Kalman VWAP Filter [BackQuant]Kalman VWAP Filter

A precision-engineered price estimator that fuses Kalman filtering with the Volume-Weighted Average Price (VWAP) to create a smooth, adaptive representation of fair value. This hybrid model intelligently balances responsiveness and stability, tracking trend shifts with minimal noise while maintaining a statistically grounded link to volume distribution.

If you would like to see my original Kalman Filter, please find it here:

Concept overview

The Kalman VWAP Filter is built on two core ideas from quantitative finance and control theory:

Kalman filtering — a recursive Bayesian estimator used to infer the true underlying state of a noisy system (in this case, fair price).

VWAP anchoring — a dynamic reference that weights price by traded volume, representing where the majority of transactions have occurred.

By merging these concepts, the filter produces a line that behaves like a "smart moving average": smooth when noise is high, fast when markets trend, and self-adjusting based on both market structure and user-defined noise parameters.

How it works

Measurement blend : Combines the chosen Price Source (e.g., close or hlc3) with either a Session VWAP or a Rolling VWAP baseline. The VWAP Weight input controls how much the filter trusts traded volume versus price movement.

Kalman recursion : Each bar updates an internal "state estimate" using the Kalman gain, which determines how much to trust new observations vs. the prior state.

Noise parameters :

Process Noise controls agility — higher values make the filter more responsive but also more volatile.

Measurement Noise controls smoothness — higher values make it steadier but slower to adapt.

Filter order (N) : Defines how many parallel state estimates are used. Larger orders yield smoother output by layering multiple one-dimensional Kalman passes.

Final output : A refined price trajectory that captures VWAP-adjusted fair value while dynamically adjusting to real-time volatility and order flow.

Why this matters

Most smoothing techniques (EMA, SMA, Hull) trade off lag for smoothness. Kalman filtering, however, adaptively rebalances that tradeoff each bar using probabilistic weighting, allowing it to follow market state changes more efficiently. Anchoring it to VWAP integrates microstructure context — capturing where liquidity truly lies rather than only where price moves.

Use cases

Trend tracking : Color-coded candle painting highlights shifts in slope direction, revealing early trend transitions.

Fair value mapping : The line represents a continuously updated equilibrium price between raw price action and VWAP flow.

Adaptive moving average replacement : Outperforms static MAs in variable volatility regimes by self-adjusting smoothness.

Execution & reversion logic : When price diverges from the Kalman VWAP, it may indicate short-term imbalance or overextension relative to volume-adjusted fair value.

Cross-signal framework : Use with standard VWAP or other filters to identify convergence or divergence between liquidity-weighted and state-estimated prices.

Parameter guidance

Process Noise : 0.01–0.05 for swing traders, 0.1–0.2 for intraday scalping.

Measurement Noise : 2–5 for normal use, 8+ for very smooth tracking.

VWAP Weight : 0.2–0.4 balances both price and VWAP influence; 1.0 locks output directly to VWAP dynamics.

Filter Order (N) : 3–5 for reactive short-term filters; 8–10 for smoother institutional-style baselines.

Interpretation

When price > Kalman VWAP and slope is positive → bullish pressure; buyers dominate above fair value.

When price < Kalman VWAP and slope is negative → bearish pressure; sellers dominate below fair value.

Convergence of price and Kalman VWAP often signals equilibrium; strong divergence suggests imbalance.

Crosses between Kalman VWAP and the base VWAP can hint at shifts in short-term vs. long-term liquidity control.

Summary

The Kalman VWAP Filter blends statistical estimation with market microstructure awareness, offering a refined alternative to static smoothing indicators. It adapts in real time to volatility and order flow, helping traders visualize balance, transition, and momentum through a lens of probabilistic fair value rather than simple price averaging.

스크립트에서 "liquidity"에 대해 찾기

ICT Macro Time WindowsICT Macro Time Windows - Master institutional market timing with automated 'Macro' trading session tracking.

What are 'Macros'?

In ICT terminology, 'Macros' refer to the key institutional trading windows throughout the day where major banks and liquidity providers are most active. These specific time frames see heightened volatility, liquidity, and strategic positioning.

Perfect Timing Automation:

• 8 Critical Macro Sessions:

London 1: 02:33-03:00 EST

London 2: 04:03-04:30 EST

NY AM1: 08:50-09:10 EST

NY AM2: 09:50-10:10 EST

NY AM3: 10:50-11:10 EST

Lunch: 11:50-12:10 EST

PM: 13:10-13:40 EST

Close: 15:15-15:45 EST

• Fully customizable time zones and session times

• Real-time session detection with visual zones & labels

• Automatic High/Low range tracking within each window

• Boxes, lines, and labels for clear visual reference

• Never miss optimal entry/exit timing again

Trade when institutions trade - stop guessing and start timing your setups with precision during these key liquidity windows! All session times are easily adjustable in settings to match your preferred trading hours.

Perfect for Forex, Futures, and Index traders following ICT concepts and institutional flow analysis.

Smart Money Dynamics Blocks - Pearson MatrixSmart Money Dynamics Blocks — Pearson Matrix

A structural fusion of Prime Number Theory, Pearson Correlation, and Cumulative Delta Geometry.

1. Mathematical Foundation

This indicator is built on the intersection of Prime Number Theory and the Pearson correlation coefficient, creating a structural framework that quantifies how price and time evolve together.

Prime numbers — unique, indivisible, and irregular — are used here as nonlinear time intervals. Each prime length (2, 3, 5, 7, 11…97) represents a regression horizon where correlation is measured between price and time. The result is a multi-scale correlation lattice — a geometric matrix that captures hidden directional strength and temporal bias beyond traditional moving averages.

2. The Pearson Matrix Logic

For every prime interval p, the indicator calculates the linear correlation:

r_p = corr(price, bar_index, p)

Each r_p reflects how closely price and time move together across a prime-defined window. All r_p values are then averaged to create avgR, a single adaptive coefficient summarizing overall structural coherence.

- When avgR > 0.8 → strong positive correlation (labeled R+).

- When avgR < -0.8 → strong negative correlation (labeled R−).

This approach gives a mathematically grounded definition of trend — one that isn’t based on pattern recognition, but on measurable correlation strength.

3. Sequential Prime Slope and Median Pivot

Using the ordered sequence of 25 prime intervals, the model computes sequential slopes between adjacent primes. These slopes represent the rate of change of structure between two prime scales. A robust median aggregator smooths the slopes, producing a clean, stable directional vector.

The system anchors this slope to the 41-bar pivot — the median of the first 25 primes — serving as the geometric midpoint of the prime lattice. The resulting yellow line on the chart is not an ordinary regression line; it’s a dynamic prime-slope function, adapting continuously with correlation feedback.

4. Regression-Style Parallel Bands

Around this prime-slope line, the indicator constructs parallel bands using standard deviation envelopes — conceptually similar to a regression channel but recalculated through the prime–Pearson matrix.

These bands adjust dynamically to:

- Volatility, via standard deviation of residuals.

- Correlation strength, via avgR sign weighting.

Together, they visualize statistical deviation geometry, making it easier to observe symmetry, expansion, and contraction phases of price structure.

5. Volume and Cumulative Delta Peaks

Below the geometric layer, the indicator incorporates a custom lower-timeframe volume feed — by default using 15-second data (custom_tf_input_volume = “15S”). This allows precise delta computation between up-volume and down-volume even on higher timeframe charts.

From this feed, the indicator accumulates delta over a configurable period (default: 100 bars). When cumulative delta reaches a local maximum or minimum, peak and trough markers appear, showing the precise bar where buying or selling pressure statistically peaked.

This combination of geometry and order flow reveals the intersection of market structure and energy — where liquidity pressure expresses itself through mathematical form.

6. Chart Interpretation

The primary chart view represents the live execution of the indicator. It displays the relationship between structural correlation and volume behavior in real time.

Orange “R+” and blue “R−” labels indicate regions of strong positive or negative Pearson correlation across the prime matrix. The yellow median prime-slope line serves as the structural backbone of the indicator, while green and red parallel bands act as dynamic regression boundaries derived from the underlying correlation strength. Peaks and troughs in cumulative delta — displayed as numerical annotations — mark statistically significant shifts in buying and selling pressure.

The secondary visualization (Prime Regression Concept) expands on this by illustrating how regression behavior evolves across prime intervals. Each colored regression fan corresponds to a prime number window (2, 3, 5, 7, …, 97), demonstrating how multiple regression lines would appear if drawn independently. The indicator integrates these into one unified geometric model — eliminating the need to plot tens of regression lines manually. It’s a conceptual tool to help visualize the internal logic: the synthesis of many small-scale regressions into a single coherent structure.

7. Interpretive Insight

This model is not a prediction tool; it’s an instrument of mathematical observation. By translating price dynamics into a prime-structured correlation space, it reveals how coherence unfolds through time — not as a forecast, but as a measurable evolution of structure.

It unifies three analytical domains:

- Prime distribution — defines a nonlinear temporal architecture.

- Pearson correlation — quantifies statistical cohesion.

- Cumulative delta — expresses behavioral imbalance in order flow.

The synthesis creates a geometric analysis of liquidity and time — where structure meets energy, and where the invisible rhythm of market flow becomes measurable.

8. Contribution & Feedback

Share your observations in the comments:

- The time gap and alternation between R+ and R− clusters.

- How different timeframes change delta sensitivity or reveal compression/expansion.

- Prime intervals/clusters that tend to sit near turning points or liquidity shifts.

- How avgR behaves across assets or regimes (trending, ranging, high-vol).

- Notable interactions with the parallel bands (touches, breaks, mean-revert).

Your field notes help others read the model more effectively and compare contexts.

Summary

- Primes define the structure.

- Pearson quantifies coherence.

- Slope median stabilizes geometry.

- Regression bands visualize deviation.

- Cumulative delta locates imbalance.

Together, they construct a framework where mathematics meets market behavior.

Multi-Timeframe SFP (Swing Failure Pattern)How to Use

1. Set Pivot Timeframe: Choose the timeframe for identifying major swing points (e.g., 'D' for Daily pivots).

2. Set SFP Timeframe: Choose the timeframe to find the SFP candle (e.g., '240' for the 4-Hour chart).

3. Set Confirmation Bars: Set how many SFP Timeframe bars must pass without invalidating the level. A value of '0' confirms immediately on the SFP bar's close. A value of '1' waits for one more bar to close.

4. Adjust Filters (Optional): Enable the 'Wick % Filter' to add a quality check for strong rejections.

5. Watch & Wait: The indicator will draw lines and labels and fire alerts for fully confirmed signals.

In-Depth Explanation

1. Overview

The Dynamic Pivot SFP Engine is a multi-timeframe tool designed to identify and validate Swing Failure Patterns (SFPs) at significant price levels.

An SFP is a common price action pattern where price briefly trades beyond a previous swing high or low (sweeping liquidity) but then fails to hold those new prices, closing back inside the previous range. This "failure" often signals a reversal.

This indicator enhances SFP detection by separating the Pivot (Liquidity) from the SFP (Rejection), allowing you to monitor them on different timeframes.

2. The Core Multi-Timeframe Logic

The indicator's power comes from two key inputs:

• Pivot Timeframe (Pivot Timeframe)

This is the "high timeframe" used to establish significant support and resistance levels. The script finds standard pivots (swing highs and lows) on this timeframe based on the Pivot Left Strength and Pivot Right Strength inputs. These pivots are the "liquidity" levels the SFP will target. The Pivot Lookback input controls how long (in Pivot Timeframe bars) a pivot remains active and monitored.

• SFP Timeframe (SFP Timeframe)

This is the "execution timeframe" where the script looks for the actual SFP. On every new bar of this timeframe, the script checks if price has swept and rejected any of the active pivots.

Example Setup:

You might set Pivot Timeframe to 'D' (Daily) to find major daily swing points. You then set SFP Timeframe to '240' (4-Hour) to find a 4-hour candle that sweeps a daily pivot and closes back below/above it.

3. The SFP Confirmation Process

An SFP is not confirmed instantly. It must pass a rigorous, multi-step validation process.

Step 1: The SFP Candle (The Sweep)

A potential SFP is identified when an SFP Timeframe bar does the following:

• Bearish SFP: The bar's high trades above an active pivot high, but the bar closes below that same pivot high.

• Bullish SFP: The bar's low trades below an active pivot low, but the bar closes above that same pivot low.

Step 2: The Wick Filter (Optional Quality Check)

If Enable Wick % Filter is checked, the SFP candle from Step 1 is also measured.

• For a bearish SFP, the upper wick (from the high to the open/close) must be at least Min. Wick % of the entire candle's range (high-to-low).

• For a bullish SFP, the lower wick (from the low to the open/close) must meet the same percentage requirement.

If the SFP candle fails this test, it is discarded, even if it met the sweep/close criteria.

Step 3: The Validation Window (The Confirmation)

This is the most critical feature, controlled by Confirmation Bars.

• If Confirmation Bars = 0: The SFP is confirmed immediately on the SFP candle's close (assuming it passed the optional wick check). The label, line, and alert are triggered at this moment.

• If Confirmation Bars > 0: The SFP enters a "pending" state. The script will wait for $N$ more SFP Timeframe bars to close.

o Invalidation: If, during this waiting period, any bar closes back across the pivot (e.g., a close above the pivot for a bearish SFP), the SFP is considered failed and invalidated. All pending plots are deleted.

o Confirmation: If the $N$ confirmation bars all complete without invalidating the level, the SFP is finally confirmed. The label, line, and alert are only triggered after this entire process is complete. This adds a significant layer of robustness, ensuring the rejection holds for a period of time.

4. Visuals & Alerts

• Lines: A horizontal line is drawn from the original pivot to the SFP bar, showing which level was targeted. Note: These lines will only be drawn on chart timeframes equal to or lower than the 'SFP Timeframe'.

• Labels: A label is placed at the SFP's extreme (the high/low of the SFP bar). The label text conveniently includes the Ticker, Pivot TF, SFP TF, and Confirmation bar settings (e.g., "Bearish SFP BTCUSD / Pivot: 1D / SFP: 4H | Conf: 1").

• MTF Boxes (Show SFP Box, Show Conf. Boxes): These boxes highlight the SFP and confirmation bars. Crucially, they are only visible when your chart timeframe is lower than the SFP Timeframe. For example, if your SFP Timeframe is '240' (4H), you will only see these boxes on the 1H, 15M, 5M, etc., charts. This allows you to see the higher-timeframe SFP unfolding on your lower-timeframe chart.

• Alerts (Enable Alerts): An alert is fired only when an SFP is fully confirmed (i.e., after the Confirmation Bars have passed successfully). For efficient, real-time monitoring, it is highly recommended to run this indicator server-side by creating an alert on TradingView set to trigger on "Any alert() function call".

USCBBS-WDTGAL-RRPONTSYDThis is the U.S. Financial Market Net Liquidity.

The calculation method is to subtract the U.S. Treasury General Account balance (WDTGAL) and then the Overnight Reverse Repo balance (RRPONTSYD) from the Federal Reserve's balance sheet total (USCBBS).

ATR Anchored Range %b by TradeSeekersAll time highs got you spooked to enter with no levels in sight?

Stuck in a multi-week range and wondering where the heck the pivots are!?

Wondering if you're longing the top or shorting the potential bottom and about to get smoked, sending you back to burger flipping?!

Fret not trading friends!

I've been crafting the ultimate map for scalpers, slingers, swingers, swindlers, swashbucklers -and traders too.

Why should I care about this, what's an ATR!?

Nearly any trader that's entered the markets has heard of ATR, perhaps even taken a stab at trying to calculate the flux capacity of a weekly ATR on a lower timeframe. Continually calculating things manually sucks!

Ok, so you haven't heard of ATR? It's the average true range... what's the true range!? It's simply the low subtracted from the high (high - low) of any given candle.

How is ATR useful?

The theory is simple, if the ATRs on the daily timeframe for a stock are 5, then traders may have a reasonable expectation that any day in the near future the stock will mostly move +/- 5 pts. This +/- 5 can be used as a possible daily high and low for traders to use.

But ATR changes as time passes, with every billionaire X post, viral cat meme, fed announcement or government shutdown the market makes it's move. This means without this tool, traders need to run the standard lame (sorry) ATR indicator and then hand draw a bunch of important levels (barf).

I'm convinced and ready to join the ATR army, what do I do?

Glad to have you aboard sailor, slap this indicator on your layout - it'll initially display a bottom panel, say nice things to it.

Usage

The lower panel provides a %b plot representative of the current price relative to the timeframe and period ATR. (Defaults to 1D timeframe and 20 - 20 trading days in a month yo)

This %b plot is a map for price against the key ATR based levels and resets each time the timeframe change occurs.

Keep reading! (maybe grab a snack, you're doing great)

If you want to see what the indicator sees, how it maths the math, open the settings and check the "overlay" option... it's amazing, I know.

Main base of operations

This will be the gray area between first red and green lines, imagine this is a future candle for the timeframe anchored. The red would represent the candle high (red means stop/overbought), and the green would represent the candle low (green means go/oversold).

Regardless of the timeframe anchored, this area always represents the area the ATR indicates will be the building area of the current candle being formed. Traders should expect most of the trading to occur within this area.

The mid line

Don't diddle in the middle, this by default is the open price and it's the ultimate bias filter for bull or bear riders.

Extension areas

Beyond the gray area is the extension zone, this provides a whole ATR from the mid line to the extension.

Assembling a trade plan

There are just a couple of key concepts to master in order to become the ultimate ATR samurai warrior, capable of slicing through even the messiest liquidity.

Above the midline and holding, but still within the gray area? Could be a great long entry with targets to upper levels. The same holds true for below open and holding while still being within the lower gray area.

As price makes it's ascension or decline towards the ends of the initial gray ATR range, consider managing trades here. If it's suspected, due to a strong hold of the midline, that the range low or high is the midline, then continue to manage trades towards the extension zones.

Timeframes and periods oh my

The tooltips already provide some hints, but not everyone goes around clicking and hovering everything in sight (maybe I'm the only one that does that?).

There's a thoughtful approach to the default values, I like to consider the big market participants with my day trades, swings trades and beyond.

By default I've chosen the daily timeframe and a period of 20, one for each trading day of the calendar month.

It's no large leap to consider alternatives, what about 1W timeframe and a period of 4 (1 month) or 52 (1 year)?

The possibilities are nearly infinite, comment on any particular favorite combos.

An Italian Special Bonus!!!

...sorry, it's not pizza....

First, did you know the famous Italian Fibonacci's real name was actually Leonardo? I'm not sure how I feel about that. Fun fact, my ancestors are Italian.

Alright, you may have guessed that the special bonus is the mythical Fibonacci inspired "Golden Pocket", maybe it's a foreshadowing of your pockets - one can only hope.

Use this feature to show the commonly referenced Fibonacci levels within each major ATR range. I've seen some totally mathematical epic-ness with these hence the addition.

Once key ATR levels have been hit look for reversals back to golden pockets (you tricksy hobbits) for potential entry back towards the prior hit ATR level.

The %b turns gold if you have the feature enabled and of course the overlay displays them also, how fun!

Final thoughts

I hope you have as much fun using this indicator as I do, it has brought much joy to my trading experience. If you don't have fun with it, well I hope you had fun reading about it at least.

100% human crafted and darn proud of it

- SyntaxGeek

Volume Rate of Change (VROC)# Volume Rate of Change (VROC)

**What it is:** VROC measures the rate of change in trading volume over a specified period, typically expressed as a percentage. Formula: `((Current Volume - Volume n periods ago) / Volume n periods ago) × 100`

## **Obvious Uses**

**1. Confirming Price Trends**

- Rising VROC with rising prices = strong bullish trend

- Rising VROC with falling prices = strong bearish trend

- Validates that price movements have conviction behind them

**2. Spotting Divergences**

- Price makes new highs but VROC doesn't = weakening momentum

- Price makes new lows but VROC doesn't = potential reversal

**3. Identifying Breakouts**

- Sudden VROC spikes often accompany legitimate breakouts from consolidation patterns

- Helps distinguish real breakouts from false ones

**4. Overbought/Oversold Conditions**

- Extreme VROC readings (very high or very low) suggest exhaustion

- Mean reversion opportunities when volume extremes occur

---

## **Non-Obvious Uses**

**1. Smart Money vs. Dumb Money Detection**

- Declining VROC during price rallies may indicate retail FOMO while institutions distribute

- Rising VROC during selloffs with price stability suggests institutional accumulation

**2. News Impact Measurement**

- Compare VROC before/after earnings or announcements

- Low VROC on "significant" news = market doesn't care (fade the move)

- High VROC = genuine market reaction (respect the move)

**3. Market Regime Changes**

- Persistent shifts in average VROC levels can signal transitions between bull/bear markets

- Declining baseline VROC over months = waning market participation/topping process

**4. Intraday Liquidity Profiling**

- VROC patterns across trading sessions identify best execution times

- Avoid trading when VROC is abnormally low (wider spreads, poor fills)

**5. Sector Rotation Analysis**

- Compare VROC across sector ETFs to identify where capital is flowing

- Rising VROC in defensive sectors + falling VROC in cyclicals = risk-off rotation

**6. Options Expiration Effects**

- VROC typically drops significantly post-options expiration

- Helps avoid false signals from mechanically-driven volume changes

**7. Algorithmic Activity Detection**

- Unusual VROC patterns (regular spikes at specific times) may indicate algo programs

- Can front-run or avoid periods of heavy algorithmic interference

**8. Liquidity Crisis Early Warning**

- Sharp, sustained VROC decline across multiple assets = liquidity withdrawal

- Can precede market stress events before price volatility emerges

**9. Cryptocurrency Wash Trading Detection**

- Comparing VROC across exchanges for same asset

- Discrepancies suggest artificial volume on certain platforms

**10. Pair Trading Optimization**

- Use relative VROC between correlated pairs

- Enter when VROC divergence is extreme, exit when it normalizes

The key to advanced VROC usage is context: combining it with price action, market structure, and other indicators rather than using it in isolation.

Fair Value Gaps by DGTFair Value Gaps

A refined, multi-timeframe Fair Value Gap (FVG) detection tool that brings institutional imbalance zones to life directly on your chart.

Designed for precision, it visualizes how price delivers into inefficiencies across chart, higher, and lower (intrabar) timeframes — offering a fluid, structural view of liquidity displacement and market flow.

The script continuously tracks unfilled, partially repaired, and fully resolved imbalances, revealing where liquidity inefficiencies concentrate and where price may seek rebalancing.

Overlapping zones naturally expose institutional footprints, potential liquidity targets, and key re-pricing regions within the broader market structure.

KEY FEATURES

⯌ Multi-Timeframe Detection

Detect and display FVGs from the current chart, higher timeframes (HTF), or lower timeframes (LTF)

⯌ Smart Fill Tracking

Automatic real-time monitoring of each FVG’s fill progress with live percentage updates

⯌ Custom Fill Logic

Choose your preferred definition of when a gap is considered filled: Any Touch

Midpoint Reached

Wick Sweep

Body Beyond

⯌ Dynamic Labels & Tooltips

Labels can be toggled on/off. Even when hidden, detailed tooltips remain available by hovering over the FVG midpoint.

⯌ Adaptive Lower-Timeframe Mode

When set to “Auto,” the script intelligently selects the optimal lower timeframe based on the chart resolution.

DISCLAIMER

This script is intended for informational and educational purposes only. It does not constitute financial, investment, or trading advice. All trading decisions made based on its output are solely the responsibility of the user.

Illuminati Zone🟣 Illuminati Zone — Hidden Power of the 11 PM NZ Candle

The Illuminati Zone reveals the hidden footprints of liquidity and market imbalance formed by the 11 PM New Zealand 15-minute candle — a time when global liquidity transitions between major sessions.

This candle often defines key intraday supply and demand boundaries, serving as a magnet for price and a pivot point for high-probability reversals or breakouts.

🧠 How it works

Automatically detects and marks the 11 PM NZ 15-minute candle each day.

Draws a translucent zone box between its high and low.

