XBT % ContangoSimilar to my other indicators, but measures XBTUSD Contango in terms of percent.

Also, built it so you could change the values that give the red and green signals. Default values are 0% or less (backwardation) indicates green. However, i found that a 0.5% setting worked will finding local bottoms for current contract of XBTH20 (March 2020). The upper value default is at 5%, and signals red when the next contract reaches over 5%.

My assumption is as BTC increases in value over time, measuring contango in terms of percent will be a better measure of the XBT futures curve.

Backwardation

Deribit Contango Calculator v3Same as XBT Contango Calc V3, however built specifically for Deribit Futures . See link to XBT Contango Calc V3 for full description.

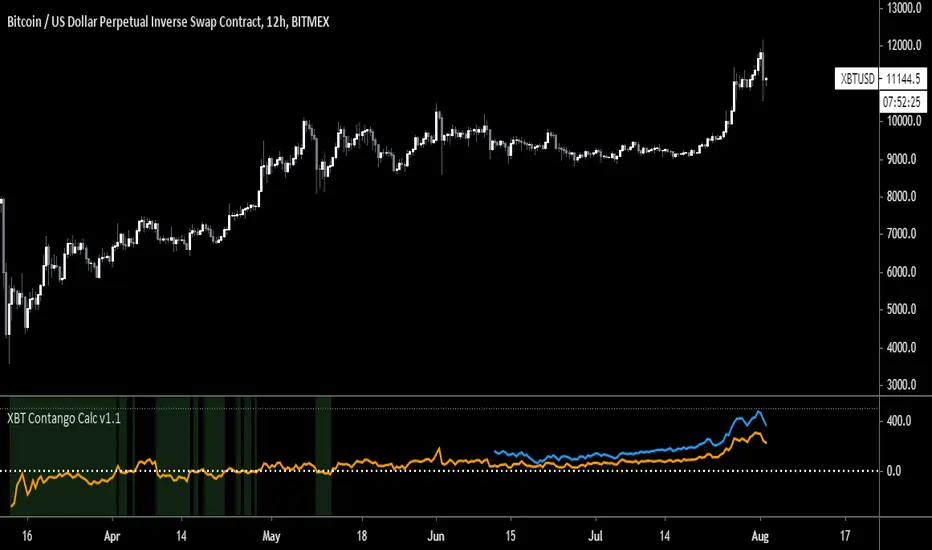

Above is capture of how this indicator performed on December Futures Contract BTC27Z19, since I assume I will loose this as the main chart when I update to June contract

Current (Dec. 2019) futures contracts are as follows:

Blue = BTC26M20

Orange = BTC27H20

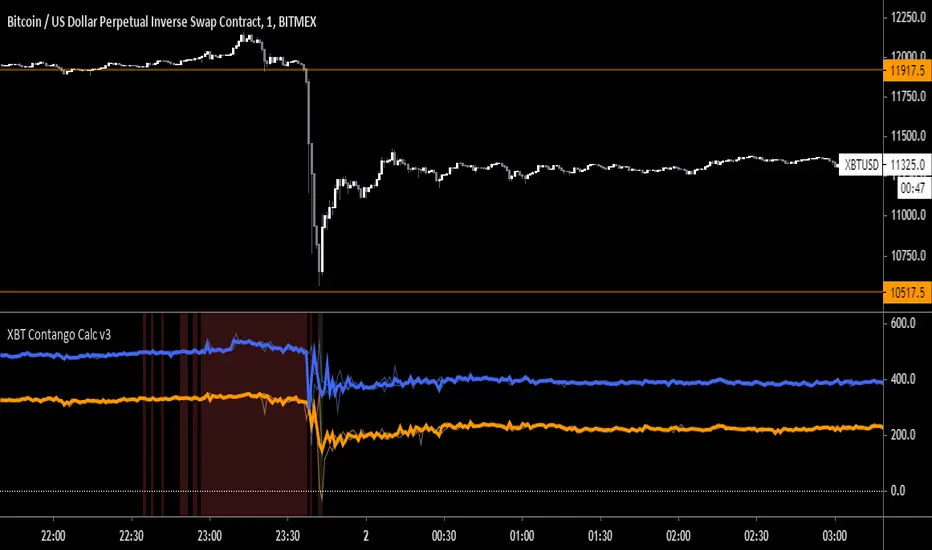

XBT Contango Calculator v3Since creating the first version of the XBT Contango Calculator, I found that the first version is good a calculating contango and backwardation in real time, however does not do a good job of capturing historical data of brief moves. Since backwardation moves are often brief, and since the first version Contango Calc was based on candlestick closes, it did not do a good job of recording the move after it occurred.

It took me a couple versions to try and fix this an eventually settled on version 3 which I have been using on my own for the last few months. You can see in the comparison chart above it does a much better job of capturing backwardation moves and extreme contango. Below is a comparison of how it performed vs. Version 1 during December futures XBTZ19

In addition I have added high/low lines that can be used to understand the amount that futures premium/discount has moved in a specific time frame. For example, the big drop Bitcoin had on September 24th, XBTZ19 went from +$273 contango to -$247 backwardation = $520 move! This move was in addition to the spot price move which was almost -$1,700 from high to low and -$1,100 from open to close. See below:

The high/low lines can also be removed from the chart by unchecking a box in the input tab.

The last update is the ability to lock the spot price to be XBT (index) no matter what chart you pull up. This can be useful if evaluation XBT futures correlation to other bitcoin derivatives such as GBTC or CME futures. You can also disable this feature in the input tab, which will then just calculate based on the current chart you are viewing.

Current Contracts (December 2019)

Blue = XBTM20

Orange = XBTH20

Bitmex BTC Backwardation / ContangoThis indicator calculates difference between price of Bitmex's XBTUSD, and Bitmex's two nearest futures.

If the difference is negative, then it is backwardation.

If the difference is positive, then it is contango.

This script will be updated every about 3 months, when the nearest Bitmex future will be expired.

This is an updated script of , with better description.

XBT Contango Calculator v1.1

This indicator measures value of basis (or spread) of current Futures contracts compared to spot. The default settings are specifically for Bitmex XBTU19 and XBTZ19 futures contracts. These will need to be updated after expiration. Also, it seems that Tradingview does not keep charts of expired contracts. If anyone knows how to import data from previous expired contracts, please let me know. This historical data could be valuable for evaluating previous XBT futures curves.

Also, VERY important to understand is this indicator only works with Spot Bitcoin charts (XBTUSD, BTCUSD, etc). If you add this to any other asset chart, it would not be useful (unless you changed settings to evaluate a different Futures product).

Contango and Backwardation are important fundamental indicators to keep track of while trading Futures markets. For a better explanation, Ugly Old Goat had done several medium articles on this. Please check out link below for his latest article on the subject...

uglyoldgoat.com

Notes on chart above should explain most of what you need to know on to use this indicator. The zero line is the spot price on the chart, so a positive value means Futures are trading at a premium (or in Contango). You can set a value of extreme Contango which will give an alert as red background (default setting is +$500). Green background will appear when Futures are trading at a discount to spot (Backwardation).

Hope some people get some use out of this. This is my first attempt at coding anything, so any feedback would be greatly appreciated!

BTC Donations: 3CypEdvBcvVHbqzHUt1FDiUG53U7pYWviV

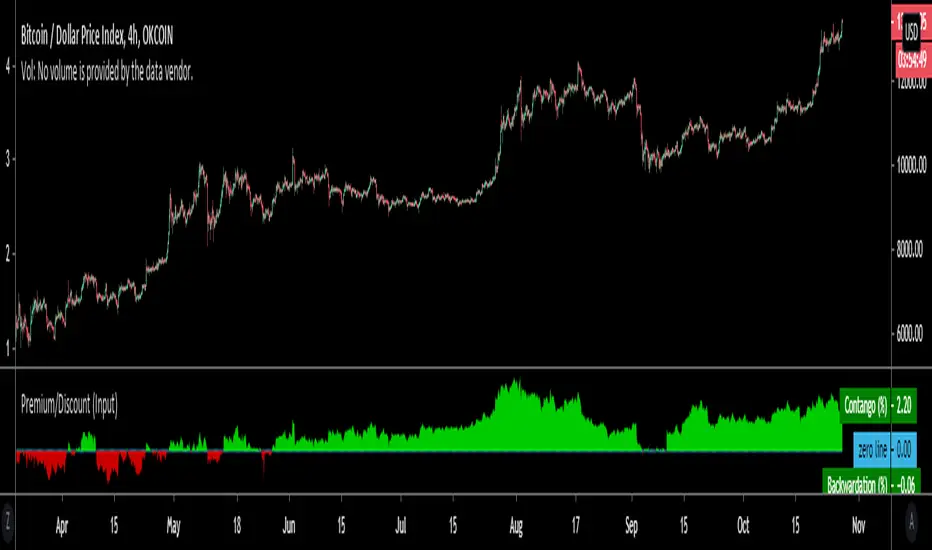

Premium/Discount (Input)Used to show Contango or Backwardation in futures contracts vs spot price. You can input your own tickers so can technically can be used to compare anything.

* In this example I'm showing Okex Quarterly contract vs Okex spot index price because it showcases it better.

* If you are using this after 2019 the default setting will not work because I set it to Bitmex which does not currently have a "current contract in front" ticker available.

It should be fairly self explanatory, but just ask below if you have any questions.

TEDong XBT Sep/Dec19 Futures Premium/Deficit:Hi Folg,

BITMEX Contango/Backwardation is fundamental analysis, act as confirmation for BUY and SELL. A change between Contango and Backwardation often highly correlated with stronger price changes.

Contango : SELL!!! (Background olor: RED)

Backwardation : BUY!!! (Background olor: GREEN)

Backwardation occurs when spot is more expensive that the futures and this confirms a buy and vise versa for Contango.

Happy Trading!

DONATE/TIP

BTC: 13nhMN2H4LoRi4VMcPcyR96jitxrH3uivB

XBT Contango / Backwardation Index [ rumpypumpydumpy ]Experimental idea calculating the momentum of contango/backwardation of spot/perp vs futures as an index. Basically the "RSI" of C/B. Histogram displays the ratio of C/B vs chart close. Multiplier is arbitrary and just to be able to "magnify" the histogram to a visible level.

Has some interesting divergences and as well as ratio trends, zero line cross overs as well as upper and lower CBI/bollinger interactions.

I haven't looked at it properly, but I suspect due to the generally low fluctuations relative to price, intraday will probably be less and less useful as you go to shorter time frames. Most likely useful for higher TFs and could possibly even indicate tops/bottoms on higher TFs, eg significantly high and highest recent ratio + CBI divergence + CBI/BB upper/lower band touch/breach.

In general it seems to be that the higher the ratio the more likely the divs are to be valid.

By default it has the bitmex index as the future's tickerid (which doesn't produce anything useful). You WILL need to add the rest of the tickerid for the futures contract you wish to use - ie BITMEX:XBTM19

Note that due to nonexistent data on the contracts' open, the first x candles (default length is 14) will be inaccurate and you should use the previous contract's data for at least that period.

---------------------------------------

If you find it useful please consider a tip/donation :

BTC - 3BMEXEDyWJ58eXUEALYPadbn1wwWKmf6sA

Contango-Backwardation-Buschi

English:

This script shows the difference between a future's continuous current contract (e. g. CL1!) and the continuous next contract (e. g. CL2!). Normally, the next contract is more expensive ("Contango" - shown in green). If the next contract is cheaper, the difference is negative ("Backwardation" - shown in red).

A change between Contango and Backwardation often corresponds with stronger price changes.

Deutsch:

Dieses Skript zeigt den Unterschied zwischen dem kontinuierlichen aktuellem Kontrakt eines Futures (z. B. CL1!) und dem kontinuierlichen Folgekontrakt (z. B. CL2!). Im Normalfall ist der Folgekontrakt teurer ("Contango" - angezeigt in grün). Wenn der Folgekontrakt billiger ist, ist die Differenz negativ ("Backwardation" - angezeigt in rot).

Ein Wechsel zwischen Contango und Backwardation korrespondiert häufig mit größeren Preisänderungen.