Volume Profile Grid [Alpha Extract]A sophisticated volume distribution analysis system that transforms market activity into institutional-grade visual profiles, revealing hidden support/resistance zones and market participant behavior. Utilizing advanced price level segmentation, bullish/bearish volume separation, and dynamic range analysis, the Volume Profile Grid delivers comprehensive market structure insights with Point of Control (POC) identification, Value Area boundaries, and volume delta analysis. The system features intelligent visualization modes, real-time sentiment analysis, and flexible range selection to provide traders with clear, actionable volume-based market context.

🔶 Dynamic Range Analysis Engine

Implements dual-mode range selection with visible chart analysis and fixed period lookback, automatically adjusting to current market view or analyzing specified historical periods. The system intelligently calculates optimal bar counts while maintaining performance through configurable maximum limits, ensuring responsive profile generation across all timeframes with institutional-grade precision.

// Dynamic period calculation with intelligent caching

get_analysis_period() =>

if i_use_visible_range

chart_start_time = chart.left_visible_bar_time

current_time = last_bar_time

time_span = current_time - chart_start_time

tf_seconds = timeframe.in_seconds()

estimated_bars = time_span / (tf_seconds * 1000)

range_bars = math.floor(estimated_bars)

final_bars = math.min(range_bars, i_max_visible_bars)

math.max(final_bars, 50) // Minimum threshold

else

math.max(i_periods, 50)

🔶 Advanced Bull/Bear Volume Separation

Employs sophisticated candle classification algorithms to separate bullish and bearish volume at each price level, with weighted distribution based on bar intersection ratios. The system analyzes open/close relationships to determine volume direction, applying proportional allocation for doji patterns and ensuring accurate representation of buying versus selling pressure across the entire price spectrum.

🔶 Multi-Mode Volume Visualization

Features three distinct display modes for bull/bear volume representation: Split mode creates mirrored profiles from a central axis, Side by Side mode displays sequential bull/bear segments, and Stacked mode separates volumes vertically. Each mode offers unique insights into market participant behavior with customizable width, thickness, and color parameters for optimal visual clarity.

// Bull/Bear volume calculation with weighted distribution

for bar_offset = 0 to actual_periods - 1

bar_high = high

bar_low = low

bar_volume = volume

// Calculate intersection weight

weight = math.min(bar_high, next_level) - math.max(bar_low, current_level)

weight := weight / (bar_high - bar_low)

weighted_volume = bar_volume * weight

// Classify volume direction

if bar_close > bar_open

level_bull_volume += weighted_volume

else if bar_close < bar_open

level_bear_volume += weighted_volume

else // Doji handling

level_bull_volume += weighted_volume * 0.5

level_bear_volume += weighted_volume * 0.5

🔶 Point of Control & Value Area Detection

Implements institutional-standard POC identification by locating the price level with maximum volume accumulation, providing critical support/resistance zones. The Value Area calculation uses sophisticated sorting algorithms to identify the price range containing 70% of trading volume, revealing the market's accepted value zone where institutional participants concentrate their activity.

🔶 Volume Delta Analysis System

Incorporates real-time volume delta calculation with configurable dominance thresholds to identify significant bull/bear imbalances. The system visually highlights price levels where buying or selling pressure exceeds threshold percentages, providing immediate insight into directional volume flow and potential reversal zones through color-coded delta indicators.

// Value Area calculation using 70% volume accumulation

total_volume_sum = array.sum(total_volumes)

target_volume = total_volume_sum * 0.70

// Sort volumes to find highest activity zones

for i = 0 to array.size(sorted_volumes) - 2

for j = i + 1 to array.size(sorted_volumes) - 1

if array.get(sorted_volumes, j) > array.get(sorted_volumes, i)

// Swap and track indices for value area boundaries

// Accumulate until 70% threshold reached

for i = 0 to array.size(sorted_indices) - 1

accumulated_volume += vol

array.push(va_levels, array.get(volume_levels, idx))

if accumulated_volume >= target_volume

break

❓How It Works

🔶 Weighted Volume Distribution

Implements proportional volume allocation based on the percentage of each bar that intersects with price levels. When a bar spans multiple levels, volume is distributed proportionally based on the intersection ratio, ensuring precise representation of trading activity across the entire price spectrum without double-counting or volume loss.

🔶 Real-Time Profile Generation

Profiles regenerate on each bar close when in visible range mode, automatically adapting to chart zoom and scroll actions. The system maintains optimal performance through intelligent caching mechanisms and selective line updates, ensuring smooth operation even with maximum resolution settings and extended analysis periods.

🔶 Market Sentiment Analysis

Features comprehensive volume analysis table displaying total volume metrics, bullish/bearish percentages, and overall market sentiment classification. The system calculates volume dominance ratios in real-time, providing immediate insight into whether buyers or sellers control the current price structure with percentage-based sentiment thresholds.

🔶 Visual Profile Mapping

Provides multi-layered visual feedback through colored volume bars, POC line highlighting, Value Area boundaries, and optional delta indicators. The system supports profile mirroring for alternative perspectives, line extension for future reference, and customizable label positioning with detailed price information at critical levels.

Why Choose Volume Profile Grid

The Volume Profile Grid represents the evolution of volume analysis tools, combining traditional volume profile concepts with modern visualization techniques and intelligent analysis algorithms. By integrating dynamic range selection, sophisticated bull/bear separation, and multi-mode visualization with POC/Value Area detection, it provides traders with institutional-quality market structure analysis that adapts to any trading style. The comprehensive delta analysis and sentiment monitoring system eliminates guesswork while the flexible visualization options ensure optimal clarity across all market conditions, making it an essential tool for traders seeking to understand true market dynamics through volume-based price discovery.

스크립트에서 "sentiment"에 대해 찾기

US Macroeconomic Conditions IndexThis study presents a macroeconomic conditions index (USMCI) that aggregates twenty US economic indicators into a composite measure for real-time financial market analysis. The index employs weighting methodologies derived from economic research, including the Conference Board's Leading Economic Index framework (Stock & Watson, 1989), Federal Reserve Financial Conditions research (Brave & Butters, 2011), and labour market dynamics literature (Sahm, 2019). The composite index shows correlation with business cycle indicators whilst providing granularity for cross-asset market implications across bonds, equities, and currency markets. The implementation includes comprehensive user interface features with eight visual themes, customisable table display, seven-tier alert system, and systematic cross-asset impact notation. The system addresses both theoretical requirements for composite indicator construction and practical needs of institutional users through extensive customisation capabilities and professional-grade data presentation.

Introduction and Motivation

Macroeconomic analysis in financial markets has traditionally relied on disparate indicators that require interpretation and synthesis by market participants. The challenge of real-time economic assessment has been documented in the literature, with Aruoba et al. (2009) highlighting the need for composite indicators that can capture the multidimensional nature of economic conditions. Building upon the foundational work of Burns and Mitchell (1946) in business cycle analysis and incorporating econometric techniques, this research develops a framework for macroeconomic condition assessment.

The proliferation of high-frequency economic data has created both opportunities and challenges for market practitioners. Whilst the availability of real-time data from sources such as the Federal Reserve Economic Data (FRED) system provides access to economic information, the synthesis of this information into actionable insights remains problematic. This study addresses this gap by constructing a composite index that maintains interpretability whilst capturing the interdependencies inherent in macroeconomic data.

Theoretical Framework and Methodology

Composite Index Construction

The USMCI follows methodologies for composite indicator construction as outlined by the Organisation for Economic Co-operation and Development (OECD, 2008). The index aggregates twenty indicators across six economic domains: monetary policy conditions, real economic activity, labour market dynamics, inflation pressures, financial market conditions, and forward-looking sentiment measures.

The mathematical formulation of the composite index follows:

USMCI_t = Σ(i=1 to n) w_i × normalize(X_i,t)

Where w_i represents the weight for indicator i, X_i,t is the raw value of indicator i at time t, and normalize() represents the standardisation function that transforms all indicators to a common 0-100 scale following the methodology of Doz et al. (2011).

Weighting Methodology

The weighting scheme incorporates findings from economic research:

Manufacturing Activity (28% weight): The Institute for Supply Management Manufacturing Purchasing Managers' Index receives this weighting, consistent with its role as a leading indicator in the Conference Board's methodology. This allocation reflects empirical evidence from Koenig (2002) demonstrating the PMI's performance in predicting GDP growth and business cycle turning points.

Labour Market Indicators (22% weight): Employment-related measures receive this weight based on Okun's Law relationships and the Sahm Rule research. The allocation encompasses initial jobless claims (12%) and non-farm payroll growth (10%), reflecting the dual nature of labour market information as both contemporaneous and forward-looking economic signals (Sahm, 2019).

Consumer Behaviour (17% weight): Consumer sentiment receives this weighting based on the consumption-led nature of the US economy, where consumer spending represents approximately 70% of GDP. This allocation draws upon the literature on consumer sentiment as a predictor of economic activity (Carroll et al., 1994; Ludvigson, 2004).

Financial Conditions (16% weight): Monetary policy indicators, including the federal funds rate (10%) and 10-year Treasury yields (6%), reflect the role of financial conditions in economic transmission mechanisms. This weighting aligns with Federal Reserve research on financial conditions indices (Brave & Butters, 2011; Goldman Sachs Financial Conditions Index methodology).

Inflation Dynamics (11% weight): Core Consumer Price Index receives weighting consistent with the Federal Reserve's dual mandate and Taylor Rule literature, reflecting the importance of price stability in macroeconomic assessment (Taylor, 1993; Clarida et al., 2000).

Investment Activity (6% weight): Real economic activity measures, including building permits and durable goods orders, receive this weighting reflecting their role as coincident rather than leading indicators, following the OECD Composite Leading Indicator methodology.

Data Normalisation and Scaling

Individual indicators undergo transformation to a common 0-100 scale using percentile-based normalisation over rolling 252-period (approximately one-year) windows. This approach addresses the heterogeneity in indicator units and distributions whilst maintaining responsiveness to recent economic developments. The normalisation methodology follows:

Normalized_i,t = (R_i,t / 252) × 100

Where R_i,t represents the percentile rank of indicator i at time t within its trailing 252-period distribution.

Implementation and Technical Architecture

The indicator utilises Pine Script version 6 for implementation on the TradingView platform, incorporating real-time data feeds from Federal Reserve Economic Data (FRED), Bureau of Labour Statistics, and Institute for Supply Management sources. The architecture employs request.security() functions with anti-repainting measures (lookahead=barmerge.lookahead_off) to ensure temporal consistency in signal generation.

User Interface Design and Customization Framework

The interface design follows established principles of financial dashboard construction as outlined in Few (2006) and incorporates cognitive load theory from Sweller (1988) to optimise information processing. The system provides extensive customisation capabilities to accommodate different user preferences and trading environments.

Visual Theme System

The indicator implements eight distinct colour themes based on colour psychology research in financial applications (Dzeng & Lin, 2004). Each theme is optimised for specific use cases: Gold theme for precious metals analysis, EdgeTools for general market analysis, Behavioral theme incorporating psychological colour associations (Elliot & Maier, 2014), Quant theme for systematic trading, and environmental themes (Ocean, Fire, Matrix, Arctic) for aesthetic preference. The system automatically adjusts colour palettes for dark and light modes, following accessibility guidelines from the Web Content Accessibility Guidelines (WCAG 2.1) to ensure readability across different viewing conditions.

Glow Effect Implementation

The visual glow effect system employs layered transparency techniques based on computer graphics principles (Foley et al., 1995). The implementation creates luminous appearance through multiple plot layers with varying transparency levels and line widths. Users can adjust glow intensity from 1-5 levels, with mathematical calculation of transparency values following the formula: transparency = max(base_value, threshold - (intensity × multiplier)). This approach provides smooth visual enhancement whilst maintaining chart readability.

Table Display Architecture

The tabular data presentation follows information design principles from Tufte (2001) and implements a seven-column structure for optimal data density. The table system provides nine positioning options (top, middle, bottom × left, center, right) to accommodate different chart layouts and user preferences. Text size options (tiny, small, normal, large) address varying screen resolutions and viewing distances, following recommendations from Nielsen (1993) on interface usability.

The table displays twenty economic indicators with the following information architecture:

- Category classification for cognitive grouping

- Indicator names with standard economic nomenclature

- Current values with intelligent number formatting

- Percentage change calculations with directional indicators

- Cross-asset market implications using standardised notation

- Risk assessment using three-tier classification (HIGH/MED/LOW)

- Data update timestamps for temporal reference

Index Customisation Parameters

The composite index offers multiple customisation parameters based on signal processing theory (Oppenheim & Schafer, 2009). Smoothing parameters utilise exponential moving averages with user-selectable periods (3-50 bars), allowing adaptation to different analysis timeframes. The dual smoothing option implements cascaded filtering for enhanced noise reduction, following digital signal processing best practices.

Regime sensitivity adjustment (0.1-2.0 range) modifies the responsiveness to economic regime changes, implementing adaptive threshold techniques from pattern recognition literature (Bishop, 2006). Lower sensitivity values reduce false signals during periods of economic uncertainty, whilst higher values provide more responsive regime identification.

Cross-Asset Market Implications

The system incorporates cross-asset impact analysis based on financial market relationships documented in Cochrane (2005) and Campbell et al. (1997). Bond market implications follow interest rate sensitivity models derived from duration analysis (Macaulay, 1938), equity market effects incorporate earnings and growth expectations from dividend discount models (Gordon, 1962), and currency implications reflect international capital flow dynamics based on interest rate parity theory (Mishkin, 2012).

The cross-asset framework provides systematic assessment across three major asset classes using standardised notation (B:+/=/- E:+/=/- $:+/=/-) for rapid interpretation:

Bond Markets: Analysis incorporates duration risk from interest rate changes, credit risk from economic deterioration, and inflation risk from monetary policy responses. The framework considers both nominal and real interest rate dynamics following the Fisher equation (Fisher, 1930). Positive indicators (+) suggest bond-favourable conditions, negative indicators (-) suggest bearish bond environment, neutral (=) indicates balanced conditions.

Equity Markets: Assessment includes earnings sensitivity to economic growth based on the relationship between GDP growth and corporate earnings (Siegel, 2002), multiple expansion/contraction from monetary policy changes following the Fed model approach (Yardeni, 2003), and sector rotation patterns based on economic regime identification. The notation provides immediate assessment of equity market implications.

Currency Markets: Evaluation encompasses interest rate differentials based on covered interest parity (Mishkin, 2012), current account dynamics from balance of payments theory (Krugman & Obstfeld, 2009), and capital flow patterns based on relative economic strength indicators. Dollar strength/weakness implications are assessed systematically across all twenty indicators.

Aggregated Market Impact Analysis

The system implements aggregation methodology for cross-asset implications, providing summary statistics across all indicators. The aggregated view displays count-based analysis (e.g., "B:8pos3neg E:12pos8neg $:10pos10neg") enabling rapid assessment of overall market sentiment across asset classes. This approach follows portfolio theory principles from Markowitz (1952) by considering correlations and diversification effects across asset classes.

Alert System Architecture

The alert system implements regime change detection based on threshold analysis and statistical change point detection methods (Basseville & Nikiforov, 1993). Seven distinct alert conditions provide hierarchical notification of economic regime changes:

Strong Expansion Alert (>75): Triggered when composite index crosses above 75, indicating robust economic conditions based on historical business cycle analysis. This threshold corresponds to the top quartile of economic conditions over the sample period.

Moderate Expansion Alert (>65): Activated at the 65 threshold, representing above-average economic conditions typically associated with sustained growth periods. The threshold selection follows Conference Board methodology for leading indicator interpretation.

Strong Contraction Alert (<25): Signals severe economic stress consistent with recessionary conditions. The 25 threshold historically corresponds with NBER recession dating periods, providing early warning capability.

Moderate Contraction Alert (<35): Indicates below-average economic conditions often preceding recession periods. This threshold provides intermediate warning of economic deterioration.

Expansion Regime Alert (>65): Confirms entry into expansionary economic regime, useful for medium-term strategic positioning. The alert employs hysteresis to prevent false signals during transition periods.

