SITFX_FuturesSpec_v17SITFX_FuturesSpec_v17 – Universal Futures Contract Library

Full-scale futures contract specification library for Pine Script v6. Covers CME, CBOT, NYMEX, COMEX, CFE, Eurex, ICE, and more – including minis, micros, metals, energies, FX, and bonds.

Key Features:

✅ Instrument‑agnostic: ES/MES, NQ/MNQ, YM/MYM, RTY/M2K, metals, energies, FX, bonds

✅ Full contract data: Tick size, tick value, point value, margins

✅ Continuation‑safe: Single‑line logic, no arrays or continuation errors

✅ Foundation for SITFX tools: Gann, Fibs, structure, and risk modules

Usage example:

import SITFX_FuturesSpec_v17/1 as fs

spec = fs.get(syminfo.root)

label.new(bar_index, high, str.format("{0}: Tick={1}, Value=${2}", spec.name, spec.tickSize, spec.tickValue))

지표 및 전략

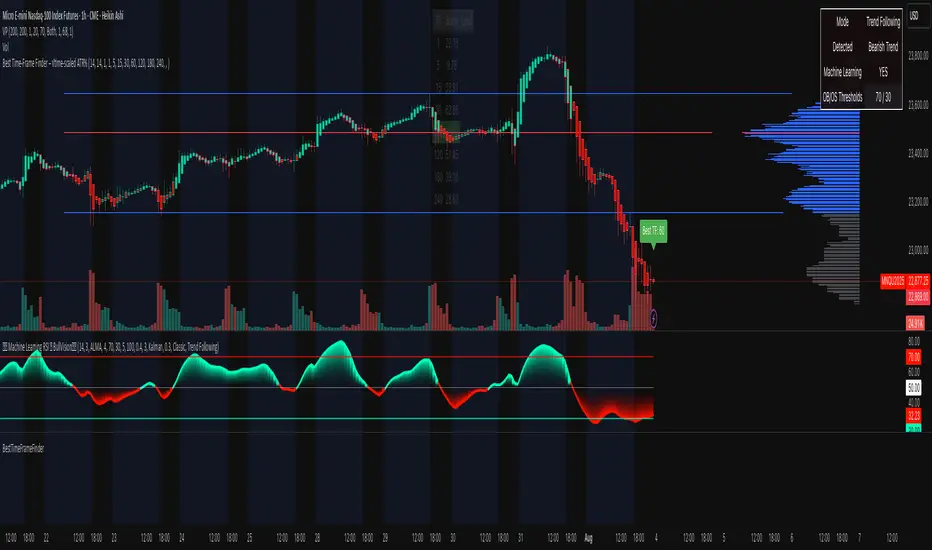

BestTimeFrameFinderLibrary "BestTimeFrameFinder"

adx(len)

Parameters:

len (simple int)

atrPercent(len)

Parameters:

len (simple int)

scaleFromTf(tf, atrWeight)

Parameters:

tf (string)

atrWeight (simple float)

scoreLocal(adxLen, atrLen, scale)

Parameters:

adxLen (simple int)

atrLen (simple int)

scale (simple float)

maxInArray(arr)

Parameters:

arr (array)

TFPS_EngineLibrary "TFPS_Engine"

f_calculate_lead_lag(series1, series2, length, max_lag)

Parameters:

series1 (float)

series2 (float)

length (int)

max_lag (int)

f_calculate_pressure_score(spx_ticker, vix_ticker, dxy_ticker, us10y_ticker, benchmark_source, trend_lookback, score_smoothing, use_dynamic_weights, corr_lookback, w_spx, w_vix, w_dxy, w_us10y, zscore_lookback, max_lag)

Parameters:

spx_ticker (string)

vix_ticker (string)

dxy_ticker (string)

us10y_ticker (string)

benchmark_source (float)

trend_lookback (int)

score_smoothing (simple int)

use_dynamic_weights (bool)

corr_lookback (int)

w_spx (float)

w_vix (float)

w_dxy (float)

w_us10y (float)

zscore_lookback (int)

max_lag (int)

LeadLagOutput

Fields:

best_lag (series int)

max_corr (series float)

TFPS_Output

Fields:

historical_score (series float)

smoothed_score (series float)

z_score (series float)

regime_signal (series int)

lead_lag_bars (series int)

lead_lag_corr (series float)

weight_spx (series float)

weight_vix (series float)

weight_dxy (series float)

weight_us10y (series float)

FunctionADFLibrary "FunctionADF"

Augmented Dickey-Fuller test (ADF), The ADF test is a statistical method used to assess whether a time series is stationary – meaning its statistical properties (like mean and variance) do not change over time. A time series with a unit root is considered non-stationary and often exhibits non-mean-reverting behavior, which is a key concept in technical analysis.

Reference:

-

- rtmath.net

- en.wikipedia.org

adftest(data, n_lag, conf)

: Augmented Dickey-Fuller test for stationarity.

Parameters:

data (array) : Data series.

n_lag (int) : Maximum lag.

conf (string) : Confidence Probability level used to test for critical value, (`90%`, `95%`, `99%`).

Returns: `adf` The test statistic. \

`crit` Critical value for the test statistic at the 10 % levels. \

`nobs` Number of observations used for the ADF regression and calculation of the critical values.

BarUtils: Get Bar Index from DateLibrary "BarUtils"

getBarIndexFromDate(targetTimestamp)

Parameters:

targetTimestamp (int)

**Description**:

This utility provides a reliable way to calculate the `bar_index` of a specific calendar date, regardless of chart resolution. It's especially useful for anchoring scripts to historical events, labeling macroeconomic moments, or marking custom time-based signals that must remain consistent across timeframes.

Unlike hardcoded `bar_index - N` approaches, this function dynamically estimates the number of bars between a given `timestamp()` and the current bar using the actual time-per-bar (`time - time `). It works correctly on intraday, daily, weekly, and monthly charts.

### 💡 **Function Provided**:

import TradeTitan120/BarUtils/1

* `getBarIndexFromDate(int targetTimestamp)`

→ Returns the estimated `bar_index` that aligns with a given timestamp

### ✅ **Use Cases**:

* Marking past events like FOMC meetings, market crashes, or personal signals

* Backtesting entry/exit conditions from specific calendar dates

* Anchoring visual elements (shapes, lines, labels) across resolutions

This tool is simple, fast, and built for accuracy. Use it to enhance multi-timeframe compatibility in any script.

lib_listaAtivos_PosseidonLibrary "lib_listaAtivos_Posseidon"

TODO: add library description here

ativos(loteSelected)

TODO: add function description here

Parameters:

loteSelected (simple int)

Returns: TODO: add what function returns

PulseLogicLibPulseLogicLib v3.6.1

PulseLogic breath-strength & momentum-structure calculator

Exports:

• getBreathScore() → int (0–100)

• hasGreenDot() → bool

• getTriangleColor() → string (“green”/“red”/“none”)

PulseLinesLibPulseLinesLib v1.3.1

PulseLines morphic-level calculator (support & resistance)

Exports:

• getLevels(lookback:int, wickRatioThresh:float, flatCandles:int, tolerancePips:float, atrMult:float) → float

hudDisplay_v1Library "hudDisplay_v1"

f_getPosition(loc)

Parameters:

loc (string)

f_getTableSize(layout, itemCount)

Parameters:

layout (string)

itemCount (int)

f_getCellPosition(layout, index)

Parameters:

layout (string)

index (int)

f_drawHUD(show, loc, layout, content, textColor, bgColor)

Parameters:

show (bool)

loc (string)

layout (string)

content (array)

textColor (color)

bgColor (color)

TrailingStopLibraryLibrary "TrailingStopLibrary"

专业移动止盈库 - 为Pine Script策略提供完整的追踪止盈功能。支持做多做空双向交易,基于风险回报比智能激活,提供收盘价和高低价两种判断模式。包含完整的状态管理、调试信息和易用的API接口。适用于股票、外汇、加密货币等各种市场的风险管理。

@version 1.0

@author runto2006

new_config(enabled, activation_ratio, pullback_percent, price_type)

创建移动止盈配置对象

Parameters:

enabled (bool) : (bool) 是否启用移动止盈,默认true

activation_ratio (float) : (float) 激活盈亏比,默认4.0,表示盈利4倍止损距离时激活

pullback_percent (float) : (float) 回撤百分比,默认1.0,表示回撤1%时触发止盈

price_type (string) : (string) 价格类型,默认"close"。"close"=收盘价模式,"hl"=高低价模式

Returns: Config 配置对象

new_state()

创建移动止盈状态对象

Returns: State 初始化的状态对象

reset(state)

重置移动止盈状态

Parameters:

state (State) : (State) 要重置的状态对象

Returns: void

calc_activation_target(entry_price, stop_price, activation_ratio, is_long)

计算激活目标价格

Parameters:

entry_price (float) : (float) 入场价格

stop_price (float) : (float) 止损价格

activation_ratio (float) : (float) 激活盈亏比

is_long (bool) : (bool) 是否为多头持仓

Returns: float 激活目标价格,如果输入无效则返回na

get_check_price(price_type, is_long, for_activation)

获取用于判断的价格

Parameters:

price_type (string) : (string) 价格类型:"close"或"hl"

is_long (bool) : (bool) 是否为多头持仓

for_activation (bool) : (bool) 是否用于激活判断,影响高低价的选择方向

Returns: float 当前判断价格

check_activation(config, state, entry_price, stop_price, is_long, has_position)

检查是否应该激活移动止盈

Parameters:

config (Config) : (Config) 移动止盈配置

state (State) : (State) 移动止盈状态

entry_price (float) : (float) 入场价格

stop_price (float) : (float) 止损价格

is_long (bool) : (bool) 是否为多头持仓

has_position (bool) : (bool) 是否有持仓

Returns: bool 是否成功激活

update_tracking(config, state, is_long)

更新移动止盈的追踪价格

Parameters:

config (Config) : (Config) 移动止盈配置

state (State) : (State) 移动止盈状态

is_long (bool) : (bool) 是否为多头持仓

Returns: void

check_trigger(config, state, entry_price, is_long)

检查是否触发移动止盈

Parameters:

config (Config) : (Config) 移动止盈配置

state (State) : (State) 移动止盈状态

entry_price (float) : (float) 入场价格

is_long (bool) : (bool) 是否为多头持仓

Returns: bool 是否触发止盈

process(config, state, entry_price, stop_price, is_long, has_position)

一体化处理移动止盈逻辑

Parameters:

config (Config) : (Config) 移动止盈配置

state (State) : (State) 移动止盈状态

entry_price (float) : (float) 入场价格

stop_price (float) : (float) 止损价格

is_long (bool) : (bool) 是否为多头持仓

has_position (bool) : (bool) 是否有持仓

Returns: bool 是否触发止盈

get_trigger_price(config, state, is_long)

获取当前触发价格

Parameters:

config (Config) : (Config) 移动止盈配置

state (State) : (State) 移动止盈状态

is_long (bool) : (bool) 是否为多头持仓

Returns: float 触发价格,未激活时返回na

get_pullback_percent(config, state, entry_price, is_long)

计算当前回撤百分比

Parameters:

config (Config) : (Config) 移动止盈配置

state (State) : (State) 移动止盈状态

entry_price (float) : (float) 入场价格

is_long (bool) : (bool) 是否为多头持仓

Returns: float 当前回撤百分比,未激活时返回na

get_status_info(config, state, entry_price, is_long)

获取状态信息字符串(用于调试)

Parameters:

config (Config) : (Config) 移动止盈配置

state (State) : (State) 移动止盈状态

entry_price (float) : (float) 入场价格

is_long (bool) : (bool) 是否为多头持仓

Returns: string 详细的状态信息

Config

移动止盈配置对象

Fields:

enabled (series bool) : (bool) 是否启用移动止盈功能

activation_ratio (series float) : (float) 激活盈亏比 - 盈利达到止损距离的多少倍时激活追踪

pullback_percent (series float) : (float) 回撤百分比 - 从最优价格回撤多少百分比时触发止盈

price_type (series string) : (string) 价格判断类型 - "close"使用收盘价,"hl"使用高低价

State

移动止盈状态对象

Fields:

activated (series bool) : (bool) 是否已激活追踪止盈

highest_price (series float) : (float) 激活后记录的最高价格

lowest_price (series float) : (float) 激活后记录的最低价格

activation_target (series float) : (float) 激活目标价格

PivotLibrary222Library "PivotLibrary222"

f_determinePivotStrength(_pivotCandidateRelativeIndex, _type, _maxStrength)

Determines the strength of a pivot (low or high).

Parameters:

_pivotCandidateRelativeIndex (int) : The relative bar index of the pivot candidate.

_type (string) : "low" for a pivot low, "high" for a pivot high.

_maxStrength (int) : The maximum number of bars to check on either side for strength.

Returns: An array containing .

f_getPlotColorForStrength(_strength)

Gets a plotting color based on pivot strength.

Parameters:

_strength (int) : The calculated pivot strength.

Returns: A color for plotting.

f_updateExistingPivotLow(f_pivotLows, f_pivotLowInfoIndex, f_newStrength, f_showLabels)

Updates an existing pivot LOW's strength and its corresponding chart label.

Parameters:

f_pivotLows (array) : The array of pivotLowInfo objects.

f_pivotLowInfoIndex (int) : The index of the pivot to update in the array.

f_newStrength (int) : The new (increased) strength of the pivot.

f_showLabels (bool) : A boolean to control if labels should be updated.

f_updateExistingPivotHigh(f_pivotHighs, f_pivotHighInfoIndex, f_newStrength, f_showLabels)

Updates an existing pivot HIGH's strength and its corresponding chart label.

Parameters:

f_pivotHighs (array) : The array of pivotHighInfo objects.

f_pivotHighInfoIndex (int) : The index of the pivot to update in the array.

f_newStrength (int) : The new (increased) strength of the pivot.

f_showLabels (bool) : A boolean to control if labels should be updated.

f_findPivotLows(f_pivotLows, f_minStrength, f_maxStrength, f_showLabels)

Finds and processes pivot lows.

Parameters:

f_pivotLows (array) : The array of pivotLowInfo objects to read from and modify.

f_minStrength (int) : Minimum strength required for a new pivot to be recorded.

f_maxStrength (int) : Maximum strength to search for when determining pivot strength.

f_showLabels (bool) : A boolean to control if new labels should be created.

f_findPivotHighs(f_pivotHighs, f_minStrength, f_maxStrength, f_showLabels)

Finds and processes pivot highs.

Parameters:

f_pivotHighs (array) : The array of pivotHighInfo objects to read from and modify.

f_minStrength (int) : Minimum strength required for a new pivot to be recorded.

f_maxStrength (int) : Maximum strength to search for when determining pivot strength.

f_showLabels (bool) : A boolean to control if new labels should be created.

pivotHighInfo

Represents a detected pivot high.

Fields:

abs_index (series int)

price (series float)

strength (series int)

label_id (series label)

pivotLowInfo

Represents a detected pivot low.

Fields:

abs_index (series int)

price (series float)

strength (series int)

label_id (series label)

DoublePatternsDetects Double Top and Double Bottom patterns from pivot points using structural symmetry, valley/peak depth, and extreme validation. Returns a detailed result object including similarity score, target price, and breakout quality.

WedgePatternsDetects Rising and Falling Wedge chart patterns using pivot points, trendline convergence, and volume confirmation. Includes adaptive wedge length analysis and a quality score for each match. Returns full wedge geometry and classification via WedgeResult.

HeadShouldersPatternsDetects Head & Shoulders and Inverse Head & Shoulders chart patterns from pivot point arrays. Includes neckline validation, shoulder symmetry checks, and head extremeness filtering. Returns a detailed result object with structure points, bar indices, and projected price target.

XABCD_HarmonicsLibrary for detecting harmonic patterns using ZigZag pivots or custom swing points. Supports Butterfly, Gartley, Bat, and Crab patterns with automatic Fibonacci ratio validation and optional D-point projection using extremes. Returns detailed PatternResult including structure points and target projection. Ideal for technical analysis, algorithmic detection, or overlay visualizations.

TextLibrary "Text"

library to format text in different fonts or cases plus a sort function.

🔸 Credits and Usage

This library is inspired by the work of three authors (in chronological order of publication date):

Unicode font function - JD - Duyck

UnicodeReplacementFunction - wlhm

font - kaigouthro

🔹 Fonts

Besides extra added font options, the toFont(fromText, font) method uses a different technique. On the first runtime bar (whether it is barstate.isfirst , barstate.islast , or between) regular letters and numbers and mapped with the chosen font. After this, each character is replaced using the build-in key - value pair map function .

Also an enum Efont is included.

Note: Some fonts are not complete, for example there isn't a replacement for every character in Superscript/Subscript.

Example of usage (besides the included table example):

import fikira/Text/1 as t

i_font = input.enum(t.Efont.Blocks)

if barstate.islast

sentence = "this sentence contains words"

label.new(bar_index, 0, t.toFont(fromText = sentence, font = str.tostring(i_font)), style=label.style_label_lower_right)

label.new(bar_index, 0, t.toFont(fromText = sentence, font = "Circled" ), style=label.style_label_lower_left )

label.new(bar_index, 0, t.toFont(fromText = sentence, font = "Wiggly" ), style=label.style_label_upper_right)

label.new(bar_index, 0, t.toFont(fromText = sentence, font = "Upside Latin" ), style=label.style_label_upper_left )

🔹 Cases

The script includes a toCase(fromText, case) method to transform text into snake_case, UPPER SNAKE_CASE, kebab-case, camelCase or PascalCase, as well as an enum Ecase .

Example of usage (besides the included table example):

import fikira/Text/1 as t

i_case = input.enum(t.Ecase.camel)

if barstate.islast

sentence = "this sentence contains words"

label.new(bar_index, 0, t.toCase(fromText = sentence, case = str.tostring(i_case)), style=label.style_label_lower_right)

label.new(bar_index, 0, t.toCase(fromText = sentence, case = "snake_case" ), style=label.style_label_lower_left )

label.new(bar_index, 0, t.toCase(fromText = sentence, case = "PascalCase" ), style=label.style_label_upper_right)

label.new(bar_index, 0, t.toCase(fromText = sentence, case = "SNAKE_CASE" ), style=label.style_label_upper_left )

🔹 Sort

The sort(strings, order, sortByUnicodeDecimalNumbers) method returns a sorted array of strings.

strings: array of strings, for example words = array.from("Aword", "beyond", "Space", "salt", "pepper", "swing", "someThing", "otherThing", "12345", "_firstWord")

order: "asc" / "desc" (ascending / descending)

sortByUnicodeDecimalNumbers: true/false; default = false

_____

• sortByUnicodeDecimalNumbers: every Unicode character is linked to a Unicode Decimal number ( wikipedia.org/wiki/List_of_Unicode_characters ), for example:

1 49

2 50

3 51

...

A 65

B 66

...

S 83

...

_ 95

` 96

a 97

b 98

...

o 111

p 112

q 113

r 114

s 115

...

This means, if we sort without adjusting ( sortByUnicodeDecimalNumbers = true ), in ascending order, the letter b (98 - small) would be after S (83 - Capital).

By disabling sortByUnicodeDecimalNumbers , Capital letters are intermediate transformed to str.lower() after which the Unicode Decimal number is retrieved from the small number instead of the capital number. For example S (83) -> s (115), after which the number 115 is used to sort instead of 83.

Example of usage (besides the included table example):

import fikira/Text/1 as t

if barstate.islast

aWords = array.from("Aword", "beyond", "Space", "salt", "pepper", "swing", "someThing", "otherThing", "12345", "_firstWord")

label.new(bar_index, 0, str.tostring(t.sort(strings= aWords, order = 'asc' , sortByUnicodeDecimalNumbers = false)), style=label.style_label_lower_right)

label.new(bar_index, 0, str.tostring(t.sort(strings= aWords, order = 'desc', sortByUnicodeDecimalNumbers = false)), style=label.style_label_lower_left )

label.new(bar_index, 0, str.tostring(t.sort(strings= aWords, order = 'asc' , sortByUnicodeDecimalNumbers = true )), style=label.style_label_upper_right)

label.new(bar_index, 0, str.tostring(t.sort(strings= aWords, order = 'desc', sortByUnicodeDecimalNumbers = true )), style=label.style_label_upper_left )

🔸 Methods/functions

method toFont(fromText, font)

toFont : Transforms text into the selected font

Namespace types: series string, simple string, input string, const string

Parameters:

fromText (string)

font (string)

Returns: `fromText` transformed to desired `font`

method toCase(fromText, case)

toCase : formats text to snake_case, UPPER SNAKE_CASE, kebab-case, camelCase or PascalCase

Namespace types: series string, simple string, input string, const string

Parameters:

fromText (string)

case (string)

Returns: `fromText` formatted to desired `case`

method sort(strings, order, sortByUnicodeDecimalNumbers)

sort : sorts an array of strings, ascending/descending and by Unicode Decimal numbers or not.

Namespace types: array

Parameters:

strings (array)

order (string)

sortByUnicodeDecimalNumbers (bool)

Returns: Sorted array of strings

AnnualizedReturnCalculatorLibrary "AnnualizedReturnCalculator"

TODO: add library description here

calculateAnnualizedReturn(isStartTime, enableLog)

Parameters:

isStartTime (bool) : 开始时间的BOOL值变量(用于标记策略开始时间)

enableLog (bool) : 是否输出日志

Returns:

返回持仓基准年化收益率、资金基准年化收益率、总收益、平均资金占用

LiliALHUNTERSystem_v2📚 **Library: LiliALHUNTERSystem_v2**

This library provides a powerful target management system for Pine Script developers.

It includes advanced calculators for EMA, RMA, and Supertrend, and introduces a central `createTargets()` function to dynamically render target lines and labels based on long/short trade logic.

🛠️ **Main Features:**

– Dynamic horizontal & vertical target lines

– Dual target configuration (Target 1 & Target 2)

– Directional logic via `isLong1`, `isLong2`

– Integrated Supertrend validation

– Visual dashboard and label display

– Works seamlessly with custom indicators

🎯 **Purpose:**

The `LiliALHUNTERSystem_v2` Library enables Pine coders to manage and visualize targets consistently across all trading strategies and indicators. It simplifies target logic while maintaining visual clarity and modular usage.

⚠️ **Disclaimer:**

This script is intended for educational and analytical purposes only. It does not constitute financial advice.

Library "LiliALHUNTERSystem_v2"

ema_calc(len, source)

Parameters:

len (simple int)

source (float)

rma_calc(len, source)

Parameters:

len (simple int)

source (float)

supertrend_calc(length, factor)

Parameters:

length (simple int)

factor (float)

createTargets(config, state, source1A, source1B, source2A, source2B)

Parameters:

config (TargetConfig)

state (TargetState)

source1A (float)

source1B (float)

source2A (float)

source2B (float)

showDashboard(state, dashLoc, textSize)

Parameters:

state (TargetState)

dashLoc (string)

textSize (string)

TargetConfig

Fields:

enableTarget1 (series bool)

enableTarget2 (series bool)

isLong1 (series bool)

isLong2 (series bool)

target1Condition (series string)

target2Condition (series string)

target1Color (series color)

target2Color (series color)

target1Style (series string)

target2Style (series string)

distTarget1 (series float)

distTarget2 (series float)

distOptions1 (series string)

distOptions2 (series string)

showLabels (series bool)

showDash (series bool)

TargetState

Fields:

target1LineV (series line)

target1LineH (series line)

target2LineV (series line)

target2LineH (series line)

target1Lbl (series label)

target2Lbl (series label)

target1Active (series bool)

target2Active (series bool)

target1Value (series float)

target2Value (series float)

countTargets1 (series int)

countTgReached1 (series int)

countTargets2 (series int)

countTgReached2 (series int)

SIC_TICKER_DATAThe SIC Ticker Data is an advanced and efficient library for ticker-to-industry classification and sector analysis. Built with enterprise-grade performance optimizations, this library provides instant access to SIC codes, industry classifications, and peer company data for comprehensive market analysis.

Perfect for: Sector rotation strategies, peer analysis, portfolio diversification, market screening, and financial research tools.

The simple idea behind this library is to pull any data related to SIC number of any US stock market ticker provided by SEC in order to see the industry and also see the exact competitors of the ticker.

The library stores 3 types of data: SIC number, Ticker, and Industry name. What makes it very useful is that you can pull any one of this data using the other. For example, if you would like to know which tickers are inside a certain SIC, or what's the SIC number of a specific ticker, or even which tickers are inside a certain industry, you can use this library to pull this data. The idea for data inside this library is to be accessible in any direction possible as long as they're related to each other.

We've also published a simple indicator that uses this library in order to demonstrate the inner workings of this library.

The library stores thousands of tickers and their relevant SIC code and industry for your use and is constantly updated with new data when available. This is a large library but it is optimized to run as fast as possible. The previous unpublished versions would take over 40 seconds to load any data but the final public version here loads the data in less than 5 seconds.

🔍 Primary Lookup Functions

createDataStore()

Initialize the library with all pre-loaded data.

store = data.createDataStore()

getSicByTicker(store, ticker)

Get SIC code for any ticker symbol.

sic = data.getSicByTicker(store, "AAPL") // Returns: "3571"

getIndustryByTicker(store, ticker)

Get industry classification for any ticker.

industry = data.getIndustryByTicker(store, "AAPL") // Returns: "Computer Hardware"

getTickersBySic(store, sic)

Get all companies in a specific SIC code.

software = data.getTickersBySic(store, "7372") // Returns: "MSFT,GOOGL,META,V,MA,CRM,ADBE,ORCL,NOW,INTU"

getTickersByIndustry(store, industry)

Get all companies in an industry.

retail = data.getTickersByIndustry(store, "Retail") // Returns: "AMZN,HD,WMT,TGT,COST,LOW"

📊 Array & Analysis Functions

getTickerArrayBySic(store, sic)

Get tickers as array for processing.

techArray = data.getTickerArrayBySic(store, "7372")

for i = 0 to array.size(techArray) - 1

ticker = array.get(techArray, i)

// Process each tech company

getTickerCountBySic(store, sic)

Count companies in a sector (ultra-fast).

pinescripttechCount = data.getTickerCountBySic(store, "7372") // Returns: 10

🎯 Utility Functions

tickerExists(store, ticker)

Check if ticker exists in database.

exists = data.tickerExists(store, "AAPL") // Returns: true

tickerInSic(store, ticker, sic)

Check if ticker belongs to specific sector.

isInTech = data.tickerInSic(store, "AAPL", "3571") // Returns: true

💡 Usage Examples

Example 1: Basic Ticker Lookup

// @version=6

import EdgeTerminal/SIC_TICKER_DATA/1 as data

indicator("Ticker Analysis", overlay=true)

store = data.createDataStore()

currentSic = data.getSicByTicker(store, syminfo.ticker)

currentIndustry = data.getIndustryByTicker(store, syminfo.ticker)

if barstate.islast and currentSic != "NOT_FOUND"

label.new(bar_index, high, syminfo.ticker + " SIC: " + currentSic + " Industry: " + currentIndustry)

Example 2: Sector Analysis

// @version=6

import EdgeTerminal/SIC_TICKER_DATA/1 as data

indicator("Sector Comparison", overlay=false)

store = data.createDataStore()

// Compare sector sizes

techCount = data.getTickerCountBySic(store, "7372") // Software

financeCount = data.getTickerCountBySic(store, "6199") // Finance

healthCount = data.getTickerCountBySic(store, "2834") // Pharmaceutical

plot(techCount, title="Tech Companies", color=color.blue)

plot(financeCount, title="Finance Companies", color=color.green)

plot(healthCount, title="Health Companies", color=color.red)

Example 3: Peer Analysis

// @version=6

import EdgeTerminal/SIC_TICKER_DATA/1 as data

indicator("Find Competitors", overlay=true)

store = data.createDataStore()

currentSic = data.getSicByTicker(store, syminfo.ticker)

if currentSic != "NOT_FOUND"

competitors = data.getTickersBySic(store, currentSic)

peerCount = data.getTickerCountBySic(store, currentSic)

if barstate.islast

label.new(bar_index, high, "Competitors (" + str.tostring(peerCount) + "): " + competitors)

Example 4: Portfolio Sector Allocation

// @version=6

import EdgeTerminal/SIC_TICKER_DATA/1 as data

indicator("Portfolio Analysis", overlay=false)

store = data.createDataStore()

// Analyze your portfolio's sector distribution

portfolioTickers = array.from("AAPL", "MSFT", "GOOGL", "JPM", "JNJ")

sectorCount = map.new()

for i = 0 to array.size(portfolioTickers) - 1

ticker = array.get(portfolioTickers, i)

industry = data.getIndustryByTicker(store, ticker)

if industry != "NOT_FOUND"

currentCount = map.get(sectorCount, industry)

newCount = na(currentCount) ? 1 : currentCount + 1

map.put(sectorCount, industry, newCount)

🔧 Advanced Feature

You can also bulk load data for large data sets like this:

// Pre-format your data as pipe-separated string

bulkData = "AAPL:3571:Computer Hardware|MSFT:7372:Software|GOOGL:7372:Software"

store = data.createDataStoreFromBulk(bulkData)

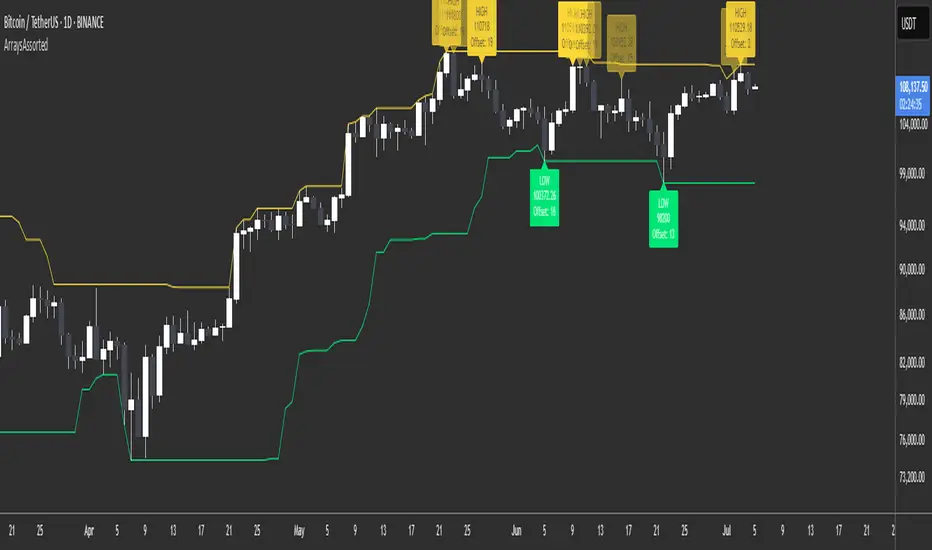

ArraysAssorted🟩 OVERVIEW

This library provides utility methods for working with arrays in Pine Script. The first method finds extreme values (highest/lowest) within a rolling lookback window and returns both the value and its position. I might extend the library for other ad-hoc methods I use to work with arrays.

🟩 HOW TO USE

Pine Script libraries contain reusable code for importing into indicators. You do not need to copy any code out of here. Just import the library and call the method you want.

For example, for version 1 of this library, import it like this:

import SimpleCryptoLife/ArraysAssorted/1

See the EXAMPLE USAGE sections within the library for examples of calling the methods.

You do not need permission to use Pine libraries in your open-source scripts.

However, you do need explicit permission to reuse code from a Pine Script library’s functions in a public protected or invite-only publication .

In any case, credit the author in your description. It is also good form to credit in open-source comments.

For more information on libraries and incorporating them into your scripts, see the Libraries section of the Pine Script User Manual.

🟩 METHOD 1: m_getHighestLowestFloat()

Finds the highest or lowest float value from an array. Simple enough. It also returns the index of the value as an offset from the end of the array.

• It works with rolling lookback windows, so you can find extremes within the last N elements

• It includes an offset parameter to skip recent elements if needed

• It handles edge cases like empty arrays and invalid ranges gracefully

• It can find either the first or last occurrence of the extreme value

We also export two enums whose sole purpose is to look pretty as method arguments.

method m_getHighestLowestFloat(_self, _highestLowest, _lookbackBars, _offset, _firstLastType)

Namespace types: array

This method finds the highest or lowest value in a float array within a rolling lookback window, and returns the value along with the offset (number of elements back from the end of the array) of its first or last occurrence.

Parameters:

_self (array) : The array of float values to search for extremes.

_highestLowest (HighestLowest) : Whether to search for the highest or lowest value. Use the enum value HighestLowest.highest or HighestLowest.lowest.

_lookbackBars (int) : The number of array elements to include in the rolling lookback window. Must be positive. Note: Array elements only correspond to bars if the consuming script always adds exactly one element on consecutive bars.

_offset (int) : The number of array elements back from the end of the array to start the lookback window. A value of zero means no offset. The _offset parameter offsets both the beginning and end of the range.

_firstLastType (FirstLast) : Whether to return the offset of the first (lowest index) or last (highest index) occurrence of the extreme value. Use FirstLast.first or FirstLast.last.

Returns: (tuple) A tuple containing the highest or lowest value and its offset -- the number of elements back from the end of the array. If not found, returns . NOTE: The _offsetFromEndOfArray value is not affected by the _offset parameter. In other words, it is not the offset from the end of the range but from the end of the array. This number may or may not have any relation to the number of *bars* back, depending on how the array is populated. The calling code needs to figure that out.

EXPORTED ENUMS

HighestLowest

Whether to return the highest value or lowest value in the range.

• highest : Find the highest value in the specified range

• lowest : Find the lowest value in the specified range

FirstLast

Whether to return the first (lowest index) or last (highest index) occurrence of the extreme value.

• first : Return the offset of the first occurrence of the extreme value

• last : Return the offset of the last occurrence of the extreme value

TimezoneFormatIANAUTCLibrary "TimezoneFormatIANAUTC"

Provides either the full IANA timezone identifier or the corresponding UTC offset for TradingView’s built-in variables and functions.

tz(_tzname, _format)

Parameters:

_tzname (string) : "London", "New York", "Istanbul", "+1:00", "-03:00" etc.

_format (string) : "IANA" or "UTC"

Returns: "Europe/London", "America/New York", "UTC+1:00"

Example Code

import ARrowofTime/TimezoneFormatIANAUTC/1 as libtz

sesTZInput = input.string(defval = "Singapore", title = "Timezone")

example1 = libtz.tz("London", "IANA") // Return Europe/London

example2 = libtz.tz("London", "UTC") // Return UTC+1:00

example3 = libtz.tz("UTC+5", "IANA") // Return UTC+5:00

example4 = libtz.tz("UTC+4:30", "UTC") // Return UTC+4:30

example5 = libtz.tz(sesTZInput, "IANA") // Return Asia/Singapore

example6 = libtz.tz(sesTZInput, "UTC") // Return UTC+8:00

sesTime1 = time("","1300-1700", example1) // returns the UNIX time of the current bar in session time or na

sesTime2 = time("","1300-1700", example2) // returns the UNIX time of the current bar in session time or na

sesTime3 = time("","1300-1700", example3) // returns the UNIX time of the current bar in session time or na

sesTime4 = time("","1300-1700", example4) // returns the UNIX time of the current bar in session time or na

sesTime5 = time("","1300-1700", example5) // returns the UNIX time of the current bar in session time or na

sesTime6 = time("","1300-1700", example6) // returns the UNIX time of the current bar in session time or na

Parameter Format Guide

This section explains how to properly format the parameters for the tz(_tzname, _format) function.

_tzname (string) must be either;

A valid timezone name exactly as it appears in the chart’s lower-right corner (e.g. New York, London).

A valid UTC offset in ±H:MM or ±HH:MM format. Hours: 0–14 (zero-padded or not, e.g. +1:30, +01:30, -0:00). Minutes: Must be 00, 15, 30, or 45

examples;

"New York" → ✅ Valid chart label

"London" → ✅ Valid chart label

"Berlin" → ✅ Valid chart label

"America/New York" → ❌ Invalid chart label. (Use "New York" instead)

"+1:30" → ✅ Valid offset with single-digit hour

"+01:30" → ✅ Valid offset with zero-padded hour

"-05:00" → ✅ Valid negative offset

"-0:00" → ✅ Valid zero offset

"+1:1" → ❌ Invalid (minute must be 00, 15, 30, or 45)

"+2:50" → ❌ Invalid (minute must be 00, 15, 30, or 45)

"+15:00" → ❌ Invalid (hour must be 14 or below)

_tztype (string) must be either;

"IANA" → returns full IANA timezone identifier (e.g. "Europe/London"). When a time function call uses an IANA time zone identifier for its timezone argument, its calculations adjust automatically for historical and future changes to the specified region’s observed time, such as daylight saving time (DST) and updates to time zone boundaries, instead of using a fixed offset from UTC.

"UTC" → returns UTC offset string (e.g. "UTC+01:00")

fibpointLibrary "fibpoint"

A library for generating Fibonacci retracement levels on a chart, including customizable lines, labels, and filled areas between levels. It provides functionality to plot Fibonacci levels based on given price points and bar indices, with options for custom levels and colors.

getFib(startPoint, endPoint, startIdx, endIdx, fibLevels, fibColors, tsp)

Calculates Fibonacci retracement levels between two price points and draws corresponding lines and labels on the chart.

Parameters:

startPoint (float) : The starting price point for the Fibonacci retracement.

endPoint (float) : The ending price point for the Fibonacci retracement.

startIdx (int) : The bar index where the Fibonacci retracement starts.

endIdx (int) : The bar index where the Fibonacci retracement ends.

fibLevels (array) : An optional array of custom Fibonacci levels (default is ).

fibColors (array) : An optional array of colors for each Fibonacci level (default is a predefined color array).

tsp (int) : The transparency level for the fill between Fibonacci levels (default is 90).

Returns: A tuple containing an array of fibItem objects (each with a line and label) and an array of linefill objects for the filled areas between levels.

fibItem

A custom type representing a Fibonacci level with its associated line and label.

Fields:

line (series line) : The line object drawn for the Fibonacci level.

label (series label) : The label object displaying the Fibonacci level value.