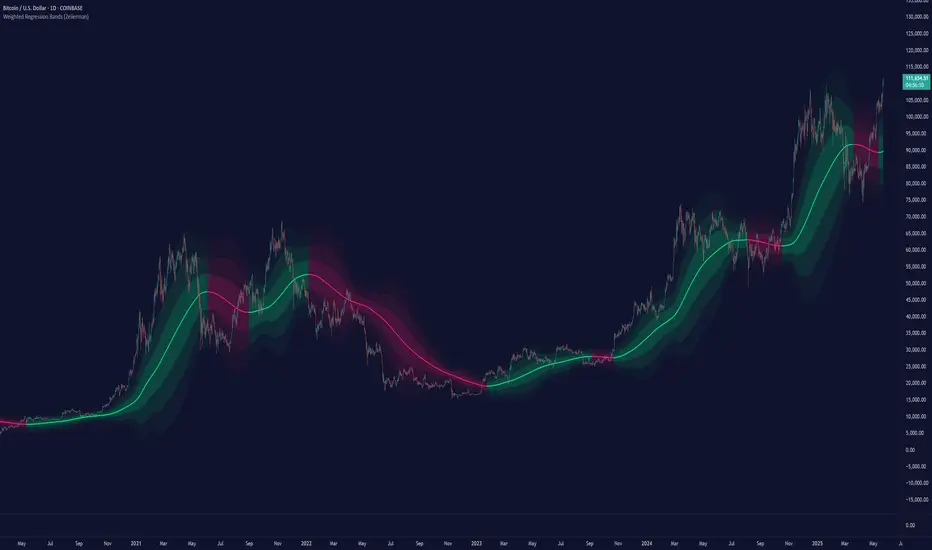

Quantum Harmonic Oscillator Overlay🧪 Quantum Harmonic Oscillator Overlay

A visual model of price behavior using quantum harmonic oscillation principles

📜 Indicator Overview

The Quantum Harmonic Oscillator Overlay applies concepts from both classical physics (harmonic motion) and quantum mechanics (energy states) to model and visualize how price orbits around a central trend line. It overlays a Linear Regression line (representing the “mean position” or ground state of price) and calculates surrounding energy levels (σ-zones) akin to quantum shells that price can "jump" between.

This indicator is particularly useful for visualizing mean reversion, volatility compression/expansion, and momentum-driven price breakthroughs.

🧠 Core Concepts

Linear Regression Line (LSR): This is the calculated center of gravity or equilibrium path of price over a user-defined period. Think of it like the lowest energy state or central axis around which price vibrates.

Standard Deviation Zones (σ-levels):

1σ: The majority of normal price activity; within this range, price tends to fluctuate if in balance.

2σ: Indicates volatility or possible breakout pressure.

3σ: Represents extreme movement — a phase shift in energy, potentially leading to reversal or continuation with higher momentum.

Quantum Analogy: Just like in a quantum harmonic oscillator, particles (here, prices) move probabilistically between discrete energy states. The further the price moves from the center, the more "energy" (momentum, volume, volatility) is implied.

⚙️ Input Parameters

Setting Description

Linear Regression Length The number of bars used to calculate the regression trend (default 100). Affects the central path and responsiveness.

σ Multipliers (1σ, 2σ, 3σ) Determine how far each band is from the regression line. Adjusting these can highlight different price behaviors.

Show Energy Level Zones Toggle visibility of the colored bands around the regression line.

Show LSR Center Line Toggles visibility of the white Linear Regression line itself.

🎨 Visual Components

Color Zone Interpretation

✅ Green ±1σ Normal oscillation / mean reversion area. Ideal for range-bound strategies.

🟧 Orange ±2σ Warning zone; price may be gaining momentum or volatility.

🔴 Red ±3σ High-momentum state or anomaly. These regions may imply trend exhaustion, reversals, or breakouts.

White Line: The LSR — the average trajectory of the price movement.

Pink Dots: Appear when price exceeds Zone 3 (outside ±3σ) — a signal of extreme behavior or a possible regime shift.

📈 How to Use This Indicator

1. Detect Overextensions

When price touches or breaches the 3σ zone, it is likely overextended. This can be used to anticipate potential snapbacks or strong breakout trends.

2. Identify Mean Reversion Trades

If price exits the 2σ or 3σ zones and returns toward the center line, this signals a likely mean reversion setup.

3. Volatility Compression or Expansion

Flat zones between σ levels suggest calm markets; widening bands suggest expanding volatility.

4. Use with Confirmation Tools

Combine with momentum oscillators (MACD, RSI) or volume-based signals to confirm reversals or continuation outside Zone 3.

🔮 Philosophical Note

This indicator embodies the metaphor that the market behaves like a quantum oscillator — price particles exist in a probabilistic field and jump between discrete zones of volatility and energy. Tracking these transitions allows the trader to see price behavior as rhythmic, wave-like, and multidimensional rather than purely linear.

Regressions

Asset Premium/Discount Monitor📊 Overview

The Asset Premium/Discount Monitor is a tool for analyzing the relative value between two correlated assets. It measures when one asset is trading at a premium or discount compared to its historical relationship with another asset, helping traders identify potential mean reversion opportunities, or pairs trading opportunities.

🎯 Use Cases

Perfect for analyzing:

NASDAQ:MSTR vs CRYPTO:BTCUSD - MicroStrategy's premium/discount to Bitcoin

NASDAQ:COIN vs BITSTAMP:BTCUSD - Coinbase's relative value to Bitcoin

NASDAQ:TSLA vs NASDAQ:QQQ - Tesla's premium to tech sector

Regional banks AMEX:KRE vs AMEX:XLF - Individual bank stocks vs financial sector

Any two correlated assets where relative value matters

Example of a trade: MSTR vs BTC - When indicator shows MSTR at 95% percentile (extreme premium): Short MSTR, Buy BTC. Then exit when the spread reverts to the mean, say 40-60% percentile.

🔧 How It Works

Core Calculation

Ratio Analysis: Calculates the price ratio between your asset and the correlated asset

Historical Baseline: Establishes the "normal" relationship using a 252-day moving average. You can change this.

Premium Measurement: Measures current deviation from historical average as a percentage

Statistical Context: Provides percentile rankings and standard deviation bands

The Math

Premium % = (Current Ratio / Historical Average Ratio - 1) × 100

🎨 Customization Options

Correlated Asset: Choose any symbol for comparison

Lookback Period: Adjust historical baseline (50-1000 days)

Smoothing: Reduce noise with moving average (1-50 days)

Visual Toggles: Show/hide bands and percentile lines

Color Themes: Customize premium/discount colors

📊 Interpretation Guide

Premium/Discount Reading

Positive %: Asset trading above historical relationship (premium)

Negative %: Asset trading below historical relationship (discount)

Near 0%: Asset at fair value relative to correlation

Percentile Ranking

90%+: Near recent highs - potential selling opportunity

10% and below: Near recent lows - potential buying opportunity

25-75%: Normal trading range

Signal Classifications

🔴 SELL PREMIUM: Asset expensive relative to recent range

🟡 Premium Rich: Moderately expensive, monitor for reversal

⚪ NEUTRAL: Fair value territory

🟡 Discount Opportunity: Moderately cheap, potential accumulation zone

🟢 BUY DISCOUNT: Asset cheap relative to recent range

🚨 Built-in Alerts

Extreme Premium Alert: Triggers when percentile > 95%

Extreme Discount Alert: Triggers when percentile < 5%

⚠️ Important Notes

Works best with highly correlated assets

Historical relationships can change - monitor correlation strength

Not investment advice - use as one factor in your analysis

Backtest thoroughly before implementing any strategy

🔄 Updates & Future Features

This indicator will be continuously improved based on user feedback. So... please give me your feedback!

Logistic Regression ICT FVG🚀 OVERVIEW

Welcome to the Logistic Regression Fair Value Gap (FVG) System — a next-gen trading tool that blends precision gap detection with machine learning intelligence.

Unlike traditional FVG indicators, this one evolves with each bar of price action, scoring and filtering gaps based on real market behavior.

🔧 CORE FEATURES

✨ Smart Gap Detection

Automatically identifies bullish and bearish Fair Value Gaps using volatility-aware candle logic.

📊 Probability-Based Filtering

Uses logistic regression to assign each gap a confidence score (0 to 1), showing only high-probability setups.

🔁 Real-Time Retest Tracking

Continuously watches how price interacts with each gap to determine if it deserves respect.

📈 Multi-Factor Assessment

Evaluates RSI, MACD, and body size at gap formation to build a full context snapshot.

🧠 Self-Learning Engine

The logistic regression model updates on each bar using gradient descent, refining its predictions over time.

📢 Built-In Alerts

Get instant alerts when a gap forms, gets retested, or breaks.

🎨 Custom Display Options

Control the color of bullish/bearish zones, and toggle on/off probability labels for cleaner charts.

🚩 WHAT MAKES IT DIFFERENT

This isn’t just another box-drawing indicator.

While others mark every imbalance, this system thinks before it draws — using statistical modeling to filter out noise and prioritize high-impact zones.

By learning from how price behaves around gaps (not just how they form), it helps you trade only what matters — not what clutters.

⚙️ HOW IT WORKS

1️⃣ Detection

FVGs are identified using ATR-based thresholds and sharp wick imbalances.

2️⃣ Behavior Monitoring

Every gap is tracked — and if respected enough times, it becomes part of the elite training set.

3️⃣ Context Capture

Each new FVG logs RSI, MACD, and body size to provide a feature-rich context for prediction.

4️⃣ Prediction (Logistic Regression)

The model predicts how likely the gap is to be respected and assigns it a probability score.

5️⃣ Classification & Alerts

Gaps above the threshold are plotted with score labels, and alerts trigger for entry/respect/break.

⚙️ CONFIGURATION PANEL

🔧 System Inputs

• Max Retests – How many times a gap must be respected to train the model

• Prediction Threshold – Minimum score to show a gap on the chart

• Learning Rate – Controls how fast the model adapts (default: 0.009)

• Max FVG Lifetime – Expiration duration for unused gaps

• Show Historic Gaps – Show/hide expired or invalidated gaps

🎨 Visual Options

• Bullish/Bearish Colors – Set gap colors to fit your chart style

• Confidence Labels – Show probability scores next to FVGs

• Alert Toggles – Enable alerts for:

– New FVG detected

– FVG respected (entry)

– FVG invalidated (break)

💡 WHY LOGISTIC REGRESSION?

Traditional FVG tools rely on candle shapes.

This system relies on probability — by training on RSI, MACD, and price behavior, it predicts whether a gap will act as a true liquidity zone.

Logistic regression lets the system continuously adapt using new data, making it more accurate the longer it runs.

That means smarter signals, fewer false positives, and a clearer view of where real opportunities lie.

Momentum Regression [BackQuant]Momentum Regression

The Momentum Regression is an advanced statistical indicator built to empower quants, strategists, and technically inclined traders with a robust visual and quantitative framework for analyzing momentum effects in financial markets. Unlike traditional momentum indicators that rely on raw price movements or moving averages, this tool leverages a volatility-adjusted linear regression model (y ~ x) to uncover and validate momentum behavior over a user-defined lookback window.

Purpose & Design Philosophy

Momentum is a core anomaly in quantitative finance — an effect where assets that have performed well (or poorly) continue to do so over short to medium-term horizons. However, this effect can be noisy, regime-dependent, and sometimes spurious.

The Momentum Regression is designed as a pre-strategy analytical tool to help you filter and verify whether statistically meaningful and tradable momentum exists in a given asset. Its architecture includes:

Volatility normalization to account for differences in scale and distribution.

Regression analysis to model the relationship between past and present standardized returns.

Deviation bands to highlight overbought/oversold zones around the predicted trendline.

Statistical summary tables to assess the reliability of the detected momentum.

Core Concepts and Calculations

The model uses the following:

Independent variable (x): The volatility-adjusted return over the chosen momentum period.

Dependent variable (y): The 1-bar lagged log return, also adjusted for volatility.

A simple linear regression is performed over a large lookback window (default: 1000 bars), which reveals the slope and intercept of the momentum line. These values are then used to construct:

A predicted momentum trendline across time.

Upper and lower deviation bands , representing ±n standard deviations of the regression residuals (errors).

These visual elements help traders judge how far current returns deviate from the modeled momentum trend, similar to Bollinger Bands but derived from a regression model rather than a moving average.

Key Metrics Provided

On each update, the indicator dynamically displays:

Momentum Slope (β₁): Indicates trend direction and strength. A higher absolute value implies a stronger effect.

Intercept (β₀): The predicted return when x = 0.

Pearson’s R: Correlation coefficient between x and y.

R² (Coefficient of Determination): Indicates how well the regression line explains the variance in y.

Standard Error of Residuals: Measures dispersion around the trendline.

t-Statistic of β₁: Used to evaluate statistical significance of the momentum slope.

These statistics are presented in a top-right summary table for immediate interpretation. A bottom-right signal table also summarizes key takeaways with visual indicators.

Features and Inputs

✅ Volatility-Adjusted Momentum : Reduces distortions from noisy price spikes.

✅ Custom Lookback Control : Set the number of bars to analyze regression.

✅ Extendable Trendlines : For continuous visualization into the future.

✅ Deviation Bands : Optional ±σ multipliers to detect abnormal price action.

✅ Contextual Tables : Help determine strength, direction, and significance of momentum.

✅ Separate Pane Design : Cleanly isolates statistical momentum from price chart.

How It Helps Traders

📉 Quantitative Strategy Validation:

Use the regression results to confirm whether a momentum-based strategy is worth pursuing on a specific asset or timeframe.

🔍 Regime Detection:

Track when momentum breaks down or reverses. Slope changes, drops in R², or weak t-stats can signal regime shifts.

📊 Trade Filtering:

Avoid false positives by entering trades only when momentum is both statistically significant and directionally favorable.

📈 Backtest Preparation:

Before running costly simulations, use this tool to pre-screen assets for exploitable return structures.

When to Use It

Before building or deploying a momentum strategy : Test if momentum exists and is statistically reliable.

During market transitions : Detect early signs of fading strength or reversal.

As part of an edge-stacking framework : Combine with other filters such as volatility compression, volume surges, or macro filters.

Conclusion

The Momentum Regression indicator offers a powerful fusion of statistical analysis and visual interpretation. By combining volatility-adjusted returns with real-time linear regression modeling, it helps quantify and qualify one of the most studied and traded anomalies in finance: momentum.

Navy Seal Trading - EdgarTrader📌 Navy Seal Trading – Asia, London, and NY Sessions

This indicator clearly displays the ranges of the Asia, London, and New York sessions, featuring:

✅ Full range visualization for each session

✅ Asia session high, low, and midline, with extended projection lines for precise reaction analysis

✅ Clean, minimalistic, and professional colors to keep your chart focused

🔷 Designed for the Navy Seal Trading community, focused on precision, discipline, and professional execution in the markets.

Use it to:

✔️ Mark liquidity zones

✔️ Identify Asia manipulation ranges

✔️ Prepare executions in London and NY with clear context

💡 Remember: Clarity in your zones gives you the confidence and discipline to execute like a true Navy Seal Trader.

LANZ Strategy 1.0🔷 LANZ Strategy 1.0 — Session-Based Directional Logic with Visual Multi-Account Risk Management

LANZ Strategy 1.0 is a structured and disciplined trading strategy designed for the 1-hour timeframe, operating during the NY session and executing trades overnight. It uses the directional behavior between 08:00 and 18:00 New York time to define precise limit entries for the following night. Ideal for traders who prefer time-based execution, clear visuals, and professional risk management across multiple accounts.

🧠 Core Components:

1. Session Direction Confirmation:

At 18:00 NY, the system evaluates the market direction by comparing the open at 08:00 vs the close at 18:00:

If the direction matches the previous day, it is reversed.

If it differs, the current day’s direction is kept.

This logic is designed to avoid trend exhaustion and favor potential reversal opportunities.

2. EP Level & Risk Definition:

Once direction is defined:

For BUY, EP is set at the Low of the session.

For SELL, EP is set at the High of the session.

The system automatically plots:

SL fixed at 18 pips from EP

TP at 3.00× the risk → 54 pips from EP

All levels (EP, SL, TP) are shown with visual lines and price labels.

3. Time-Restricted Entry Execution:

The entry is only valid if price touches the EP between 19:00 and 08:00 NY.

If EP is not touched before 08:00 NY, the trade is automatically cancelled.

4. Multi-Account Lot Sizing:

Traders can configure up to five different accounts, each with its own capital and risk percentage.

The system calculates and displays the lot size per account, based on SL distance and pip value, in a dynamic floating label.

5. Outcome Tracking:

If TP is hit, a +3.00% profit label is displayed along with a congratulatory alert.

If SL is hit, a -1.00% label appears with a loss alert.

If the trade is still open by 09:00 NY, it is manually closed, and the result is shown as a percentage of the initial risk.

📊 Visual Features:

Custom-colored angle and guide lines.

Dynamic angle line starts at 08:00 NY and tracks price until 18:00.

Shaded backgrounds for key time zones (e.g., 08:00, 18:00, 19:00).

BUY/SELL signals shown at 19:00 based on match/divergence logic.

Label panel showing risk metrics and lot size for each active account.

⚙️ How It Works:

08:00 NY: Marks the session open and initiates a dynamic angle line.

18:00 NY: Evaluates the session direction and calculates EP/SL/TP based on outcome.

19:00 NY: Activates limit order monitoring.

During the night (until 08:00 NY): If EP is touched, the trade is triggered.

At 08:00 NY: If no touch occurred, trade is cancelled.

Overnight: TP/SL logic is enforced, showing percentage outcomes.

At 09:00 NY: If still open, trade is closed manually and result is labeled visually.

🔔 Alerts:

🚀 EP execution alert when touched

💢 Stop Loss hit alert

⚡ Take Profit hit alert

✅ Manual close at 09:00 NY with performance result

🔔 Daily reminder at 19:00 NY to configure and prepare the trade

📝 Notes:

Strategy is exclusive to the 1-hour timeframe.

Works best on assets with clean NY session movement.

Perfect for structured, semi-automated swing/overnight trading styles.

Fully visual, self-explanatory, and backtest-friendly.

👨💻 Credits:

Developed by LANZ

A strategy created with precision, discipline, and a vision for traders who value time-based entries, clean execution logic, and visual confidence on the chart.

Special thanks to Kairos — your AI assistant — for the detailed structure, scripting, and documentation of the strategy.

CAGR + Log Slope ColorThis custom TradingView indicator combines two important analytical concepts to help traders identify strong trends with visual clarity:

CAGR (Compound Annual Growth Rate):

Measures the geometric average annual return of the asset over a specified period. It smooths out short-term fluctuations and provides a long-term growth perspective.

Logarithmic Slope Coloring:

The slope of the log-scaled price is calculated and visualized with color gradients. Steeper upward slopes indicate stronger momentum and are highlighted with more intense colors. Downward slopes are shown in contrasting colors for easier identification of bearish trends.

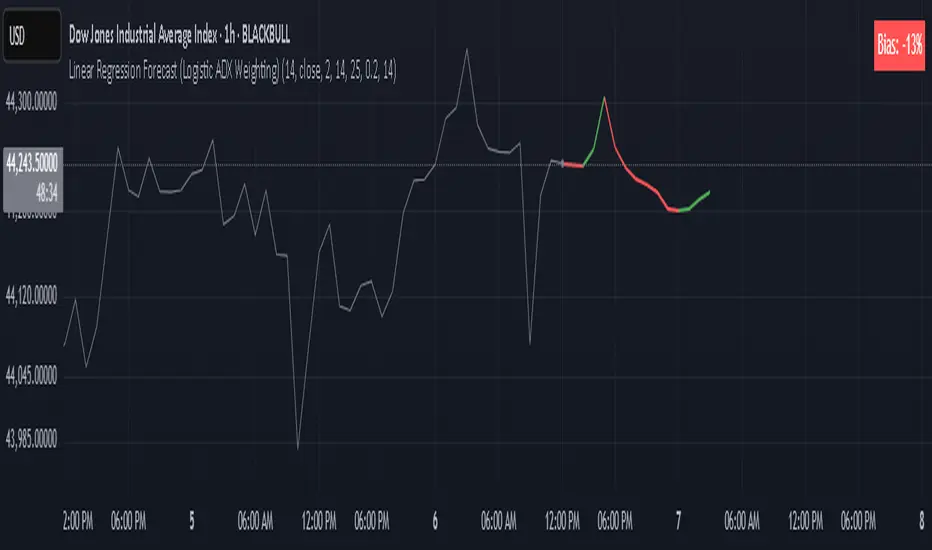

Linear Regression Forecast (ADX Adaptive)Linear Regression Forecast (ADX Adaptive)

This indicator is a dynamic price projection tool that combines multiple linear regression forecasts into a single, adaptive forecast curve. By integrating trend strength via the ADX and directional bias, it aims to visualize how price might evolve in different market environments—from strong trends to mean-reverting conditions.

Core Concept:

This tool builds forward price projections based on a blend of linear regression models with varying lookback lengths (from 2 up to a user-defined max). It then adjusts those projections using two key mechanisms:

ADX-Weighted Forecast Blending

In trending conditions (high ADX), the model follows the raw forecast direction. In ranging markets (low ADX), the forecast flips or reverts, biasing toward mean-reversion. A logistic transformation of directional bias, controlled by a steepness parameter, determines how aggressively this blending reacts to price behavior.

Volatility Scaling

The forecast’s magnitude is scaled based on ADX and directional conviction. When trends are unclear (low ADX or neutral bias), the projection range expands to reflect greater uncertainty and volatility.

How It Works:

Regression Curve Generation

For each regression length from 2 to maxLength, a forward projection is calculated using least-squares linear regression on the selected price source. These forecasts are extrapolated into the future.

Directional Bias Calculation

The forecasted points are analyzed to determine a normalized bias value in the range -1 to +1, where +1 means strongly bullish, -1 means strongly bearish, and 0 means neutral.

Logistic Bias Transformation

The raw bias is passed through a logistic sigmoid function, with a user-defined steepness. This creates a probability-like weight that favors either following or reversing the forecast depending on market context.

ADX-Based Weighting

ADX determines the weighting between trend-following and mean-reversion modes. Below ADX 20, the model favors mean-reversion. Above 25, it favors trend-following. Between 20 and 25, it linearly blends the two.

Blended Forecast Curve

Each forecast point is blended between trend-following and mean-reverting values, scaled for volatility.

What You See:

Forecast Lines: Projected future price paths drawn in green or red depending on direction.

Bias Plot: A separate plot showing post-blend directional bias as a percentage, where +100 is strongly bullish and -100 is strongly bearish.

Neutral Line: A dashed horizontal line at 0 percent bias to indicate neutrality.

User Inputs:

-Max Regression Length

-Price Source

-Line Width

-Bias Steepness

-ADX Length and Smoothing

Use Cases:

Visualize expected price direction under different trend conditions

Adjust trading behavior depending on trending vs ranging markets

Combine with other tools for deeper analysis

Important Notes:

This indicator is for visualization and analysis only. It does not provide buy or sell signals and should not be used in isolation. It makes assumptions based on historical price action and should be interpreted with market context.

Zero-Lag Linear Regression Candles🚀 Zero-Lag Linear Regression Candles

📊 What It Does

The Zero-Lag Linear Regression Candles change traditional candlestick analysis by creating smoothed, predictive candles that eliminate the lag inherent in standard linear regression methods. Instead of waiting for price confirmation, this indicator anticipates market movements using advanced mathematical modeling.

🎯 Key Features

Tri-Layer Super Responsive System

Layer 1: Weighted Linear Regression with exponential decay weighting

Layer 2: Zero-lag correction algorithm that projects future price direction

Layer 3: Adaptive intelligence that adjusts to current market volatility and momentum

Smart Market Adaptation

Automatically adjusts sensitivity based on market volatility (ATR)

Responds to momentum changes in real-time

Filters out market noise while preserving important signals

Customizable

Regression Length: Fine-tune responsiveness (2-50 periods)

Weight Decay Factor: Control how much emphasis to place on recent vs. historical data

Zero-Lag Periods: Adjust the aggressiveness of lag elimination

Adaptive Factor: Set market adaptation strength

🛠️ Usage Instructions

1. Add to Chart: Apply the indicator to any timeframe

2. Configure Settings: Adjust regression length and sensitivity to match your trading style

3. Interpret Signals:

- Green Candles: Bullish linear regression trend

- Red Candles: Bearish linear regression trend

Created by B3AR_Trades

LRHA Trend Shift DetectorLRHA Trend Shift Detector (TSD)

The LRHA Trend Shift Detector is an advanced momentum exhaustion indicator that identifies potential trend reversals and changes by analyzing Linear Regression Heikin Ashi (LRHA) candle patterns. TSD focuses on detecting when strong directional moves begin to lose momentum.

🔬 Methodology

The indicator employs a three-stage detection process:

LRHA Calculation: Applies linear regression smoothing to Heikin Ashi candles, creating ultra-smooth trend-following candles that filter out market noise

Extended Move Detection: Identifies sustained directional moves by counting consecutive bullish or bearish LRHA candles

Momentum Exhaustion Analysis: Monitors for significant changes in candle size compared to recent averages

When an extended move shows clear signs of momentum exhaustion, the indicator signals a potential trend shift with red dots plotted above or below your candlesticks.

⚙️ Parameters

Core Settings

LRHA Length (11): Linear regression period for smoothing calculations. Lower values = more responsive, higher values = smoother trends.

Minimum Trend Bars (4): Consecutive candles required to establish an "extended move." Higher number detects longer term trend changes.

Exhaustion Bars (3): Number of consecutively smaller candles needed to signal exhaustion. Lower is more sensitive.

Size Reduction Threshold (40%): Percentage decrease in candle size to qualify as "exhaustion." Lower is more sensitive.

Trend Trading

Pullback Entries: Identify exhaustion in counter-trend moves for trend continuation

Exit Strategy: Recognize when main trend momentum is fading

Position Sizing: Reduce size when seeing exhaustion in your direction

🎛️ Optimization Tips

For More Signals (Aggressive)

- Decrease LRHA Length (7-9)

- Reduce Minimum Trend Bars (2-3)

- Lower Size Reduction Threshold (25-35%)

For Higher Quality (Conservative)

- Increase LRHA Length (13-18)

- Raise Minimum Trend Bars (5-6)

- Higher Size Reduction Threshold (45-55%)

⚠️ Important Notes⚠️

- **Not a Complete Strategy**: Use as confluence with other analysis methods

- **Market Context Matters**: Consider overall trend direction and key support/resistance levels

- **Risk Management Essential**: Always use proper position sizing and stop losses

- **Backtest First**: Optimize parameters for your specific trading style and instruments

Oculus Ultra Parallel S/R Channel**Oculus Ultra Parallel S/R Channel**

*Version 1.0 | Pine Script v6*

**Overview**

This indicator overlays a statistically-driven support/resistance channel on your chart by fitting a linear regression (median) line and plotting parallel bands at a configurable multiple of standard deviation. It adapts dynamically to both trend and volatility, highlights potential reaction zones, and offers optional alerts when price touches key levels.

**Key Features**

* **Median Regression Line**

Fits a best-fit line through the chosen lookback of price data, showing the underlying trend.

* **Volatility-Based Bands**

Upper and lower bands offset by *N*× standard deviation of regression residuals, capturing dynamic S/R zones.

* **Dynamic Coloring**

* Median line turns **teal** when sloping up, **orange** when sloping down.

* Bands tinted green or red depending on their position relative to the median.

* **Channel Fill**

Optional shaded area between the bands for immediate visual context.

* **Touch Alerts**

Precision alerts and on-chart markers when price touches the support or resistance band, with configurable tick tolerance.

* **Clean Layout**

Minimal lines and plots to avoid chart clutter, adjustable via toggle inputs.

**How to Use**

1. **Apply the Script** – Add to any timeframe in overlay mode.

2. **Configure Inputs** –

* **Channel Length**: Number of bars for regression and volatility calculation.

* **Deviation Factor**: Multiplier for band width (in standard deviations).

* **Show/Hide Elements**: Toggle median line, bands, fill, and touch alerts.

* **Color by Slope**: Enable slope-based median coloring.

* **Touch Tolerance**: Number of ticks within which a band touch is registered.

3. **Interpret the Channel** –

* **Trend**: Follow the slope and color of the median line.

* **Support/Resistance**: Bands represent dynamic zones where price often reacts.

* **Alerts**: Use touch markers or alert pop-ups to time entries or exits at band levels.

**Inputs**

* **Channel Length** (default: 100)

* **Deviation Factor** (default: 1.0)

* **Show Median Regression Line** (true/false)

* **Show Channel Bands** (true/false)

* **Fill Between Bands** (true/false)

* **Color Median by Slope** (true/false)

* **Alert on Band Touch** (true/false)

* **Touch Tolerance (ticks)** (default: 2)

**Version History**

* **1.0** – Initial release with dynamic regression channel, slope coloring, band fill, and touch alerts.

**Disclaimer**

This indicator is intended for educational purposes. Always backtest with your own settings and apply sound risk management before trading live.

VWAP Supply & Demand Zones PRO**Overview:**

This script represents a major evolution of the original "VWAP Supply and Demand Zones" indicator. Initially created to explore price interaction with VWAP, it has now matured into a robust and feature-rich tool for identifying high-probability zones of institutional buying and selling pressure. The update introduces volume and momentum validation, dynamic zone management, alert logic, and a visual dashboard (HUD) — all designed for improved precision and clarity. The structural improvements, anti-repainting logic, and significant added utility warranted releasing this as a new script rather than a minor update.

---

### What It Does:

This indicator dynamically detects **supply and demand zones** using VWAP-based logic combined with **volume** and **momentum confirmation**. When price crosses VWAP with strength, it identifies the potential zone of excess demand (below VWAP) or supply (above VWAP), marking it visually with colored regions on the chart.

Each zone is extended for a user-defined duration, monitored for touch interactions (tests), and tracked for possible breaks. The script helps traders interpret price behavior around these institutional zones as either **reversal** opportunities or **continuation** confirmation depending on context and strategy preference.

---

### How It Works:

* **VWAP Basis**: Zones are anchored at VWAP at the time of a significant cross.

* **Volume & Momentum Filters**: Crosses are only considered valid if backed by above-average volume and notable price momentum.

* **Zone Drawing**: Validated supply and demand zones are drawn as boxes on the chart. Each is extended forward for a customizable number of bars.

* **Touch Counting**: Zones track the number of price touches. Alerts are issued after a user-defined number of tests.

* **Break Detection**: If price closes significantly beyond a zone boundary, the zone is marked as broken and visually dimmed.

* **Visual Dashboard (HUD)**: A compact real-time HUD displays VWAP value, active zone counts, and current market bias.

---

### How to Use It:

**Reversal Trading:**

* Look for price **rejecting** a zone after touching it.

* Use rejection candles or secondary indicators (e.g., RSI divergence) to confirm.

* These setups may offer low-risk entries when price respects the zone.

**Continuation Trading:**

* A **break of a zone** suggests strong directional bias.

* Use confirmed zone breaks to enter in the direction of momentum.

* Ideal in trending environments, especially with high volume and ATR movement.

---

### Key Inputs:

* **VWAP Length**: Moving VWAP period (default: 20)

* **Zone Width %**: Percentage size of zone buffer (default: 0.5%)

* **Min Touches**: How many times price must test a zone before alerts trigger

* **Zone Extension**: How far into the future zones are projected

* **Volume & ATR Filters**: Ensure only strong, valid crossovers create zones

---

### Alerts:

You can enable alerts for:

* **New zone creation**

* **Zone tests (after minimum touch count)**

* **Zone breaks**

* **VWAP crosses**

* **Active presence inside a zone (entry conditions)**

These alerts help automate market monitoring, making it suitable for discretionary or systematic workflows.

---

### Why It's a New Script:

This is not a cosmetic update. The internal logic, signal generation, filtering methodology, visual engine, and UX framework have been entirely rebuilt from the ground up. The result is a highly adaptive, precision-oriented tool — appropriate for intraday scalpers and swing traders alike. It goes far beyond the original in terms of functionality and reliability, justifying a fresh release.

---

### Suitable Markets and Timeframes:

* Works across all liquid markets (crypto, equities, futures, forex)

* Best used on timeframes where volume data is stable (5m and above recommended)

* Recalibrate inputs for optimal detection across instruments

Wavelet Filter with Adaptive Upsampling [BackQuant]Wavelet Filter with Adaptive Upsampling

The Wavelet Filter with Adaptive Upsampling is an advanced filtering and signal reconstruction tool designed to enhance the analysis of financial time series data. It combines wavelet transforms with adaptive upsampling techniques to filter and reconstruct price data, making it ideal for capturing subtle market movements and enhancing trend detection. This system uses high-pass and low-pass filters to decompose the price series into different frequency components, applying adaptive thresholding to eliminate noise and preserve relevant signal information.

Shout out to Loxx for the Least Squares fitting of trigonometric series and Quinn and Fernandes algorithm for finding frequency

www.tradingview.com

Key Features

1. Frequency Decomposition with High-Pass and Low-Pass Filters:

The indicator decomposes the input time series using high-pass and low-pass filters to separate the high-frequency (detail) and low-frequency (trend) components of the data. This decomposition allows for a more accurate analysis of underlying trends, while mitigating the impact of noise.

2. Soft Thresholding for Noise Reduction:

A soft thresholding function is applied to the high-frequency component, allowing for the reduction of noise while retaining significant market signals. This function adjusts the coefficients of the high-frequency data, removing small fluctuations and leaving only the essential price movements.

3. Adaptive Upsampling Process:

The upsampling process in this script can be customized using different methods: sinusoidal upsampling, advanced upsampling, and simple upsampling. Each method serves a unique purpose:

Sinusoidal Upsample uses a sine wave to interpolate between data points, providing a smooth transition.

Advanced Upsample utilizes a Quinn-Fernandes algorithm to estimate frequency and apply more sophisticated interpolation techniques, adapting to the market’s cyclical behavior.

Simple Upsample linearly interpolates between data points, providing a basic upsampling technique for less complex analysis.

4. Reconstruction of Filtered Signal:

The indicator reconstructs the filtered signal by summing the high and low-frequency components after upsampling. This allows for a detailed yet smooth representation of the original time series, which can be used for analyzing underlying trends in the market.

5. Visualization of Reconstructed Data:

The reconstructed series is plotted, showing how the upsampling and filtering process enhances the clarity of the price movements. Additionally, the script provides the option to visualize the log returns of the reconstructed series as a histogram, with positive returns shown in green and negative returns in red.

6. Cumulative Series and Trend Detection:

A cumulative series is plotted to visualize the compounded effect of the filtered and reconstructed data. This feature helps traders track the overall performance of the asset over time, identifying whether the asset is following a sustained upward or downward trend.

7. Adaptive Thresholding and Noise Estimation:

The system estimates the noise level in the high-frequency component and applies an adaptive thresholding process based on the standard deviation of the downsampled data. This ensures that only significant price movements are retained, further refining the trend analysis.

8. Customizable Parameters for Flexibility:

Users can customize the following parameters to adjust the behavior of the indicator:

Frequency and Phase Shift: Control the periodicity of the wavelet transformation and the phase of the upsampling function.

Upsample Factor: Adjust the level of interpolation applied during the upsampling process.

Smoothing Period: Determine the length of time used to smooth the signal, helping to filter out short-term fluctuations.

References

Enhancing Cross-Sectional Currency Strategies with Context-Aware Learning to Rank

arxiv.org

Daubechies Wavelet - Wikipedia

en.wikipedia.org

Quinn Fernandes Fourier Transform of Filtered Price by Loxx

Note on Usage for Mean-Reversion Strategy

This indicator is primarily designed for trend-following strategies. However, by taking the inverse of the signals, it can be adapted for mean-reversion strategies. This involves buying underperforming assets and selling outperforming ones. Caution: This method may not work effectively with highly correlated assets, as the price movements between correlated assets tend to mirror each other, limiting the effectiveness of mean-reversion strategies.

Final Thoughts

The Wavelet Filter with Adaptive Upsampling is a powerful tool for traders seeking to improve their understanding of market trends and noise. By using advanced wavelet decomposition and adaptive upsampling, this system offers a clearer, more refined picture of price movements, enhancing trend-following strategies. It’s particularly useful for detecting subtle shifts in market momentum and reconstructing price data in a way that removes noise, providing more accurate insights into market conditions.

Curved Trend Channels (Zeiierman)█ Overview

Curved Trend Channels (Zeiierman) is a next-generation trend visualization tool engineered to adapt dynamically to both linear and non-linear market behavior. It introduces a novel curvature-based channeling system that grows over time during trending conditions, mirroring the natural acceleration of price trends, while simultaneously leveraging adaptive range filtering and dual-layer candle trend logic.

This tool is ideal for traders seeking smooth yet reactive dynamic channels that evolve with market structure. Whether used in curved mode or traditional slope mode, it provides exceptional clarity on trend transitions, volatility compression, and breakout development.

█ How It Works

⚪ Adaptive Range Filter Foundation

The core of the system is a volatility-based range filter that determines the underlying structure of the bands:

Pre-Smoothing of High/Low Data – Highs and lows are smoothed using a selectable moving average (SMA, EMA, HMA, KAMA, etc.) before calculating the volatility range.

Volatility Envelope – The range is scaled using a fixed factor (2.618) and further adjusted by a Band Multiplier to form the primary envelope around price.

Smoothed Volatility Curve – Final bands are stabilized using a long lookback, ensuring clean visual structure and trend clarity.

⚪ Curved Channel Logic

In Curved Mode, the trend channel grows over time when the trend direction remains unchanged:

Base Step Size (× ATR) – Sets the minimum unit of slope change.

Growth per Bar (× ATR) – Defines the acceleration rate of the channel slope with time.

Trend Persistence Recognition – The longer a trend persists, the more pronounced the slope becomes, mimicking real market accelerations.

This dynamic, time-dependent logic enables the channel to "curve" upward or downward, tracking long-standing trends with increasing confidence.

⚪ Trend Slope

As an alternative to curved logic, traders can activate a regular Trend slope using:

Slope Length – Determines how quickly the trend line adapts to price shifts.

Multiplicative Factor – Amplifies the sensitivity of the slope, useful in fast-moving markets or lower timeframes.

⚪ Candle Trend Confirmation

A robust second-layer trend detection method, the Candle Trend System evaluates directional pressure by analyzing smoothed price action:

Multi-tier Smoothing – Trend lines are derived from short-, medium-, and long-term candle movement.

█ How to Use

⚪ Trend Identification

When the Trend Line direction and Candle Colors are in agreement, this indicates strong, persistent directional conviction. Use these moments to enter with trend confirmation and manage risk more confidently.

⚪ Retest

During ongoing trends, the price will often pull back into the dynamic channel. Look for:

Support/resistance interactions at the upper or lower bands.

█ Settings

Scaled Volatility Length – Controls the historical depth used to stabilize the volatility bands.

Smoothing Type – Choose from HMA, KAMA, VIDYA, FRAMA, Super Smoother, etc. to match your asset and trading style.

Volatility MA Length – Smoothing length for the calculated range; shorter = more reactive.

High/Low Smoother Length – Additional smoothing to reduce noise from spikes or false pivots.

Band Multiplier – Widens or tightens the band range based on personal preference.

Enable Curved Channel – Toggle between curved or regular trend slope behavior.

Base Step (× ATR) – The starting point for curved slope progression.

Growth per Bar (× ATR) – How much the slope accelerates per bar during a sustained trend.

Slope – Reactivity of the standard trend line to price movements.

Multiplicative Factor – Sensitivity adjustment for HyperTrend slope.

Candle Trend Length – Lookback period for trend determination from candle structure.

-----------------

Disclaimer

The content provided in my scripts, indicators, ideas, algorithms, and systems is for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or a solicitation to buy or sell any financial instruments. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

Regression Channel (Interactive)Weighted Interactive Regression Channel (WIRC)

Overview

The Weighted Interactive Regression Channel improves on traditional regression channels by emphasizing key price points through intelligent weighting. Instead of treating all candles equally, WIRC adapts to market dynamics for better trend detection and channel accuracy.

Key Differences from Standard Channels

Weighted vs. Equal: Prioritizes significant events over uniform weighting

Dynamic vs. Static: Adapts in real time to market changes

Accurate vs. Basic: Reduces noise, enhances signal clarity

Customizable vs. Fixed: Full control over weights and visuals

Weighting Methods

Direction Change – Highlights reversal points via local peaks/troughs

Volume-Based – Emphasizes high-volume candles, ideal for breakouts

Price Range – Weights wide-range candles to capture volatility

Time Decay – Prioritizes recent data for current market relevance

Interactive Features

Data Range: Set channel start/end over 1–500 bars

Visuals: Line styles, color coding, fill options, reference lines

Stats: Slope, R², standard deviation, point count, weight method

Technical Implementation

Weighted Regression Formula: Uses weights for slope, intercept, and deviation

Channel Lines: Center = weighted regression; bounds = ± deviation × multiplier

Usage Scenarios

Trend Analysis: Use Direction Change + longer range

Breakouts: Use Volume weighting + fill + boundary watching

Volatility: Apply Price Range weighting + monitor standard deviation

Current Market: Use Time Decay + shorter ranges + stat display

Parameter Tips

Channel Width:

Narrow (1.0–1.5): Responsive

Standard (1.5–2.0): Balanced

Wide (2.0–3.0+): Conservative

Weighting Intensity:

Conservative (1.5–2.0)

Moderate (2.0–3.0)

Aggressive (3.0+)

Advanced Use

Multi-Timeframe: Use different weightings per timeframe

Market Structure: Detect swings, institutional zones

Risk Management: Dynamic S/R levels, volatility-driven sizing

Best Practices

Start with Direction Change

Test different ranges

Monitor stats

Combine with other indicators

Adjust to market context

Recalibrate regularly

Conclusion

WIRC delivers a smarter, more adaptive view of price action than standard regression tools. With real-time customization and multiple weighting options, it’s ideal for traders seeking precision across strategies—trend tracking, breakout confirmation, or volatility insight.

WLSMA: fast approximation🙏🏻 Sup TV & @alexgrover

O(N) algocomplexity, just one loop inside. No, you can't do O(1) @ updates in moving window mode, only expanding window will allow that.

Now I have time series & stats models of my own creation, nowhere else available, just TV and my github for now, ain’t no legacy academic industry I always have fun about, but back in 2k20 when I consciously ain’t known much about quant, I remember seeing post by @alexgrover recreating Moving Regression Endpoint dropped on price chart (called LSMA here) as a linear filter combination of filters (yea yeah DSP terms) as 3WMA - 2SMA. Now it’s my time to do smth alike aye?

...

This script is remake of my 1st degree WLSMA via linear filter combo. It’s much faster, we aint calculate moving regression per se, we just match its freq response. You can see it on the screen (WLSMAfa) almost perfectly matching the original one (WLSMA).

...

While humans like to overfit, I fw generalizations. So your lovely WMA is actually just one case of a more general weight pattern: pow(len - i, e), where pow is the power function and e is the exponent itself. So:

- If e = 0, then we have SMA (every number in 0th power is one)

- If e = 1, we get WMA

- If e = 2, we get quadratic weights.

We can recreate WLSMA freq response then by combining 2 filters with e = 1 and e = 2.

This is still an approximation, even tho enormously precise for the tasks you’ve shared with me. Due to the non-linear nature of the thing it’s all we can do, and as window size grows, even this small discrepancy converges with true WLSMA value, so we’re all good. Pls don’t try to model this 0.00xxxx discrepancy, it’s not natural.

...

DSP approach is unnatural for prices, but you can put this thing on volume delta and be happy, or on other metrics of yours, if for some reason u dont wanna estimate thresholds by fitting a distro.

All good TV

∞

P.S.: strangely, the first script made & dropped in the location in Saint P where my actual quant way has started ~5 years ago xD, very thankful

Support and Resistance Logistic Regression | Flux Charts💎 GENERAL OVERVIEW

Introducing our new Logistic Regression Support / Resistance indicator! This tool leverages advanced statistical modeling "Logistic Regressions" to identify and project key price levels where the market is likely to find support or resistance. For more information about the process, please check the "HOW DOES IT WORK ?" section.

Logistic Regression Support / Resistance Features :

Intelligent S/R Identification : The indicator uses a logistic regression model to intelligently identify and plot significant support and resistance levels.

Predictive Probability : Each identified level comes with a calculated probability, indicating how likely it is to act as a true support or resistance based on historical data.

Retest & Break Labels : The indicator clearly marks on your chart when a detected support or resistance level is retested (price touches and respects the level) or broken (price decisively crosses through the level).

Alerts : Real-time alerts for support retests, resistance retests, support breaks, and resistance breaks.

Customizable : You can change support & resistance line style, width and colors.

🚩 UNIQUENESS

What makes this indicator truly unique is its application of logistic regression to the concept of support and resistance. Instead of merely identifying historical highs and lows, our indicator uses a statistical model to predict the future efficacy of these levels. It analyzes underlying market conditions (like RSI and body size at pivot formation) to assign a probability to each potential S/R zone. This predictive insight, combined with dynamic, real-time labeling of retests and breaks, provides a more robust and adaptive understanding of market structure than traditional, purely historical methods.

📌HOW DOES IT WORK ?

The Logistic Regression Support / Resistance indicator operates in several key steps:

First, it identifies significant pivot highs and lows on the chart based on a user-defined "Pivot Length." These pivots are potential areas of support or resistance.

For each detected pivot, the indicator extracts relevant market data at that specific point, including the RSI (Relative Strength Index) and the Body Size (the absolute difference between the open and close price of the candle). These serve as input features for the model.

The core of the indicator lies in its logistic regression model. This model is continuously trained on past pivot data and their subsequent behavior (i.e., whether they were "respected" as support/resistance multiple times). It learns the relationship between the extracted features (RSI, Body Size) and the likelihood of a pivot becoming a significant S/R level.

When a new pivot is identified, the model uses its learned insights to calculate a prediction value—a probability (from 0 to 1) that this specific pivot will act as a strong support or resistance.

If the calculated probability exceeds a user-defined "Probability Threshold," the pivot is designated a "Regression Pivot" and drawn on the chart as a support or resistance line. The indicator then actively tracks how price interacts with these levels, displaying "R" labels for retests when the price bounces off the level and "B" labels for breaks when the price closes beyond it.

⚙️ SETTINGS

1. General Configuration

Pivot Length: This setting defines the number of bars used to determine a significant high or low for pivot detection.

Target Respects: This input specifies how many times a level must be "respected" by price action for it to be considered a strong support or resistance level by the underlying model.

Probability Threshold: This is the minimum probability output from the logistic regression model for a detected pivot to be considered a valid support or resistance level and be plotted on the chart.

2. Style

Show Prediction Labels: Enable or disable labels that display the calculated probability of a newly identified regression S/R level.

Show Retests: Toggle the visibility of "R" labels on the chart, which mark instances where price has retested a support or resistance level.

Show Breaks: Toggle the visibility of "B" labels on the chart, which mark instances where price has broken through a support or resistance level.

TrueTrend MaxRThe TrueTrend MaxR indicator is designed to identify the most consistent exponential price trend over extended periods. It uses statistical analysis on log-transformed prices to find the trendline that best fits historical price action, and highlights the most frequently tested or traded level within that trend channel.

For optimal results, especially on high timeframes such as weekly or monthly, it is recommended to use this indicator on charts set to logarithmic scale. This ensures proper visual alignment with the exponential nature of long-term price movements.

How it works

The indicator tests 50 different lookback periods, ranging from 300 to 1280 bars. For each period, it:

- Applies a linear regression on the natural logarithm of the price

- Computes the slope and intercept of the trendline

- Calculates the unbiased standard deviation from the regression line

- Measures the correlation strength using Pearson's R coefficient

The period with the highest Pearson R value is selected, meaning the trendline drawn corresponds to the log-scale trend with the best statistical fit.

Trendline and deviation bands

Once the optimal period is identified, the indicator plots:

- A main log-scale trendline

- Upper and lower bands, based on a user-defined multiple of the standard deviation

These bands help visualize how far price deviates from its core trend, and define the range of typical fluctuations.

Point of Control (POC)

Inside the trend channel, the space between upper and lower bands is divided into 15 logarithmic levels. The script evaluates how often price has interacted with each level, using one of two selectable methods:

- Touches: Counts the number of candles crossing each level

- Volume: Weighs each touch by the traded volume at that candle

The level with the highest cumulative interaction is considered the dynamic Point of Control (POC), and is plotted as a line.

Annualized performance and confidence display

When used on daily or weekly timeframes, the script also calculates the annualized return (CAGR) based on the detected trend, and displays:

- A performance estimate in percentage terms

- A textual label describing the confidence level based on the Pearson R value

Why this indicator is useful

- Automatically detects the most statistically consistent exponential trendline

- Designed for log-scale analysis, suited to long-term investment charts

- Highlights key price levels frequently visited or traded within the trend

- Provides objective, data-based trend and volatility insights

- Displays annualized growth rate and correlation strength for quick evaluation

Notes

- All calculations are performed only on the last bar

- No future data is used, and the script does not repaint

- Works on any instrument or timeframe, with optimal use on higher timeframes and logarithmic scaling

Custom Paul MACD-likePaul MACD is an indicator created by David Paul. It is implemented to effectively represent trend periods and non-trend (sideways/consolidation) periods, and its calculation method is particularly designed to reduce whipsaw.

Unlike the existing MACD which uses the difference between short-term (12) and long-term (26) exponential moving averages (EMA), Paul MACD has a different calculation method. This indicator uses a "center value" or "intermediate value". Calculation occurs when this intermediate value is higher than the High value (specifically, the difference between the center and High is calculated) or lower than the Low value (specifically, the difference between the center and Low is calculated). Otherwise, the value becomes 0. Here, the High and Low values are intended to be smoothly reflected using Smoothed Moving Average (SMMA). The indicator's method itself (using SMMA and ZLMA) is aimed at diluting whipsaws.

Thanks to this calculation method, in sections where whipsaw occurs, meaning when the intermediate value is between High and Low, the indicator value is expressed as 0 and appears as a horizontal line (zero line). This serves to visually clearly show sideways/consolidation periods.

Linear Regression ForecastDescription:

This indicator computes a series of simple linear regressions anchored at the current bar, using look-back windows from 2 bars up to the user-defined maximum. Each regression line is projected forward by the same number of bars as its look-back, producing a family of forecast endpoints. These endpoints are then connected into a continuous polyline: ascending segments are drawn in green, and descending segments in red.

Inputs:

maxLength – Maximum number of bars to include in the longest regression (minimum 2)

priceSource – Price series used for regression (for example, close, open, high, low)

lineWidth – Width of each line segment

Calculation:

For each window size N (from 2 to maxLength):

• Compute least-squares slope and intercept over the N most recent bars (with bar 0 = current bar, bar 1 = one bar ago, etc.).

• Project the regression line to bar_index + N to obtain the forecast price.

Collected forecast points are sorted by projection horizon and then joined:

• First segment: current bar’s price → first forecast point

• Subsequent segments: each forecast point → next forecast point

Segment colors reflect slope direction: green for non-negative, red for negative.

Usage:

Apply this overlay to any price chart. Adjust maxLength to control the depth and reach of the forecast fan. Observe how shorter windows produce nearer-term, more reactive projections, while longer windows yield smoother, more conservative forecasts. Use the colored segments to gauge the overall bias of the fan at each step.

Limitations:

This tool is for informational and educational purposes only. It relies on linear regression assumptions and past price behavior; it does not guarantee future performance. Users should combine it with other technical or fundamental analyses and risk management practices.

Tangent Extrapolation ForecastTangent Extrapolation Forecast

This indicator visually projects price direction by drawing a smoothed sequence of tangent lines based on recent price movements. For each bar in a user-defined lookback window, it calculates the slope over a smoothing period and extends the projected price forward. The resulting polyline forecast connect the endpoints of the extrapolations, and is color-coded to reflect directional changes: green for upward moves, red for downward, and gray for flat segments. This tool can assist traders in visualizing short-term momentum and potential trend continuity without introducing artificial future gaps.

Inputs:

Bars to Use: Number of historical bars used in the forecast.

Slope Smoothing Window: The number of bars used to calculate slope for projection.

Source: Price input for calculations (default is close).

This indicator does not generate buy/sell signals. It is intended as a visual aid to support discretionary analysis.

Linear Volume MACD | Lyro RS📊 Linear Volume MACD | Lyro RS is an advanced momentum and trend detection tool that fuses price action with volume-weighted MACD logic and linear regression analysis . Designed for traders seeking deeper insights into market strength and directional conviction, this indicator highlights trend shifts, volume anomalies, and potential reversal zones with precision.

✨ Key Features :

🔁 Multi-Mode Analysis: Switch between Linear Regression , Strong/Weak Trend , or Volume MACD logic.

📐 Volume-Adjusted MACD: Incorporates volume for a more realistic momentum view.

📊 Linear Regression Signal: Smoother and more reactive trend analysis.

🎯 Dynamic Stdev Bands: Visualize ±1 and ±2 standard deviation thresholds for anomaly detection.

🌈 Custom Color Themes: Choose from built-in palettes or define your own bullish/bearish signal colors.

⚠️ Alert Conditions: Built-in alerts notify you of potential trend shifts across all signal modes.

📈 How It Works :

🧮 MACD Core: Uses volume-weighted price to generate fast and slow EMAs, forming the MACD and signal lines.

📉 Histogram Logic: Histogram is either the traditional MACD histogram or its linear regression version.

📊 Signal Modes:

• Linear Regression: Detect trend based on smoothed MACD behavior.

• Strong/Weak Trend: Identifies accelerating/decelerating trend strength.

• Volume MACD: Classic volume MACD behavior for divergence spotting.

📏 Stdev Bands: Calculated over a long period (default 200) to highlight statistically significant moves.

🎨 Color-coded Feedback: Bar and background colors adjust dynamically with market condition.

⚙️ Customization Options :

🔄 Choose your Signal Type from three unique analysis modes.

📏 Modify Fast/Slow/Signal lengths and Regression parameters to suit your strategy.

📈 Enable or disable Stdev Bands and adjust multiplier.

🎨 Select from Classic, Mystic, Accented, or Royal color palettes — or create your own.

📌 Use Cases :

🟢 Identify trend continuation or reversal zones with volume-adjusted signals.

🔴 Detect volatility breakouts using standard deviation bands.

🧭 Use in confluence with price structure, RSI, or market sentiment.

⚠️ Disclaimer :

This indicator is for educational purposes only. It is not financial advice. Always use in conjunction with your own research and risk management strategy.

Weighted Regression Bands (Zeiierman)█ Overview

Weighted Regression Bands is a precision-engineered trend and volatility tool designed to adapt to the real market structure instead of reacting to price noise.

This indicator analyzes Weighted High/Low medians and applies user-selectable smoothing methods — including Kalman Filtering, ALMA, and custom Linear Regression — to generate a Fair Value line. Around this, it constructs dynamic standard deviation bands that adapt in real-time to market volatility.

The result is a visually clean and structurally intelligent trend framework suitable for breakout traders, mean reversion strategies, and trend-driven analysis.

█ How It Works

⚪ Structural High/Low Analysis

At the heart of this indicator is a custom high/low weighting system. Instead of using just the raw high or low values, it calculates a midline = (high + low) / 2, then applies one of three weighting methods to determine which price zones matter most.

Users can select the method using the “Weighted HL Method” setting:

Simple

Selects the single most dominant median (highest or lowest) in the lookback window. Ideal for fast, reactive signals.

Advanced

Ranks each bar based on a composite score: median × range × recency. This method highlights structurally meaningful bars that had both volatility and recency. A built-in Kalman filter is applied for extra stability.

Smooth

Blends multiple bars into a single weighted average using smoothed decay and range. This provides the softest and most stable structural response.

⚪ Smoothing Methods (ALMA / Linear Regression)

ALMA provides responsive, low-lag smoothing for fast trend reading.

Linear Regression projects the Fair Value forward, ideal for trend modeling.

⚪ Kalman Smoothing Filter

Before trend calculations, the indicator applies an optional Kalman-style smoothing filter. This helps:

Reduce choppy false shifts in trend,

Retain signal clarity during volatile periods,

Provide stability for long-term setups.

⚪ Deviation Bands (Dynamic Volatility Envelopes)

The indicator builds ±1, ±2, and ±3 standard deviation bands around the fair value line:

Calculated from the standard deviation of price,

Bands expand and contract based on recent volatility,

Visualizes potential overbought/oversold or trending conditions.

█ How to Use

⚪ Trend Trading & Filtering

Use the Fair Value line to identify the dominant direction.

Only trade in the direction of the slope for higher probability setups.

⚪ Volatility-Based Entries

Watch for price reaching outer bands (+2σ, +3σ) for possible exhaustion.

Mean reversion entries become higher quality when far from Fair Value.

█ Settings

Length – Lookback for Weighted HL and trend smoothing

Deviation Multiplier – Controls how wide the bands are from the fair value line

Method – Choose between ALMA or Linear Regression smoothing

Smoothing – Strength of Kalman Filter (1 = none, <1 = stronger smoothing)

-----------------

Disclaimer

The content provided in my scripts, indicators, ideas, algorithms, and systems is for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or a solicitation to buy or sell any financial instruments. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.