Flux Power Dashboard (Updated and Renamed)Flux Power Dashboard is a compact market-state heads-up display for TradingView. It blends trend, momentum, and volume-flow into a single on-chart panel with color-coded cues and minimal lag. You get:

Clean visual trend via fast/slow MA with slope/debounce filters

MACD state and most recent cross (with “freshness” tint)

OBV confirmation and gating to reduce noise

Session awareness (Asia/London/New York + pre-sessions + overlap)

Optional HTF Regime row and regime gate to align signals to higher-timeframe bias

Context from VIX/VXN (volatility regime)

A single Flux Score (0–100) as a top-level read

It is deliberately “dashboard-first”: fast to read, consistent between symbols/timeframes, and designed to limit overtrading in chop.

What it can do (capabilities)

Signal gating: You can require multiple pillars to agree (Trend, MACD, OBV) before a “strong” bias is shown.

Debounced trend: Uses slope + confirmation bars to avoid flip-flopping.

Session presets: Auto-adjust the minimum confirmation bars by session (e.g., NY vs London vs Asia) to better match liquidity/volatility.

MACD presets: Quick switch between Scalp / Classic / Slow or roll your own custom speeds.

OBV confirmation: Volume flow must agree for trend/entries to “count” (optional).

HTF Regime awareness: Shows the higher-timeframe backdrop and (optionally) gates signals so you don’t fight the dominant trend.

Volatility context: VIX/VXN auto-colored cells based on your thresholds.

Top-center Session Title: Broadcasts the active session (or Overlap) with a matched background color.

Customizable UI: Column fonts, params font, transparency, dashboard corner, marker styles, colors, widths—tune it to your chart.

Practical use: Start with Flux Score + Summary for a snapshot, confirm with Trend & MACD, check OBV agreement (implicit in signal strength), glance at Regime to avoid counter-trend trades, and use Session + VIX/VXN for timing and risk context.

How it avoids common pitfalls

Repaint-aware: “Confirm on Close” can be enabled to read prior bar states, reducing intrabar noise.

Auto MA sanity: If fast ≥ slow length, it auto-swaps under the hood to keep calculations valid.

Debounce & confirm: Trend flips only after X bars satisfy conditions, cutting false flips in chop.

Freshness tint: New Cross/Signal rows tint slightly brighter for a few bars, so you can spot recency at a glance.

Every line of the dashboard (what it shows, how it’s colored)

Flux Score

What: Composite 0–100 built from three pillars: Trend (40%), MACD (30%), OBV (30%).

Read: ≥70 Bullish, ≤30 Bearish, else Neutral.

Use: Quick “state of play” gauge—stronger alignment pushes the score toward extremes.

Regime (optional row)

What: Higher-timeframe (your Regime TF) backdrop using the same MA pair with HTF slope/ATR buffer.

Values: Bull / Bear / Range.

Gate (optional): If Regime Gate is ON, Trend/Signals only go directional when HTF agrees.

Summary

What: One-line narrative combining the three pillars: MACD (up/down/flat), OBV (up/down/flat), Trend (up/down/flat).

Use: Human-readable cross-check; should rhyme with Flux Score.

Trend

What: Debounced MA relationship on the current chart.

Strict: needs fast > slow and slow rising (mirror for down) + slope debounce + confirmation bars.

Lenient: allows fast > slow or slow rising (mirror for down) with the same debounce/confirm.

Color: Green = UP, Red = DOWN, Gray = FLAT.

Use: Your structural bias on the trading timeframe.

MACD

What: Current MACD line vs signal, using your selected preset (or custom).

Values: Bull (line above), Bear (below), Flat (equal/indeterminate).

Color: Green/Red/Gray.

Cross

What: Most recent MACD cross and how many bars ago it occurred (e.g., “MACD XUP | 3 bars”).

Freshness: If the cross happened within Fresh Signal Tint bars, the cell brightens slightly.

Use: Timing helper for inflection points.

Signal

What: Latest directional shift (from short-bias to long-bias or vice versa) and age in bars.

Strength:

Strong = Trend + MACD + OBV all align

Weak = partial alignment (e.g., Trend + MACD, or Trend + OBV)

Color: Green for long bias, Red for short bias; fresh signals tint brighter.

Use: Action cue—treat Strong as higher quality; Weak as situational.

MA

What: Your slow MA type and length, plus slope direction (“up”/“down”).

Use: Context even when Trend is FLAT; slope often turns before full trend flips.

Session

What: Current market session by Eastern Time: New York / London / Asia, Pre- windows, Overlap, or Off-hours.

Logic: If ≥2 main sessions are active, shows Overlap (and grays the top title background).

Use: Timing and expectations for liquidity/volatility; also drives session-based confirmation presets if enabled.

VIX

What: Real-time CBOE:VIX on your chosen TF.

Auto-color (if on):

Calm (< Calm) → Green

Watch (< Watch) → Yellow

Elevated (< Elevated) → Orange

Very High (≥ Elevated) → Red

Use: Equity market–wide risk mood; higher = bigger moves, lower = quieter.

VXN

What: CBOE:VXN (Nasdaq volatility index) on your chosen TF.

Auto-color thresholds like VIX.

Use: Tech-heavy risk mood; helpful for growth/QQQ/NDX names.

Footer (params row, bottom-right)

What: Key live settings so you always know the context:

P= Trend Confirmation Bars

O= OBV Confirmation Bars

Strict/Lenient (trend mode)

MACD preset (or “Custom”)

swap if MA lengths were auto-swapped for validity

Regime gate if enabled

Candles for clarity

Use: Quick integrity check when comparing charts/screenshots or changing presets.

Recommended workflow

Start at Flux Score & Summary → snapshot of alignment.

Check Trend (color) and MACD (Bull/Bear).

Look at Signal (Strong vs Weak, and age).

Glance at Regime (and use gate if you’re trend-following).

Use Session + VIX/VXN to adjust expectations (breakout vs mean-revert, risk sizing, patience).

Keep Confirm on Close ON when you want stability; turn it OFF for faster (but noisier) reads.

Notes & limitations

Not advice: This is an informational tool; always combine with your own risk rules.

Repaint vs responsiveness: With “Confirm on Close” OFF you’ll see faster state changes but may get more churn intrabar.

Presets matter: Scalp MACD reacts fastest; Slow reduces whipsaw. Choose for your timeframe.

Session windows depend on the strings you set; adjust if your broker’s feed or DST handling needs tweaks.

스크립트에서 "vix"에 대해 찾기

Index Options Expirations and Calendar EffectsFeatures

- Highlights monthly equity options expiration (opex) dates.

- Marks VIX options expiration dates based on standard 30-day offset.

- Shows configurable vanna/charm pre-expiration window (green shading).

- Shows configurable post-opex weakness window (red shading).

- Adjustable colors, start/end offsets, and on/off toggles for each element.

What this does

This overlay highlights option-driven calendar windows around monthly equity options expiration (opex) and VIX options expiration. It draws:

- Solid blue lines on the third Friday of each month (typical monthly opex).

- Dashed orange lines on the Wednesday ~30 days before next month’s opex (typical VIX expiration schedule).

- Green shading during a pre-expiration window when vanna/charm effects are often strongest.

- Red shading during the post-expiration "window of non-strength" often observed into the Tuesday after opex.

How it works

1. Monthly opex is detected when Friday falls between the 15th–21st of the month.

2. VIX expiration is calculated by finding next month’s opex date, then subtracting 30 calendar days and marking that Wednesday.

3. Vanna/charm window (green) : starts on the Monday of the week before opex and ends on Tuesday of opex week.

4. Post-opex weakness window (red) : starts Wednesday of opex week and ends Tuesday after opex.

How to use

- Add to any chart/timeframe.

- Adjust inputs to toggle VIX/opex lines, choose colors, and fine-tune the start/end offsets for shaded windows.

- This is an educational visualization of typical timing and not a trading signal.

Limitations

- Exchange holidays and contract-specific exceptions can shift expirations; this script uses standard calendar rules.

- No forward-looking data is used; all dates are derived from historical and current bar time.

- Past patterns do not guarantee future behavior.

Originality

Provides a single, adjustable visualization combining opex, VIX expiration, and configurable vanna/charm/weakness windows into one tool. Fully explained so non-coders can use it without reading the source code.

Volatility Arbitrage Spread Oscillator Model (VASOM)The Volatility Arbitrage Spread Oscillator Model (VASOM) is a systematic approach to capitalizing on price inefficiencies in the VIX futures term structure. By analyzing the differential between front-month and second-month VIX futures contracts, we employ a momentum-based oscillator (Relative Strength Index, RSI) to signal potential market reversion opportunities. Our research builds upon existing financial literature on volatility risk premia and contango/backwardation dynamics in the volatility markets (Zhang & Zhu, 2006; Alexander & Korovilas, 2012).

Volatility derivatives have become essential tools for managing risk and engaging in speculative trades (Whaley, 2009). The Chicago Board Options Exchange (CBOE) Volatility Index (VIX) measures the market’s expectation of 30-day forward-looking volatility derived from S&P 500 option prices (CBOE, 2018). Term structures in VIX futures often exhibit contango or backwardation, depending on macroeconomic and market conditions (Alexander & Korovilas, 2012).

This strategy seeks to exploit the spread between the front-month and second-month VIX futures as a proxy for term structure dynamics. The spread’s momentum, quantified by the RSI, serves as a signal for entry and exit points, aligning with empirical findings on mean reversion in volatility markets (Zhang & Zhu, 2006).

• Entry Signal: When RSI_t falls below the user-defined threshold (e.g., 30), indicating a potential undervaluation in the spread.

• Exit Signal: When RSI_t exceeds a threshold (e.g., 70), suggesting mean reversion has occurred.

Empirical Justification

The strategy aligns with findings that suggest predictable patterns in volatility futures spreads (Alexander & Korovilas, 2012). Furthermore, the use of RSI leverages insights from momentum-based trading models, which have demonstrated efficacy in various asset classes, including commodities and derivatives (Jegadeesh & Titman, 1993).

References

• Alexander, C., & Korovilas, D. (2012). The Hazards of Volatility Investing. Journal of Alternative Investments, 15(2), 92-104.

• CBOE. (2018). The VIX White Paper. Chicago Board Options Exchange.

• Jegadeesh, N., & Titman, S. (1993). Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency. The Journal of Finance, 48(1), 65-91.

• Zhang, C., & Zhu, Y. (2006). Exploiting Predictability in Volatility Futures Spreads. Financial Analysts Journal, 62(6), 62-72.

• Whaley, R. E. (2009). Understanding the VIX. The Journal of Portfolio Management, 35(3), 98-105.

Volatility IndicatorThe volatility indicator presented here is based on multiple volatility indices that reflect the market’s expectation of future price fluctuations across different asset classes, including equities, commodities, and currencies. These indices serve as valuable tools for traders and analysts seeking to anticipate potential market movements, as volatility is a key factor influencing asset prices and market dynamics (Bollerslev, 1986).

Volatility, defined as the magnitude of price changes, is often regarded as a measure of market uncertainty or risk. Financial markets exhibit periods of heightened volatility that may precede significant price movements, whether upward or downward (Christoffersen, 1998). The indicator presented in this script tracks several key volatility indices, including the VIX (S&P 500), GVZ (Gold), OVX (Crude Oil), and others, to help identify periods of increased uncertainty that could signal potential market turning points.

Volatility Indices and Their Relevance

Volatility indices like the VIX are considered “fear gauges” as they reflect the market’s expectation of future volatility derived from the pricing of options. A rising VIX typically signals increasing investor uncertainty and fear, which often precedes market corrections or significant price movements. In contrast, a falling VIX may suggest complacency or confidence in continued market stability (Whaley, 2000).

The other volatility indices incorporated in the indicator script, such as the GVZ (Gold Volatility Index) and OVX (Oil Volatility Index), capture the market’s perception of volatility in specific asset classes. For instance, GVZ reflects market expectations for volatility in the gold market, which can be influenced by factors such as geopolitical instability, inflation expectations, and changes in investor sentiment toward safe-haven assets. Similarly, OVX tracks the implied volatility of crude oil options, which is a crucial factor for predicting price movements in energy markets, often driven by geopolitical events, OPEC decisions, and supply-demand imbalances (Pindyck, 2004).

Using the Indicator to Identify Market Movements

The volatility indicator alerts traders when specific volatility indices exceed a defined threshold, which may signal a change in market sentiment or an upcoming price movement. These thresholds, set by the user, are typically based on historical levels of volatility that have preceded significant market changes. When a volatility index exceeds this threshold, it suggests that market participants expect greater uncertainty, which often correlates with increased price volatility and the possibility of a trend reversal.

For example, if the VIX exceeds a pre-determined level (e.g., 30), it could indicate that investors are anticipating heightened volatility in the equity markets, potentially signaling a downturn or correction in the broader market. On the other hand, if the OVX rises significantly, it could point to an upcoming sharp movement in crude oil prices, driven by changing market expectations about supply, demand, or geopolitical risks (Geman, 2005).

Practical Application

To effectively use this volatility indicator in market analysis, traders should monitor the alert signals generated when any of the volatility indices surpass their thresholds. This can be used to identify periods of market uncertainty or potential market turning points across different sectors, including equities, commodities, and currencies. The indicator can help traders prepare for increased price movements, adjust their risk management strategies, or even take advantage of anticipated price swings through options trading or volatility-based strategies (Black & Scholes, 1973).

Traders may also use this indicator in conjunction with other technical analysis tools to validate the potential for significant market movements. For example, if the VIX exceeds its threshold and the market is simultaneously approaching a critical technical support or resistance level, the trader might consider entering a position that capitalizes on the anticipated price breakout or reversal.

Conclusion

This volatility indicator is a robust tool for identifying market conditions that are conducive to significant price movements. By tracking the behavior of key volatility indices, traders can gain insights into the market’s expectations of future price fluctuations, enabling them to make more informed decisions regarding market entries and exits. Understanding and monitoring volatility can be particularly valuable during times of heightened uncertainty, as changes in volatility often precede substantial shifts in market direction (French et al., 1987).

References

• Bollerslev, T. (1986). Generalized Autoregressive Conditional Heteroskedasticity. Journal of Econometrics, 31(3), 307-327.

• Christoffersen, P. F. (1998). Evaluating Interval Forecasts. International Economic Review, 39(4), 841-862.

• Whaley, R. E. (2000). Derivatives on Market Volatility. Journal of Derivatives, 7(4), 71-82.

• Pindyck, R. S. (2004). Volatility and the Pricing of Commodity Derivatives. Journal of Futures Markets, 24(11), 973-987.

• Geman, H. (2005). Commodities and Commodity Derivatives: Modeling and Pricing for Agriculturals, Metals and Energy. John Wiley & Sons.

• Black, F., & Scholes, M. (1973). The Pricing of Options and Corporate Liabilities. Journal of Political Economy, 81(3), 637-654.

• French, K. R., Schwert, G. W., & Stambaugh, R. F. (1987). Expected Stock Returns and Volatility. Journal of Financial Economics, 19(1), 3-29.

Z ScoreWhat Is Z-Score?

Z-score is a statistical measurement that describes a value's relationship to the mean of a group of values. Z-score is measured in terms of standard deviations from the mean. If a Z-score is 0, it indicates that the data point's score is identical to the mean score. A Z-score of 1.0 would indicate a value that is one standard deviation from the mean. Z-scores may be positive or negative, with a positive value indicating the score is above the mean and a negative score indicating it is below the mean.

CBOE Volatility Index

VIX is the ticker symbol and the popular name for the Chicago Board Options Exchange's CBOE Volatility Index, a popular measure of the stock market's expectation of volatility based on S&P 500 index options. It is calculated and disseminated on a real-time basis by the CBOE, and is often referred to as the fear index or fear gauge. To summarize, VIX is a volatility index derived from S&P 500 options for the 30 days following the measurement date, with the price of each option representing the market's expectation of 30-day forward-looking volatility. The resulting VIX index formulation provides a measure of expected market volatility on which expectations of further stock market volatility in the near future might be based

Z Scores of VIX

When the Z-scored VIX indicator exceeds the +2 standard deviation mark, the system forecasts mean reversion and decreasing volatility and the possibility of an upward trend in S&P500.

When the Z-scored VIX indicator falls below -2 standard deviations, the system predicts future increasing volatility and the possibility of a downward trend in S&P500.

BankNifty Multi-TimeFrames Price Panel [MaestroTrader]█ OVERVIEW

Price Panel provides Nifty /BankNifty Index comprehensive Price Insights on different time intervals. It helps to determine the trend of Index using top Index Heavy Weights along with Dow, India VIX & Index Spot Prices. It helps to determine the price behavior of the underlying Index/stock to make informed decisions while trading.

█ FEATURES

a) Displays Price in Multi Time Frames for Multi time frame analysis

b) Displays Weighted Securities price for Weighted INDEX price analysis.

c) Displays INDIA VIX and DOW for Combined INDIX VOLATALITY Analysis

█ MUTLI TIME FRAME ANALYSIS

How to use Multiple time frame analysis?

Multiple time frame analysis follows a top-down approach when trading and allows traders to gauge the longer-term trend while spotting ideal entries on a smaller time frame. Traders can then conduct technical analysis using multiple time frames to confirm or reject their trading bias.

Multiple time frame analysis, is the process of viewing the same symbols under different time frames. Usually, the larger time frame is used to establish a longer-term trend, while a shorter time frame is used to spot ideal entries into the market.

Let’s Say 75 & 15 TF’s Trend is up, then shorter time 5M is used to spot ideal entries on long side.

█ WEIGHTED INDEXS PRICE ANALYSIS

How to use Weighted Index Price Movement in Multi timeframes?

The index future trading price is based on the trading prices of the individual securities (stocks) that comprise the index basket. In other words, the stocks with higher weights will have more impact on the movement of the index. Price Panel provides the insights of these heavy weight stock price movement in different time frames, that can help you confirm or reject your trading bias.

HDFC Bank (28% Weight) will have more impact on the BankNifty Movement. By looking the top 4 bank's price movement in different timeframes, you can derive the BankNifty price trend.

█ VOLATALITY ANALYSIS

India VIX is a short form for India Volatility Index. It is the volatility index that measures the market’s expectation of volatility over the near term.

A lower VIX level usually implies that the market is confident about the movement and is expecting lower volatility and a stable range.

A higher VIX level usually signals high volatility and lower trader confidence about the current range of the market. A major directional move can be expected in the market and a quick broadening of range can be expected.

█ SETTINGS

• Time Frame Settings: Configure Time Frames 5 Min, 15 Min, 75 Min

• Table Settings: Configure Table Styles- Position- Font Color

• Symbol Settings: Configure Securities. Toggle (on/Off) Securities display.

• Index Settings: Display Bank Nifty or Nifty Heavy Weights.

█ PANEL DISPLAY VARIATIONS

BANK NIFTY VIEW

NIFTY VIEW

WITHOUT STOCKS - ONLY INDEX, VIX, DOW

█ THANKS

Thanks to Pine Team for this new great feature tables & Thanks to PineCoders for the `f_strRightOf` function.

█ DISCLIAMER

Indicator is built for educational purposes. Test it before use.

Hope - These features help you get quick insights of the price movement to take informed trades.

You are free to use the code, please share the credit for reuse.

Happy Trading !!

Equity Risk PremiumInspired by the article "2020's Best Performing Hedge Fund Warns Of 'Incredible Move' Around The Election" from ZeroHedge:

This script explores the relationship and attempts to find dislocation between equity risk (VIX) and high-yield corporate debt risk (VXHYG, The Cboe VXHYG Index is an estimate of the expected 30-day volatility of the return on iShares' High Yield Grade ETF (HYG). VXHYG is derived by applying the VIX algorithm to options on HYG).

The basic logic is (closing price of VIX / closing price of VXHYG) - 1. When equity risk is high and credit risk is low, the value of premium will be high, and vice-versa.

“'Equity volatility is almost inescapably high. Is that a good form of insurance? The payoff profiles are nothing like they were back in January. Whereas in credit, we’re almost back to where we were in January.

I find today the risk-reward profile of credit to be basically among the worst, relative to other things, I’ve seen in my career,' Weinstein said. 'A VIX at 20 used to be quite a feat. Here we are at 30, and the credit market hasn’t blinked.'

As a result of the gaping divergence between the VIX and credit spreads - the two had moved in tandem for years, but in August the two series blew out as the VIX started rising as spreads kept falling - Weinstein has pounced on the trade, betting on vol compression."

When equity risk premium is high, the market may be forming a local top.

When equity risk premium is low, the market may be forming a local bottom.

Make sure to select your current timeframe on the dropdown menu.

Composite Sentiment Indicator (SPY/QQQ/SOXX + VixFix)# Multi-Index Composite Sentiment Indicator

A comprehensive sentiment indicator that works across SPY, QQQ, SOXX, and custom symbols. Combines volatility, options flow, macro factors, technicals, and seasonality into a single z-score composite.

## What It Does

Takes multiple market sentiment inputs (VIX, put/call ratios, breadth, yields, etc.) and smooshes them into one normalized line. When the composite is high = markets getting spooked. When it's low = markets getting complacent.

## Key Features

- **Multi-Index Support**: Automatically adapts for SPY (uses VIX), QQQ (uses VXN), SOXX (uses VixFix), or custom symbols

- **VixFix Integration**: Larry Williams' VixFix for indices without dedicated VIX measures

- **Signal MA**: Choose from SMA/EMA/WMA/HMA/TEMA/DEMA with color coding (red above MA = risk-on, green below = risk-off)

- **September Focus**: Built-in seasonality weighting for September weakness patterns

- **Comprehensive Components**: Volatility, options sentiment, macro factors, technicals, and sector-specific metrics

## How to Use

**Basic Setup:**

1. Pick your index (SPY/QQQ/SOXX)

2. Choose signal MA type and length (EMA 21 is a good start)

3. Watch for extreme readings and MA crossovers

**Color Signals:**

- Red composite = above signal MA = bearish sentiment

- Green composite = below signal MA = bullish sentiment

- Extreme high readings (red background) = potential tops

- Extreme low readings (green background) = potential bottoms

**For Different Indices:**

- **QQQ**: Uses NASDAQ VIX (VXN) when available, falls back to VixFix

- **SOXX**: Includes semiconductor cycle indicators, uses VixFix for volatility

- **Custom**: Adapts automatically, relies on VixFix and general market metrics

## Components Included

**Volatility**: VIX/VXN/VixFix, term structure, historical vol

**Options**: Put/call ratios, SKEW index

**Macro**: DXY, 10Y yields, yield curve, TIPS spreads

**Technical**: RSI deviation, momentum

**Seasonality**: September effects, quad witching, month-end patterns

**Breadth**: S&P 500 and NASDAQ breadth measures

## Pro Tips

- Works well on Daily Timeframe

- September gets extra weight automatically - watch for August setup signals

- Keltner envelope breaks often mark sentiment exhaustion points

- Use alerts for extreme readings and MA crossovers

Works best when you understand that sentiment extremes often mark turning points, not continuation signals. High readings don't mean "keep shorting" - they mean "start looking for reversal setups."

## Settings Worth Tweaking

- Signal MA type/length for your timeframe

- Component weights based on what matters for your index

- Envelope multipliers for your risk tolerance

- VixFix parameters if default doesn't fit your symbol's volatility

The table shows all current component readings so you can see what's driving the signal. Good for context and debugging weird readings.

Defense Mode Dashboard ProWhat it is

A one‑look market regime dashboard for ES, NQ, YM, RTY, and SPY that tells you when to play defense, when you might have an offense cue, and when to chill. It blends VIX, VIX term structure, ATR 5 over 60, and session gap signals with clean alerts and a compact table you can park anywhere.

Why traders like it

Because it filters out the noise. Regime first, tactics second. You avoid trading size into landmines and lean in when volatility cooperates.

What it measures

Volatility stress with VIX level and VIX vs 20‑SMA

Term structure using VX1 vs VX2 with two modes

Diff mode: VX1 minus VX2

Ratio mode: VX1 divided by VX2

Realized volatility using ATR5 over ATR60 with optional smoothing

Session risk from RTH opening gaps and overnight range, normalized by ATR

How to use in 30 seconds

Pick a preset in the inputs. ES, NQ, YM, RTY, SPY are ready.

Leave thresholds at defaults to start.

Add one TradingView alert using “Any alert() function call”.

Trade smaller or stand aside when the header reads DEFENSE ON. Consider leaning in only when you see OFFENSE CUE and your playbook agrees.

Defaults we recommend

VIX triggers: 22 and 1.25× the 20‑SMA

Term mode: Diff with tolerance 0.00. Use Ratio at 1.00+ for choppier markets

ATR 5/60 defense: 1.25. Offense cue: 0.85 or lower

ATR smoothing: 1. Try 2 to 3 if you want fewer flips

Gap mode: RTH. Turn Both on if you want ON range to count too

RTH wild gap: 0.60× ATR5. ON wild range: 0.80× ATR5

Alert cadence: Once per RTH session

Snooze: Quick snooze first 30 minutes on. Fire on snooze exit off, unless you really want the catch‑up ping

New since the last description

Multi‑asset presets set symbols and RTH windows for ES, NQ, YM, RTY, SPY

Term ratio mode with near‑flat warning when ratio is between 1.00 and your trigger

ATR smoothing for the 5 over 60 ratio

RTH keying for cadence, so “Once per RTH session” behaves like a trader expects

Snooze upgrades with quick snooze tied to the first N minutes of RTH and an optional fire‑on‑snooze‑exit

Compact title merge and user color controls for labels, values, borders, and background

Exposed series for integrations: DefenseOn(1=yes) and OffenseCue(1=yes)

Debug toggle to visualize gap points, ON range, and term readings

Stronger NA handling with a clear “No core data” row when feeds are missing

Notes

Dynamic alerts require “Any alert() function call”.

Works on any chart timeframe. Daily reads and 1‑minute anchors handle the regime logic.

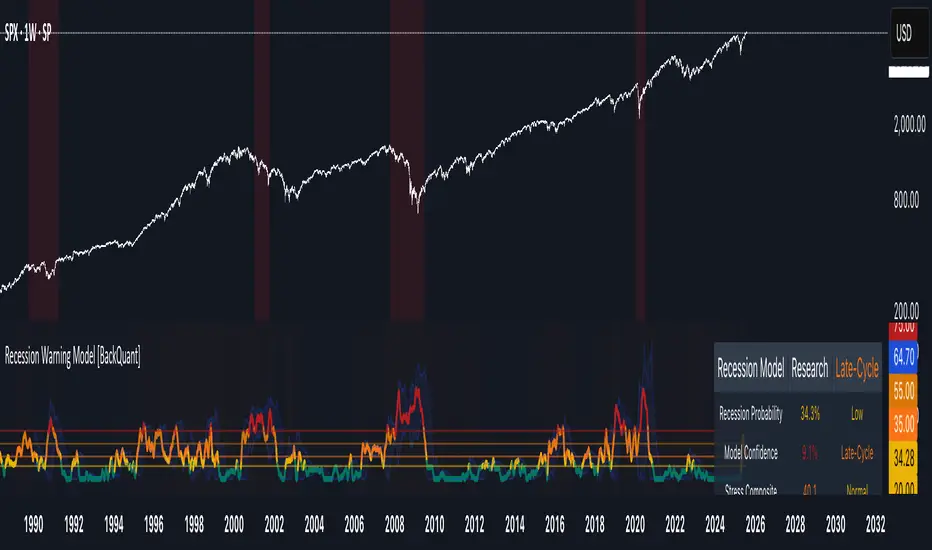

Recession Warning Model [BackQuant]Recession Warning Model

Overview

The Recession Warning Model (RWM) is a Pine Script® indicator designed to estimate the probability of an economic recession by integrating multiple macroeconomic, market sentiment, and labor market indicators. It combines over a dozen data series into a transparent, adaptive, and actionable tool for traders, portfolio managers, and researchers. The model provides customizable complexity levels, display modes, and data processing options to accommodate various analytical requirements while ensuring robustness through dynamic weighting and regime-aware adjustments.

Purpose

The RWM fulfills the need for a concise yet comprehensive tool to monitor recession risk. Unlike approaches relying on a single metric, such as yield-curve inversion, or extensive economic reports, it consolidates multiple data sources into a single probability output. The model identifies active indicators, their confidence levels, and the current economic regime, enabling users to anticipate downturns and adjust strategies accordingly.

Core Features

- Indicator Families : Incorporates 13 indicators across five categories: Yield, Labor, Sentiment, Production, and Financial Stress.

- Dynamic Weighting : Adjusts indicator weights based on recent predictive accuracy, constrained within user-defined boundaries.

- Leading and Coincident Split : Separates early-warning (leading) and confirmatory (coincident) signals, with adjustable weighting (default 60/40 mix).

- Economic Regime Sensitivity : Modulates output sensitivity based on market conditions (Expansion, Late-Cycle, Stress, Crisis), using a composite of VIX, yield-curve, financial conditions, and credit spreads.

- Display Options : Supports four modes—Probability (0-100%), Binary (four risk bins), Lead/Coincident, and Ensemble (blended probability).

- Confidence Intervals : Reflects model stability, widening during high volatility or conflicting signals.

- Alerts : Configurable thresholds (Watch, Caution, Warning, Alert) with persistence filters to minimize false signals.

- Data Export : Enables CSV output for probabilities, signals, and regimes, facilitating external analysis in Python or R.

Model Complexity Levels

Users can select from four tiers to balance simplicity and depth:

1. Essential : Focuses on three core indicators—yield-curve spread, jobless claims, and unemployment change—for minimalistic monitoring.

2. Standard : Expands to nine indicators, adding consumer confidence, PMI, VIX, S&P 500 trend, money supply vs. GDP, and the Sahm Rule.

3. Professional : Includes all 13 indicators, incorporating financial conditions, credit spreads, JOLTS vacancies, and wage growth.

4. Research : Unlocks all indicators plus experimental settings for advanced users.

Key Indicators

Below is a summary of the 13 indicators, their data sources, and economic significance:

- Yield-Curve Spread : Difference between 10-year and 3-month Treasury yields. Negative spreads signal banking sector stress.

- Jobless Claims : Four-week moving average of unemployment claims. Sustained increases indicate rising layoffs.

- Unemployment Change : Three-month change in unemployment rate. Sharp rises often precede recessions.

- Sahm Rule : Triggers when unemployment rises 0.5% above its 12-month low, a reliable recession indicator.

- Consumer Confidence : University of Michigan survey. Declines reflect household pessimism, impacting spending.

- PMI : Purchasing Managers’ Index. Values below 50 indicate manufacturing contraction.

- VIX : CBOE Volatility Index. Elevated levels suggest market anticipation of economic distress.

- S&P 500 Growth : Weekly moving average trend. Declines reduce wealth effects, curbing consumption.

- M2 + GDP Trend : Monitors money supply and real GDP. Simultaneous declines signal credit contraction.

- NFCI : Chicago Fed’s National Financial Conditions Index. Positive values indicate tighter conditions.

- Credit Spreads : Proxy for corporate bond spreads using 10-year vs. 2-year Treasury yields. Widening spreads reflect stress.

- JOLTS Vacancies : Job openings data. Significant drops precede hiring slowdowns.

- Wage Growth : Year-over-year change in average hourly earnings. Late-cycle spikes often signal economic overheating.

Data Processing

- Rate of Change (ROC) : Optionally applied to capture momentum in data series (default: 21-bar period).

- Z-Score Normalization : Standardizes indicators to a common scale (default: 252-bar lookback).

- Smoothing : Applies a short moving average to final signals (default: 5-bar period) to reduce noise.

- Binary Signals : Generated for each indicator (e.g., yield-curve inverted or PMI below 50) based on thresholds or Z-score deviations.

Probability Calculation

1. Each indicator’s binary signal is weighted according to user settings or dynamic performance.

2. Weights are normalized to sum to 100% across active indicators.

3. Leading and coincident signals are aggregated separately (if split mode is enabled) and combined using the specified mix.

4. The probability is adjusted by a regime multiplier, amplifying risk during Stress or Crisis regimes.

5. Optional smoothing ensures stable outputs.

Display and Visualization

- Probability Mode : Plots a continuous 0-100% recession probability with color gradients and confidence bands.

- Binary Mode : Categorizes risk into four levels (Minimal, Watch, Caution, Alert) for simplified dashboards.

- Lead/Coincident Mode : Displays leading and coincident probabilities separately to track signal divergence.

- Ensemble Mode : Averages traditional and split probabilities for a balanced view.

- Regime Background : Color-coded overlays (green for Expansion, orange for Late-Cycle, amber for Stress, red for Crisis).

- Analytics Table : Optional dashboard showing probability, confidence, regime, and top indicator statuses.

Practical Applications

- Asset Allocation : Adjust equity or bond exposures based on sustained probability increases.

- Risk Management : Hedge portfolios with VIX futures or options during regime shifts to Stress or Crisis.

- Sector Rotation : Shift toward defensive sectors when coincident signals rise above 50%.

- Trading Filters : Disable short-term strategies during high-risk regimes.

- Event Timing : Scale positions ahead of high-impact data releases when probability and VIX are elevated.

Configuration Guidelines

- Enable ROC and Z-score for consistent indicator comparison unless raw data is preferred.

- Use dynamic weighting with at least one economic cycle of data for optimal performance.

- Monitor stress composite scores above 80 alongside probabilities above 70 for critical risk signals.

- Adjust adaptation speed (default: 0.1) to 0.2 during Crisis regimes for faster indicator prioritization.

- Combine RWM with complementary tools (e.g., liquidity metrics) for intraday or short-term trading.

Limitations

- Macro indicators lag intraday market moves, making RWM better suited for strategic rather than tactical trading.

- Historical data availability may constrain dynamic weighting on shorter timeframes.

- Model accuracy depends on the quality and timeliness of economic data feeds.

Final Note

The Recession Warning Model provides a disciplined framework for monitoring economic downturn risks. By integrating diverse indicators with transparent weighting and regime-aware adjustments, it empowers users to make informed decisions in portfolio management, risk hedging, or macroeconomic research. Regular review of model outputs alongside market-specific tools ensures its effective application across varying market conditions.

Liquid Pulse Liquid Pulse by Dskyz (DAFE) Trading Systems

Liquid Pulse is a trading algo built by Dskyz (DAFE) Trading Systems for futures markets like NQ1!, designed to snag high-probability trades with tight risk control. it fuses a confluence system—VWAP, MACD, ADX, volume, and liquidity sweeps—with a trade scoring setup, daily limits, and VIX pauses to dodge wild volatility. visuals include simple signals, VWAP bands, and a dashboard with stats.

Core Components for Liquid Pulse

Volume Sensitivity (volumeSensitivity) controls how much volume spikes matter for entries. options: 'Low', 'Medium', 'High' default: 'High' (catches small spikes, good for active markets) tweak it: 'Low' for calm markets, 'High' for chaos.

MACD Speed (macdSpeed) sets the MACD’s pace for momentum. options: 'Fast', 'Medium', 'Slow' default: 'Medium' (solid balance) tweak it: 'Fast' for scalping, 'Slow' for swings.

Daily Trade Limit (dailyTradeLimit) caps trades per day to keep risk in check. range: 1 to 30 default: 20 tweak it: 5-10 for safety, 20-30 for action.

Number of Contracts (numContracts) sets position size. range: 1 to 20 default: 4 tweak it: up for big accounts, down for small.

VIX Pause Level (vixPauseLevel) stops trading if VIX gets too hot. range: 10 to 80 default: 39.0 tweak it: 30 to avoid volatility, 50 to ride it.

Min Confluence Conditions (minConditions) sets how many signals must align. range: 1 to 5 default: 2 tweak it: 3-4 for strict, 1-2 for more trades.

Min Trade Score (Longs/Shorts) (minTradeScoreLongs/minTradeScoreShorts) filters trade quality. longs range: 0 to 100 default: 73 shorts range: 0 to 100 default: 75 tweak it: 80-90 for quality, 60-70 for volume.

Liquidity Sweep Strength (sweepStrength) gauges breakouts. range: 0.1 to 1.0 default: 0.5 tweak it: 0.7-1.0 for strong moves, 0.3-0.5 for small.

ADX Trend Threshold (adxTrendThreshold) confirms trends. range: 10 to 100 default: 41 tweak it: 40-50 for trends, 30-35 for weak ones.

ADX Chop Threshold (adxChopThreshold) avoids chop. range: 5 to 50 default: 20 tweak it: 15-20 to dodge chop, 25-30 to loosen.

VWAP Timeframe (vwapTimeframe) sets VWAP period. options: '15', '30', '60', '240', 'D' default: '60' (1-hour) tweak it: 60 for day, 240 for swing, D for long.

Take Profit Ticks (Longs/Shorts) (takeProfitTicksLongs/takeProfitTicksShorts) sets profit targets. longs range: 5 to 100 default: 25.0 shorts range: 5 to 100 default: 20.0 tweak it: 30-50 for trends, 10-20 for chop.

Max Profit Ticks (maxProfitTicks) caps max gain. range: 10 to 200 default: 60.0 tweak it: 80-100 for big moves, 40-60 for tight.

Min Profit Ticks to Trail (minProfitTicksTrail) triggers trailing. range: 1 to 50 default: 7.0 tweak it: 10-15 for big gains, 5-7 for quick locks.

Trailing Stop Ticks (trailTicks) sets trail distance. range: 1 to 50 default: 5.0 tweak it: 8-10 for room, 3-5 for fast locks.

Trailing Offset Ticks (trailOffsetTicks) sets trail offset. range: 1 to 20 default: 2.0 tweak it: 1-2 for tight, 5-10 for loose.

ATR Period (atrPeriod) measures volatility. range: 5 to 50 default: 9 tweak it: 14-20 for smooth, 5-9 for reactive.

Hardcoded Settings volLookback: 30 ('Low'), 20 ('Medium'), 11 ('High') volThreshold: 1.5 ('Low'), 1.8 ('Medium'), 2 ('High') swingLen: 5

Execution Logic Overview trades trigger when confluence conditions align, entering long or short with set position sizes. exits use dynamic take-profits, trailing stops after a profit threshold, hard stops via ATR, and a time stop after 100 bars.

Features Multi-Signal Confluence: needs VWAP, MACD, volume, sweeps, and ADX to line up.

Risk Control: ATR-based stops (capped 15 ticks), take-profits (scaled by volatility), and trails.

Market Filters: VIX pause, ADX trend/chop checks, volatility gates. Dashboard: shows scores, VIX, ADX, P/L, win %, streak.

Visuals Simple signals (green up triangles for longs, red down for shorts) and VWAP bands with glow. info table (bottom right) with MACD momentum. dashboard (top right) with stats.

Chart and Backtest:

NQ1! futures, 5-minute chart. works best in trending, volatile conditions. tweak inputs for other markets—test thoroughly.

Backtesting: NQ1! Frame: Jan 19, 2025, 09:00 — May 02, 2025, 16:00 Slippage: 3 Commission: $4.60

Fee Typical Range (per side, per contract)

CME Exchange $1.14 – $1.20

Clearing $0.10 – $0.30

NFA Regulatory $0.02

Firm/Broker Commis. $0.25 – $0.80 (retail prop)

TOTAL $1.60 – $2.30 per side

Round Turn: (enter+exit) = $3.20 – $4.60 per contract

Disclaimer this is for education only. past results don’t predict future wins. trading’s risky—only use money you can lose. backtest and validate before going live. (expect moderators to nitpick some random chart symbol rule—i’ll fix and repost if they pull it.)

About the Author Dskyz (DAFE) Trading Systems crafts killer trading algos. Liquid Pulse is pure research and grit, built for smart, bold trading. Use it with discipline. Use it with clarity. Trade smarter. I’ll keep dropping badass strategies ‘til i build a brand or someone signs me up.

2025 Created by Dskyz, powered by DAFE Trading Systems. Trade smart, trade bold.

Previous High and Low Count with Probabilities + Risk On/Off1. Purpose of the Script:

This trading script combines two important concepts:

Previous High and Low Count: It tracks whether the current price exceeds the previous day’s high or low and calculates probabilities for the next price movement (up or down).

Risk On / Risk Off Indicator: It evaluates market sentiment through various indicators (such as the Fear & Greed Index, VIX, and others) and shows whether the market is in a risk-on or risk-off state. This information impacts the probabilities of price movement.

2. How it Works:

Previous High and Low:

The script tracks how often the price exceeds the previous day’s high or low and calculates the probability of an upward or downward movement based on that. This gives you an idea of how often the market reacts at the previous day's high or low.

Risk On / Risk Off:

Based on various market factors (Fear & Greed Index, VIX, Put-Call Ratio, etc.), the script calculates the Risk On or Risk Off state.

In Risk On, the probability of an upward movement increases, and the probability of a downward movement decreases. In Risk Off, it’s the opposite.

Adjusted Probabilities:

The probabilities for an Up or Down movement are adjusted based on the current Risk On / Risk Off state. In a Risk On environment, the probability for an upward move increases, while in a Risk Off environment, the probability for a downward move increases.

3. How to Use the Script:

Add the Script in TradingView:

TradingView:

Click on "Add to Chart" to apply the script to your chart.

Manual Input of Indicators:

For the Fear & Greed Index, VIX, and other indicators, you need to manually enter the current values. You can get these values from various publicly available sources:

Fear & Greed Index: CNN Fear & Greed Index

VIX (Volatility Index): VIX Index

Other indicators like Put-Call Ratio, Bitcoin Volatility, Oil Prices, and US Dollar Index can also be manually inputted, and they can be found on finance websites like Yahoo Finance, MarketWatch, and Bloomberg.

Observe the Colors and Symbols:

If the market is in a Risk On state, the background will turn green, and a green triangle will appear below the candle.

If the market is in a Risk Off state, the background will turn red, and a red triangle will appear above the candle.

Track the Probabilities:

A label will appear on the chart showing the calculated probabilities for Up and Down movements. These probabilities are adjusted based on the current market state (Risk On/Off).

4. Meaning of the Probabilities:

Up Probability: Indicates the probability that the price will rise.

Down Probability: Indicates the probability that the price will fall.

The probabilities are dynamic and adjust based on the Risk On / Risk Off state, helping you make better decisions based on the current market conditions.

Financial Crisis Predictor - Doomsday ClockThe **Financial Crisis Predictor - Doomsday Clock** is a composite indicator that evaluates multiple market conditions to determine financial risk levels. It combines four key metrics: market volatility (via VIX), yield curve spread, stock market momentum, and credit risk (via high-yield spread). Each metric contributes to a weighted "risk score," scaled between 0 and 100, which helps gauge the probability of a financial crisis. Here's a breakdown of how it works:

### 1. **Market Volatility (VIX)**

- **How it's measured:**

- Uses the VIX index, which represents expected market volatility.

- Applies two exponential moving averages (EMAs) to smooth out the data—one fast and one slow.

- Triggers a signal if the fast EMA crosses above the slow EMA and VIX exceeds a defined threshold (default is 30).

- **Weighting:**

- Contributes up to 35% of the total risk score when active.

### 2. **Yield Curve Spread**

- **How it's measured:**

- Takes the difference between the yields of 10-year and 2-year U.S. Treasury bonds (inversion indicates recession risk).

- If the spread drops below a certain threshold (default is 0.2), it signals a potential recession.

- **Weighting:**

- Contributes up to 25% of the risk score.

### 3. **Stock Market Momentum**

- **How it's measured:**

- Analyzes the S&P 500 (SPY) using a 20-day EMA for price momentum.

- Checks for a cross under the 20-day EMA and if the 5-day rate of change (ROC) is less than -2.

- This combination signals bearish market momentum.

- **Weighting:**

- Contributes up to 20% of the risk score.

### 4. **Credit Risk (High Yield Spread)**

- **How it's measured:**

- Assesses high-yield corporate bond spreads using EMAs, similar to the VIX logic.

- A crossover of the fast EMA above the slow EMA combined with spreads exceeding a defined threshold (default is 5.0) indicates increased credit risk.

- **Weighting:**

- Contributes up to 20% of the total risk score.

### 5. **Risk Score Calculation**

- The final **risk score** ranges from 0 to 100 and is calculated using the weighted sum of the four indicators.

- The score is smoothed to minimize false signals and maintain stability.

### 6. **Risk Zones**

- **Extreme Risk:** If the risk score is ≥ 75, indicating a severe crisis warning.

- **High Risk:** If the risk score is between 15 and 75, signaling heightened risk.

- **Moderate Risk:** If the risk score is between 10 and 15, representing potential concerns.

- **Low Risk:** If the risk score is < 10, suggesting stable conditions.

### 7. **Visual & Alerts**

- The indicator plots the risk score on a chart with color-coded backgrounds to indicate risk levels: green (low), yellow (moderate), orange (high), and red (extreme).

- Alert conditions are set for each risk zone, notifying users when the risk level transitions into a higher zone.

This indicator aims to quickly detect potential financial crises by aggregating signals from key market factors, making it a versatile tool for traders, analysts, and risk managers.

[blackcat] L2 Votatility of Williams VixFix Risk AssessmentHey there! I previously wrote an article about the Larry Williams ViX Fix technical indicator. Soon after, friends from the TradingView community told me that this indicator could be combined with the Risk Assessment indicator I wrote about earlier to determine when to go long or short. At the time, I found it a bit cumbersome to use both indicators together, so I came up with a solution: to merge them. This way, we can use one technical indicator to visually see whether we should go long or short. Isn't that cool? The indicator has a very common name: ** L2 Votatility of Williams VixFix Risk Assessment, or VoWVRA for short.**

This TradingView Pine Script is a custom indicator based on the Larry Williams ViX Fix technical indicator, designed to help traders with risk assessment and trading decisions. The Larry Williams ViX Fix indicator is derived from the volatility of the S&P 500 index and is mainly used to display changes in current market sentiment. The indicator determines market volatility by calculating the distance between the highest price, the lowest price, and the closing price. The higher the value of the indicator, the more tense the market sentiment, and the higher the market volatility; conversely, the lower the value, the more stable the market sentiment and the lower the market volatility.

The VoWVRA indicator is based on the Larry Williams ViX Fix indicator, combined with technical indicators such as Bollinger Bands and EMA, to assess market risk. The indicator can be customized with input parameters to suit different markets and investor needs. Using the VoWVRA indicator can help traders make wiser choices in risk control and trading decisions.

In addition, this TradingView Pine Script also includes a risk assessment indicator. The indicator calculates a series of values and then applies the exponential moving average (EMA) to the percentage change between the closing price and the highest and lowest prices within a certain range to determine the safety level. The safety level is then compared to different thresholds to determine the market's risk level. The risk assessment indicator can be customized with input parameters such as risk length, safety length, and EMA length to suit different market conditions and investor preferences. Using the risk assessment indicator can help traders make wiser decisions in risk management and trading strategies.

By using the VoWVRA and risk assessment indicators, traders can more accurately assess market risk and make wiser choices in trading decisions.

Expected SPX Movement by timeframeTHIS INDICATOR ONLY WORKS FOR SP:SPX CHART

This code will help you to measure the expected movement of SP:SPX in a previously selected timeframe based on the current value of VIX index

E.g. if the current value of VIX is 30 we calculate first the expected move of the next 12 months.

If you selected the Daily timeframe it will calculate the expected move of SPX in the next Day by dividing the current VIX Value by the squared root of 252

(The 252 value corresponds to the approximate amount of trading sessions of the year)

If you selected the Weekly timeframe it will calculate the expected move of SPX in the next Week by dividing the current VIX Value by the squared root of 52

(The 52 value corresponds to the amount of weeks of the year)

If you selected the Monthly timeframe it will calculate the expected move of SPX in the next Week by dividing the current VIX Value by the squared root of 12

(The 12 value corresponds to the amount of months of the year)

For lower timeframes you have to calculate the amount of ticks in each trading session of the year in order to get that specific range

Once you have that calculation it it'll provide the range expressed as percentage of the expected move for the following period.

This script will plot that information in a range of 2 lines which represents the expected move of the SPX for the next period

The red flag indicator tells if that period closed between the 2 previous values marked by the range

MACD PlusMoving Average Convergence Divergence – MACD

The MACD is an extremely popular indicator used in technical analysis. It can be used to identify aspects of a security's overall trend. Most notably these aspects are momentum, as well as trend direction and duration. What makes the MACD so informative is that it is actually the combination of two different types of indicators. First, the MACD employs two Moving Averages of varying lengths (which are lagging indicators) to identify trend direction and duration. Then, it takes the difference in values between those two Moving Averages (MACD Line) and an EMA of those Moving Averages (Signal Line) and plots that difference between the two lines as a histogram which oscillates above and below a center Zero Line. The histogram is used as a good indication of a security's momentum.

Added Color Plots to Settings Pane.

Switched MTF Logic to turn ON/OFF automatically w/ TradingView's Built in Feature.

Added Ability to Turn ON/OFF Show MacD & Signal Line.

Added Ability to Turn ON/OFF Show Histogram.

Added Ability to Change MACD Line Colors Based on Trend.

Added Ability to Highlight Price Bars Based on Trend.

Added Alerts to Settings Pane.

Customized Alerts to Show Symbol, TimeFrame, Closing Price, MACD Crosses Up & MACD Crosses Down Signals in Alert.

Alerts are Pre-Set to only Alert on Bar Close.

Added ability to show Dots when MACD Crosses.

Added Ability to Change Plot Widths in Settings Pane.

Added in Alert Feature where Cross Up if above 0 or cross down if below 0 (OFF By Default).

Squeeze Pro

Traditionally, John Carter's version uses 20 period SMAs as the basis lines on both the BB and the KC.

In this version, I've given the freedom to change this and try out different types of moving averages.

The original squeeze indicator had only one Squeeze setting, though this new one has three.

The gray dot Squeeze, call it a "low squeeze" or an "early squeeze" - this is the easiest Squeeze to form based on its settings.

The orange dot Squeeze is the original from the first Squeeze indicator.

And finally, the yellow dot squeeze, call it a "high squeeze" or "power squeeze" - is the most difficult to form and suggests price is under extreme levels of compression.

Colored Directional Movement Index (CDMI) , a custom interpretation of J. Welles Wilder’s Directional Movement Index (DMI), where :

DMI is a collection of three separate indicators ( ADX , +DI , -DI ) combined into one and measures the trend’s strength as well as its direction

CDMI is a custom interpretation of DMI which presents ( ADX , +DI , -DI ) with a color scale - representing the trend’s strength, color density - representing momentum/slope of the trend’s strength, and triangle up/down shapes - representing the trend’s direction. CDMI provides all the information in a single line with colored triangle shapes plotted on the bottom. DMI can provide quality information and even trading signals but it is not an easy indicator to master, whereus CDMI simplifies its usage. The CDMI adds additional insight of verifying/confirming the trend as well as its strength

Label :

Displaying the trend strength and direction

Displaying adx and di+/di- values

Displaying adx's momentum (growing or falling)

Where tooltip label describes "howto read colored dmi line"

Ability to display historical values of DMI readings displayed in the label.

Added "Expert Trend Locator - XTL"

The XTL was developed by Tom Joseph (in his book Applying Technical Analysis ) to identify major trends, similar to Elliott Wave 3 type swings.

Blue bars are bullish and indicate a potential upwards impulse.

Red bars are bearish and indicate a potential downwards impulse.

White bars indicate no trend is detected at the moment.

Added "Williams Vix Fix" signal. The Vix is one of the most reliable indicators in history for finding market bottoms. The Williams Vix Fix is simply a code from Larry Williams creating almost identical results for creating the same ability the Vix has to all assets.

The VIX has always been much better at signaling bottoms than tops. Simple reason is when market falls retail traders panic and increase volatility , and professionals come in and capitalize on the situation. At market tops there is no one panicking... just liquidity drying up.

The FE green triangles are "Filtered Entries"

The AE green triangles are "Aggressive Filtered Entries"

MACandles-LinearRegression-StrategyThis is combination of multiple indicators and strategies. Mainly useful for indexes and to time the entry and exits of indexes. No stoploss used - makes it less desirable for leveraged trades or trading individual stocks.

Let us rewind and look back at some of the indicators/strategies published earlier.

1. Moving Average Candles - this is one of my favourite tool for general trend filtering. Applying supertrend on moving average candles is one of the easiest ways to find reversal in trending market without exiting positions too early. Few scripts published on this basis are:

MA Candles Supertrend

MA Candles Supertrend Strategy

2. VixFix and Linear Regression - this itself is combination of two indicators.

Williams-Vix-Fix-Finds-Market-Bottoms - by @ChrisMoody

Squeeze-Momentum-Indicator - by @LazyBear

I have combined these two indicators to derive VIX-Fix linear regression to find absolute market bottoms. More description here:

VixFixLinReg-Strategy

VixFixLinReg-Indicator

Now, in this strategy, we combine all these together.

Derive moving average candles

Derive momentum of moving average candles

Derive Linear regression on momentum

Optionally, also calculate VIX Fix and Linear regression on VixFix momentum

To find market bottom:

There are two options

1. Use when momentum of MA candles hit bottom (red) and slowly turn up (orange). In aggressiveLong mode, signals are also generated when momentum starts going positive from negative.

2. Use Vix Fix linear regression of MA candles as described in the original script of VixFixLinReg-Strategy

To find market top

Here only Ma candles momentum decreasing is used as signal. If looking for longTrades , exit signal is generated only when momentum is turning negative extreme(orange). Or else, exit signal is generated when momentum has turned neutral.

At this stage, it is very much experimental - use it with caution :)

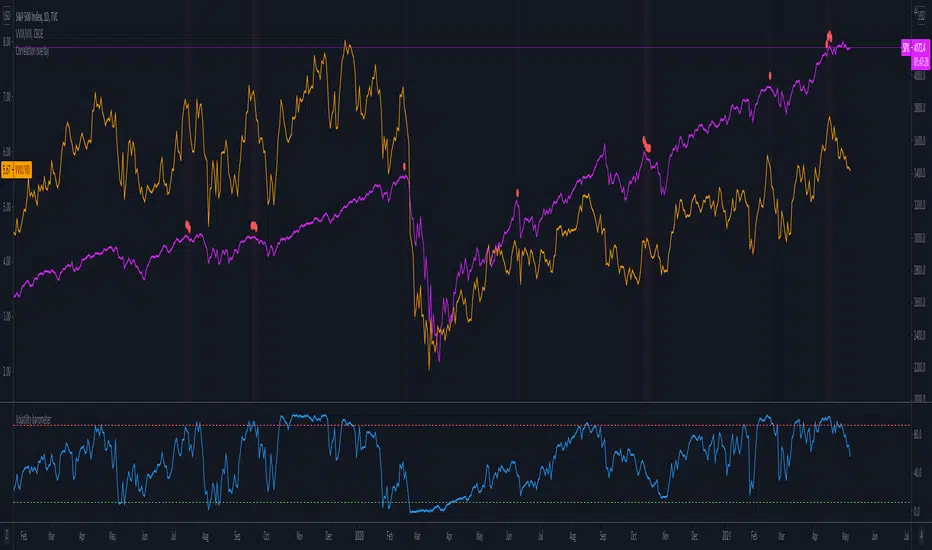

Volatility barometerIt is the indicator that analyzes the behaviour of VIX against CBOE volaility indices (VIX3M, VIX6M and VIX1Y) and VIX futures (next contract to the front one - VX!2). Because VIX is a derivate of SPX, the indicator shall be used on the SPX chart (or equivalent like SPY).

When the readings get above 90 / below 10, it means the market is overbought / oversold in terms of implied volatility. However, it does not mean it will reverse - if the price go higher along with the indicator readings then everything is fine. There is an alarming situation when the SPX is diverging - e.g. the price go higher, the readings lower. It means the SPX does not play in the same team as IVOL anymore and might reverse.

You can use it in conjunction with other implied volatility indicators for stronger signals: the Correlation overlay ( - the indicator that measures the correlation between VVIX and VIX) and VVIX/VIX ratio (it generates a signal the ratio makes 50wk high).

Squeeze Momentum [Plus]The "Momentum" in this indicator is smoothed out using linear regression. The Momentum is what is displayed on the indicator as a histogram, its purpose is obvious (to show momentum).

What is a Squeeze? A squeeze occurs when Bollinger Bands tighten up enough to slip inside of Keltner Channels .

This is interpreted as price is compressing and building up energy before releasing it and making a big move.

Traditionally, John Carter's version uses 20 period SMAs as the basis lines on both the BB and the KC.

In this version, I've given the freedom to change this and try out different types of moving averages.

The original squeeze indicator had only one Squeeze setting, though this new one has three.

The gray dot Squeeze, call it a "low squeeze" or an "early squeeze" - this is the easiest Squeeze to form based on its settings.

The orange dot Squeeze is the original from the first Squeeze indicator.

And finally, the yellow dot squeeze, call it a "high squeeze" or "power squeeze" - is the most difficult to form and suggests price is under extreme levels of compression.

Now to explain the parameters:

Squeeze Input - This is just the source for the Squeeze to use, default value is closing price.

Length - This is the length of time used to calculate the Bollinger Bands and Keltner Channels .

Bollinger Bands Calculation Type - Selects the type of moving average used to create the Bollinger Bands .

Keltner Channel Calculation Type - Selects the type of moving average used to create the Keltner Channel.

Color Format - you to choose one of 5 different color schemes.

Draw Divergence - Self explanatory here, this will auto-draw divergence on the indicator.

Gray Background for Dark Mode - to make them more visually appealing.

Added ADX (Average Directional Index) that measure a trend’s strength. The higher the ADX value, the stronger the trend. The ADX line is white when it has a positive slope, otherwise it is gray. When the ADX has a very large dispersion with respect to the momentum histogram, increase the scale number.

Added "H (Hull Moving Average) Signal". Hull is a extremely responsive and smooth moving average created by Alan Hull in 2005. Have option to chose between 3 Hull variations.

Added "Williams Vix Fix" signal. The Vix is one of the most reliable indicators in history for finding market bottoms. The Williams Vix Fix is simply a code from Larry Williams creating almost identical results for creating the same ability the Vix has to all assets.

The VIX has always been much better at signaling bottoms than tops. Simple reason is when market falls retail traders panic and increase volatility, and professionals come in and capitalize on the situation. At market tops there is no one panicking... just liquidity drying up.

The FE green triangles are "Filtered Entries"

The AE green triangles are "Aggressive Filtered Entries"

DynamoSent DynamoSent Pro+ — Professional Listing (Preview)

— Adaptive Macro Sentiment (v6)

— Export, Adaptive Lookback, Confidence, Boxes, Heatmap + Dynamic OB/OS

Preview / Experimental build. I’m actively refining this tool—your feedback is gold.

If you spot edge cases, want new presets, or have market-specific ideas, please comment or DM me on TradingView.

⸻

What it is

DynamoSent Pro+ is an adaptive, non-repainting macro sentiment engine that compresses VIX, DXY and a price-based activity proxy (e.g., SPX/sector ETF/your symbol) into a 0–100 sentiment line. It scales context by volatility (ATR%) and can self-calibrate with rolling quantile OB/OS. On top of that, it adds confidence scoring, a plain-English Context Coach, MTF agreement, exportable sentiment for other indicators, and a clean Light/Dark UI.

Why it’s different

• Adaptive lookback tracks regime changes: when volatility rises, we lengthen context; when it falls, we shorten—less whipsaw, more relevance.

• Dynamic OB/OS (quantiles) self-calibrates to each instrument’s distribution—no arbitrary 30/70 lines.

• MTF agreement + Confidence gate reduce false positives by highlighting alignment across timeframes.

• Exportable output: hidden plot “DynamoSent Export” can be selected as input.source in your other Pine scripts.

• Non-repainting rigor: all request.security() calls use lookahead_off + gaps_on; signals wait for bar close.

Key visuals

• Sentiment line (0–100), OB/OS zones (static or dynamic), optional TF1/TF2 overlays.

• Regime boxes (Overbought / Oversold / Neutral) that update live without repaint.

• Info Panel with confidence heat, regime, trend arrow, MTF readout, and Coach sentence.

• Session heat (Asia/EU/US) to match intraday behavior.

• Light/Dark theme switch in Inputs (auto-contrasted labels & headers).

⸻

How to use (examples & recipes)

1) EURUSD (swing / intraday blend)

• Preset: EURUSD 1H Swing

• Chart: 1H; TF1=1H, TF2=4H (default).

• Proxies: Defaults work (VIX=D, DXY=60, Proxy=D).

• Dynamic OB/OS: ON at 20/80; Confidence ≥ 55–60.

• Playbook:

• When sentiment crosses above 50 + margin with Δ ≥ signalK and MTF agreement ≥ 0.5, treat as trend breakout.

• In Oversold with rising Coach & TF agreement, take fade longs back toward mid-range.

• Alerts: Enable Breakout Long/Short and Fade; keep cooldown 8–12 bars.

2) SPY (daytrading)

• Preset: SPY 15m Daytrade; Chart: 15m.

• VIX (D) matters more; preset weights already favor it.

• Start with static 30/70; later try dynamic 25/75 for adaptive thresholds.

• Use Coach: in US session, when it says “Overbought + MTF agree → sell rallies / chase breakouts”, lean momentum-continuation after pullbacks.

3) BTCUSD (crypto, 24/7)

• Preset: BTCUSD 1H; Chart: 1H.

• DXY and BTC.D inform macro tone; keep Carry-forward ON to bridge sparse ticks.

• Prefer Dynamic OB/OS (15/85) for wider swings.

• Fade signals on weekend chop; Breakout when Confidence > 60 and MTF ≥ 1.0.

4) XAUUSD (gold, macro blend)

• Preset: XAUUSD 4H; Chart: 4H.

• Weights tilt to DXY and US10Y (handled by preset).

• Coach + MTF helps separate trend legs from news pops.

⸻

Best practices

• Theme: Switch Light/Dark in Inputs; the panel adapts contrast automatically.

• Export: In another script → Source → DynamoSent Pro+ → DynamoSent Export. Build your own filters/strategies atop the same sentiment.

• Dynamic vs Static OB/OS:

• Static 30/70: fast, universal baseline.

• Dynamic (quantiles): instrument-aware; use 20/80 (default) or 15/85 for choppy markets.

• Confidence gate: Start at 50–60% to filter noise; raise when you want only A-grade setups.

• Adaptive Lookback: Keep ON. For ultra-liquid indices, you can switch it OFF and set a fixed lookback.

⸻

Non-repainting & safety notes

• All request.security() calls use lookahead=barmerge.lookahead_off and gaps=barmerge.gaps_on.

• No forward references; signals & regime flips are confirmed on bar close.

• History-dependent funcs (ta.change, ta.percentile_linear_interpolation, etc.) are computed each bar (not conditionally).

• Adaptive lookback is clamped ≥ 1 to avoid lowest/highest errors.

• Missing-data warning triggers only when all proxies are NA for a streak; carry-forward can bridge small gaps without repaint.

⸻

Known limits & tips

• If a proxy symbol isn’t available on your plan/exchange, you’ll see the NA warning: choose a different symbol via Symbol Search, or keep Carry-forward ON (it defaults to neutral where needed).

• Intraday VIX is sparse—using Daily is intentional.

• Dynamic OB/OS needs enough history (see dynLenFloor). On short histories it gracefully falls back to static levels.

Thanks for trying the preview. Your comments drive the roadmap—presets, new proxies, extra alerts, and integrations.

Fear & Greed [theUltimator5]This indicator attempts to replicate CNN's Fear & Greed Index methodology to measure market sentiment on a scale from 0-100. It combines seven key market components into a single sentiment score, where lower values indicate fear and higher values indicate greed.

Note: It is impossible to perfectly replicate the true Fear & Greed indicator due to data limitations, so this indicator attempts to best replicate the output for each of the (7) components using available data.

The uniqueness of this indicator comes from the calculation methods for the 7 components as well as the visual representation of the data, which includes a table and selectable plots for each of the 7 components which make up the overall sentiment. Existing variants of the Fear & Greed Index have substantial flaws in the calculations of several of the components which result in warped final sentiment numbers. This indicator attempts to better track all 7 components and provide a closer model to the actual Fear & Greed index.

Here are the seven components and a brief description of how each are calculated:

1. Market Momentum

Calculation: S&P 500 current price vs. 125-day moving average

Measures how far the market has moved from its long-term trend

Uses CNN-style Z-score normalization over 252 trading days

Higher values indicate strong upward momentum (greed)

Lower values suggest declining momentum (fear)

2. Stock Strength

Calculation: S&P 500 RSI scaled to 252-day range

Uses 14-period RSI of the S&P 500 index

Normalizes RSI values based on their 252-day minimum and maximum

Measures overbought/oversold conditions relative to recent history

Higher values indicate overbought conditions (greed)

Lower values suggest oversold conditions (fear)

3. Price Breadth

Calculation: Modified McClellan Oscillator

Primary: Uses NYSE advancing vs. declining issues with 7-day smoothing

Fallback: Compares sector performance (QQQ, IWM vs. SPY)

Measures how many stocks participate in market moves

Broader participation indicates healthier trends

Narrow breadth suggests selective or weak trends

4. Put/Call Ratio

Calculation: Inverted CBOE Put/Call ratios

Primary: CBOE Equity-only Put/Call ratio (more sensitive)

Fallback: CBOE Total Put/Call ratio

Uses 5-day average and applies CNN normalization

Higher put/call ratios indicate fear (inverted to lower scores)

Lower put/call ratios suggest complacency (higher scores)

5. Market Volatility

Calculation: VIX relative to its 50-day average

Compares current VIX level to its 50-day moving average

Measures deviation from normal volatility expectations

Higher VIX relative to average indicates fear (lower scores)

Lower relative VIX suggests complacency (higher scores)

6. Safe Haven Demand

Calculation: Stock returns vs. bond yield changes

Compares 20-day smoothed S&P 500 returns to Treasury yield changes

When stocks outperform bonds, indicates risk appetite (higher scores)

When bonds outperform stocks, suggests risk aversion (lower scores)

Uses Treasury 10-year yields as the safe haven benchmark

7. Junk Bond Demand

Calculation: High-yield bond spread analysis

Measures yield spread between junk bonds (JNK ETF) and Treasuries

Compares current spread to its 5-day average

Narrowing spreads indicate risk appetite (higher scores)

Widening spreads suggest risk aversion (lower scores)

The combined sentiment is plotted as a single line which changes color based on the current sentiment value.

0-25: Extreme Fear (Red) - Market panic, oversold conditions

26-45: Fear (Orange) - Cautious sentiment, bearish bias

46-55: Neutral (Yellow) - Balanced market sentiment

56-75: Greed (Light Green) - Optimistic sentiment, bullish bias

76-100: Extreme Greed (Green) - Market euphoria, potentially overbought

There are dashed lines to represent the threshold values for each of the sentiments to better visualize transitions.

The table displays each of the (7) components of the index and their respective values. The table can be toggled on/off and the position can be moved.

An optional secondary line can be toggled on to display (1) of the (7) components as a unique color and the component name and value will highlight on the table. The secondary line can be used to dig into the main driving forces behind the overall index value.

Rolling Correlation BTC vs Hedge AssetsRolling Correlation BTC vs Hedge Assets

Overview

This indicator calculates and plots the rolling correlation between Bitcoin (BTC) returns and several key hedge assets:

• XAUUSD (Gold)

• EURUSD (proxy for DXY, U.S. Dollar Index)

• VIX (Volatility Index)

• TLT (20y U.S. Treasury Bonds ETF)

By monitoring these dynamic correlations, traders can identify whether BTC is moving in sync with risk assets or decoupling as a hedge, and adjust their trading strategy accordingly.

How it works

1. Computes returns for BTC and each asset using percentage change.

2. Uses the rolling correlation function (ta.correlation) over a configurable window length (default = 12 bars).

3. Plots each correlation as a separate colored line (Gold = Yellow, EURUSD = Blue, VIX = Red, TLT = Green).

4. Adds threshold levels at +0.3 and -0.3 to help classify correlation regimes.

How to use it

• High positive correlation (> +0.3): BTC is moving together with the asset (risk-on behavior).

• Near zero (-0.3 to +0.3): BTC is showing little to no correlation — neutral/independent moves.

• Negative correlation (< -0.3): BTC is moving in the opposite direction — potential hedge opportunity.

Practical strategies:

• Watch BTC vs VIX: a spike in volatility (VIX ↑) usually coincides with BTC selling pressure.

• Track BTC vs EURUSD: stronger USD often puts downside pressure on BTC.

• Observe BTC vs Gold: during “flight to safety” events, gold rises while BTC weakens.

• Monitor BTC vs TLT: rising yields (falling TLT) often align with BTC weakness.

Inputs

• Window Length (bars): Number of bars used to calculate rolling correlations (default = 12).

• Comparison Timeframe: Default = 5m. Can be changed to align with your intraday or swing trading style.

Notes

• Works best on intraday charts (1m, 5m, 15m) for scalping and short-term setups.

• Use correlations as context, not standalone signals — combine with volume, VWAP, and price action.

• Correlations are dynamic; they can switch regimes quickly during macro events (CPI, NFP, FOMC).

This tool is designed for traders who want to manage risk exposure by monitoring whether BTC is behaving as a risk-on asset or hedge, and to exploit opportunities during decoupling phases.

Dynamic 5DMA/EMA with Color for Multiple Products🔹 Dynamic 5DMA/EMA with Slope-Based Coloring (All Timeframes)

This indicator plots a dynamic 5-period moving average that adapts intelligently to your chart's timeframe and product type — giving you a clean, slope-sensitive visual edge across intraday, daily, and weekly views.

✅ Key Features:

📈 Dynamic MA Length Scaling:

On intraday timeframes, the MA adjusts for your selected market session (RTH, ETH, VIX, or Futures), calculating a true 5-day average based on actual session length — not just a flat bar count.

🔄 Automatic Timeframe Detection:

Daily Chart: Uses standard 5DMA or 5EMA.

Weekly Chart: Applies a true 5-week MA.

Intraday Charts: Converts 5 days into bar-length equivalent dynamically.

🎨 Color-Coded Slope Logic:

Green = Rising MA (bullish slope)

Red = Falling MA (bearish slope)

Neutral slope = previous color held for visual continuity

No more guessing — direction is instantly clear.

⚠️ Built-In Slope Flip Alerts:

Set alerts when the slope of the MA turns up or down. Ideal for timing pullback entries or exits across any product.

⚙️ Session Settings for Proper Scaling:

Choose your product's market structure to ensure accurate 5-day conversion on intraday charts:

Stocks - RTH: 390 mins/day

Stocks - ETH: 780 mins/day

VIX: 855 mins/day

Futures: 1440 mins/day

This ensures the MA reflects 5 full trading days, regardless of session irregularities or bar interval.

📌 Why Use This Indicator?

Most MAs misrepresent trend direction on intraday charts because they assume static daily bar counts. This tool corrects that, then adds slope-based coloring to give you a fast, visual read on short-term momentum. Whether you’re swing trading SPY, scalping VIX, or position trading futures, this indicator keeps your view aligned with how institutions see moving averages across timeframes.

🔧 Best For:

VIX & volatility traders

Short-term SPY/SPX traders

Swing traders who value clean setups

Anyone wanting a true 5-day trend anchor on any chart