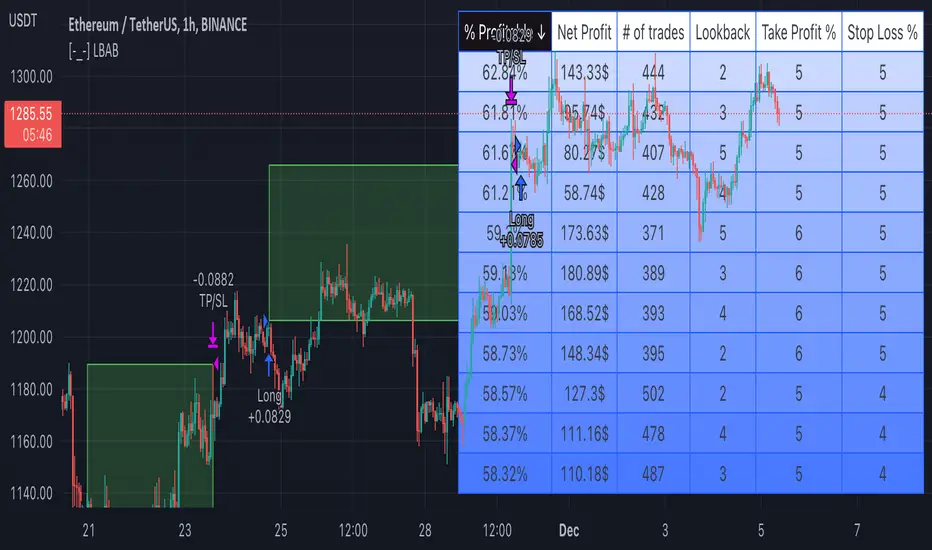

[-_-] Level Breakout, Auto Backtesting StrategyDescription:

A Long only strategy based on breakout from a certain level formed by High price. It has auto-backtesting capabilities (you set ranges for the three main parameters: Lookback, TP and SL; the strategy then goes through different combinations of those parameters and displays a table with results that you can sort by Percentage of profitable trades AND/OR Net profit AND/OR Number of trades). So you can, for example, sort only by Net profit to find combination of parameters that gives highest net profit, or sort by Net profit and Percentage profitable to find a combination of parameters that gives the best balance between profitability and profit. The auto-backtesting also takes into account the commission which is set in % in the inputs (make sure to set the same value in properties of the strategy so that auto-backtesting and real backtesting results match).

NOTE: auto-backtesting only find the best combinations and displays them in a table, you will then need to manually set the Lookback, TP and SL inputs for real backtesting to match.

Parameters:

- Lookback -> # of bars for filtering signals; recommended range from 2 to 5

- TP (%) -> take profit; recommended range from 5 to 10

- SL (%) -> stop loss; recommended range from 1 to 5

- Commission (%) -> commission per trade

- Min/Max Lookback -> lookback range for auto-backtesting

- Min/Max TP -> take profit range for auto-backtesting

- Min/Max SL -> stop loss range for auto-backtesting

- Percentage profitable -> sort by percentage of profitable trades

- Net profit -> sort by net profit

- Number of trades -> sort by number of trades

스크립트에서 "range"에 대해 찾기

Hanzo Strategy - Volume & Smart Money📊 HANZO STRATEGY - Complete Description

## 🎯 Strategy Overview

The **Hanzo Strategy** is an advanced institutional trading system that combines Volume Profile analysis, Smart Money Concepts, and Price Action patterns to identify high-probability trade setups. This strategy is specifically designed for trading Gold (XAUUSD), NAS100, and US30 on the 15-minute timeframe.

---

## 🧠 Core Trading Philosophy

The Hanzo Strategy operates on the principle that **institutional money leaves footprints** in the market through:

- Volume accumulation at key price levels

- Liquidity sweeps and stop hunts

- Order block formations

- Strategic wick rejections at support/resistance

By identifying these institutional behaviors and combining them with precise volume analysis, the strategy aims to trade **with** the smart money, not against it.

---

## 🔑 Key Components

### 1️⃣ **Fixed Range Volume Profile (FRVP)**

- **What it does:** Analyzes the last 2 days of price action and calculates where the most volume traded

- **Point of Control (POC):** The price level with the highest trading volume - acts as a magnet for price

- **How we use it:** Price tends to revert to POC. When price is far from POC and starts moving toward it, we prepare for entries

- **Visual:** Yellow cross line on the chart marking the POC

### 2️⃣ **Wick Cluster Detection**

- **What it does:** Automatically identifies price levels where multiple candle wicks have rejected (2-6+ wicks)

- **Why it matters:** Multiple rejections at the same level indicate strong institutional support/resistance

- **Upper wick clusters:** Resistance zones where price was rejected downward

- **Lower wick clusters:** Support zones where price was rejected upward

- **Visual:** Dashed lines (red for resistance, green for support)

### 3️⃣ **Session Volatility Boxes**

- **London Session (8:00-16:00 UTC+3):** Captures European market volatility range

- **New York Session (13:30-20:00 UTC+3):** Captures US market volatility range

- **How we use it:** These ranges often act as support/resistance for the rest of the day

- **Visual:** Blue box for London, Orange box for New York

### 4️⃣ **Smart Money Zones**

**Order Blocks:**

- Strong institutional areas where banks and hedge funds placed large orders

- **Bullish Order Block:** Area where smart money bought heavily before a strong upward move

- **Bearish Order Block:** Area where smart money sold heavily before a strong downward move

- **Visual:** Green/Red filled boxes with "Bull OB" or "Bear OB" labels

**Liquidity Sweeps:**

- Price breaks above recent high or below recent low, then quickly reverses

- This is a "stop hunt" - institutions triggering retail stops before moving in the real direction

- **Bullish Sweep:** Price dips below support, grabs stops, then reverses up

- **Bearish Sweep:** Price pops above resistance, grabs stops, then reverses down

- **Visual:** Triangle markers (green up = bullish, red down = bearish)

### 5️⃣ **Engulfing Pattern Recognition**

- **Bullish Engulfing:** Large green candle fully engulfs the previous red candle - shows strong buying pressure

- **Bearish Engulfing:** Large red candle fully engulfs the previous green candle - shows strong selling pressure

- **How we use it:** Confirmation signal when combined with other factors

- **Visual:** Small circles below/above candles

### 6️⃣ **Trend Bias Indicator**

- Dynamically calculates market bias based on price position relative to POC

- **Bullish:** Price > 0.2% above POC

- **Neutral:** Price within 0.2% of POC

- **Bearish:** Price > 0.2% below POC

- **Visual:** Label at top of chart showing current bias

---

## 📈 Entry Signal Logic

The strategy generates **LONG** and **SHORT** signals based on confluence of multiple factors:

### 🟢 LONG ENTRY CONDITIONS:

1. **POC Break:** Price crosses above POC from below + Trend Bias is Bullish

**OR**

2. **Support Bounce:** Price touches a lower wick cluster + Bullish Engulfing pattern forms

3. **Additional Filter:** Trend Bias must NOT be Bearish

### 🔴 SHORT ENTRY CONDITIONS:

1. **POC Break:** Price crosses below POC from above + Trend Bias is Bearish

**OR**

2. **Resistance Rejection:** Price touches an upper wick cluster + Bearish Engulfing pattern forms

3. **Additional Filter:** Trend Bias must NOT be Bullish

---

## 🎯 Risk Management

### Stop Loss:

- **Calculation:** 2 × ATR(14) from entry price

- **Logic:** Uses Average True Range to adapt to current market volatility

- **Example:** If ATR = 10 points, stop loss is 20 points away

### Take Profit:

- **Calculation:** 3 × ATR(14) from entry price

- **Risk:Reward Ratio:** 1:1.5 (risking 2 ATR to make 3 ATR)

- **Example:** If ATR = 10 points, take profit is 30 points away

### Position Sizing:

- **Default:** 2% of account equity per trade

- **Adjustable:** Can be modified in strategy settings

---

## ⚙️ Strategy Settings & Customization

### Volume Profile Settings:

- **Lookback Days:** How many days to analyze (default: 2)

- **Profile Rows:** Resolution of volume calculation (default: 24)

- **POC Distance Threshold:** Minimum distance from POC for "far from POC" status (default: 0.3%)

### Wick Cluster Settings:

- **Min Wicks for Cluster:** How many wicks needed to form a cluster (default: 3)

- **Lookback Bars:** How far back to search for wicks (default: 50)

- **Tolerance %:** How close wicks must be to cluster together (default: 0.15%)

### Session Settings:

- **London Session:** 08:00-16:00 (adjustable)

- **New York Session:** 13:30-20:00 (adjustable)

- **UTC Offset:** Timezone adjustment (default: +3)

### Smart Money Settings:

- **Order Block Lookback:** How far back to search for order blocks (default: 20)

- **Toggle On/Off:** Can enable/disable order blocks and liquidity sweeps independently

---

## 📊 Performance Metrics Display

The strategy includes a real-time **Information Table** (top-right corner) showing:

| Metric | Description |

|--------|-------------|

| **Trend Bias** | Current market direction (Bullish/Neutral/Bearish) |

| **POC Price** | Current Point of Control price level |

| **Distance from POC** | How far current price is from POC (%) |

| **ATR (14)** | Current volatility measurement |

| **High Wick Clusters** | Number of resistance clusters detected |

| **Low Wick Clusters** | Number of support clusters detected |

| **Current Signal** | Active signal (LONG/SHORT/None) |

---

## 🚨 Alert System

The strategy can send alerts for:

1. **LONG Signal Triggered** - When all conditions met for long entry

2. **SHORT Signal Triggered** - When all conditions met for short entry

3. **Price Touching Support Cluster** - Warning that price at key support

4. **Price Touching Resistance Cluster** - Warning that price at key resistance

**Alert Frequency:** Once per bar (prevents spam)

---

## 📅 Best Trading Timeframes & Instruments

### ✅ Recommended Timeframes:

- **Primary Entry:** 15-minute chart

- **Trend Confirmation:** 30-minute or 1-hour chart

- **Higher Timeframe Filter:** 4-hour for major trend direction

### ✅ Recommended Instruments:

1. **Gold (XAUUSD)** - High volatility, respects key levels well

2. **NAS100 (US Tech 100)** - Strong trends, good liquidity

3. **US30 (Dow Jones)** - Reliable institutional participation

4. **EUR/USD, GBP/USD** - Can work on major forex pairs with adjustments

### ⏰ Best Trading Sessions:

- **London Open (08:00-12:00 UTC+3)** - High volatility, clear directional moves

- **New York Open (13:30-17:00 UTC+3)** - Strongest moves, highest volume

- **Overlap (13:30-16:00 UTC+3)** - Best liquidity and movement

### ⚠️ Avoid Trading:

- Asian session (low volatility)

- Major news events (first 15 minutes after high-impact news)

- Sundays and holidays (low liquidity)

---

## 💡 Pro Trading Tips

### 1. **Multiple Timeframe Confirmation**

- Check 1-hour chart for overall trend before taking 15-minute signals

- Only take LONG signals if 1-hour is bullish

- Only take SHORT signals if 1-hour is bearish

### 2. **POC Strategy**

- Best entries occur when price returns to POC after being far away

- Wait for POC touch + confirmation pattern (engulfing, order block)

- POC acts as support in uptrends, resistance in downtrends

### 3. **Wick Cluster Strategy**

- Strongest signals occur when wick clusters align with POC

- Look for 4+ wicks at the same level for highest probability

- Recent clusters (formed in last 2 days) are stronger than old ones

### 4. **Order Block Strategy**

- Fresh order blocks (just formed) are more powerful

- Wait for price to return to order block zone before entering

- Best when order block + wick cluster occur at same level

### 5. **London/NY Box Strategy**

- If price breaks above session high → look for LONG pullback entries

- If price breaks below session low → look for SHORT pullback entries

- Price often returns to session mid-point before continuing

### 6. **Risk Management Rules**

- **Never risk more than 2% per trade**

- **Don't trade more than 3 positions simultaneously**

- **If 2 losses in a row, reduce size to 1% or stop for the day**

- **Move stop to breakeven after 1:1 profit reached**

### 7. **High-Probability Setups**

Look for **CONFLUENCE** - the more factors aligned, the better:

✅ **BEST LONG SETUP:**

- Price at lower wick cluster (support)

- Price at/near POC

- Bullish order block present

- Bullish engulfing pattern forms

- Trend Bias = Bullish

- 1-hour chart = uptrend

✅ **BEST SHORT SETUP:**

- Price at upper wick cluster (resistance)

- Price at/near POC

- Bearish order block present

- Bearish engulfing pattern forms

- Trend Bias = Bearish

- 1-hour chart = downtrend

---

## 📈 Performance Expectations

### Typical Win Rate:

- **Conservative Trading (high confluence only):** 55-65% win rate

- **Moderate Trading (good setups):** 45-55% win rate

- **Aggressive Trading (all signals):** 35-45% win rate

### Typical Risk:Reward:

- **Average R:R:** 1:1.5 (with 2 ATR stop and 3 ATR target)

- **Breakeven adjusted:** Often improves to 1:2+ when stop moved to BE

### Monthly Trade Frequency (15M chart):

- **Gold:** 60-100 signals per month

- **NAS100:** 50-80 signals per month

- **US30:** 40-70 signals per month

---

## 🎓 Strategy Philosophy Summary

The Hanzo Strategy is built on three core principles:

1. **Follow the Volume** - Trade where institutions are active

2. **Respect the Levels** - Key support/resistance zones matter

3. **Confirm with Price Action** - Wait for confirmation before entering

This is NOT a holy grail - it requires:

- ✅ Discipline to wait for proper setups

- ✅ Patience to let trades play out

- ✅ Risk management to protect capital

- ✅ Emotional control to handle losses

---

## 🛠️ How to Use This Strategy

### Step 1: Initial Setup

1. Add strategy to 15-minute chart

2. Check that all components are visible (POC, clusters, boxes, etc.)

3. Adjust colors if needed for your chart theme

### Step 2: Daily Routine

1. **Pre-Market (before 8:00 AM):**

- Check POC location

- Note wick clusters from previous days

- Mark London/NY session boxes from yesterday

2. **London Session (8:00-16:00):**

- Watch for POC interactions

- Monitor for order blocks forming

- Wait for confluence setups

3. **NY Session (13:30-20:00):**

- Highest activity period

- Best signal quality

- More aggressive entries allowed

### Step 3: Trade Execution

1. Wait for signal label (LONG or SHORT) to appear

2. Check confluence factors (minimum 3)

3. Enter immediately or on next candle

4. Set stop loss at 2 × ATR from entry

5. Set take profit at 3 × ATR from entry

6. Move stop to breakeven at +1.5 ATR profit

### Step 4: Trade Management

- **Don't move stop closer** (let trade breathe)

- **Can trail stop** after 2:1 profit reached

- **Can take partial profits** at 1.5:1 and let rest run

- **Journal every trade** for future improvement

---

## ⚠️ Important Disclaimers

1. **Past performance does not guarantee future results**

2. **This strategy involves risk** - only trade with money you can afford to lose

3. **Backtest thoroughly** on your specific instruments before live trading

4. **Start small** - test with minimum position sizes first

5. **Market conditions change** - what works today may not work tomorrow

6. **Use proper risk management** - this is the #1 key to long-term success

---

## 🎯 Quick Reference Checklist

Before taking any trade, ask yourself:

- ✅ Is there a clear LONG or SHORT signal?

- ✅ Are we in London or NY session?

- ✅ Is price at/near POC or wick cluster?

- ✅ Is trend bias aligned with my direction?

- ✅ Is there an order block or engulfing pattern?

- ✅ Is my risk:reward at least 1:1.5?

- ✅ Am I risking no more than 2% of my account?

**If 5+ are YES → Take the trade!**

**If 3 or fewer YES → Skip and wait for better setup!**

---

## 🚀 Final Words

The Hanzo Strategy is a professional-grade trading system that combines institutional analysis with precise technical execution. Success comes not from taking every signal, but from taking only the **highest probability setups** with proper risk management.

**Trade smart. Trade safe. Trade like an institution.**

📊 **Good luck and profitable trading!** 📊

Hash Supertrend [Hash Capital Research]Hash Supertrend Strategy by Hash Capital Research

Overview

Hash Supertrend is a professional-grade trend-following strategy that combines the proven Supertrend indicator with institutional visual design and flexible time filtering.

The strategy uses ATR-based volatility bands to identify trend direction and executes position reversals when the trend flips.This implementation features a distinctive fluorescent color system with customizable glow effects, making trend changes immediately visible while maintaining the clean, professional aesthetic expected in quantitative trading environments.

Entry Signals:

Long Entry: Price crosses above the Supertrend line (trend flips bullish)

Short Entry: Price crosses below the Supertrend line (trend flips bearish)

Controls the lookback period for volatility calculation

Lower values (7-10): More sensitive to price changes, generates more signals

Higher values (12-14): Smoother response, fewer signals but potentially delayed entries

Recommended range: 7-14 depending on market volatility

Factor (Default: 3.0)

Restricts trading to specific hours

Useful for avoiding low-liquidity sessions, overnight gaps, or known choppy periods

When disabled, strategy trades 24/7

Start Hour (Default: 9) & Start Minute (Default: 30)

Define when the trading session begins

Uses exchange timezone in 24-hour format

Example: 9:30 = 9:30 AM

End Hour (Default: 16) & End Minute (Default: 0)

Controls the vibrancy of the fluorescent color system

1-3: Subtle, muted colors

4-6: Balanced, moderate saturation

7-10: Bright, highly saturated fluorescent appearance

Affects both the Supertrend line and trend zones

Glow Effect (Default: On)

Adds luminous halo around the Supertrend line

Creates a multi-layered visual with depth

Particularly effective during strong trends

Glow Intensity (Default: 5.0)

Displays tiny fluorescent dots at entry points

Green dot below bar: Long entry

Red dot above bar: Short entry

Provides clear visual confirmation of executed trades

Show Trend Zone (Default: On)

Strong trending markets (2020-style bull runs, sustained bear markets)

Markets with clear directional bias

Instruments with consistent volatility patterns

Timeframes: 15m to Daily (optimal on 1H-4H)

Challenging Conditions:

Choppy, range-bound markets

Low volatility consolidation periods

Highly news-driven instruments with frequent gaps

Very low timeframes (1m-5m) prone to noise

Recommended AssetsCryptocurrency:

ATH대비 지정하락률에 도착 시 매수 - 장기홀딩 선물 전략(ATH Drawdown Re-Buy Long Only)본 스크립트는 과거 하락 데이터를 이용하여, 정해진 하락 %가 발생하는 경우 자기 자본의 정해진 %만큼을 진입하게 설계되어진 스트레티지입니다.

레버리지를 사용할 수 있으며 기본적으로 셋팅해둔 값이 내장되어있습니다.(자유롭게 바꿔서 쓰시면 됩니다.) 추가적으로 2번의 진입 외에도 다른 진입 기준, 진입 %를 설정하실 수 있으며 - ChatGPT에게 요청하면 수정해줄 것입니다.

실제 사용용도로는 KillSwitch 기능을 꺼주세요. 바 돋보기 기능을 켜주세요.

ATH Drawdown Re-Buy Long Only 전략 설명

1. 전략 개요

ATH Drawdown Re-Buy Long Only 전략은 자산의 역대 최고가(ATH, All-Time High)를 기준으로 한 하락폭(드로우다운)을 활용하여,

특정 구간마다 단계적으로 롱 포지션을 구축하는 자동 재매수(Long Only) 전략입니다.

본 전략은 다음과 같은 목적을 가지고 설계되었습니다.

급격한 조정 구간에서 체계적인 분할 매수 및 레버리지 활용

ATH를 기준으로 한 명확한 진입 규칙 제공

실시간으로

평단가

레버리지

청산가 추정

계좌 MDD

수익률

등을 시각적으로 제공하여 리스크와 포지션 상태를 직관적으로 확인할 수 있도록 지원

※ 본 전략은 교육·연구·백테스트 용도로 제공되며,

어떠한 형태의 투자 권유 또는 수익을 보장하지 않습니다.

2. 전략의 핵심 개념

2-1. ATH(역대 최고가) 기준 드로우다운

전략은 차트 상에서 항상 가장 높은 고가(High)를 ATH로 기록합니다.

새로운 고점이 형성될 때마다 ATH를 갱신하고, 해당 ATH를 기준으로 다음을 계산합니다.

현재 바의 저가(Low)가 ATH에서 몇 % 하락했는지

현재 바의 종가(Close)가 ATH에서 몇 % 하락했는지

그리고 사전에 설정한 두 개의 드로우다운 구간에서 매수를 수행합니다.

1차 진입 구간: ATH 대비 X% 하락 시

2차 진입 구간: ATH 대비 Y% 하락 시

각 구간은 ATH가 새로 갱신될 때마다 한 번씩만 작동하며,

새로운 ATH가 생성되면 다시 “1차 / 2차 진입 가능 상태”로 초기화됩니다.

2-2. 첫 포지션 100% / 300% 특수 규칙

이 전략의 중요한 특징은 **“첫 포지션 진입 시의 예외 규칙”**입니다.

전략이 현재 어떠한 포지션도 들고 있지 않은 상태에서

최초로 롱 포지션을 진입하는 시점(첫 포지션)에 대해:

기본적으로는 **자산의 100%**를 기준으로 포지션을 구축하지만,

만약 그 순간의 가격이 ATH 대비 설정값 이상(예: 약 –72.5% 이상 하락한 상황) 이라면

→ 자산의 300% 규모로 첫 포지션을 진입하도록 설계되어 있습니다.

이 규칙은 다음과 같이 동작합니다.

첫 진입이 1차 드로우다운 구간에서 발생하든,

첫 진입이 2차 드로우다운 구간에서 발생하든,

현재 하락폭이 설정된 기준 이상(예: –72.5% 이상) 이라면

→ “이 정도 하락이면 첫 진입부터 더 공격적으로 들어간다”는 의미로 300% 규모로 진입

그 이하의 하락폭이라면

→ 첫 진입은 100% 규모로 제한

즉, 전략은 다음 두 가지 모드로 동작합니다.

일반적인 상황의 첫 진입: 자산의 100%

심각한 드로우다운 구간에서의 첫 진입: 자산의 300%

이 특수 규칙은 깊은 하락에서는 공격적으로, 평소에는 상대적으로 보수적으로 진입하도록 설계된 것입니다.

3. 전략 동작 구조

3-1. 매수 조건

차트 상 High 기준으로 ATH를 추적합니다.

각 바마다 해당 ATH에서의 하락률을 계산합니다.

사용자가 설정한 두 개의 드로우다운 구간(예시):

1차 구간: 예를 들어 ATH – 50%

2차 구간: 예를 들어 ATH – 72.5%

각 구간에 대해 다음과 같은 조건을 확인합니다.

“이번 ATH 구간에서 아직 해당 구간 매수를 한 적이 없는 상태”이고,

현재 바의 저가(Low)가 해당 구간 가격 이하를 찍는 순간

→ 해당 바에서 매수 조건 충족으로 간주

실제 주문은:

해당 구간 가격에 맞춰 롱 포지션 진입(리밋/시장가 기반 시뮬레이션) 으로 처리됩니다.

3-2. ATH 갱신과 진입 기회 리셋

차트 상에서 새로운 고점(High)이 기존 ATH를 넘어서는 순간,

ATH가 갱신되고,

1차 / 2차 진입 여부를 나타내는 내부 플래그가 초기화됩니다.

이를 통해, 시장이 새로운 고점을 돌파해 나갈 때마다,

해당 구간에서 다시 한 번씩 1차·2차 드로우다운 진입 기회를 갖게 됩니다.

4. 포지션 사이징 및 레버리지

4-1. 계좌 자산(Equity) 기준 포지션 크기 결정

전략은 현재 계좌 자산을 다음과 같이 정의하여 사용합니다.

현재 자산 = 초기 자본 + 실현 손익 + 미실현 손익

각 진입 구간에서의 포지션 가치는 다음과 같이 결정됩니다.

1차 진입 구간:

“자산의 몇 %를 사용할지”를 설정값으로 입력

설정된 퍼센트를 계좌 자산에 곱한 뒤,

다시 전략 내 레버리지 배수(Leverage) 를 곱하여 실제 포지션 가치를 계산

2차 진입 구간:

동일한 방식으로, 독립된 퍼센트 설정값을 사용

즉, 포지션 가치는 다음과 같이 계산됩니다.

포지션 가치 = 현재 자산 × (해당 구간 설정 % / 100) × 레버리지 배수

그리고 이를 해당 구간의 진입 가격으로 나누어 실제 수량(토큰 단위) 를 산출합니다.

4-2. 첫 포지션의 예외 처리 (100% / 300%)

첫 포지션에 대해서는 위의 일반적인 퍼센트 설정 대신,

다음과 같은 고정 비율이 사용됩니다.

기본: 자산의 100% 규모로 첫 포지션 진입

단, 진입 시점의 ATH 대비 하락률이 설정값 이상(예: –72.5% 이상) 일 경우

→ 자산의 300% 규모로 첫 포지션 진입

이때 역시 다음 공식을 사용합니다.

포지션 가치 = 현재 자산 × (100% 또는 300%) × 레버리지

그리고 이를 가격으로 나누어 실제 진입 수량을 계산합니다.

이 규칙은:

첫 진입이 1차 구간이든 2차 구간이든 동일하게 적용되며,

“충분히 깊은 하락 구간에서는 첫 진입부터 더 크게,

평소에는 비교적 보수적으로” 라는 운용 철학을 반영합니다.

4-3. 실레버리지(Real Leverage)의 추적

전략은 각 바 단위로 다음을 추적합니다.

바가 시작할 때의 기존 포지션 크기

해당 바에서 새로 진입한 수량

이를 바탕으로, 진입이 발생한 시점에 다음을 계산합니다.

실제 레버리지 = (포지션 가치 / 현재 자산)

그리고 차트 상에 예를 들어:

Lev 2.53x 와 같은 형식의 레이블로 표시합니다.

이를 통해, 매수 시점마다 실제 계좌 레버리지가 어느 정도였는지를 직관적으로 확인할 수 있습니다.

5. 시각화 및 모니터링 요소

5-1. 차트 상 시각 요소

전략은 차트 위에 다음과 같은 정보를 직접 표시합니다.

ATH 라인

High 기준으로 계산된 역대 최고가를 주황색 선으로 표시

평단가(평균 진입가) 라인

현재 보유 포지션이 있을 때,

해당 포지션의 평균 진입가를 노란색 선으로 표시

추정 청산가(고정형 청산가) 라인

포지션 수량이 변화하는 시점을 감지하여,

당시의 평단가와 실제 레버리지를 이용해 근사적인 청산가를 계산

이를 빨간색 선으로 차트에 고정 표시

포지션이 없거나 레버리지가 1배 이하인 경우에는 청산가 라인을 제거

매수 마커 및 레이블

1차/2차 매수 조건이 충족될 때마다 해당 지점에 매수 마커를 표시

"Buy XX% @ 가격", "Lev XXx" 형태의 라벨로

진입 비율과 당시 레버리지를 함께 시각화

레이블의 위치는 설정에서 선택 가능:

바 아래 (Below Bar)

바 위 (Above Bar)

실제 가격 위치 (At Price)

5-2. 우측 상단 정보 테이블

차트 우측 상단에는 현재 계좌·포지션 상태를 요약한 정보 테이블이 표시됩니다.

대표적으로 다음 항목들이 포함됩니다.

Pos Qty (Token)

현재 보유 중인 포지션 수량(토큰 기준, 절대값 기준)

Pos Value (USDT)

현재 포지션의 시장 가치 (수량 × 현재 가격)

Leverage (Now)

현재 실레버리지 (포지션 가치 / 현재 자산)

DD from ATH (%)

현재 가격 기준, 최근 ATH에서의 하락률(%)

Avg Entry

현재 포지션의 평균 진입 가격

PnL (%)

현재 포지션 기준 미실현 손익률(%)

Max DD (Equity %)

전략 전체 기간 동안 기록된 계좌 기준 최대 손실(MDD, Max Drawdown)

Last Entry Price

가장 최근에 포지션을 추가로 진입한 직후의 평균 진입 가격

Last Entry Lev

위 “Last Entry Price” 시점에서의 실레버리지

Liq Price (Fixed)

위에서 설명한 고정형 추정 청산가

Return from Start (%)

전략 시작 시점(초기 자본) 대비 현재 계좌 자산의 총 수익률(%)

이 테이블을 통해 사용자는:

현재 계좌와 포지션의 상태

리스크 수준

누적 성과

를 직관적으로 파악할 수 있습니다.

6. 시간 필터 및 라벨 옵션

6-1. 전략 동작 기간 설정

전략은 옵션으로 특정 기간에만 전략을 동작시키는 시간 필터를 제공합니다.

“Use Date Range” 옵션을 활성화하면:

시작 시각과 종료 시각을 지정하여

해당 구간에 한해서만 매매가 발생하도록 제한

옵션을 비활성화하면:

전략은 전체 차트 구간에서 자유롭게 동작

6-2. 진입 라벨 위치 설정

사용자는 매수/레버리지 라벨의 위치를 선택할 수 있습니다.

바 아래 (Below Bar)

바 위 (Above Bar)

실제 가격 위치 (At Price)

이를 통해 개인 취향 및 차트 가독성에 맞추어

시각화 방식을 유연하게 조정할 수 있습니다.

7. 활용 대상 및 사용 예시

본 전략은 다음과 같은 목적에 적합합니다.

현물 또는 선물 롱 포지션 기준 장기·스윙 관점 추매 전략 백테스트

“고점 대비 하락률”을 기준으로 한 규칙 기반 운용 아이디어 검증

레버리지 사용 시

계좌 레버리지·청산가·MDD를 동시에 모니터링하고자 하는 경우

특정 자산에 대해

“새로운 고점이 형성될 때마다

일정한 규칙으로 깊은 조정 구간에서만 분할 진입하고자 할 때”

실거래에 그대로 적용하기보다는,

전략 아이디어 검증 및 리스크 프로파일 분석,

자신의 성향에 맞는 파라미터 탐색 용도로 사용하는 것을 권장합니다.

8. 한계 및 유의사항

백테스트 결과는 미래 성과를 보장하지 않습니다.

과거 데이터에 기반한 시뮬레이션일 뿐이며,

실제 시장에서는

유동성

슬리피지

수수료 체계

강제청산 규칙

등 다양한 변수가 존재합니다.

청산가는 단순화된 공식에 따른 추정치입니다.

거래소별 실제 청산 규칙, 유지 증거금, 수수료, 펀딩비 등은

본 전략의 계산과 다를 수 있으며,

청산가 추정 라인은 참고용 지표일 뿐입니다.

레버리지 및 진입 비율 설정에 따라 손실 폭이 매우 커질 수 있습니다.

특히 **“첫 포지션 300% 진입”**과 같이 매우 공격적인 설정은

시장 급락 시 계좌 손실과 청산 리스크를 크게 증가시킬 수 있으므로

신중한 검토가 필요합니다.

실거래 연동 시에는 별도의 리스크 관리가 필수입니다.

개별 손절 기준

포지션 상한선

전체 포트폴리오 내 비중 관리 등

본 전략 외부에서 추가적인 안전장치가 필요합니다.

9. 결론

ATH Drawdown Re-Buy Long Only 전략은 단순한 “저가 매수”를 넘어서,

ATH 기준으로 드로우다운을 구조적으로 활용하고,

첫 포지션에 대한 **특수 규칙(100% / 300%)**을 적용하며,

레버리지·청산가·MDD·수익률을 통합적으로 시각화함으로써,

하락 구간에서의 규칙 기반 롱 포지션 구축과

리스크 모니터링을 동시에 지원하는 전략입니다.

사용자는 본 전략을 통해:

자신의 시장 관점과 리스크 허용 범위에 맞는

드로우다운 구간

진입 비율

레버리지 설정

다양한 시나리오에 대한 백테스트와 분석

을 수행할 수 있습니다.

다시 한 번 강조하지만,

본 전략은 연구·학습·백테스트를 위한 도구이며,

실제 투자 판단과 책임은 전적으로 사용자 본인에게 있습니다.

/ENG Version.

This script is designed to use historical drawdown data and automatically enter positions when a predefined percentage drop from the all-time high occurs, using a predefined percentage of your account equity.

You can use leverage, and default parameter values are provided out of the box (you can freely change them to suit your style).

In addition to the two main entry levels, you can add more entry conditions and custom entry percentages – just ask ChatGPT to modify the script.

For actual/live usage, please turn OFF the KillSwitch function and turn ON the Bar Magnifier feature.

ATH Drawdown Re-Buy Long Only Strategy

1. Strategy Overview

The ATH Drawdown Re-Buy Long Only strategy is an automatic re-buy (Long Only) system that builds long positions step-by-step at specific drawdown levels, based on the asset’s all-time high (ATH) and its subsequent drawdown.

This strategy is designed with the following goals:

Systematic scaled buying and leverage usage during sharp correction periods

Clear, rule-based entry logic using drawdowns from ATH

Real-time visualization of:

Average entry price

Leverage

Estimated liquidation price

Account MDD (Max Drawdown)

Return / performance

This allows traders to intuitively monitor both risk and position status.

※ This strategy is provided for educational, research, and backtesting purposes only.

It does not constitute investment advice and does not guarantee any profits.

2. Core Concepts

2-1. Drawdown from ATH (All-Time High)

On the chart, the strategy always tracks the highest high as the ATH.

Whenever a new high is made, ATH is updated, and based on that ATH the following are calculated:

How many percent the current bar’s Low is below the ATH

How many percent the current bar’s Close is below the ATH

Using these, the strategy executes buys at two predefined drawdown zones:

1st entry zone: When price drops X% from ATH

2nd entry zone: When price drops Y% from ATH

Each zone is allowed to trigger only once per ATH cycle.

When a new ATH is created, the “1st / 2nd entry possible” flags are reset, and new opportunities open up for that ATH leg.

2-2. Special Rule for the First Position (100% / 300%)

A key feature of this strategy is the special rule for the very first position.

When the strategy currently holds no position and is about to open the first long position:

Under normal conditions, it builds the position using 100% of account equity.

However, if at that moment the price has dropped by at least a predefined threshold from ATH (e.g. around –72.5% or more),

→ the strategy will open the first position using 300% of account equity.

This rule works as follows:

Whether the first entry happens at the 1st drawdown zone or at the 2nd drawdown zone,

If the current drawdown from ATH is at or below the threshold (e.g. –72.5% or worse),

→ the strategy interprets this as “a sufficiently deep crash” and opens the initial position with 300% of equity.

If the drawdown is less severe than the threshold,

→ the first entry is capped at 100% of equity.

So the strategy has two modes for the first entry:

Normal market conditions: 100% of equity

Deep drawdown conditions: 300% of equity

This special rule is intended to be aggressive in extremely deep crashes while staying more conservative in normal corrections.

3. Strategy Logic & Execution

3-1. Entry Conditions

The strategy tracks the ATH using the High price.

For each bar, it calculates the drawdown from ATH.

The user defines two drawdown zones, for example:

1st zone: ATH – 50%

2nd zone: ATH – 72.5%

For each zone, the strategy checks:

If no buy has been executed yet for that zone in the current ATH leg, and

If the current bar’s Low touches or falls below that zone’s price level,

→ That bar is considered to have triggered a buy condition.

Order simulation:

The strategy simulates entering a long position at that zone’s price level

(using a limit/market-like approximation for backtesting).

3-2. ATH Reset & Entry Opportunity Reset

When a new High goes above the previous ATH:

The ATH is updated to this new high.

Internal flags that track whether the 1st and 2nd entries have been used are reset.

This means:

Each time the market makes a new ATH,

The strategy once again has a fresh opportunity to execute 1st and 2nd drawdown entries for that new ATH leg.

4. Position Sizing & Leverage

4-1. Position Size Based on Account Equity

The strategy defines current equity as:

Current Equity = Initial Capital + Realized PnL + Unrealized PnL

For each entry zone, the position value is calculated as follows:

The user inputs:

“What % of equity to use at this zone”

The strategy:

Multiplies current equity by that percentage

Then multiplies by the strategy’s leverage factor

Thus:

Position Value = Current Equity × (Zone % / 100) × Leverage

Finally, this position value is divided by the entry price to determine the actual position size in tokens.

4-2. Exception for the First Position (100% / 300%)

For the very first position (when there is no open position),

the strategy does not use the zone % parameters. Instead, it uses fixed ratios:

Default: Enter the first position with 100% of equity.

If the drawdown from ATH at that moment is greater than or equal to a predefined threshold (e.g. –72.5% or more)

→ Enter the first position with 300% of equity.

The position value is computed as:

Position Value = Current Equity × (100% or 300%) × Leverage

Then it is divided by the entry price to obtain the token quantity.

This rule:

Applies regardless of whether the first entry occurs at the 1st zone or 2nd zone.

Embeds the philosophy:

“In very deep crashes, go much larger on the first entry; otherwise, stay more conservative.”

4-3. Tracking Real Leverage

On each bar, the strategy tracks:

The existing position size at the start of the bar

The newly added size (if any) on that bar

When a new entry occurs, it calculates the real leverage at that moment:

Real Leverage = (Position Value / Current Equity)

This is then displayed on the chart as a label, for example:

Lev 2.53x

This makes it easy to see the actual leverage level at each entry point.

5. Visualization & Monitoring

5-1. On-Chart Visual Elements

The strategy plots the following directly on the chart:

ATH Line

The all-time high (based on High) is plotted as an orange line.

Average Entry Price Line

When a position is open, the average entry price of that position is plotted as a yellow line.

Estimated Liquidation Price (Fixed) Line

The strategy detects when the position size changes.

At each size change, it uses the current average entry price and real leverage to compute an approximate liquidation price.

This “fixed liquidation price” is then plotted as a red line on the chart.

If there is no position, or if leverage is 1x or lower, the liquidation line is removed.

Entry Markers & Labels

When 1st/2nd entry conditions are met, the strategy:

Marks the entry point on the chart.

Displays labels such as "Buy XX% @ Price" and "Lev XXx",

showing both entry percentage and real leverage at that time.

The label placement is configurable:

Below Bar

Above Bar

At Price

5-2. Information Table (Top-Right Panel)

In the top-right corner of the chart, the strategy displays a summary table of the current account and position status. It typically includes:

Pos Qty (Token)

Absolute size of the current position (in tokens)

Pos Value (USDT)

Market value of the current position (qty × current price)

Leverage (Now)

Current real leverage (position value / current equity)

DD from ATH (%)

Current drawdown (%) from the latest ATH, based on current price

Avg Entry

Average entry price of the current position

PnL (%)

Unrealized profit/loss (%) of the current position

Max DD (Equity %)

The maximum equity drawdown (MDD) recorded over the entire backtest period

Last Entry Price

Average entry price immediately after the most recent add-on entry

Last Entry Lev

Real leverage at the time of the most recent entry

Liq Price (Fixed)

The fixed estimated liquidation price described above

Return from Start (%)

Total return (%) of equity compared to the initial capital

Through this table, users can quickly grasp:

Current account and position status

Current risk level

Cumulative performance

6. Time Filters & Label Options

6-1. Strategy Date Range Filter

The strategy provides an option to restrict trading to a specific time range.

When “Use Date Range” is enabled:

You can specify start and end timestamps.

The strategy will only execute trades within that range.

When this option is disabled:

The strategy operates over the entire chart history.

6-2. Entry Label Placement

Users can customize where entry/leverage labels are drawn:

Below Bar (Below Bar)

Above Bar (Above Bar)

At the actual price level (At Price)

This allows you to adjust visualization according to personal preference and chart readability.

7. Use Cases & Applications

This strategy is suitable for the following purposes:

Long-term / swing-style re-buy strategies for spot or futures long positions

Testing rule-based strategies that rely on “drawdown from ATH” as a main signal

Monitoring account leverage, liquidation price, and MDD when using leverage

Handling situations where, for a given asset:

“Every time a new ATH is formed,

you want to wait for deep corrections and enter only at specific drawdown zones”

It is generally recommended to use this strategy not as a direct plug-and-play live system, but as a tool for:

Strategy idea validation

Risk profile analysis

Parameter exploration to match your personal risk tolerance and style

8. Limitations & Warnings

Backtest results do not guarantee future performance.

They are based on historical data only.

In live markets, additional factors exist:

Liquidity

Slippage

Fee structures

Exchange-specific liquidation rules

Funding fees, etc.

The liquidation price is only an approximate estimate, derived from a simplified formula.

Actual liquidation rules, maintenance margin requirements, fees, and other details differ by exchange.

The liquidation line should be treated as a reference indicator, not an exact guarantee.

Depending on the configured leverage and entry percentages, losses can be very large.

In particular, extremely aggressive settings such as “first position 300% of equity” can greatly increase the risk of large account drawdowns and liquidation during sharp market crashes.

Use such settings with extreme caution.

For live trading, additional risk management is essential:

Your own stop-loss rules

Maximum position size limits

Portfolio-level exposure controls

And other external safety mechanisms beyond this strategy

9. Conclusion

The ATH Drawdown Re-Buy Long Only strategy goes beyond simple “buy the dip” logic. It:

Systematically utilizes drawdowns from ATH as a structural signal

Applies a special first-position rule (100% / 300%)

Integrates visualization of leverage, liquidation price, MDD, and returns

All of this supports rule-based long position building in drawdown phases and comprehensive risk monitoring.

With this strategy, users can:

Explore different:

Drawdown zones

Entry percentages

Leverage levels

Run various backtests and scenario analyses

Better understand the risk/return profile that fits their own market view and risk tolerance

Once again, this strategy is intended for research, learning, and backtesting only.

All real trading decisions and their consequences are solely the responsibility of the user.

ORBSMMAATRVOLREENTRY2Contracts📈 Opening Range Fibonacci Breakout (TradingView Strategy)

Overview:

The Opening Range Fibonacci Breakout strategy is designed to capture high-probability intraday moves by combining the power of the 15-minute opening range, trend confirmation via SMMA, and volume-based momentum filtering.

At the start of each trading session, the script automatically plots the Opening Range Box based on the first 15 minutes of price action — highlighting key intraday support and resistance levels.

How It Works:

Opening Range Setup

The first 15 minutes of the session define the range high and low.

A visual box marks this zone on the chart for easy reference.

Signal Generation

A Smoothed Moving Average (SMMA) with a user-defined period determines overall trend bias.

Candle volume is analyzed to confirm momentum strength.

Long Signal: Price breaks above the opening range high, SMMA trending up, and volume supports the move.

Short Signal: Price breaks below the opening range low, SMMA trending down, and volume supports the move.

Take Profit & Targets

Fibonacci extension levels are automatically plotted from the opening range.

These dynamic levels serve as structured Take Profit (TP) zones for partial or full exits.

Features:

✅ 15-Minute Opening Range Box

✅ Adjustable SMMA period

✅ Volume-based confirmation filter

✅ Automatic Fibonacci profit targets

✅ Visual Long/Short alerts & signals

Ideal For:

Scalpers and intraday traders who rely on early-session momentum, breakout confirmation, and precision exit targets.

Backtested for MNQ/NQ futures trading

Adaptive Trend 1m ### Overview

The "Adaptive Trend Impulse Parallel SL/TP 1m Realistic" strategy is a sophisticated trading system designed specifically for high-volatility markets like cryptocurrencies on 1-minute timeframes. It combines trend-following with momentum filters and adaptive parameters to dynamically adjust to market conditions, ensuring more reliable entries and risk management. This strategy uses SuperTrend for primary trend detection, enhanced by MACD, RSI, Bollinger Bands, and optional volume spikes. It incorporates parallel stop-loss (SL) and multiple take-profit (TP) levels based on ATR, with options for breakeven and trailing stops after the first TP. Optimized for realistic backtesting on short timeframes, it avoids over-optimization by adapting indicators to market speed and efficiency.

### Principles of Operation

The strategy operates on the principle of adaptive impulse trading, where entry signals are generated only when multiple conditions align to confirm a strong trend reversal or continuation:

1. **Trend Detection (SuperTrend)**: The core signal comes from an adaptive SuperTrend indicator. It calculates upper and lower bands using ATR (Average True Range) with dynamic periods and multipliers. A buy signal occurs when the price crosses above the lower band (from a downtrend), and a sell signal when it crosses below the upper band (from an uptrend). Adaptation is based on Rate of Change (ROC) to measure market speed, shortening periods in fast markets for quicker responses.

2. **Momentum and Trend Filters**:

- **MACD**: Uses adaptive fast and slow lengths. In "Trend Filter" mode (default when "Use MACD Cross" is false), it checks if the MACD line is above/below the signal for long/short. In cross mode, it requires a crossover/crossunder.

- **RSI**: Adaptive period RSI must be above 50 for longs and below 50 for shorts, confirming overbought/oversold conditions dynamically.

- **Bollinger Bands (BB)**: Depending on the mode ("Midline" by default), it requires the price to be above/below the BB midline for longs/shorts, or a breakout in "Breakout" mode. Deviation adapts to market efficiency.

- **Volume Spike Filter** (optional): Entries require volume to exceed an adaptive multiple of its SMA, signaling strong impulse.

3. **Volatility Filter**: Entries are only allowed if current ATR percentage exceeds a historical minimum (adaptive), preventing trades in low-volatility ranges.

4. **Risk Management (Parallel SL/TP)**:

- **Stop-Loss**: Set at an adaptive ATR multiple below/above entry for long/short.

- **Take-Profits**: Three levels at adaptive ATR multiples, with partial position closures (e.g., 51% at TP1, 25% at TP2, remainder at TP3).

- **Post-TP1 Features**: Optional breakeven moves SL to entry after TP1. Trailing SL uses BB midline as a dynamic trail.

- All levels are calculated per trade using the ATR at entry, making them "realistic" for 1m charts by widening SL and tightening initial TPs.

The strategy enters long on buy signals with all filters met, and short on sell signals. It uses pyramid margin (100% long/short) for full position sizing.

Adaptation is driven by:

- **Market Speed (normSpeed)**: Based on ROC, tightens multipliers in volatile periods.

- **Efficiency Ratio (ER)**: Measures trend strength, adjusting periods for trending vs. ranging markets.

This ensures the strategy "adapts" without manual tweaks, reducing false signals in varying conditions.

### Main Advantages

- **Adaptability**: Unlike static strategies, parameters dynamically adjust to market volatility and trend strength, improving performance across ranging and trending phases without over-optimization.

- **Realistic Risk Management for 1m**: Wider SL and tiered TPs prevent premature stops in noisy short-term charts, while partial profits lock in gains early. Breakeven/trailing options protect profits in extended moves.

- **Multi-Filter Confirmation**: Combines trend, momentum, and volume for high-probability entries, reducing whipsaws. The volatility filter avoids flat markets.

- **Debug Visualization**: Built-in plots for signals, levels, and component checks (when "Show Debug" is enabled) help users verify logic on charts.

- **Efficiency**: Low computational load, suitable for real-time trading on TradingView with alerts.

Backtesting shows robust results on volatile assets, with a focus on sustainable risk (e.g., SL at 3x ATR avoids excessive drawdowns).

### Uniqueness

What sets this strategy apart is its **fully adaptive framework** integrating multiple indicators with real-time market metrics (ROC for speed, ER for efficiency). Most trend strategies use fixed parameters, leading to poor adaptation; here, every key input (periods, multipliers, deviations) scales dynamically within bounds, creating a "self-tuning" system. The "parallel SL/TP with 1m realism" adds custom handling for micro-timeframes: tightened initial TPs for quick wins and adaptive min-ATR filter to skip low-vol bars. Unlike generic mashups, it justifies the combination—SuperTrend for trend, MACD/RSI/BB for impulse confirmation, volume for conviction—working synergistically to capture "trend impulses" while filtering noise. The post-TP1 breakeven/trailing tied to BB adds a unique profit-locking mechanism not common in open-source scripts.

### Recommended Settings

These settings are optimized and recommended for trading ASTER/USDT on Bybit, with 1-minute chart, x10 leverage, and cross margin mode. They provide a balanced risk-reward for this volatile pair:

- **Base Inputs**:

- Base ATR Period: 10

- Base SuperTrend ATR Multiplier: 2.5

- Base MACD Fast: 8

- Base MACD Slow: 17

- Base MACD Signal: 6

- Base RSI Period: 9

- Base Bollinger Period: 12

- Bollinger Deviation: 1.8

- Base Volume SMA Period: 19

- Base Volume Spike Multiplier: 1.8

- Adaptation Window: 54

- ROC Length: 10

- **TP/SL Settings**:

- Use Stop Loss: True

- Base SL Multiplier (ATR): 3

- Use Take Profits: True

- Base TP1 Multiplier (ATR): 5.5

- Base TP2 Multiplier (ATR): 10.5

- Base TP3 Multiplier (ATR): 19

- TP1 % Position: 51

- TP2 % Position: 25

- Breakeven after TP1: False

- Trailing SL after TP1: False

- Base Min ATR Filter: 0.001

- Use Volume Spike Filter: True

- BB Condition: Midline

- Use MACD Cross (false=Trend Filter): True

- Show Debug: True

For backtesting, use initial capital of 30 USD, base currency USDT, order size 100 USDT, pyramiding 1, commission 0.1%, slippage 0 ticks, long/short margin 0%.

Always backtest on your platform and use risk management—risk no more than 1-2% per trade. This is not financial advice; trade at your own risk.

Supertrend Strategy With Multi Tp & TslHello Traders,

This strategy is based on the popular Supertrend indicator, which many traders use as a simple trend-following tool. The core entry logic is straightforward:

Buy (Long) when the price closes above the Supertrend line.

Sell (Short) when the price closes below the Supertrend line.

However, trading success isn’t only about entries — proper risk management makes all the difference. That’s why this strategy includes four stop-loss methods, two take-profit types, and a trailing stop-loss system. You can customize all of these settings to create your own personalized version.

🛑 Stop-Loss Methods

Tick – Uses the instrument’s smallest price increment. Ideal for tick-based markets such as Futures or Forex.

Percent – Defines the stop-loss as a percentage of entry price. Commonly used in Crypto trading.

ATR – Uses the Average True Range value to determine stop-loss distance. Perfect for adapting to changing market volatility.

Supertrend – The stop-loss level is set at the Supertrend line value at the time of entry.

🔁 Trailing Stop-Loss & Reverse Signals

Trailing SL: If enabled, the chosen stop-loss method will trail the price dynamically from the moment the position opens.

Close with Reverse Signals: When activated, the current position closes and reverses on an opposite signal. If disabled, the strategy waits until the current position is closed before opening a new one.

🎯 Take-Profit Options

Tick – Set a fixed take-profit level based on tick distance.

Percent – Set take-profit based on a percentage change from entry.

Ratio – Sets take-profit based on the entry-to-stop-loss distance × ratio value.

Each take-profit method allows you to define the percentage of position to close at that level.

⚖️ Breakeven Option

When Breakeven is enabled, after the first take-profit is triggered, the stop-loss automatically moves to the entry level, protecting your capital.

⚙️ Additional Settings

Position Type: Choose between Long only, Short only, or Both directions.

Session Filter: Trade only during specific time ranges. Activate this option and set your desired session hours (make sure to select your correct timezone).

📈 Visuals

The strategy plots entry, stop-loss, and take-profit levels directly on the chart, allowing you to clearly visualize your trades and manage them effectively.

Feel free to ask any questions or suggest improvements — this strategy is built for flexibility and experimentation!

Trend-Following & Breakout — Index Quant Strategy (NASDAQ)📈 Trend-Following & Breakout — Index Quant Strategy (NASDAQ & S&P 500)

Type: Invite-only strategy

Markets: NASDAQ 100 (NAS100 / US100 / NQ), S&P 500 (US500 / SPX), and other major equity indices.

🧠 Concept: Continuous trend model combining EWMAC (trend-following) and Donchian (breakout) signals, scaled by forecast strength and portfolio risk.

⚙️ Execution: Rebalances only on decision-bar closes, using hysteresis and a no-trade band to reduce churn.

📊 Default bias: Long-only — aligned with equity index drift.

🧩 How it works

• EWMAC Trend: Difference between fast and slow EMAs, normalized by an EWMA of absolute returns.

• Donchian Breakout: Distance beyond a 200-bar channel (Strict mode) or relative z-score position within it.

• Forecast combination: Weighted sum of trend and breakout points, clamped to ± capPoints.

• Hysteresis: Prevents quick sign flips near zero forecast.

• Risk scaling: Maps forecast strength to position size using equity × risk budget × ATR-based stop distance.

• Rebalance: Executes only if the required quantity change exceeds the Δqty threshold; can optionally block increases on Sundays (for CFDs).

⚙️ Default parameters

Deployed on NQ / US100 / NAS100 on Daily Timeframe

• Decision timeframe = 360 min (other options from 1 min to 1 week).

• Trend (EWMAC): Fast = 64, Slow = 256, Vol Norm = 32, Weight = 0.8.

• Breakout (Donchian): Length = 200, Mode = Strict, Weight = 0.2.

• Forecast scaling: ptsPerSigma = 1.0, capPoints = 10.

• Risk % per rebalance = 4 % of equity.

• ATR stop: ATR(14) × 1.0.

• No-trade band (Δqty) = 4 units.

• Hysteresis = 2 forecast points.

• Bias = Long-only (Neutral / Long-bias 50 % optional).

• Skip Sunday increases = false (default).

📋 Backtest properties (documented)

• Initial capital = 100 000 USD.

• Commission = 0.20 % per trade.

• Pyramiding = 10.

• Calc on every tick = false.

• Point value = 1 (for NAS100 CFD).

• No financing or slippage modeled.

• If using CFDs, account for overnight funding.

• On futures (NQ / ES), carry is implicit.

📊 Typical behaviour

• Many small scratches, a few large winners.

• Performs best during multi-week / multi-month trends.

• Underperforms in tight or volatile ranges.

• Average hold ≈ 30 – 90 days in historical tests.

💡 Risk and performance guide (illustrative)

Sharpe ≈ 1.25

Sortino ≈ 1.10 – 1.30

Max drawdown ≈ –18 % to –25 %

Annual volatility ≈ 24 – 28 %

CAGR ≈ 50 – 60 % (at 4 % risk)

Edge ratio ≈ 5 (MFE / MAE)

Historical backtests only — past performance does not guarantee future results.

🌍 Intended markets and timeframes

Optimized for NASDAQ 100 and S&P 500; also effective on similar indices (DAX, Dow Jones, FTSE).

Best on Daily or higher timeframes.

Aligns with long-term index drift — suitable for long-bias systematic trend portfolios.

⚠️ Limitations

• Backtests exclude CFD funding costs.

• Trend models will have losing streaks in range-bound markets.

• Designed for experienced traders seeking systematic exposure.

🔑 Requesting access

Send a private TradingView message to with the text:

“Request access to Trend-Following & Breakout — Index Quant Strategy.”

Access is granted only on explicit request.

For further information, see my TradingView Signature.

🆕 Release notes (v1.0)

• Initial release (360 min TF): EWMAC 64/256 + Donchian 200 Strict.

• Risk 4 %, ATR × 1.0, Long-only bias, hysteresis 2 pts, Δqty ≥ 4.

• Developed for NASDAQ 100 and S&P 500 indices.

• Implements continuous risk-scaled positioning and no-trade band logic.

🧾 Originality statement

This strategy is original work built entirely from TradingView built-ins (EMA, ATR, Highest, Lowest).

It does not reuse open-source invite-only code.

Any future reuse of open scripts will be done with explicit permission and credit.

Grand Master's Candlestick Dominance (ATR Enhanced)### Grand Master's Candlestick Dominance (ATR Enhanced)

**Overview**

Unleash the ancient wisdom of Japanese candlestick charting with a modern twist! This comprehensive Pine Script v5 strategy and indicator scans for over 75 classic and advanced candlestick patterns (bullish, bearish, and neutral), assigning dynamic strength scores (1-10) to each for precise signal filtering. Enhanced with Average True Range (ATR) for volatility-aware body size validation, it dominates the markets by combining timeless pattern recognition with robust confirmation layers. Whether used as a backtestable strategy or visual indicator, it empowers traders to spot high-probability reversals, continuations, and indecision setups with surgical accuracy.

Inspired by Steve Nison's *Japanese Candlestick Charting Techniques*, this tool elevates pattern analysis beyond basics—think Hammers, Engulfing patterns, Morning Stars, and rare gems like Abandoned Baby or Concealing Baby Swallow—all consolidated into intelligent arrays for real-time averaging and prioritization.

**Key Features**

- **Extensive Pattern Library**:

- **Bullish (25+ patterns)**: Hammer (8.0), Bullish Engulfing (10.0), Morning Star (7.0), Three White Soldiers (9.0), Dragonfly Doji (8.0), and more (e.g., Rising Three, Unique Three River Bottom).

- **Bearish (25+ patterns)**: Hanging Man (8.0), Bearish Engulfing (10.0), Evening Star (7.0), Three Black Crows (9.0), Gravestone Doji (8.0), and exotics like Upside Gap Two Crows or Stalled Pattern.

- **Neutral/Indecision (34+ patterns)**: Doji variants (Long-Legged, Four Price), Spinning Tops, Harami Crosses, and multi-bar setups like Upside Tasuki Gap or Advancing Block.

Each pattern includes duration tracking (1-5 bars) and ATR-adjusted body/shadow criteria for relevance in volatile conditions.

- **Smart Confirmation Filters** (All Toggleable):

- **Trend Alignment**: 20-period SMA (customizable) ensures entries align with the prevailing trend; optional higher timeframe (e.g., Daily) MA crossover for multi-timeframe confluence.

- **Support/Resistance (S/R)**: Pivot-based levels with 0.01% tolerance to confirm bounces or breaks.

- **Volume Surge**: 20-period volume MA with 1.5x spike multiplier to validate momentum.

- **ATR Body Sizing**: Filters small bodies (<0.3x ATR) and long bodies (>0.8x ATR) for context-aware pattern reliability.

- **Follow-Through**: Ensures post-pattern confirmation via bullish/bearish closes or closes beyond prior bars.

Minimum average strength (default 7.0) and individual pattern thresholds (5.0) prevent weak signals.

- **Entry & Exit Logic**:

- **Long Entry**: Bullish average strength ≥7.0 (outweighing bearish), uptrend, volume spike, near support, follow-through, and HTF alignment.

- **Short Entry**: Mirror for bearish dominance in downtrends near resistance.

- **Exits**: Bearish/neutral shift, or fixed TP (5%) / SL (2%)—pyramiding disabled, 10% equity sizing.

- Backtest range: Jan 1, 2020 – Dec 31, 2025 (editable). Initial capital: $10,000.

- **Interactive Dashboard** (Top-Right Panel):

Real-time insights including:

- Market phase (e.g., "Bullish Phase (Avg Str: 8.2)"), active pattern (e.g., "BULLISH: Bullish Engulfing (Str: 10.0, Bars: 2)"), and trend status.

- Strength breakdowns (Bull/Bear/Neutral counts & averages).

- Filter status (e.g., "Volume: ✔ Spike", "ATR: Enabled (L:0.8, S:0.3)").

- Backtest stats: Total trades, win rate, streak, and last entry/exit details (price & timestamp).

Toggle mode: Strategy (live trades) or Indicator (signals only).

- **Advanced Alerts** (15+ Toggleable Types):

Set up via TradingView's "Any alert() function call" for bar-close triggers:

- Entry/Exit signals with strength & pattern details.

- Strong patterns (≥2 bullish/bearish), neutral indecision, volume spikes.

- S/R breakouts, HTF reversals, high-confidence singles (≥8.0 strength).

- Conflicting signals, MA crossovers, ATR volatility bursts, multi-bar completions.

Example: "STRONG BULLISH PATTERN detected! Strength: 9.5 | Top Pattern: Three White Soldiers | Trend: Up".

**Customization & Usage Tips**

- **Inputs Groups**: Strategy toggles, confirmations, exits, backtest dates, and 15+ alert switches—all intuitively grouped.

- **Optimization**: Tune min strengths for aggressive (lower) or conservative (higher) trading; enable/disable filters to suit your style (e.g., disable S/R for scalping).

- **Best For**: Forex, stocks, crypto on 1H–Daily charts. Test on historical data to refine TP/SL.

- **Limitations**: No external data installs; relies on built-in TA functions. Patterns are probabilistic—combine with your risk management.

Master the candles like a grandmaster. Deploy on TradingView, backtest relentlessly, and let dominance begin! Questions? Drop a comment.

*Version: 1.0 | Updated: September 2025 | Credits: Built on Pine Script v5 with nods to Nison's timeless techniques.*

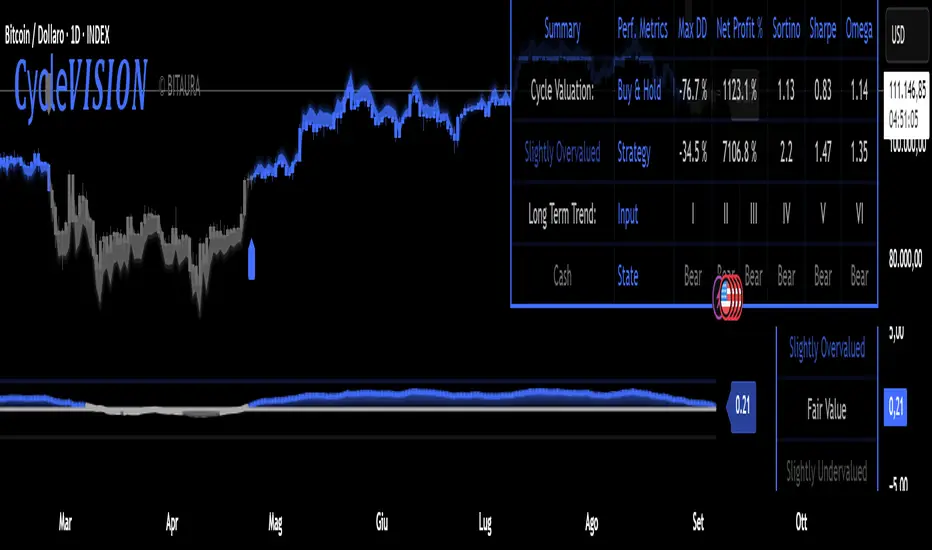

CycleVISION [BitAura]𝐂ycle𝑽𝑰𝑺𝑰𝑶𝑵

This Pine Script® indicator combines a long-term trend-following strategy with a cycle valuation Z-score analysis to generate a Trend Probability Indicator (TPI). The TPI aggregates signals from multiple trend and on-chain metrics to identify optimal entry and exit points for a single asset, with USD as a cash position. The system also calculates a comprehensive Z-score based on performance and valuation metrics to assess market cycles, aiming to enhance risk-adjusted returns for long-term investors.

Logic and Core Concepts

The 𝐂ycle𝑽𝑰𝑺𝑰𝑶𝑵 System uses two primary components to guide investing decisions:

1. Trend Probability Indicator (TPI)

Mechanism : Aggregates five proprietary, universal, trend signals and three on-chain metrics into a composite TPI score, normalized between -1 and 1.

Thresholds : Enters a long position when the TPI score exceeds a user-defined long threshold (default: 0.0) and exits to cash when it falls below a short threshold (default: -0.5).

Execution : Trades are executed only on confirmed bars within a user-specified backtest date range, ensuring robust signal reliability.

2. Cycle Valuation Z-Score

Mechanism : Computes an average Z-score from six metrics: Sharpe Ratio, Sortino Ratio, Omega Ratio, Weekly RSI, Crosby Ratio, and Price Z-Score, using a 1200-bar lookback period.

Purpose : Identifies overvalued or undervalued market conditions to complement TPI signals, with thresholds at ±1.8 for extreme valuations.

Visualization : Displays the average Z-score and individual components, with gradient-based bar coloring to reflect valuation strength.

Features

Dynamic Trend Signals : Combines trend and on-chain data into a single TPI score for clear long/cash decisions.

Comprehensive Valuation : Calculates Z-scores for multiple performance and price metrics to assess market cycles.

Customizable Inputs : Allows users to adjust TPI thresholds, backtest date ranges, and valuation metrics visibility.

Visual Outputs :

Valuation Table : Displays TPI score, Z-scores, and performance metrics (Sharpe, Sortino, Omega, Max Drawdown, Net Profit) in a configurable table (Lite, Medium, Full).

Equity Curve : Plots the system’s equity curve compared to buy-and-hold performance.

Price and TPI Plot : Overlays TPI-adjusted price bands with glow effects and filled gaps for trend visualization on the price chart.

Valuation Coloring : Applies backgrounds based on Z-score ranges (e.g., strong buy above 1.8, strong sell below -1.8).

Configurable Alerts : Notifies users of TPI signal changes (Long to Cash or Cash to Long) with detailed messages.

Color Presets : Offers five color themes (e.g., Arctic Blast, Fire vs. Ice) or custom color options for long/short signals.

Pine Script v6 : Leverages matrices, tables, and gradient coloring for enhanced usability.

How to Use

Add to Chart : Apply the indicator to any chart (the chart’s ticker is used for calculations, e.g., INDEX:BTCUSD ).

Configure Settings : Adjust TPI thresholds, backtest start date (default: 01 Feb 2018), and valuation metrics visibility in the Inputs menu.

Select Color Theme : Choose a preset color mode (e.g., Arctic Blast) or enable custom colors in the Colors group.

Monitor Outputs : Check the Valuation Table for TPI and Z-score data, and view the Price and TPI Plot for trend signals.

Analyze Performance : Enable the equity curve and performance metrics in the Backtesting Options group to compare results.

Set Alerts : Right-click a plot, select "Add alert," and choose "Trend Change: Long to Cash" or "Trend Change: Cash to Long" for notifications.

The system is optimized for daily timeframe and tested across various assets to ensure robustness.

Notes

The script is closed-source.

Use a standard price series (not Heikin Ashi or other non-standard types) for accurate results.

The script avoids lookahead bias by using barmerge.lookahead_off in request.security() calls.

A minimum 1200-bar lookback is mandatory for Z-score calculations to avoid errors, with warnings displayed if insufficient price history is available.

The BitAura watermark can be toggled in the Table Settings group.

Disclaimer : This script is for educational and analytical purposes only and does not constitute financial advice. Trading involves significant risk, and past performance is not indicative of future results. Always conduct your own research and apply proper risk management.

The Barking Rat LiteMomentum & FVG Reversion Strategy

The Barking Rat Lite is a disciplined, short-term mean-reversion strategy that combines RSI momentum filtering, EMA bands, and Fair Value Gap (FVG) detection to identify short-term reversal points. Designed for practical use on volatile markets, it focuses on precise entries and ATR-based take profit management to balance opportunity and risk.

Core Concept

This strategy seeks potential reversals when short-term price action shows exhaustion outside an EMA band, confirmed by momentum and FVG signals:

EMA Bands:

Parameters used: A 20-period EMA (fast) and 100-period EMA (slow).

Why chosen:

- The 20 EMA is sensitive to short-term moves and reflects immediate momentum.

- The 100 EMA provides a slower, structural anchor.

When price trades outside both bands, it often signals overextension relative to both short-term and medium-term trends.

Application in strategy:

- Long entries are only considered when price dips below both EMAs, identifying potential undervaluation.

- Short entries are only considered when price rises above both EMAs, identifying potential overvaluation.

This dual-band filter avoids counter-trend signals that would occur if only a single EMA was used, making entries more selective..

Fair Value Gap Detection (FVG):

Parameters used: The script checks for dislocations using a 12-bar lookback (i.e. comparing current highs/lows with values 12 candles back).

Why chosen:

- A 12-bar displacement highlights significant inefficiencies in price structure while filtering out micro-gaps that appear every few bars in high-volatility markets.

- By aligning FVG signals with candle direction (bullish = close > open, bearish = close < open), the strategy avoids random gaps and instead targets ones that suggest exhaustion.

Application in strategy:

- Bullish FVGs form when earlier lows sit above current highs, hinting at downward over-extension.

- Bearish FVGs form when earlier highs sit below current lows, hinting at upward over-extension.

This gives the strategy a structural filter beyond simple oscillators, ensuring signals have price-dislocation context.

RSI Momentum Filter:

Parameters used: 14-period RSI with thresholds of 80 (overbought) and 20 (oversold).

Why chosen:

- RSI(14) is a widely recognized momentum measure that balances responsiveness with stability.

- The thresholds are intentionally extreme (80/20 vs. the more common 70/30), so the strategy only engages at genuine exhaustion points rather than frequent minor corrections.

Application in strategy:

- Longs trigger when RSI < 20, suggesting oversold exhaustion.

- Shorts trigger when RSI > 80, suggesting overbought exhaustion.

This ensures entries are not just technically valid but also backed by momentum extremes, raising conviction.

ATR-Based Take Profit:

Parameters used: 14-period ATR, with a default multiplier of 4.

Why chosen:

- ATR(14) reflects the prevailing volatility environment without reacting too much to outliers.

- A multiplier of 4 is a pragmatic compromise: wide enough to let trades breathe in volatile conditions, but tight enough to enforce disciplined exits before mean reversion fades.

Application in strategy:

- At entry, a fixed target is set = Entry Price ± (ATR × 4).

- This target scales automatically with volatility: narrower in calm periods, wider in explosive markets.

By avoiding discretionary exits, the system maintains rule-based discipline.

Visual Signals on Chart

Blue “▲” below candle: Potential long entry

Orange/Yellow “▼” above candle: Potential short entry

Green “✔️”: Trade closed at ATR take profit

Blue (20 EMA) & Orange (100 EMA) lines: Dynamic channel reference

⚙️Strategy report properties

Position size: 25% equity per trade

Initial capital: 10,000.00 USDT

Pyramiding: 10 entries per direction

Slippage: 2 ticks

Commission: 0.055% per side

Backtest timeframe: 1-minute

Backtest instrument: HYPEUSDT

Backtesting range: Jul 28, 2025 — Aug 17, 2025

Note on Sample Size:

You’ll notice the report displays fewer than the ideal 100 trades in the strategy report above. This is intentional. The goal of the script is to isolate high-quality, short-term reversal opportunities while filtering out low-conviction setups. This means that the Barking Rat Lite strategy is very selective, filtering out over 90% of market noise. The brief timeframe shown in the strategy report here illustrates its filtering logic over a short window — not its full capabilities. As a result, even on lower timeframes like the 1-minute chart, signals are deliberately sparse — each one must pass all criteria before triggering.

For a larger dataset:

Once the strategy is applied to your chart, users are encouraged to expand the lookback range or apply the strategy to other volatile pairs to view a full sample.

💡Why 25% Equity Per Trade?

While it's always best to size positions based on personal risk tolerance, we defaulted to 25% equity per trade in the backtesting data — and here’s why:

Backtests using this sizing show manageable drawdowns even under volatile periods.

The strategy generates a sizeable number of trades, reducing reliance on a single outcome.

Combined with conservative filters, the 25% setting offers a balance between aggression and control.

Users are strongly encouraged to customize this to suit their risk profile.

What makes Barking Rat Lite valuable

Combines multiple layers of confirmation: EMA bands + FVG + RSI

Adaptive to volatility: ATR-based exits scale with market conditions

Clear, actionable visuals: Easy to monitor and manage trades

The Barking Rat ReversionsMean Reversion with Multi-Layered Precision

The Barking Rat Reversions is a short-term mean reversion strategy tailored for high-volatility markets. It combines several well-established technical tools in a configuration to identify overextended price movements likely to revert toward equilibrium. The goal is to isolate high-quality, short-term reversal opportunities while filtering out low-conviction setups.

At its core, our strategy triggers off Fair Value Gaps (FVGs) that occur a considerable distance away from a dynamically defined equilibrium band. It then validates these gaps by checking proximity to recent support and resistance drawn from swing extremes.

Additional confirmation comes from momentum filters and wick-rejection patterns, ensuring each entry aligns with both price structure and stretched momentum. Exits use volatility-adjusted profit targets. Keeping the approach disciplined and adaptive.

🧠Core Logic: Selectivity & Structure

This strategy is intentionally very selective. We have designed it to filter out roughly 95% of all market noise, highlighting only setups that pass multiple validation layers outlined below.

Fair Value Gaps (FVGs) as the Primary Trigger

FVGs identify imbalance zones where price historically retraces. These inefficient zones often become magnets for reversion as the market seeks to rebalance.

Dynamic Equilibrium Band + S/R

Defines a fair value zone with a long-term moving average and combines it with shorter-term swing pivots to establish support/resistance. Only FVGs that occur outside the band and near recent pivots are considered, ensuring reversals are sufficiently distanced and not taken too close to the mean.

Proximity to Support/Resistance

Setup validity depends on location. The strategy filters for FVGs near well-defined structural levels — areas where price has previously turned (i.e., recent swing highs or lows). This increases the likelihood that reversals are occurring at legitimate zones of confluence.

Wick-Rejection Confirmation

Confirms potential exhaustion through characteristic candle wick patterns beyond the equilibrium region. This acts as another filter to improve signal accuracy.

Sequential Filtered Signals

Custom logic ensures that a new signal in any direction must improve upon the previous one, preventing repetitive or suboptimal entries.

Multi-Step Confirmation

All validation layers must coincide on the same bar before a signal triggers, dramatically reducing false positives.

📈Chart Visuals: Designed for Clarity

To ensure transparency and easy interpretation, the script overlays intuitive visuals:

Green “▲” below a candle: Indicates a potential long entry

Red “▼” above a candle: Indicates a potential short entry

Green “✔️”: Marks exit from a trade when ATR target is met

Background shading (green/red): Indicates trade direction while active

Support/Resistance lines: Auto-plotted from recent swing levels

🔔Alerts: Stay Notified Without Watching

The strategy supports real-time alerts on candle close, ensuring that signals are only triggered once fully confirmed.

You must manually set up alerts within your TradingView account. Once configured, you’ll be able to set up one alert per instrument. This one alert covers all relevant signals and exits — ideal for hands-free monitoring.

⚙️Strategy report properties

Position size: 25% equity per trade

Initial capital: 10,000.00 USDT

Pyramiding: 10 entries per direction

Slippage: 2 ticks

Commission: 0.055% per side

Backtest timeframe: 1-minute

Backtest instrument: HYPEUSDT

Backtesting range: Jul 21, 2025 — Aug 7, 2025

Note on Sample Size:

You’ll notice the report displays fewer than the ideal 100 trades in the strategy report above. This is intentional. The goal of the script is to isolate high-quality, short-term reversal opportunities while filtering out low-conviction setups. This means that the Barking Rat Reversions strategy is ultra-selective, filtering out over 95% of market noise by enforcing multiple validation layers. The brief timeframe shown in the strategy report here illustrates its filtering logic over a short window — not its full capabilities. As a result, even on lower timeframes like the 1-minute chart, signals are deliberately sparse — each one must pass all criteria before triggering.

We conducted a broader backtest covering the period from December 5, 2024 to July 31, 2025, during which the strategy identified 968 high-probability setups on the same instrument and timeframe as the strategy report.

For a larger dataset:

Once the strategy is applied to your chart, users are encouraged to expand the lookback range or apply the strategy to other volatile pairs to view a full sample.

💡Why 25% Equity Per Trade?

While it's always best to size positions based on personal risk tolerance, we defaulted to 25% equity per trade in the backtesting data — and here’s why:

Backtests using this sizing show manageable drawdowns even under volatile periods

The strategy generates a sizeable number of trades, reducing reliance on a single outcome

Combined with conservative filters, the 25% setting offers a balance between aggression and control

Users are strongly encouraged to customize this to suit their risk profile.

🔍What Makes This Strategy Unique?

Multi-factor confirmation using FVGs, EMA deviation, RSI, wick rejection, and S/R

Clean, Intuitive Chart Experience

Real-time alerts triggered only on confirmation

Variables monitor prior reversal points, guaranteeing each new signal offers an improved entry

Tracks active positions and resets filters upon exit.

HSI1! First 30m Candle Strategy (15m Chart)## HSI1! First 30-Minute Candle Breakout Strategy (15m Chart) — Description

### Overview

This strategy is designed for trading **Hang Seng Index (HSI) Futures** on a 15-minute chart. It uses the price range established during the first 30 minutes of the Hong Kong main session (09:15–09:44:59) to define key breakout levels for a systematic trade entry each day.

### How the Strategy Works

#### 1. Reference Candle Period

- **Aggregation Window:** The strategy monitors the first two 15-minute bars of the session (09:15:00–09:44:59 HKT).

- **Range Capture:** It records the highest and lowest prices (the "reference high/low") during this window.

#### 2. Trade Setup

- After the 09:45 bar completes, the reference range is locked in.

- Throughout the rest of the trading day (within session hours), the strategy looks for breakouts beyond the reference range.

#### 3. Entry Rules

- **Long Entry (Buy):**

- Triggered if price rises to or above the reference high.

- Only entered if the user's settings permit "Buy Only" or "Both".

- **Short Entry (Sell):**

- Triggered if price falls to or below the reference low.

- Only entered if the user's settings permit "Sell Only" or "Both".

- **Single trade per day:**

- Once any trade executes, no additional trades are opened until the next session.

#### 4. Exit Rules

- **Take Profit (TP):**

- Target profit is set to a distance equal to the initial range added above the long entry (or subtracted below the short entry).

- Example: For a 100-point range, a long trade targets entry + 100 points.

- **Stop Loss (SL):**

- Longs are stopped out if price falls back to the session's reference low; shorts are stopped out if price rallies to the reference high.

#### 5. Session Control

- Active only within the regular day session (09:15–12:00 and 13:00–16:00 HKT).

- Trade tracking resets each new trading day.

#### 6. Trade Direction Manual Setting

- A user input allows restriction to "Buy Only", "Sell Only" or "Both" directions, providing discretion over daily bias.

### Example Workflow

| Step | Action |

|---------------------------|-------------------------------------------------------------------------|

| 09:15–09:44 | Aggregate first two 15m candles; record daily high/low |

| After 09:45 | Wait for a breakout (price crossing either the high or the low) |

| Long trade triggered | Enter at the reference high, target is "high + range", SL is at the low |

| Short trade triggered | Enter at the reference low, target is "low - range", SL at the high |

| Trade management | No more trades for the day, regardless of further breakouts |

| End of session (if open) | Trades may be closed per further logic or left to strategy to handle |

### Key Features and Benefits

- **Discipline:** Only one trade per day, minimizing overtrading.

- **Clarity:** Transparent entry/exit rules; no discretionary execution.

- **Flexibility:** User can bias system to buy-only, sell-only, or allow both, depending on trend or personal view.

- **Simple Risk Control:** Pre-defined stop loss and profit target for every trade.

- **Works best in:** Trending, breakout-prone markets with a history of impulsive moves early in the session.

This strategy is ideal for systematic traders looking to capture the Hang Seng's early session momentum, with robust rule-based management and minimal intervention.

S4_IBS_Mean_Rev_3candleExitOverview: