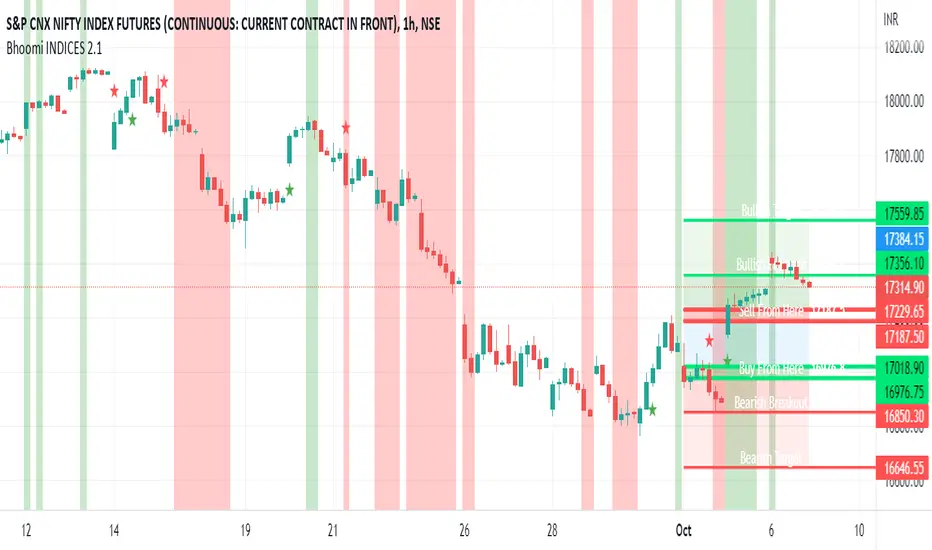

Bhoomi INDICES 2.1Bhoomi 2.0 is a Market Directional Indicator. It predicts the same by plotting respective zones and Labels.

To request access and to know more Information please contact us here.

Bhoomi 2.0 INDICES works on the Major World Indices as listed on tradingview. More to come in future, but please find the current list below. If you do not see the INDEX you trades, please comment below and we will add that for you.

"SPCFD:SPX"

"TVC:IXIC"

"DJCFD:DJI"

"TVC:NI225"

"CBOE:VIX"

"TSX:TSX"

"TVC:UKX"

"XETR:DAX"

"EURONEXT:PX1"

"EURONEXT:PX1GR"

"EURONEXT:PX1NR"

"TVC:FTMIB"

"TVC:NI225"

"TVC:KOSPI"

"TVC:SHCOMP "

"SZSE:399001"

"HSI:HSI"

"TVC:STI"

"ASX:XJO"

"NZX:NZ50G"

"TWSE:TAIEX"

"FTSEMYX:FBMKLCI"

"IDX:COMPOSITE"

"TVC:SX5E"

"BME:IBC"

"SIX:SMI"

"GPW:WIG20"

"EURONEXT:AEX"

"EURONEXT:BEL20"

"INDEX:BEL20"

"MOEX:IMOEX"

"OMXHEX:OMXH25"

"OMXICE:OMXI10"

"OMXSTO:OMXS30"

"OMXCOP:OMXC25"

"BELEX:BELEX15"

"OMXRSE:OMXRGI"

"OMXTSE:OMXTGI"

"OMXVSE:OMXVGI"

"BIST:XU100"

"TASE:TA35"

"TVC:SA40"

"NSE:NIFTY"

"BSE:SENSEX"

"DFM:DFMGI"

"TADAWUL:TASI"

"QSE:GNRI"

"BAHRAIN:BSEX"

"NSENG:NSE30"

"EGX:EGX30"

"BMFBOVESPA:IBOV"

"BMV:ME"

"BYMA:IMV"

"BVC:ICAP"

"BCS:SP_IPSA"

"BVL:SPBLPGPT"

"CURRENCYCOM:US500"

"CURRENCYCOM:US300"

"CURRENCYCOM:US100"

"CURRENCYCOM:US30"

"INDEX:DEU30"

"CBOE:VXD"

INDEX:DE40

Optionstrading

5MSM VISHNU5MSM VISHNU Indicator for Trending Markets originally written by patrick1994.

It was originally based on the MACD 12-26 and the 50 bar EMA .

The macd hist is color coded with green as buy and sell as red.

I added an option to use a couple of lower lag ema's (See line 13 - ema_signal).

5MSM VISHNU with MACD Indicator for Trending Markets

Originally written by Trading Rush

Note that the user may choose lower lags to compute the MACD signals

added lower lag ema functions - see lines 21 to 30

added plot for the MACD signal 'hist' - computed in lines 36 to 41

The extra MACD line was added for clarity for the placement of the buy sell signals.

MACD Willy StrategyThis strategy is mainly developed for scalping / intraday trading. It could potentially be used to identify entry/exit signals for short term options trading. It performs decently well on popular stocks when used on time frames between 5 min to 15 min using regular session bar data. It combines 3 popular indicators, EMA, MACD, and William %range, to generate both long and short signals.

EMA:

Default is 200 EMA line.

MACD:

Default is 12/26 lengths for fast/slow signal inputs.

William %R - Smoothed (Published):

This is a custom indicator that generates two moving average lines from the original William %R line.

How it works:

Entry conditions:

1. Long/short entries when bar closes above/below EMA line

2. Long/short entries when MACD line is above/below signal line (histogram > 0 for long, < 0 for short)

3. Long/short entries when William %R fast MA line is above/below slow MA line

Exit conditions:

1. Exit long when MACD line is below signal line, vise versa for exit short

2. Exit long when William %R fast MA line is below slow MA line, vise versa for exit short

3. Exit long when William %R fast MA line must in below the overbought (-20) limit, exit short when above the oversold (-80) limit.

***Note that parameters are NOT optimized for any particular stocks / instruments.

Enjoy~~!!

Volatility Risk Premium GOLD & SILVER 1.0ENGLISH

This indicator (V-R-P) calculates the (one month) Volatility Risk Premium for GOLD and SILVER.

V-R-P is the premium hedgers pay for over Realized Volatility for GOLD and SILVER options.

The premium stems from hedgers paying to insure their portfolios, and manifests itself in the differential between the price at which options are sold (Implied Volatility) and the volatility GOLD and SILVER ultimately realize (Realized Volatility).

I am using 30-day Implied Volatility (IV) and 21-day Realized Volatility (HV) as the basis for my calculation, as one month of IV is based on 30 calendaristic days and one month of HV is based on 21 trading days.

At first, the indicator appears blank and a label instructs you to choose which index you want the V-R-P to plot on the chart. Use the indicator settings (the sprocket) to choose one of the precious metals (or both).

Together with the V-R-P line, the indicator will show its one year moving average within a range of +/- 15% (which you can change) for benchmarking purposes. We should consider this range the “normalized” V-R-P for the actual period.

The Zero Line is also marked on the indicator.

Interpretation

When V-R-P is within the “normalized” range, … well... volatility and uncertainty, as it’s seen by the option market, is “normal”. We have a “premium” of volatility which should be considered normal.

When V-R-P is above the “normalized” range, the volatility premium is high. This means that investors are willing to pay more for options because they see an increasing uncertainty in markets.

When V-R-P is below the “normalized” range but positive (above the Zero line), the premium investors are willing to pay for risk is low, meaning they see decreasing uncertainty and risks in the market, but not by much.

When V-R-P is negative (below the Zero line), we have COMPLACENCY. This means investors see upcoming risk as being lower than what happened in the market in the recent past (within the last 30 days).

CONCEPTS :

Volatility Risk Premium

The volatility risk premium (V-R-P) is the notion that implied volatility (IV) tends to be higher than realized volatility (HV) as market participants tend to overestimate the likelihood of a significant market crash.

This overestimation may account for an increase in demand for options as protection against an equity portfolio. Basically, this heightened perception of risk may lead to a higher willingness to pay for these options to hedge a portfolio.

In other words, investors are willing to pay a premium for options to have protection against significant market crashes even if statistically the probability of these crashes is lesser or even negligible.

Therefore, the tendency of implied volatility is to be higher than realized volatility, thus V-R-P being positive.

Realized/Historical Volatility

Historical Volatility (HV) is the statistical measure of the dispersion of returns for an index over a given period of time.

Historical volatility is a well-known concept in finance, but there is confusion in how exactly it is calculated. Different sources may use slightly different historical volatility formulas.

For calculating Historical Volatility I am using the most common approach: annualized standard deviation of logarithmic returns, based on daily closing prices.

Implied Volatility

Implied Volatility (IV) is the market's forecast of a likely movement in the price of the index and it is expressed annualized, using percentages and standard deviations over a specified time horizon (usually 30 days).

IV is used to price options contracts where high implied volatility results in options with higher premiums and vice versa. Also, options supply and demand and time value are major determining factors for calculating Implied Volatility.

Implied Volatility usually increases in bearish markets and decreases when the market is bullish.

For determining GOLD and SILVER implied volatility I used their volatility indices: GVZ and VXSLV (30-day IV) provided by CBOE.

Warning

Please be aware that because CBOE doesn’t provide real-time data in Tradingview, my V-R-P calculation is also delayed, so you shouldn’t use it in the first 15 minutes after the opening.

This indicator is calibrated for a daily time frame.

----------------------------------------------------------------------

ESPAŇOL

Este indicador (V-R-P) calcula la Prima de Riesgo de Volatilidad (de un mes) para GOLD y SILVER.

V-R-P es la prima que pagan los hedgers sobre la Volatilidad Realizada para las opciones de GOLD y SILVER.

La prima proviene de los hedgers que pagan para asegurar sus carteras y se manifiesta en el diferencial entre el precio al que se venden las opciones (Volatilidad Implícita) y la volatilidad que finalmente se realiza en el ORO y la PLATA (Volatilidad Realizada).

Estoy utilizando la Volatilidad Implícita (IV) de 30 días y la Volatilidad Realizada (HV) de 21 días como base para mi cálculo, ya que un mes de IV se basa en 30 días calendario y un mes de HV se basa en 21 días de negociación.

Al principio, el indicador aparece en blanco y una etiqueta le indica que elija qué índice desea que el V-R-P represente en el gráfico. Use la configuración del indicador (la rueda dentada) para elegir uno de los metales preciosos (o ambos).

Junto con la línea V-R-P, el indicador mostrará su promedio móvil de un año dentro de un rango de +/- 15% (que puede cambiar) con fines de evaluación comparativa. Deberíamos considerar este rango como el V-R-P "normalizado" para el período real.

La línea Cero también está marcada en el indicador.

Interpretación

Cuando el V-R-P está dentro del rango "normalizado",... bueno... la volatilidad y la incertidumbre, como las ve el mercado de opciones, es "normal". Tenemos una “prima” de volatilidad que debería considerarse normal.

Cuando V-R-P está por encima del rango "normalizado", la prima de volatilidad es alta. Esto significa que los inversores están dispuestos a pagar más por las opciones porque ven una creciente incertidumbre en los mercados.

Cuando el V-R-P está por debajo del rango "normalizado" pero es positivo (por encima de la línea Cero), la prima que los inversores están dispuestos a pagar por el riesgo es baja, lo que significa que ven una disminución, pero no pronunciada, de la incertidumbre y los riesgos en el mercado.

Cuando V-R-P es negativo (por debajo de la línea Cero), tenemos COMPLACENCIA. Esto significa que los inversores ven el riesgo próximo como menor que lo que sucedió en el mercado en el pasado reciente (en los últimos 30 días).

CONCEPTOS :

Prima de Riesgo de Volatilidad

La Prima de Riesgo de Volatilidad (V-R-P) es la noción de que la Volatilidad Implícita (IV) tiende a ser más alta que la Volatilidad Realizada (HV) ya que los participantes del mercado tienden a sobrestimar la probabilidad de una caída significativa del mercado.

Esta sobreestimación puede explicar un aumento en la demanda de opciones como protección contra una cartera de acciones. Básicamente, esta mayor percepción de riesgo puede conducir a una mayor disposición a pagar por estas opciones para cubrir una cartera.

En otras palabras, los inversores están dispuestos a pagar una prima por las opciones para tener protección contra caídas significativas del mercado, incluso si estadísticamente la probabilidad de estas caídas es menor o insignificante.

Por lo tanto, la tendencia de la Volatilidad Implícita es de ser mayor que la Volatilidad Realizada, por lo cual el V-R-P es positivo.

Volatilidad Realizada/Histórica

La Volatilidad Histórica (HV) es la medida estadística de la dispersión de los rendimientos de un índice durante un período de tiempo determinado.

La Volatilidad Histórica es un concepto bien conocido en finanzas, pero existe confusión sobre cómo se calcula exactamente. Varias fuentes pueden usar fórmulas de Volatilidad Histórica ligeramente diferentes.

Para calcular la Volatilidad Histórica, utilicé el enfoque más común: desviación estándar anualizada de rendimientos logarítmicos, basada en los precios de cierre diarios.

Volatilidad Implícita

La Volatilidad Implícita (IV) es la previsión del mercado de un posible movimiento en el precio del índice y se expresa anualizada, utilizando porcentajes y desviaciones estándar en un horizonte de tiempo específico (generalmente 30 días).

IV se utiliza para cotizar contratos de opciones donde la alta Volatilidad Implícita da como resultado opciones con primas más altas y viceversa. Además, la oferta y la demanda de opciones y el valor temporal son factores determinantes importantes para calcular la Volatilidad Implícita.

La Volatilidad Implícita generalmente aumenta en los mercados bajistas y disminuye cuando el mercado es alcista.

Para determinar la Volatilidad Implícita de GOLD y SILVER utilicé sus índices de volatilidad: GVZ y VXSLV (30 días IV) proporcionados por CBOE.

Precaución

Tenga en cuenta que debido a que CBOE no proporciona datos en tiempo real en Tradingview, mi cálculo de V-R-P también se retrasa, y por este motivo no se recomienda usar en los primeros 15 minutos desde la apertura.

Este indicador está calibrado para un marco de tiempo diario.

TICK strategy for SPY optionsImportant notes:

1. This strategy is designed for same day SPY option scalping. All profit shown in back testing report is based on Profit/Loss (P/L) estimates from trading options with approximately 6 months of data. By default, it is set to 10 option contracts. By default the initial capital is set to $5000. Pyramiding is set to 3.

2. This strategy works better with non-extended market data.

3. This strategy is mainly developed for SPY trading on 5 min chart, it probably will not be very profitable with other tickers or time frame without tweaking all the parameters first.

4. This strategy will work with QQQ as well, but please adjust the profit multiplier to match the P/L of QQQ options.

How it works:

When trading the indices, many rely on the TICK for market directions. This strategy is a trend following strategy that uses a combination of conditions using the following indicators:

- TICK

- RSI

- VIX volatility index

- EMA

For entries, the conditions are:

1. TICK moving average crossover with a delayed signal line

2. Bullish or bearish RSI signal, RSI > 50 for bullish, < 50 for bearish

3. VIX must be above a certain threshold to take advantage of high market volatility

4. Price must be on top of EMA line for long, and below for short

For exits, there are 3 scenarios:

1. Stop loss set by a percentage of the daily ATR value

2. Trend changes on the TICK and the RSI

3. Bearish or bullish divergence on price with TICK

This strategy automatically signal to close all trades at 3:50 pm EST at the end of the day.

Extras:

- There is an option to show P/L for reinvesting profits

Enjoy~!!! Let's all make $$$

NCTA Aurora SystemAurora System

This system is designed to present a simple view of trending signals. The signals within the Aurora System will alert the beginning of a possible new trend. The signals also indicate when a trend is continuing or weakening, which advises the trader to adjust their stop or exit the trade. If the trend resumes, the system will print a new confirmation of an entry.

When traded properly, using a 2-3 timeframe alignment, the system will display both trending trades, which anticipate a potentially longer move, or catch trades which are likely shorter moves, which at times may be counter trend, so traders will be looking for a smaller profit.

There are two settings, CXA and PBA. CXA is more sensitive to triggering possible entries while PBA is more conservative. The system will display on the indicator which “mode” is set, CXA or PBA.

How to Use:

When the first red bar appears, labeled with a “S”, go short. This is indicating the start of a possible short trend.

When the first blue bar appears, labeled with a “L”, go long. This is indicating the start of a possible long trend.

White bars indicate a neutral or no trend.

This system can be used individually on a single time frame, but reduces chop and noise when used on a combination of time frames such as an alignment between the 3 minute and 10 minute chart for intraday trading.

3 Minute and 10 Minute Alignment Example:

For example: When the 10 minute PBA signal appears (Red bar with “S” or Blue bar with “L”), monitor the 3 minute chart for a confirmation of that signal (Red bar with “S” or Blue bar with “L”) and enter based on the 3 minute chart

At times, the 10m will first print when the 3m is on a retracement. It may take another 3 - 6 min before the 3m signals a valid entry

Exit when 10m PBA signal stops (could be a white bar or just a blank space on the indicator)

Next Bar Alert:

Included is an optional "Next Bar Alert" setting. Since many of these signals benefit from very prompt action at the beginning of a price bar, there is an additional option in Settings to set an arbitrary number of seconds to be alerted before the next price bar opens. Simply set this to a level you prefer, then set an alert in TradingView on the indicator using the "Next Bar Alert" alert parameter.

Monthly Options Expiration 2022Monthly options expiration for the year 2022.

Also you can set a flag X no. of days before the expiration date. I use it at as marker to take off existing positions in expiration week or roll to next expiration date or to place new trades.

Happy new year 2022 in advance and all the best traders.

wEMPlotDescription:

Plots the Weekly Expected Move (wEM) using the following week's Option Chain ATM Call+Put ask price to determine the EM for the following week

The wEM is the options market pricing in the expected future volatility for the following week.

The wEM is the range that the underlying price will be contained during the week 68% of the time.

These levels can be used as targets for options or equity trades for either directional or non-directional trades.

The options market in the major indices, such as SPX, can drive the overall market's order flow and so the EM can provide

useful insight into the hedging levels being used by professionals and market markers.

As Trading View does not currently provide access to option chain data, the option chain expected move for an underlying has to be manually

entered each week, but the script provides an easy to use framework to enter the parameters for the next week.

These parameters are as follows:

eg.

t1_1 = timestamp(2021, 02, 08) <==== timestamp for the start of next week (yyyy,mm,dd)

t1_2 = timestamp(2021, 02, 12) <==== timestamp for the end of next week (yyyy,mm,dd)

plotwem("QQQ", 331.36, 5.86, t1_1, t1_2, 0, 0)

^^^^

plotwem(Symbol, Close-last-week, Expected Move next week, Next week start timestamp, Next week end timestamp, Highlight-Upper-EM, Highlight-Lower-EM)

Parameters are:

Symbol : Underlying chart symbol (aka ticker). Can be a symbol for equity, future or index.

Close-last-week: Closing price at the end of last week.

Expected Move next week: The Expected Move for next week: Calculated from next week's Option Chain ATM Call+Put ask price

Next week start timestamp : Timestamp for the start of next week

Next week end timestamp : Timestamp for the end of next week

Highlight-Upper-EM : highlight upper expected move level. Set to 1 to highlight with red color. Set to 0 is no highlight.

Highlight-Lower-EM : highlight lower expected move level. Set to 1 to highlight with red color. Set to 0 is no highlight.

The highlight parameters can be updated at any point to indicate that the underlying has either touched the EM level or breached the level.

The highlights can be used to visually determine periods of market instability which can provide insight into applicable strategies for the market conditions.

Nifty-Banknifty-Option-WriterNifty-Banknifty-Option-Writer tool is having signals like below

1) Bullish signal for taking long trade

2) Bearish signal for taking short trade

3) Triangle UP signal for trend change Long trade

4) Triangle Down signal for trend change Short trade

5) Big Arrow down signal for closing long trade if u have any short trades

6) Big Arrow UP signal for closing Short trade if i have any long trades

7) This tool is having three zone GREEN, RED and GRAY

8) small red arrow and small green arrow

===========================================================================================

How to use this tool:-

You should take long trade in index call option or sell put option when you will get Bullish signal or Big green Triangle and book the profit when you get any red signal either Its Big red triangle or Bearish signal or big downward red arrow close long trade or small red arrow.

Similarly you can take long trade for Index put option or sell call option for Short trade when you get Bearish signal or Big red triangle and book the profit when you will get close long big green arrow signal or small green arrow or Bullish signal or Big green triangle.

-If candle formation is having above GREEN and GRAY zone then it signifies strength is bullish and remain in Long trade till you are not getting close long trade signal or small red downward arrow signal.

-If candle formation is happening below RED and GRAY zone then it signifies strength is bearish and remain in short trade till you are not getting close short trade signal or small green upward arrow signal.

I have taken combination of ATR, Super trend and RSI to get the trend and trend change of underlying.

this tool i have created for any underlying not specific to Nifty or Banknifty though I have used this name so Indian can take benefit for Index trading.

Still didn't understand then ping me or give me call on my number given in signature i will make zoom call with you so will understand how to use this script.

=============================================================

I have taking consideration of Bullish and Bearish trade for strategy and its giving its optimal result in 1 hr time frame.

I have added commission/slippage for trade so actual result can be displayed in strategy tester.

Ping me or DM me to subscribe this indicator.

I have given all my indicator details below link (Signature URL). You can check indicators and call me on given number or email me on given email to access the scripts and indicators. Telegram link is also given you can ping me there.

--------------------------------------------------------------------------------------------------------------------------------------

Disclaimer : Past performance of the indicator is not giving guarantee for future performance as well, it may change as per market condition.

-------------------------------------------------------------------------------------------------------------------------------------

Monthly Options Expiration 2021Monthly options expiration for the year 2021.

Also you can set a flag X no. of days before the expiration date. I use it at as marker to take off existing positions in expiration week or roll to next expiration date or to place new trades.

Happy new year 2021 in advance and all the best traders.

Volatility Price TargetsPrints lines on the chart marking the price points for the standard deviation move using historical volatility. This script was born out of a need to easily spot target points for the wings of my Iron Condor Options trades. The study only shows on the Daily chart. Volatility is calculated based on the standard deviation of the daily returns of price. Price targets are calculated off yesterday's closing price and will not reprint.

Inputs

Days to Expiration - allow you to enter the number of days to expiration for the option, default is 30 for those monthly options traders but can be adjusted to your desire.

Standard Deviation - you can enter the number of deviations for which to calculate the price points 1,2, or 3.

Days in Year - you can adjust the number of days in the year used to calculate the daily volatility multiplier.

Swing Reversal IndicatorSwing Reversal Indicator was meant to help identify pivot points on the chart which indicate momentum to buy and sell. The indicator uses 3 main questions to help plot the points:

Criteria

Did price take out yesterday's high or low?

Is today's range bigger than yesterday? (Indicates activity in price)

Is the close in the upper/lower portion of the candle? Thus, indicating momentum in that direction

This indicator was built to help me find pivot points for directional options trading however can be used for equities and forex swing trading and other strategies. Used in conjunction with a BB extreme can provide good setups.

Alerts are available for both the long and the short positions and the indicator will repaint as price moves.

The character Plotted can be changed in the settings

The size of the candle area can be changed as well if you want to tighten/loosen the trigger points based on the third question above.

Implied Volatility PercentileThis script calculates the Implied Volatility (IV) based on the daily returns of price using a standard deviation. It then annualizes the 30 day average to create the historical Implied Volatility. This indicator is intended to measure the IV for options traders but could also provide information for equities traders to show how price is extended in the expected price range based on the historical volatility.

The IV Rank (Green line) is then calculated by looking at the high and low volatility over the number of days back specified in the input parameter, default is 252 (trading days in 1 year) and then calculating the rank of the current IV compared to the High and Low. This is not as reliable as the IV Percentile as the and extreme high or low could have a side effect on the ranking but it is included for those that want to use.

The IV Percentile is calculated by counting the number of days below the current IV, then returns this as a % of the days back in the input

You can adjust the number of days back to check the IV Rank & IV Percentile if you are not wanting to look back a whole year.

This will only work on Daily or higher timeframe charts.

Future put ratio spread debit indicatorFuture Put ratio spread debit indicator developed by Chobotaru Brothers.

You need to have basic knowledge in option trading to use this indicator!

This spread is a DEBIT SPREAD.

The indicator shows P&L lines of the options strategy. Use only for futures since the mathematical model of options for Future instruments is different from stocks. Plus, the days' representation in futures is also different from stocks (stocks have fewer days than futures ).

***Each strategy in options is based on different mathematical equations, use this indicator only for the strategy in the headline.***

What does the indicator do?

The indicator is based on the Black-Scholes model, which uses partial differential equations to determine the option pricing. Due to options non-linear behavior, it is hard to visualize the option price. The indicator calculates the solutions of the Black-Scholes equation and plots them on the chart so traders can view how the option pricing will behave.

How the indicator does it?

The indicator uses five values (four dominants and one less dominant) to solve the Black-Scholes equation. The values are stock price, the strike price of the option, time to expiration, risk-free interest rate, and implied volatility .

How the indicator help the users?

-View the risks and rewards so you can know the profit targets in advance which means you can compare different options in different strikes.

-View the volatility change impact so you can know the risk and the P&L changes in case of a change in the volatility over the life of the option before you enter the trade.

-View the passage of time impact so you can know where and when you could realize a profit.

-Multi-timeframes so you can stay on the same chart (Daily and below).

All these features are to help the user improve his analysis while trading options.

How to use it?

The user needs to obtain from the “option chain” the following inputs:

-Debit paid: The debit paid for one unit of options strategy. Minimum value: 0.00001.

-Instrument price when entered spread: the stock price when you enter the options strategy.

-Upper strike price: the upper strike price of the options strategy.

-Lower strike price: the lower strike price of the options strategy.

- Upper Strike numbers of puts . This number has to be less than the number of puts that were sold.

- Lower Strike number of puts . This number has to be greater than the number of puts that were bought.

-Interest rate: find the risk-free interest rate from the U.S. DEPARTMENT OF THE TREASURY. Example: for 2% interest rate, input: 0.02.

-Days to expire: how many days until the option expires.

-Volatility: the implied volatility of the option bought/sold. Example: for 45% implied volatility , input: 0.45.

-Day of entry: A calendar day of the month that the option bought/sold.

-Month of entry: Calendar month the option bought/sold.

-Year of entry: Calendar year the option bought/sold.

After entering all the inputs, press Ok and you should see “Calculation Complete” on the chart.

The user should not change the entry date and days to expire inputs as time passes after he entered the trade.

How to access the indicator?

Use the link below to obtain access to the indicator

Future put ratio spread credit indicatorFuture Put ratio spread credit indicator developed by Chobotaru Brothers.

You need to have basic knowledge in option trading to use this indicator!

This spread is a CREDIT SPREAD.

The indicator shows P&L lines of the options strategy. Use only for futures since the mathematical model of options for Future instruments is different from stocks. Plus, the days' representation in futures is also different from stocks (stocks have fewer days than futures ).

***Each strategy in options is based on different mathematical equations, use this indicator only for the strategy in the headline.***

What does the indicator do?

The indicator is based on the Black-Scholes model, which uses partial differential equations to determine the option pricing. Due to options non-linear behavior, it is hard to visualize the option price. The indicator calculates the solutions of the Black-Scholes equation and plots them on the chart so traders can view how the option pricing will behave.

How the indicator does it?

The indicator uses five values (four dominants and one less dominant) to solve the Black-Scholes equation. The values are stock price, the strike price of the option, time to expiration, risk-free interest rate, and implied volatility .

How the indicator help the users?

-View the risks and rewards so you can know the profit targets in advance which means you can compare different options in different strikes.

-View the volatility change impact so you can know the risk and the P&L changes in case of a change in the volatility over the life of the option before you enter the trade.

-View the passage of time impact so you can know where and when you could realize a profit.

-Multi-timeframes so you can stay on the same chart (Daily and below).

All these features are to help the user improve his analysis while trading options.

How to use it?

The user needs to obtain from the “option chain” the following inputs:

-Credit received: The credit received for one unit of options strategy. Minimum value: 0.00001.

-Instrument price when entered spread: the stock price when you enter the options strategy.

-Upper strike price: the upper strike price of the options strategy.

-Lower strike price: the lower strike price of the options strategy.

- Upper Strike numbers of puts . This number has to be less than the number of puts that were sold.

- Lower Strike number of puts . This number has to be greater than the number of puts that were bought.

-Interest rate: find the risk-free interest rate from the U.S. DEPARTMENT OF THE TREASURY. Example: for 2% interest rate, input: 0.02.

-Days to expire: how many days until the option expires.

-Volatility: the implied volatility of the option bought/sold. Example: for 45% implied volatility , input: 0.45.

-Day of entry: A calendar day of the month that the option bought/sold.

-Month of entry: Calendar month the option bought/sold.

-Year of entry: Calendar year the option bought/sold.

After entering all the inputs, press Ok and you should see “Calculation Complete” on the chart.

The user should not change the entry date and days to expire inputs as time passes after he entered the trade.

How to access the indicator?

Use the link below to obtain access to the indicator

Future call ratio spread debit indicatorFuture Call ratio spread debit indicator developed by Chobotaru Brothers.

You need to have basic knowledge in option trading to use this indicator!

This spread is a DEBIT SPREAD.

The indicator shows P&L lines of the options strategy. Use only for stocks since the mathematical model of options for Future instruments is different from futures . Plus, the days' representation in futures is also different from stocks (stocks have fewer days than futures ).

***Each strategy in options is based on different mathematical equations, use this indicator only for the strategy in the headline.***

What does the indicator do?

The indicator is based on the Black-Scholes model, which uses partial differential equations to determine the option pricing. Due to options non-linear behavior, it is hard to visualize the option price. The indicator calculates the solutions of the Black-Scholes equation and plots them on the chart so traders can view how the option pricing will behave.

How the indicator does it?

The indicator uses five values (four dominants and one less dominant) to solve the Black-Scholes equation. The values are stock price, the strike price of the option, time to expiration, risk-free interest rate, and implied volatility .

How the indicator help the users?

-View the risks and rewards so you can know the profit targets in advance which means you can compare different options in different strikes.

-View the volatility change impact so you can know the risk and the P&L changes in case of a change in the volatility over the life of the option before you enter the trade.

-View the passage of time impact so you can know where and when you could realize a profit.

-Multi-timeframes so you can stay on the same chart (Daily and below).

All these features are to help the user improve his analysis while trading options.

How to use it?

The user needs to obtain from the “option chain” the following inputs:

-Debit paid: The debit paid for one unit of options strategy. Minimum value: 0.00001.

-Instrument price when entered spread: the stock price when you enter the options strategy.

-Upper strike price: the upper strike price of the options strategy.

-Lower strike price: the lower strike price of the options strategy.

- Upper Strike numbers of calls . This number has to be greater than the number of calls that were bought.

- Lower Strike number of calls . This number has to be less than the number of calls that were sold.

-Interest rate: find the risk-free interest rate from the U.S. DEPARTMENT OF THE TREASURY. Example: for 2% interest rate, input: 0.02.

-Days to expire: how many days until the option expires.

-Volatility: the implied volatility of the option bought/sold. Example: for 45% implied volatility , input: 0.45.

-Day of entry: A calendar day of the month that the option bought/sold.

-Month of entry: Calendar month the option bought/sold.

-Year of entry: Calendar year the option bought/sold.

After entering all the inputs, press Ok and you should see “Calculation Complete” on the chart.

The user should not change the entry date and days to expire inputs as time passes after he entered the trade.

How to access the indicator?

Use the link below to obtain access to the indicator

Future Call ratio spread credit indicatorFuture Call ratio spread credit indicator developed by Chobotaru Brothers.

You need to have basic knowledge in option trading to use this indicator!

This spread is a CREDIT SPREAD.

The indicator shows P&L lines of the options strategy. Use only for futures since the mathematical model of options for Future instruments is different from stocks. Plus, the days' representation in futures is also different from stocks (stocks have fewer days than futures ).

***Each strategy in options is based on different mathematical equations, use this indicator only for the strategy in the headline.***

What does the indicator do?

The indicator is based on the Black-Scholes model, which uses partial differential equations to determine the option pricing. Due to options non-linear behavior, it is hard to visualize the option price. The indicator calculates the solutions of the Black-Scholes equation and plots them on the chart so traders can view how the option pricing will behave.

How the indicator does it?

The indicator uses five values (four dominants and one less dominant) to solve the Black-Scholes equation. The values are stock price, the strike price of the option, time to expiration, risk-free interest rate, and implied volatility .

How the indicator help the users?

-View the risks and rewards so you can know the profit targets in advance which means you can compare different options in different strikes.

-View the volatility change impact so you can know the risk and the P&L changes in case of a change in the volatility over the life of the option before you enter the trade.

-View the passage of time impact so you can know where and when you could realize a profit.

-Multi-timeframes so you can stay on the same chart (Daily and below).

All these features are to help the user improve his analysis while trading options.

How to use it?

The user needs to obtain from the “option chain” the following inputs:

-Credit received: The credit received for one unit of options strategy. Minimum value: 0.00001.

-Instrument price when entered spread: the stock price when you enter the options strategy.

-Upper strike price: the upper strike price of the options strategy.

-Lower strike price: the lower strike price of the options strategy.

- Upper Strike numbers of calls . This number has to be greater than the number of calls that were bought.

- Lower Strike number of calls . This number has to be less than the number of calls that were sold.

-Interest rate: find the risk-free interest rate from the U.S. DEPARTMENT OF THE TREASURY. Example: for 2% interest rate, input: 0.02.

-Days to expire: how many days until the option expires.

-Volatility: the implied volatility of the option bought/sold. Example: for 45% implied volatility , input: 0.45.

-Day of entry: A calendar day of the month that the option bought/sold.

-Month of entry: Calendar month the option bought/sold.

-Year of entry: Calendar year the option bought/sold.

After entering all the inputs, press Ok and you should see “Calculation Complete” on the chart.

The user should not change the entry date and days to expire inputs as time passes after he entered the trade.

How to access the indicator?

Use the link below to obtain access to the indicator

Future Put Bull Spread indicatorFuture Put bull spread indicator developed by Chobotaru Brothers.

You need to have basic knowledge in option trading to use this indicator!

This spread is a CREDIT SPREAD.

The indicator shows P&L lines of the options strategy. Use only for futures since the mathematical model of options for Future instruments is different from stocks. Plus, the days' representation in futures is also different from stocks (stocks have fewer days than futures ).

***Each strategy in options is based on different mathematical equations, use this indicator only for the strategy in the headline.***

What does the indicator do?

The indicator is based on the Black-Scholes model, which uses partial differential equations to determine the option pricing. Due to options non-linear behavior, it is hard to visualize the option price. The indicator calculates the solutions of the Black-Scholes equation and plots them on the chart so traders can view how the option pricing will behave.

How the indicator does it?

The indicator uses five values (four dominants and one less dominant) to solve the Black-Scholes equation. The values are stock price, the strike price of the option, time to expiration, risk-free interest rate, and implied volatility .

How the indicator help the users?

-View the risks and rewards so you can know the profit targets in advance which means you can compare different options in different strikes.

-View the volatility change impact so you can know the risk and the P&L changes in case of a change in the volatility over the life of the option before you enter the trade.

-View the passage of time impact so you can know where and when you could realize a profit.

-Multi-timeframes so you can stay on the same chart (Daily and below).

All these features are to help the user improve his analysis while trading options.

How to use it?

The user needs to obtain from the “option chain” the following inputs:

- Put spread price (Credit): The credit received for one unit of options strategy.

-Instrument price when entered spread: the stock price when you enter the options strategy.

-Upper strike price: the upper strike price of the options strategy.

-Lower strike price: the lower strike price of the options strategy.

-Interest rate: find the risk-free interest rate from the U.S. DEPARTMENT OF THE TREASURY. Example: for 2% interest rate, input: 0.02.

-Days to expire: how many days until the option expires.

-Volatility: the implied volatility of the option bought/sold. Example: for 45% implied volatility , input: 0.45.

-Day of entry: A calendar day of the month that the option bought/sold.

-Month of entry: Calendar month the option bought/sold.

-Year of entry: Calendar year the option bought/sold.

-% of Max Profit/Loss: Profit/loss line defined by the user. Minimum input (-0.95) ; maximum input (0.95).

Example: In this spread, -0.95 means, 95% of the options strategy maximum loss is reached and, 0.95 means, 95% of the options strategy maximum profit is reached.

After entering all the inputs, press Ok and you should see “Calculation Complete” on the chart.

The user should not change the entry date and days to expire inputs as time passes after he entered the trade.

How to access the indicator?

Use the link below to obtain access to the indicator

Future Put bear spread indicatorFuture Put bear spread indicator developed by Chobotaru Brothers.

You need to have basic knowledge in option trading to use this indicator!

This spread is a DEBIT SPREAD.

The indicator shows P&L lines of the options strategy. Use only for futures since the mathematical model of options for Future instruments is different from stocks. Plus, the days' representation in futures is also different from stocks (stocks have fewer days than futures ).

***Each strategy in options is based on different mathematical equations, use this indicator only for the strategy in the headline.***

What does the indicator do?

The indicator is based on the Black-Scholes model, which uses partial differential equations to determine the option pricing. Due to options non-linear behavior, it is hard to visualize the option price. The indicator calculates the solutions of the Black-Scholes equation and plots them on the chart so traders can view how the option pricing will behave.

How the indicator does it?

The indicator uses five values (four dominants and one less dominant) to solve the Black-Scholes equation. The values are stock price, the strike price of the option, time to expiration, risk-free interest rate, and implied volatility .

How the indicator help the users?

-View the risks and rewards so you can know the profit targets in advance which means you can compare different options in different strikes.

-View the volatility change impact so you can know the risk and the P&L changes in case of a change in the volatility over the life of the option before you enter the trade.

-View the passage of time impact so you can know where and when you could realize a profit.

-Multi-timeframes so you can stay on the same chart (Daily and below).

All these features are to help the user improve his analysis while trading options.

How to use it?

The user needs to obtain from the “option chain” the following inputs:

- Put spread price (Debit): The debit paid for one unit of options strategy.

-Instrument price when entered spread: the stock price when you enter the options strategy.

-Upper strike price: the upper strike price of the options strategy.

-Lower strike price: the lower strike price of the options strategy.

-Interest rate: find the risk-free interest rate from the U.S. DEPARTMENT OF THE TREASURY. Example: for 2% interest rate, input: 0.02.

-Days to expire: how many days until the option expires.

-Volatility: the implied volatility of the option bought/sold. Example: for 45% implied volatility , input: 0.45.

-Day of entry: A calendar day of the month that the option bought/sold.

-Month of entry: Calendar month the option bought/sold.

-Year of entry: Calendar year the option bought/sold.

-% of Max Profit/Loss: Profit/loss line defined by the user. Minimum input (-0.95) ; maximum input (0.95).

Example: In this spread, -0.95 means, 95% of the options strategy maximum loss is reached and, 0.95 means, 95% of the options strategy maximum profit is reached.

After entering all the inputs, press Ok and you should see “Calculation Complete” on the chart.

The user should not change the entry date and days to expire inputs as time passes after he entered the trade.

How to access the indicator?

Use the link below to obtain access to the indicator

Future Iron Condor / Butterfly buy or sell indicatorFuture Iron Condor / butterfly indicator developed by Chobotaru Brothers.

You need to have basic knowledge in option trading to use this indicator!

The indicator shows P&L lines of the options strategy. Use only for futures since the mathematical model of options for Future instruments is different from stocks. Plus, the days' representation in futures is also different from stocks (stocks have fewer days than futures ).

***Each strategy in options is based on different mathematical equations, use this indicator only for the strategy in the headline.***

What does the indicator do?

The indicator is based on the Black-Scholes model, which uses partial differential equations to determine the option pricing. Due to options non-linear behavior, it is hard to visualize the option price. The indicator calculates the solutions of the Black-Scholes equation and plots them on the chart so traders can view how the option pricing will behave.

How the indicator does it?

The indicator uses five values (four dominants and one less dominant) to solve the Black-Scholes equation. The values are stock price, the strike price of the option, time to expiration, risk-free interest rate, and implied volatility .

How the indicator help the users?

-View the risks and rewards so you can know the profit targets in advance which means you can compare different options in different strikes.

-View the volatility change impact so you can know the risk and the P&L changes in case of a change in the volatility over the life of the option before you enter the trade.

-View the passage of time impact so you can know where and when you could realize a profit.

-Multi-timeframes so you can stay on the same chart (Daily and below).

All these features are to help the user improve his analysis while trading options.

How to use it?

The user needs to obtain from the “option chain” the following inputs:

-Buy or sell (the strategy)

- Iron Condor price bought/sold: enter the price that you bought/sold one options strategy.

-Instrument price when bought/sold: the stock price when you bought/sold the options strategy.

-Upper strike price Top: the top upper strike price of the options strategy.

-Lower strike price Top: the top lower strike price of the options strategy.

-Upper strike price Bottom: the bottom upper strike price of the options strategy.

-Lower strike price Bottom: the bottom lower strike price of the options strategy.

-Interest rate: find the risk-free interest rate from the U.S. DEPARTMENT OF THE TREASURY. Example: for 2% interest rate, input: 0.02.

-Days to expire: how many days until the option expires.

-Volatility: the implied volatility of the option bought/sold. Example: for 45% implied volatility , input: 0.45.

-Day of entry: A calendar day of the month that the option bought/sold.

-Month of entry: Calendar month the option bought/sold.

-Year of entry: Calendar year the option bought/sold.

-% of Profit/Loss: Profit/loss line defined by the user. Minimum input (-0.95) ; maximum input (0.95).

Example: If the strategy was bought, -0.95 means, 95% of the options strategy maximum loss is reached. : If the strategy was bought, 0.95 means, 95% of the options strategy maximum profit is reached.

After entering all the inputs, press Ok and you should see “Calculation Complete” on the chart.

The user should not change the entry date and days to expire inputs as time passes after he entered the trade.

How to access the indicator?

Use the link below to obtain access to the indicator

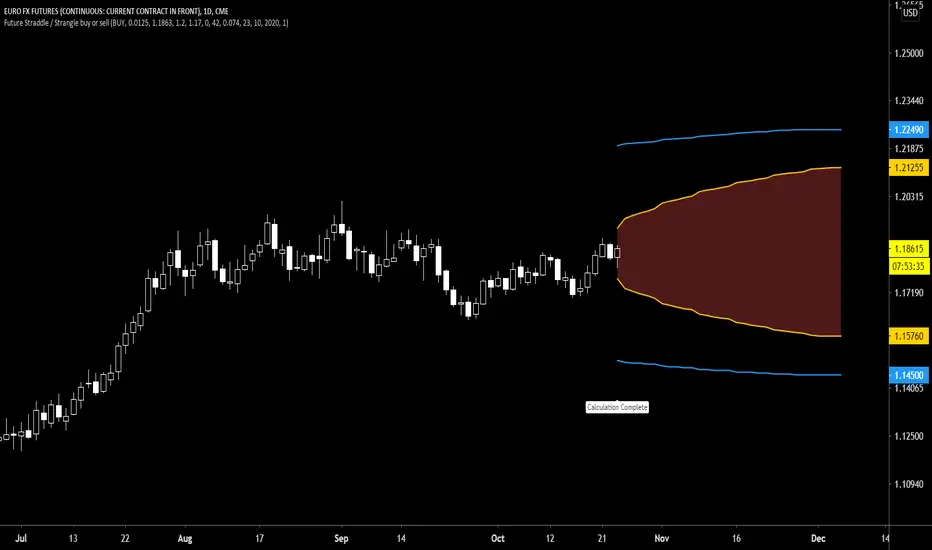

Future Straddle / Strangle buy or sell indicatorFuture Straddle / strangle buy or sell indicator developed by Chobotaru Brothers.

You need to have basic knowledge in option trading to use this indicator!

The indicator shows P&L lines of the options strategy. Use only for futures since the mathematical model of options for Future instruments is different from stocks. Plus, the days' representation in futures is also different from stocks (stocks have fewer days than futures ).

***Each strategy in options is based on different mathematical equations, use this indicator only for the strategy in the headline.***

What does the indicator do?

The indicator is based on the Black-Scholes model, which uses partial differential equations to determine the option pricing. Due to options non-linear behavior, it is hard to visualize the option price. The indicator calculates the solutions of the Black-Scholes equation and plots them on the chart so traders can view how the option pricing will behave.

How the indicator does it?

The indicator uses five values (four dominants and one less dominant) to solve the Black-Scholes equation. The values are stock price, the strike price of the option, time to expiration, risk-free interest rate, and implied volatility .

How the indicator help the users?

-View the risks and rewards so you can know the profit targets in advance which means you can compare different options in different strikes.

-View the volatility change impact so you can know the risk and the P&L changes in case of a change in the volatility over the life of the option before you enter the trade.

-View the passage of time impact so you can know where and when you could realize a profit.

-Multi-timeframes so you can stay on the same chart (Daily and below).

All these features are to help the user improve his analysis while trading options.

How to use it?

The user needs to obtain from the “option chain” the following inputs:

-Buy or sell (the strategy)

- Straddle/strangle price bought/sold: enter the price that you bought/sold one options strategy.

-Instrument price when bought/sold: the stock price when you bought/sold the options strategy.

-Upper strike price: the upper strike price of the options strategy.

-Lower strike price: the lower strike price of the options strategy.

-Interest rate: find the risk-free interest rate from the U.S. DEPARTMENT OF THE TREASURY. Example: for 2% interest rate, input: 0.02.

-Days to expire: how many days until the option expires.

-Volatility: the implied volatility of the option bought/sold. Example: for 45% implied volatility , input: 0.45.

-Day of entry: A calendar day of the month that the option bought/sold.

-Month of entry: Calendar month the option bought/sold.

-Year of entry: Calendar year the option bought/sold.

-Risk to reward: Profit/loss line defined by the user. Minimum input (-0.95) ; maximum input (3).

Example: If the strategy was bought, -0.95 means, 95% of the options strategy value is lost (unrealized). If the strategy was bought, 3 means, the risk to reward is 3.

After entering all the inputs, press Ok and you should see “Calculation Complete” on the chart.

The user should not change the entry date and days to expire inputs as time passes after he entered the trade.

How to access the indicator?

Use the link below to obtain access to the indicator

Future Call Bear Spread indicatorFuture Call bear spread indicator developed by Chobotaru Brothers.

You need to have basic knowledge in option trading to use this indicator!

This spread is a CREDIT SPREAD.

The indicator shows P&L lines of the options strategy. Use only for futures since the mathematical model of options for Future instruments is different from stocks. Plus, the days' representation in futures is also different from stocks (stocks have fewer days than futures ).

***Each strategy in options is based on different mathematical equations, use this indicator only for the strategy in the headline.***

What does the indicator do?

The indicator is based on the Black-Scholes model, which uses partial differential equations to determine the option pricing. Due to options non-linear behavior, it is hard to visualize the option price. The indicator calculates the solutions of the Black-Scholes equation and plots them on the chart so traders can view how the option pricing will behave.

How the indicator does it?

The indicator uses five values (four dominants and one less dominant) to solve the Black-Scholes equation. The values are stock price, the strike price of the option, time to expiration, risk-free interest rate, and implied volatility .

How the indicator help the users?

-View the risks and rewards so you can know the profit targets in advance which means you can compare different options in different strikes.

-View the volatility change impact so you can know the risk and the P&L changes in case of a change in the volatility over the life of the option before you enter the trade.

-View the passage of time impact so you can know where and when you could realize a profit.

-Multi-timeframes so you can stay on the same chart (Daily and below).

All these features are to help the user improve his analysis while trading options.

How to use it?

The user needs to obtain from the “option chain” the following inputs:

- Call spread price (Credit): The credit received for one unit of options strategy.

-Instrument price when entered spread: the stock price when you enter the options strategy.

-Upper strike price: the upper strike price of the options strategy.

-Lower strike price: the lower strike price of the options strategy.

-Interest rate: find the risk-free interest rate from the U.S. DEPARTMENT OF THE TREASURY. Example: for 2% interest rate, input: 0.02.

-Days to expire: how many days until the option expires.

-Volatility: the implied volatility of the option bought/sold. Example: for 45% implied volatility , input: 0.45.

-Day of entry: A calendar day of the month that the option bought/sold.

-Month of entry: Calendar month the option bought/sold.

-Year of entry: Calendar year the option bought/sold.

-% of Max Profit/Loss: Profit/loss line defined by the user. Minimum input (-0.95) ; maximum input (0.95).

Example: In this spread, -0.95 means, 95% of the options strategy maximum loss is reached and, 0.95 means, 95% of the options strategy maximum profit is reached.

After entering all the inputs, press Ok and you should see “Calculation Complete” on the chart.

The user should not change the entry date and days to expire inputs as time passes after he entered the trade.

How to access the indicator?

Use the link below to obtain access to the indicator

Future Call bull spread indicatorFuture Call bull spread indicator developed by Chobotaru Brothers.

You need to have basic knowledge in option trading to use this indicator!

This spread is a DEBIT SPREAD.

The indicator shows P&L lines of the options strategy. Use only for futures since the mathematical model of options for Future instruments is different from stocks. Plus, the days' representation in futures is also different from stocks (stocks have fewer days than futures ).

***Each strategy in options is based on different mathematical equations, use this indicator only for the strategy in the headline.***

What does the indicator do?

The indicator is based on the Black-Scholes model, which uses partial differential equations to determine the option pricing. Due to options non-linear behavior, it is hard to visualize the option price. The indicator calculates the solutions of the Black-Scholes equation and plots them on the chart so traders can view how the option pricing will behave.

How the indicator does it?

The indicator uses five values (four dominants and one less dominant) to solve the Black-Scholes equation. The values are stock price, the strike price of the option, time to expiration, risk-free interest rate, and implied volatility .

How the indicator help the users?

-View the risks and rewards so you can know the profit targets in advance which means you can compare different options in different strikes.

-View the volatility change impact so you can know the risk and the P&L changes in case of a change in the volatility over the life of the option before you enter the trade.

-View the passage of time impact so you can know where and when you could realize a profit.

-Multi-timeframes so you can stay on the same chart (Daily and below).

All these features are to help the user improve his analysis while trading options.

How to use it?

The user needs to obtain from the “option chain” the following inputs:

- Call spread price (Debit): The debit paid for one unit of options strategy.

-Instrument price when entered spread: the stock price when you enter the options strategy.

-Upper strike price: the upper strike price of the options strategy.

-Lower strike price: the lower strike price of the options strategy.

-Interest rate: find the risk-free interest rate from the U.S. DEPARTMENT OF THE TREASURY. Example: for 2% interest rate, input: 0.02.

-Days to expire: how many days until the option expires.

-Volatility: the implied volatility of the option bought/sold. Example: for 45% implied volatility , input: 0.45.

-Day of entry: A calendar day of the month that the option bought/sold.

-Month of entry: Calendar month the option bought/sold.

-Year of entry: Calendar year the option bought/sold.

-% of Max Profit/Loss: Profit/loss line defined by the user. Minimum input (-0.95) ; maximum input (0.95).

Example: In this spread, -0.95 means, 95% of the options strategy maximum loss is reached and, 0.95 means, 95% of the options strategy maximum profit is reached.

After entering all the inputs, press Ok and you should see “Calculation Complete” on the chart.

The user should not change the entry date and days to expire inputs as time passes after he entered the trade.

How to access the indicator?

Use the link below to obtain access to the indicator