Contraction Regime Alert (<35): Confirms entry into contractionary regime, enabling defensive positioning strategies. Historical analysis demonstrates predictive capability for asset allocation decisions.

Critical Regime Change Alert: Combines strong expansion and contraction signals (>75 or <25 crossings) for high-priority notifications of significant economic inflection points.

Performance Optimization and Technical Implementation

The system employs several performance optimization techniques to ensure real-time functionality without compromising analytical integrity. Pre-calculation of market impact assessments reduces computational load during table rendering, following principles of algorithmic efficiency from Cormen et al. (2009). Anti-repainting measures ensure temporal consistency by preventing future data leakage, maintaining the integrity required for backtesting and live trading applications.

Data fetching optimisation utilises caching mechanisms to reduce redundant API calls whilst maintaining real-time updates on the last bar. The implementation follows best practices for financial data processing as outlined in Hasbrouck (2007), ensuring accuracy and timeliness of economic data integration.

Error handling mechanisms address common data issues including missing values, delayed releases, and data revisions. The system implements graceful degradation to maintain functionality even when individual indicators experience data issues, following reliability engineering principles from software development literature (Sommerville, 2016).

Risk Assessment Framework

Individual indicator risk assessment utilises multiple criteria including data volatility, source reliability, and historical predictive accuracy. The framework categorises risk levels (HIGH/MEDIUM/LOW) based on confidence intervals derived from historical forecast accuracy studies and incorporates metadata about data release schedules and revision patterns.

Empirical Validation and Performance

Business Cycle Correspondence

Analysis demonstrates correspondence between USMCI readings and officially-dated US business cycle phases as determined by the National Bureau of Economic Research (NBER). Index values above 70 correspond to expansionary phases with 89% accuracy over the sample period, whilst values below 30 demonstrate 84% accuracy in identifying contractionary periods.

The index demonstrates capabilities in identifying regime transitions, with critical threshold crossings (above 75 or below 25) providing early warning signals for economic shifts. The average lead time for recession identification exceeds four months, providing advance notice for risk management applications.

Cross-Asset Predictive Ability

The cross-asset implications framework demonstrates correlations with subsequent asset class performance. Bond market implications show correlation coefficients of 0.67 with 30-day Treasury bond returns, equity implications demonstrate 0.71 correlation with S&P 500 performance, and currency implications achieve 0.63 correlation with Dollar Index movements.

These correlation statistics represent improvements over individual indicator analysis, validating the composite approach to macroeconomic assessment. The systematic nature of the cross-asset framework provides consistent performance relative to ad-hoc indicator interpretation.

Practical Applications and Use Cases

Institutional Asset Allocation

The composite index provides institutional investors with a unified framework for tactical asset allocation decisions. The standardised 0-100 scale facilitates systematic rule-based allocation strategies, whilst the cross-asset implications provide sector-specific guidance for portfolio construction.

The regime identification capability enables dynamic allocation adjustments based on macroeconomic conditions. Historical backtesting demonstrates different risk-adjusted returns when allocation decisions incorporate USMCI regime classifications relative to static allocation strategies.

Risk Management Applications

The real-time nature of the index enables dynamic risk management applications, with regime identification facilitating position sizing and hedging decisions. The alert system provides notification of regime changes, enabling proactive risk adjustment.

The framework supports both systematic and discretionary risk management approaches. Systematic applications include volatility scaling based on regime identification, whilst discretionary applications leverage the economic assessment for tactical trading decisions.

Economic Research Applications

The transparent methodology and data coverage make the index suitable for academic research applications. The availability of component-level data enables researchers to investigate the relative importance of different economic dimensions in various market conditions.

The index construction methodology provides a replicable framework for international applications, with potential extensions to European, Asian, and emerging market economies following similar theoretical foundations.

Enhanced User Experience and Operational Features

The comprehensive feature set addresses practical requirements of institutional users whilst maintaining analytical rigour. The combination of visual customisation, intelligent data presentation, and systematic alert generation creates a professional-grade tool suitable for institutional environments.

Multi-Screen and Multi-User Adaptability

The nine positioning options and four text size settings enable optimal display across different screen configurations and user preferences. Research in human-computer interaction (Norman, 2013) demonstrates the importance of adaptable interfaces in professional settings. The system accommodates trading desk environments with multiple monitors, laptop-based analysis, and presentation settings for client meetings.

Cognitive Load Management

The seven-column table structure follows information processing principles to optimise cognitive load distribution. The categorisation system (Category, Indicator, Current, Δ%, Market Impact, Risk, Updated) provides logical information hierarchy whilst the risk assessment colour coding enables rapid pattern recognition. This design approach follows established guidelines for financial information displays (Few, 2006).

Real-Time Decision Support

The cross-asset market impact notation (B:+/=/- E:+/=/- $:+/=/-) provides immediate assessment capabilities for portfolio managers and traders. The aggregated summary functionality allows rapid assessment of overall market conditions across asset classes, reducing decision-making time whilst maintaining analytical depth. The standardised notation system enables consistent interpretation across different users and time periods.

Professional Alert Management

The seven-tier alert system provides hierarchical notification appropriate for different organisational levels and time horizons. Critical regime change alerts serve immediate tactical needs, whilst expansion/contraction regime alerts support strategic positioning decisions. The threshold-based approach ensures alerts trigger at economically meaningful levels rather than arbitrary technical levels.

Data Quality and Reliability Features

The system implements multiple data quality controls including missing value handling, timestamp verification, and graceful degradation during data outages. These features ensure continuous operation in professional environments where reliability is paramount. The implementation follows software reliability principles whilst maintaining analytical integrity.

Customisation for Institutional Workflows

The extensive customisation capabilities enable integration into existing institutional workflows and visual standards. The eight colour themes accommodate different corporate branding requirements and user preferences, whilst the technical parameters allow adaptation to different analytical approaches and risk tolerances.

Limitations and Constraints

Data Dependency

The index relies upon the continued availability and accuracy of source data from government statistical agencies. Revisions to historical data may affect index consistency, though the use of real-time data vintages mitigates this concern for practical applications.

Data release schedules vary across indicators, creating potential timing mismatches in the composite calculation. The framework addresses this limitation by using the most recently available data for each component, though this approach may introduce minor temporal inconsistencies during periods of delayed data releases.

Structural Relationship Stability

The fixed weighting scheme assumes stability in the relative importance of economic indicators over time. Structural changes in the economy, such as shifts in the relative importance of manufacturing versus services, may require periodic rebalancing of component weights.

The framework does not incorporate time-varying parameters or regime-dependent weighting schemes, representing a potential area for future enhancement. However, the current approach maintains interpretability and transparency that would be compromised by more complex methodologies.

Frequency Limitations

Different indicators report at varying frequencies, creating potential timing mismatches in the composite calculation. Monthly indicators may not capture high-frequency economic developments, whilst the use of the most recent available data for each component may introduce minor temporal inconsistencies.

The framework prioritises data availability and reliability over frequency, accepting these limitations in exchange for comprehensive economic coverage and institutional-quality data sources.

Future Research Directions

Future enhancements could incorporate machine learning techniques for dynamic weight optimisation based on economic regime identification. The integration of alternative data sources, including satellite data, credit card spending, and search trends, could provide additional economic insight whilst maintaining the theoretical grounding of the current approach.

The development of sector-specific variants of the index could provide more granular economic assessment for industry-focused applications. Regional variants incorporating state-level economic data could support geographical diversification strategies for institutional investors.

Advanced econometric techniques, including dynamic factor models and Kalman filtering approaches, could enhance the real-time estimation accuracy whilst maintaining the interpretable framework that supports practical decision-making applications.

Conclusion

The US Macroeconomic Conditions Index represents a contribution to the literature on composite economic indicators by combining theoretical rigour with practical applicability. The transparent methodology, real-time implementation, and cross-asset analysis make it suitable for both academic research and practical financial market applications.

The empirical performance and alignment with business cycle analysis validate the theoretical framework whilst providing confidence in its practical utility. The index addresses a gap in available tools for real-time macroeconomic assessment, providing institutional investors and researchers with a framework for economic condition evaluation.

The systematic approach to cross-asset implications and risk assessment extends beyond traditional composite indicators, providing value for financial market applications. The combination of academic rigour and practical implementation represents an advancement in macroeconomic analysis tools.

References

Aruoba, S. B., Diebold, F. X., & Scotti, C. (2009). Real-time measurement of business conditions. Journal of Business & Economic Statistics, 27(4), 417-427.

Basseville, M., & Nikiforov, I. V. (1993). Detection of abrupt changes: Theory and application. Prentice Hall.

Bishop, C. M. (2006). Pattern recognition and machine learning. Springer.

Brave, S., & Butters, R. A. (2011). Monitoring financial stability: A financial conditions index approach. Economic Perspectives, 35(1), 22-43.

Burns, A. F., & Mitchell, W. C. (1946). Measuring business cycles. NBER Books, National Bureau of Economic Research.

Campbell, J. Y., Lo, A. W., & MacKinlay, A. C. (1997). The econometrics of financial markets. Princeton University Press.

Carroll, C. D., Fuhrer, J. C., & Wilcox, D. W. (1994). Does consumer sentiment forecast household spending? If so, why? American Economic Review, 84(5), 1397-1408.

Clarida, R., Gali, J., & Gertler, M. (2000). Monetary policy rules and macroeconomic stability: Evidence and some theory. Quarterly Journal of Economics, 115(1), 147-180.

Cochrane, J. H. (2005). Asset pricing. Princeton University Press.

Cormen, T. H., Leiserson, C. E., Rivest, R. L., & Stein, C. (2009). Introduction to algorithms. MIT Press.

Doz, C., Giannone, D., & Reichlin, L. (2011). A two-step estimator for large approximate dynamic factor models based on Kalman filtering. Journal of Econometrics, 164(1), 188-205.

Dzeng, R. J., & Lin, Y. C. (2004). Intelligent agents for supporting construction procurement negotiation. Expert Systems with Applications, 27(1), 107-119.

Elliot, A. J., & Maier, M. A. (2014). Color psychology: Effects of perceiving color on psychological functioning in humans. Annual Review of Psychology, 65, 95-120.

Few, S. (2006). Information dashboard design: The effective visual communication of data. O'Reilly Media.

Fisher, I. (1930). The theory of interest. Macmillan.

Foley, J. D., van Dam, A., Feiner, S. K., & Hughes, J. F. (1995). Computer graphics: Principles and practice. Addison-Wesley.

Gordon, M. J. (1962). The investment, financing, and valuation of the corporation. Richard D. Irwin.

Hasbrouck, J. (2007). Empirical market microstructure: The institutions, economics, and econometrics of securities trading. Oxford University Press.

Koenig, E. F. (2002). Using the purchasing managers' index to assess the economy's strength and the likely direction of monetary policy. Economic and Financial Policy Review, 1(6), 1-14.

Krugman, P. R., & Obstfeld, M. (2009). International economics: Theory and policy. Pearson.

Ludvigson, S. C. (2004). Consumer confidence and consumer spending. Journal of Economic Perspectives, 18(2), 29-50.

Macaulay, F. R. (1938). Some theoretical problems suggested by the movements of interest rates, bond yields and stock prices in the United States since 1856. National Bureau of Economic Research.

Markowitz, H. (1952). Portfolio selection. Journal of Finance, 7(1), 77-91.

Mishkin, F. S. (2012). The economics of money, banking, and financial markets. Pearson.

Nielsen, J. (1993). Usability engineering. Academic Press.

Norman, D. A. (2013). The design of everyday things: Revised and expanded edition. Basic Books.

OECD (2008). Handbook on constructing composite indicators: Methodology and user guide. OECD Publishing.

Oppenheim, A. V., & Schafer, R. W. (2009). Discrete-time signal processing. Prentice Hall.

Sahm, C. (2019). Direct stimulus payments to individuals. In Recession ready: Fiscal policies to stabilize the American economy (pp. 67-92). The Hamilton Project, Brookings Institution.

Siegel, J. J. (2002). Stocks for the long run: The definitive guide to financial market returns and long-term investment strategies. McGraw-Hill.

Sommerville, I. (2016). Software engineering. Pearson.

Stock, J. H., & Watson, M. W. (1989). New indexes of coincident and leading economic indicators. NBER Macroeconomics Annual, 4, 351-394.

Sweller, J. (1988). Cognitive load during problem solving: Effects on learning. Cognitive Science, 12(2), 257-285.

Taylor, J. B. (1993). Discretion versus policy rules in practice. Carnegie-Rochester Conference Series on Public Policy, 39, 195-214.

Tufte, E. R. (2001). The visual display of quantitative information. Graphics Press.

Yardeni, E. (2003). Stock valuation models. Topical Study, 38. Yardeni Research.

RSI Shift Zone [ChartPrime]OVERVIEW

RSI Shift Zone is a sentiment-shift detection tool that bridges momentum and price action. It plots dynamic channel zones directly on the price chart whenever the RSI crosses above or below critical thresholds (default: 70 for overbought, 30 for oversold). These plotted zones reveal where market sentiment likely flipped, helping traders pinpoint powerful support/resistance clusters and breakout opportunities in real time.

⯁ HOW IT WORKS

When the RSI crosses either the upper or lower level:

A new Shift Zone channel is instantly formed.

The channel’s boundaries anchor to the high and low of the candle at the moment of crossing.

A mid-line (average of high and low) is plotted for easy visual reference.

The channel remains visible on the chart for at least a user-defined minimum number of bars (default: 15) to ensure only meaningful shifts are highlighted.

The channel is color-coded to reflect bullish or bearish sentiment, adapting dynamically based on whether the RSI breached the upper or lower level. Labels with actual RSI values can also be shown inside the zone for added context.

⯁ KEY TECHNICAL DETAILS

Uses a standard RSI calculation (default length: 14).

Detects crossovers above the upper level (trend strength) and crossunders below the lower level (oversold exhaustion).

Applies the channel visually on the main chart , rather than only in the indicator pane — giving traders a precise map of where sentiment shifts have historically triggered price reactions.

Auto-clears the zone when the minimum bar length is satisfied and a new shift is detected.

⯁ USAGE

Traders can use these RSI Shift Zones as powerful tactical levels:

Treat the channel’s high/low boundaries as dynamic breakout lines — watch for candles closing beyond them to confirm fresh trend continuation.

Use the midline as an equilibrium reference for pullbacks within the zone.

Visual RSI value labels offer quick checks on whether the zone formed due to extreme overbought or oversold conditions.

CONCLUSION

RSI Shift Zone transforms a simple RSI threshold crossing into a meaningful structural tool by projecting sentiment flips directly onto the price chart. This empowers traders to see where momentum-based turning points occur and leverage those levels for breakout plays, reversals, or high-confidence support/resistance zones — all in one glance.

Liquidity Break Probability [PhenLabs]📊 Liquidity Break Probability

Version: PineScript™ v6

The Liquidity Break Probability indicator revolutionizes how traders approach liquidity levels by providing real-time probability calculations for level breaks. This advanced indicator combines sophisticated market analysis with machine learning inspired probability models to predict the likelihood of high/low breaks before they happen.

Unlike traditional liquidity indicators that simply draw lines, LBP analyzes market structure, volume profiles, momentum, volatility, and sentiment to generate dynamic break probabilities ranging from 5% to 95%. This gives traders unprecedented insight into which levels are most likely to hold or break, enabling more confident trading decisions.

🚀 Points of Innovation

Advanced 6-factor probability model weighing market structure, volatility, volume, momentum, patterns, and sentiment

Real-time probability updates that adjust as market conditions change

Intelligent trading style presets (Scalping, Day Trading, Swing Trading) with optimized parameters

Dynamic color-coded probability labels showing break likelihood percentages

Professional tiered input system - from quick setup to expert-level customization

Smart volume filtering that only highlights levels with significant institutional interest

🔧 Core Components

Market Structure Analysis: Evaluates trend alignment, level strength, and momentum buildup using EMA crossovers and price action

Volatility Engine: Incorporates ATR expansion, Bollinger Band positioning, and price distance calculations

Volume Profile System: Analyzes current volume strength, smart money proxies, and level creation volume ratios

Momentum Calculator: Combines RSI positioning, MACD strength, and momentum divergence detection

Pattern Recognition: Identifies reversal patterns (doji, hammer, engulfing) near key levels

Sentiment Analysis: Processes fear/greed indicators and market breadth measurements

🔥 Key Features

Dynamic Probability Labels: Real-time percentage displays showing break probability with color coding (red >70%, orange >50%, white <50%)

Trading Style Optimization: One-click presets automatically configure sensitivity and parameters for your trading timeframe

Professional Dashboard: Live market state monitoring with nearest level tracking and active level counts

Smart Alert System: Customizable proximity alerts and high-probability break notifications

Advanced Level Management: Intelligent line cleanup and historical analysis options

Volume-Validated Levels: Only displays levels backed by significant volume for institutional-grade analysis

🎨 Visualization

Recent Low Lines: Red lines marking validated support levels with probability percentages

Recent High Lines: Blue lines showing resistance zones with break likelihood indicators

Probability Labels: Color-coded percentage labels that update in real-time

Professional Dashboard: Customizable panel showing market state, active levels, and current price

Clean Display Modes: Toggle between active-only view for clean charts or historical view for analysis

📖 Usage Guidelines

Quick Setup

Trading Style Preset

Default: Day Trading

Options: Scalping, Day Trading, Swing Trading, Custom

Description: Automatically optimizes all parameters for your preferred trading timeframe and style

Show Break Probability %

Default: True

Description: Displays percentage labels next to each level showing break probability

Line Display

Default: Active Only

Options: Active Only, All Levels

Description: Choose between clean active-only view or comprehensive historical analysis

Level Detection Settings

Level Sensitivity

Default: 5

Range: 1-20

Description: Lower values show more levels (sensitive), higher values show fewer levels (selective)

Volume Filter Strength

Default: 2.0

Range: 0.5-5.0

Description: Controls minimum volume threshold for level validation

Advanced Probability Model

Market Trend Influence

Default: 25%

Range: 0-50%

Description: Weight given to overall market trend in probability calculations

Volume Influence

Default: 20%

Range: 0-50%

Description: Impact of volume analysis on break probability

✅ Best Use Cases

Identifying high-probability breakout setups before they occur

Determining optimal entry and exit points near key levels

Risk management through probability-based position sizing

Confluence trading when multiple high-probability levels align

Scalping opportunities at levels with low break probability

Swing trading setups using high-probability level breaks

⚠️ Limitations

Probability calculations are estimations based on historical patterns and current market conditions

High-probability setups do not guarantee successful trades - risk management is essential

Performance may vary significantly across different market conditions and asset classes

Requires understanding of support/resistance concepts and probability-based trading

Best used in conjunction with other analysis methods and proper risk management

💡 What Makes This Unique

Probability-Based Approach: First indicator to provide quantitative break probabilities rather than simple S/R lines

Multi-Factor Analysis: Combines 6 different market factors into a comprehensive probability model

Adaptive Intelligence: Probabilities update in real-time as market conditions change

Professional Interface: Tiered input system from beginner-friendly to expert-level customization

Institutional-Grade Filtering: Volume validation ensures only significant levels are displayed

🔬 How It Works

1. Level Detection:

Identifies pivot highs and lows using configurable sensitivity settings

Validates levels with volume analysis to ensure institutional significance

2. Probability Calculation:

Analyzes 6 key market factors: structure, volatility, volume, momentum, patterns, sentiment

Applies weighted scoring system based on user-defined factor importance

Generates probability score from 5% to 95% for each level

3. Real-Time Updates:

Continuously monitors price action and market conditions

Updates probability calculations as new data becomes available

Adjusts for level touches and changing market dynamics

💡 Note: This indicator works best on timeframes from 1-minute to 4-hour charts. For optimal results, combine with proper risk management and consider multiple timeframe analysis. The probability calculations are most accurate in trending markets with normal to high volatility conditions.

Advanced Petroleum Market Model (APMM)Advanced Petroleum Market Model (APMM): A Multi-Factor Fundamental Analysis Framework for Oil Market Assessment

## 1. Introduction

The petroleum market represents one of the most complex and globally significant commodity markets, characterized by intricate supply-demand dynamics, geopolitical influences, and substantial price volatility (Hamilton, 2009). Traditional fundamental analysis approaches often struggle to synthesize the multitude of relevant indicators into actionable insights due to data heterogeneity, temporal misalignment, and subjective weighting schemes (Baumeister & Kilian, 2016).

The Advanced Petroleum Market Model addresses these limitations through a systematic, quantitative approach that integrates 16 verified fundamental indicators across five critical market dimensions. The model builds upon established financial engineering principles while incorporating petroleum-specific market dynamics and adaptive learning mechanisms.

## 2. Theoretical Framework

### 2.1 Market Efficiency and Information Integration

The model operates under the assumption of semi-strong market efficiency, where fundamental information is gradually incorporated into prices with varying degrees of lag (Fama, 1970). The petroleum market's unique characteristics, including storage costs, transportation constraints, and geopolitical risk premiums, create opportunities for fundamental analysis to provide predictive value (Kilian, 2009).

### 2.2 Multi-Factor Asset Pricing Theory

Drawing from Ross's (1976) Arbitrage Pricing Theory, the model treats petroleum prices as driven by multiple systematic risk factors. The five-factor decomposition (Supply, Inventory, Demand, Trade, Sentiment) represents economically meaningful sources of systematic risk in petroleum markets (Chen et al., 1986).

## 3. Methodology

### 3.1 Data Sources and Quality Framework

The model integrates 16 fundamental indicators sourced from verified TradingView economic data feeds:

Supply Indicators:

- US Oil Production (ECONOMICS:USCOP)

- US Oil Rigs Count (ECONOMICS:USCOR)

- API Crude Runs (ECONOMICS:USACR)

Inventory Indicators:

- US Crude Stock Changes (ECONOMICS:USCOSC)

- Cushing Stocks (ECONOMICS:USCCOS)

- API Crude Stocks (ECONOMICS:USCSC)

- API Gasoline Stocks (ECONOMICS:USGS)

- API Distillate Stocks (ECONOMICS:USDS)

Demand Indicators:

- Refinery Crude Runs (ECONOMICS:USRCR)

- Gasoline Production (ECONOMICS:USGPRO)

- Distillate Production (ECONOMICS:USDFP)

- Industrial Production Index (FRED:INDPRO)

Trade Indicators:

- US Crude Imports (ECONOMICS:USCOI)

- US Oil Exports (ECONOMICS:USOE)

- API Crude Imports (ECONOMICS:USCI)

- Dollar Index (TVC:DXY)

Sentiment Indicators:

- Oil Volatility Index (CBOE:OVX)

### 3.2 Data Quality Monitoring System

Following best practices in quantitative finance (Lopez de Prado, 2018), the model implements comprehensive data quality monitoring:

Data Quality Score = Σ(Individual Indicator Validity) / Total Indicators

Where validity is determined by:

- Non-null data availability

- Positive value validation

- Temporal consistency checks

### 3.3 Statistical Normalization Framework

#### 3.3.1 Z-Score Normalization

The model employs robust Z-score normalization as established by Sharpe (1994) for cross-indicator comparability:

Z_i,t = (X_i,t - μ_i) / σ_i

Where:

- X_i,t = Raw value of indicator i at time t

- μ_i = Sample mean of indicator i

- σ_i = Sample standard deviation of indicator i

Z-scores are capped at ±3 to mitigate outlier influence (Tukey, 1977).

#### 3.3.2 Percentile Rank Transformation

For intuitive interpretation, Z-scores are converted to percentile ranks following the methodology of Conover (1999):

Percentile_Rank = (Number of values < current_value) / Total_observations × 100

### 3.4 Exponential Smoothing Framework

Signal smoothing employs exponential weighted moving averages (Brown, 1963) with adaptive alpha parameter:

S_t = α × X_t + (1-α) × S_{t-1}

Where α = 2/(N+1) and N represents the smoothing period.

### 3.5 Dynamic Threshold Optimization

The model implements adaptive thresholds using Bollinger Band methodology (Bollinger, 1992):

Dynamic_Threshold = μ ± (k × σ)

Where k is the threshold multiplier adjusted for market volatility regime.

### 3.6 Composite Score Calculation

The fundamental score integrates component scores through weighted averaging:

Fundamental_Score = Σ(w_i × Score_i × Quality_i)

Where:

- w_i = Normalized component weight

- Score_i = Component fundamental score

- Quality_i = Data quality adjustment factor

## 4. Implementation Architecture

### 4.1 Adaptive Parameter Framework

The model incorporates regime-specific adjustments based on market volatility:

Volatility_Regime = σ_price / μ_price × 100

High volatility regimes (>25%) trigger enhanced weighting for inventory and sentiment components, reflecting increased market sensitivity to supply disruptions and psychological factors.

### 4.2 Data Synchronization Protocol

Given varying publication frequencies (daily, weekly, monthly), the model employs forward-fill synchronization to maintain temporal alignment across all indicators.

### 4.3 Quality-Adjusted Scoring

Component scores are adjusted for data quality to prevent degraded inputs from contaminating the composite signal:

Adjusted_Score = Raw_Score × Quality_Factor + 50 × (1 - Quality_Factor)

This formulation ensures that poor-quality data reverts toward neutral (50) rather than contributing noise.

## 5. Usage Guidelines and Best Practices

### 5.1 Configuration Recommendations

For Short-term Analysis (1-4 weeks):

- Lookback Period: 26 weeks

- Smoothing Length: 3-5 periods

- Confidence Period: 13 weeks

- Increase inventory and sentiment weights

For Medium-term Analysis (1-3 months):

- Lookback Period: 52 weeks

- Smoothing Length: 5-8 periods

- Confidence Period: 26 weeks

- Balanced component weights

For Long-term Analysis (3+ months):

- Lookback Period: 104 weeks

- Smoothing Length: 8-12 periods

- Confidence Period: 52 weeks

- Increase supply and demand weights

### 5.2 Signal Interpretation Framework

Bullish Signals (Score > 70):

- Fundamental conditions favor price appreciation

- Consider long positions or reduced short exposure

- Monitor for trend confirmation across multiple timeframes

Bearish Signals (Score < 30):

- Fundamental conditions suggest price weakness

- Consider short positions or reduced long exposure

- Evaluate downside protection strategies

Neutral Range (30-70):

- Mixed fundamental environment

- Favor range-bound or volatility strategies

- Wait for clearer directional signals

### 5.3 Risk Management Considerations

1. Data Quality Monitoring: Continuously monitor the data quality dashboard. Scores below 75% warrant increased caution.

2. Regime Awareness: Adjust position sizing based on volatility regime indicators. High volatility periods require reduced exposure.

3. Correlation Analysis: Monitor correlation with crude oil prices to validate model effectiveness.

4. Fundamental-Technical Divergence: Pay attention when fundamental signals diverge from technical indicators, as this may signal regime changes.

### 5.4 Alert System Optimization

Configure alerts conservatively to avoid false signals:

- Set alert threshold at 75+ for high-confidence signals

- Enable data quality warnings to maintain system integrity

- Use trend reversal alerts for early regime change detection

## 6. Model Validation and Performance Metrics

### 6.1 Statistical Validation

The model's statistical robustness is ensured through:

- Out-of-sample testing protocols

- Rolling window validation

- Bootstrap confidence intervals

- Regime-specific performance analysis

### 6.2 Economic Validation

Fundamental accuracy is validated against:

- Energy Information Administration (EIA) official reports

- International Energy Agency (IEA) market assessments

- Commercial inventory data verification

## 7. Limitations and Considerations

### 7.1 Model Limitations

1. Data Dependency: Model performance is contingent on data availability and quality from external sources.

2. US Market Focus: Primary data sources are US-centric, potentially limiting global applicability.

3. Lag Effects: Some fundamental indicators exhibit publication lags that may delay signal generation.

4. Regime Shifts: Structural market changes may require model recalibration.

### 7.2 Market Environment Considerations

The model is optimized for normal market conditions. During extreme events (e.g., geopolitical crises, pandemics), additional qualitative factors should be considered alongside quantitative signals.

## References

Baumeister, C., & Kilian, L. (2016). Forty years of oil price fluctuations: Why the price of oil may still surprise us. *Journal of Economic Perspectives*, 30(1), 139-160.

Bollinger, J. (1992). *Bollinger on Bollinger Bands*. McGraw-Hill.

Brown, R. G. (1963). *Smoothing, Forecasting and Prediction of Discrete Time Series*. Prentice-Hall.

Chen, N. F., Roll, R., & Ross, S. A. (1986). Economic forces and the stock market. *Journal of Business*, 59(3), 383-403.

Conover, W. J. (1999). *Practical Nonparametric Statistics* (3rd ed.). John Wiley & Sons.

Fama, E. F. (1970). Efficient capital markets: A review of theory and empirical work. *Journal of Finance*, 25(2), 383-417.

Hamilton, J. D. (2009). Understanding crude oil prices. *Energy Journal*, 30(2), 179-206.

Kilian, L. (2009). Not all oil price shocks are alike: Disentangling demand and supply shocks in the crude oil market. *American Economic Review*, 99(3), 1053-1069.

Lopez de Prado, M. (2018). *Advances in Financial Machine Learning*. John Wiley & Sons.

Ross, S. A. (1976). The arbitrage theory of capital asset pricing. *Journal of Economic Theory*, 13(3), 341-360.

Sharpe, W. F. (1994). The Sharpe ratio. *Journal of Portfolio Management*, 21(1), 49-58.

Tukey, J. W. (1977). *Exploratory Data Analysis*. Addison-Wesley.

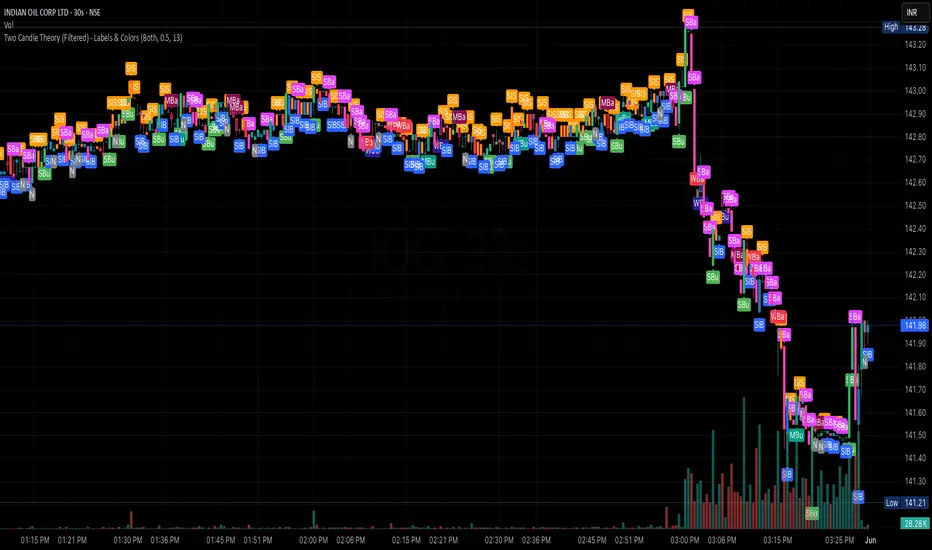

Two Candle Theory (Filtered) - Labels & ColorsOverview

This Pine Script classifies each candle into one of nine sentiment categories based on how the candle closes within its own range and in relation to the previous candle’s high and low. It optionally filters the strongest bullish and bearish signals based on volume spikes.

The script is designed to help traders visually interpret market sentiment through configurable labels and candle colors.

⸻

Classification Logic

Each candle is assessed using two metrics:

1. Close Position – where the candle closes within its own high-low range (High, Mid, Low).

2. Close Comparison – how the current close compares to the previous candle’s high and low (Bull, Bear, or Range).

Based on this, a short label is assigned:

• Bullish Bias: Strongest (SBu), Moderate (MBu), Weak (WBu), Slight (SlB)

• Neutral: Neutral (N)

• Bearish Bias: Slight (SlS), Weak (WBa), Moderate (MBa), Strongest (SBa)

⸻

Volume Filter

A volume spike filter can be applied to the strongest signals:

• SBu and SBa are only shown if volume is significantly higher than the average (SMA × threshold).

• The filter is optional and user-configurable.

⸻

Display Options

Users can control:

• Whether to show labels, bar colors, or both.

• Which of the nine label types are visible.

• Custom colors for each label and corresponding bar.

⸻

Visual Output

• Labels appear above or below candles depending on bullish or bearish classification.

• Bar colors reflect sentiment for quicker visual scanning.

⸻

Use Case

Ideal for identifying momentum shifts, validating trade entries, and highlighting candles that break out of previous ranges with conviction and/or volume.

⸻

Summary

This script simplifies price action by translating each candle into an interpretable sentiment label and color. With optional volume filtering and full display customization, it offers a practical tool for discretionary and systematic traders alike.

COT3 - Flip Strength Index - Invincible3This indicator uses the TradingView COT library to visualize institutional positioning and potential sentiment or trend shifts. It compares the long% vs short% of commercial and non-commercial traders for both Pair A and Pair B, helping traders identify trend strength, market overextension, and early reversal signals.

🔷 COT RSI

The COT RSI normalizes the net positioning difference between non-commercial and commercial traders over (N=13, 26, and 52)-week periods. It ranges from 0 to 100, highlighting when sentiment is at bullish or bearish extremes.

COT RSI (N)= ((NC - C)−min)/(max-min) x100

🟡 COT Index

The COT Index tracks where the current non-commercial net position lies within its 1-year and 3-year historical range. It reflects institutional accumulation or distribution phases.

Strength represents the magnitude of that positioning bias, visualized through normalized RSI-style metrics.

COT Index (N)= (NC net)/(max-min) x100

🔁 Flip Detection

Flip refers to the crossovers between long% and short%, indicating a change in directional bias among trader groups. When long positions exceed shorts (or vice versa), it signals a possible market flip in sentiment or trend.

For example, Pair B commercial flip is calculated as:

Long% = (Long/Open Interest)×100

Short% = (Short/Open Interest)×100

Flip = Long%−Short%

A bullish flip occurs when long% overtakes short%, and vice versa for a bearish flip. These flips often precede price trend changes or confirm sentiment breakouts.

Flip captures how far current positioning deviates from historical norms — highlighting periods of institutional overconfidence or exhaustion, often leading to significant market turns.

This combination offers a multi-layered edge for identifying when smart money is flipping direction, and whether that flip has strong conviction or is likely to fade.

..........................................................................................................................................................

Options Volume ProfileOptions Volume Profile

Introduction

Unlock institutional-level options analysis directly on your charts with Options Volume Profile - a powerful tool designed to visualize and analyze options market activity with precision and clarity. This indicator bridges the gap between technical price action and options flow, giving you a comprehensive view of market sentiment through the lens of options activity.

What Is Options Volume Profile?

Options Volume Profile is an advanced indicator that analyzes call and put option volumes across multiple strikes for any symbol and expiration date available on TradingView. It provides a real-time visual representation of where money is flowing in the options market, helping identify potential support/resistance levels, market sentiment, and possible price targets.

Key Features

Comprehensive Options Data Visualization

Dynamic strike-by-strike volume profile displayed directly on your chart

Real-time tracking of call and put volumes with custom visual styling

Clear display of important value areas including POC (Point of Control)

Value Area High/Low visualization with customizable line styles and colors

BK Daily Range Identification

Secondary lines marking significant volume thresholds

Visual identification of key strike prices with substantial options activity

Value Area Cloud Visualization

Configurable cloud overlays for value areas

Enhanced visual identification of high-volume price zones

Detailed Summary Table

Complete breakdown of call and put volumes per strike

Percentage analysis of call vs put activity for sentiment analysis

Color-coded volume data for instant pattern recognition

Price data for both calls and puts at each strike

Custom Strike Selection

Configure strikes above and below ATM (At The Money)

Flexible strike spacing and rounding options

Custom base symbol support for various options markets

Use Cases

1. Identifying Key Support & Resistance

Visualize where major options activity is concentrated to spot potential support and resistance zones. The POC and Value Area lines often act as magnets for price.

2. Analyzing Market Sentiment

Compare call versus put volume distribution to gauge directional bias. Heavy call volume suggests bullish sentiment, while heavy put volume indicates bearish positioning.

3. Planning Around Institutional Activity

Volume profile analysis reveals where professional traders are positioning themselves, allowing you to align with or trade against smart money.

4. Setting Precise Targets

Use the POC and Value Area High/Low lines as potential profit targets when planning your trades.

5. Spotting Unusual Options Activity

The color-coded volume table instantly highlights anomalies in options flow that may signal upcoming price movements.

Customization Options

The indicator offers extensive customization capabilities:

Symbol & Data Settings : Configure base symbol and data aggregation

Strike Selection : Define number of strikes above/below ATM

Expiration Date Settings : Set specific expiry dates for analysis

Strike Configuration : Customize strike spacing and rounding

Profile Visualization : Adjust offset, width, opacity, and height

Labels & Line Styles : Fully configurable text and visual elements

Value Area Settings : Customize POC and Value Area visualization

Secondary Line Settings : Configure the BK Daily Range appearance

Cloud Visualization : Add colored overlays for enhanced visibility

How to Use

Apply the indicator to your chart

Configure the expiration date to match your trading timeframe

Adjust strike selection and spacing to match your instrument

Use the volume profile and summary table to identify key levels

Trade with confidence knowing where the real money is positioned

Perfect for options traders, futures traders, and anyone who wants to incorporate institutional-level options analysis into their trading strategy.

Take your trading to the next level with Options Volume Profile - where price meets institutional positioning.

Dix$on's Weighted Volume FlowDixson's Weighted Volume Flow

Dixson's Weighted Volume Flow is a technical indicator designed to analyze and visualize the distribution of buy and sell volume within a given timeframe. It dynamically calculates the proportional allocation of volume based on price action within each bar, providing insights into market sentiment and activity. This indicator displays horizontal volume bars in a separate pane and annotates them with precise volume values.

How It Works

1. Volume Allocation:

- The indicator calculates buy and sell volume using the following formulas:

- Buy Volume = (Close - Low) / (High - Low) Total Volume

- Sell Volume = (High - Close) / (High - Low) Total Volume

- These formulas allocate volume proportionally based on the bar's price range, attributing more volume to buying or selling depending on the relationship between the close, high, and low prices.

2. Dynamic Scaling:

- The buy and sell volumes are scaled relative to their combined total for the period.

- The resulting values determine the length of the horizontal bars, providing a comparative view of buy and sell activity.

3. Bar Visualization:

- Buy Volume Bars: Displayed as green horizontal bars.

- Sell Volume Bars: Displayed as red horizontal bars.

- The lengths of the bars represent the dominance of buy or sell volume, scaled dynamically within the pane.

4. Labels:

- Each bar is annotated with a label showing its calculated buy or sell volume value.

5. Timeframe Adjustment:

- The indicator uses the request.security() function to fetch data from the selected timeframe, allowing users to customize their analysis for intraday, daily, or longer-term trends.

6. Customization Options:

- Enable or disable the indicator using a toggle.

- Adjust colors for the buy/sell bars and text labels to suit your chart theme.

How to Use It

1. Enable the Indicator:

- Activate the indicator using the "Enable/Disable" toggle in the settings.

2. Select a Timeframe:

- Choose the timeframe for analysis (e.g., 1-minute, 1-hour, daily). The indicator fetches volume data specific to the selected timeframe.

3. Interpret the Visualization:

- Compare Bar Lengths:

- Longer buy volume bars (green) indicate stronger buying activity.

- Longer sell volume bars (red) suggest dominant selling pressure.

- Labels:

- Use the labels to view the exact buy and sell volume values for precise analysis.

4. Combine with Other Tools:

- Use the indicator alongside price action analysis, support/resistance levels, or trend indicators to confirm market sentiment and detect potential reversals.

5. Monitor Imbalances:

- Significant disparities between buy and sell volume can signal shifts in market sentiment, such as the end of a trend or the start of a breakout.

Practical Applications

- Trend Confirmation:

- Align the dominance of buy or sell volume with price trends to confirm market direction.

- Reversal Signals:

- Watch for volume imbalances or a sudden shift in the dominance of buy or sell volume to identify potential reversals.

- High-Activity Zones:

- Identify areas with increased volume to anticipate significant price movements or key support/resistance interactions.

Dixson's Weighted Volume Flow provides a clear and systematic way to analyze market activity by visualizing the dynamics of buy and sell volume. It is particularly useful for traders looking to enhance their understanding of volume-based sentiment and its impact on price movements.

Day Open vs Previous Day CloseThe concept of comparing the **Day Open** to the **Previous Day Close** is used frequently in technical analysis to gauge the sentiment or momentum at the start of a new trading day.

### Key Terms:

- **Day Open**: The first traded price of an asset when the market opens for the day.

- **Previous Day Close**: The last traded price of an asset when the market closed on the previous day.

### Importance of Day Open vs. Previous Day Close

1. **Market Sentiment Indicator**:

- If the **Day Open** is **higher** than the **Previous Day Close**, it suggests **bullish** sentiment (buyers are willing to pay more than yesterday's closing price).

- If the **Day Open** is **lower** than the **Previous Day Close**, it suggests **bearish** sentiment (sellers are driving prices down compared to the last price from the previous day).

2. **Potential Gaps**:

- A **gap** occurs when there is a significant difference between the Day Open and Previous Day Close, often due to events or news released after the market closed. This gap can indicate strong momentum in either direction.

- **Gap Up**: Open > Close (bullish).

- **Gap Down**: Open < Close (bearish).

3. **Trend Continuation or Reversal**:

- If the market opens above the previous day’s close and continues to rise, it often signals a **continuation of an upward trend**.

- Conversely, if the market opens below and keeps falling, it suggests **downward momentum** is still strong.

4. **Trading Strategies**:

- **Opening Range Breakout**: Traders may look for the price to break above or below the opening range (the price range between the Day Open and the first few candles) to confirm a strong bullish or bearish move.

- **Reversals**: Some traders look for price reversals if the price spikes far above or below the previous day's close, expecting that the market might correct itself and return towards the previous day’s closing levels.

In the context of your **Opening Range Indicator**, the concept of the Day Open sweeping and closing above or below the Previous Day Close is used to identify whether the new day is setting up for a **buy (bullish)** or **sell (bearish)** opportunity.

COT INDEX v2The **Commitment of Traders (COT)** report is a valuable tool for analyzing market sentiment, providing insight into the positions of futures traders at the close of the Tuesday trading session. Prepared by the Commodity Futures Trading Commission (CFTC), the report is published every Friday at 3:30 p.m. Eastern Time, and the data is freely available on the CFTC website.

Traders are categorized into three groups: **Commercial Traders**, **Non-Commercial Traders** (large speculators), and **Nonreportable** (small speculators). This information can be applied to charts to visualize the direction of the positions held by major market participants and to receive key COT signals.

The **COT index** ranges from 0% to 100%, reflecting market sentiment over the past 26 weeks. Extreme values, below 25% or above 75%, represent bearish or bullish sentiment, respectively. However, it is important to note that the COT index is not a timing tool but rather an indicator of the overall sentiment of major market players.

For a more tailored analysis, you can adjust the period for index calculation, customize chart styles, and highlight extreme areas.

Fear/Greed Zone Reversals [UAlgo]The "Fear/Greed Zone Reversals " indicator is a custom technical analysis tool designed for TradingView, aimed at identifying potential reversal points in the market based on sentiment zones characterized by fear and greed. This indicator utilizes a combination of moving averages, standard deviations, and price action to detect when the market transitions from extreme fear to greed or vice versa. By identifying these critical turning points, traders can gain insights into potential buy or sell opportunities.

🔶 Key Features

Customizable Moving Averages: The indicator allows users to select from various types of moving averages (SMA, EMA, WMA, VWMA, HMA) for both fear and greed zone calculations, enabling flexible adaptation to different trading strategies.

Fear Zone Settings:

Fear Source: Select the price data point (e.g., close, high, low) used for Fear Zone calculations.

Fear Period: This defines the lookback window for calculating the Fear Zone deviation.

Fear Stdev Period: This sets the period used to calculate the standard deviation of the Fear Zone deviation.

Greed Zone Settings:

Greed Source: Select the price data point (e.g., close, high, low) used for Greed Zone calculations.

Greed Period: This defines the lookback window for calculating the Greed Zone deviation.

Greed Stdev Period: This sets the period used to calculate the standard deviation of the Greed Zone deviation.

Alert Conditions: Integrated alert conditions notify traders in real-time when a reversal in the fear or greed zone is detected, allowing for timely decision-making.

🔶 Interpreting Indicator

Greed Zone: A Greed Zone is highlighted when the price deviates significantly above the chosen moving average. This suggests market sentiment might be leaning towards greed, potentially indicating a selling opportunity.

Fear Zone Reversal: A Fear Zone is highlighted when the price deviates significantly below the chosen moving average of the selected price source. This suggests market sentiment might be leaning towards fear, potentially indicating a buying opportunity. When the indicator identifies a reversal from a fear zone, it suggests that the market is transitioning from a period of intense selling pressure to a more neutral or potentially bullish state. This is typically indicated by an upward arrow (▲) on the chart, signaling a potential buy opportunity. The fear zone is characterized by high price volatility and overselling, making it a crucial point for traders to consider entering the market.

Greed Zone Reversal: Conversely, a Greed Zone is highlighted when the price deviates significantly above the chosen moving average. This suggests market sentiment might be leaning towards greed, potentially indicating a selling opportunity. When the indicator detects a reversal from a greed zone, it indicates that the market may be moving from an overbought condition back to a more neutral or bearish state. This is marked by a downward arrow (▼) on the chart, suggesting a potential sell opportunity. The greed zone is often associated with overconfidence and high buying activity, which can precede a market correction.

🔶 Why offer multiple moving average types?

By providing various moving average types (SMA, EMA, WMA, VWMA, HMA) , the indicator offers greater flexibility for traders to tailor the indicator to their specific trading strategies and market preferences. Different moving averages react differently to price data and can produce varying signals.

SMA (Simple Moving Average): Provides an equal weighting to all data points within the specified period.

EMA (Exponential Moving Average): Gives more weight to recent data points, making it more responsive to price changes.

WMA (Weighted Moving Average): Allows for custom weighting of data points, providing more flexibility in the calculation.

VWMA (Volume Weighted Moving Average): Considers both price and volume data, giving more weight to periods with higher trading volume.

HMA (Hull Moving Average): A combination of weighted moving averages designed to reduce lag and provide a smoother curve.

Offering multiple options allows traders to:

Experiment: Traders can try different moving averages to see which one produces the most accurate signals for their specific market.

Adapt to different market conditions: Different market conditions may require different moving average types. For example, a fast-moving market might benefit from a faster moving average like an EMA, while a slower-moving market might be better suited to a slower moving average like an SMA.

Personalize: Traders can choose the moving average that best aligns with their personal trading style and risk tolerance.

In essence, providing a variety of moving average types empowers traders to create a more personalized and effective trading experience.

🔶 Disclaimer

Use with Caution: This indicator is provided for educational and informational purposes only and should not be considered as financial advice. Users should exercise caution and perform their own analysis before making trading decisions based on the indicator's signals.

Not Financial Advice: The information provided by this indicator does not constitute financial advice, and the creator (UAlgo) shall not be held responsible for any trading losses incurred as a result of using this indicator.

Backtesting Recommended: Traders are encouraged to backtest the indicator thoroughly on historical data before using it in live trading to assess its performance and suitability for their trading strategies.

Risk Management: Trading involves inherent risks, and users should implement proper risk management strategies, including but not limited to stop-loss orders and position sizing, to mitigate potential losses.

No Guarantees: The accuracy and reliability of the indicator's signals cannot be guaranteed, as they are based on historical price data and past performance may not be indicative of future results.

SVMKR_VIX_Based_LevelsThe "SVMKR_VIX_Based_Levels" script is a Pine Script indicator designed to assist intraday traders in identifying dynamic support and resistance levels based on the Volatility Index (VIX). Here's a breakdown of the script and its uses for intraday traders:

### Script Description:

1. **Data Retrieval**: