Multi‑Day Rolling VWAP with Deviation Bands📄 Description:

This script introduces a multi-day rolling VWAP (Volume-Weighted Average Price) indicator designed for traders who seek deeper structural insights beyond session-based VWAPs. It is particularly effective on intraday charts like 15m, 45m, 1H, and 4H, and is optimized for crypto swing, position, and trend exhaustion strategies.

Unlike traditional VWAPs that reset daily or weekly, this tool computes persistent VWAP levels by aggregating daily price-volume data across rolling windows such as the past 7, 30, or 365 days. These levels act as anchored support/resistance zones derived from real traded volume — helping traders identify where price is fair or stretched over time.

To enhance confluence and precision, each VWAP level optionally includes standard deviation bands, which act as dynamic volatility envelopes. These bands support custom multipliers, including Fibonacci levels like 0.272, 0.618, 1.0, and 1.618, providing flexible tools for identifying potential reversal or mean reversion zones.

✅ Key Features:

📊 Rolling VWAP over user-defined lookback windows (e.g. 7, 30, 365 days)

📐 Optional deviation bands based on volume-weighted standard deviation

🔢 Supports both traditional and Fibonacci multipliers for precise band tuning

⚙️ Independent configuration for up to 3 VWAP profiles (short/mid/long)

🔁 Auto-updates daily and tracks consistent volume-based anchoring

💼 Designed for crypto markets, especially high-volatility altcoins

🧠 How it Works:

At the start of each new day, the script logs cumulative volume and typical price values.

It maintains a rolling window of those daily values over configurable periods.

VWAPs are recalculated from the historical data each bar, ensuring persistence.

Deviation bands use a volume-weighted standard deviation formula, not naive price stddevs.

All inputs are optional — bands can be turned off by setting their multipliers to 0.

💡 Use Cases:

Identify long-term fair value zones in trending or consolidating markets

Spot overextended conditions using deviation confluence

Build trend continuation or exhaustion strategies around VWAP clusters

Anchor intraday decisions to multi-day volume context

🔒 Why Closed Source?

This script applies a proprietary method of rolling VWAP construction and deviation banding that goes beyond typical session or anchored VWAPs. The volume aggregation logic and smoothing techniques used are custom-built for tracking persistent volume-weighted structure — which is especially valuable in fragmented crypto markets. To protect this unique methodology, the code is published as closed-source.

Disclaimer: This indicator is a tool, not a guarantee. Always manage your risk.

For educational purposes only. Past performance does not guarantee future results.

거래량 가중 평균가 (VWAP)

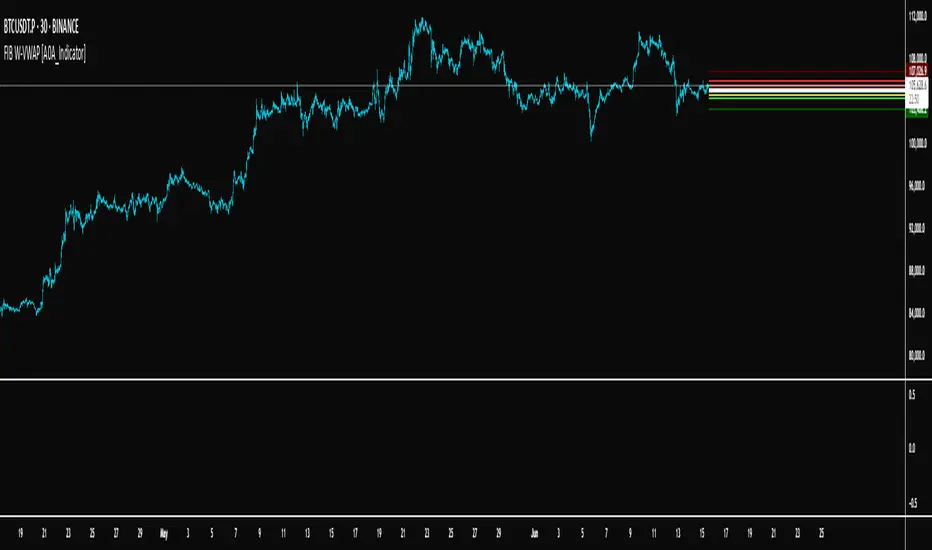

FIB W-VWAP [A0A_Indicator]FIB W-VWAP is an advanced weekly anchored VWAP indicator that leverages Fibonacci-based deviation bands and a custom price source for improved market relevance.

Key Features:

Weekly Anchored VWAP: Resets automatically at the Friday NYSE close, providing a rolling weekly anchor that aligns with professional trading practice.

Fibonacci Deviation Levels: Plots multiple deviation bands around the VWAP, calculated using fixed Fibonacci-inspired multipliers for both positive and negative directions. These serve as key support and resistance zones for mean reversion or trend continuation strategies.

Dynamic Standard Deviation: Each band is based on the live, rolling standard deviation of price within the current weekly session, adapting in real time to changing volatility.

Unique Hybrid Price Source:

VWAP and deviation bands are calculated using a custom price formula:

hidden

This approach gives extra weight to the closing price while still considering intrabar extremes, resulting in a smoother and more robust anchor compared to classic VWAP formulas (such as typical price or close-only).

Visual Enhancements:

Distinct color fills and lines for each band

Configurable transparency and labels

Clearly marked VWAP and all deviation levels, labeled with their corresponding Fibonacci levels

Adaptable for Discretionary and Systematic Trading:

Useful for identifying mean reversion trades, breakouts, and overextended moves during the trading week.

How it works:

At each new weekly session (NY close on Friday), the VWAP and its standard deviation reset.

The script continuously updates cumulative price × volume, cumulative volume, and cumulative price² × volume to maintain accurate VWAP and standard deviation calculations.

Each deviation band is plotted as a multiple of the weekly standard deviation above and below the VWAP, using fixed Fibonacci coefficients.

Labels and horizontal lines extend into the future for clear, actionable visual reference.

Why use this version?

This indicator offers greater precision in turbulent markets, robust support/resistance mapping, and is especially effective for traders seeking a more nuanced, statistically informed view of weekly price structure. The hybrid source makes it more reliable during volatility spikes than classic VWAP methods.

Ready for all timeframes and asset classes—especially powerful for intraday and swing traders working with weekly cycles.

A+ Trade CheckList with Comprehensive Relative StrengthThe indicator designed for traders who need real-time market assessment across multiple timeframes and benchmarks. This comprehensive tool combines traditional technical analysis with sophisticated relative strength measurements to provide a complete market picture in one convenient table display.

The indicator tracks essential trading levels including:

QQQ and SPY trend analysis using exponential moving averages

Previous day and week high/low levels for key support and resistance

Market open levels from the first 5 and 15 minutes of trading (9:30 AM ET)

VWAP positioning for institutional price reference

Short-term EMA positioning for momentum assessment

Advanced Relative Strength Analysis

The standout feature of this indicator is its comprehensive 8-metric relative strength scoring system that compares your current ticker against both QQQ (Nasdaq-100) and SPY (S&P 500) benchmarks.

The 4-Metric Relative Strength System Explained

Metric 1: Relative Strength Ratio (RSR)

Purpose: Measures whether your ticker is outperforming or underperforming relative to its historical relationship with the benchmarks.

How it works:

Calculates the ratio of your ticker's price to QQQ/SPY prices

Compares current ratio to a 20-period moving average of the ratio

Scores +1 if ratio is above average (relative strength), -1 if below (relative weakness)

Trading significance: Identifies when a stock is breaking out of its normal correlation pattern with major indices.

Metric 2: Percentage-Based Relative Performance

Purpose: Compares short-term percentage changes to identify immediate relative momentum.

How it works:

Calculates 5-day percentage change for your ticker and benchmarks

Subtracts benchmark performance from ticker performance

Scores +1 if outperforming by >1%, -1 if underperforming by >1%, 0 for neutral

Trading significance: Captures recent momentum shifts and identifies stocks moving independently of market direction.

Metric 3: Beta-Adjusted Relative Strength (Alpha)

Purpose: Measures risk-adjusted performance by accounting for the ticker's natural volatility relationship with benchmarks.

How it works:

Calculates rolling beta (correlation and variance relationship)

Determines expected returns based on benchmark moves and beta

Measures alpha (excess returns above/below expectations)

Scores based on whether alpha is consistently positive or negative

Trading significance: Identifies stocks generating returns beyond what their risk profile would suggest, indicating fundamental strength or weakness.

Metric 4: Volume-Weighted Relative Strength

Purpose: Incorporates volume analysis to validate price-based relative strength signals.

How it works:

Compares VWAP-based percentage changes between ticker and benchmarks

Applies volume weighting factor based on relative volume strength

Enhances score when high relative volume confirms price movements

Trading significance: Distinguishes between genuine institutional-driven moves and low-volume price action that may not sustain.

Combined Scoring System

The indicator generates 8 individual scores (4 metrics × 2 benchmarks) that combine into a single strength assessment:

Score Interpretation

Strong (4-8 points): Ticker significantly outperforming both benchmarks across multiple methodologies

Moderate Strong (1-3 points): Ticker showing good relative strength with some mixed signals

Neutral (0 points): Balanced performance relative to benchmarks

Moderate Weak (-1 to -3 points): Ticker showing relative weakness with some mixed signals

Weak (-4 to -8 points): Ticker significantly underperforming both benchmarks

Display Format

The indicator shows results as: "Strong (6/8)" indicating the ticker scored 6 out of 8 possible points.

Rolling VWAP Channel [LuxAlgo]The Rolling VWAP Channel indicator creates a channel by analyzing a large number of Volume Weighted Average Prices (VWAPs) and determining a Channel based on percentile linear interpolation throughout the VWAPs.

🔶 USAGE

In this indicator, we have formed a Channel by first calculating multiple VWAPs, each with their respective anchor, then locating prices using "Percentile Linear Interpolation".

Note: Percentile Linear Interpolation locates the price point at which a specified percentage of VWAPs fall below it.

For example, a percentile of 50% would mean that 50% of the VWAP values fall below this price.

This method of analysis is important since the VWAPs are not often evenly distributed; therefore, we are able to draw importance to different levels by analyzing in percentiles.

When visualized, there is typically clustering of the VWAP values, which occurs at any given time, as seen below.

The channel can be tailored to each individual, with full control of each percentile represented in the channel. That being said, a general concept is that these clustered areas are clear results of sideways price action, which would lead us to believe that after interactions at these levels, we should expect to see a directional decision made by the market closely after.

🔶 DETAILS

The Rolling VWAP calculation calculates a user-specified number of VWAPs (up to 500), each anchored to a unique starting point in the chart based on the start of a new timeframe.

Each new timeframe that occurs causes a new VWAP to initialize. When the total number of desired VWAPs is reached, the oldest VWAP is removed and re-initialized, anchored to the current bar. Hence, the name " Rolling " VWAPs

This method allows us to automatically generate and manage large amounts of VWAPs without the need for user interaction.

After we have generated these VWAPs, we are able to run analyses on their returned values, such as the "Percentile Linear Interpolation" mentioned in the section above.

🔶 SETTINGS

Anchor Period: Choose which time period to use as the anchor point to initialize new VWAPs from.

VWAP Source: Choose the source for your VWAPs to calculate.

VWAP Amount: Sets the number of VWAPs to use. After this amount is on the chart, the oldest will be rolled.

🔹 Channel Lines

Toggle: Enable the associated VWAP Channel percentile line.

Percentile: Adjust each line's percentile independently for your needs.

Width: Adjust the width of the associated percentile line.

🔹 Calculation

Calculated Bars: Tells the indicator how many bars to calculate on, for faster calculations with less history, use a lower value. Setting this to 0 will remove the bar constraint.

VWAP %BVWAP %B - Volume Weighted Average Price Percent B

The VWAP %B indicator combines the reliability of VWAP (Volume Weighted Average Price) with the analytical power of %B oscillators, similar to Bollinger Bands %B but using volume-weighted statistics.

## How It Works

This indicator calculates where the current price sits relative to VWAP-based standard deviation bands, expressed as a percentage from 0 to 1:

• **VWAP Calculation**: Uses volume-weighted average price as the center line

• **Standard Deviation Bands**: Creates upper and lower bands using standard deviation around VWAP

• **%B Formula**: %B = (Price - Lower Band) / (Upper Band - Lower Band)

## Key Levels & Interpretation

• **Above 1.0**: Price is trading above the upper VWAP band (strong bullish momentum)

• **0.8 - 1.0**: Overbought territory, potential resistance

• **0.5**: Price exactly at VWAP (equilibrium)

• **0.2 - 0.0**: Oversold territory, potential support

• **Below 0.0**: Price is trading below the lower VWAP band (strong bearish momentum)

## Trading Applications

**Trend Following**: During strong trends, breaks above 1.0 or below 0.0 often signal continuation rather than reversal.

**Mean Reversion**: In ranging markets, extreme readings (>0.8 or <0.2) may indicate potential reversal points.

**Volume Context**: Unlike traditional %B, this incorporates volume weighting, making it more reliable during high-volume periods.

## Parameters

• **Length (20)**: Period for standard deviation calculation

• **Standard Deviation Multiplier (2.0)**: Controls band width

• **Source (close)**: Price input for calculations

## Visual Features

• Reference lines at key levels (0, 0.2, 0.5, 0.8, 1.0)

• Background highlighting for extreme breaks

• Real-time values table

• Clean oscillator format below price chart

Perfect for intraday traders and swing traders who want to combine volume analysis with momentum oscillators.

8EMA/VWAP14 Oscillator w/ Trend Exhaustion Bands8EMA/VWAP14 Oscillator w/ Trend Exhaustion Bands + Performance Screener

Introducing the 8EMA/VWAP14 Oscillator with Trend Exhaustion Bands + Screener Suite - a comprehensive trading system that combines trend identification, momentum analysis, and real-time performance tracking all in one indicator. This system features a four-tier signal approach: early momentum warning dots before anything happens, confirmed entry/exit triangles when it's time to act, a dynamic trend ribbon on your price chart, and adaptive exhaustion bands that adjust to each asset's unique characteristics. The built-in performance tracker shows exactly how well your signals are working - success rates, average time to hit targets, and more - providing clear insight for confident trading decisions. Optimized for daily and weekly timeframes, this suite is suitable for both manual traders and automated strategies.

Aim of the Indicator

The 8EMA/VWAP14 Oscillator with Trend Exhaustion Bands is an advanced momentum oscillator system that combines trend identification, momentum analysis, and forward-looking performance validation. This comprehensive tool measures the percentage difference between an 8-period Exponential Moving Average and a 14-period Volume Weighted Average Price while providing multiple layers of signal confirmation through visual trend ribbons, momentum shift alerts, and adaptive exhaustion detection.

How to Interpret the Indicator

Visual Trend System: The indicator displays a dynamic ribbon between the 8EMA and 14VWAP lines on the price chart, automatically colored green when EMA8 is above VWAP14 (bullish trend) and red when below (bearish trend), providing instant trend context.

Four-Tier Signal System:

Tiny Green Dots (Below Bars): Early bullish momentum shifts when the oscillator crosses above its adaptive baseline

Green Triangles (Below Bars): Confirmed buy signals when EMA8 crosses above VWAP14

Tiny Red Dots (Above Bars): Early bearish momentum shifts when the oscillator crosses below its adaptive baseline

Red Triangles (Above Bars): Confirmed sell signals when EMA8 crosses below VWAP14

Oscillator Analysis: The separate pane displays the momentum oscillator with a dynamic zero line (thin blue) representing the recent average EMA8/VWAP14 relationship. Trend exhaustion is detected through adaptive bands - orange for potential upside exhaustion and purple for potential downside exhaustion, calculated dynamically based on the oscillator's historical range relative to its adaptive baseline.

Key Settings and Flexibility

Signal Source Customization: Choose from Open, High, Low, Close, OHLC Average, or HL Average to optimize signal sensitivity for different market conditions and trading styles.

Multi-Timeframe Capability: Enable higher timeframe analysis to use signals from longer periods while trading on shorter timeframes, significantly reducing noise and improving signal quality for more reliable entries.

Dynamic Baseline Controls: Adjust the adaptive zero line calculation period (5-100 bars) - shorter periods provide more responsive momentum detection, while longer periods offer smoother trend context and reduced false signals.

Entry Timing Options: "Bar Opening Only" mode ensures signals trigger only at confirmed bar close using realistic entry prices, eliminating mid-bar noise and providing accurate backtesting results for automated trading systems.

Adaptive Exhaustion Detection: Customize lookback periods and threshold multipliers to fine-tune exhaustion sensitivity for different volatility environments and asset classes.

Comprehensive Performance Tracking: Set custom profit targets (1-50%) and maximum holding periods to analyze forward-looking signal effectiveness with real-time success rate monitoring.

Advanced Features and Benefits

Forward-Looking Performance Analytics: Unlike traditional backtesting, this system tracks how often buy signals reach specified profit targets and measures average time to target, providing immediate validation of signal quality across different assets and timeframes.

Adaptive Baseline Technology: The dynamic zero line automatically adjusts to each asset's unique EMA8/VWAP14 relationship patterns, making momentum signals contextually relevant rather than using static thresholds that may not suit all market conditions.

Professional Entry/Exit Tracking: When "Bar Opening Only" is enabled, all performance calculations use actual tradeable prices (next bar's open) rather than theoretical mid-bar prices, ensuring realistic performance expectations.

Visual Performance Dashboard: Real-time table displaying success rate, average bars to target, fastest/slowest target achievement, and active position tracking with complete transparency about timeframe, signal source, and methodology being used.

Integrated Alert System: Comprehensive alerts for both early momentum shifts and confirmed crossover signals, enabling automated trading integration and timely manual intervention.

Best Practices for Timing Entries and Exits

Entry Timing Strategy:

Watch for Early Warning: Monitor tiny green dots as momentum builds - this is your preparation phase

Confirm with Ribbon: Ensure the ribbon color aligns with your intended direction (green for long positions)

Enter on Triangle Signal: Execute entries when confirmed buy triangles appear, using realistic bar opening prices

Avoid Exhaustion Zones: Be cautious entering when the oscillator is near orange (upper) exhaustion bands

Exit Timing Strategy:

Monitor Momentum Shifts: Red dots above bars provide early warning of potential reversals before actual sell signals

Use Exhaustion Bands: Consider partial profit-taking when oscillator reaches exhaustion zones (orange/purple bands)

Confirm with Sell Signals: Exit positions when red triangles appear, especially if preceded by bearish momentum dots

Time-Based Exits: Utilize the "Max Bars to Target" setting to avoid holding losing positions indefinitely

Risk Management Integration:

Position Sizing: Use success rate metrics to adjust position sizes - higher success rates may warrant larger positions

Multi-Timeframe Confluence: Combine daily signals with weekly context for highest probability setups

Avoid False Signals: Wait for momentum dots before triangles for stronger signal confirmation, reducing whipsaw trades

Optimal Market Conditions:

Trending Markets: Ribbon provides clear directional bias - trade in direction of ribbon color

Range-Bound Markets: Focus on exhaustion bands for reversal opportunities near dynamic support/resistance levels

Volatile Conditions: Use higher timeframe settings to filter noise and focus on more significant moves

Optimal Timeframe Usage

This indicator achieves exceptional performance on Daily timeframes and delivers superior results on Weekly timeframes. Weekly analysis is particularly powerful for position trading and swing strategies, as the adaptive exhaustion bands and momentum shifts have greater statistical significance over extended periods. The ribbon visualization becomes especially valuable on longer timeframes, clearly delineating major trend phases while filtering out intraday noise that can plague shorter-term analysis.

Alternative Applications

Multi-Timeframe Confluence System: Use weekly signals for trend direction while executing entries on daily timeframes, combining the indicator's momentum dots and triangles across different time horizons for high-probability setups.

Automated Trading Integration: The indicator's comprehensive alert system and realistic entry tracking make it ideal for automated trading platforms, with clear signal hierarchy and performance validation built into the system.

Risk-Adjusted Position Sizing: Utilize real-time success rate data and average holding period metrics to dynamically adjust position sizes based on current market effectiveness of the strategy.

Market Regime Detection: The ribbon color changes and exhaustion band interactions help identify when markets transition between trending and ranging conditions, allowing strategy adaptation accordingly.

Performance Validation Tool: Test signal effectiveness across different assets, timeframes, and market conditions before committing capital, using the forward-looking analytics to validate strategy assumptions.

Conclusion

The 8EMA/VWAP14 Oscillator with Trend Exhaustion Bands represents a comprehensive trading system that bridges the gap between manual analysis and automated execution. Its multi-layered approach provides both leading momentum indicators and lagging confirmation signals, while the adaptive baseline technology ensures relevance across different market conditions and asset classes. The integration of visual trend ribbons, performance analytics, and flexible timing controls makes it suitable for both discretionary traders seeking enhanced market insight and systematic traders requiring robust signal validation for automated strategies.

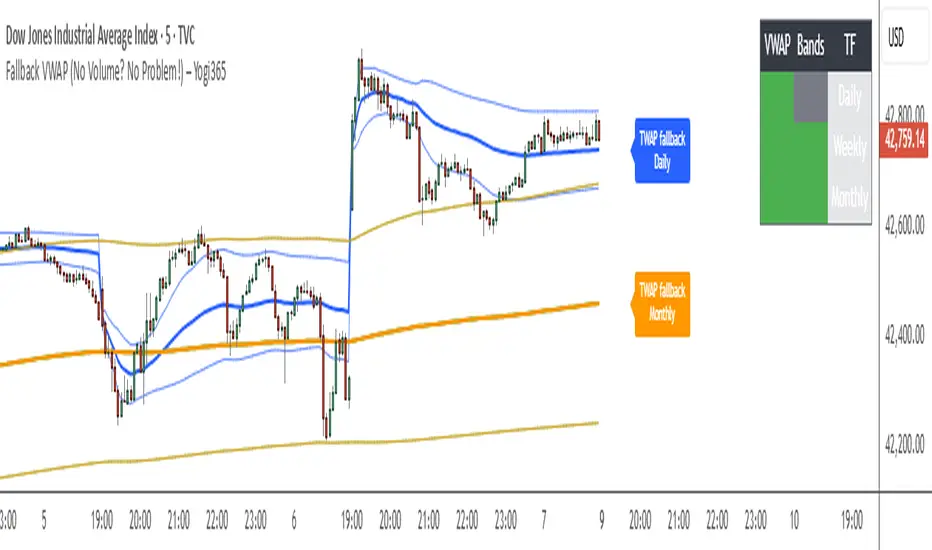

Fallback VWAP (No Volume? No Problem!) – Yogi365Fallback VWAP (No Volume? No Problem!) – Yogi365

This script plots Daily, Weekly, and Monthly VWAPs with ±1 Standard Deviation bands. When volume data is missing or zero (common in indices or illiquid assets), it automatically falls back to a TWAP-style calculation, ensuring that your VWAP levels always remain visible and accurate.

Features:

Daily, Weekly, and Monthly VWAPs with ±1 Std Dev bands.

Auto-detection of missing volume and seamless fallback.

Clean, color-coded trend table showing price vs VWAP/bands.

Uses hlc3 for VWAP source.

Labels indicate when fallback is used.

Best Used On:

Any asset or index where volume is unavailable.

Intraday and swing trading.

Works on all timeframes but optimized for overlay use.

How it Works:

If volume == 0, the script uses a constant fallback volume (1), turning the VWAP into a TWAP (Time-Weighted Average Price) — still useful for intraday or index-based analysis.

This ensures consistent plotting on instruments like indices (e.g., NIFTY, SENSEX,DJI etc.) which might not provide volume on TradingView.

David_FairPriceCandlestick_calculatedDescription:

This indicator displays the "Typical Price" for each candle as a visual marker (cross) directly on the chart. The Typical Price is calculated as the average of the High, Low, and Close values of each bar:

(High + Low + Close) / 3

The marker provides a quick visual reference to the fair or average price level within every single candle.

Unlike a Point of Control (POC) or volume-based indicators, this script works purely with price data and is independent of volume or order flow.

Use cases:

Identify where most trading activity may have been concentrated within the candle (for price-based strategies)

Support as a reference line for mean-reversion or fair value concepts

Works on all timeframes and instruments

Customization:

You can easily change the marker style (cross, dot, triangle, etc.) and color within the script.

Enhanced Zones with Volume StrengthEnhanced Zones with Volume Strength

Your reliable visual guide to market zones — now with Multi-Timeframe (MTF) power!

What you get:

Clear visual zones on your chart — color-coded boxes that highlight important price areas.

Blue Boxes for neutral zones — easy to spot areas of indecision or balance.

Gray Boxes to show normal volume conditions, giving you context without clutter.

Green Boxes highlighting bullish zones where strength is showing.

Red Boxes marking bearish zones where weakness might be in play.

Multi-Timeframe Support:

Seamlessly visualize these zones from higher timeframes directly on your current chart for a bigger-picture view, helping you make smarter trading decisions.

How to use it:

Adjust the box width (in bars) to fit your trading style and timeframe.

Customize colors and opacity to suit your chart theme.

Toggle neutral blue and gray volume boxes on/off to focus on what matters most to you.

Set the maximum number of boxes to keep your chart clean and performant.

Why you’ll love it:

This indicator cuts through the noise by visually marking zones where volume and price action matter the most — without overwhelming your chart. The MTF feature means you’re always aligned with higher timeframe trends without switching views.

Pro tip:

Use these boxes as dynamic support/resistance areas or to confirm trade setups alongside your favorite indicators.

No complicated formulas here, just crisp, actionable visuals designed for clarity and confidence.

Neural Adaptive VWAPNeural Adaptive VWAP with ML Features is an advanced trading indicator that enhances traditional Volume Weighted Average Price (VWAP) calculations through machine learning-inspired adaptive algorithms and predictive volume modeling.

🌟 Key Features:

🧠 Machine Learning-Inspired Adaptation

Dynamic weight adjustment system that learns from prediction errors

Multi-feature volume prediction using time-of-day patterns, price momentum, and volatility

Adaptive learning mechanism that improves accuracy over time

📊 Enhanced VWAP Calculation

Combines actual and predicted volume for forward-looking VWAP computation

Session-based reset with proper daily anchoring

Confidence bands based on rolling standard deviation for dynamic support/resistance

🎯 Advanced Signal Generation

Volume-confirmed crossover signals to reduce false entries

Color-coded candle visualization based on VWAP position

Multi-level strength indicators (strong/weak bullish/bearish zones)

⚙️ Intelligent Feature Engineering

Normalized volume analysis with statistical z-score

Time-series pattern recognition for intraday volume cycles

Price momentum and volatility integration

Sigmoid activation functions for realistic predictions

📈 How It Works:

The indicator employs a sophisticated feature engineering approach that extracts meaningful patterns from:

Volume Patterns: Normalized volume analysis and historical comparisons

Temporal Features: Time-of-day and minute-based cyclical patterns

Market Dynamics: Price momentum, volatility, and rate of change

Adaptive Learning: Error-based weight adjustment similar to neural network training

Unlike static VWAP indicators, this system continuously adapts its calculation methodology based on real-time market feedback, making it more responsive to changing market conditions while maintaining the reliability of traditional VWAP analysis.

🔧 Customizable Parameters:

VWAP Length (1-200 bars)

Volume Pattern Lookback (5-50 periods)

Learning Rate (0.001-0.1) for adaptation speed

Prediction Horizon (1-10 bars ahead)

Adaptation Period for weight updates

📊 Visual Elements:

Blue Line: Adaptive VWAP with predictive elements

Red/Green Bands: Dynamic confidence zones

Colored Candles: Position-based strength visualization

Signal Arrows: Volume-confirmed entry points

Info Table: Real-time performance metrics and weight distribution

🎯 Best Use Cases:

Intraday Trading: Enhanced execution timing with volume prediction

Institutional-Style Execution: Improved VWAP-based order placement

Trend Following: Adaptive trend identification with confidence zones

Support/Resistance Trading: Dynamic levels that adjust to market conditions

2-Day Volume Weighted Average Price (VWAP)This indicator extends TradingView’s built-in VWAP by calculating a volume-weighted average price over a continuous two-day window (yesterday + today), anchoring VWAP at the start of yesterday’s session and carrying it through to today’s close, but only plotting the segment that falls within the current trading session—yesterday’s data feeds into the calculation to ensure today’s VWAP reflects the prior session’s volume and price action, while the line drawn on your chart always begins at today’s session open.

Standard Deviation Bands: Optional ±1σ, ±2σ, and ±3σ envelopes, exactly as in the default VWAP, but based on the rolling two-day data.

Leslie's EMA Ribbon: 5/9/21 + VWAPEMA + VWAP Crossover Indicator with Alerts

This script blends three Exponential Moving Averages (5, 9, 21) with VWAP to identify momentum shifts and volume-confirmed trend signals. It’s optimized for the Daily timeframe, but also adaptable to shorter-term trading.

🔍 Why this combination?

EMAs provide fast and reliable trend signals:

- 5/9 EMA crossover → short-term shifts (more frequent)

- 9/21 EMA crossover → swing confirmation (less noise)

- VWAP adds volume context used by institutions for fair value tracking.

- 9EMA crossing VWAP confirms price action supported by volume.

Together, these tools offer a multi-layered view of market momentum — combining speed, confirmation, and conviction.

⚙️ Features:

Clean plots with dynamic labels on latest bar

Adjustable line weights for clarity

Alerts included for all crossovers:

- 5EMA / 9EMA

- 9EMA / 21EMA

- 9EMA / VWAP

✅ How to Use:

- Best on the Daily timeframe

- Use 5/9 as early signals, 9/21 for trend filtering, and 9/VWAP for volume-backed setups

- Turn on alerts to stay informed of key shifts without staring at charts

Adjustable Quad VWAPOverview

A powerful multi-timeframe VWAP indicator that displays four customizable rolling VWAPs with advanced features for comprehensive trend analysis and signal generation.

Key Features

🔧 Four Adjustable VWAPs

Fast VWAP: Default 7 days (1-365 adjustable)

Slow VWAP: Default 30 days (1-365 adjustable)

Medium VWAP: Default 90 days (1-365 adjustable)

Long VWAP: Default 365 days (1-365 adjustable)

VWAP Adaptive (RelVol-Adjusted)This indicator provides an Adaptive VWAP that adjusts volume weighting using RelVol (Relative Volume at Time), offering a more accurate and context-aware price reference during sessions with irregular volume behavior.

Classic VWAP calculates the average price weighted by raw volume, without considering the time of day. This becomes a serious limitation during major market events such as CPI releases, FOMC announcements, NFP, or large-cap earnings. These events often trigger massive volume spikes within one or two candles. As a result, the classic VWAP gets pulled toward those extreme prices and becomes permanently skewed for the rest of the session.

In such conditions, classic VWAP becomes unreliable. It no longer reflects fair value and often misleads traders relying on it for dynamic support, resistance, or reversion signals.

This Adaptive VWAP improves on that by using RelVol, which compares the current volume to the average volume seen at the same time over previous sessions. It gives more weight to price when volume is typical for that moment, and adjusts the influence when volume is statistically abnormal. This reduces the impact of isolated volume spikes and stabilizes the VWAP path, even in high-volatility environments.

For example, on SPY 1-minute or 5-minute charts during a CPI release, a massive spike in volume and price can occur within a single candle. Classic VWAP will immediately anchor itself to that spike. Adaptive VWAP using RelVol softens that effect and maintains a more realistic trajectory.

Key features:

- Adaptive VWAP weighted by time-adjusted Relative Volume (RelVol)

- Designed to maintain VWAP reliability during macroeconomic events

- Flexible anchoring: Session, Week, Month, Quarter, Earnings, etc.

- Optional display of Classic VWAP for comparison

- Up to 3 customizable deviation bands (standard deviation or percentage)

This tool is ideal for intraday traders who need a VWAP that remains usable and unbiased, even in volatile sessions. It adds robustness to VWAP-based strategies by incorporating time-sensitive volume normalization.

Retail Pain Index (RPIx) (RPIx) Retail Pain Index (DAFE)

See the Market’s Pain. Trade the Edge.

The Retail Pain Index (RPIx) is a next-generation volatility and sentiment tool designed to reveal the hidden moments when retail traders are most likely being squeezed, stopped out, or forced to capitulate. This is not just another oscillator—it’s a behavioral market scanner that quantifies “pain” as price rips away from the average entry zone, often marking the fuel for the next big move.

Why is RPIx so Unique?

Behavioral Volatility Engine:

RPIx doesn’t just track price or volume. It measures how far price is moving away from where the crowd has recently entered (using a rolling VWAP average), then normalizes this “distance” into a Z-score. The result? You see when the market is inflicting maximum pain on the most participants.

Dynamic, Intuitive Coloring:

The main RPIx line is purple in normal conditions, but instantly turns red when pain is extreme to the upside (+2.00 or higher) and green when pain is extreme to the downside (-2.00 or lower). This makes it visually obvious when the market is entering a “max pain” regime.

Threshold Lines for Clarity:

Dashed red and green lines at +2.00 and -2.00 Z-score levels make it easy to spot rare, high-pain events at a glance.

Signature Dashboard & Info Line:

Dashboard: A compact, toggleable panel in the top right of the indicator pane shows the current Z-score, threshold, and status—perfect for desktop users who want a quick read on market stress.

Info Line: For mobile or minimalist traders, a single-line info label gives you the essentials without cluttering your screen.

Inputs & Customization

Entry Cluster Lookback: Adjusts how many bars are used to calculate the “entry zone” (VWAP average). A higher value smooths the signal, a lower value makes it more responsive.

Pain Z-Score Threshold:

Sets the sensitivity for what counts as “extreme pain.” Default is ±2.00, but you can fine-tune this to match your asset’s volatility or your own risk appetite.

Show Dashboard / Show Compact Info Label:

Toggle these features on or off to fit your workflow and screen size.

How to utilize RPIx's awesomeness:

Extreme Readings = Opportunity:

When RPIx spikes above +2.00 (red) or below -2.00 (green), the market is likely running stops, liquidating weak hands, or forcing retail traders to capitulate. These moments often precede sharp reversals, trend accelerations, or volatility expansions.

Combine with Price Action:

Use RPIx as a confirmation tool for your existing strategy, or as a standalone alert for “pain points” where the crowd is most vulnerable.

Visual Edge:

The color-coded line and threshold levels make it easy to spot regime shifts and rare events—no more squinting at numbers or guessing when the market is about to snap.

Why RPIx?

Works on Any Asset, Any Timeframe:

Stocks, futures, crypto, forex—if there’s a crowd, there’s pain, and RPIx will find it.

Behavioral Alpha:

Most indicators lag. RPIx quantifies the psychological stress in the market, giving you a real-time edge over the herd.

Customizable, Clean, and Powerful:

Designed for both power users and mobile traders, with toggles for every workflow.

See the pain. Trade the edge.

Retail Pain Index: Because the market’s next move is written in the crowd’s discomfort.

For educational purposes only. Not financial advice. Always use proper risk management

Use with discipline. Trade your edge.

— Dskyz , for DAFE Trading Systems, for DAFE Trading Systems

Big Money TrackerOI-Anchored VWAP: Big Money Position Tracker

Understanding VWAP in Big Money Trading

Volume Weighted Average Price (VWAP) is the benchmark most widely used by institutions to assess their execution quality and market timing. It represents the average price a security has traded at throughout the day, weighted by volume.

Why Institutions Care About VWAP:

Portfolio managers often mandate trades to be executed at or better than VWAP

Large orders are broken down and executed around VWAP to minimize market impact

Trading desks use VWAP as a neutral price to assess if they're buying too high or selling too low

Algorithmic trading systems use VWAP as a key reference for order execution

The OI-VWAP Edge

This indicator takes Big Money VWAP trading to the next level by anchoring VWAP calculations to significant Open Interest (OI) changes. This helps identify not just where institutions are trading, but where they're establishing significant positions in the crypto markets.

Key Features:

Dynamic OI-based VWAP anchoring that identifies where large positions are established

Previous VWAP level tracking to monitor historical Big Money interest points

Smart sweep detection system for both current and previous VWAP levels

Standard deviation bands for volatility context

What Makes This Indicator Unique:

Uses aggregated Open Interest data from major exchanges (Binance, BitMEX, Bybit, Kraken)

Automatically detects significant OI increases to anchor VWAP levels

Tracks both current and previous Big Money reference prices

Identifies potential stop runs and liquidity sweeps

Trading Applications:

The indicator helps identify where large positions are established and how they might influence price action:

Defense Zones: When price approaches a VWAP level with high OI, institutions often defend their positions

Liquidation Levels: Previous VWAP levels can become liquidation targets for trapped positions

Stop Runs: Sweep detection helps identify when large players might be hunting stops or creating liquidity

Mean Reversion: SD bands help identify potential reversal zones around Big Money average prices

Best Practices:

Look for price reaction at current VWAP when OI is increasing

Monitor sweeps of previous VWAP levels for potential reversals

Use SD bands to gauge volatility expansion/contraction around Big Money positions

Pay attention to failed sweeps as they often indicate strong position defense

Trading Scenarios:

// Bullish Position Defense:

// 1. High OI increase creates new VWAP (Big Money entry)

// 2. Price tests VWAP from above (retest of entry)

// 3. Failed bearish sweeps = shorts trapped

// 4. Strong defense + trapped shorts = potential squeeze

// Bearish Liquidation:

// 1. Previous VWAP level above current price

// 2. High OI trapped at higher prices

// 3. Price sweeps above then fails = more trapped longs

// 4. Break below = potential cascading liquidations

ZenAlgo - MultiverseThe ZenAlgo – Multiverse indicator provides a multi-timeframe view of Volume-Weighted Average Price (VWAP) levels and their dynamic interaction with price across seven defined timeframes: Daily, Weekly, Monthly, Quarterly, Semi-Annual, and Yearly. The indicator is intended to help traders contextualize price within time-based value areas and examine how price interacts with statistically relevant bands derived from those VWAPs.

VWAP Calculation and Period Structure

At the core, this script computes VWAP levels anchored to six distinct timeframes using volume data and a configurable source (default is HLC3). Each VWAP resets at the start of its corresponding period (e.g., Daily VWAP resets at the beginning of a new day) using timeframe.change() as a detection mechanism. This allows each VWAP level to reflect a clean aggregation of price and volume over its specified period.

VWAP levels are only computed if volume data is present and cumulative volume increases, ensuring logical consistency. If volume is missing or inconsistent, the script terminates execution with an error to prevent invalid outputs.

Band Calculation

Each VWAP is accompanied by one or two optional bands on both sides, calculated using percentage-based offset. Daily VWAP is configurable per user preference to use either standard deviation or a percentage-based offset. These bands provide a dynamic value area that expands or contracts with volatility or proportional price distance, respectively.

The bands help classify price as:

Inside the main band (e.g., between ±1 band): near average value

Inside extended band (e.g., ±2 bands): stretched but not extreme

Beyond extended band: potentially overheated or oversold conditions

This layering creates a multi-zoned map of value perception across timeframes.

Labeling and Historical Tracking

As each new VWAP is computed, it is stored in a bounded array alongside metadata such as label position, line objects, test count, and test state (whether price has interacted with it). Each level is drawn as a dotted horizontal line and labeled with its value and corresponding period (e.g., "D", "W", "M").

Price interaction with a VWAP level (i.e., candle high/low crossing the line) changes the styling of the label and line, marking it as "tested." A cap on how many tested levels are retained (default 10) avoids excessive clutter and resource usage.

These persistent horizontal levels give the trader a visual reference of where value was defined in previous periods and how price has respected or ignored those levels over time.

Summary Tables and Grid

Two visual table overlays are provided:

1. VWAP Summary Table , this table shows:

VWAP values per timeframe

Trend interpretation (rising, falling, stable) relative to price

Ranked order of VWAP values (from highest to lowest)

The order is recalculated each bar to reflect the vertical positioning of each VWAP on the price chart.

2. VWAP Relationship Grid

A grid matrix compares each VWAP and current price against all others. Each cell reflects whether a given source is above, below, or within a tolerance threshold relative to another. Colors (green, red, gray) visually encode the result, with the diagonal marked in black and unused cells disabled.

This matrix helps identify alignment or dissonance among timeframes, allowing users to detect whether shorter-term value is leading or lagging longer-term value.

Price Band Classification

For the Daily VWAP specifically, the script includes an extra classification system. It assigns the current price to a zone (e.g., "At VWAP", "Bear Band", "Above Bull Band 2") based on where the price lies in relation to the VWAP bands. This classification is also used for dynamic coloring and added to the daily label.

Display Controls

The script offers fine-grained controls:

Toggle visibility of each VWAP and band group independently

Adjust the offset of labels from the current bar

Customize band multipliers and color transparency

Limit the number of historical VWAP labels plotted

Position both the summary and grid tables flexibly on screen

These options allow traders to declutter their charts and focus on the most relevant context for their strategy.

How to Interpret and Use

This indicator provides a structured view of market value perception across various timeframes. For example:

When price converges with multiple VWAPs, it may suggest consensus on value.

When price moves away from all VWAPs, it may indicate trending or stretched conditions.

Crosses and retests of VWAPs (especially higher-timeframe ones) can act as areas of interest.

The band-based classification helps identify transitional zones and whether price is situated in an area where value is being accepted or rejected.

The summary tables offer a high-level dashboard of price positioning and value structure, which can assist with top-down analysis, filtering setups, or contextual decision-making.

Added Value Compared to Free Alternatives

Most free VWAP scripts:

Cover only a single timeframe (often daily or session-based)

Lack historical level tracking with tested/retested visualization

Do not support grid-level relationships or multi-timeframe band analysis

Offer limited configuration over how bands are calculated or displayed

This script consolidates multiple value areas in one consistent framework and goes further by tracking historical relevance, providing interaction logs, and organizing data into actionable overlays.

For traders seeking comprehensive value context across intraday and swing horizons, this tool offers persistent and structured data views that are otherwise unavailable through individual, isolated VWAP tools.

Limitations and Disclaimers

The indicator depends on volume data. On instruments with unreliable or synthetic volume (e.g., certain spot forex or CFDs), results may not be meaningful.

Band-based interpretation should not be used as a signal mechanism on its own.

On low timeframes, longer-period VWAPs may appear flat or visually compressed.

As with any analytical tool, interpretation requires trader discretion and should be combined with broader context.

Multi VWAPsMulti VWAPs Inspired by Biran Shannon and his book:

"MAXIMUM TRADING GAINS WITH ANCHORED VWAP . The Perfect Combination of Price, Time & Volume."

(ISBN 9798986868004)

A comprehensive VWAP (Volume Weighted Average Price) indicator that combines multiple timeframes and sessions in one view. Perfect for day trading and swing trading across different markets.

Features:

• Multiple VWAP Timeframes:

- Daily VWAP

- Weekly VWAP

- Monthly VWAP

- Quarterly VWAP

- Yearly VWAP

• Session-specific VWAPs:

- London Session (3:00 AM - 11:30 AM NY time)

- New York Session (9:30 AM - 4:00 PM NY time)

• Additional Indicators:

- Midnight Price Line (Previous day's closing price)

- 5-Day Moving Average

- 50-Day Moving Average

• Customization Options:

- Toggle individual VWAPs and indicators

- Customize colors for each component

- Adjustable label positioning

- MA smoothing settings

- Option to show/hide previous day's midnight price

• Smart Features:

- Auto-adjusting calculations based on timeframe

- Clear session boundaries

- Optimized for all chart timeframes

- Clean label system

Perfect for:

• Day traders tracking multiple timeframe momentum

• Swing traders using longer-term VWAPs

• Session traders focusing on London/NY hours

• Multi-timeframe analysis

• Price action trading with VWAP support/resistance

This indicator combines essential trading tools in one clean interface, helping you make informed decisions without cluttering your chart.

Money Flow Index + VWAP Trend FilterThis indicator combines the volume-weighted momentum analysis of the Money Flow Index (MFI) with the trend-filtering capabilities of the Volume Weighted Average Price (VWAP) to generate reliable buy and sell signals. By requiring MFI overbought/oversold conditions to align with the trend direction relative to VWAP, this indicator reduces false signals, making it ideal for trading on timeframes like 5-minute to 4-hour charts.

How It Works

The indicator uses two technical components to produce signals:

Money Flow Index (MFI) for Momentum Extremes:

The MFI, calculated over a default 14-period length, measures buying and selling pressure using price and volume data. A buy signal is triggered when MFI crosses above the oversold level (default: 20), indicating potential buying pressure, while a sell signal occurs when MFI crosses below the overbought level (default: 80), suggesting selling pressure.

Volume Weighted Average Price (VWAP) for Trend Direction:

The VWAP calculates the average price of an asset, weighted by volume, resetting at the start of each trading session (e.g., daily for stocks). It acts as a dynamic support/resistance level. A bullish trend is confirmed when the price is above the VWAP, and a bearish trend when the price is below the VWAP. This ensures MFI signals are filtered to align with the broader trend direction, plotted as a purple line on the chart.

Signal Generation

Signals are generated using the previous bar’s values to prevent repainting:

Buy Signal: The MFI crosses above the oversold level, and the price is above the VWAP (bullish trend). Displayed as a green upward triangle below the bar.

Sell Signal: The MFI crosses below the overbought level, and the price is below the VWAP (bearish trend). Displayed as a red downward triangle above the bar.

TLC sessionA Professional Intraday Session Tracker with VWAP and Economic Event Integration

Description

This indicator provides visual tracking of major trading sessions (Asian, London, New York) combined with VWAP calculations and macroeconomic event zones. It's designed for intraday traders who need to monitor session overlaps, liquidity periods, and high-impact news events.

The basic script of trading sessions was taken as a basis and refined for greater convenience.

Key Features:

Customizable Session Tracking: Visualize up to 3 trading sessions with adjustable time zones (supports IANA & GMT formats)

Dynamic VWAP Integration: Built-in Volume-Weighted Average Price calculation

Macro Event Zones: Highlights key economic announcement windows (adjustable for summer/winter time)

Price Action Visualization: Displays open/close prices, session ranges, and average price levels

Automatic DST Adjustment: Uses IANA timezone database for daylight savings awareness

How It Works

1. Trading Session Detection

Three fully configurable sessions (e.g., Asia, London, New York)

Each session displays:

Colored background zone

Opening price (dashed line)

Closing price (dashed line)

Average price (dotted line)

Optional label with session name

2. VWAP Calculation

Standard Volume-Weighted Average Price plotted as circled line

Helps identify fair value within each session

3. Macro Event Zones

Special highlighted period for economic news releases

Automatically adjusts for summer/winter time

Default set to 1000-1200 (summer) or 0900-1100 (winter) GMT-5 (US session open)

Why This Indicator is Unique

Multi-Session Awareness

Unlike simple session indicators, this tool:

Tracks price development within each session

Shows session overlaps (critical for volatility periods)

Maintains separate VWAP calculations across sessions

Professional-Grade Features

IANA timezone support (automatic DST handling)

Customizable visual elements (toggle labels, ranges, averages)

Object-based architecture (clean, efficient rendering)

News event integration (helps avoid trading during high-impact releases)

Usage Recommendations

Best Timeframes

1-minute to 1-hour charts (intraday focus)

Not recommended for daily+ timeframes

Trading Applications

1. Session Breakout Strategy: Trade breakouts when London/New York sessions open

2. VWAP Reversion: Fade moves that deviate too far from VWAP

3. News Avoidance: Reduce position sizing during macro event windows

Visual Example

Asian session (red)

London session (blue)

New York session (purple)

Macro event zone (white)

VWAP line (gold circles)

The basic script of trading sessions was taken as a basis and refined for greater convenience.

Moving Volume-Weighted Avg Price, % Channel, BBsThis script includes:

- Moving Volume-Weighted Average Price line.

- User-defined % band above and below, very useful for "breakout" signals, and mentally adjusting to the magnitude of price swings when viewing an automatic scale on the price axis.

- Volume-Weighted Bollinger Bands, which are more sensitive to volume.

More detail:

- This is like TV's basic VWAP in concept, except the major flaw in that is that it has reset periods that you can't override, and the volume is cumulative until the next hard reset. The 'reset' is OK for securities trading, that resets every day anyway. But not for crypto - and not if/when securities trading goes 24/7. Also, the denominator accumulating over the entire period is also *not* OK, because then what is shown means something different as the day progresses - which kind of makes it useless. In other words, it starts out very sensitive to volume, and gets progressively more numb to it as they day progresses, and starts flattening out.

- This fixes both problems, by using a user-definable moving window for the average. Essentially combining SMA with volume-weighting.

- You may also find an invaluable trading aid, in the % bands above and below.

- What can optionally be shown is standard deviation bands, aka Bollinger bands. The advantage over regular BB is that it's volume-weighted. Since it is already calculated on a moving average, the period for the standard deviation has been shortened by default, and the magnitude increased, to better approximate regular Bollinger Bands - but it's still more responsive to volume.

Multi-VWAP System🚀 Multi-VWAP System — Anchored VWAP & Deviation Bands

Overview

The Multi-VWAP System provides traders with a professional-grade approach to anchored VWAP analysis. Inspired by Brian Shannon's pioneering work on Anchored VWAP, this indicator automatically calculates and plots:

Current Session VWAP

Previous Session VWAP (also known as "2-Day VWAP")

High-of-Day (HOD) Anchored VWAP

Each VWAP can also display optional Standard Deviation Bands to highlight statistically significant deviations from the volume-weighted average price.

🔍 Why Anchored VWAP Matters

Volume Weighted Average Price (VWAP) is among the most critical institutional indicators, as it represents the average price paid for a stock adjusted by trading volume. This makes VWAP crucial for identifying fair value and significant areas of institutional activity.

Institutions utilize VWAP extensively to guide their execution algorithms. For instance, if price dips below a 2-day anchored VWAP (anchored to the previous session's open), many institutions interpret this as a discounted entry, potentially triggering large-scale buy programs. Conversely, sustained movement above VWAP signals strong buying pressure and bullish sentiment.

📌 Why Multiple Anchors?

Traders commonly anchor VWAPs at critical reference points:

Current Session VWAP:

Essential for day traders as a reference for intraday sentiment. Price action above this line generally indicates bullish sentiment, while price below signals bearish sentiment.

Previous Session (2-Day) VWAP:

Heavily used by institutions and swing traders, it provides insight into multi-session sentiment. Institutions commonly activate buy or sell programs based on whether price is trading at a premium or discount relative to this VWAP.

High-of-Day (HOD) VWAP:

Frequently used by momentum traders, this anchor captures sentiment after the most recent intraday high. Price above the HOD VWAP suggests sustained bullish momentum, while price below might signal weakening momentum.

🌟 Standard Deviation Bands

Each anchored VWAP in this indicator includes optional Standard Deviation Bands, highlighting statistical extremes. Traders use these bands to:

Identify potentially overextended moves (beyond +2σ or +3σ).

Gauge momentum strength (holding above +1σ).

Spot mean-reversion setups when price returns to VWAP after extreme moves.

🎨 Dynamic Background and Momentum Colorization

To visually highlight strength or weakness in price action relative to VWAP:

Dynamic Background Fill between Current and Previous VWAPs:

Green background appears when the Current VWAP is above the Previous VWAP and the linear regression slope (adjustable length) is positive, indicating bullish sentiment.

Red background appears when the Current VWAP is below the Previous VWAP and the slope is negative, indicating bearish sentiment.

No fill when conditions are mixed or momentum is uncertain.

Gold Fill above HOD VWAP:

When price action is above the High-of-Day VWAP and momentum (linear regression slope) is positive, a subtle gold shading appears, quickly highlighting bullish momentum.

⚙ Fully Customizable Settings

Session Times: Adjust session start and end times to match your specific market hours.

Standard Deviation Bands: Enable or disable each VWAP’s deviation bands individually and select how many bands (1σ, 2σ, or 3σ) you'd like to display.

Momentum Slope Length: Adjustable lookback for linear regression slope calculation—giving you full control of trend sensitivity.

🎯 Who Should Use This Indicator?

This indicator is perfect for:

Day Traders who want quick insights into intraday sentiment shifts.

Swing Traders tracking institutional footprints and seeking optimal entry/exit points.

Momentum Traders who rely on clearly visible momentum signals from HOD anchored VWAPs.

Institutional Traders and Professionals seeking sophisticated, institutionally-inspired VWAP analysis without manual anchoring.

📈 Summary of Features

✅ Automatic VWAP Anchors (Current Session, Previous Session, High-of-Day)

✅ Optional Standard Deviation Bands for each VWAP anchor

✅ Dynamic Background Coloring based on price action and momentum conditions

✅ Gold Momentum Highlight for quick bullish momentum identification above HOD VWAP

✅ Fully Customizable Inputs for precise personalization and flexibility

📢 Conclusion

The Multi-VWAP System isn't just another VWAP indicator. It's an institutional-level, dynamic, multi-dimensional analysis tool inspired by the work of Brian Shannon and leading institutional traders. It takes the guesswork out of anchoring and analysis, leaving you free to focus on identifying and executing high-probability trade setups.

Enjoy trading smarter—not harder. Happy Trading! 🚀📊

Volume-Weighted Pivot BandsThe Volume-Weighted Pivot Bands are meant to be a dynamic, rolling pivot system designed to provide traders with responsive support and resistance levels that adapt to both price volatility and volume participation. Unlike traditional daily pivot levels, this tool recalculates levels bar-by-bar using a rolling window of volume-weighted averages, making it highly relevant for intraday traders, scalpers, swing traders, and algorithmic systems alike.

-- What This Indicator Does --

This tool calculates a rolling VWAP-based pivot level, and surrounds that central pivot with up to five upper bands (R1–R5) and five lower bands (S1–S5). These act as dynamic zones of potential resistance (R) and support (S), adapting in real time to price and volume changes.

Rather than relying on static session or daily data, this indicator provides continually evolving levels, offering more relevant levels during sideways action, trending periods, and breakout conditions.

-- How the Bands Are Calculated --

Pivot (VWAP Pivot):

The core of this system is a rolling Volume-Weighted Average Price, calculated over a user-defined window (default 20 bars). This ensures that each bar’s price impact is weighted by its volume, giving a more accurate view of fair value during the selected lookback.

Volume-Weighted Range (VW Range):

The highest high and lowest low over the same window are used to calculate the volatility range — this acts as a spread factor.

Support & Resistance Bands (S1–S5, R1–R5):

The bands are offset above and below the pivot using multiples of the VW Range:

R1 = Pivot + (VW Range × multiplier)

R2 = R1 + (VW Range × multiplier)

R3 = R2 + (VW Range x multiplier)

...

S1 = Pivot − (VW Range × multiplier)

S2 = S1 − (VW Range × multiplier)

S3 = S2 - (VW Range x multiplier)

...

You can control the multiplier manually (default is 0.25), to widen or tighten band spacing.

Smoothing (Optional):

To prevent erratic movements, you can optionally toggle on/off a simple moving average to the pivot line (default length = 20), providing a smoother trend base for the bands.

-- How to Use It --

This indicator can be used for:

Support and resistance identification:

Price often reacts to R1/S1, and the outer bands (R4/R5 or S4/S5) act as overshoot zones or strong reversal areas.

Trend context:

If price is respecting upper bands (R2–R3), the trend is likely bullish. If price is pressing into S3 or lower, it may indicate sustained selling pressure or a breakdown.

Volatility framing:

The distance between bands adjusts based on price range over the rolling window. In tighter markets, the bands compress — in volatile moves, they expand. This makes the indicator self-adaptive.

Mean reversion trades:

A move into R4/R5 or S4/S5 without continuation can be a sign of exhaustion — potential for reversal toward the pivot.

Alerting:

Built-in alerts are available for crosses of all major bands (R1–R5, S1–S5), enabling trade automation or scalp alerts with ease.

-- Visual Features --

Fuchsia Lines: Mark all Resistance (R1–R5) levels.

Lime Lines: Mark all Support (S1–S5) levels.

Gray Circle Line: Marks the rolling pivot (VWAP-based).

-- Customizable Settings --

Rolling Length: Number of bars used to calculate VWAP and VW Range.

Multiplier: Controls how wide the bands are spaced.

Smooth Pivot: Toggle on/off to smooth the central pivot.

Pivot Smoothing Length: Controls how many bars to average when smoothing is enabled.

Offset: Visually shift all bands forward/backward in time.

-- Why Use This Over Standard Pivots? --

Traditional pivots are based on previous session data and remain fixed. That’s useful for static setups, but may become irrelevant as price action evolves. In contrast:

This system updates every bar, adjusting to current price behavior.

It includes volume — a key feature missing from most static pivots.

It shows multiple bands, giving a full view of compression, breakout potential, or trend exhaustion.

-- Who Is This For? --

This tool is ideal for:

Day traders & scalpers who need relevant intraday levels.

Swing traders looking for evolving areas of confluence.

Algorithmic/systematic traders who rely on quantifiable, volume-aware support/resistance.

Traders on all assets: works on crypto, stocks, futures, forex — any chart that has volume.