Volume Profile (Simple)Simple Volume Profile (Simple)

Master the Market's Structure with a Clear View of Volume

by mercaderoaurum

The Simple Volume Profile (Simple) indicator removes the guesswork by showing you exactly where the most significant trading activity has occurred. By visualizing the Point of Control (POC) and Value Area (VA) for today and yesterday, you can instantly identify the price levels that matter most, giving you a critical edge in your intraday trading.

This tool is specifically optimized for day trading SPY on a 1-minute chart, but it's fully customizable for any symbol or timeframe.

Key Features

Multi-Day Analysis: Automatically plots the volume profiles for the current and previous trading sessions, allowing you to see how today's market is reacting to yesterday's key levels.

Automatic Key Level Plotting: Instantly see the most important levels from each session:

Point of Control (POC): The single price level with the highest traded volume, acting as a powerful magnet for price.

Value Area High (VAH): The upper boundary of the area where 50% of the volume was traded. It often acts as resistance.

Value Area Low (VAL): The lower boundary of the 50% value area, often acting as support.

Extended Levels: The POC, VAH, and VAL from previous sessions are automatically extended into the current day, providing a clear map of potential support and resistance zones.

Customizable Sessions: While optimized for the US stock market, you can define any session time and time zone, making it a versatile tool for forex, crypto, and futures traders.

Core Trading Strategies

The Simple Volume Profile helps you understand market context. Instead of trading blind, you can now make decisions based on where the market has shown the most interest.

1. Identifying Support and Resistance

This is the most direct way to use the indicator. The extended lines from the previous day are your roadmap for the current session.

Previous Day's POC (pPOC): This is the most significant level. Watch for price to react strongly here. It can act as powerful support if approached from above or strong resistance if approached from below.

Previous Day's VAH (pVAH): Expect this level to act as initial resistance. A clean break above pVAH can signal a strong bullish trend.

Previous Day's VAL (pVAL): Expect this level to act as initial support. A firm break below pVAL can indicate a strong bearish trend.

Example Strategy: If SPY opens and rallies up to the previous day's VAH and stalls, this is a high-probability area to look for a short entry, with a stop loss just above the level.

2. The "Open-Drive" Rejection

How the market opens in relation to the previous day's value area is a powerful tell.

Open Above Yesterday's Value Area: If the market opens above the pVAH, it signals strength. The first pullback to test the pVAH is often a key long entry point. The level is expected to flip from resistance to support.

Open Below Yesterday's Value Area: If the market opens below the pVAL, it signals weakness. The first rally to test the pVAL is a potential short entry, as the level is likely to act as new resistance.

3. Fading the Extremes

When price pushes far outside the previous day's value area, it can become overextended.

Reversal at Highs: If price rallies significantly above the pVAH and then starts to lose momentum (e.g., forming bearish divergence on RSI or a topping pattern), it could be an opportunity to short the market, targeting a move back toward the pVAH or pPOC.

Reversal at Lows: Conversely, if price drops far below the pVAL and shows signs of bottoming, it can be a good opportunity to look for a long entry, targeting a reversion back to the value area.

Recommended Settings (SPY Intraday)

These settings are the default and are optimized for scalping or day trading SPY on a 1-minute chart.

Value Area (%): 50%. This creates a tighter, more sensitive value area, perfect for identifying the most critical intraday zones.

Number of Rows: 1000. This high resolution is essential for a low-volatility instrument like SPY, ensuring that the profile is detailed and the levels are precise.

Session Time: 0400-1800 in America/New_York. This captures the full pre-market and core session, which is crucial for understanding the day's complete volume story.

Ready to trade with an edge? Add the Simple Volume Profile (Multi-Day) to your chart now and see the market in a new light!

스크립트에서 "session"에 대해 찾기

Time-Based VWAP (TVWAP)(TVWAP) Indicator

The Time-Based Volume Weighted Average Price (TVWAP) indicator is a customized version of VWAP designed for intraday trading sessions with defined start and end times. Unlike the traditional VWAP, which calculates the volume-weighted average price over an entire trading day, this indicator allows you to focus on specific time periods, such as ICT kill zones (e.g., London Open, New York Open, Power Hour). It helps crypto scalpers and advanced traders identify price deviations relative to volume during key trading windows.

Key Features:

Custom Time Interval:

You can set the exact start and end times for the VWAP calculation using input settings for hours and minutes (24-hour format).

Ideal for analyzing short, high-liquidity periods.

Dynamic Accumulation of Price and Volume:

The indicator resets at the beginning of the specified session and accumulates price-volume data until the end of the session.

Ensures that the TVWAP reflects the weighted average price specific to the chosen session.

Visual Representation:

The indicator plots the TVWAP line only during the specified time window, providing a clear visual reference for price action during that period.

Outside the session, the TVWAP line is hidden (na).

Use Cases:

ICT Scalp Trading:

Monitor price rebalances or potential liquidity sweeps near TVWAP during important trading sessions.

Mean Reversion Strategies:

Detect pullbacks toward the session’s average price for potential entry points.

Breakout Confirmation:

Confirm price direction relative to TVWAP during kill zones or high-volume times to determine if a breakout is supported by volume.

Inputs:

Start Hour/Minute: The time when the TVWAP calculation starts.

End Hour/Minute: The time when the TVWAP calculation ends.

Technical Explanation:

The indicator uses the timestamp function to create time markers for the session start and end.

During the session, the price-volume (close * volume) is accumulated along with the total volume.

TVWAP is calculated as:

TVWAP = (Sum of (Price × Volume)) ÷ (Sum of Volume)

Once the session ends, the TVWAP resets for the next trading period.

Customization Ideas:

Alerts: Add notifications when the price touches or deviates significantly from TVWAP.

Different Colors: Use different line colors based on upward or downward trends.

Multiple Sessions: Add support for multiple TVWAP lines for different time periods (e.g., London + New York).

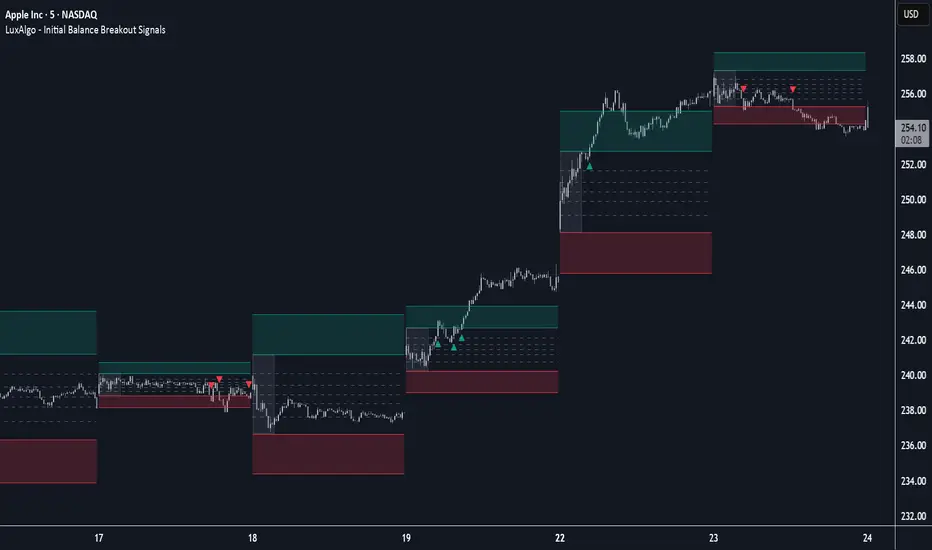

Initial Balance Breakout Signals [LuxAlgo]The Initial Balance Breakout Signals help traders identify breakouts of the Initial Balance (IB) range.

The indicator includes automatic detection of IB or can use custom sessions, highlights top and bottom IB extensions, custom Fibonacci levels, and goes further with an IB forecast with two different modes.

🔶 USAGE

The initial balance is the price range made within the first hour of the trading session. It is an intraday concept based on the idea that high volume and volatility enter the market through institutional trading at the start of the session, setting the tone for the rest of the day.

The initial balance is useful for gauging market sentiment, or, in other words, the relationship between buyers and sellers.

Bullish sentiment: Price trades above the IB range.

Mixed sentiment: Price trades within the IB range.

Bearish sentiment: Price trades below the IB range.

The initial balance high and low are important levels that many traders use to gauge sentiment. There are two main ideas behind trading around the IB range.

IB Extreme Breakout: When the price breaks and holds the IB high or low, there is a high probability that the price will continue in that direction.

IB Extreme Rejection: When the price tries to break those levels but fails, there is a high probability that it will reach the opposite IB extreme.

This indicator is a complete Initial Balance toolset with custom sessions, breakout signals, IB extensions, Fibonacci retracements, and an IB forecast. All of these features will be explained in the following sections.

🔹 Custom Sessions and Signals

By default, sessions for Initial Balance and breakout signals are in Auto mode. This means that Initial Balance takes the first hour of the trading session and shows breakout signals for the rest of the session.

With this option, traders can use the tool for open range trading, making it highly versatile. The concept behind open range (OR) is the same as that of initial balance (IB), but in OR, the range is determined by the first minute, three or five minutes, or up to the first 30 minutes of the trading session.

As shown in the image above, the top chart uses the Auto feature for the IB and Breakouts sessions. The bottom chart has the Auto feature disabled to use custom sessions for both parameters. In this case, the first three minutes of the trading session are used, turning the tool into an Open Range trading indicator.

This chart shows another example of using custom sessions to display overnight NASDAQ futures sessions.

The left chart shows a custom session from the Tokyo open to the London open, and the right chart shows a custom session from the London open to the New York open.

The chart shows both the Asian and European sessions, their top and bottom extremes, and the breakout signals from those extremes.

🔹 Initial Balance Extensions

Traders can easily extend both extremes of the Initial Balance to display their preferred targets for breakouts. Enable or disable any of them and set the IB percentage to use for the extension.

As the chart shows, the percentage selected on the settings panel directly affects the displayed levels.

Setting 25 means the tool will use a quarter of the detected initial balance range for extensions beyond the IB extremes. Setting 100 means the full IB range will be used.

Traders can use these extensions as targets for breakout signals.

🔹 Fibonacci Levels

Traders can display default or custom Fibonacci levels on the IB range to trade retracements and assess the strength of market movements. Each level can be enabled or disabled and customized by level, color, and line style.

As we can see on the chart, after the IB was completed, prices were unable to fall below the 0.236 Fibonacci level. This indicates significant bullish pressure, so it is expected that prices will rise.

Traders can use these levels as guidelines to assess the strength of the side trying to penetrate the IB. In this case, the sellers were unable to move the market beyond the first level.

🔹 Initial Balance Forecast

The tool features two different forecasting methods for the current IB. By default, it takes the average of the last ten values and applies a multiplier of one.

IB Against Previous Open: averages the difference between IB extremes and the open of the previous session.

Filter by current day of the week: averages the difference between IB extremes and the open of the current session for the same day of the week.

This feature allows traders to see the difference between the current IB and the average of the last IBs. It makes it very easy to interpret: if the current IB is higher than the average, buyers are in control; if it is lower than the average, sellers are in control.

For example, on the left side of the chart, we can see that the last day was very bullish because the IB was completely above the forecasted value. This is the IB mean of the last ten trading days.

On the right, we can see that on Monday, September 15, the IB traded slightly higher but within the forecasted value of the IB mean of the last ten Mondays. In this case, it is within expectations.

🔶 SETTINGS

Display Last X IBs: Select how many IBs to display.

Initial Balance: Choose a custom session or enable the Auto feature.

Breakouts: Enable or disable breakouts. Choose custom session or enable the Auto feature.

🔹 Extensions

Top Extension: Enable or disable the top extension and choose the percentage of IB to use.

Bottom extension: Enable or disable the bottom extension and choose the percentage of IB to use.

🔹 Fibonacci Levels

Display Fibonacci: Enable or disable Fibonacci levels.

Reverse: Reverse Fibonacci levels.

Levels, Colors & Style

Display Labels: Enable or disable labels and choose text size.

🔹 Forecast

Display Forecast: Select the forecast method.

- IB Against Previous Open: Calculates the average difference between the IB high and low and the previous day's IB open price.

- Filter by Current Day of Week: Calculates the average difference between the IB high and low and the IB open price for the same day of the week.

Forecast Memory: The number of data points used to calculate the average.

Forecast Multiplier: This multiplier will be applied to the average. Bigger numbers will result in wider predicted ranges.

Forecast Colors: Choose from a variety of colors.

Forecast Style: Choose a line style.

🔹 Style

Initial Balance Colors

Extension Transparency: Choose the extension's transparency. 0 is solid, and 100 is fully transparent.

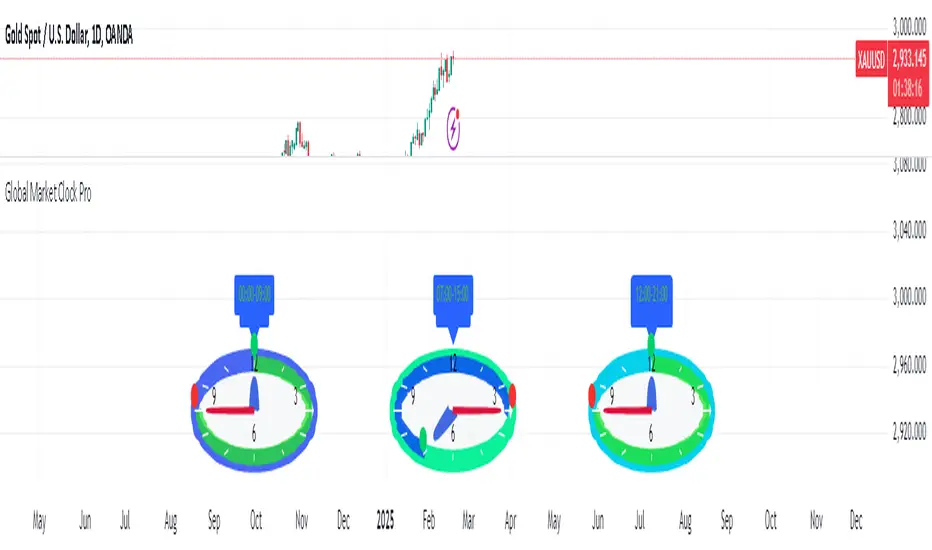

Global Market Clock Pro🌍✨ Global Market Clock Pro is a market session visualizer that combines utility and fun on your charts! 📊⏰ This indicator includes three analog clocks representing the Tokyo, London, and New York sessions, added in an entertaining way to make analysis more enjoyable and dynamic. 😊 Each clock clearly shows the session start and end times through arcs and distinctive markers, making it easier to identify active market periods. 💡

Also, a statistics table is added offering detailed information for each session:

📊 Percentage Change : Displays the price variation between sessions.

💰 Price Range : Highlights volatility within each session.

📈 Session Volume : Evaluates market activity based on traded volume.

📊 Average Volatility : Helps measure price fluctuations over time.

📌 Mean (Average Close) : Calculated by dividing the sum of closing prices of each bar by the total number of bars recorded during the session. This value gives you a reference for average price behavior, helping you detect general trends and key support/resistance levels. 📉

📌 Max Range (Maximum Range) : Represents the largest difference recorded between the highest and lowest prices during the session. This indicator is crucial for identifying volatility peaks, as it shows how far the market moved during its most active moments. 🔥

⚠️ VERY IMPORTANT : This tool works best only in timeframes under 4 hours ! ⏳

By integrating these data points directly into your chart, this indicator becomes a powerful tool to align your strategies with market activity in each session. Whether you're a day trader or a long-term investor, Global Market Clock Pro provides clear, data-driven insights to enhance decision-making. 💻📈

Español:

🌍✨ Global Market Clock Pro es un visualizador de sesiones de mercado que combina utilidad y diversión en tus gráficos. 📊⏰ Este indicador incluye tres relojes analógicos que representan las sesiones de Tokio, Londres y Nueva York, agregados de manera entretenida para hacer el análisis más ameno y dinámico. 😊 Cada reloj muestra con claridad los horarios de inicio y cierre de sesión mediante arcos y marcadores distintivos, facilitando la identificación de los periodos activos del mercado. 💡

Además, se añade una tabla de estadísticas que ofrece información detallada de cada sesión:

📊 Cambio porcentual : Muestra la variación de precio entre sesiones.

💰 Rango de precios : Destaca la volatilidad dentro de cada sesión.

📈 Volumen de sesión : Evalúa la actividad del mercado mediante el volumen negociado.

📊 Volatilidad promedio : Ayuda a medir las fluctuaciones del precio a lo largo del tiempo.

📌 Mean (Promedio de Cierre) : Se calcula dividiendo la suma de los precios de cierre de cada barra entre el número total de barras registradas durante la sesión. Este valor te brinda una referencia del comportamiento medio del precio, permitiéndote detectar tendencias generales y niveles clave de soporte o resistencia. 📉

📌 Max Range (Rango Máximo) : Representa la mayor diferencia registrada entre el precio más alto y el más bajo durante la sesión. Este indicador es fundamental para identificar los picos de volatilidad, ya que muestra hasta qué punto el mercado se movió en sus momentos de mayor actividad. 🔥

⚠️ ¡MUY IMPORTANTE! : Esta herramienta funciona mejor solo en temporalidades menores a 4 horas . ⏳

Al integrar estos datos directamente en el gráfico, este indicador se convierte en una herramienta poderosa para sincronizar tus estrategias con la actividad del mercado en cada sesión. Ya seas un trader intradía o un inversor a largo plazo, Global Market Clock Pro proporciona claridad basada en datos para mejorar la toma de decisiones. 💻📈

🚀 ¡No dejes pasar la oportunidad de optimizar tu experiencia de trading con esta innovadora herramienta! ✨

Advanced Time Dividers & Killzones IndicatorOverview

A comprehensive Pine Script v6 indicator that displays customizable time period dividers and trading session killzones on your chart. Perfect for intraday traders who need clear visual separation of time periods and want to identify key trading sessions.

✨ Features

Time Period Dividers

Weekly Lines: Vertical lines marking the start of each week

Monthly Lines: Vertical lines marking the start of each month

Quarterly Lines: Vertical lines marking the start of each quarter (Q1, Q2, Q3, Q4)

Yearly Lines: Vertical lines marking the start of each year

Trading Session Killzones

London Session: 2:00-5:00 GMT (Blue shaded box)

New York Session: 7:00-10:00 GMT (Green shaded box)

London Close: 10:00-12:00 GMT (Orange shaded box)

Asia Session: 20:00-00:00 GMT (Pink shaded box)

🎨 Customization Options

Display Controls

Toggle each time divider type individually

Toggle each killzone individually

Adjust historical and future display range

Show/hide labels on dividers and killzones

Style Customization

Line Styles: Choose between Solid, Dashed, or Dotted lines

Line Width: Adjustable from 1 to 5 pixels

Colors: Fully customizable colors for each element with transparency control

Label Size: Choose from Tiny, Small, Normal, or Large

Period Settings

Control how many bars to display in the past (0-5000)

Control how many bars to display in the future (0-1000)

📋 Usage Instructions

Add to Chart: Add the indicator to any chart

Select Timeframe: Works best on intraday timeframes (1H, 15min, 5min) for killzones

Customize: Open settings to enable/disable features and customize colors

Trading: Use the dividers to identify time periods and killzones to spot high-liquidity sessions

💡 Trading Applications

Time Dividers

Weekly/Monthly Analysis: Identify major time period transitions

Market Structure: Analyze how price behaves at period boundaries

Event Correlation: Align with economic calendar events

Killzones

High Liquidity Periods: Trade during peak market activity

ICT Strategy: Follows Inner Circle Trader killzone concepts

Session-Based Trading: Focus on specific trading sessions

Volatility Windows: Identify when major moves typically occur

⚙️ Technical Details

Version: Pine Script v6

Type: Overlay indicator

Max Lines: 500 (optimized performance)

Max Boxes: 500 (for killzone visualization)

Timezone: GMT/UTC for killzones

Memory Efficient: Automatic cleanup of old objects

🎯 Best Practices

Combine with Price Action: Use dividers to frame your analysis

Focus on Killzones: Most significant price moves occur during these sessions

Adjust Transparency: Find the right balance between visibility and chart clarity

Use Labels Wisely: Toggle labels on/off based on your needs

Timeframe Selection: Use lower timeframes (≤1H) to see killzones clearly

📝 Notes

Killzone times are in GMT/UTC timezone

Works on all instruments (Forex, Crypto, Stocks, Futures)

Optimized for performance with automatic memory management

Fully compatible with other indicators

🔄 Updates & Support

This indicator is actively maintained. Feel free to suggest improvements or report issues in the comments.

JK_Traders_Reality_LibLibrary "JK_Traders_Reality_Lib"

This library contains common elements used in Traders Reality scripts

calcPvsra(pvsraVolume, pvsraHigh, pvsraLow, pvsraClose, pvsraOpen, redVectorColor, greenVectorColor, violetVectorColor, blueVectorColor, darkGreyCandleColor, lightGrayCandleColor)

calculate the pvsra candle color and return the color as well as an alert if a vector candle has apperared.

Situation "Climax"

Bars with volume >= 200% of the average volume of the 10 previous chart TFs, or bars

where the product of candle spread x candle volume is >= the highest for the 10 previous

chart time TFs.

Default Colors: Bull bars are green and bear bars are red.

Situation "Volume Rising Above Average"

Bars with volume >= 150% of the average volume of the 10 previous chart TFs.

Default Colors: Bull bars are blue and bear are violet.

Parameters:

pvsraVolume (float) : the instrument volume series (obtained from request.sequrity)

pvsraHigh (float) : the instrument high series (obtained from request.sequrity)

pvsraLow (float) : the instrument low series (obtained from request.sequrity)

pvsraClose (float) : the instrument close series (obtained from request.sequrity)

pvsraOpen (float) : the instrument open series (obtained from request.sequrity)

redVectorColor (simple color) : red vector candle color

greenVectorColor (simple color) : green vector candle color

violetVectorColor (simple color) : violet/pink vector candle color

blueVectorColor (simple color) : blue vector candle color

darkGreyCandleColor (simple color) : regular volume candle down candle color - not a vector

lightGrayCandleColor (simple color) : regular volume candle up candle color - not a vector

@return

adr(length, barsBack)

Parameters:

length (simple int) : how many elements of the series to calculate on

barsBack (simple int) : starting possition for the length calculation - current bar or some other value eg last bar

@return adr the adr for the specified lenght

adrHigh(adr, fromDo)

Calculate the ADR high given an ADR

Parameters:

adr (float) : the adr

fromDo (simple bool) : boolean flag, if false calculate traditional adr from high low of today, if true calcualte from exchange midnight

@return adrHigh the position of the adr high in price

adrLow(adr, fromDo)

Parameters:

adr (float) : the adr

fromDo (simple bool) : boolean flag, if false calculate traditional adr from high low of today, if true calcualte from exchange midnight

@return adrLow the position of the adr low in price

splitSessionString(sessXTime)

given a session in the format 0000-0100:23456 split out the hours and minutes

Parameters:

sessXTime (simple string) : the session time string usually in the format 0000-0100:23456

@return

calcSessionStartEnd(sessXTime, gmt)

calculate the start and end timestamps of the session

Parameters:

sessXTime (simple string) : the session time string usually in the format 0000-0100:23456

gmt (simple string) : the gmt offset string usually in the format GMT+1 or GMT+2 etc

@return

drawOpenRange(sessXTime, sessXcol, showOrX, gmt)

draw open range for a session

Parameters:

sessXTime (simple string) : session string in the format 0000-0100:23456

sessXcol (simple color) : the color to be used for the opening range box shading

showOrX (simple bool) : boolean flag to toggle displaying the opening range

gmt (simple string) : the gmt offset string usually in the format GMT+1 or GMT+2 etc

@return void

drawSessionHiLo(sessXTime, showRectangleX, showLabelX, sessXcolLabel, sessXLabel, gmt, sessionLineStyle)

Parameters:

sessXTime (simple string) : session string in the format 0000-0100:23456

showRectangleX (simple bool)

showLabelX (simple bool)

sessXcolLabel (simple color) : the color to be used for the hi/low lines and label

sessXLabel (simple string) : the session label text

gmt (simple string) : the gmt offset string usually in the format GMT+1 or GMT+2 etc

sessionLineStyle (simple string) : the line stile for the session high low lines

@return void

calcDst()

calculate market session dst on/off flags

@return indicating if DST is on or off for a particular region

timestampPreviousDayOfWeek(previousDayOfWeek, hourOfDay, gmtOffset, oneWeekMillis)

Timestamp any of the 6 previous days in the week (such as last Wednesday at 21 hours GMT)

Parameters:

previousDayOfWeek (simple string) : Monday or Satruday

hourOfDay (simple int) : the hour of the day when psy calc is to start

gmtOffset (simple string) : the gmt offset string usually in the format GMT+1 or GMT+2 etc

oneWeekMillis (simple int) : the amount if time for a week in milliseconds

@return the timestamp of the psy level calculation start time

getdayOpen()

get the daily open - basically exchange midnight

@return the daily open value which is float price

newBar(res)

new_bar: check if we're on a new bar within the session in a given resolution

Parameters:

res (simple string) : the desired resolution

@return true/false is a new bar for the session has started

toPips(val)

to_pips Convert value to pips

Parameters:

val (float) : the value to convert to pips

@return the value in pips

rLabel(ry, rtext, rstyle, rcolor, valid, labelXOffset)

a function that draws a right aligned lable for a series during the current bar

Parameters:

ry (float) : series float the y coordinate of the lable

rtext (simple string) : the text of the label

rstyle (simple string) : the style for the lable

rcolor (simple color) : the color for the label

valid (simple bool) : a boolean flag that allows for turning on or off a lable

labelXOffset (int) : how much to offset the label from the current position

rLabelOffset(ry, rtext, rstyle, rcolor, valid, labelOffset)

a function that draws a right aligned lable for a series during the current bar

Parameters:

ry (float) : series float the y coordinate of the lable

rtext (string) : the text of the label

rstyle (simple string) : the style for the lable

rcolor (simple color) : the color for the label

valid (simple bool) : a boolean flag that allows for turning on or off a lable

labelOffset (int)

rLabelLastBar(ry, rtext, rstyle, rcolor, valid, labelXOffset)

a function that draws a right aligned lable for a series only on the last bar

Parameters:

ry (float) : series float the y coordinate of the lable

rtext (string) : the text of the label

rstyle (simple string) : the style for the lable

rcolor (simple color) : the color for the label

valid (simple bool) : a boolean flag that allows for turning on or off a lable

labelXOffset (int) : how much to offset the label from the current position

drawLine(xSeries, res, tag, xColor, xStyle, xWidth, xExtend, isLabelValid, xLabelOffset, validTimeFrame)

a function that draws a line and a label for a series

Parameters:

xSeries (float) : series float the y coordinate of the line/label

res (simple string) : the desired resolution controlling when a new line will start

tag (simple string) : the text for the lable

xColor (simple color) : the color for the label

xStyle (simple string) : the style for the line

xWidth (simple int) : the width of the line

xExtend (simple string) : extend the line

isLabelValid (simple bool) : a boolean flag that allows for turning on or off a label

xLabelOffset (int)

validTimeFrame (simple bool) : a boolean flag that allows for turning on or off a line drawn

drawLineDO(xSeries, res, tag, xColor, xStyle, xWidth, xExtend, isLabelValid, xLabelOffset, validTimeFrame)

a function that draws a line and a label for the daily open series

Parameters:

xSeries (float) : series float the y coordinate of the line/label

res (simple string) : the desired resolution controlling when a new line will start

tag (simple string) : the text for the lable

xColor (simple color) : the color for the label

xStyle (simple string) : the style for the line

xWidth (simple int) : the width of the line

xExtend (simple string) : extend the line

isLabelValid (simple bool) : a boolean flag that allows for turning on or off a label

xLabelOffset (int)

validTimeFrame (simple bool) : a boolean flag that allows for turning on or off a line drawn

drawPivot(pivotLevel, res, tag, pivotColor, pivotLabelColor, pivotStyle, pivotWidth, pivotExtend, isLabelValid, validTimeFrame, levelStart, pivotLabelXOffset)

draw a pivot line - the line starts one day into the past

Parameters:

pivotLevel (float) : series of the pivot point

res (simple string) : the desired resolution

tag (simple string) : the text to appear

pivotColor (simple color) : the color of the line

pivotLabelColor (simple color) : the color of the label

pivotStyle (simple string) : the line style

pivotWidth (simple int) : the line width

pivotExtend (simple string) : extend the line

isLabelValid (simple bool) : boolean param allows to turn label on and off

validTimeFrame (simple bool) : only draw the line and label at a valid timeframe

levelStart (int) : basically when to start drawing the levels

pivotLabelXOffset (int) : how much to offset the label from its current postion

@return the pivot line series

getPvsraFlagByColor(pvsraColor, redVectorColor, greenVectorColor, violetVectorColor, blueVectorColor, lightGrayCandleColor)

convert the pvsra color to an internal code

Parameters:

pvsraColor (color) : the calculated pvsra color

redVectorColor (simple color) : the user defined red vector color

greenVectorColor (simple color) : the user defined green vector color

violetVectorColor (simple color) : the user defined violet vector color

blueVectorColor (simple color) : the user defined blue vector color

lightGrayCandleColor (simple color) : the user defined regular up candle color

@return pvsra internal code

updateZones(pvsra, direction, boxArr, maxlevels, pvsraHigh, pvsraLow, pvsraOpen, pvsraClose, transperancy, zoneupdatetype, zonecolor, zonetype, borderwidth, coloroverride, redVectorColor, greenVectorColor, violetVectorColor, blueVectorColor)

a function that draws the unrecovered vector candle zones

Parameters:

pvsra (int) : internal code

direction (simple int) : above or below the current pa

boxArr (array) : the array containing the boxes that need to be updated

maxlevels (simple int) : the maximum number of boxes to draw

pvsraHigh (float) : the pvsra high value series

pvsraLow (float) : the pvsra low value series

pvsraOpen (float) : the pvsra open value series

pvsraClose (float) : the pvsra close value series

transperancy (simple int) : the transparencfy of the vecor candle zones

zoneupdatetype (simple string) : the zone update type

zonecolor (simple color) : the zone color if overriden

zonetype (simple string) : the zone type

borderwidth (simple int) : the width of the border

coloroverride (simple bool) : if the color overriden

redVectorColor (simple color) : the user defined red vector color

greenVectorColor (simple color) : the user defined green vector color

violetVectorColor (simple color) : the user defined violet vector color

blueVectorColor (simple color) : the user defined blue vector color

cleanarr(arr)

clean an array from na values

Parameters:

arr (array) : the array to clean

@return if the array was cleaned

calcPsyLevels(oneWeekMillis, showPsylevels, psyType, sydDST)

calculate the psy levels

4 hour res based on how mt4 does it

mt4 code

int Li_4 = iBarShift(NULL, PERIOD_H4, iTime(NULL, PERIOD_W1, Li_0)) - 2 - Offset;

ObjectCreate("PsychHi", OBJ_TREND, 0, Time , iHigh(NULL, PERIOD_H4, iHighest(NULL, PERIOD_H4, MODE_HIGH, 2, Li_4)), iTime(NULL, PERIOD_W1, 0), iHigh(NULL, PERIOD_H4,

iHighest(NULL, PERIOD_H4, MODE_HIGH, 2, Li_4)));

so basically because the session is 8 hours and we are looking at a 4 hour resolution we only need to take the highest high an lowest low of 2 bars

we use the gmt offset to adjust the 0000-0800 session to Sydney open which is at 2100 during dst and at 2200 otherwize. (dst - spring foward, fall back)

keep in mind sydney is in the souther hemisphere so dst is oposite of when london and new york go into dst

Parameters:

oneWeekMillis (simple int) : a constant value

showPsylevels (simple bool) : should psy levels be calculated

psyType (simple string) : the type of Psylevels - crypto or forex

sydDST (bool) : is Sydney in DST

@return

adrHiLo(length, barsBack, fromDO)

Parameters:

length (simple int) : how many elements of the series to calculate on

barsBack (simple int) : starting possition for the length calculation - current bar or some other value eg last bar

fromDO (simple bool) : boolean flag, if false calculate traditional adr from high low of today, if true calcualte from exchange midnight

@return adr, adrLow and adrHigh - the adr, the position of the adr High and adr Low with respect to price

drawSessionHiloLite(sessXTime, showRectangleX, showLabelX, sessXcolLabel, sessXLabel, gmt, sessionLineStyle, sessXcol)

Parameters:

sessXTime (simple string) : session string in the format 0000-0100:23456

showRectangleX (simple bool)

showLabelX (simple bool)

sessXcolLabel (simple color) : the color to be used for the hi/low lines and label

sessXLabel (simple string) : the session label text

gmt (simple string) : the gmt offset string usually in the format GMT+1 or GMT+2 etc

sessionLineStyle (simple string) : the line stile for the session high low lines

sessXcol (simple color) : - the color for the box color that will color the session

@return void

msToHmsString(ms)

converts milliseconds into an hh:mm string. For example, 61000 ms to '0:01:01'

Parameters:

ms (int) : - the milliseconds to convert to hh:mm

@return string - the converted hh:mm string

countdownString(openToday, closeToday, showMarketsWeekends, oneDay)

that calculates how much time is left until the next session taking the session start and end times into account. Note this function does not work on intraday sessions.

Parameters:

openToday (int) : - timestamps of when the session opens in general - note its a series because the timestamp was created using the dst flag which is a series itself thus producing a timestamp series

closeToday (int) : - timestamp of when the session closes in general - note its a series because the timestamp was created using the dst flag which is a series itself thus producing a timestamp series

@return a countdown of when next the session opens or 'Open' if the session is open now

showMarketsWeekends (simple bool)

oneDay (simple int)

countdownStringSyd(sydOpenToday, sydCloseToday, showMarketsWeekends, oneDay)

that calculates how much time is left until the next session taking the session start and end times into account. special case of intraday sessions like sydney

Parameters:

sydOpenToday (int)

sydCloseToday (int)

showMarketsWeekends (simple bool)

oneDay (simple int)

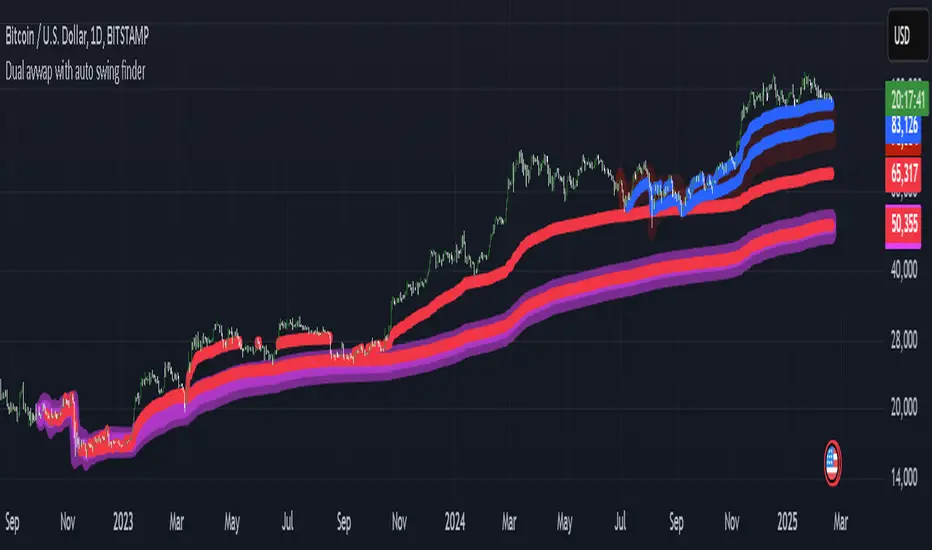

My auto dual avwap with Auto swing low/pivot low finderWelcome to My Auto Dual AVWAP with Auto Swing Low/Pivot Low Finder – an open-source TradingView indicator designed to enhance your technical analysis toolbox. This indicator is published under the Mozilla Public License 2.0 and is available for anyone to study, modify, and distribute.

Key Features

Auto Pivot/Swing Low Finder:

In addition to VWAP lines, the indicator incorporates an automatic detection mechanism for swing lows/pivot lows. This feature assists in identifying potential support areas and price reversals, further enhancing your trading strategy.

Dual VWAP Calculation with high/low range:

The indicator calculates two separate volume-weighted average price (VWAP) lines based on different price inputs (low and high prices) and defined time sessions. This allows traders to gain a more nuanced view of market activity during specific trading periods.

Customizable Time Sessions:

You can specify distinct start and end times for each VWAP calculation session. This flexibility helps you align the indicator with your preferred trading hours or market sessions, making it adaptable to various time zones and trading styles.

Easy to Customize:

With clear code structure and detailed comments, the script is designed to be accessible even for traders who want to customize or extend its functionality. Whether you're a seasoned coder or just starting out, the code is written with transparency in mind.

How It Works

Session Initialization:

The script sets up two distinct time sessions using user-defined start and end times. For each session, it detects the beginning of the trading period to reset cumulative values.

Cumulative Calculations:

During each session, the indicator accumulates the product of price and volume as well as the total volume. The VWAP is then computed as the ratio of these cumulative values.

Dual Data Sources:

Two separate data inputs (using low and high prices) are used to calculate two VWAP lines. This dual approach provides a broader perspective on market trends and can help in identifying dynamic support and resistance levels.

Visualization:

The calculated VWAP lines are plotted directly on your chart with distinct colors and thickness settings for easy visualization. This makes it simple to interpret the data at a glance.

Why Use This Indicator?

Whether you are a day trader, swing trader, or simply looking to refine your market analysis, My Auto Dual AVWAP with Auto Swing Low/Pivot Low Finder offers a robust set of features that can help you identify key price levels and improve your decision-making process. Its open-source nature invites collaboration and customization, ensuring that you can tailor it to fit your unique trading style.

Feel free to explore, modify, and share this indicator. Happy trading!

Overnight High/LowThe script identifies the Overnight High (the highest price) and Overnight Low (the lowest price) for a trading instrument during a specified overnight session. It then plots these levels on the chart for reference in subsequent trading sessions.

Key Features:

Time Settings:

The script defines the start (startHour) and end (endHour + endMinute) times for the overnight session.

The session spans across two calendar days, such as 5:00 PM (17:00) to 9:30 AM (09:30).

Tracking High and Low:

During the overnight session, the script dynamically tracks:

Overnight High: The highest price reached during the session.

Overnight Low: The lowest price reached during the session.

Reset Mechanism:

After the overnight session ends (at the specified end time), the script resets the overnightHigh and overnightLow variables, preparing for the next session.

Visual Representation:

The script uses horizontal dotted lines to plot:

A green line for the Overnight High.

A red line for the Overnight Low.

These lines extend to the right of the chart, providing visual reference points for traders.

How It Works:

Session Detection:

The script checks whether the current time falls within the overnight session:

If the hour is greater than or equal to the start hour (e.g., 17:00).

Or if the hour is less than or equal to the end hour (e.g., 09:30), considering the next day.

The end minute (e.g., 30 minutes past the hour) is also considered for precision.

High and Low Calculation:

During the overnight session:

If the overnightHigh is not yet defined, it initializes with the current candle's high.

If already defined, it updates by comparing the current candle's high to the existing overnightHigh using the math.max function.

Similarly, overnightLow is initialized or updated using the math.min function.

Post-Session Reset:

After the session ends, the script clears the overnightHigh and overnightLow variables by setting them to na (not available).

Line Drawing:

The script draws horizontal dotted lines for the Overnight High and Low during and after the session.

The lines extend indefinitely to the right of the chart.

Benefits:

Visual Aid: Helps traders quickly identify overnight support and resistance levels, which are critical for intraday trading.

Automation: Removes the need for manually plotting these levels each day.

Customizable: Time settings can be adjusted to match different markets or trading strategies.

This script is ideal for traders who use the overnight range as part of their analysis for breakouts, reversals, or trend continuation strategies.

chrono_utilsLibrary "chrono_utils"

Collection of objects and common functions that are related to datetime windows session days and time

ranges. The main purpose of this library is to handle time-related functionality and make it easy to reason about a

future bar checking if it will be part of a predefined session and/or inside a datetime window. All existing session

functionality I found in the documentation e.g. "not na(time(timeframe, session, timezone))" are not suitable for

strategy scripts, since the execution of the orders is delayed by one bar, due to the script execution happening at

the bar close. Moreover, a history operator with a negative value that looks forward is not allowed in any pinescript

expression. So, a prediction for the next bar using the bars_back argument of "time()"" and "time_close()" was

necessary. Thus, I created this library to overcome this small but very important limitation. In the meantime, I

added useful functionality to handle session-based behavior. An interesting utility that emerged from this

development is the data anomaly detection where a comparison between the prediction and the actual value is happening.

If those two values are different then a data inconsistency happened between the prediction bar and the actual bar

(probably due to a holiday, half session day, a timezone change etc..)

exTimezone(timezone)

exTimezone - Convert extended timezone to timezone string

Parameters:

timezone (simple string) : - The timezone or a special string

Returns: string representing the timezone

nameOfDay(day)

nameOfDay - Convert the day id into a short nameOfDay

Parameters:

day (int) : - The day id to convert

Returns: - The short name of the day

today()

today - Get the day id of this day

Returns: - The day id

nthDayAfter(day, n)

nthDayAfter - Get the day id of n days after the given day

Parameters:

day (int) : - The day id of the reference day

n (int) : - The number of days to go forward

Returns: - The day id of the day that is n days after the reference day

nextDayAfter(day)

nextDayAfter - Get the day id of next day after the given day

Parameters:

day (int) : - The day id of the reference day

Returns: - The day id of the next day after the reference day

nthDayBefore(day, n)

nthDayBefore - Get the day id of n days before the given day

Parameters:

day (int) : - The day id of the reference day

n (int) : - The number of days to go forward

Returns: - The day id of the day that is n days before the reference day

prevDayBefore(day)

prevDayBefore - Get the day id of previous day before the given day

Parameters:

day (int) : - The day id of the reference day

Returns: - The day id of the previous day before the reference day

tomorrow()

tomorrow - Get the day id of the next day

Returns: - The next day day id

normalize(num, min, max)

normalizeHour - Check if number is inthe range of

Parameters:

num (int)

min (int)

max (int)

Returns: - The normalized number

normalizeHour(hourInDay)

normalizeHour - Check if hour is valid and return a noralized hour range from

Parameters:

hourInDay (int)

Returns: - The normalized hour

normalizeMinute(minuteInHour)

normalizeMinute - Check if minute is valid and return a noralized minute from

Parameters:

minuteInHour (int)

Returns: - The normalized minute

monthInMilliseconds(mon)

monthInMilliseconds - Calculate the miliseconds in one bar of the timeframe

Parameters:

mon (int) : - The month of reference to get the miliseconds

Returns: - The number of milliseconds of the month

barInMilliseconds()

barInMilliseconds - Calculate the miliseconds in one bar of the timeframe

Returns: - The number of milliseconds in one bar

method to_string(this)

to_string - Formats the time window into a human-readable string

Namespace types: DateTimeWindow

Parameters:

this (DateTimeWindow) : - The time window object with the from and to datetimes

Returns: - The string of the time window

method to_string(this)

to_string - Formats the session days into a human-readable string with short day names

Namespace types: SessionDays

Parameters:

this (SessionDays) : - The session days object with the day selection

Returns: - The string of the session day short names

method to_string(this)

to_string - Formats the session time into a human-readable string

Namespace types: SessionTime

Parameters:

this (SessionTime) : - The session time object with the hour and minute of the time of the day

Returns: - The string of the session time

method to_string(this)

to_string - Formats the session time into a human-readable string

Namespace types: SessionTimeRange

Parameters:

this (SessionTimeRange) : - The session time range object with the start and end time of the daily session

Returns: - The string of the session time

method to_string(this)

to_string - Formats the session into a human-readable string

Namespace types: Session

Parameters:

this (Session) : - The session object with the day and the time range selection

Returns: - The string of the session

method init(this, fromDateTime, toDateTime)

init - Initialize the time window object from boolean values of each session day

Namespace types: DateTimeWindow

Parameters:

this (DateTimeWindow) : - The time window object that will hold the from and to datetimes

fromDateTime (int) : - The starting datetime of the time window

toDateTime (int) : - The ending datetime of the time window

Returns: - The time window object

method init(this, refTimezone, chTimezone, fromDateTime, toDateTime)

init - Initialize the time window object from boolean values of each session day

Namespace types: DateTimeWindow

Parameters:

this (DateTimeWindow) : - The time window object that will hold the from and to datetimes

refTimezone (simple string) : - The timezone of reference of the 'from' and 'to' dates

chTimezone (simple string) : - The target timezone to convert the 'from' and 'to' dates

fromDateTime (int) : - The starting datetime of the time window

toDateTime (int) : - The ending datetime of the time window

Returns: - The time window object

method init(this, sun, mon, tue, wed, thu, fri, sat)

init - Initialize the session days object from boolean values of each session day

Namespace types: SessionDays

Parameters:

this (SessionDays) : - The session days object that will hold the day selection

sun (bool) : - Is Sunday a trading day?

mon (bool) : - Is Monday a trading day?

tue (bool) : - Is Tuesday a trading day?

wed (bool) : - Is Wednesday a trading day?

thu (bool) : - Is Thursday a trading day?

fri (bool) : - Is Friday a trading day?

sat (bool) : - Is Saturday a trading day?

Returns: - The session days object

method init(this, unixTime)

init - Initialize the object from the hour and minute of the session time in exchange timezone (syminfo.timezone)

Namespace types: SessionTime

Parameters:

this (SessionTime) : - The session time object with the hour and minute of the time of the day

unixTime (int) : - The unix time

Returns: - The session time object

method init(this, hourInDay, minuteInHour)

init - Initialize the object from the hour and minute of the session time in exchange timezone (syminfo.timezone)

Namespace types: SessionTime

Parameters:

this (SessionTime) : - The session time object with the hour and minute of the time of the day

hourInDay (int) : - The hour of the time

minuteInHour (int) : - The minute of the time

Returns: - The session time object

method init(this, hourInDay, minuteInHour, refTimezone)

init - Initialize the object from the hour and minute of the session time

Namespace types: SessionTime

Parameters:

this (SessionTime) : - The session time object with the hour and minute of the time of the day

hourInDay (int) : - The hour of the time

minuteInHour (int) : - The minute of the time

refTimezone (string) : - The timezone of reference of the 'hour' and 'minute'

Returns: - The session time object

method init(this, startTime, endTime)

init - Initialize the object from the start and end session time in exchange timezone (syminfo.timezone)

Namespace types: SessionTimeRange

Parameters:

this (SessionTimeRange) : - The session time range object that will hold the start and end time of the daily session

startTime (SessionTime) : - The time the session begins

endTime (SessionTime) : - The time the session ends

Returns: - The session time range object

method init(this, startTimeHour, startTimeMinute, endTimeHour, endTimeMinute, refTimezone)

init - Initialize the object from the start and end session time

Namespace types: SessionTimeRange

Parameters:

this (SessionTimeRange) : - The session time range object that will hold the start and end time of the daily session

startTimeHour (int) : - The time hour the session begins

startTimeMinute (int) : - The time minute the session begins

endTimeHour (int) : - The time hour the session ends

endTimeMinute (int) : - The time minute the session ends

refTimezone (string)

Returns: - The session time range object

method init(this, days, timeRanges)

init - Initialize the session object from session days and time range

Namespace types: Session

Parameters:

this (Session) : - The session object that will hold the day and the time range selection

days (SessionDays) : - The session days object that defines the days the session is happening

timeRanges (array) : - The array of all the session time ranges during a session day

Returns: - The session object

method init(this, days, timeRanges, names, colors)

init - Initialize the session object from session days and time range

Namespace types: SessionView

Parameters:

this (SessionView) : - The session view object that will hold the session, the names and the color selections

days (SessionDays) : - The session days object that defines the days the session is happening

timeRanges (array) : - The array of all the session time ranges during a session day

names (array) : - The array of the names of the sessions

colors (array) : - The array of the colors of the sessions

Returns: - The session object

method get_size_in_secs(this)

get_size_in_secs - Count the seconds from start to end in the given timeframe

Namespace types: DateTimeWindow

Parameters:

this (DateTimeWindow) : - The time window object with the from and to datetimes

Returns: - The number of seconds inside the time widow for the given timeframe

method get_size_in_secs(this)

get_size_in_secs - Calculate the seconds inside the session

Namespace types: SessionTimeRange

Parameters:

this (SessionTimeRange) : - The session time range object with the start and end time of the daily session

Returns: - The number of seconds inside the session

method get_size_in_bars(this)

get_size_in_bars - Count the bars from start to end in the given timeframe

Namespace types: DateTimeWindow

Parameters:

this (DateTimeWindow) : - The time window object with the from and to datetimes

Returns: - The number of bars inside the time widow for the given timeframe

method get_size_in_bars(this)

get_size_in_bars - Calculate the bars inside the session

Namespace types: SessionTimeRange

Parameters:

this (SessionTimeRange) : - The session time range object with the start and end time of the daily session

Returns: - The number of bars inside the session for the given timeframe

method is_bar_included(this, offset_forward)

is_bar_included - Check if the given bar is between the start and end dates of the window

Namespace types: DateTimeWindow

Parameters:

this (DateTimeWindow) : - The time window object with the from and to datetimes

offset_forward (simple int) : - The number of bars forward. Default is 1

Returns: - Whether the current bar is inside the datetime window

method is_bar_included(this, offset_forward)

is_bar_included - Check if the given bar is inside the session as defined by the input params (what "not na(time(timeframe.period, this.to_sess_string()) )" should return if you could write it

Namespace types: Session

Parameters:

this (Session) : - The session with the day and the time range selection

offset_forward (simple int) : - The bar forward to check if it is between the from and to datetimes. Default is 1

Returns: - Whether the current time is inside the session

method to_sess_string(this)

to_sess_string - Formats the session days into a session string with day ids

Namespace types: SessionDays

Parameters:

this (SessionDays) : - The session days object

Returns: - The string of the session day ids

method to_sess_string(this)

to_sess_string - Formats the session time into a session string

Namespace types: SessionTime

Parameters:

this (SessionTime) : - The session time object with the hour and minute of the time of the day

Returns: - The string of the session time

method to_sess_string(this)

to_sess_string - Formats the session time into a session string

Namespace types: SessionTimeRange

Parameters:

this (SessionTimeRange) : - The session time range object with the start and end time of the daily session

Returns: - The string of the session time

method to_sess_string(this)

to_sess_string - Formats the session into a session string

Namespace types: Session

Parameters:

this (Session) : - The session object with the day and the time range selection

Returns: - The string of the session

method from_sess_string(this, sess)

from_sess_string - Initialize the session days object from the session string

Namespace types: SessionDays

Parameters:

this (SessionDays) : - The session days object that will hold the day selection

sess (string) : - The session string part that represents the days

Returns: - The session days object

method from_sess_string(this, sess)

from_sess_string - Initialize the session time object from the session string in exchange timezone (syminfo.timezone)

Namespace types: SessionTime

Parameters:

this (SessionTime) : - The session time object that will hold the hour and minute of the time

sess (string) : - The session string part that represents the time HHmm

Returns: - The session time object

method from_sess_string(this, sess, refTimezone)

from_sess_string - Initialize the session time object from the session string

Namespace types: SessionTime

Parameters:

this (SessionTime) : - The session time object that will hold the hour and minute of the time

sess (string) : - The session string part that represents the time HHmm

refTimezone (simple string) : - The timezone of reference of the 'hour' and 'minute'

Returns: - The session time object

method from_sess_string(this, sess)

from_sess_string - Initialize the session time range object from the session string in exchange timezone (syminfo.timezone)

Namespace types: SessionTimeRange

Parameters:

this (SessionTimeRange) : - The session time range object that will hold the start and end time of the daily session

sess (string) : - The session string part that represents the time range HHmm-HHmm

Returns: - The session time range object

method from_sess_string(this, sess, refTimezone)

from_sess_string - Initialize the session time range object from the session string

Namespace types: SessionTimeRange

Parameters:

this (SessionTimeRange) : - The session time range object that will hold the start and end time of the daily session

sess (string) : - The session string part that represents the time range HHmm-HHmm

refTimezone (simple string) : - The timezone of reference of the time ranges

Returns: - The session time range object

method from_sess_string(this, sess)

from_sess_string - Initialize the session object from the session string in exchange timezone (syminfo.timezone)

Namespace types: Session

Parameters:

this (Session) : - The session object that will hold the day and the time range selection

sess (string) : - The session string that represents the session HHmm-HHmm,HHmm-HHmm:ddddddd

Returns: - The session time range object

method from_sess_string(this, sess, refTimezone)

from_sess_string - Initialize the session object from the session string

Namespace types: Session

Parameters:

this (Session) : - The session object that will hold the day and the time range selection

sess (string) : - The session string that represents the session HHmm-HHmm,HHmm-HHmm:ddddddd

refTimezone (simple string) : - The timezone of reference of the time ranges

Returns: - The session time range object

method nth_day_after(this, day, n)

nth_day_after - The nth day after the given day that is a session day (true) in the object

Namespace types: SessionDays

Parameters:

this (SessionDays) : - The session days object with the day selection

day (int) : - The day id of the reference day

n (int) : - The number of days after

Returns: - The day id of the nth session day of the week after the given day

method nth_day_before(this, day, n)

nth_day_before - The nth day before the given day that is a session day (true) in the object

Namespace types: SessionDays

Parameters:

this (SessionDays) : - The session days object with the day selection

day (int) : - The day id of the reference day

n (int) : - The number of days after

Returns: - The day id of the nth session day of the week before the given day

method next_day(this)

next_day - The next day that is a session day (true) in the object

Namespace types: SessionDays

Parameters:

this (SessionDays) : - The session days object with the day selection

Returns: - The day id of the next session day of the week

method previous_day(this)

previous_day - The previous day that is session day (true) in the object

Namespace types: SessionDays

Parameters:

this (SessionDays) : - The session days object with the day selection

Returns: - The day id of the previous session day of the week

method get_sec_in_day(this)

get_sec_in_day - Count the seconds since the start of the day this session time represents

Namespace types: SessionTime

Parameters:

this (SessionTime) : - The session time object with the hour and minute of the time of the day

Returns: - The number of seconds passed from the start of the day until that session time

method get_ms_in_day(this)

get_ms_in_day - Count the milliseconds since the start of the day this session time represents

Namespace types: SessionTime

Parameters:

this (SessionTime) : - The session time object with the hour and minute of the time of the day

Returns: - The number of milliseconds passed from the start of the day until that session time

method is_day_included(this, day)

is_day_included - Check if the given day is inside the session days

Namespace types: SessionDays

Parameters:

this (SessionDays) : - The session days object with the day selection

day (int) : - The day to check if it is a trading day

Returns: - Whether the current day is included in the session days

DateTimeWindow

DateTimeWindow - Object that represents a datetime window with a beginning and an end

Fields:

fromDateTime (series int) : - The beginning of the datetime window

toDateTime (series int) : - The end of the datetime window

SessionDays

SessionDays - Object that represent the trading days of the week

Fields:

days (map) : - The map that contains all days of the week and their session flag

SessionTime

SessionTime - Object that represents the time (hour and minutes)

Fields:

hourInDay (series int) : - The hour of the day that ranges from 0 to 24

minuteInHour (series int) : - The minute of the hour that ranges from 0 to 59

minuteInDay (series int) : - The minute of the day that ranges from 0 to 1440. They will be calculated based on hourInDay and minuteInHour when method is called

SessionTimeRange

SessionTimeRange - Object that represents a range that extends from the start to the end time

Fields:

startTime (SessionTime) : - The beginning of the time range

endTime (SessionTime) : - The end of the time range

isOvernight (series bool) : - Whether or not this is an overnight time range

Session

Session - Object that represents a session

Fields:

days (SessionDays) : - The map of the trading days

timeRanges (array) : - The array with all time ranges of the session during the trading days

SessionView

SessionView - Object that visualize a session

Fields:

sess (Session) : - The Session object to be visualized

names (array) : - The names of the session time ranges

colors (array) : - The colors of the session time ranges

ICT Kill Zones PanelICT Kill Zones Panel - Clean & Simple Trading Sessions Indicator

A simple, objective indicator to identify ICT Kill Zones with real-time status and smart visual highlighting based on New York timezone.

WHAT MAKES IT DIFFERENT:

Traditional indicators clutter charts with dozens of colored boxes from past sessions. This tool provides a clean alternative:

- Real-time information panel showing current active session

- Smart dual-transparency painting: ACTIVE session displays stronger (more visible), historical sessions display softer (less clutter)

- Accurate session timing: Only shows active when session is actually happening

- Mobile-optimized size for phone trading

- Professional interface that doesn't interfere with price action

FEATURES:

- Real-Time Detection: Panel uses actual NYC time (timenow) to show which session is active NOW

- Precise Timing: Sessions activate ONLY during their specific time windows - all zones show inactive outside trading hours

- Smart Visual System: Currently active session has stronger background color, past sessions are softer

- Color Synchronization: Active session color in panel matches chart background color automatically

- Clean Highlighting: Optional background painting with adjustable transparency levels

- Full Customization: 9 panel positions, 4 sizes (Mobile/Small/Normal/Large), fully customizable colors

- All Sessions: Asian (20:00-01:00), London (02:00-05:00), NY AM (08:00-11:00), London Close (10:00-12:00), NY PM (13:00-16:00)

KILL ZONE SCHEDULE (NYC TIME):

1. Asian: 20:00 - 01:00 (5 hours)

2. INACTIVE: 01:00 - 02:00

3. London: 02:00 - 05:00 (3 hours)

4. INACTIVE: 05:00 - 08:00

5. NY AM: 08:00 - 11:00 (3 hours) - overlaps with London Close

6. London Close: 10:00 - 12:00 (2 hours) - overlaps with NY AM

7. INACTIVE: 12:00 - 13:00

8. NY PM: 13:00 - 16:00 (3 hours)

9. INACTIVE: 16:00 - 20:00

During INACTIVE periods, all sessions show as inactive in the panel.

COLOR SYSTEM:

ALL COLORS ARE FULLY CUSTOMIZABLE:

- Each Kill Zone has its own color setting (Asian, London, NY AM, London Close, NY PM)

- Default colors shown in screenshots are just examples

- Active session in panel: displays with its assigned color (e.g., green for NY AM by default)

- Same color appears on chart background with adjustable transparency

- Inactive sessions in panel: display with gray (also customizable)

- Panel background and text colors: fully customizable

- Choose colors that match your chart theme

The green color shown for active sessions in examples is the DEFAULT color for NY AM - you can change it to any color you prefer.

TRANSPARENCY SYSTEM EXPLAINED:

ACTIVE SESSION (happening right now):

- Default 70% transparency = STRONGER/MORE VISIBLE background

- Instantly shows which Kill Zone is unfolding

- Panel row highlights with the session's assigned color

- Chart background displays same color stronger

HISTORICAL SESSIONS (already passed):

- Default 90% transparency = SOFTER/LESS VISIBLE background

- Provides context without visual clutter

- Panel rows show gray (inactive color)

- Both transparency levels fully adjustable in settings

MOBILE OPTIMIZED:

Select "Mobile" panel size for optimal viewing on phone screens - compact layout perfect for smaller displays.

REPAINTING BEHAVIOR:

Panel Status & Colors: Update in real-time as sessions change - panel color switches to match the new active session (intentional for current awareness)

Active Session Highlighting: Adjusts in real-time to show current session stronger on chart

Historical Background Colors: Do NOT repaint - accurately mark when sessions occurred

Session Activation: Sessions activate and deactivate precisely at their scheduled times

CUSTOMIZATION:

- Panel: 9 positions, 4 sizes including Mobile

- Colors: Individual customizable color for each Kill Zone

- Panel Colors: Customizable background, text, and inactive zone colors

- Transparency: Separate controls for active (default 70%) and historical (default 90%) sessions

- Toggle: Show/hide individual zones

- Chart Painting: On/off

HOW TO USE:

1. Add to chart - panel appears top-right

2. Active session displays with its assigned color in panel and stronger on chart

3. Panel shows all zones as inactive during non-trading hours (accurate timing)

4. Panel color automatically changes when new session begins

5. Adjust all colors in settings to match your preferences

6. Adjust transparency settings for optimal visibility

7. Use "Mobile" size for phone trading

BEST FOR:

- ICT traders timing entries during high-liquidity periods

- Smart money concepts (FVG, Order Blocks, Liquidity)

- Traders who want clean charts with essential information

- Traders needing accurate session timing without false signals

- Mobile traders needing compact, clear displays

- Traders who want to customize colors to match their chart theme

TECHNICAL:

- Works on all timeframes

- Built with Pine Script v6

- NYC timezone with automatic DST adjustment

- Precise hour-based session detection

- Lightweight and optimized

- Open source

FEEDBACK WELCOME:

All comments, critiques, and suggestions are welcome! Your input helps improve this tool for the trading community.

Created by ivrank13 for traders who value simplicity, accuracy, and clean charts.

© 2026 ivrank13. All Rights Reserved.

#ICT #KillZones #SmartMoney #ForexSessions #CleanCharts #MobileTrading #CustomColors #AccurateTiming

[Statistics] killzone SFPSFP Statistics (ICT Sessions)

This indicator automatically finds and draws the high and low of the Asia, London, and New York trading sessions. It then hunts for Swing Failure Patterns (SFPs) that sweep these key session levels.

The main purpose of this script is to gather statistics on when these high-probability SFPs occur, allowing you to map out and identify the times of day when they are most frequent.

How to Use This Indicator

Set Your SFP Timeframe: In the settings, choose the timeframe you want to hunt for SFPs on (e.g., 1H, 15m). Important: You must also set your main chart to this exact same timeframe for the statistics to be collected correctly.

Define Your Sessions: Go to the "Session Definitions" tab.

Set the Global Timezone to your preferred trading timezone (e.g., "America/New_York"). This controls all session times and table times.

Adjust the start and end times for Asia, London, and NY AM sessions.

You can turn off sessions you don't want to track (like NY Lunch or NY PM).

You can also change the colors and text style for the session boxes here.

Set Confirmation Bars: In "SFP Engine Settings," the "Confirmation Bars" (default is 2) defines how many bars must close after the SFP bar without invalidating the level. An SFP is only "confirmed" and drawn after this period.

0 = Confirms immediately on the SFP candle's close.

2 = Confirms 2 bars after the SFP candle's close.

Read the Statistics: The "Custom SFP Statistics" table will appear on your chart. This table logs every confirmed SFP and tells you:

Which time of day they happen most.

How many were Bearish (swept a high) vs. Bullish (swept a low).

It's set by default to show the "Top 20" most frequent times, sorted chronologically.

Filter Your Chart (Optional): If your chart feels cluttered, go to "Visual Time Filter" and turn it ON.

Set a time window (e.g., "09:30-11:00").

The indicator will now only draw SFP signals that occurred within that specific time window. This is perfect for focusing on a single killzone.

How to Set Up Alerts

You can set up server-side alerts to be notified every time a new SFP is confirmed.

Check the "Enable SFP Alerts" box at the top of the indicator's settings.

Click the "Alert" button (alarm clock icon) on the TradingView toolbar.

In the "Condition" dropdown, select "SFP Statistics (ICT Sessions)".

In the second dropdown, choose "Any alert() function call".

Most Important Step: In the "Message" box, delete any default text and type in this exact placeholder:

{{alert_message}}

Set the trigger to "Once Per Bar Close".

Click "Create".

How Alerts Work (Triggers & Filtering)

Trigger: Alerts are tied to the confirmed signal. An alert will only fire after your "Confirmation Bars" have passed and the SFP is locked in. This prevents you from getting alerts on fake-outs.

Alert Filtering: The alerts are linked to the "Visual Time Filter". If you turn on the Visual Time Filter (e.g., to 09:30-11:00), you will only receive alerts for SFPs that are confirmed within that time window. If an SFP happens at 14:00, the script will ignore it, it will not be drawn, and it will not send you an alert. This allows you to get alerts only for the session you are actively trading.

Note: This is a first draft of this indicator. I will continue to work on it and improve it over time, as it may still contain small bugs.

Acknowledgements:

A big thank you to TFO (tradeforopp). The session detection logic and the visual style for the session boxes were adapted from his excellent "ICT Killzones & Pivots " indicator.

Globex Trap w/ percentage [SLICKRICK]Globex Trap w/ Percentage

Overview

The Globex Trap w/ Percentage indicator is a powerful tool designed to help traders identify high-probability trading opportunities by analyzing price action during the Globex (overnight) session and regular trading hours. By combining Globex session ranges with Supply & Demand zones, this indicator highlights potential "trap" areas where significant price reactions may occur. Additionally, it calculates the Globex session range as a percentage of the daily Average True Range (ATR), providing valuable context for assessing market volatility.

This indicator is ideal for traders in futures markets or other instruments traded during Globex sessions, offering a visual and analytical edge for spotting key price levels and potential reversals or breakouts.

Key Features

Globex Session Tracking:

Visualizes the high and low of the Globex session (default: 3:00 PM to 6:30 AM PST) with customizable time settings.

Displays a semi-transparent box to mark the Globex range, with labels for "Globex High" and "Globex Low."

Calculates the Globex range as a percentage of the daily ATR, displayed as a label for quick reference.

Supply & Demand Zones:

Identifies Supply & Demand zones during regular trading hours (default: 6:00 AM to 8:00 AM PST) with customizable time settings.

Draws semi-transparent boxes to highlight these zones, aiding in the identification of key support and resistance areas.

Trap Area Identification:

Highlights potential trap zones where Globex ranges and Supply & Demand zones overlap, indicating areas where price may reverse or consolidate due to trapped traders.

Customizable Settings:

Adjust Globex and Supply & Demand session times to suit your trading preferences.

Toggle visibility of Globex and Supply & Demand zones independently.

Customize box colors for better chart readability.

Set the lookback period (default: 10 days) to control how many historical zones are displayed.

Configure the ATR length (default: 14) for the percentage calculation.

PST Timezone Default:

All times are based on Pacific Standard Time (PST) by default, ensuring accurate session tracking for users in this timezone or those aligning with U.S. West Coast market hours.

Recommended Usage

Timeframes: Best used on 1-hour charts or lower (e.g., 15-minute, 5-minute) for precise entry and exit points.

Markets: Optimized for futures (e.g., ES, NQ, CL) and other instruments traded during Globex sessions.

Historical Data: Ensure at least 10 days of historical data for optimal visualization of zones.

Strategy Integration: Use the indicator to identify potential reversals or breakouts at Globex highs/lows or Supply & Demand zones. The ATR percentage provides context for whether the Globex range is significant relative to typical daily volatility.

How It Works

Globex Session:

Tracks the high and low prices during the user-defined Globex session (default: 3:00 PM to 6:30 AM PST).

When the session ends, a box is drawn from the start to the end of the session, capturing the high and low prices.

Labels are placed at the midpoint of the session, showing "Globex High," "Globex Low," and the range as a percentage of the daily ATR (e.g., "75.23% of Daily ATR").

Supply & Demand Zones:

Tracks the high and low prices during the user-defined regular trading hours (default: 6:00 AM to 8:00 AM PST).

Draws a box to mark these zones, which often act as key support or resistance levels.

ATR Percentage:

Calculates the Globex range (high minus low) and divides it by the daily ATR to express it as a percentage.

This metric helps traders gauge whether the overnight price movement is significant compared to the instrument’s typical volatility.

Time Handling:

Uses PST (UTC-8) for all time calculations, ensuring accurate session timing for users aligning with this timezone.

Properly handles overnight sessions that cross midnight, ensuring seamless tracking.

Input Settings

Globex Session Settings:

Show Globex Session: Enable/disable Globex session visualization (default: true).

Globex Start/End Time: Set the start and end times for the Globex session (default: 3:00 PM to 6:30 AM PST).

Globex Box Color: Customize the color of the Globex session box (default: semi-transparent gray).

Supply & Demand Zone Settings: