines** | 日足ブレイク候補ラインを描画する |

| **Show 4-Hour Candidate Lines** | 4時間足ブレイク候補ラインを描画する |

| **Show 1-Hour Candidate Lines** | 1時間足ブレイク候補ラインを描画する |

| **Show Only Current TF Candidate Lines** | チャート時間足の候補ラインのみ表示 |

| **Show Table Only on 4H Chart** | テーブルを4Hチャートのみ表示 |

*Please note: The default alert message "1-Hour Break Detected" is also in English.*

※日本語訳

ろうそく足実体ブレイク(M/W/D/4H/1H)マルチタイムフレーム・インジケーター(日本語訳)

このインジケーターは、月足(M)、週足(W)、日足(D)、4時間足(4H)、1時間足(1H)の5つの主要な時間足におけるろうそく足実体ブレイクを検出し、プロットします。

コアロジック:ろうそく足実体ブレイク

このロジックの中核は、直近の**逆行ろうそく足(カウンター・トレンド・キャンドル)**の実体によって定義されたスイングの高値/安値のブレイクです。終値が実体のレンジ外で確定することを純粋に追跡します。

スイングの記憶(Remembering the Swing):

強気のブレイク(上昇トレンド)の後、インジケーターは最初に現れる弱気(終値<始値)のろうそく足を待ちます。この弱気ろうそく足の高値(rememberedHigh)と安値(rememberedLow)が、ブレイクアウトレベルとして保存されます。

その後、安値を更新する弱気ろうそく足が続いた場合、この保存されたレベルが更新され、実体のレンジによって確立された最新の重要なレジスタンス/サポートにレベルが継続的に調整されます。

ブレイクの実行(Executing the Break):

ブルブレイク(買いシグナル): 最後に記憶された弱気ろうそく足の高値(rememberedHigh)を、強気ろうそく足の終値が上回ったときに発生します。

ベアブレイク(売りシグナル): 最後に記憶された強気ろうそく足の安値(rememberedLow_Bull)を、弱気ろうそく足の終値が下回ったときに発生します。

一度ブレイクが発生すると、記憶されたレベルはクリアされ、インジケーターは次の逆行ろうそく足が出現し、新しいレベルを確立するのを待ちます。

機能

マルチタイムフレーム分析: 現在のチャートの時間足に関わらず、M、W、D、4H、1Hのブレイクラインとラベルを表示します。

時間足フィルタリング: ブレイクラインは、現在のチャート時間足と同じか、それよりも上位の時間足のもののみが表示されます(例:4時間足チャートでは、4H、D、W、Mのブレイクのみが表示されます)。

候補ライン(緑の点線): 次のシグナルをトリガーするためにブレイクされる必要がある、現在の潜在的なブレイクアウトレベル(記憶された高値/安値)をプロットします。

方向テーブル: 右上隅のテーブルに、5つの全時間足の最新のブレイク方向(⇧ 上昇 / ⇩ 下降)をまとめて表示します。これは、オプションで4時間足チャートのみに表示するように制限できます。

1時間足アラート: 1時間足のブレイクが検出されたときにアラートをトリガーします。

入力設定の翻訳

コード内の入力設定(UIテキスト)の日本語訳は以下の通りです。

英語の入力テキスト 日本語訳

Show Monthly Break Lines 月足ブレイクを描画する

Show Weekly Break Lines 週足ブレイクを描画する

Show Daily Break Lines 日足ブレイクを描画する

Show 4-Hour Break Lines 4時間足ブレイクを描画する

Show 1-Hour Break Lines 1時間足ブレイクを描画する

Show Monthly Candidate Lines 月足ブレイク候補ラインを描画する

Show Weekly Candidate Lines 週足ブレイク候補ラインを描画する

Show Daily Candidate Lines 日足ブレイク候補ラインを描画する

Show 4-Hour Candidate Lines 4時間足ブレイク候補ラインを描画する

Show 1-Hour Candidate Lines 1時間足ブレイク候補ラインを描画する

Show Only Current TF Candidate Lines チャート時間足の候補ラインのみ表示

Show Table Only on 4H Chart テーブルを4Hチャートのみ表示

Alert Message: 1-Hour Break Detected アラートメッセージ: 1時間足ブレイク発生

Golden Cross Screener [Pineify]Golden Cross Screener Pineify – Multi-Symbol Trend Detection Screener for TradingView

Discover the Golden Cross Screener Pineify for TradingView: a multi-symbol, multi-timeframe indicator for crypto and other assets. Customizable Golden Cross detection, robust algorithm, and intuitive screener design for smarter portfolio trend analysis.

Key Features

Multi-symbol screening across major cryptocurrencies or assets – BTCUSD, ETHUSD, XRPUSD, USDT, BNB, SOLUSD, DOGEUSD, TRXUSD (fully customizable).

Multi-timeframe analysis (e.g., 1m, 5m, 10m, 30m), enabling robust trend detection from scalp to swing.

Customizable Moving Average settings for both Fast and Slow MA (source and length).

Efficient screener table, highlighting Golden Cross events and current asset trends in one panel.

Visual cues for bullish, bearish, and cross states using intuitive color-coding and labels.

Flexible symbol and timeframe inputs to tailor the screener to any portfolio or watchlist.

How It Works

The Golden Cross Screener Pineify leverages the classic Golden Cross methodology—a bullish trend signal triggered when a shorter-term moving average crosses above a longer-term moving average. To improve robustness, you are empowered to configure both Fast MA and Slow MA periods and sources, making the detection logic applicable to any symbol, timeframe, or asset class.

Internally, the script runs dedicated calculations on each chosen symbol and timeframe, generating independent signals using exponential moving averages (EMA). Using the TradingView `request.security` function, it fetches and processes price data for up to eight portfolio assets on four timeframes, displaying the detected Golden Cross, Bullish, or Bearish states in a central screener table.

Trading Ideas and Insights

Spot emerging bullish or bearish trends across your favorite crypto pairs or trading assets in real time.

Capture prime opportunities when multiple assets align with Golden Cross signals—ideal for portfolio rebalancing or rotational strategies.

Analyze trend consistency by monitoring cross events at multiple timeframes for a given asset.

Swiftly identify when short-term and long-term momentum diverge—flagging potential reversals or trend initiations.

The Golden Cross Screener Pineify is not just a trend signal; it’s a holistic multi-asset scanner built for traders who know the power of combining technical breadth with agile timing.

How Multiple Indicators Work Together

This screener stands out with its modular approach: each asset/timeframe pair is monitored in isolation, yet displayed collectively for multidimensional market insight. Each symbol’s price action is processed through independently configured EMAs—Fast and Slow—whose crossovers are analyzed for directional bias. The implementation’s real innovation is in its screener table engine: it aggregates signals, synchronizes timeframes, and color-codes market states, allowing users to see confluences, divergences, and sector trends at a glance.

Combining Golden Cross detection with customizable moving averages and flexible multi-timeframe, multi-symbol scanning means users can fine-tune sensitivity, focus on specific signals, and adapt screener logic for scalping, swing trading, or investing.

Unique Aspects

True multi-symbol screener within the TradingView indicator framework.

Full customization of screener assets, timeframes, and moving averages.

Advanced, efficient use of TradingView table for clear, actionable visualization.

No dependency on standard, static MA settings—adjust everything to match your strategy.

Big-picture and granular trend detection in one tool, designed for both active traders and portfolio managers.

How to Use

Add the Golden Cross Screener Pineify to your TradingView chart.

Choose up to eight symbols—crypto, stock, forex, or custom assets.

Set four timeframes for screening, from lower to higher intervals.

Adjust moving average sources (price, close, etc.) and period lengths for both Fast and Slow MAs to suit your trading style.

Interpret table cells: clear labels and color indicate Golden Cross (trend shift), Bullish (uptrend), Bearish (downtrend) states for each symbol/timeframe.

React to signal alignments—deploy or rebalance positions, increase alert sensitivity, or backtest sequence confluences.

Customization

The indicator’s inputs panel gives full control:

Select which symbols to screen, making it perfect for any asset watchlist.

Pick the desired timeframes—mix daily, hourly, or minute-based intervals.

Adjust Fast and Slow MA settings: switch source type, change period length, and fine-tune detection logic as needed.

Style your screener table via TradingView settings (colors, font sizes, alignment).

Every element is customizable—adapt the Golden Cross Screener Pineify for your specific portfolio, trading timeframe, and strategy focus.

Conclusion

The Golden Cross Screener Pineify elevates multi-symbol trend detection to a new level on TradingView. By combining configurable Golden Cross logic with a powerful screener engine, it serves both precision and broad market insight—crucial for agile traders and strategic portfolio managers. Whether you’re tracking crypto pairs, stocks, forex, or a mix, this tool transforms static trend analysis into an active, multi-dimensional trading edge.

RVol+ Enhanced Relative Volume Indicator📊 RVol+ Enhanced Relative Volume Indicator

Overview

RVol+ (Relative Volume Plus) is an advanced time-based relative volume indicator designed specifically for swing traders and breakout detection. Unlike simple volume comparisons, RVol+ analyzes volume at the same time of day across multiple sessions, providing statistically significant insights into institutional activity and breakout potential.

🎯 Key Features

Core Volume Analysis

Time-Based RVol Calculation - Compares current cumulative volume to the average volume at this exact time over the past N days

Statistical Z-Score - Measures volume in standard deviations from the mean for true anomaly detection

Volume Percentile - Shows where current volume ranks historically (0-100%)

Sustained Volume Filter - 3-bar moving average prevents false signals from single-bar spikes

Breakout Detection

🚀 Confirmed Breakouts - Identifies price breakouts validated by high volume (RVol > 1.5x)

⚠️ False Breakout Warnings - Alerts when price breaks key levels on low volume (high failure risk)

Multi-Timeframe Context - Weekly volume overlay prevents chasing daily noise

Advanced Metrics

OBV Divergence Detection - Spots bullish/bearish accumulation/distribution patterns

Volume Profile Integration - Identifies institutional positioning

Money Flow Analysis - Tracks smart money vs retail activity

Extreme Volume Alerts - 🔥 Labels mark unusual spikes beyond the display cap

Visual Intelligence

Smart Color Coding:

🟢 Bright Teal = High activity (RVol ≥ 1.5x)

🟡 Medium Teal = Caution zone (RVol ≥ 1.2x)

⚪ Light Teal = Normal activity

🟠 Orange = Breakout confirmed

🔴 Red = False breakout risk

Comprehensive Stats Table:

Current Volume (formatted as M/K/B)

RVol ratio

Z-Score with significance

Volume percentile

Historical average and standard deviation

Sustained volume confirmation

📈 How to Use

For Swing Trading (1D - 3W Holds)

Perfect Setup:

✓ RVol > 1.5x (bright teal)

✓ Z-Score > 2.0 (⚡ alert)

✓ Percentile > 90%

✓ Sustained = ✓

✓ 🚀 Breakout label appears

Avoid:

✗ Red "Low Vol" warning during breakouts

✗ RVol < 1.0 at key levels

✗ Sustained volume not confirmed

Signal Interpretation

⚡ Z>2 Labels - Statistically significant volume (95th+ percentile) - highest probability moves

↗️ OBV+ Labels - Bullish accumulation (OBV rising while price consolidates)

↘️ OBV- Labels - Bearish distribution (OBV falling while price rises)

🔵 Blue Background - Weekly volume elevated (confirms daily strength)

⚙️ Customization

Basic Settings

N Day Average - Number of historical days for comparison (default: 5)

RVol Thresholds - Customize highlight levels (default: 1.2x, 1.5x)

Visual Display Cap - Prevent extreme spikes from compressing view (default: 4.0x)

Advanced Metrics (Toggle On/Off)

Z-Score analysis

Weekly RVol context

OBV divergence detection

Volume percentile ranking

Breakout signal generation

Table Customization

Position - 9 placement options to avoid chart overlap

Size - Tiny to Huge

Colors - Full customization of positive/negative/neutral values

Transparency - Adjustable background

Debug Mode

Enable Pine Logs for calculation transparency

Adjustable log frequency

Real-time calculation breakdown

🔬 Technical Details

Algorithm:

Binary search for historical lookups (O(log n) performance)

Time-zone aware session detection

DST-safe timestamp calculations

Exponentially weighted standard deviation

Anti-repainting architecture

Performance:

Optimized for max_bars_back = 5000

Efficient array management

Built-in function optimization

Memory-conscious data structures

📊 What Makes RVol+ Different?

vs. Standard Volume:

Context-aware (time-of-day matters)

Statistical significance testing

False breakout filtering

vs. Basic RVol:

Z-Score normalization (2-3 sigma detection)

Multi-timeframe confirmation

OBV divergence integration

Sustained volume filtering

Smart visual scaling

vs. Professional Tools:

Free and open-source

Fully customizable

No black-box algorithms

Educational debug logs

💡 Best Practices

Wait for Confirmation - Don't enter on first bar; wait for sustained volume ✓

Combine with Price Action - RVol validates, price structure determines entry

Weekly Context Matters - Blue background = institutional interest

Z-Score is King - Focus on ⚡ alerts for highest probability

Avoid Low Volume Breakouts - Red ⚠️ labels = high failure risk

🎓 Trading Psychology

Volume precedes price. When RVol+ shows:

High RVol + Rising OBV = Accumulation before breakout

High RVol at Resistance = Test of conviction

Low RVol on Breakout = Retail-driven (fade candidate)

Z-Score > 3 = Potential "whale" positioning

📝 Credits

Based on the time-based RVol concept from /u/HurlTeaInTheSea, enhanced with:

Statistical analysis (z-scores, percentiles)

Multi-timeframe integration

OBV divergence detection

Professional-grade visualization

Swing trading optimization

🔧 Version History

v2.0 - Enhanced Edition

Added Z-Score analysis

Multi-timeframe volume context

OBV divergence detection

Breakout confirmation system

Smart color coding

Customizable stats table

Debug logging mode

Performance optimizations

📚 Learn More

For optimal use with swing trading:

Combine with support/resistance levels

Watch for volume clusters in consolidation

Use weekly timeframe for trend confirmation

Monitor OBV divergence for early warnings

⚠️ Disclaimer

This indicator is for educational purposes. Volume analysis is one component of trading decisions. Always use proper risk management, consider multiple timeframes, and validate signals with price structure. Past performance does not guarantee future results.

🚀 Getting Started

Add indicator to chart

Adjust "N Day Average" to your preference (5-10 days typical)

Position stats table to avoid overlap

Enable features you want to monitor

Watch for 🚀 breakout confirmations!

Happy Trading! 📈

Intraday Rising & Reversal ScannerPine Script Description: Intraday Rising & Reversal ScannerThis Pine Script is a TradingView indicator designed to identify stocks with intraday (1-hour timeframe) potential for bullish (rising) or bearish (reversal) movements. It scans for stocks based on user-defined technical criteria, including price change, relative volume, RSI, EMA, ATR, and VWAP. The script plots signals on the chart, displays a summary table, and triggers alerts when conditions are met.FeaturesBullish Signal (Rising Stocks):1H Price Change: > 1% (configurable, e.g., >2% for volatile markets).

Relative Volume: > 2.0 (volume is at least twice the 20-period average).

RSI (14): Between 50 and 70 (strong but not overbought momentum).

Price vs EMA 13: Price above the 13-period EMA (confirms short-term uptrend).

ATR (14): Current ATR above its 20-period average (indicates volatility).

VWAP: Price above VWAP (optional, shown on chart for manual confirmation).

Bearish Signal (Reversal Stocks):1H Price Change: < -1% (configurable, e.g., <-2% for stronger reversals).

Relative Volume: > 2.0 (high volume confirms selling pressure).

RSI (14): > 70 (overbought, increasing reversal likelihood).

Price vs EMA 13: Price below the 13-period EMA (confirms short-term downtrend).

ATR (14): Current ATR above its 20-period average (indicates volatility).

VWAP: Price below VWAP (optional, shown on chart for manual confirmation).

Visualization:Bullish Signal: Green triangle below the bar.

Bearish Signal: Red triangle above the bar.

VWAP: Plotted as a blue line for manual verification.

Table: Displays real-time metrics (Change %, Relative Volume, RSI, Price vs EMA, ATR, VWAP) in the top-right corner, color-coded (green for bullish, red for bearish).

Alerts:Separate alerts for bullish ("Intraday Bullish Signal") and bearish ("Intraday Bearish Signal") conditions.

Customizable alert messages include parameter values for easy tracking.

How It WorksThe script runs on the 1-hour (1H) timeframe, ensuring all calculations are based on hourly data.

Indicators are computed:Change %: Percentage price change over the last hour.

Relative Volume: Current volume divided by the 20-period SMA of volume.

RSI: 14-period Relative Strength Index.

EMA 13: 13-period Exponential Moving Average.

ATR: 14-period Average True Range, compared to its 20-period SMA.

VWAP: Volume Weighted Average Price, plotted for visual confirmation.

Signals are generated when all conditions for either bullish or bearish criteria are met.

A table summarizes key metrics, and alerts can be set up for real-time notifications.

Usage InstructionsApply the Script:Open TradingView’s Pine Editor.

Copy and paste the script.

Click "Add to Chart" and set the chart to the 1-hour (1H) timeframe.

Set Up Alerts:Right-click on the chart > "Add Alert".

Select "Intraday Bullish Signal" or "Intraday Bearish Signal" as the condition.

Configure notifications (e.g., SMS, email, or TradingView alerts).

Manual VWAP Check:VWAP is plotted as a blue line. Verify that the price is above VWAP for bullish signals or below for bearish signals using the table or chart.

To make VWAP a mandatory filter, uncomment the VWAP conditions in the bull_signal and bear_signal definitions.

BOCS Channel Scalper Indicator - Mean Reversion Alert System# BOCS Channel Scalper Indicator - Mean Reversion Alert System

## WHAT THIS INDICATOR DOES:

This is a mean reversion trading indicator that identifies consolidation channels through volatility analysis and generates alert signals when price enters entry zones near channel boundaries. **This indicator version is designed for manual trading with comprehensive alert functionality.** Unlike automated strategies, this tool sends notifications (via popup, email, SMS, or webhook) when trading opportunities occur, allowing you to manually review and execute trades. The system assumes price will revert to the channel mean, identifying scalp opportunities as price reaches extremes and preparing to bounce back toward center.

## INDICATOR VS STRATEGY - KEY DISTINCTION:

**This is an INDICATOR with alerts, not an automated strategy.** It does not execute trades automatically. Instead, it:

- Displays visual signals on your chart when entry conditions are met

- Sends customizable alerts to your device/email when opportunities arise

- Shows TP/SL levels for reference but does not place orders

- Requires you to manually enter and exit positions based on signals

- Works with all TradingView subscription levels (alerts included on all plans)

**For automated trading with backtesting**, use the strategy version. For manual control with notifications, use this indicator version.

## ALERT CAPABILITIES:

This indicator includes four distinct alert conditions that can be configured independently:

**1. New Channel Formation Alert**

- Triggers when a fresh BOCS channel is identified

- Message: "New BOCS channel formed - potential scalp setup ready"

- Use this to prepare for upcoming trading opportunities

**2. Long Scalp Entry Alert**

- Fires when price touches the long entry zone

- Message includes current price, calculated TP, and SL levels

- Notification example: "LONG scalp signal at 24731.75 | TP: 24743.2 | SL: 24716.5"

**3. Short Scalp Entry Alert**

- Fires when price touches the short entry zone

- Message includes current price, calculated TP, and SL levels

- Notification example: "SHORT scalp signal at 24747.50 | TP: 24735.0 | SL: 24762.75"

**4. Any Entry Signal Alert**

- Combined alert for both long and short entries

- Use this if you want a single alert stream for all opportunities

- Message: "BOCS Scalp Entry: at "

**Setting Up Alerts:**

1. Add indicator to chart and configure settings

2. Click the Alert (⏰) button in TradingView toolbar

3. Select "BOCS Channel Scalper" from condition dropdown

4. Choose desired alert type (Long, Short, Any, or Channel Formation)

5. Set "Once Per Bar Close" to avoid false signals during bar formation

6. Configure delivery method (popup, email, webhook for automation platforms)

7. Save alert - it will fire automatically when conditions are met

**Alert Message Placeholders:**

Alerts use TradingView's dynamic placeholder system:

- {{ticker}} = Symbol name (e.g., NQ1!)

- {{close}} = Current price at signal

- {{plot_1}} = Calculated take profit level

- {{plot_2}} = Calculated stop loss level

These placeholders populate automatically, creating detailed notification messages without manual configuration.

## KEY DIFFERENCE FROM ORIGINAL BOCS:

**This indicator is designed for traders seeking higher trade frequency.** The original BOCS indicator trades breakouts OUTSIDE channels, waiting for price to escape consolidation before entering. This scalper version trades mean reversion INSIDE channels, entering when price reaches channel extremes and betting on a bounce back to center. The result is significantly more trading opportunities:

- **Original BOCS**: 1-3 signals per channel (only on breakout)

- **Scalper Indicator**: 5-15+ signals per channel (every touch of entry zones)

- **Trade Style**: Mean reversion vs trend following

- **Hold Time**: Seconds to minutes vs minutes to hours

- **Best Markets**: Ranging/choppy conditions vs trending breakouts

This makes the indicator ideal for active day traders who want continuous alert opportunities within consolidation zones rather than waiting for breakout confirmation. However, increased signal frequency also means higher potential commission costs and requires disciplined trade selection when acting on alerts.

## TECHNICAL METHODOLOGY:

### Price Normalization Process:

The indicator normalizes price data to create consistent volatility measurements across different instruments and price levels. It calculates the highest high and lowest low over a user-defined lookback period (default 100 bars). Current close price is normalized using: (close - lowest_low) / (highest_high - lowest_low), producing values between 0 and 1 for standardized volatility analysis.

### Volatility Detection:

A 14-period standard deviation is applied to the normalized price series to measure price deviation from the mean. Higher standard deviation values indicate volatility expansion; lower values indicate consolidation. The indicator uses ta.highestbars() and ta.lowestbars() to identify when volatility peaks and troughs occur over the detection period (default 14 bars).

### Channel Formation Logic:

When volatility crosses from a high level to a low level (ta.crossover(upper, lower)), a consolidation phase begins. The indicator tracks the highest and lowest prices during this period, which become the channel boundaries. Minimum duration of 10+ bars is required to filter out brief volatility spikes. Channels are rendered as box objects with defined upper and lower boundaries, with colored zones indicating entry areas.

### Entry Signal Generation:

The indicator uses immediate touch-based entry logic. Entry zones are defined as a percentage from channel edges (default 20%):

- **Long Entry Zone**: Bottom 20% of channel (bottomBound + channelRange × 0.2)

- **Short Entry Zone**: Top 20% of channel (topBound - channelRange × 0.2)

Long signals trigger when candle low touches or enters the long entry zone. Short signals trigger when candle high touches or enters the short entry zone. Visual markers (arrows and labels) appear on chart, and configured alerts fire immediately.

### Cooldown Filter:

An optional cooldown period (measured in bars) prevents alert spam by enforcing minimum spacing between consecutive signals. If cooldown is set to 3 bars, no new long alert will fire until 3 bars after the previous long signal. Long and short cooldowns are tracked independently, allowing both directions to signal within the same period.

### ATR Volatility Filter:

The indicator includes a multi-timeframe ATR filter to avoid alerts during low-volatility conditions. Using request.security(), it fetches ATR values from a specified timeframe (e.g., 1-minute ATR while viewing 5-minute charts). The filter compares current ATR to a user-defined minimum threshold:

- If ATR ≥ threshold: Alerts enabled

- If ATR < threshold: No alerts fire

This prevents notifications during dead zones where mean reversion is unreliable due to insufficient price movement. The ATR status is displayed in the info table with visual confirmation (✓ or ✗).

### Take Profit Calculation:

Two TP methods are available:

**Fixed Points Mode**:

- Long TP = Entry + (TP_Ticks × syminfo.mintick)

- Short TP = Entry - (TP_Ticks × syminfo.mintick)

**Channel Percentage Mode**:

- Long TP = Entry + (ChannelRange × TP_Percent)

- Short TP = Entry - (ChannelRange × TP_Percent)

Default 50% targets the channel midline, a natural mean reversion target. These levels are displayed as visual lines with labels and included in alert messages for reference when manually placing orders.

### Stop Loss Placement:

Stop losses are calculated just outside the channel boundary by a user-defined tick offset:

- Long SL = ChannelBottom - (SL_Offset_Ticks × syminfo.mintick)

- Short SL = ChannelTop + (SL_Offset_Ticks × syminfo.mintick)

This logic assumes channel breaks invalidate the mean reversion thesis. SL levels are displayed on chart and included in alert notifications as suggested stop placement.

### Channel Breakout Management:

Channels are removed when price closes more than 10 ticks outside boundaries. This tolerance prevents premature channel deletion from minor breaks or wicks, allowing the mean reversion setup to persist through small boundary violations.

## INPUT PARAMETERS:

### Channel Settings:

- **Nested Channels**: Allow multiple overlapping channels vs single channel

- **Normalization Length**: Lookback for high/low calculation (1-500, default 100)

- **Box Detection Length**: Period for volatility detection (1-100, default 14)

### Scalping Settings:

- **Enable Long Scalps**: Toggle long alert generation on/off

- **Enable Short Scalps**: Toggle short alert generation on/off

- **Entry Zone % from Edge**: Size of entry zone (5-50%, default 20%)

- **SL Offset (Ticks)**: Distance beyond channel for stop (1+, default 5)

- **Cooldown Period (Bars)**: Minimum spacing between alerts (0 = no cooldown)

### ATR Filter:

- **Enable ATR Filter**: Toggle volatility filter on/off

- **ATR Timeframe**: Source timeframe for ATR (1, 5, 15, 60 min, etc.)

- **ATR Length**: Smoothing period (1-100, default 14)

- **Min ATR Value**: Threshold for alert enablement (0.1+, default 10.0)

### Take Profit Settings:

- **TP Method**: Choose Fixed Points or % of Channel

- **TP Fixed (Ticks)**: Static distance in ticks (1+, default 30)

- **TP % of Channel**: Dynamic target as channel percentage (10-100%, default 50%)

### Appearance:

- **Show Entry Zones**: Toggle zone labels on channels

- **Show Info Table**: Display real-time indicator status

- **Table Position**: Corner placement (Top Left/Right, Bottom Left/Right)

- **Long Color**: Customize long signal color (default: darker green for readability)

- **Short Color**: Customize short signal color (default: red)

- **TP/SL Colors**: Customize take profit and stop loss line colors

- **Line Length**: Visual length of TP/SL reference lines (5-200 bars)

## VISUAL INDICATORS:

- **Channel boxes** with semi-transparent fill showing consolidation zones

- **Colored entry zones** labeled "LONG ZONE ▲" and "SHORT ZONE ▼"

- **Entry signal arrows** below/above bars marking long/short alerts

- **TP/SL reference lines** with emoji labels (⊕ Entry, 🎯 TP, 🛑 SL)

- **Info table** showing channel status, last signal, entry/TP/SL prices, risk/reward ratio, and ATR filter status

- **Visual confirmation** when alerts fire via on-chart markers synchronized with notifications

## HOW TO USE:

### For 1-3 Minute Scalping with Alerts (NQ/ES):

- ATR Timeframe: "1" (1-minute)

- ATR Min Value: 10.0 (for NQ), adjust per instrument

- Entry Zone %: 20-25%

- TP Method: Fixed Points, 20-40 ticks

- SL Offset: 5-10 ticks

- Cooldown: 2-3 bars to reduce alert spam

- **Alert Setup**: Configure "Any Entry Signal" for combined long/short notifications

- **Execution**: When alert fires, verify chart visuals, then manually place limit order at entry zone with provided TP/SL levels

### For 5-15 Minute Day Trading with Alerts:

- ATR Timeframe: "5" or match chart

- ATR Min Value: Adjust to instrument (test 8-15 for NQ)

- Entry Zone %: 20-30%

- TP Method: % of Channel, 40-60%

- SL Offset: 5-10 ticks

- Cooldown: 3-5 bars

- **Alert Setup**: Configure separate "Long Scalp Entry" and "Short Scalp Entry" alerts if you trade directionally based on bias

- **Execution**: Review channel structure on alert, confirm ATR filter shows ✓, then enter manually

### For 30-60 Minute Swing Scalping with Alerts:

- ATR Timeframe: "15" or "30"

- ATR Min Value: Lower threshold for broader market

- Entry Zone %: 25-35%

- TP Method: % of Channel, 50-70%

- SL Offset: 10-15 ticks

- Cooldown: 5+ bars or disable

- **Alert Setup**: Use "New Channel Formation" to prepare for setups, then "Any Entry Signal" for execution alerts

- **Execution**: Larger timeframes allow more analysis time between alert and entry

### Webhook Integration for Semi-Automation:

- Configure alert webhook URL to connect with platforms like TradersPost, TradingView Paper Trading, or custom automation

- Alert message includes all necessary order parameters (direction, entry, TP, SL)

- Webhook receives structured data when signal fires

- External platform can auto-execute based on alert payload

- Still maintains manual oversight vs full strategy automation

## USAGE CONSIDERATIONS:

- **Manual Discipline Required**: Alerts provide opportunities but execution requires judgment. Not all alerts should be taken - consider market context, trend, and channel quality

- **Alert Timing**: Alerts fire on bar close by default. Ensure "Once Per Bar Close" is selected to avoid false signals during bar formation

- **Notification Delivery**: Mobile/email alerts may have 1-3 second delay. For immediate execution, use desktop popups or webhook automation

- **Cooldown Necessity**: Without cooldown, rapidly touching price action can generate excessive alerts. Start with 3-bar cooldown and adjust based on alert volume

- **ATR Filter Impact**: Enabling ATR filter dramatically reduces alert count but improves quality. Track filter status in info table to understand when you're receiving fewer alerts

- **Commission Awareness**: High alert frequency means high potential trade count. Calculate if your commission structure supports frequent scalping before acting on all alerts

## COMPATIBLE MARKETS:

Works on any instrument with price data including stock indices (NQ, ES, YM, RTY), individual stocks, forex pairs (EUR/USD, GBP/USD), cryptocurrency (BTC, ETH), and commodities. Volume-based features are not included in this indicator version. Multi-timeframe ATR requires higher-tier TradingView subscription for request.security() functionality on timeframes below chart timeframe.

## KNOWN LIMITATIONS:

- **Indicator does not execute trades** - alerts are informational only; you must manually place all orders

- **Alert delivery depends on TradingView infrastructure** - delays or failures possible during platform issues

- **No position tracking** - indicator doesn't know if you're in a trade; you must manage open positions independently

- **TP/SL levels are reference only** - you must manually set these on your broker platform; they are not live orders

- **Immediate touch entry can generate many alerts** in choppy zones without adequate cooldown

- **Channel deletion at 10-tick breaks** may be too aggressive or lenient depending on instrument tick size

- **ATR filter from lower timeframes** requires TradingView Premium/Pro+ for request.security()

- **Mean reversion logic fails** in strong breakout scenarios - alerts will fire but trades may hit stops

- **No partial closing capability** - full position management is manual; you determine scaling out

- **Alerts do not account for gaps** or overnight price changes; morning alerts may be stale

## RISK DISCLOSURE:

Trading involves substantial risk of loss. This indicator provides signals for educational and informational purposes only and does not constitute financial advice. Past performance does not guarantee future results. Mean reversion strategies can experience extended drawdowns during trending markets. Alerts are not guaranteed to be profitable and should be combined with your own analysis. Stop losses may not fill at intended levels during extreme volatility or gaps. Never trade with capital you cannot afford to lose. Consider consulting a licensed financial advisor before making trading decisions. Always verify alerts against current market conditions before executing trades manually.

## ACKNOWLEDGMENT & CREDITS: