Tick CVD [Kioseff Trading]Hello!

This script "Tick CVD" employs live tick data to calculate CVD and volume delta! No tick chart required.

Features

Live price ticks are recorded

CVD calculated using live ticks

Delta calculated using live ticks

Tick-based HMA, WMA, EMA, or SMA for CVD and price

Key tick levels (S/R CVD & price) are recorded and displayed

Price/CVD displayable as candles or lines

Polylines are used - data visuals are not limited to 500 points.

Efficiency mode - remove all the bells and whistles to capitalize on efficiently calculated/displayed tick CVD and price

How it works

While historical tick-data isn't available to non-professional subscribers, live tick data is programmatically accessible. Consequently, this indicator records live tick data to calculate CVD, delta, and other metrics for the user!

Generally, Pine Scripts use the following rules to calculate volume/price-related metrics:

Bullish Volume: When the close price is greater than the open price.

Bearish Volume: When the close price is less than the open price.

This script, however, improves on that logic by utilizing live ticks. Instead of relying on time-series charts, it records up ticks as buying volume and down ticks as selling volume. This allows the script to create a more accurate CVD, delta, or price tick chart by tracking real-time buying and selling activity.

Price can tick fast; therefore, tick aggregation can occur. While tick aggregation isn't necessarily "incorrect", if you prefer speed and efficiency it's advised to enable "efficiency mode" in a fast market.

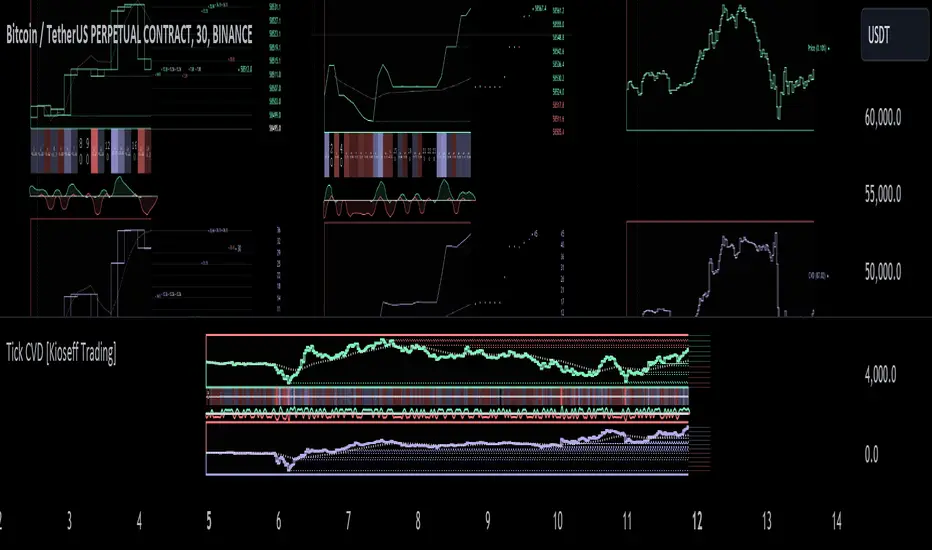

The image above highlights the tick CVD and price tick graph!

Green price tick graph = price is greater than its origin point (first script load)

Red price tick graph = price is less than its origin point

Blue tick CVD graph = CVD, over the calculation period, is greater than 0.

Red tick CVD graph = CVD is less than 0 over the calculation period.

The image above explains the right-oriented scales. The upper scale is for the price graph and the lower scale for the CVD graph.

The image above explains the circles superimposed on the scale lines for the price graph and the CVD graph.

The image above explains the "wavy" lines shown by the indicator. The wavy lines correspond to tick delta - whether the recorded tick was an uptick or down tick and whether buy volume or sell volume transpired.

The image above explains the blue/red boxes displayed by the indicator. The boxes offer an alternative visualization of tick delta, including the magnitude of buying/selling volume for the recorded tick.

Blue boxes = buying volume

Red boxes = selling volume

Bright blue = high buying volume (relative)

Bright red = high selling volume (relative)

Dim blue = low buying volume (relative)

Dim red = low selling volume (relative)

The numbers displayed in the box show the numbered tick and the volume delta recorded for the tick.

The image above further explains visuals for the CVD graph.

Dotted red lines indicate key CVD peaks, while dotted blue lines indicate key CVD bottoms.

The white dotted line reflects the CVD average of your choice: HMA, WMA, EMA, SMA.

The image above offers a similar explanation of visuals for the price graph.

The image above offers an alternative view for the indicator!

The image above shows the indicator when efficiency mode is enabled. When trading a fast market, enabling efficiency mode is advised - the script will perform quicker.

Of course, thank you to @RicardoSantos for his awesome library I use in almost every script :D

Thank you for checking this out!

Tickvolume

Effort & Result (normalized)It is recommended to use a column display. This indicator measures the relationship between the body of the candlestick and the volume. Therefore, it measures the relationship between effort (volume) and result (price). It is still necessary to contextualize the price and not use the indicator without considering structure or relevant zones.

As we can see, this is an oscillator that ranges from 100 to -100 and helps visualize Volume Spread Analysis.

It can indicate three different types of relationships between candlesticks and volume:

1. Absorption : This is a significant discrepancy that shows that despite considerable effort in terms of volume, there has not been an adequate price result. High volume and little price movement. It can be detected when the indicator values are negative, and the closer to -100, the more pronounced the absorption. It indicates strong aggressive participation, but equally strong passive participation. It should be interpreted as an opposite signal; if the candlestick closes long with absorption, then it is likely that the bullish movement will not continue.

2. Absence of Resistance : This is a discrepancy that occurs when, despite low volumetric effort, there is a significant price movement. This is due to the absence of passive orders and is exactly the opposite of absorption. It is measured when the indicator value is positive. It means that a wide buy candlestick with low volume has not encountered resistance from passive sellers during its path, and vice versa for a sell candlestick. It should be interpreted as a "green light"; therefore, a buy candlestick that closes with a positive value in the indicator signals a likely price increase shortly thereafter.

3. Congruence : When the indicator value is close to 0, a situation of congruence occurs, where the result (price) is adequate to the effort (volumes). This indicates an efficient market with balanced participation from sellers and buyers, both passive and aggressive.

The pattern shown in the figure illustrates in the first line a sell candlestick with a very small body but a very high volumetric effort. Indeed, the corresponding column in the indicator shows negative values ("Absorption"). The second line shows how, after a few minutes, an "Absence of Resistance" situation occurs, this time for a buy candlestick that, despite low volumes, closed with a very wide body, in fact the indicator shows positive values. This specific pattern should be read as a long signal since sellers have been absorbed by passive buyers, and buyers have not encountered resistance from passive sellers. This indicates greater coordination and participation from both aggressive and passive buyers.

Interval Volatility Bands [DW]This is an experimental study that utilizes Volume Weighted Average Price or Time Weighted Average Price calculations, Bollinger Bands, and Fibonacci numbers to estimate volatility over a specified interval.

First, the basis is calculated by selecting:

-VWAP, which has the option to be calculated using real volume or tick volume

-TWAP, which has the option to be calculated using the standard method or exponential method

Next, standard deviation from the basis is calculated and multiplied by a specified expansion coefficient. The result is then added to and subtracted from the basis to calculate the high and low bands.

There are three band calculation methods to chosse from in this script:

-Standard, which uses the default calculations

-Average, which takes a cumulative average of standard deviation

-Hybrid, which takes the maximum of the standard and average standard deviation methods

Lastly, the high and low band ranges are multiplied by Fibonacci Percentages 23.6 - 78.6.

A custom color scheme with eight default presets to choose from is included.

DVDIQQE [DW]This is an experimental study inspired by the Quantitative Qualitative Estimation indicator designed to identify trend and wave activity.

In this study, rather than using RSI for the calculation, the Dual Volume Divergence Index oscillator is utilized.

First, the DVDI oscillator is calculated by taking the difference between PVI and its EMA, and NVI and its EMA, then taking the difference between the two results.

Optional parameters for DVDI calculation are included within this script:

- An option to use tick volume rather than real volume for the volume source

- An option to use cumulative data, which sums the movements of the oscillator from the beginning to the end of TradingView's maximum window to give a more broad picture of market sentiment

Next, two trailing levels are calculated using the average true range of the oscillator. The levels are then used to determine wave direction.

Lastly, rather than using 0 as the center line, it is instead calculated by taking a cumulative average of the oscillator.

Custom bar colors are included.

Note: For charts that have no real volume component, use tick volume as the volume source.