OPEN-SOURCE SCRIPT

업데이트됨 Pocket Pivot with extrapolated Volume and Moving Averages

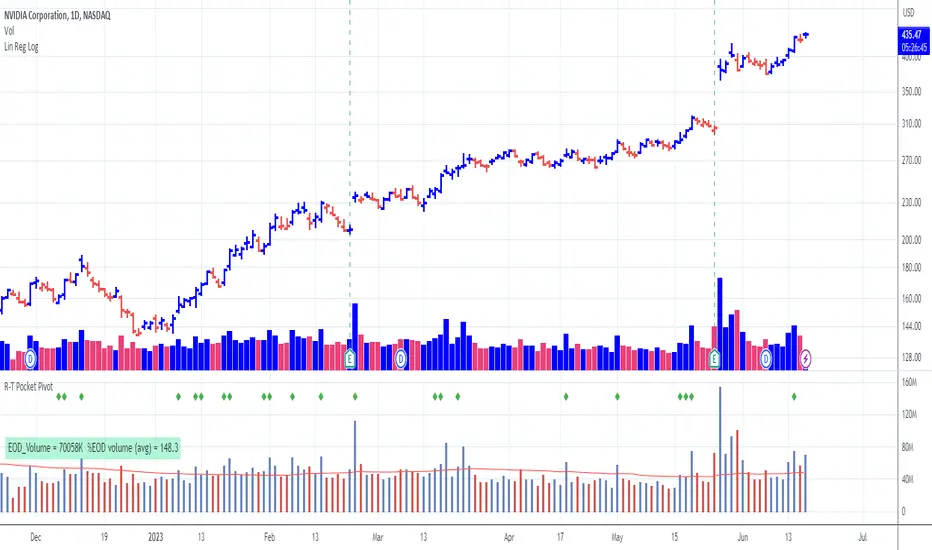

The script shows historical pocket pivots, much as other scripts with a green diamond shape on the volume pane.

When the market is open, the current bar, however, is extrapolated to the end of the day using a sixth-order polynomial.

Thus real-time pocket pivots are shown. To work properly, the user must input a time-zone offset parameter; the default is west coast USA.

Time-zone offset is -12 hours to +12 hours compared to the NYSE exchange time zone (USA west coast: -3.)

The volume extrapolation polynomial is based on a historical NASDAQ intraday volume model developed locally by a team.

Only ten-day lookback pocket pivots are computed as defined initially by Dr. Chris Kacher. (The default lookback can be changed by the user.)

Only pocket pivots are shown where the low of the daily bar is within user-defined proximity to the 50-day moving average or 10-day moving average (for continuation pocket pivots.)

When the market is open, the current bar, however, is extrapolated to the end of the day using a sixth-order polynomial.

Thus real-time pocket pivots are shown. To work properly, the user must input a time-zone offset parameter; the default is west coast USA.

Time-zone offset is -12 hours to +12 hours compared to the NYSE exchange time zone (USA west coast: -3.)

The volume extrapolation polynomial is based on a historical NASDAQ intraday volume model developed locally by a team.

Only ten-day lookback pocket pivots are computed as defined initially by Dr. Chris Kacher. (The default lookback can be changed by the user.)

Only pocket pivots are shown where the low of the daily bar is within user-defined proximity to the 50-day moving average or 10-day moving average (for continuation pocket pivots.)

릴리즈 노트

Original script incorrectly computed end of trading day and beginning of trading day by subtracting the timezone offset from the NYSE market time.The corrected script adds the timezone offset to correctly use that term.

릴리즈 노트

The prior indicator applied extrapolation to volume on weekends: this is not proper. Added line to test if the market is closed (session.ismarket ==false).Also tweaked the lineWidth default value to equal 4.

릴리즈 노트

Modified method to turn off extrapolation on weekends by testing if dayofweek(time) == dayofweek.saturday or dayofweek.sunday.Erroneously extrapolating volume on weekends has been a bug since the beginning and it has taken me time to learn of the above test. The remaining hole in the strategy are market holidays and short trading sessions. I do not have a method for this.

릴리즈 노트

Removed requirement for setting local time zone offset릴리즈 노트

Yet again getting the extrapolation disabled on weekends. My errors.릴리즈 노트

Yet again trying to disable the extrapolation function on weekends...릴리즈 노트

Minor cleanup. I noticed that the extrapolation wasn't working at a time when the market was open. The volume extrapolation is supposed to work when the market is open.릴리즈 노트

Added test for chart timeframe. Volume extrapolation is only valid on daily charts. Extrapolation is disabled for other timeframes. 2023-06-16오픈 소스 스크립트

트레이딩뷰의 진정한 정신에 따라, 이 스크립트의 작성자는 이를 오픈소스로 공개하여 트레이더들이 기능을 검토하고 검증할 수 있도록 했습니다. 작성자에게 찬사를 보냅니다! 이 코드는 무료로 사용할 수 있지만, 코드를 재게시하는 경우 하우스 룰이 적용된다는 점을 기억하세요.

면책사항

해당 정보와 게시물은 금융, 투자, 트레이딩 또는 기타 유형의 조언이나 권장 사항으로 간주되지 않으며, 트레이딩뷰에서 제공하거나 보증하는 것이 아닙니다. 자세한 내용은 이용 약관을 참조하세요.

오픈 소스 스크립트

트레이딩뷰의 진정한 정신에 따라, 이 스크립트의 작성자는 이를 오픈소스로 공개하여 트레이더들이 기능을 검토하고 검증할 수 있도록 했습니다. 작성자에게 찬사를 보냅니다! 이 코드는 무료로 사용할 수 있지만, 코드를 재게시하는 경우 하우스 룰이 적용된다는 점을 기억하세요.

면책사항

해당 정보와 게시물은 금융, 투자, 트레이딩 또는 기타 유형의 조언이나 권장 사항으로 간주되지 않으며, 트레이딩뷰에서 제공하거나 보증하는 것이 아닙니다. 자세한 내용은 이용 약관을 참조하세요.