(JS) Multi-Time Frame Pivot Point Detector 2.0So here's an updated version of my automatic Pivot Point detector.

If you don't like having a bunch of Pivots on your chart at once, or having to cycle through various resolutions to see different ones, this is for you!

What does this indicator do? It automatically detects the nearest daily, weekly, and monthly pivot points both above and below the current price and automatically plots them for you. It's really just as simple as that.

You select how far back you want it to plot with the "Pivot Point Look Back Period" option.

I also have transparency options for each type of pivot so its easy to find the opacity you prefer and save it as a default setting.

With "Turn Off Each Pivot Point On All Time Frames" turned on, as an example, if you were to uncheck "S1/R1" then it turns S1/R1 plots off across all 3 pivot resolutions. By default however, I have it set where you can pick and choose each one individually.

I also added the default "VWAP Periodic" script from TradingView in there with it (not in prior version). This works identical to the built in indicator (because it is identical).

Trading algorithms like to target pivot points and liquidity, so I figured they would pair together nicely for active trading.

D-VWAP

Midas 6 Anchored VWAP [xdecow]This script plots 6 anchored vwap from the selected bars.

The labels are only to help identify the starting points and can be disabled in the options.

VWAP MTF TT by Chill00rThis is an "Volume-weighted Average Price" Indicator for Multi Timeframe.

VWAP color is trend-based

Different settings are available (some are off by default):

"Show Daily VWAP"

"Show Weekly VWAP"

"Show Monthly VWAP"

"Show Quarterly VWAP"

"Show Yearly VWAP"

"Show previous VWAP close"

Hit the Like Button

My VWAP Reversal + Pivot Points StandardThis indicator, with the addition of a standard VWAP indicator to the 5m chart, helps the operator when using a closing candle Price to initiate a VWAP Reversal strategy.

The strategy involves Price gapping up, look for a Close below the 1st 5m candle Low; else look for a Close above the 1st 5m candle High. On a break of VWAP, take the trade in the opposite direction of the gap, hence the VWAP Reversal. Not my own strat, credit to T3 Newsbeat, publicly posted on YouTube.

The Pivot Points Standard in the Pine 4 user manual, was the base source code, and leaving it here will allow me to remove the PP indicator I was using.

[HM] VWAP Envelope dinamic intraday v1- VWAP, volume weighted average price;

- Plus Envelope bands:

1) Dinamic, adjusted by volatility:

- - - daily ATR or

- - - daily Standard Deviation

2) or simple fixed % increments bands, defined by user.

# Intraday timeframe only.

# If volume data is absent, the indicator will not work at all.

Hope this could help the community.

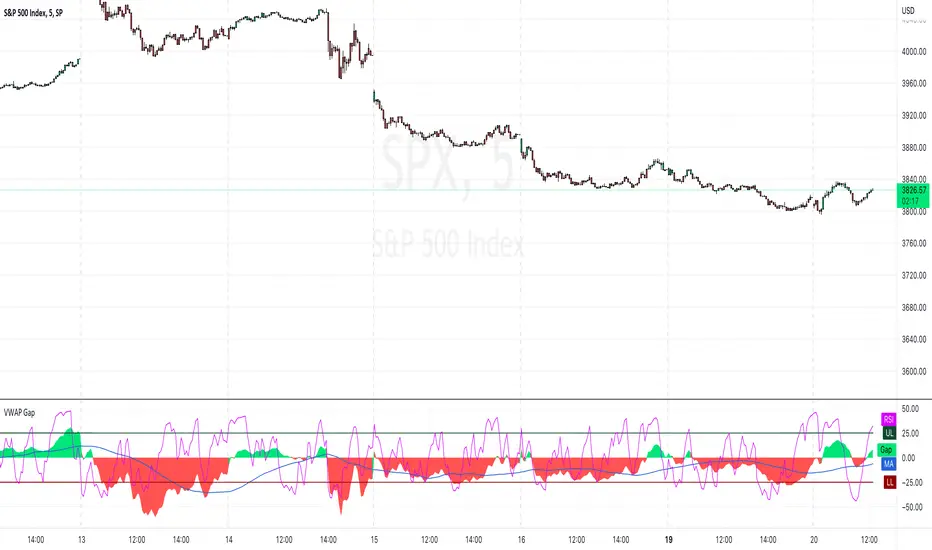

VWAP Gap [AR]This simple indicator measure the difference between price and VWAP line

The VWAP Gap indicator works best on intraday charts

SET-UP INFO

1. Add VWAP to your chart and set it up

2. Open "VWAP Gap Indicator" settings

3. Change source to "VWAP"

Enjoy!

Alex R.

Scalp King v2.0 - Multi-time VWAP, multi-condition alertsMulti time-range VWAP with Multiple condition alerts - version 2.0 - by Viral Killer

This is a script that contains 3 VWAP modes, 5 min, 60 min and 240 min timeframes, all on the same indicator. You add it to the 5 min chart, but seems to work on other ranges.

Usually, when the VWAP wave crosses above, it is a buy signal, although not perfect. This ensures there is also a MAC-D buy confirmation, for a much stronger buy signal.

You can setup SUPER alerts which ensure multiple time ranges line up, before alerting. Some are already built in.

Yellow Wave is 5 min VWAP , crossing from below into positive is a buy signal. Note the word signal, not guaranteed buy.

Orange Wave is 60 min VWAP , crossing from below into positive is a buy signal.

Purple Wave is 240 min VWAP , crossing from below into positive is a buy signal.

The blue wave is 5 the minutes RSI and the other lines are 1h/4h, corresponding to oversold and overbought signals.

U will see a trail of red and blue arrows on the MAC-D, this script knows when the MAC-D is losing power.

Green dots are a buy, dark dots are a sell. Green with orange rim is a weak buy.

If you see 2 or 3 green dots from different time frames very close together, that is a much stronger buy signal. If the MAC-D also agrees, well, it is very strong. This is shown as blue circle white arrow up.

Exit when you see a red cross or red arrow down, RSI overbought and MAC-D crossing down respectively.

You can use multi condition alerts, i.e. alert me to a STRONG BUY when 5 min VWAP crossed above while the 60 min is positive too, aaaand the MAC-D agrees.

Enjoy.

-Viral Killer

Rolling Anchored VWAPRolling Anchored VWAP

This is my Rolling Anchored VWAP. Instead of being anchored to a fixed point of time, its anchored to a specific time-frame (ex. 24 hours to the minute) so the anchor point is constantly moving with time.

Enjoy

VWAP Standard DeviationsVWAP Standard Deviations

VWAPSD is an indicator that can be used to identify Support & Resistance lines based on Volume per Price.

Such an indicator can be easily used to place a limit order on the SR levels

PivotBoss Vwap BandsThis script has the Vwap and three standard deviation to it. Used for mean reversion

Anchored VWAP w/ Stdev and VWMA CloudThis is a fun little project that allows you to anchor the Volume Weighed Average Price (VWAP) to a specific day and plot up to 4 standard deviations up or down.

I've also added a Volume Weighted Moving Average (VWMA) plot and accompanying cloud to more easily visualize how volume-based momentum affects trends.

Typically, you'll see price respecting the VWMA Cloud and can expect price bounces off of the VWAP standard deviations.

When setting the initial anchor point, it's best to select a day with high volume and volatility.

This idea is not 100% original, but I couldn't find 1) a public script combining the ideas and 2) the correct plotting of the standard deviation via accumulation.

Happy Trading!

FAQ

Why is your script Protected?

Users like to take my open-source code and charge to use it without my permission.

How do I use this to trade?

Add it to your chart and see what stacks up with your current setup. I trade Forex, so what looks bad on my charts might look golden on yours.

How long have you been doing this?

I've been coding for about 8 years and actively trading for 2 years. My degree is in Robotics Engineering and I became obsessed with investing at 22.

How do you trade?

Hurst + SNR + MESA MAMA + ATR + LSTM + Pure Grid. You can't completely code this setup using Pinescript, but if you learn C++ or Python you're there!

Are your returns good?

I average 0.68% every weekday or 22.65% monthly, using the method above.

Can you build my indicator or strategy?

Absolutely! If it hasn't been done before and it improves our community, then consider it done.

But can you build an indicator or strategy for me and only me?

Citing the house rules, I cannot solicit for any purpose. So saying "PM me" would be a grievous violation of said rules, obviously.

