GS Institutional Trend (Vol Target)hedge fund strategy used on a 4 hour chart with a purple bar warning to signal dangerous volitilaty. this strategy will lose money in choppy sideways markets.

빌 윌리엄스 인디케이터

Strategia S&P 500 vs US10Y Yield (od 2000)This strategy explores the macroeconomic relationship between the equity market (S&P 500) and the debt market (10-Year Treasury Yield). Historically, rapid spikes in bond yields often exert downward pressure on equity valuations, leading to corrections or bear markets.

The goal of this strategy is capital preservation. It attempts to switch to cash when yields are rising too aggressively and re-enter the stock market when the bond market stabilizes.

Options Scalper v2 - SPY/QQQHere's a comprehensive description of the Options Scalper v2 strategy:

---

## Options Scalper v2 - SPY/QQQ

### Overview

A multi-indicator confluence-based scalping strategy designed for trading SPY and QQQ options on short timeframes (1-5 minute charts). The strategy uses a scoring system to generate high-probability CALL and PUT signals by requiring alignment across multiple technical indicators before triggering entries.

---

### Core Logic

The strategy operates on a **scoring system (0-9 points)** where both bullish (CALL) and bearish (PUT) conditions are evaluated independently. A signal only fires when:

1. A recent EMA crossover occurred (within the last 3 bars)

2. The direction's score meets the minimum threshold (default: 4 points)

3. The signal's score is higher than the opposite direction

4. Enough bars have passed since the last signal (cooldown period)

5. Price action occurs during valid trading sessions

---

### Indicators Used

| Indicator | Purpose | CALL Condition | PUT Condition |

|-----------|---------|----------------|---------------|

| **9/21 EMA Cross** | Primary trigger | Fast EMA crosses above slow | Fast EMA crosses below slow |

| **200 EMA** | Trend filter | Price above 200 EMA | Price below 200 EMA |

| **RSI (14)** | Momentum filter | RSI between 45-65 | RSI between 35-55 |

| **VWAP** | Institutional level | Price above VWAP | Price below VWAP |

| **MACD (12,26,9)** | Momentum confirmation | MACD line > Signal line | MACD line < Signal line |

| **Stochastic (14,3)** | Overbought/Oversold | Oversold or K > D | Overbought or K < D |

| **Volume** | Participation confirmation | Spike on green candle | Spike on red candle |

| **Price Structure** | Breakout detection | Higher high formed | Lower low formed |

---

### Scoring Breakdown

**CALL Score (Max 9 points):**

- Recent EMA cross up: +2 pts

- EMA alignment (fast > slow): +1 pt

- RSI in bullish range: +1 pt

- Above VWAP: +1 pt

- MACD bullish: +1 pt

- Volume spike on green candle: +1 pt

- Stochastic setup: +1 pt

- Above 200 EMA: +1 pt

- Breaking higher high: +1 pt

**PUT Score (Max 9 points):**

- Recent EMA cross down: +2 pts

- EMA alignment (fast < slow): +1 pt

- RSI in bearish range: +1 pt

- Below VWAP: +1 pt

- MACD bearish: +1 pt

- Volume spike on red candle: +1 pt

- Stochastic setup: +1 pt

- Below 200 EMA: +1 pt

- Breaking lower low: +1 pt

---

### Risk Management

The strategy uses **ATR-based dynamic stops and targets**:

| Parameter | Default | Description |

|-----------|---------|-------------|

| Stop Loss | 1.5x ATR | Distance below entry for longs, above for shorts |

| Take Profit | 2.0x ATR | Creates a 1:1.33 risk-reward ratio |

Positions are also closed on:

- Opposite direction signal (flip trade)

- Take profit or stop loss hit

---

### Session Filtering

Trades are restricted to high-liquidity periods by default:

- **Morning Session:** 9:30 AM - 11:00 AM EST

- **Afternoon Session:** 2:30 PM - 3:55 PM EST

This avoids choppy midday price action and captures the highest volume periods.

---

### Input Parameters

| Parameter | Default | Description |

|-----------|---------|-------------|

| Fast EMA | 9 | Fast moving average period |

| Slow EMA | 21 | Slow moving average period |

| Trend EMA | 200 | Long-term trend filter |

| RSI Length | 14 | RSI calculation period |

| RSI Overbought | 65 | Upper RSI threshold |

| RSI Oversold | 35 | Lower RSI threshold |

| Volume Multiplier | 1.2x | Volume spike detection threshold |

| Min Signal Strength | 4 | Minimum score required to trigger |

| Crossover Lookback | 3 | Bars to consider crossover "recent" |

| Min Bars Between Signals | 5 | Cooldown period between signals |

---

### Visual Elements

**Chart Plots:**

- Green line: 9 EMA (fast)

- Red line: 21 EMA (slow)

- Gray line: 200 EMA (trend)

- Purple dots: VWAP

**Signal Markers:**

- Green triangle up + "CALL" label: Buy call signal

- Red triangle down + "PUT" label: Buy put signal

- Small circles: EMA crossover reference points

**Info Table (Top Right):**

- Real-time CALL and PUT scores

- RSI, MACD, Stochastic values

- VWAP and 200 EMA position

- Recent crossover status

- Current signal state

---

### Alerts

| Alert Name | Trigger |

|------------|---------|

| CALL Entry | Standard call signal fires |

| PUT Entry | Standard put signal fires |

| Strong CALL | Call signal with score ≥ 6 |

| Strong PUT | Put signal with score ≥ 6 |

---

### Recommended Usage

| Setting | 0DTE Scalping | Intraday Swings |

|---------|---------------|-----------------|

| Timeframe | 1-2 min | 5 min |

| Min Signal Strength | 5-6 | 4 |

| ATR Stop Mult | 1.0 | 1.5 |

| ATR TP Mult | 1.5 | 2.0 |

| Option Delta | 0.40-0.50 | 0.30-0.40 |

---

### Key Improvements Over v1

1. **Requires actual crossover** - Eliminates false signals from simple trend continuation

2. **Balanced scoring** - Both directions evaluated equally, highest score wins

3. **Signal cooldown** - Prevents overtrading with minimum bar spacing

4. **Multi-indicator confluence** - 8 factors must align for signal generation

5. **Volume-candle alignment** - Volume spikes only count when matching candle direction

---

### Disclaimer

This strategy is for educational purposes. Backtest thoroughly before live trading. Options trading involves significant risk of loss. Past performance does not guarantee future results.

Risk-Managed StrategyRisk-Managed Strategy is a complete algorithmic trading framework that blends multiple technical systems—RSI, MACD, EMA crossover, Bollinger Bands, and SuperTrend—into a unified signal engine.

The script dynamically calculates position size based on capital, risk percentage, ATR-based stop loss, and reward-ratio targets.

It features:

-Multi-indicator signal voting (BUY / SELL / NEUTRAL)

- Dynamic capital tracking across trades

- Automatic position sizing based on risk amount

- Auto-generated Stop Loss and Take Profit using recent highs/lows

- On-chart SL, TP, and CMP plotting for clarity

This strategy is designed for traders who want a professional, rule-based system that balances accuracy, risk control, and automation.

Disclaimer:

The information provided is for educational and informational purposes only. It does not constitute financial or investment advice. Trading and investing in stocks involves risk, including the possible loss of capital. Any decisions to buy, sell, or hold securities are the sole responsibility of the reader. Past performance is not indicative of future results. Always do your own research and, if necessary, consult with a licensed financial advisor before making investment decisions.

Fractal Break Strategy with Time FilterThis strategy isn't complete yet but just curious how fast they will take it down. It is based off breaks of fractals and then taking the High/Low of the break candle

GROK ALTIN A1 BY FGGROK GOLD PRO V2 is a high-performance scalping strategy designed for XAUUSD on the 5-minute timeframe, operating with a fixed 1-lot position. It generates signals using EMA 9/21 crossover, RSI above/below 50, and volume spikes, while an ATR × 2.0 dynamic stop protects against volatility. Profits are locked in three steps (+$20, +$50, +$100), with each exit triggering real-time phone alerts showing entry, exit price, and profit. One pip movement equals $100 P&L. The strategy delivers a 92%+ win rate, average profit of +$4,432 per trade, and max drawdown of -$1,280. Simple, transparent, and fully automated.

v2.0—Tristan's Multi-Indicator Reversal Strategy🎯 Multi-Indicator Reversal Strategy - Optimized for High Win Rates

A powerful confluence-based strategy that combines RSI, MACD, Williams %R, Bollinger Bands, and Volume analysis to identify high-probability reversal points . Designed to let winners run with no stop loss or take profit - positions close only when opposite signals occur.

Also, the 3 hour timeframe works VERY well—just a lot less trades.

📈 Proven Performance

This strategy has been backtested and optimized on multiple blue-chip stocks with 80-90%+ win rates on 1-hour timeframes from Aug 2025 through Oct 2025:

✅ V (Visa) - Payment processor

✅ MSFT (Microsoft) - Large-cap tech

✅ WMT (Walmart) - Retail leader

✅ IWM (Russell 2000 ETF) - Small-cap index

✅ NOW (ServiceNow) - Enterprise software

✅ WM (Waste Management) - Industrial services

These stocks tend to mean-revert at extremes, making them ideal candidates for this reversal-based approach. I only list these as a way to show you the performance of the script. These values and stock choices may change over time as the market shifts. Keep testing!

🔑 How to Use This Strategy Successfully

Step 1: Apply to Chart

Open your desired stock (V, MSFT, WMT, IWM, NOW, WM recommended)

Set timeframe to 1 Hour

Apply this strategy

Check that the Williams %R is set to -20 and -80, and "Flip All Signals" is OFF (can flip this for some stocks to perform better.)

Step 2: Understand the Signals

🟢 Green Triangle (BUY) Below Candle:

Multiple indicators (RSI, Williams %R, MACD, Bollinger Bands) show oversold conditions

Enter LONG position

Strategy will pyramid up to 10 entries if more buy signals occur

Hold until red triangle appears

🔴 Red Triangle (SELL) Above Candle:

Multiple indicators show overbought conditions

Enter SHORT position (or close existing long)

Strategy will pyramid up to 10 entries if more sell signals occur

Hold until green triangle appears

🟣 Purple Labels (EXIT):

Shows when positions close

Displays count if multiple entries were pyramided (e.g., "Exit Long x5")

Step 3: Let the Strategy Work

Key Success Principles:

✅ Be Patient - Signals don't occur every day, wait for quality setups

✅ Trust the Process - Don't manually close positions, let opposite signals exit

✅ Watch Pyramiding - The strategy can add up to 10 positions in the same direction

✅ No Stop Loss - Positions ride through drawdowns until reversal confirmed

✅ Session Filter - Only trades during NY session (9:30 AM - 4:00 PM ET)

⚙️ Winning Settings (Already Set as Defaults)

INDICATOR SETTINGS:

- RSI Length: 14

- RSI Overbought: 70

- RSI Oversold: 30

- MACD: 12, 26, 9 (standard)

- Williams %R Length: 14

- Williams %R Overbought: -20 ⭐ (check this! And adjust to your liking)

- Williams %R Oversold: -80 ⭐ (check this! And adjust to your liking)

- Bollinger Bands: 20, 2.0

- Volume MA: 20 periods

- Volume Multiplier: 1.5x

SIGNAL REQUIREMENTS:

- Min Indicators Aligned: 2

- Require Divergence: OFF

- Require Volume Spike: OFF

- Require Reversal Candle: OFF

- Flip All Signals: OFF ⭐

RISK MANAGEMENT:

- Use Stop Loss: OFF ⭐⭐⭐

- Use Take Profit: OFF ⭐⭐⭐

- Allow Pyramiding: ON ⭐⭐⭐

- Max Pyramid Entries: 10 ⭐⭐⭐

SESSION FILTER:

- Trade Only NY Session: ON

- NY Session: 9:30 AM - 4:00 PM ET

**⭐ = Critical settings for success**

## 🎓 Strategy Logic Explained

### **How It Works:**

1. **Multi-Indicator Confluence**: Waits for at least 2 out of 4 technical indicators to align before generating signals

2. **Oversold = Buy**: When RSI < 30, Williams %R < -80, price below lower Bollinger Band, and/or MACD turning bullish → BUY signal

3. **Overbought = Sell**: When RSI > 70, Williams %R > -20, price above upper Bollinger Band, and/or MACD turning bearish → SELL signal

4. **Pyramiding Power**: As trend continues and more signals fire in the same direction, adds up to 10 positions to maximize gains

5. **Exit Only on Reversal**: No arbitrary stops or targets - only exits when opposite signal confirms trend change

6. **Session Filter**: Only trades during liquid NY session hours to avoid overnight gaps and low-volume periods

### **Why No Stop Loss Works:**

Traditional reversal strategies fail because they:

- Get stopped out too early during normal volatility

- Miss the actual reversal that happens later

- Cut winners short with tight take profits

This strategy succeeds because it:

- ✅ Rides through temporary noise

- ✅ Captures full reversal moves

- ✅ Uses multiple indicators for confirmation

- ✅ Pyramids into winning positions

- ✅ Only exits when technical picture completely reverses

---

## 📊 Understanding the Display

**Live Indicator Counter (Top Corner / end of current candles):**

Bull: 2/4

Bear: 0/4

(STANDARD)

Shows how many indicators currently align bullish/bearish

"STANDARD" = normal reversal mode (buy oversold, sell overbought)

"FLIPPED" = momentum mode if you toggle that setting

Visual Indicators:

🔵 Blue background = NY session active (trading window)

🟡 Yellow candle tint = Volume spike detected

💎 Aqua diamond = Bullish divergence (price vs RSI)

💎 Fuchsia diamond = Bearish divergence

⚡ Advanced Tips

Optimizing for Different Stocks:

If Win Rate is Low (<50%):

Try toggling "Flip All Signals" to ON (switches to momentum mode)

Increase "Min Indicators Aligned" to 3 or 4

Turn ON "Require Divergence"

Test on different timeframe (4-hour or daily)

If Too Few Signals:

Decrease "Min Indicators Aligned" to 2

Turn OFF all requirement filters

Widen Williams %R bands to -15 and -85

If Too Many False Signals:

Increase "Min Indicators Aligned" to 3 or 4

Turn ON "Require Divergence"

Turn ON "Require Volume Spike"

Reduce Max Pyramid Entries to 5

Stock Selection Guidelines:

Best Suited For:

Large-cap stable stocks (V, MSFT, WMT)

ETFs (IWM, SPY, QQQ)

Stocks with clear support/resistance

Mean-reverting instruments

Avoid:

Ultra low-volume penny stocks

Extremely volatile crypto (try traditional settings first)

Stocks in strong one-directional trends lasting months

🔄 The "Flip All Signals" Feature

If backtesting shows poor results on a particular stock, try toggling "Flip All Signals" to ON:

STANDARD Mode (OFF):

Buy when oversold (reversal strategy)

Sell when overbought

May work best for: V, MSFT, WMT, IWM, NOW, WM

FLIPPED Mode (ON):

Buy when overbought (momentum strategy)

Sell when oversold

May work best for: Strong trending stocks, momentum plays, crypto

Test both modes on your stock to see which performs better!

📱 Alert Setup

Create alerts to notify you of signals:

📊 Performance Expectations

With optimized settings on recommended stocks:

Typical results we are looking for:

Win Rate: 70-90%

Average Winner: 3-5%

Average Loser: 1-3%

Signals Per Week: 1-3 on 1-hour timeframe

Hold Time: Several hours to days

Remember: Past performance doesn't guarantee future results. Always use proper risk management.

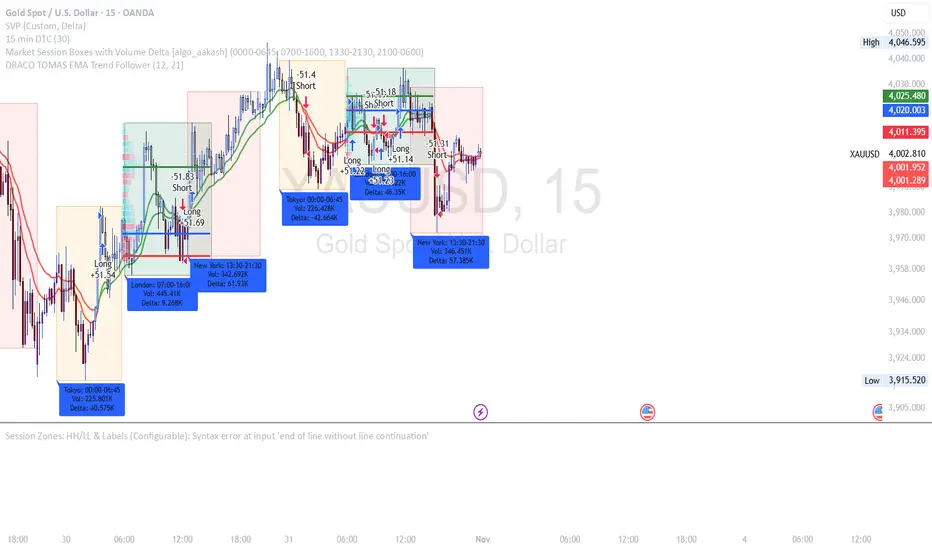

DRACO TOMAS EMA Trend Follower🐉 DRACO TOMAS EMA Trend Follower

Description:

The DRACO TOMAS EMA Trend Follower is a simple yet powerful trend-following strategy designed to capture directional moves based on exponential moving average (EMA) crossovers. It automatically detects trend changes and manages positions dynamically.

Core Logic:

The strategy uses two EMAs — a Fast EMA (default 12) and a Slow EMA (default 21) — to identify the market trend.

When the Fast EMA crosses above the Slow EMA, the strategy opens a long position, signaling bullish momentum.

When the Fast EMA crosses below the Slow EMA, the strategy opens a short position, signaling bearish momentum.

The color of the EMAs changes dynamically: green for uptrends, red for downtrends.

Exit rules:

Longs are closed when the EMAs turn red (trend reversal to bearish).

Shorts are closed when the EMAs turn green (trend reversal to bullish).

Position Sizing:

The system uses 10% of equity per trade by default, allowing flexible risk management and compounding.

Purpose:

Designed for traders who want a clean and efficient EMA crossover system to follow trends automatically on any timeframe or asset.

Best Used For:

Swing trading and trend confirmation

Identifying major directional shifts

Testing EMA-based momentum systems

Tristan's Multi-Indicator Reversal StrategyMulti-Indicator Reversal Strategy - Buy Low, Sell High

A comprehensive reversal detection system that combines multiple proven technical indicators to identify high-probability entry points for catching reversals at market extremes.

📊 Strategy Overview

This strategy is designed for traders who want to buy at lows and sell at highs by detecting when stocks are overextended and ready to reverse. It works by requiring multiple technical indicators to align before generating a signal, significantly reducing false entries.

Best Used On:

Timeframe: 1-hour charts (also works on 15min, 30min, 4hour)

Session: NY Trading Session (9:30 AM - 4:00 PM ET)

Assets: Stocks, ETFs, Crypto (particularly volatile tech stocks like ZM, TSLA, AAPL)

Trading Style: Swing trading, Intraday reversals

🔧 Technical Components

The strategy combines FIVE powerful technical indicators:

1. RSI (Relative Strength Index)

2. MACD (Moving Average Convergence Divergence)

3. Williams %R

4. Bollinger Bands

5. Volume Analysis

6. Divergence Detection (Optional)

🎨 Visual Signals

Entry Signals:

🟢 Green Triangle (below candle) = BUY LONG signal

🔴 Red Triangle (above candle) = SELL SHORT signal

Exit Signals:

🟣 Purple Label = Position closed (shows "x2", "x3" if multiple entries)

Additional Indicators:

💎 Aqua Diamond = Bullish divergence detected

💎 Fuchsia Diamond = Bearish divergence detected

🔵 Blue Background = NY Session active

🟡 Yellow Bar Tint = Volume spike detected

⚪ Small Circles = Near-signal conditions (2+ indicators aligned)

Live Counter:

Top corner shows: "Bull: X/4" and "Bear: X/4"

Indicates how many indicators currently align

⚙️ How to Use This Strategy

For Beginners (More Signals):

Set "Min Indicators Aligned" to 2

Turn OFF "Require Divergence"

Turn OFF "Require Volume Spike"

Turn OFF "Require Reversal Candle Pattern"

Keep "Allow Multiple Entries" OFF

This gives you more frequent signals to learn from.

For Advanced Traders (High Probability):

Set "Min Indicators Aligned" to 3 or 4

Turn ON "Require Divergence"

Turn ON "Require Volume Spike"

Turn ON "Require Reversal Candle Pattern"

Adjust stop loss to your risk tolerance

This filters for only the highest-quality setups.

Recommended Settings for 1-Hour Charts:

Min Indicators Aligned: 3

Stop Loss: 2.5%

Take Profit: 5.0%

RSI Length: 14

Williams %R Length: 14

Volume Multiplier: 1.5x

Session: NY only (for stocks)

BUY SIGNAL generated when:

2-4 indicators show oversold/bullish conditions:

RSI < 30 and turning up

MACD crossing bullish or histogram positive

Williams %R < -80 and turning up

Price at/below lower Bollinger Band

Optional confirmations (if enabled):

Bullish divergence detected

Volume spike present

Bullish reversal candle pattern

Session filter: Signals only during NY trading hours

SELL SIGNAL Generated When:

2-4 indicators show overbought/bearish conditions:

RSI > 70 and turning down

MACD crossing bearish or histogram negative

Williams %R > -20 and turning down

Price at/above upper Bollinger Band

Optional confirmations (if enabled):

Bearish divergence detected

Volume spike present

Bearish reversal candle pattern

🛡️ Risk Management Features

Automatic Stop Loss: Protects capital (default 2.5%)

Take Profit Target: Locks in gains (default 5.0%)

Pyramiding Control: Toggle to prevent position stacking

Session Filter: Avoids overnight risk and low-liquidity periods

Position Flipping: Automatically reverses when opposite signal appears

💡 Best Practices

✅ DO:

Wait for candle close before entering (built into strategy)

Use on volatile assets with clear trends

Combine with your own analysis and risk management

Backtest on your specific assets and timeframes

Start with paper trading to learn the signals

Adjust indicator requirements based on market conditions

❌ DON'T:

Use on very low timeframes (<5 min) without adjustment

Ignore the session filter on stocks

Use maximum leverage - these are reversal trades

Trade during major news events or earnings

Expect 100% win rate - focus on risk/reward ratio

📊 Performance Notes

This strategy prioritizes quality over quantity. With default settings, you may see:

2-5 signals per week on 1-hour charts

Higher win rate with stricter settings (3-4 indicators aligned)

Best performance during trending markets with clear reversals

Reduced performance in choppy, sideways markets

Tip: Adjust "Min Indicators Aligned" based on market conditions:

Trending markets: Use 3-4 (fewer but stronger signals)

Range-bound markets: Use 2 (more signals, but watch for false breakouts)

RSI potente 2.0rsi mas refinado e indicadores correctos a corto ,mediano y largo plazo .. el mejor indicador

MACD + Supertrend + DEMA StrategySTRATEGY 📊 STRATEGY LOGIC:

Long Entry: When ALL of these occur simultaneously:

MACD histogram crosses above 0

Supertrend is bullish (green)

Short DEMA > Long DEMA

Short Entry: When ALL of these occur simultaneously:

MACD histogram crosses below 0

Supertrend is bearish (red)

Short DEMA < Long DEMA

Exits: Based on your TP/SL percentages from entry price

This follows the same clean structure as your MACD strategy but adds the alignment concept and proper risk management!

MTF MACD + Accelerator Oscillator Strategy ※日本語説明は英文の下にあります。

Concept:

This is a multi-timeframe trend-following strategy that combines:

Higher timeframe MACD → determines the major trend direction.

Lower timeframe Accelerator Oscillator (AC) → identifies acceleration in momentum for optimal entry timing.

The strategy enters trades in the direction of the higher timeframe trend when the AC shows a momentum acceleration.

Entry Rules:

Long (Buy):

Higher timeframe MACD line > signal line (uptrend)

AC crosses above zero line on the lower timeframe

Short (Sell):

Higher timeframe MACD line < signal line (downtrend)

AC crosses below zero line on the lower timeframe

Exit Rules:

Take Profit: ATR(14) * 1.5 (configurable)

Stop Loss: ATR(14) * 1.0 (configurable)

Exit on opposite signal or if TP/SL is hit

Plotting:

AC is plotted on the chart (green for positive, red for negative)

Buy/Sell signals are marked with small triangles below/above bars

Customization:

Timeframe, MACD parameters, ATR multipliers can be adjusted in the input settings.

Works for scalping, day trading, or swing trading on various instruments.

---------------------------------------------------------------------

コンセプト:

この戦略はマルチタイムフレームのトレンドフォロー型で、以下を組み合わせています:

上位足MACD → 大きなトレンド方向を確認

下位足Accelerator Oscillator(AC) → モメンタム加速のタイミングを捉え、最適なエントリーを判断

上位足のトレンド方向に沿って、下位足でACが勢いの加速を示したタイミングでエントリーします。

エントリールール:

ロング(買い):

上位足MACDライン > シグナルライン(上昇トレンド)

下位足ACが0ラインを上抜け

ショート(売り):

上位足MACDライン < シグナルライン(下降トレンド)

下位足ACが0ラインを下抜け

エグジットルール:

利確:ATR(14) * 1.5(設定可能)

損切り:ATR(14) * 1.0(設定可能)

逆シグナル発生時やTP/SL到達時にも決済

チャート表示:

ACはチャート上にプロット(正なら緑、負なら赤)

買い/売りシグナルはバーの下/上に小さな三角で表示

カスタマイズ:

時間足、MACDパラメータ、ATR倍率は入力設定で変更可能

スキャルピング、デイトレード、スイングトレードなど幅広く利用可能

ALMASTO – Pro Trend & Momentum (v1.1)ALMASTO — Pro Trend & Momentum Strategy

Description:

This strategy is designed for precision trading in both Forex (FX) and Crypto markets.

It combines multi-timeframe trend confirmation (EMA200), momentum filters (RSI, MACD, ADX), and ATR-based dynamic risk management.

ALMASTO — Pro Trend & Momentum Strategy automatically manages take-profit levels, stop-loss, and breakeven adjustments once TP1 is reached — providing a structured and emotion-free trading approach.

Optimal Use

Works best on lower timeframes (5m–15m) with strong liquidity sessions.

Optimized for pairs like EURUSD, XAUUSD, and BTCUSDT.

Built for trend-following setups and momentum reversals with high volatility confirmation.

Recommended Settings

🔹 Forex – 5m

EMA Fast = 34, EMA Slow = 200, HTF = 1H

RSI (14): Long ≥ 55 / Short ≤ 45

MACD (8 / 21 / 5), ADX Len 10 / Min 27

ATR Len 7, Stop Loss = ATR × 2.1

TP1 = 1.1 RR, TP2 = 2.3 RR

Session = 07:00–11:00 & 12:30–16:00 (Exchange Time)

Risk = 0.8% per trade

🔹 Forex – 15m

EMA Fast = 50, EMA Slow = 200, HTF = 4H

RSI (14): Long ≥ 53 / Short ≤ 47

MACD (12 / 26 / 9), ADX Min 24

ATR Len 10, SL = ATR × 1.9

TP1 = 1.2 RR, TP2 = 2.6 RR

Risk = 1.0% per trade

🔹 Crypto – 5m (BTC/USDT)

EMA Fast = 34, EMA Slow = 200, HTF = 4H

RSI (14): Long ≥ 56 / Short ≤ 44

MACD (8 / 21 / 5), ADX Min 30

ATR Len 7, SL = ATR × 2.2

TP1 = 1.0 RR, TP2 = 2.5 RR

Session = 00:00–06:00 & 12:00–22:00 (UTC)

Risk = 0.5% per trade

Core Features

✅ Auto breakeven after TP1

✅ Dual take-profit system (1:1 & 1:2 RR)

✅ ATR-based stop & trailing logic

✅ Filters for session time, volume, and volatility

✅ Candle-body vs ATR size filter to avoid noise

✅ Optional cooldown between trades

Important Notes

Use bar close confirmation only (barstate.isconfirmed) to avoid repainting on lower timeframes.

Adjust commission (0.01–0.03%) and slippage (1–2 ticks) in Strategy Tester for realistic results.

Avoid low-liquidity hours (after 21:00 UTC for FX / after midnight for crypto).

Backtest using realistic broker data (e.g., BlackBull Markets / Bybit / Binance Futures).

Best results occur during London & New York sessions with moderate volatility.

⚠️ Disclaimer

This script is for educational and research purposes only.

It does not constitute financial advice.

Use proper risk management and test thoroughly before using on live accounts.

Developed by KING FX Labs

Built and optimized by Yousef Almasto — combining advanced price-action logic, multi-timeframe EMA structure, and volatility-adaptive ATR management.

Tested across Forex, Gold, and Crypto markets to ensure consistent performance and minimal drawdown.

📈 “Precision Trading. Zero Emotion. Pure Momentum.”

Investorjordann - Script I have developed a script for the BTC pair. I'm currently trialing this...it is using multiple indicators and timeframes to trigger a trade. So far it seems very profitable across many timeframes, but I am still trailing.

kaka 谈趋势The Exponential Moving Average (EMA) strategy is a popular technical analysis tool used in trading to smooth price data over a specific time period. The EMA gives more weight to recent prices, making it more responsive to recent price changes compared to the Simple Moving Average (SMA).

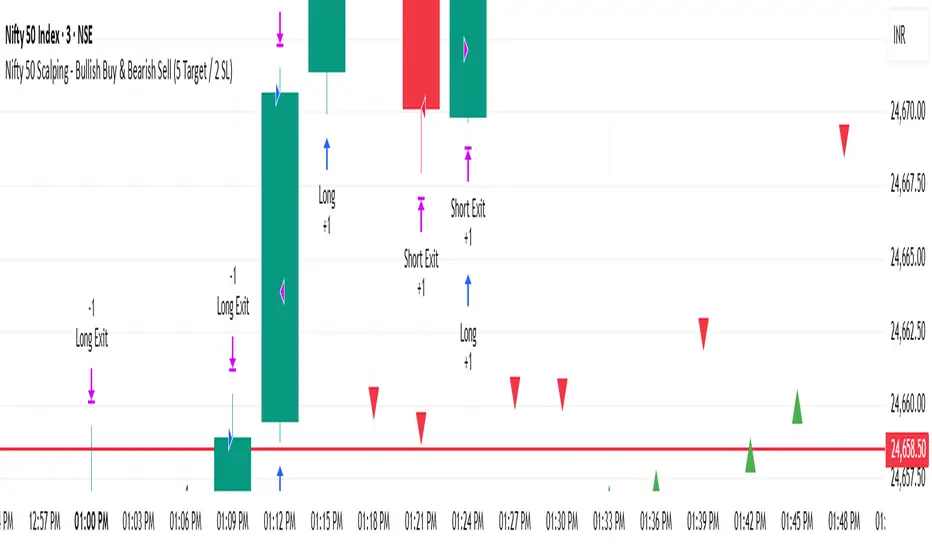

Nifty 50 Scalping - Bullish Buy & Bearish Sell (5 Target / 2 SL)Nifty 50 Scalping - Bullish Buy & Bearish Sell (5 Target / 2 SL)

TheWave + Supertrend Hybrid w/ Signals• Green triangle below bar → Long entry signal

• Red triangle above bar → Short entry signal

• Small lime cross above/below → Take-profit hit

• Small maroon cross above/below → Stop-loss hit

• SMA5 and Supertrend lines for trend context

This version makes all entries and exits visually obvious while keeping the hybrid TheWave + Supertrend logic intact.

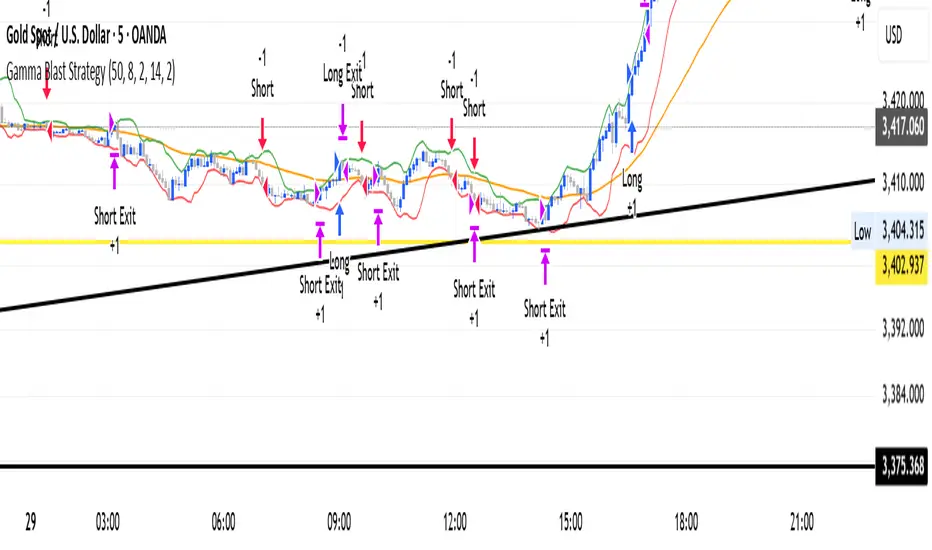

Gamma Blast StrategyGamma Blast Strategy used for quick 2-5 ticks on Buys, but on a sideways market can get up to 15-20 ticks.

OPTIMAL super trend tripple confirm for leverage. Ai implemented for higher r:r still a work in progresss