Jerry J5 Dashboard & Buy Sell Strategy

----- Strategy

The strategy allows you to select from multiple moving averages and uses the concave function and the price being above or below a user defined EMA to provide buy and sell signals. You can select long trades, short trades, or both.

Concavity describes the direction of the curve and how it bends. And, just like a direction the concavity of curves can change and we call these changing points (technically they are inflection points). These changing points are used in conjunction with the stock price relationship to user defined EMAs and provide buy and sell signals when the trend is changing.

Moving Averages available in this strategy are the Exponential Moving Average (EMA), Simple Moving Average (SMA), Weighted Moving Average (WMA), Hull Moving Average (HMA), and Arnaud Legoux Moving Average (ALMA). Best results are typically with HMA and ALMA.

The indicator can be used for every type of market: indices, stocks, cryptocurrencies, currencies and others.

----- 27 Data Point Dashboard

Short Term Trend

Total Trades

Profit Factor

Win Rate %

Net Profit $, % & ROI

Buy & Hold Profit

Max Win $ & %

Max Loss $ & %

Avg Trade $, ROI%, & Bars

Avg Win $, ROI%, & Bars

Avg Loss $, ROI%, & Bars

Max Drawdown $ & %

Open Trade P&L $ & ROI%

For the dashboard you are able to set the target profit factor, win rate, net profit target ROI, winning trade target ROI, Strategy Start Date, and the Buy and Hold Start Date. The inputs are used to color dashboard labels making it easier to identify winning and losing trades based on your criteria.

Option Traders will likely appreciate the ROI% and number of bars being readily available. For example if the Average Winning Trade has a 5% ROI over 5 bars this can help you decide when to enter a trade and how long to stay in the trade.

Some of the label data is available in the TradingView Strategy Tester. However, I wanted a custom dashboard that was always visible on my chart and the J5 dashboard displays a total of 27 data points plus buy and sell signals .

Note: We calculate the ROI for Net Profit, Avg Trade, Avg Win, Avg Loss, and Open Trade based on the capital used for those trade(s). TradingView uses a different method and calculates the return percentage based on initial capital.

Indicators are not a magic pill and should be used to support trading decisions, not to make them for you. Past performance is not a guarantee of future returns. The results of individual stocks with any strategy do not constitute proof they will repeat in the future.

I hope you enjoy the J5.

DISCLAIMER: The information contained in our scripts/indicators/ideas does not constitute financial advice or a solicitation to buy or sell any securities of any type. Trading and investing in the stock market and cryptocurrencies involves substantial risk of loss and is not suitable for every investor. I’m NOT a financial adviser. All trading strategies are used at your own risk.

Please Use the link below for more information.

스크립트에서 "profit factor"에 대해 찾기

MA trading tool v1.0Background to the tool

The tool was built out of frustration. Having traded for many years with a reasonable level of success I was always frustrated that my trading never went up a level. The world of trading is filled with people having so much more success than me and this level of FOMO really bothered me and resulted in inconsistency and countless hours sitting in front of a screen, hoping for the best. I also became a little bit of an indicator junkie - was there a holy grail indicator out there for me? I always felt that as a retail trader I was behind the curve. I started to investigate how the major market participants trade and make money and I was astounded at the level of success that they get from creating strategies and sticking to it. The market is driven largely by a "black boxes" which, for us retail traders are outside of our ability to access. I wanted to build a tool that could give me a traders edge.

Another factor that has always bothered me was when reading investing books there is a general assumption that a standard entry, say 8/13 cross over, works on all stocks. However, it is not the case and it can be frustrating for a trader using a set up and not realizing that the set up was/is the problem, not the trader. This realization alone has made a huge impact on my trading. The big boxes that control the market know this already.

Also, a lot of indicators that are available don’t take advantage of the backtesting capability provided in Tradingview. It is fairly simple to find 8-9 trades where a set up worked and then fall into the trade of assuming that it cannot fail. Knowing which set ups work and how frequently it will print will change the way that you trade.

The goal with the tool is to identify setups that have worked in the past with a high degree of profitability, high profit factor and low drawdown and using the planning tool allows you to customize the setup to find exactly what you are looking for across any tradeable asset on TradingView.

Over the past 20 years I have realized the following:

1) Not all entries and signals work the same on all stocks and knowing the historical performance of a strategy is critical

2) Not having a plan in advance lowers your probability of success

3) Developing consistency in analysis is critical

4) Developing confidence in your own plan is more important than whose trades you try to copy

5) Having 30 indicators does not help you trade better - it leads to more frustration

So here is the product of these realisations:

1) The tool looks across the most common entry strategies (RMA / EMA/ SMA/ HMA/WMA cross on 5 dimensions of type and 5 common crossovers) and can be used on 19 different time frames giving you guidance on what the best set up is for the stock you are analysing

2) It incorporates volatility into the strategy – when stocks are trading outside of a predetermined volatility band, a trade will not be entered. This accommodates traders who tend to get shaken out of trades too early.

3) It looks at the impact of “buying the dip” – often a common strategy employed by many traders which now can be backtested and reviewed to see if it actually helped or hindered the trade.

4) It measures your trade plan against your R – what you are willing to risk – and calculates your target profit based on your R multiple

5) It provides a non repaint signal on your base strategy and provides you with signals to trade smaller or shorter signals within the bigger strategy.

There are some additional visual tools:

• Squeeze signals - I am a big fan of the TTM squeeze however the Squeeze by itself can be hard to trade. Seeing a squeeze fire long on a chart can add to trade confidence.

• Seeing zones of support and resistance rather than single lines can also give you some leeway in terms of not getting pushed out of a trade too soon.

The backtester is always reviewed on a 2 to 3 year period to get an understanding of win rate %, profit ratio and average duration of trade. As an option trader knowing that a high probability move is playing out allows me to make sure that I don’t undercut the time frame for the expiration of the option relative to the historical average duration of a trade. Backtesting on shorter times is unrealistic.

Key benefits

1) It will save you a ton of time. I don’t have to sit in front of a screen watching ticks each day. I can plan for an entry, set an alert for a trade and when the conditions are met the TradingView system sends me a message and I will go and confirm a trade, execute it, set my alerts for control and move on with my life.

2) It allows me to review trade ideas in a consistent manner using the best trade plan and set up for a stock.

3) It forces me to be patient and not panic (always a good thing). With an adjustable volatility feature I can modify the volatility band in the trade plan to accommodate choppy market conditions.

4) It looks at both sides of the market (long and short) and you can calculate the impact of being market neutral or having a directional bias.

I hope this tool helps you to achieve some degree of peace in your trading.

To get access to the tool, please contact the author.

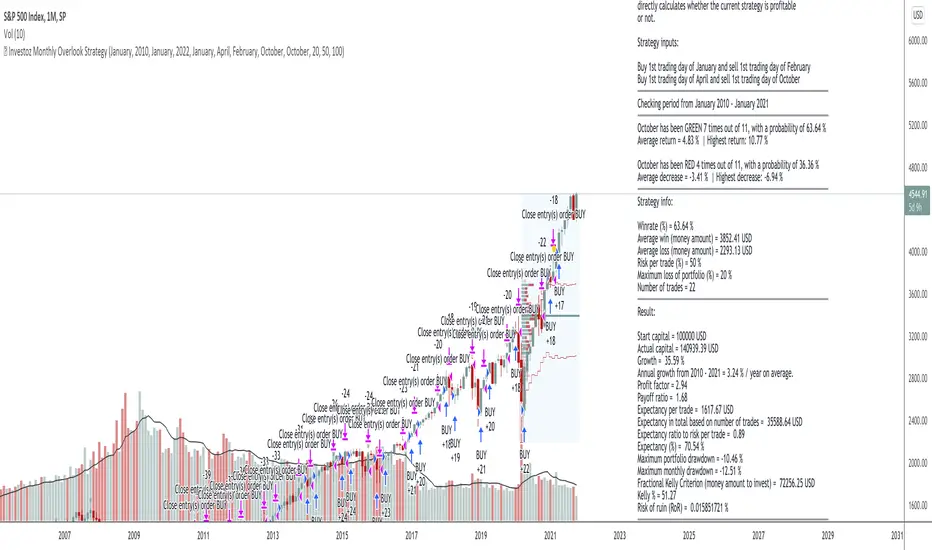

© Investoz Monthly Overlook Strategy“The best time to get involved with cyclicals is when the economy is at its weakest, earnings are at their lowest, and public sentiment is at its bleakest.”

Peter Lynch

Before I begin, read the following.

Important! The script for this strategy is only intended to work correctly for the monthly time period and does not work for other time periods, as it is based on monthly data.

The strategy

This strategy is simple and based on monthly buy and sell. However, the strategy is only intended to go long and no short positions are therefore possible.

This strategy is perfectly suited for all indices, but also for cyclical companies and cyclical markets.

Monthly analysis

You do not need to use this strategy for a buying signal only. You can use this for a more comprehensive analysis of how return per month has looked historically. It's easy to analyze, by flipping through all the months of the year. You will see average return per month, but also the largest return and decrease for each individual month.

It is also possible to choose between which time periods you want to analyze. You can go all the way back to the year 1900.

This is necessary if you are going to analyze markets that have a long historical data to analyze.

How it works

1. Start by choosing which time period the analysis or strategy should apply between.

2. Choose which month the first and second buy will be valid from. Here it is important to know that depending on which month you choose, is meant a buy after the current month's closing.

Example: 1 = January. Buy will therefore be after January closes, ie the first trading day in February. It will be displayed as 1st trading day in February. If you only want one buy option, then choose the same month for both first and second buy.

3. Choose which month the first and second sell will be valid from. The same applies here as above.

4. Choose money management according to the criteria that suit you and press "OK".

Result

Based on the choices you have made, you will now get a result of how the strategy has performed over the given period. You will be able to read following data.

Data

Start Capital -the trading capital you have from the beginning.

Actual Capital -the current trading capital you have at the moment.

Growth -percentage growth over the total trading period.

Annual growth -average return for the chosen period.

Profit factor -the profit factor looks at the total gains and losses.

Payoff ratio -looks at the average profit and loss.

Expectancy per trade -the expected profit or loss of a single trade.

Expectancy in total based on number of trades -the expected profit or loss for all the trades made.

Expectancy ratio -the power of an edge. With this, you are always looking for a positive expectancy to show you that the trade is profitable.

Expectancy % -the expected return in percentage based on all the trades

Maximun drawdown -drawdown for a single trade based on current trading capital

Fractional Kelly Criterion -the optimal amount to invest based on the strategy and multiplying it by a certain fraction (%). This results in less volatile returns and a lower chance of the account balance hitting zero.

Kelly % -percentage of capital to be put into a single trade.

Risk of ruin -the chance that you will lose all the amount you typed in for "Maximum loss of portfolio".

Conclusion

It is important to know if you have an edge in your strategy and above all to understand risk. With the help of all this information, it will therefore be easier to adapt the risk to the strategy, not the other way around. This approach applies to all types of strategies. Be aware of the risk, first!

=============================================================================================================================================================

DISCLAIMER

Any data and information is provided 'as is' solely for informational purposes, and is not intended for trading purposes or advice. Past performance is not indicative of future results.

Educate yourself on the risks associated with trading, and seek advice from an independent financial or tax advisor if you have any questions.

=============================================================================================================================================================

MACD/RVSI/Stoch/RSI/EXP(Drawdown)I have been trying for several months to get a script to work on the 1min and this one gives some good backtest results. This script will also work on higher timeframes however, I've not extensively tested on higher timeframes. My aim was to get results on about 20 crypto coins then run the 1min bots in parallel looking for small frequent profits across all the coins. If you would like me to try and fit backtest results to any coin or pair on any timeframe please do get in touch anytime.

It's based on several indicators which are combined and then a newish way for the stop loss to implement based on an exponential rising which limits the time in each trade unless the price moves in the direction of the trade. The other useful feature is drawdown minimization which previously made all of my 1minute bot attempts non-practical due to differences between backtesting and actually running the bot(s) live.

Its possible at the top to paste in strategy comments which can be used through web-hooks for auto trading bots. Leaving these blank just defaults to the pre-programmed comments that provide some indication of why a trade was exited.

It is possible to select for Short and/or Long trades. Note however, that there are exponential markers on the charts for both long and short trades in any setting. I found that this way the bot worked well with regards to timing.

The next part of the user interface settings gets a bit tricky so try and use the sample parameters provided below. For example, select a crypto coin then try some of the options below until a reasonable backtest result in obtained (or select the best from the parameter groups tested) then move down the settings interface to optimise with the remaining settings.

So 'Use MACD/RVSI', 'RSI clause' and 'Use Stochastic' are set to true for the below sample settings (1min timeframe).

MACD/RVSI Confluence Resolution (1min, 2min, 5min, 10min, 1hour)

Timeframe RSI (1min, 2min, 3min, 15min, 1hour)

FastStoch, SlowStoch (1min, 45min: 5min, 30min: 1min, 1hour: 5min, 1hour)

Eg. for FTX:ETHPERP (MACD/RVSI Confluence Resolution=1hour, Timeframe RSI= 1min, FastStoch = 1min, SlowStoch = 45min)

Setting the timings is tricky - there is a lot going on. Have a look at the chart and select/deselect the options. The MACD/RVSI Confluence Resolution shows red and green vertical regions on the chart background. The Timeframe RSI colors the candle bodies red and green. These go green if the RSI crossed over 31% or red in the RSI crossed under 69%. The MACD/RVSI Confluence Resolution is explained in more detail in one of my other scripts. Then the Slow Stoch colors above and below the price action with red or green lines depending if on an uptrend or downtrend (approximately). Where there is also an up/down trend on the faster timeframe stoch there are vertical shaded fill regions between the slow stop above/below lines.

With all the above conditions selected to represent the data (looking at strategy backtest results whilst adjusting) there is a reasonable approximation to a credible trade.

So once an ok backtest result is obtained by selecting timing settings. Its ontot the Stop Ramp Settings. This is an exponential line which rises rapidly after a period of time thus exiting the trade or going upwards with the trade. It kind of limits the maximum time a trade will stay in position which forms part of the timing aspect of this bot. Look at the chart exponential red lines and adjust the settings, along with the backtest results to select a good timing.

Then its the Drawdown Catcher and the Take Profit Setting. Start with the drawdown catcher disabled i.e. set to zero. Put in a conservative Take Profit, for example if a Take Profit at 6% gives the best backtest results, go for 4% to account for differences between backtest results and actual live bot performance.

Then start to increase the Drawdown Catcher. This shades a lime region where the bot will not enter a trade. I found that with most trades using this bot, if the price action moved in the direction of the trade (long or short) at the onset - this gave most of the good results (high probability of positive trade). Also if a trade entered at the start price and when south, the accumilated drawdown from these failing trades made all previous 1min bot attempt non=profitable in practice (even with good backtest results). The exp timing and also this drawdown reduction strategies seem to be the thing which makes this approach credible.

Try to go for settings that give a very high change of positive trade. For example, an 85% profitable trades will probably provide say 55% positive trades in practice as its always highly possible to just fit the parameters to the exact position/trade timings - and in reality going forwards these don't play out the same. Also a Profit Factor of 2 is about the minimum I would accept - again this provides for example a Profit Factor of 1.2 in practive.

However all being said - I think its possible with this bot on the 1min across lots of coins - with regularly updating settings - to make profits. (Not financial advice)

Please do get in touch if you would like me to fit this bot to anytimeframe to any trade.

MoonFlag PhD

ELLIPSE: Bidirectional Swing Trading Strategy (Strategy Version)The eternal question that has occupied humanity since its early existence is what is the meaning of life and why am I here? On a daily basis this quest for meaning is distilled into a somewhat simpler question: What is the reason for getting up every morning?

For many of us, these thoughts arise even more as autumn arrives and it gets dark, bleak and cold outside. I guess it is easier to forget about the meaning of your life, while swimming on a sandy beach, enjoying a cocktail. Than you are living you life and you don’t need to rationalize it. Everything makes perfect sense!

In winter however, you need to get more “creative”. I, for example, would always try to change my perspective of things by doing something that makes my heart beat faster, like drinking a bottle of Heineken on a Friday evening or having endless conversations with my mates about stupid things, or kicking a ball against BALLONTHEROOF 7 on a Saturday morning. During the week, I would take out my frustrations on the fitness equipment at the local gym.

But what if all of this is canceled by CORONA? All that’s left is to work for the boss and run your 10km lap twice a week. The question is, what do you do now, with this huge amount of ”free” time than any old person would give anything for. When you are young time is never ending, when you are older it is never enough. Time has reached a different dimension in these days.

However, you can still do 2 things. You can slowly let the walls come to you and give up or you can actually do something useful with your time and find something that you are good at.

For us this choice was easy. After the success of our positioning trading strategy the MATRIX, at the time of the corona lockdown, we started making a swing trading strategy for the 4H timeframe, called ELLIPSE. We have included all feedback and any improvements we received about the positioning strategy and integrated it into the 4H script.

The main requirements of the script that we had set ourselves were:

Bidirectional

Low max drawdown

High profit factor

Works on all main crypto coins

By fully focusing ourselves on the script over the past few months, I can’t help but (unhumbly) say that we have not only succeeded in our mission, but that we have absolutely surpassed ourselves!

The only bright spot in this heavy corona time is, if a drug becomes available, there is extra money in the bank!

***The script is invite-only, message us to get script access***

-------------------------------------------------------------------------------------------------

User Guidelines:

The trading strategy was designed and optimized for trading cryptocurrencies only; furthermore it works best on established cryptocurrencies that have a clear historical trend such as:

BTCUSD

ETHUSD

LTCUSD

XRPUSD

ADAUSD

The trading strategy is based on swing trading methodology. The script must therefore be used on 4h candles only .

Use USD trading pairs only (e.g. use ETHUSD instead of the ETHBTC) since the individual trend is captured more effectively and therefore gives better results.

The trading strategy is bidirectional , both long and short entries are generated.

-------------------------------------------------------------------------------------------------

Indicators used in this strategy:

Ichimoku Cloud ; acts as the leading indicator.

Volume ; without strong volume , a market move is not valid.

MACD and Vortex ; both being used as confirmation indicators.

Choppiness index ; avoids trading in choppy markets.

Simple and Exponential Moving Averages ; prevents trading against the trend.

The trading strategy is easy to use, bidirectional, trend based and without repainting, meaning once a signal has been made it is permanent and that no future data is used in the decision making. It detects the trend and filters out market noise based on more than 10 technical indicators. ONLY when all indicators align with each other the algorithm prints a LONG or SHORT signal. The trading strategy provides high probability trading signals and minimizes risk! This script aims to capture the profit from short to medium trending moves and by doing so filters out non-substantial trends and avoids the associated risks with these trades.

-------------------------------------------------------------------------------------------------

Features:

NO Repaint once candle is closed.

Stop loss feature ; set your own stop loss to manage your risks.

Customizable Display for the Ichimoku cloud indicator display.

Bidirectional ; both long and short trading positions can be enabled.

Full backtest feature ; Easily generate your own backtest results for each asset (Strategy Version Script).

Alerts ; Get notified via email / pop-up / sms / app once a signal is given! (Alert Version Script).

-------------------------------------------------------------------------------------------------

Backtest results

Below are the back test results. Only well established cryptocurrencies are displayed with a clear historical trend:

Long and short trading positions,

Signal to signal trading (no multiple orders),

Initial Capital: 10 000 USD,

Order size: 10% of equity per trade,

commission fee 0.1%, period: start of chart,

Exchange-----Asset------Timeframe---Percent Profitable----Profit Factor---Total Trades----Max Drawdown----------Net Profit------

Bínance------BTCUSDT------4H-----------------54.4---------------5.32-----------------57----------------1.58%------------40.34%-(4034 USD)

Bínance------ETHUSD-------4H-----------------50.9---------------5.01---------------- 57----------------2.96%------------54.93%-(5493 USD)

Bínance------LTCUSD--------4H-----------------61.0---------------5.08-----------------59----------------2.09%------------57.06%-(5706 USD)

Bínance------XRPUSD-------4H-----------------43.13--------------3.52-----------------51----------------2.42%------------43.13%-(4313 USD)

Bínance------ADAUSD-------4H-----------------57.5---------------3.36-----------------47----------------3.46%------------40.82%-(4082 USD)

-------------------------------------------------------------------------------------------------

Reminder: Use this trading strategy at your own risk and trade responsibly. We are not responsible for any financial loss using this strategy.

***The script is invite-only, message us to get script access***

Dompeet Pompeet (Breakout bot)Dompeet Pompeet is my first attempt at a viable swingtrading algo.

It uses volatility and some trend analysis to enter trade when the market is about to breakout or break down. Having a trailing stop locks in profits and prevents runaway losses for low drawdown and 2:1 profit factor.

Settings to use:

BTCUSD or XBTUSD

4hr Timeframe or 2hr or 1hr (not shorter)

Bars window: 13, 16 or 20 bars

Moving average settings: 100/10 EMA to confirm trend

Trade the Trend - check on to only take trades long in a confirmed uptrend (vice versa short), otherwise it will attempt to buy and sell counter trend, which increases profits but also increases loss rate.

Trailing stop, values from 2-5% give the best results.

Take with a pinch of salt, there are some bugs in pine script which are difficult to track down but overall I'm pleased with the idea.

TrendMaster, v. 5.1TrendMaster (ver 5.0, a.k.a. "Mr. T") is a trend-anticipating system which shows eye-popping results. Rather than a simple "trend-rider" which continually lags, TrendMaster uses pattern recognition to anticipate trend changes. It hunts for turns in market cycles using a proprietary decision matrix of 27 "trade triggers" (variants of classic technical indicators). In backtesting the annualized return (July 2017-July2018) of the top 100 largest capitalized equities, not only did its results beat the indexes, but it outstripped a buy-and-hold strategy by a whopping 700%: i.e., while the 100 largest equities had an average annual yield of 17%, the strategy produced a 129% return across the entire range of stocks.* Even more staggering results can be seen when using the system in strongly-trending markets like cryptos. (See, for instance, the particularly stunning results for Bitcoin Cash in the screen shot at the end). [ ]

The following charts give you some sample tests of best performing (top chart) and worst performing (bottom chart) equities, ETFs, and cryptos (July 2017-July2018 time range).

TrendMaster / "Mr T" 5.1, Example Annualized returns

>>> Higher Performing Instruments (best performing interval between 15min - 1 day) <<<

Symbol Description Interval % Return Trades % Profitable Profit Factor Max Drawdown Sharpe Ratio Buy & Hold

DUST 3x Short Gold miners 30 min 3050% 421 43% 1.5 ( -17% ) 1.8 ( - 27 % )

NUGT 3x Long Gold miners 15 min 3300% 423 44 1.2 ( -11% ) 1.2 ( - 10 % )

APPL Apple, Inc 1 hour 118% 354 46 2.2 ( -6% ) 1.3 32%

GOOG Alphabet, Inc 30 min 128% 660 44 1.9 ( -5% ) 1 27%

BABA Alibaba Group 30 min 389% 642 46 2.3 ( -3% ) 1.6 37%

BTC/USDT Bitcoin 1 hour 1000000% 1573 53 3.1 ( -8% ) 1 57%

ETH/USDT Ethereum 1 hour 13000000% 1533 55 3.2 ( -12% ) 1.2 56%

LTC/ USDT Litecoin 30 min 5000000% 1946 54 2.8 ( -12% ) 1.2 ( - 71% )

>>> Lower Performing Instruments and/or Lower Performing Market Settings (worst performing interval between 15 min - 1 day) <<<

Symbol Description Interval % Return Trades % Profitable Profit Factor Max Drawdown Sharpe Ratio Buy & Hold

PSQ Short Nasdaq ETF 5 min ( - 14% ) 1894 28% ( - 0.9 % ) ( -20% ) ( -0.3 ) ( - 20 % )

SH Short S&P ETF 1 day 20% 35 51% 2.8 ( -7% ) 0.5 ( - 12 % )

MSFT Microsoft 1 hour 37% 249 37% 1.4 ( -4% ) 0.5 45%

AZN Astrazeneca, PLC 1 day 22% 32 50% 1.9 ( -6% ) 0.3 ( - 4 % )

MUFG Mitsubishi UFJ 1 day 296% 1255 39% ( - 0.6 ) ( -27% ) ( - 0.3 ) ( - 16 % )

BTC/USDT Bitcoin 1 min ( - 33 % ) 1349 25% ( - 0.5 ) ( - 33% ) ( - 1.1 ) 5%

ETH/USDT Ethereum 1 min ( - 40 % ) 1595 24% ( - 0.6 ) ( -40% ) ( - 1.1 ) 6%

LTC/USDT Litecoin 1 day 123 14 57% 4.8 ( - 5% ) 1.1 ( - 48% )

Note, of course, that any trend-anticipating bot has limitations. The Lower Performing results above show that because the system seeks gains in trends, it can underperform in choppy, aimless markets. Similarly, very short time frames (i.e. 1 - 5 minutes) can provide too many gaps and too few runs for it to reliably track. Backtesting is therefore essential to make sure this system is suitable for your (a) market, (b) time frame, and (c) trading mindset. On the other hand, a broad range of data show that almost any trending market, in almost any time frame, can be very productive.

Contact us if you would like to experience this bot.

I_Heikin Ashi CandleWhen apply a strategy to Heikin Ashi Candle chart (HA candle), the strategy will use the open/close/high/low values of the Heikin Ashi candle to calculate the Profit and Loss, hence also affecting the Percent Profitable, Profit Factor, etc., often resulting a unrealistic high Percent Profitable and Profit Factor, which is misleading. But if you want to use the HA candle's values to calculate your indicator / strategy, but pass the normal candle's open/close/high/low values to the strategy to calculate the Profit / Loss, you can do this:

1) set up the main chart to be a normal candle chart

2) use this indicator script to plot a secondary window with indicator looks exactly like a HA-chart

3) to use the HA-candle's open/close/high/low value to calculate whatever indicator you want (you may need to create a separate script if you want to plot this indicator in a separate indicator window)

[AutoView] MovingAvg Cross - Video AttachedThere is nothing special or spectacular about this script. It's your standard Moving Average Cross Strategy. It is actually a built in script everyone has access to already. I only changed some of the settings and flipped the orders.

The reason I actually published this, is because people have been asking me what the best way to find the best settings for a strategy. So I made a YouTube video showing people how I personally do it. I took this built in strategy and within 5 minutes took it from a net profit loss and profit factor of 0.5 to a net profit win with a profit factor of 3-5.

Of course this is only on the 1 minute candles, so forward testing the strategy is a must as I do not recommend straight up taking this and trading it.

You can watch the video here:

www.youtube.com

Hope this helps everyone speed up their back testing and fine tuning their strategies.

CM Stochastic POP Method 2-Jake Bernstein_V1Yesterday Jake Bernstein authorized me to post his updated results with the Stochastic Pop Trading System he developed many years ago.

You can take a look at the Original System with Updated Settings at

This indicator is a different set of rules Jake mentioned in the PDF he allowed me to post.

To view the PDF use this link:

dl.dropboxusercontent.com

Today we’re releasing the version described in the PDF that uses the StochK values of 55, 50, and 45. The rules are discussed in the PDF but here is a simple breakdown:

Enter Long when StochK is below 50 and Crosses Above 55

Exit Long on Cross Below 55

Enter Short when StochK is Above 50 and crosses Below 45

Exit Short on Cross Above 45

Two Important Items to understand about this method:

To code the rules Precisely we need a function that will be available when Strategy Capabilities are released on TradingView.

There is one of Jakes Profit Maximizing Strategies that needs to be integrated with this code…which again we need the Strategy based Function that will be coming soon.

To Compare this system to the Stochastic Pop Method 1 System shown yesterday at I used the same Symbol and dates for you to compare…but remember to give this Method 2 System a Fair Look/Evaluation…we need the Soon To Be Released…TradingView Strategy Capabilities.

BackTesting Results Example: EUR-USD Daily Chart Since 01/01/2005

Strategy 1 – Stochastic Pop Method 2 System:

Go Long When Stochasticis below 50 and Crosses Above 55. Go Short When Stochastic is above 50 and Crosses Below 45. Exit Long/Short When Stochastic has a Reverse Cross of Entry Value.

Results:

Total Trades = 151

Profit = 40,758 Pips

Win% = 37.1%

Profit Factor = 1.26

Avg Trade = 270 Pips Profit

***Most Consecutive Wins = 4 ... Most Consecutive Losses = 7

Strategy 2:

Rules - Proprietary Optimization Jake Will Teach. Only Added 1 Additional Exit Rule.

Results:

Total Trades = 151

Profit = 60.305 Pips

Win% = 37.1%

Profit Factor = 1.38

Avg Trade = 399 Pips Profit

***Most Consecutive Wins = 4 ... Most Consecutive Losses = 7

Indicator Includes:

-Ability to Color Candles (CheckBox In Inputs Tab)

Green = Long Trade

Blue = No Trade

Red = Short Trade

Jake Bernstein will be a contributor on TradingView when Backtesting/Strategies are released. Jake is one of the Top Trading System Developers in the world with 45+ years experience and he is going to teach TradingView.com’s community how to create Trading Systems and how to Optimize the correct way.

Link To PDF:

dl.dropboxusercontent.com

Link to Original Version of Indicator with Updated Settings.

CM Stochastic POP Method 1 - Jake Bernstein_V1A good friend ucsgears recently published a Stochastic Pop Indicator designed by Jake Bernstein with a modified version he found.

I spoke to Jake this morning and asked if he had any updates to his Stochastic POP Trading Method. Attached is a PDF Jake published a while back (Please read for basic rules, which also Includes a New Method). I will release the Additional Method Tomorrow.

Jake asked me to share that he has Updated this Method Recently. Now across all symbols he has found the Stochastic Values of 60 and 30 to be the most profitable. NOTE - This can be Significantly Optimized for certain Symbols/Markets.

Jake Bernstein will be a contributor on TradingView when Backtesting/Strategies are released. Jake is one of the Top Trading System Developers in the world with 45+ years experience and he is going to teach how to create Trading Systems and how to Optimize the correct way.

Below are a few Strategy Results....Soon You Will Be Able To Find Results Like This Yourself on TradingView.com

BackTesting Results Example: EUR-USD Daily Chart Since 01/01/2005

Strategy 1:

Go Long When Stochastic Crosses Above 60. Go Short When Stochastic Crosses Below 30. Exit Long/Short When Stochastic has a Reverse Cross of Entry Value.

Results:

Total Trades = 164

Profit = 50, 126 Pips

Win% = 38.4%

Profit Factor = 1.35

Avg Trade = 306 Pips Profit

***Most Consecutive Wins = 3 ... Most Consecutive Losses = 6

Strategy 2:

Rules - Proprietary Optimization Jake Will Teach. Only Added 1 Additional Exit Rule.

Results:

Total Trades = 164

Profit = 62, 876 Pips!!!

Win% = 38.4%

Profit Factor = 1.44

Avg Trade = 383 Pips Profit

***Most Consecutive Wins = 3 ... Most Consecutive Losses = 6

Strategy 3:

Rules - Proprietary Optimization Jake Will Teach. Only added 1 Additional Exit Rule.

Results:

Winning Percent Increases to 72.6%!!! , Same Amount of Trades.

***Most Consecutive Wins = 21 ...Most Consecutive Losses = 4

Indicator Includes:

-Ability to Color Candles (CheckBox In Inputs Tab)

Green = Long Trade

Blue = No Trade

Red = Short Trade

-Color Coded Stochastic Line based on being Above/Below or In Between Entry Lines.

Link To Jakes PDF with Rules

dl.dropboxusercontent.com

Autoback Grid Lab [trade_lexx]Autoback Grid Lab: Your personal laboratory for optimizing grid strategies.

Introduction

First of all, it is important to understand that Autoback Grid Lab is a powerful professional tool for backtesting and optimization, created specifically for traders using both grid strategies and regular take profit with stop loss.

The main purpose of this script is to save you weeks and months of manual testing and parameter selection. Instead of manually testing one combination of settings after another, Autoback Grid Lab automatically tests thousands of unique strategies on historical data, providing you with a comprehensive report on the most profitable and, more importantly, sustainable ones.

If you want to find mathematically sound, most effective settings for your grid strategy on a specific asset and timeframe, then this tool was created for you.

Key Features

My tool has functionality that transforms the process of finding the perfect strategy from a routine into an exciting exploration.

🧪 Mass testing of thousands of combinations

The script is able to systematically generate and run a huge number of unique combinations of parameters through the built-in simulator. You set the ranges, and the indicator does all the work, testing all possible options for the following grid settings:

* Number of safety orders (SO Count)

* Grid step (SO Step)

* Step Multiplier (SO Multiplier) for building nonlinear grids

* Martingale for controlling the volume of subsequent orders

* Take Profit (%)

* Stop Loss (%), with the possibility of calculating both from the entry point and from the dynamic breakeven line

* The volume of the base order (Volume BO) as a percentage of the deposit

🏆 Unique `FinalScore` rating system

Sorting strategies by net profit alone is a direct path to self—deception and choosing strategies that are "tailored" to history and will inevitably fail in real trading. To solve this problem, we have developed FinalScore, a comprehensive assessment of the sustainability and quality of the strategy.

How does it work?

FinalScore analyzes each combination not one by one, but by nine key performance metrics at once, including Net Profit, Drawdown, Profit Factor, WinRate, Sharpe coefficients, Sortino, Squid and Omega. Each of these indicators is normalized, that is, reduced to a single scale. Then, to test the strategy for strength, the system performs 30 iterations, each time assigning random weights to these 9 metrics. A strategy gets a high FinalScore only if it shows consistently high results under different evaluation criteria. This proves her reliability and reduces the likelihood that her success was an accident.

📈 Realistic backtesting engine

The test results are meaningless if they do not take into account the actual trading conditions. Our simulator simulates real trading as accurately as possible, taking into account:

* Leverage: Calculation of the required margin to open and hold positions.

* Commission: A percentage commission is charged each time an order is opened and closed.

* Slippage: The order execution price is adjusted by a set percentage to simulate real market conditions.

* Liquidation model: This is one of the most important functions. The script continuously monitors the equity of the account (capital + unrealized P&L). If equity falls below the level of the supporting margin (calculated from the current value of the position), the simulator forcibly closes the position, as it would happen on a real exchange. This eliminates unrealistic scenarios where the strategy survives after a huge drawdown.

🔌 Integration with external signals

The indicator operates in two modes:

1. `No Signal': Standard mode. The trading cycle starts immediately as soon as the previous one has been closed. Ideal for testing the "pure" mechanics of the grid.

2. `External Signal`: In this mode, a new trading cycle will start only when a signal is received from an external source. You can connect any other indicator (such as the RSI, MACD, or your own strategy) to the script and use it as a trigger to log in. This allows you to combine the power of a grid strategy with your own entry points.

📊 Interactive and informative results panel

Upon completion of the calculations, a detailed table with the TOP N best strategies appears on the screen, sorted according to your chosen criterion. For each strategy in the rating, you will see not only the key metrics (Profit, Drawdown, duration of transactions), but also all the parameters that led to this result. You can immediately take these settings and apply them in your trading.

Application Options: How To Solve Your Problems

Autoback Grid Lab is a flexible tool that can be adapted to solve various tasks, from complete grid optimization to fine—tuning existing strategies. Here are some key scenarios for its use:

1. Complete Optimization Of The Grid Strategy

This is the basic and most powerful mode of use. You can find the most efficient grid configuration for any asset from scratch.

* How to use: Set wide ranges for all key grid parameters ('SO Count`, SO Step, SO Multiplier, Martingale, TP, etc.).

* In the `No Signal` mode: You will find the most stable grid configuration that works as an independent, constantly active strategy, regardless of which-or entrance indicators.

* In the `External Signal` mode: You can connect your favorite indicator for input (for example, RSI, MACD or a complex author's script) and find the optimal grid parameters that best complement your input signals. This allows you to turn a simple signaling strategy into a full-fledged grid system.

2. Selecting the Optimal Take Profit and Stop Loss for Your Strategy

Do you already have an entry strategy, but you are not sure where it is best to put Take Profit and Stop Loss? Autoback Grid Lab can solve this problem as well.

* How to use:

1. Disable optimization of all grid parameters (uncheck SO Count, SO Step, Martingale, etc.). Set the Min value for SO Count to 0.

2. Set the ranges for iteration only for 'Take Profit` and `Stop Loss'.

3. Turn on the External Signal mode and connect your indicator with input signals.

* Result: The script will run your historical entry signals with hundreds of different TP and SL combinations and show you which stop order levels bring maximum profit with minimal risk specifically for your entry points.

3. Building a Secure Network with Risk Management

Many traders are afraid of grid strategies because of the risk of large drawdowns. With the help of the optimizer, you can purposefully find the parameters for such a grid, which includes mandatory risk management through Stop Loss.

* How to use: Enable and set the range for Stop Loss, along with other grid parameters. Don't forget to test both types of SL calculations (`From entry point` and `From breakeven line`) to determine which one works more efficiently.

* Result: You will find balanced strategies in which the grid parameters (number of orders, martingale) and the Stop Loss level are selected in such a way as to maximize profits without going beyond the acceptable risk level for you.

How To Use The Indicator (Step-By-Step Guide)

Working with the Autoback Grid Lab is a sequential process consisting of four main steps: from initial setup to analysis of the finished results. Follow this guide to get the most out of the tool.

Step 1: Initial Setup

1. Add the indicator to the chart of your chosen asset and timeframe.

2. Open the script settings. The first thing you should pay attention to is the ⚙️ Optimization Settings ⚙️ group.

3. Set the `Bars Count'. This parameter determines how much historical data will be used for testing.

* Important: The more bars you specify, the more statistically reliable the backtest results will be. We recommend using the maximum available value (25,000) to test strategies at different market phases.

* Consider: The indicator performs all calculations on the last historical bar. After applying the TradingView settings, it will take some time to load all the specified bars. The results table will appear only after the data is fully loaded. Don't worry if it doesn't appear instantly. And if an error occurs, simply switch the number of combinations to 990 and back to 1000 until the table appears.

Step 2: Optimization Configuration

At this stage, you define the "universe" of parameters that our algorithm will explore.

1. Set the search ranges (🛠 Optimization Parameters 🛠 group).

For each grid parameter that you want to optimize (for example, SO Count or `Take Profit'), you must specify three values:

* Min: The minimum value of the range.

* Max: The maximum value of the range.

* Step: The step with which the values from Min to Max will be traversed.

*Example:* If you set Min=5, Max=10, and Step=1 for SO Count, the script will test strategies with 5, 6, 7, 8, 9, and 10 safety orders.

* Tip for users: To get the first results quickly, start with a larger step (for example, TP from 0.5% to 2.5% in 0.5 increments instead of 0.1). After you identify the most promising areas, you can perform a deeper analysis by expanding the ranges around these values.

2. Set Up Money Management (Group `💰 Money Management Settings 💰`).

Fill in these fields with the values that best match your actual trading conditions. This is critically important for obtaining reliable results.

* Capital: Your initial deposit.

* Leverage: Leverage.

* Commission (%): Your trading commission as a percentage.

* Slippage (%): Expected slippage.

* Liquidation Level (%): The level of the supporting margin (MMR in %). For example, for Binance Futures, this value is usually between 0.4% and 2.5%, depending on the asset and position size. Specify this value for your exchange.

3. Select the Sorting Criterion and the Direction (Group `⚙️ Optimization Settings ⚙️').

* `Sort by': Specify the main criteria by which the best strategies will be selected and sorted. I strongly recommend using finalScore to find the most balanced and sustainable strategies.

* `Direction': Choose which trades to test: Long, Short or Both.

Step 3: Start Testing and Work with "Parts"

The total number of unique combinations generated based on your ranges can reach tens of millions. TradingView has technical limitations on the number of calculations that the script can perform at a time. To get around this, I implemented a "Parts" system.

1. What are `Part` and `Combinations in Part'?

* `Combinations in Part': This is the number of backtests that the script performs in one run (1000 by default).

* `Part`: This is the number of the "portion" of combinations that you want to test.

2. How does it work in practice?

* After you have everything set up, leave Part:1 and wait for the results table to appear. You will see the TOP N best strategies from the first thousand tested.

* Analyze them. Then, to check the next thousand combinations, just change the Part to 2 in the settings and click OK. The script will run a test for the next batch.

* Repeat this process by increasing the Part number (`3`, 4, 5...), until you reach the last available part.

* Where can I see the total number of parts? In the information row below the results table, you will find Total parts. This will help you figure out how many more tests are left to run.

Step 4: Analyze the Results in the Table

The results table is your main decision—making tool. It displays the best strategies found, sorted by the criteria you have chosen.

1. Study the performance metrics:

* Rating: Position in the rating.

* Profit %: Net profit as a percentage of the initial capital.

* Drawdown%: The maximum drawdown of the deposit for the entire test period.

* Max Length: The maximum duration of one transaction in days, hours and minutes.

* Trades: The total number of completed trades.

2. Examine the winning parameters:

* To the right of the performance metrics are columns showing the exact settings that led to this result ('SO Count`, SO Step, TP (%), etc.).

3. How to choose the best strategy?

* Don't chase after the maximum profit! The strategy with the highest profit often has the highest drawdown, which makes it extremely risky.

* Seek a balance. The ideal strategy is a compromise between high profitability, low drawdown (Drawdown) and the maximum length of trades acceptable to you (Max Length).

* finalScore was created to find this balance. Trust him — he often highlights not the most profitable, but the most stable and reliable options.

Detailed Description Of The Settings

This section serves as a complete reference for each parameter available in the script settings. The parameters are grouped in the same way as in the indicator interface for your convenience.

Group: ⚙️ Optimization Settings ⚙️

The main parameters governing the testing process are collected here.

* `Enable Optimizer': The main switch. Activates or deactivates all backtesting functionality.

* `Direction': Determines which way trades will be opened during the simulation.

* Long: Shopping only.

* Short: Sales only.

* Both: Testing in both directions. Important: This mode only works in conjunction with an External Signal, as the script needs an external signal to determine the direction for each specific transaction.

* `Signal Mode`: Controls the conditions for starting a new trading cycle (opening a base order).

* No Signal: A new cycle starts immediately after the previous one is completed. This mode is used to test "pure" grid mechanics without reference to market conditions.

* External Signal: A new cycle begins only when a signal is received from an external indicator connected via the Signal field.

* `Signal': A field for connecting an external signal source (works only in the `External Signal` mode). You can select any other indicator on the chart.

* For Long** trades, the signal is considered received if the value of the external indicator ** is greater than 0.

* For Short** trades, the signal is considered received if the value of the external indicator ** is less than 0.

* `Bars Count': Sets the depth of the history in the bars for the backtest. The maximum value (25000) provides the most reliable results.

* `Sort by`: A key criterion for selecting and ranking the best strategies in the final table.

* FinalScore: Recommended mode. A comprehensive assessment that takes into account 9 metrics to find the most balanced and sustainable strategies.

* Profit: Sort by net profit.

* Drawdown: Sort by minimum drawdown.

* Max Length: Sort by the minimum length of the longest transaction.

* `Combinations Count': Indicates how many of the best strategies (from 1 to 50) will be displayed in the results table.

* `Close last trade`: If this option is enabled, any active trade will be forcibly closed at the closing price of the last historical bar. For grid strategies, it is recommended to always enable this option in order to get the correct calculation of the final profit and eliminate grid strategies that have been stuck for a long time.

Group: 💰 Money Management Settings 💰

The parameters in this group determine the financial conditions of the simulation. Specify values that are as close as possible to your actual values in order to get reliable results.

* `Capital': The initial deposit amount for the simulation.

* `Leverage`: The leverage used to calculate the margin.

* `Slippage` (%): Simulates the difference between the expected and actual order execution price. The specified percentage will be applied to each transaction.

* `Commission` (%): The trading commission of your exchange as a percentage. It is charged at the execution of each order (both at opening and closing).

* `Liquidation Level' (%): Maintenance Margin Ratio. This is a critical parameter for a realistic test. Liquidation in the simulator occurs if the Equity of the account (Capital + Unrealized P&L) falls below the level of the supporting margin.

Group: 🛠 Optimization Parameters 🛠

This is the "heart" of the optimizer, where you set ranges for iterating through the grid parameters.

* `Part`: The portion number of the combinations to be tested. Start with 1, and then increment (`2`, 3, ...) sequentially to check all generated strategies.

* `Combinations in Part': The number of backtests performed at a time (in one "Part"). Increasing the value may speed up the process, but it may cause the script to error due to platform limitations. If an error occurs, it is recommended to switch to the step below and back.

Three fields are available for each of the following parameters (`SO Count`, SO Step, SO Multiplier, etc.):

* `Min`: Minimum value for testing.

* `Max': The maximum value for testing.

* `Step`: The step with which the values in the range from Min to Max will be iterated over.

There is also a checkbox for each parameter. If it is enabled, the parameter will be optimized in the specified range. If disabled, only one value specified in the Min field will be used for all tests.

* 'Stop Loss': In addition to the standard settings Min, Max, Step, it has an additional parameter:

* `Type`: Defines how the stop loss price is calculated.

* From entry point: The SL level is calculated once from the entry price (base order price).

* From breakeven line: The SL level is dynamically recalculated from the average position price after each new safety order is executed.

Group: ⚡️Filters⚡️

Filters allow you to filter out those results from the final table that do not meet your minimum requirements.

For each filter (`Max Profit`, Min Drawdown, `Min Trade Length`), you can:

1. Turn it on or off using the checkbox.

2. Select the comparison condition: Greater (More) or Less (Less).

3. Set a threshold value.

*Example:* If you set Less and 20 for the Min Drawdown filter, only those strategies with a maximum drawdown of less than 20% will be included in the final table.

Group: 🎨 Visual Settings 🎨

Here you can customize the appearance of the results table.

* `Position': Selects the position of the table on the screen (for example, Bottom Left — bottom left).

* `Font Size': The size of the text in the table.

* `Header Background / Data Background`: Background colors for the header and data cells.

* `Header Font Color / Data Font Color`: Text colors for the header and data cells.

Important Notes and Limitations

So that you can use the Autoback Grid Lab as efficiently and consciously as possible, please familiarize yourself with the following key features of its work.

1. It is a Tool for Analysis, not for Signals

It is extremely important to understand that this script does not generate trading signals in real time. Its sole purpose is to conduct in—depth research (**backtesting**) on historical data.

* The results you see in the table are a report on how a particular strategy would have worked in the past.

* The script does not provide alerts and does not draw entry/exit points on the chart for the current market situation.

* Your task is to take the best sets of parameters found during optimization and use them in your real trading, for example, when setting up a trading bot or in a manual trading system.

2. Features Of Calculations (This is not a "Repainting")

You will notice that the results table appears and is updated only once — when all historical bars on the chart are loaded. It does not change in real time with each tick of the price.

This is correct and intentional behavior.:

* To test thousands, and sometimes millions of combinations, the script needs to perform a huge amount of calculations. In the Pine Script™ environment, it is technically possible to do this only once, at the very last bar in history.

* The script does not show false historical signals, which then disappear or change. It provides a static report on the results of the simulation, which remains unchanged for a specific historical period.

3. Past Results do not Guarantee Future Results.

This is the golden rule of trading, and it fully applies to the results of backtesting. Successful strategy performance in the past is not a guarantee that it will be as profitable in the future. Market conditions, volatility and trends are constantly changing.

My tool, especially when sorting by finalScore, is aimed at finding statistically stable and reliable strategies to increase the likelihood of their success in the future. However, it is a tool for managing probabilities, not a crystal ball for predicting the future. Always use proper risk management.

4. Dependence on the Quality and Depth of the Story

The reliability of the results directly depends on the quantity and quality of the historical data on which the test was conducted.

* Always strive to use the maximum number of bars available (`Bars Count: 25,000`) so that your strategy is tested on different market cycles (rise, fall, flat).

* The results obtained on data for one month may differ dramatically from the results obtained on data for two years. The longer the testing period, the higher the confidence in the parameters found.

Conclusion

The Autoback Grid Lab is your personal research laboratory, designed to replace intuitive guesses and endless manual selection of settings with a systematic, data—driven approach. Experiment with different assets, timeframes, and settings ranges to find the unique combinations that best suit your trading style.

HorizonSigma Pro [CHE]HorizonSigma Pro

Disclaimer

Not every timeframe will yield good results . Very short charts are dominated by microstructure noise, spreads, and slippage; signals can flip and the tradable edge shrinks after costs. Very high timeframes adapt more slowly, provide fewer samples, and can lag regime shifts. When you change timeframe, you also change the ratios between horizon, lookbacks, and correlation windows—what works on M5 won’t automatically hold on H1 or D1. Liquidity, session effects (overnight gaps, news bursts), and volatility do not scale linearly with time. Always validate per symbol and timeframe, then retune horizon, z-length, correlation window, and either the neutral band or the z-threshold. On fast charts, “components” mode adapts quicker; on slower charts, “super” reduces noise. Keep prior-shift and calibration enabled, monitor Hit Rate with its confidence interval and the Brier score, and execute only on confirmed (closed-bar) values.

For example, what do “UP 61%” and “DOWN 21%” mean?

“UP 61%” is the model’s estimated probability that the close will be higher after your selected horizon—directional probability, not a price target or profit guarantee. “DOWN 21%” still reports the probability of up; here it’s 21%, which implies 79% for down (a short bias). The label switches to “DOWN” because the probability falls below your short threshold. With a neutral-band policy, for example ±7%, signals are: Long above 57%, Short below 43%, Neutral in between. In z-score mode, fixed z-cutoffs drive the call instead of percentages. The arrow length on the chart is an ATR-scaled projection to visualize reach; treat it as guidance, not a promise.

Part 1 — Scientific description

Objective.

The indicator estimates the probability that price will be higher after a user-defined horizon (a chosen number of bars) and emits long, short, or neutral decisions under explicit thresholds. It combines multi‑feature, z‑normalized inputs, adaptive correlation‑based weighting, a prior‑shifted sigmoid mapping, optional rolling probability calibration, and repaint‑safe confirmation. It also visualizes an ATR‑scaled forward projection and prints a compact statistics panel.

Data and labeling.

For each bar, the target label is whether price increased over the past chosen horizon. Learning is deliberately backward‑looking to avoid look‑ahead: features are associated with outcomes that are only known after that horizon has elapsed.

Feature engineering.

The feature set includes momentum, RSI, stochastic %K, MACD histogram slope, a normalized EMA(20/50) trend spread, ATR as a share of price, Bollinger Band width, and volume normalized by its moving average. All features are standardized over rolling windows. A compressed “super‑feature” is available that aggregates core trend and momentum components while penalizing excessive width (volatility). Users can switch between a “components” mode (weighted sum of individual features) and a “super” mode (single compressed driver).

Weighting and learning.

Weights are the rolling correlations between features (evaluated one horizon ago) and realized directional outcomes, smoothed by an EMA and optionally clamped to a bounded range to stabilize outliers. This produces an adaptive, regime‑aware weighting without explicit machine‑learning libraries.

Scoring and probability mapping.

The raw score is either the weighted component sum or the weighted super‑feature. The score is standardized again and passed through a sigmoid whose steepness is user‑controlled. A “prior shift” moves the sigmoid’s midpoint to the current base rate of up moves, estimated over the evaluation window, so that probabilities remain well‑calibrated when markets drift bullish or bearish. Probabilities and standardized scores are EMA‑smoothed for stability.

Decision policy.

Two modes are supported:

- Neutral band: go long if the probability is above one half plus a user‑set band; go short if it is below one half minus that band; otherwise stay neutral.

- Z‑score thresholds: use symmetric positive/negative cutoffs on the standardized score to trigger long/short.

Repaint protection.

All values used for decisions can be locked to confirmed (closed) bars. Intrabar updates are available as a preview, but confirmed values drive evaluation and stats.

Calibration.

An optional rolling linear calibration maps past confirmed probabilities to realized outcomes over the evaluation window. The mapping is clipped to the unit interval and can be injected back into the decision logic if desired. This improves reliability (probabilities that “mean what they say”) without necessarily improving raw separability.

Evaluation metrics.

The table reports: hit rate on signaled bars; a Wilson confidence interval for that hit rate at a chosen confidence level; Brier score as a measure of probability accuracy; counts of long/short trades; average realized return by side; profit factor; net return; and exposure (signal density). All are computed on rolling windows consistent with the learning scheme.

Visualization.

On the chart, an arrowed projection shows the predicted direction from the current bar to the chosen horizon, with magnitude scaled by ATR (optionally scaled by the square‑root of the horizon). Labels display either the decision probability or the standardized score. Neutral states can display a configurable icon for immediate recognition.

Computational properties.

The design relies on rolling means, standard deviations, correlations, and EMAs. Per‑bar cost is constant with respect to history length, and memory is constant per tracked series. Graphical objects are updated in place to obey platform limits.

Assumptions and limitations.

The method is correlation‑based and will adapt after regime changes, not before them. Calibration improves probability reliability but not necessarily ranking power. Intrabar previews are non‑binding and should not be evaluated as historical performance.

Part 2 — Trader‑facing description

What it does.

This tool tells you how likely price is to be higher after your chosen number of bars and converts that into Long / Short / Neutral calls. It learns, in real time, which components—momentum, trend, volatility, breadth, and volume—matter now, adjusts their weights, and shows you a probability line plus a forward arrow scaled by volatility.

How to set it up.

1) Choose your horizon. Intraday scalps: 5–10 bars. Swings: 10–30 bars. The default of 14 bars is a balanced starting point.

2) Pick a feature mode.

- components: granular and fast to adapt when leadership rotates between signals.

- super: cleaner single driver; less noise, slightly slower to react.

3) Decide how signals are triggered.

- Neutral band (probability based): intuitive and easy to tune. Widen the band for fewer, higher‑quality trades; tighten to catch more moves.

- Z‑score thresholds: consistent numeric cutoffs that ignore base‑rate drift.

4) Keep reliability helpers on. Leave prior shift and calibration enabled to stabilize probabilities across bullish/bearish regimes.

5) Smoothing. A short EMA on the probability or score reduces whipsaws while preserving turns.

6) Overlay. The arrow shows the call and a volatility‑scaled reach for the next horizon. Treat it as guidance, not a promise.

Reading the stats table.

- Hit Rate with a confidence interval: your recent accuracy with an uncertainty range; trust the range, not only the point.

- Brier Score: lower is better; it checks whether a stated “70%” really behaves like 70% over time.

- Profit Factor, Net Return, Exposure: quick triage of tradability and signal density.

- Average Return by Side: sanity‑check that the long and short calls each pull their weight.

Typical adjustments.

- Too many trades? Increase the neutral band or raise the z‑threshold.

- Missing the move? Tighten the band, or switch to components mode to react faster.

- Choppy timeframe? Lengthen the z‑score and correlation windows; keep calibration on.

- Volatility regime change? Revisit the ATR multiplier and enable square‑root scaling of horizon.

Execution and risk.

- Size positions by volatility (ATR‑based sizing works well).

- Enter on confirmed values; use intrabar previews only as early signals.

- Combine with your market structure (levels, liquidity zones). This model is statistical, not clairvoyant.

What it is not.

Not a black‑box machine‑learning model. It is transparent, correlation‑weighted technical analysis with strong attention to probability reliability and repaint safety.

Suggested defaults (robust starting point).

- Horizon 14; components mode; weight EMA 10; correlation window 500; z‑length 200.

- Neutral band around seven percentage points, or z‑threshold around one‑third of a standard deviation.

- Prior shift ON, Calibration ON, Use calibrated for decisions OFF to start.

- ATR multiplier 1.0; square‑root horizon scaling ON; EMA smoothing 3.

- Confidence setting equivalent to about 95%.

Disclaimer

No indicator guarantees profits. HorizonSigma Pro is a decision aid; always combine with solid risk management and your own judgment. Backtest, forward test, and size responsibly.

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Enhance your trading precision and confidence 🚀

Best regards

Chervolino

Tensor Market Analysis Engine (TMAE)# Tensor Market Analysis Engine (TMAE)

## Advanced Multi-Dimensional Mathematical Analysis System

*Where Quantum Mathematics Meets Market Structure*

---

## 🎓 THEORETICAL FOUNDATION

The Tensor Market Analysis Engine represents a revolutionary synthesis of three cutting-edge mathematical frameworks that have never before been combined for comprehensive market analysis. This indicator transcends traditional technical analysis by implementing advanced mathematical concepts from quantum mechanics, information theory, and fractal geometry.

### 🌊 Multi-Dimensional Volatility with Jump Detection

**Hawkes Process Implementation:**

The TMAE employs a sophisticated Hawkes process approximation for detecting self-exciting market jumps. Unlike traditional volatility measures that treat price movements as independent events, the Hawkes process recognizes that market shocks cluster and exhibit memory effects.

**Mathematical Foundation:**

```

Intensity λ(t) = μ + Σ α(t - Tᵢ)

```

Where market jumps at times Tᵢ increase the probability of future jumps through the decay function α, controlled by the Hawkes Decay parameter (0.5-0.99).

**Mahalanobis Distance Calculation:**

The engine calculates volatility jumps using multi-dimensional Mahalanobis distance across up to 5 volatility dimensions:

- **Dimension 1:** Price volatility (standard deviation of returns)

- **Dimension 2:** Volume volatility (normalized volume fluctuations)

- **Dimension 3:** Range volatility (high-low spread variations)

- **Dimension 4:** Correlation volatility (price-volume relationship changes)

- **Dimension 5:** Microstructure volatility (intrabar positioning analysis)

This creates a volatility state vector that captures market behavior impossible to detect with traditional single-dimensional approaches.

### 📐 Hurst Exponent Regime Detection

**Fractal Market Hypothesis Integration:**

The TMAE implements advanced Rescaled Range (R/S) analysis to calculate the Hurst exponent in real-time, providing dynamic regime classification:

- **H > 0.6:** Trending (persistent) markets - momentum strategies optimal

- **H < 0.4:** Mean-reverting (anti-persistent) markets - contrarian strategies optimal

- **H ≈ 0.5:** Random walk markets - breakout strategies preferred

**Adaptive R/S Analysis:**

Unlike static implementations, the TMAE uses adaptive windowing that adjusts to market conditions:

```

H = log(R/S) / log(n)

```

Where R is the range of cumulative deviations and S is the standard deviation over period n.

**Dynamic Regime Classification:**

The system employs hysteresis to prevent regime flipping, requiring sustained Hurst values before regime changes are confirmed. This prevents false signals during transitional periods.

### 🔄 Transfer Entropy Analysis

**Information Flow Quantification:**

Transfer entropy measures the directional flow of information between price and volume, revealing lead-lag relationships that indicate future price movements:

```

TE(X→Y) = Σ p(yₜ₊₁, yₜ, xₜ) log

```

**Causality Detection:**

- **Volume → Price:** Indicates accumulation/distribution phases

- **Price → Volume:** Suggests retail participation or momentum chasing

- **Balanced Flow:** Market equilibrium or transition periods

The system analyzes multiple lag periods (2-20 bars) to capture both immediate and structural information flows.

---

## 🔧 COMPREHENSIVE INPUT SYSTEM

### Core Parameters Group

**Primary Analysis Window (10-100, Default: 50)**

The fundamental lookback period affecting all calculations. Optimization by timeframe:

- **1-5 minute charts:** 20-30 (rapid adaptation to micro-movements)

- **15 minute-1 hour:** 30-50 (balanced responsiveness and stability)

- **4 hour-daily:** 50-100 (smooth signals, reduced noise)

- **Asset-specific:** Cryptocurrency 20-35, Stocks 35-50, Forex 40-60

**Signal Sensitivity (0.1-2.0, Default: 0.7)**

Master control affecting all threshold calculations:

- **Conservative (0.3-0.6):** High-quality signals only, fewer false positives

- **Balanced (0.7-1.0):** Optimal risk-reward ratio for most trading styles

- **Aggressive (1.1-2.0):** Maximum signal frequency, requires careful filtering

**Signal Generation Mode:**

- **Aggressive:** Any component signals (highest frequency)

- **Confluence:** 2+ components agree (balanced approach)

- **Conservative:** All 3 components align (highest quality)

### Volatility Jump Detection Group

**Volatility Dimensions (2-5, Default: 3)**

Determines the mathematical space complexity:

- **2D:** Price + Volume volatility (suitable for clean markets)

- **3D:** + Range volatility (optimal for most conditions)

- **4D:** + Correlation volatility (advanced multi-asset analysis)

- **5D:** + Microstructure volatility (maximum sensitivity)

**Jump Detection Threshold (1.5-4.0σ, Default: 3.0σ)**

Standard deviations required for volatility jump classification:

- **Cryptocurrency:** 2.0-2.5σ (naturally volatile)

- **Stock Indices:** 2.5-3.0σ (moderate volatility)

- **Forex Major Pairs:** 3.0-3.5σ (typically stable)

- **Commodities:** 2.0-3.0σ (varies by commodity)

**Jump Clustering Decay (0.5-0.99, Default: 0.85)**

Hawkes process memory parameter:

- **0.5-0.7:** Fast decay (jumps treated as independent)

- **0.8-0.9:** Moderate clustering (realistic market behavior)

- **0.95-0.99:** Strong clustering (crisis/event-driven markets)

### Hurst Exponent Analysis Group

**Calculation Method Options:**

- **Classic R/S:** Original Rescaled Range (fast, simple)

- **Adaptive R/S:** Dynamic windowing (recommended for trading)

- **DFA:** Detrended Fluctuation Analysis (best for noisy data)

**Trending Threshold (0.55-0.8, Default: 0.60)**

Hurst value defining persistent market behavior:

- **0.55-0.60:** Weak trend persistence

- **0.65-0.70:** Clear trending behavior

- **0.75-0.80:** Strong momentum regimes

**Mean Reversion Threshold (0.2-0.45, Default: 0.40)**

Hurst value defining anti-persistent behavior:

- **0.35-0.45:** Weak mean reversion

- **0.25-0.35:** Clear ranging behavior

- **0.15-0.25:** Strong reversion tendency

### Transfer Entropy Parameters Group

**Information Flow Analysis:**

- **Price-Volume:** Classic flow analysis for accumulation/distribution

- **Price-Volatility:** Risk flow analysis for sentiment shifts

- **Multi-Timeframe:** Cross-timeframe causality detection

**Maximum Lag (2-20, Default: 5)**

Causality detection window:

- **2-5 bars:** Immediate causality (scalping)

- **5-10 bars:** Short-term flow (day trading)

- **10-20 bars:** Structural flow (swing trading)

**Significance Threshold (0.05-0.3, Default: 0.15)**

Minimum entropy for signal generation:

- **0.05-0.10:** Detect subtle information flows

- **0.10-0.20:** Clear causality only

- **0.20-0.30:** Very strong flows only

---

## 🎨 ADVANCED VISUAL SYSTEM

### Tensor Volatility Field Visualization

**Five-Layer Resonance Bands:**

The tensor field creates dynamic support/resistance zones that expand and contract based on mathematical field strength:

- **Core Layer (Purple):** Primary tensor field with highest intensity

- **Layer 2 (Neutral):** Secondary mathematical resonance

- **Layer 3 (Info Blue):** Tertiary harmonic frequencies

- **Layer 4 (Warning Gold):** Outer field boundaries

- **Layer 5 (Success Green):** Maximum field extension

**Field Strength Calculation:**

```

Field Strength = min(3.0, Mahalanobis Distance × Tensor Intensity)

```

The field amplitude adjusts to ATR and mathematical distance, creating dynamic zones that respond to market volatility.

**Radiation Line Network:**

During active tensor states, the system projects directional radiation lines showing field energy distribution:

- **8 Directional Rays:** Complete angular coverage

- **Tapering Segments:** Progressive transparency for natural visual flow

- **Pulse Effects:** Enhanced visualization during volatility jumps

### Dimensional Portal System

**Portal Mathematics:**

Dimensional portals visualize regime transitions using category theory principles:

- **Green Portals (◉):** Trending regime detection (appear below price for support)

- **Red Portals (◎):** Mean-reverting regime (appear above price for resistance)

- **Yellow Portals (○):** Random walk regime (neutral positioning)

**Tensor Trail Effects:**

Each portal generates 8 trailing particles showing mathematical momentum:

- **Large Particles (●):** Strong mathematical signal

- **Medium Particles (◦):** Moderate signal strength

- **Small Particles (·):** Weak signal continuation

- **Micro Particles (˙):** Signal dissipation

### Information Flow Streams

**Particle Stream Visualization:**

Transfer entropy creates flowing particle streams indicating information direction:

- **Upward Streams:** Volume leading price (accumulation phases)

- **Downward Streams:** Price leading volume (distribution phases)

- **Stream Density:** Proportional to information flow strength

**15-Particle Evolution:**

Each stream contains 15 particles with progressive sizing and transparency, creating natural flow visualization that makes information transfer immediately apparent.

### Fractal Matrix Grid System

**Multi-Timeframe Fractal Levels:**

The system calculates and displays fractal highs/lows across five Fibonacci periods:

- **8-Period:** Short-term fractal structure