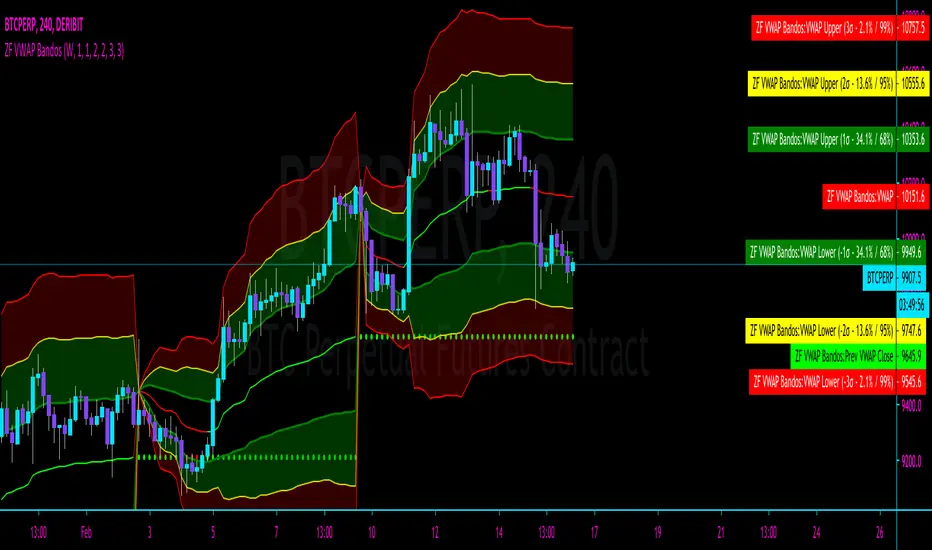

ZFelds' OrderFlow VWAP BandosVWAP with 3 standard deviations, based on the "Orderflow VWAP from NinjaTrader.

When Price is ABOVE VWAP = VWAP turns GREEN

When Price is BELOW VWAP = VWAP turns RED

The Standard Deviation Bands are considered "echoes" of the VWAP with different multipliers, acting as support/resistance and areas of interest.

Big thanks to @CryptoMF and @Barnz from The Cave for the assistance with this indicator.

VWAP TF-Aware===========================================================

8/Feb/2020 02:57 PM AUTHOR: Brandon Gum

-

DESCRIPTION:

This is a timeframe aware VWAP indicator. The built-in VWAP indicator was changed in late 2019 which resulted in it no longer being restricted to low timeframes. As a result the indicator would plot on higher timeframe charts and create "noise" between candles.

This Version of vwap only displays vwap on 30 minute and below times frames.

===========================================================

NSDT Triple VWAP with Adjustable Start TimesAllows you to plot 3 VWAP's with 3 different start times. Very useful for trading futures where there are multiple sessions involved. Can also be used with stocks to set as previous day, pre-market, and market open.

[KICK] Ultimate VWAPsThis indicator provides numerous indicator tools/functions all related to Volume Weighted Price Averages (VWAPs). Specifically the ability to add multiple anchored VWAPs to arbitrary points (highs, lows, significant events such as earnings , flash crashes, etc...) is a very powerful way to see where market participants that were active at those times are in regards those positions relative to current price.

With this indicator you can:

Enable a typical session-based VWAP (resets every session) - does not render line from last candle of session to first candle of new session so as to keep your charts looking a bit neater.

Enable a week-to-date VWAP , month-to-date VWAP , or year-to-date VWAP

Enable an anchored VWAP that can be automatically anchored to the high within the last week (timeframe independent) or to a high within a certain number of candles back, or set to a specific date and time. There is also an "ignore" recent candle filter if using the candle range method for auto-locating the high.

Enable an anchored VWAP that can be automatically anchored to the low within the last week (timeframe independent) or to a low within a certain number of candles back, or set to a specific date and time. There is also an "ignore recent candle" filter if using the candle range method for auto-locating the low.

The week/month/year-to-date VWAP can also be treated as an Ad-Hoc anchored VWAP and have it’s anchor set to an arbitrary date and time.

A support/resistance line can be added in for the last session’s VWAP close.

Z-Score bands can be added (band values configurable) and attached to any of the above VWAPs (Session, AutoHigh, AutoLow, AdHoc/Week/Month/Year). These are calculated using the proper unbiased standard deviation calculation (not the built in PineScript biased stdev function).

(note: not all functionality is shown in the chart above because it would be a mess - all the options for this indicator are not necessarily intended to be used simultaneously on the same chart, though they can be if you really like that sort of thing)

Use the link below to watch a tutorial video, request a trial, or purchase for access.

[ProfitTrailer] MVWAPPERCENTAGE Buy/Sell StudyProfitTrailer buy/sell study for MVWAPPERCENTAGE strategy.

The script highlights the region where trailing is most likely to succeed.

[ProfitTrailer] VWAPPERCENTAGE Buy/Sell StudyProfitTrailer buy/sell study for VWAPPERCENTAGE strategy.

The script highlights the region where trailing is most likely to succeed.

Flunki ZWAPometer Lite - ZWAP Trend Strength

Simple version of the ZWAPometer

Measures bars since ZWAP peak, effectively showing trend strength.

See previous indicator for more detail.

This does not show trend direction, only when it is exhausted, whether it is bull or bear will require other confirmation.

So in summary, this tracks bars since price hit a peak distance away from VWAP , indicating price will revert back to VWAP .

Enjoy,

Flunkimoku

Flunki ZWAPometer - ZWAP Resets / Extremes

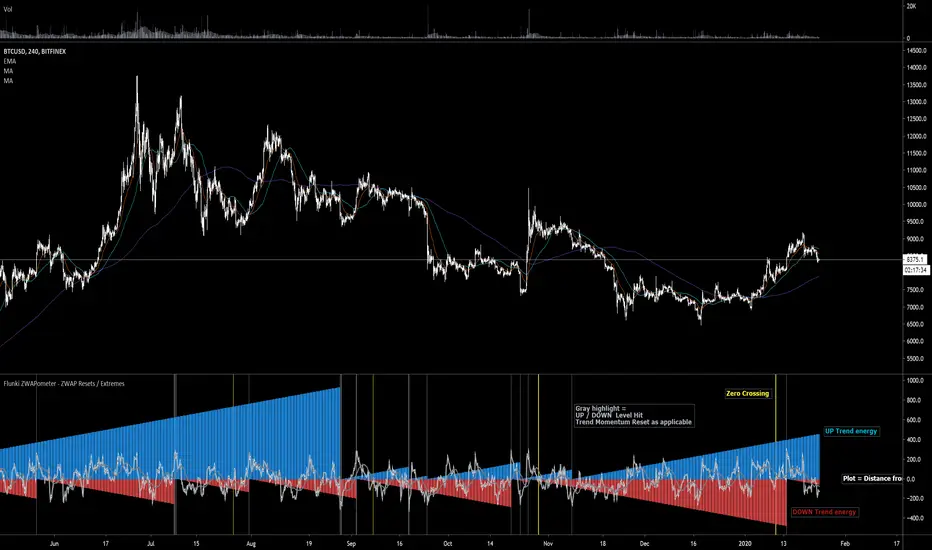

Here with another VWAP based indicator, this time using ZWAP (distance from VWAP) and flagging the extremities and crosses of each side, and graphing the bars since the last breach.

This basically gives a Bull / Bear energy / momentum

Yellow highlights = zero crossing , not entirely sure this is useful as of yet, but can give an early warning of a change - let me know if you find a genuine use for it !

Gray highlights = extreme reached, this generally signals exhaustion of the trend energy for Bull or Bear (depending on which side is reset obviously)

May develop further ; add bar colour options and more precise highlights, but only if it's of use to anyone.

Enjoy !

Flunkimoku

VWAP-ATRstopAdapted ATR-stop with only VWAP and ATR.

Didnt test it, feel free to use it the way you want. You can turn off the bar color function and change any config.

Anchored VWAPPine implementation of VWAP, similar to build-in, with anchors to Session, Week, Month and Year

VWAPVWMAATRAdapted ATR that i am using in BTC 15M charts. It is an usual ATR-Stop smoothed by a VWAP and a VWMA.

This crazy config i am using only for BTC, but i found others configs with others assets, like brlusd contracts.

You can turn off the barcolor function and change the lenght of the VWAP and VWMA.

Multiple VWAPAn intraday indicator which plots the 3 different VWAP.

1. D-VWAP shows VWAP from the first candle of the day

2. W-VWAP shows VWAP from the first candle of the week

3. M-VWAP shows VWAP from the first candle of the month