Extends two reference lines at +1 × range and –1 × range above and below the zone — ideal for spotting overextensions or liquidity sweeps.

Supports custom lookback, colors, and visual options.

💡 How to use it

Watch how price interacts with the zone — rejection often signals smart-money activity.

Use +1 and –1 levels as overextended zones for potential reversals or breakout retests.

Combine with your own confluence tools or volume analysis for precision entries.

⚙️ Customization Options

Target hour (NZ time)

Days back to display

Zone and line colors

Transparency and visual preferences

🔮 Pro Tip: Pair it with a volume or imbalance indicator for surgical-level precision in identifying where smart money positions are built or released.

Mean Reverting Suite [OmegaTools]Overview

The Mean Reverting Suits (MR Suite) by OmegaTools is an advanced analytical and visualization framework designed to identify directional exhaustion, statistical overextensions, and conditions consistent with mean-reversion dynamics. It integrates three pillars into a single display: a composite momentum-normalized oscillator, a percentile-based extension model with volume contextualization, and a dynamic structural mapping engine built on confirmed pivots. The indicator does not generate signals or prescribe trade actions; it provides objective context so users can evaluate market balance and the likelihood that price is departing from its recent statistical baseline.

Core logic

The composite oscillator blends MFI on two horizons and RSI on HL2, then averages them to produce a stabilized mean-reversion gauge. Candle and bar colors are mapped by a dual gradient centered at 50. Readings above 50 progressively shift from neutral gray toward the bearish accent color to reflect increasing momentum saturation; readings below 50 shift from the bullish accent color toward gray to reflect potential accumulation or temporary undervaluation. This continuous mapping avoids rigid thresholds and conveys the strength and decay of momentum as a smooth spectrum.

The percentile-based extension model measures the persistence of directional bias by tracking how many bars have elapsed since the last opposing condition. These rolling counts are compared to the 80th percentile of their own historical distributions stored in arrays. When a current streak exceeds its respective percentile, the environment is labeled as statistically extended in that direction. Background shading communicates this information and is modulated by relative volume, computed as live volume divided by a blended average of SMA(30) and EMA(11). Higher opacity implies greater liquidity participation during the extension.

The structural mapping module uses confirmed pivot highs and lows at the chosen length to create persistent horizontal levels that extend forward and automatically maintain themselves until price invalidates or refreshes them. These levels represent market memory zones and assist in reading where reactions previously formed. The engine updates in real time, ensuring the framework continuously reflects the prevailing structure.

Standard deviation and z-score overlay

The updated version introduces a mean and dispersion layer. A simple moving average of HL2 over twice the length provides the reference mean. Dispersion is estimated as the moving average of the absolute deviation between close and the mean over five times the length. The z-score is computed as the distance of price from the mean divided by this dispersion proxy. Visual arrows highlight observations where the absolute z-score exceeds two standard deviations, offering a concise view of statistically unusual departures from the local mean. This layer complements the percentile extension model by adding an orthogonal measure of extremity based on distributional distance rather than run length.

Visualization

Candle bodies and borders inherit the oscillator’s gradient color, creating an immediate sense of directional pressure and potential momentum fatigue. The chart background activates when the extension model detects a statistically rare streak, using blue tones for bearish extension and red tones for bullish extension, with intensity scaling by relative volume. Horizontal lines denote active pivot-based levels, automatically extending, truncating, and refreshing as structure evolves. The z-score arrows appear only when deviations exceed the ±2 threshold, keeping the display focused on noteworthy statistical events.

Inputs and configuration

Length controls the sensitivity of all modules. Lower values make the oscillator and pivot detection more reactive; higher values smooth readings and widen structural context. Bullish and Bearish colors are user-selectable to match platform themes or accessibility requirements.

Interpretation guidance

A strong red background indicates an unusually extended bullish run in the presence of meaningful volume; a strong blue background indicates an unusually extended bearish run in the presence of meaningful volume. Candle gradients near deep bearish tones suggest oscillator readings well above 50; gradients near deep bullish tones suggest oscillator readings well below 50. Pivot lines mark the most recently confirmed structural levels that the market has reacted to. Z-score arrows denote points where price has moved beyond approximately two standard deviations of its local mean, signaling statistically uncommon distance rather than directional persistence. None of these elements are directives; they are objective descriptors designed to improve situational awareness.

Advantages

The framework is adaptive by design and self-normalizes to each instrument’s volatility and rhythm through percentile logic and dispersion-based distance. It is volume-aware, visually encoding liquidity pressure so that users can distinguish thin extensions from structurally significant ones. It reduces chart clutter by unifying momentum state, statistical extension, standard deviation distance, and structural levels into a single coherent view. It is asset- and timeframe-agnostic, suitable for intraday through swing horizons across futures, equities, FX, and digital assets.

Usage notes

MR Suite is intended for analytical and educational purposes. It does not provide trading signals, risk parameters, or strategy instructions. Users may employ its context alongside their own methodologies, risk frameworks, and execution rules. The indicator’s value derives from quantifying how unusual a move is, showing how much liquidity supports it, and anchoring that information to evolving structural references, thereby improving the clarity and consistency of discretionary assessment without prescribing actions.

cd_VWAP_mtg_CxCd_VWAP_mtg_Cx

Overview

The most important condition for being successful and profitable in the market is to consistently follow the same rules without compromise, while the price constantly moves in countless different ways.

Regardless of the concept or trading school, those who have rules win.

In this indicator, we will define and use three main sections to set and apply our rules.

The indicator uses the VWAP (Volume Weighted Average Price) — price weighted by volume.

Two VWAPs can be displayed either by manually entering date and time, or by selecting from the menu.

From the menu, you can select the following reference levels:

• HTF Open: Opening candle of the higher timeframe

• ATH / ATL: All-Time High / All-Time Low candles

• PMH / PML, PWH / PWL, PDH / PDL, PH4H / PH4L: Previous Month, Week, Day, or H4 Highs/Lows

• MH / ML, WH / WL, DH / DL, H4H / H4L: Current Month, Week, Day, or H4 Highs/Lows

Additionally, it includes:

• Mitigation / Order Block zones (local buyer-seller balance) across two timeframes.

• Buy/Sell Side Liquidity levels (BSL / SSL) from the aligned higher timeframe (target levels).

________________________________________

Components and Usage

1 – VWAP

Calculated using the classical method:

• High + Volume for the upper value

• Close + Volume for the middle value

• Low + Volume for the lower value

The VWAP is displayed as a colored band, where the coloring represents the bias.

Let’s call this band FVB (Fair Value Band) for ease of explanation.

The FVB represents the final line of defense, the buyer/seller boundary, and in technical terms, it can be viewed as premium/discount zones or support/resistance levels.

Within this critical area, the strong side continues its move, while the weaker side is forced to retreat.

But does the side that breaks beyond the band always keep going?

We all know that’s not always the case — in different pairs and timeframes, price often violates both the upper and lower edges multiple times.

To achieve more consistent analysis, we’ll define a new set of rules.

________________________________________

2 – Mitigation / Order Blocks

In trading literature, there are dozens of different definitions and uses of mitigation or order blocks.

Here, we will interpret the candlesticks to create our own definition, and we’ll use the zones defined by candles that fit this pattern.

For simplicity, let’s abbreviate mitigation as “mtg.”

For a candle to be selected as an mtg, it must clearly show strength from one side (buyers or sellers) — which can also be observed visually on the chart.

________________________________________

Bullish mtg criteria:

1. The first candle must be bullish (close > open) → buyers are strong.

2. The next candle makes a new high (buyers push higher) but fails to close above and pulls back to close inside the previous range → sellers react.

It also must not break the previous low → buyers defend.

3. In the following candle(s), as long as the first candle’s low is protected and the second candle’s high is broken, it indicates buyer strength → a bullish mtg is confirmed.

When price returns to this zone later (gets mitigated), the expectation is that the zone holds and price pushes upward again.

If the low is violated, the mtg becomes invalid.

In technical terms:

If the previous candle’s high is broken but no close occurs above it, the expectation is a reversal move that will retest its low.

Question:

What if the low is protected and in the next candle(s) a new high forms?

Answer: → Bullish mtg.

Bearish mtg (opposite)

3 – Buy/Sell Side Liquidity Levels

With the help of the aligned higher timeframe (swing points), we will define our market structure framework and set our liquidity targets accordingly.

Let’s put the pieces together.

If we continue explaining from a trade-focused perspective, our first priority should be our bias — our projection or expectation of the market’s potential movement.

We will determine this bias using the FVB.

Since we know the band often gets violated on both sides, we want the price action to convince us of its strength.

To do that, we’ll use the first candle that closes beyond the band.

The distance from that candle’s high to low will be our threshold range

Bullish level = high + (candle length × coefficient)

Bearish level = low - (candle length × coefficient)

When the price closes beyond this threshold, it demonstrates strength, and our bias will now align in that direction.

How long will this bias remain valid?

→ Until a closing candle appears on the opposite side of the band.

If a close occurs on the opposite side, then a new bias will only be confirmed once the new threshold level is broken.

During the period in between, we have no bias.

Let’s continue on the chart:

Now that our bias has been established, where and how do we look for trade opportunities?

There are two possible entry approaches:

• Aggressive entry: Enter immediately with the breakout.

• Conservative entry: Wait for a pullback and enter once a suitable structure forms.

(The choice depends on the user’s preference.)

At this stage, the user can apply their own entry model. Let’s give an example:

Let’s assume we’re looking for setups using HTF sweep + LTF CISD confirmation.

Once our bias turns bearish, we look for an HTF sweep forming on or near an FVB or mtg block, and then confirm the entry with a CISD signal.

In summary:

• FVB defines the bias, the entry zone, and the target zone.

• Mtg blocks represent entry zones.

• BSL / SSL levels suggest target zones.

Overlapping FVB and mtg blocks are expected to be more effective.

The indicator also provides an option for a second FVB.

A band attached to a lower timeframe can be used as confirmation.

• Main band: Bias + FVB

• Extra band: Entry trigger confirmed by a close beyond it.

Mtg blocks can provide trade entry opportunities, especially when the price is moving strongly in one direction (flow).

Consecutive or complementary mtg blocks indicate that the price is decisive in one direction, while sometimes also showing areas where we should wait before entering.

Mtg blocks that contain an FVG (Fair Value Gap) within their body are expected to be more effective.

Settings:

The default values are set to 1-3-5m, optimized for scalping trades.

VWAP settings:

Main VWAP (FVB):

• Can be set by selecting a start time, manually entering date and time, or choosing a predefined level.

Extra VWAP (FVB):

• Set from the menu. If not needed, select “none.”

• Visibility, color, and fill settings for VWAP are located here.

• Threshold levels visibility and color options are also in this section.

• The multiplier is used for calculating the threshold level.

Important:

• If the Extra VWAP is selected but not displayed, you need to increase the chart timeframe.

o Example: If the chart is on 3m and you select WH from the extra options, it will not display correctly.

• Upper limits for VWAP:

o 1m and 3m charts: daily High/Low

o 5m chart: weekly High/Low

________________________________________

Mtg Settings:

• Visibility and color settings for blocks are configured here.

• To display on a second timeframe, the box must be checked and the timeframe specified.

• Optional display modes: “only active blocks,” “only last violated mtg,” or “all.”

• For confirmation and removal criteria, choosing high/low or close determines the source used for mtg block formation and deletion conditions.

BSL/SSL Settings:

• Visibility, color, font size, and line style can be configured in this section.

When “Auto” is selected, the aligned timeframe is determined automatically by the indicator, while in manual mode, the user defines the timeframe.

Final Words:

Simply opening trades every time the price touches the VWAP or mtg blocks will not make you a profitable trader. Searching for setups with similar structures while maintaining proper risk management will yield better results in the long run.

I would be happy to hear your feedback and suggestions.

Happy trading!

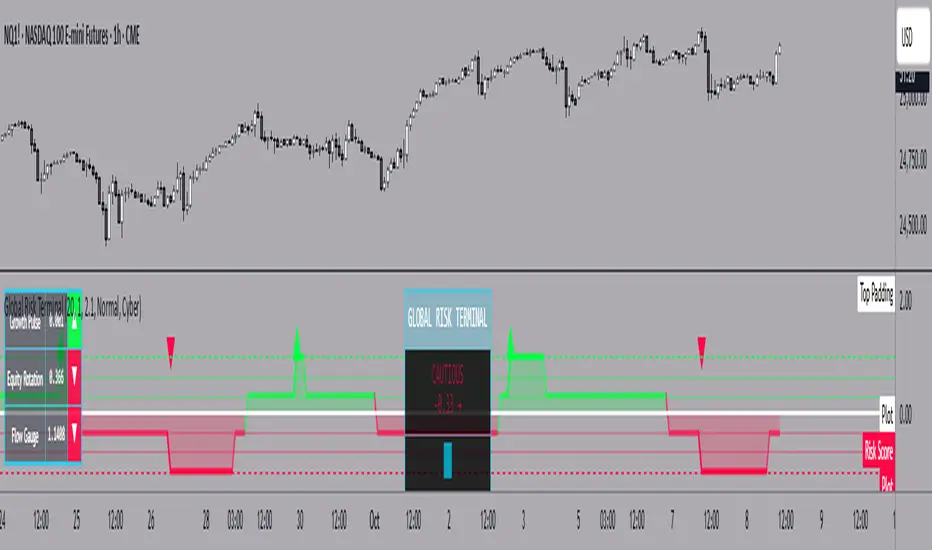

Global Risk Terminal – Multi-Asset Macro Sentiment IndicatorDescription:

The Global Risk Terminal is a sophisticated macro sentiment indicator that synthesizes signals from three key cross-asset relationships to produce a single, actionable risk appetite score. It is designed to help traders and investors identify whether global markets are in a risk-on (growth-seeking) or risk-off (defensive) regime. The indicator analyzes the behavior of commodities, equities, bonds, and currencies to generate a comprehensive view of market conditions.

Indicator Output:

The Global Risk Terminal produces a normalized risk score ranging from -1 to +1:

Positive values indicate risk-on conditions (growth assets favored)

Negative values indicate risk-off conditions (safe-haven assets favored)

Core Components:

Growth Pulse (Copper to Gold Ratio, HG/GC)

Purpose: Measures investor preference for industrial growth versus safe-haven assets.

Interpretation:

Rising ratio → Copper outperforming gold → Risk-on environment

Falling ratio → Gold outperforming copper → Risk-off environment

Flat ratio → Transitional market phase

Technical Implementation: Dual moving average slope method (fast MA default 20, slow MA default 40). Positive slope = +1, negative slope = -1, flat slope = 0

Equity Rotation (Russell 2000 to S&P 500 Ratio, RTY/ES)

Purpose: Tracks rotation between small-cap and large-cap equities, revealing market risk appetite.

Interpretation:

Rising ratio → Small-caps outperforming → Strong risk-on

Falling ratio → Large-caps outperforming → Defensive positioning

Technical Implementation: Dual moving average slope method (same as Growth Pulse)

Flow Gauge (10-Year Treasury to US Dollar Index, ZN/DXY)

Purpose: Captures liquidity conditions and cross-asset capital flows.

Interpretation:

Rising ratio → Treasury prices rising or USD weakening → Liquidity expansion, risk-on environment

Falling ratio → Treasury prices falling or USD strengthening → Liquidity contraction, risk-off environment

Technical Implementation: Dual moving average slope method

Composite Risk Score Calculation:

Analyze each component for trend using dual moving averages

Assign signal values: +1 (risk-on), -1 (risk-off), 0 (neutral)

Average the three signals:

Risk Score = (Growth Pulse + Equity Rotation + Flow Gauge) / 3

Optional smoothing with exponential moving average (default 3 periods) to reduce noise

Interpreting the Risk Score:

+0.66 to +1.0: Full risk-on – favor cyclical sectors, small-caps, growth strategies

+0.33 to +0.66: Moderate risk-on – mostly bullish environment, watch for fading momentum

-0.33 to +0.33: Neutral/transition – markets in flux, signals mixed, exercise caution

-0.66 to -0.33: Cautious risk-off – favor defensive sectors, reduce high-beta exposure

-1.0 to -0.66: Full risk-off – strong defensive positioning, prioritize safe-haven assets

How to Use the Global Risk Terminal to Frame Trades:

Aligning Trades with Market Regime

Risk-On (+0.33 and above): Look for buying opportunities in cyclical stocks, high-beta equities, commodities, and emerging markets. Use long entries for swing trades or intraday positions, following confirmed price action.

Risk-Off (-0.33 and below): Shift focus to defensive sectors, large-cap quality stocks, U.S. Treasuries, and safe-haven currencies. Prefer short entries or reduced exposure in risky assets.

Entry and Exit Framing

Use the risk score as a macro filter before executing trades:

Example: The risk score is +0.7 (strong risk-on). Prefer long positions in equities or commodities that are showing bullish confirmation on your regular chart.

Conversely, if the risk score is -0.7 (strong risk-off), avoid aggressive longs and consider short or defensive trades.

Watch for threshold crossings (+/-0.33, +/-0.66) as potential inflection points for adjusting position size, stop-loss levels, or sector rotation.

Confirming Trade Decisions

Combine the Global Risk Terminal with price action, volume, and trend indicators:

If equities rally but the risk score is declining, this may indicate a fragile rally driven by few leaders—trade cautiously.

If equities fall but the risk score is rising, consider counter-trend entries or buying dips.

Risk Management and Position Sizing

Strong alignment across components → increase position size and hold with wider stops

Mixed or neutral signals → reduce exposure, tighten stops, or avoid new trades

Defensive regimes → rotate into stable, low-volatility assets and increase cash buffer

Framing Trades Across Timeframes

Use the indicator as a strategic guide rather than a precise timing tool. Even without the MTF table:

Daily trend alignment → Guide swing trade bias

Shorter timeframe price action → Refine entry points and stop placement

Example: Daily chart shows +0.6 risk score → identify high-probability long setups using intraday technical patterns (breakouts, trend continuation).

Sector and Asset Rotation

Risk-On: Focus on cyclical sectors (financials, industrials, materials, energy), small-caps, high-beta instruments

Risk-Off: Focus on defensive sectors (utilities, consumer staples, healthcare), large-caps, safe-haven instruments

Alert Integration

Set alerts on the risk score to notify you when markets move from neutral to risk-on or risk-off regimes. Use these alerts to plan entries, exits, or portfolio adjustments in advance.

Customization Options:

Moving Average Length (5–100): Adjust sensitivity of trend detection

Score Smoothing (1–10): Reduce noise or see raw risk score

Visual Themes: Six preset themes (Cyber, Ocean, Sunset, Monochrome, Matrix, Custom)

Display Options: Show or hide component dashboards, main header, risk level lines, gradient fill, and component signals

Label Size: Tiny, Small, Normal, Large

Alert Conditions:

Risk score crosses above +0.66 → Strong risk-on

Risk score crosses below -0.66 → Strong risk-off

Risk score crosses zero → Neutral line

Risk score crosses above +0.33 → Moderate risk-on

Risk score crosses below -0.33 → Moderate risk-off

Data Sources:

HG1! – Copper Futures (COMEX)

GC1! – Gold Futures (COMEX)

RTY1! – Russell 2000 E-mini Futures (CME)

ES1! – S&P 500 E-mini Futures (CME)

ZN1! – 10-Year U.S. Treasury Note Futures (CBOT)

DXY – U.S. Dollar Index (ICE)

Notes and Limitations:

Works best during clear macro regimes and aligned trends

Use with price action, volume, and other technical tools

Not a standalone trading system; serves as a macro context filter

Equal weighting assumes all three components are equally important, but market conditions may vary

Past performance does not guarantee future results

Conclusion:

The Global Risk Terminal consolidates complex cross-asset signals into a simple, actionable score that informs market regime, portfolio positioning, sector rotation, and trading decisions. Its user-friendly layout and extensive customization options make it suitable for traders of all experience levels seeking macro-driven insights. By framing trades around risk score thresholds and combining macro context with tactical execution, traders can identify higher-probability opportunities and optimize position sizing, entries, and exits across a wide range of market conditions.

Opening Range IndicatorComplete Trading Guide: Opening Range Breakout Strategy

What Are Opening Ranges?

Opening ranges capture the high and low prices during the first few minutes of market open. These levels often act as key support and resistance throughout the trading day because:

Heavy volume occurs at market open as overnight orders execute

Institutional activity is concentrated during opening minutes

Price discovery happens as market participants react to overnight news

Psychological levels are established that traders watch all day

Understanding the Three Timeframes

OR5 (5-Minute Range: 9:30-9:35 AM)

Most sensitive - captures immediate market reaction

Quick signals but higher false breakout rate

Best for scalping and momentum trading

Use for early entry when conviction is high

OR15 (15-Minute Range: 9:30-9:45 AM)

Balanced approach - most popular among day traders

Moderate sensitivity with better reliability

Good for swing trades lasting several hours

Primary timeframe for most strategies

OR30 (30-Minute Range: 9:30-10:00 AM)

Most reliable but slower signals

Lower false breakout rate

Best for position trades and trend following

Use when looking for major moves

Core Trading Strategies

Strategy 1: Basic Breakout

Setup:

Wait for price to break above OR15 high or below OR15 low

Enter on the breakout candle close

Stop loss: Opposite side of the range

Target: 2-3x the range size

Example:

OR15 range: $100.00 - $102.00 (Range = $2.00)

Long entry: Break above $102.00

Stop loss: $99.50 (below OR15 low)

Target: $104.00+ (2x range size)

Strategy 2: Multiple Confirmation

Setup:

Wait for OR5 break first (early signal)

Confirm with OR15 break in same direction

Enter on OR15 confirmation

Stop: Below OR30 if available, or OR15 opposite level

Why it works:

Multiple timeframe confirmation reduces false signals and increases probability of sustained moves.

Strategy 3: Failed Breakout Reversal

Setup:

Price breaks OR15 level but fails to hold

Wait for re-entry into the range

Enter reversal trade toward opposite OR level

Stop: Recent breakout high/low

Target: Opposite side of range + extension

Key insight: Failed breakouts often lead to strong moves in the opposite direction.

Advanced Techniques

Range Quality Assessment

High-Quality Ranges (Trade these):

Range size: 0.5% - 2% of stock price

Clean boundaries (not choppy)

Volume spike during range formation

Clear rejection at range levels

Low-Quality Ranges (Avoid these):

Very narrow ranges (<0.3% of stock price)

Extremely wide ranges (>3% of stock price)

Choppy, overlapping candles

Low volume during formation

Volume Confirmation

For Breakouts:

Look for volume spike (2x+ average) on breakout

Declining volume often signals false breakout

Rising volume during range formation shows interest

Market Context Filters

Best Conditions:

Trending market days (SPY/QQQ with clear direction)

Earnings reactions or news-driven moves

High-volume stocks with good liquidity

Volatility above average (VIX considerations)

Avoid Trading When:

Extremely low volume days

Major economic announcements pending

Holidays or half-days

Choppy, sideways market conditions

Risk Management Rules

Position Sizing

Conservative: Risk 0.5% of account per trade

Moderate: Risk 1% of account per trade

Aggressive: Risk 2% maximum per trade

Stop Loss Placement

Inside the range: Quick exit but higher stop-out rate

Outside opposite level: More room but larger risk

ATR-based: 1.5-2x Average True Range below entry

Profit Taking

Target 1: 1x range size (take 50% off)

Target 2: 2x range size (take 25% off)

Runner: Trail remaining 25% with moving stops

Specific Entry Techniques

Breakout Entry Methods

Method 1: Immediate Entry

Enter as soon as price closes above/below range

Fastest entry but highest false signal rate

Best for strong momentum situations

Method 2: Pullback Entry

Wait for breakout, then pullback to range level

Enter when price bounces off former resistance/support

Better risk/reward but may miss some moves

Method 3: Volume Confirmation

Wait for breakout + volume spike

Enter after volume confirmation candle

Reduces false signals significantly

Multiple Timeframe Entries

Aggressive: OR5 break → immediate entry

Conservative: OR5 + OR15 + OR30 all align → enter

Balanced: OR15 break with OR30 support → enter

Common Mistakes to Avoid

1. Trading Poor-Quality Ranges

❌ Don't trade ranges that are too narrow or too wide

✅ Focus on clean, well-defined ranges with good volume

2. Ignoring Volume

❌ Don't chase breakouts without volume confirmation

✅ Always check for volume spike on breakouts

3. Over-Trading

❌ Don't force trades when ranges are unclear

✅ Wait for high-probability setups only

4. Poor Risk Management

❌ Don't risk more than planned or use tight stops in volatile conditions

✅ Stick to predetermined risk levels

5. Fighting the Trend

❌ Don't fade breakouts in strongly trending markets

✅ Align trades with overall market direction

Daily Trading Routine

Pre-Market (8:00-9:30 AM)

Check overnight news and earnings

Review major indices (SPY, QQQ, IWM)

Identify potential opening range candidates

Set alerts for range breakouts

Market Open (9:30-10:00 AM)

Watch opening range formation

Note volume and price action quality

Mark key levels on charts

Prepare for breakout signals

Trading Session (10:00 AM - 4:00 PM)

Execute breakout strategies

Manage existing positions

Trail stops as profits develop

Look for additional setups

Post-Market Review

Analyze winning and losing trades

Review range quality vs. outcomes

Identify improvement areas

Prepare for next session

Best Stocks/ETFs for Opening Range Trading

Large Cap Stocks (Best for beginners):

AAPL, MSFT, GOOGL, AMZN, TSLA

High liquidity, predictable behavior

Good range formation most days

ETFs (Consistent patterns):

SPY, QQQ, IWM, XLF, XLE

Excellent liquidity

Clear range boundaries

Mid-Cap Growth (Advanced traders):

Stocks with good volume (1M+ shares daily)

Recent news catalysts

Clean technical patterns

Performance Optimization

Track These Metrics:

Win rate by range type (OR5 vs OR15 vs OR30)

Average R/R (risk vs reward ratio)

Best performing market conditions

Time of day performance

Continuous Improvement:

Keep detailed trade journal

Review failed breakouts for patterns

Adjust position sizing based on win rate

Refine entry timing based on backtesting

Final Tips for Success

Start small - Paper trade or use tiny positions initially

Focus on quality - Better to miss trades than take bad ones

Stay disciplined - Stick to your rules even during losing streaks

Adapt to conditions - What works in trending markets may fail in choppy conditions

Keep learning - Markets evolve, so should your approach

The opening range strategy is powerful because it captures natural market behavior, but like all strategies, it requires practice, discipline, and proper risk management to be profitable long-term.

Extremum Range MA Crossover Strategy1. Principle of Work & Strategy Logic ⚙️📈

Main idea: The strategy tries to catch the moment of a breakout from a price consolidation range (flat) and the start of a new trend. It combines two key elements:

Moving Average (MA) 📉: Acts as a dynamic support/resistance level and trend filter.

Range Extremes (Range High/Low) 🔺🔻: Define the borders of the recent price channel or consolidation.

The strategy does not attempt to catch absolute tops and bottoms. Instead, it enters an already formed move after the breakout, expecting continuation.

Type: Trend-following, momentum-based.

Timeframes: Works on different TFs (H1, H4, D), but best suited for H4 and higher, where breakouts are more meaningful.

2. Justification of Indicators & Settings ⚙️

A. Moving Average (MA) 📊

Why used: Core of the strategy. It smooths price fluctuations and helps define the trend. The price (via extremes) must cross the MA → signals a potential trend shift or strengthening.

Parameters:

maLength = 20: Default length (≈ one trading month, 20-21 days). Good balance between sensitivity & smoothing.

Lower TF → reduce (10–14).

Higher TF → increase (50).

maSource: Defines price source (default = Close). Alternatives (HL2, HLC3) → smoother, less noisy MA.

maType: Default = EMA (Exponential MA).

Why EMA? Faster reaction to recent price changes vs SMA → useful for breakout strategies.

Other options:

SMA 🟦 – classic, slowest.

WMA 🟨 – weights recent data stronger.

HMA 🟩 – near-zero lag, but “nervous,” more false signals.

DEMA/TEMA 🟧 – even faster & more sensitive than EMA.

VWMA 🔊 – volume-weighted.

ZLEMA ⏱ – reduced lag.

👉 Choice = tradeoff between speed of reaction & false signals.

B. Range Extremes (Previous High/Low) 📏

Why used: Define borders of recent trading range.

prevHigh = local resistance.

prevLow = local support.

Break of these levels on close = trigger.

Parameters:

lookbackPeriod = 5: Searches for highest high / lowest low of last 5 candles. Very recent range.

Higher value (10–20) → wider, stronger ranges but rarer signals.

3. Entry & Exit Rules 🎯

Long signals (BUY) 🟢📈

Condition (longCondition): Previous Low crosses MA from below upwards.

→ Price bounced from the bottom & strong enough to push range border above MA.

Execution: Auto-close short (if any) → open long.

Short signals (SELL) 🔴📉

Condition (shortCondition): Previous High crosses MA from above downwards.

→ Price rejected from the top, upper border failed above MA.

Execution: Auto-close long (if any) → open short.

Exit conditions 🚪

Exit Long (exitLongCondition): Close below prevLow.

→ Uptrend likely ended, range shifts down.

Exit Short (exitShortCondition): Close above prevHigh.

→ Downtrend likely ended, range shifts up.

⚠️ Important: Exit = only on candle close beyond extremes (not just wick).

4. Trading Settings ⚒️

overlay = true → indicators shown on chart.

initial_capital = 10000 💵.

default_qty_type = strategy.cash, default_qty_value = 100 → trades fixed $100 per order (not lots). Can switch to % of equity.

commission_type = strategy.commission.percent, commission_value = 0.1 → default broker fee = 0.1%. Adjust for your broker!

slippage = 3 → slippage = 3 ticks. Adjust to asset liquidity.

currency = USD.

margin_long = 100, margin_short = 100 → no leverage (100% margin).

5. Visualization on Chart 📊

The strategy draws 3 lines:

🔵 MA line (thickness 2).

🔴 Previous High (last N candles).

🟢 Previous Low (last N candles).

Also: entry/exit arrows & equity curve shown in backtest.

Disclaimer ⚠️📌

Risk Warning: This description & code are for educational purposes only. Not financial advice. Trading (Forex, Stocks, Crypto) carries high risk and may lead to full capital loss. You trade at your own risk.

Testing: Always backtest & demo test first. Past results ≠ future profits.

Responsibility: Author of this strategy & description is not responsible for your trading decisions or losses.

Dynamic Swing Anchored VWAP STRAT (Zeiierman/PineIndicators)Dynamic Swing Anchored VWAP STRATEGY — Zeiierman × PineIndicators (Pine Script v6)

A pivot-to-pivot Anchored VWAP strategy that adapts to volatility, enters long on bullish structure, and closes on bearish structure. Built for TradingView in Pine Script v6.

Full credits to zeiierman.

Repainting notice: The original indicator logic is repainting. Swing labels (HH/HL/LH/LL) are finalized after enough bars have printed, so labels do not occur in real time. It is not possible to execute at historical label points. Treat results as educational and validate with Bar Replay and paper trading before considering any discretionary use.

Concept

The script identifies swing highs/lows over a user-defined lookback ( Swing Period ). When structure flips (most recent swing low is newer than the most recent swing high, or vice versa), a new regime begins.

At each confirmed pivot, a fresh Anchored VWAP segment is started and updated bar-by-bar using an EWMA-style decay on price×volume and volume.

Responsiveness is controlled by Adaptive Price Tracking (APT) . Optionally, APT auto-adjusts with an ATR ratio so that high volatility accelerates responsiveness and low volatility smooths it.

Longs are opened/held in bullish regimes and closed when the regime turns bearish. No short positions are taken by design.

How it works (under the hood)

Swing detection: Uses ta.highestbars / ta.lowestbars over prd to update swing highs (ph) and lows (pl), plus their bar indices (phL, plL).

Regime logic: If phL > plL → bullish regime; else → bearish regime. A change in this condition triggers a re-anchor of the VWAP at the newest pivot.

Adaptive VWAP math: APT is converted to an exponential decay factor ( alphaFromAPT ), then applied to running sums of price×volume and volume, producing the current VWAP estimate.

Rendering: Each pivot-anchored VWAP segment is drawn as a polyline and color-coded by regime. Optional structure labels (HH/HL/LH/LL) annotate the swing character.

Orders: On bullish flips, strategy.entry("L") opens/maintains a long; on bearish flips, strategy.close("L") exits.

Inputs & controls

Swing Period (prd) — Higher values identify larger, slower swings; lower values catch more frequent pivots but add noise.

Adaptive Price Tracking (APT) — Governs the VWAP’s “half-life.” Smaller APT → faster/closer to price; larger APT → smoother/stabler.

Adapt APT by ATR ratio — When enabled, APT scales with volatility so the VWAP speeds up in turbulent markets and slows down in quiet markets.

Volatility Bias — Tunes the strength of APT’s response to volatility (above 1 = stronger effect; below 1 = milder).

Style settings — Colors for swing labels and VWAP segments, plus line width for visibility.

Trade logic summary

Entry: Long when the swing structure turns bullish (latest swing low is more recent than the last swing high).

Exit: Close the long when structure turns bearish.

Position size: qty = strategy.equity / close × 5 (dynamic sizing; scales with account equity and instrument price). Consider reducing the multiplier for a more conservative profile.

Recommended workflow

Apply to instruments with reliable volume (equities, futures, crypto; FX tick volume can work but varies by broker).

Start on your preferred timeframe. Intraday often benefits from smaller APT (more reactive); higher timeframes may prefer larger APT (smoother).

Begin with defaults ( prd=50, APT=20 ); then toggle “Adapt by ATR” and vary Volatility Bias to observe how segments tighten/loosen.

Use Bar Replay to watch how pivots confirm and how the strategy re-anchors VWAP at those confirmations.

Layer your own risk rules (stops/targets, max position cap, session filters) before any discretionary use.

Practical tips

Context filter: Consider combining with a higher-timeframe bias (e.g., daily trend) and using this strategy as an entry timing layer.

First pivot preference: Some traders prefer only the first bullish pivot after a bearish regime (and vice versa) to reduce whipsaw in choppy ranges.

Deviations: You can add VWAP deviation bands to pre-plan partial exits or re-entries on mean-reversion pulls.

Sessions: Session-based filters (RTH vs. ETH) can materially change behavior on futures and equities.

Extending the script (ideas)

Add stops/targets (e.g., ATR stop below last swing low; partial profits at k×VWAP deviation).

Introduce mirrored short logic for two-sided testing.

Include alert conditions for regime flips or for price-VWAP interactions.

Incorporate HTF confirmation (e.g., only long when daily VWAP slope ≥ 0).

Throttle entries (e.g., once per regime flip) to avoid over-trading in ranges.

Known limitations

Repainting: Swing labels and pivot confirmations depend on future bars; historical labels can look “perfect.” Treat them as annotations, not executable signals.

Execution realism: Strategy includes commission and slippage fields, yet actual fills differ by venue/liquidity.

No guarantees: Past behavior does not imply future results. This publication is for research/education only and not financial advice.

Defaults (backtest environment)

Initial capital: 10,000

Commission value: 0.01

Slippage: 1

Overlay: true

Max bars back: 5000; Max labels/polylines set for deep swing histories

Quick checklist

Add to chart and verify that the instrument has volume.

Use defaults, then tune APT and Volatility Bias with/without ATR adaptation.

Observe how each pivot re-anchors VWAP and how regime flips drive entries/exits.

Paper trade across several symbols/timeframes before any discretionary decisions.

Attribution & license

Original indicator concept and logic: Zeiierman — please credit the author.

Strategy wrapper and publication: PineIndicators .

License: CC BY-NC-SA 4.0 (Attribution-NonCommercial-ShareAlike). Respect the license when forking or publishing derivatives.

AVWAP+RSI Confluence — 1R TesterRSI + 1R ATR - Monthly P\&L (v4)

WHAT THIS STRATEGY DOES (OVERVIEW)

* Pine strategy (v4) that combines a simple momentum trigger with a symmetric 1R ATR risk model and an on-chart Monthly/Yearly P\&L table.

* Momentum filter: trades only when RSI crosses its own SMA in the direction of the trend (price vs Trend EMA).

* Risk engine: exits use fixed 1R ATR brackets captured at entry (no drifting targets/stops).

* Accounting: the table aggregates percentage returns by month and year using strategy equity.

ENTRY LOGIC (LONGS & OPTIONAL SHORTS)

Indicators used:

* RSI(rsiLen) and its SMA: SMA(RSI, rsiMaLen)

* Trend filter: EMA(emaTrendLen) on price

Longs:

1. RSI crosses above its RSI SMA

2. RSI > rsiBuyThr (filters weak momentum)

3. Close > EMA(emaTrendLen)

Shorts (optional via enableShort):

1. RSI crosses below its RSI SMA

2. RSI < rsiSellThr

3. Close < EMA(emaTrendLen)

EXIT LOGIC AND RISK MODEL (1R ATR)

* On entry, snapshot ATR(atrLen) into atrAtEntry and the average fill price into entryPx.

* Longs: stop = entryPx - ATR \* atrMult; target = entryPx + ATR \* atrMult

* Shorts: mirrored.

* Stops and targets are posted immediately and remain fixed for the life of the trade.

POSITION SIZING AND COSTS

* Default position size: 25% of equity per trade (adjustable in Properties/inputs).

* Commission percent and a small slippage are set in strategy() so backtests include friction by default.

MONTHLY / YEARLY P\&L TABLE (HOW IT WORKS)

* Uses strategy equity to compute bar returns: equity / equity\ - 1.

* Compounds bar returns into current month and current year; commits each finished period at month/year change (or last bar).

* Renders rows as years; columns Jan..Dec plus a Year total column.

* Cells colored by sign; precision and maximum rows are controlled by inputs.

* Values represent percentage returns, not currency P\&L.

VISUAL AIDS

* Two pivot trails (pivot high/low) are plotted for context only; they do not affect entries or exits.

CUSTOMIZATION TIPS

* Raise rsiBuyThr (long) or lower rsiSellThr (short) to filter weak momentum.

* Increase emaTrendLen to tighten trend alignment.

* Adjust atrLen and atrMult to fit your timeframe/instrument volatility.

* Leave enableShort = false if you prefer long-only behavior or shorting is constrained.

NON-REPAINTING AND BACKTEST NOTES

* Signals use bar-close crosses of built-in indicators (RSI, EMA, ATR); no future bars are referenced.

* calc\_on\_every\_tick = true for responsive visuals; Strategy Tester evaluates on bar close in history.

* Backtest stop/limit fills are simulated and may differ from live execution/liquidity.

DISCLAIMERS

* Educational use only. This is not financial advice. Markets involve risk. Past performance does not guarantee future results.

INPUTS (QUICK REFERENCE)

* rsiLen, rsiMaLen, rsiBuyThr, rsiSellThr

* emaTrendLen

* atrLen, atrMult, enableShort

* leftBars, rightBars, prec, showTable, maxYearsRows

SHORT TAGLINE

RSI momentum with 1R ATR brackets and a built-in Monthly/Yearly P\&L table.

TAGS

strategy, RSI, ATR, trend, risk-management, backtest, Pine-v4

Live Market - Performance MonitorLive Market — Performance Monitor

Study material (no code) — step-by-step training guide for learners

________________________________________

1) What this tool is — short overview

This indicator is a live market performance monitor designed for learning. It scans price, volume and volatility, detects order blocks and trendline events, applies filters (volume & ATR), generates trade signals (BUY/SELL), creates simple TP/SL trade management, and renders a compact dashboard summarizing market state, risk and performance metrics.

Use it to learn how multi-factor signals are constructed, how Greeks-style sensitivity is replaced by volatility/ATR reasoning, and how a live dashboard helps monitor trade quality.

________________________________________

2) Quick start — how a learner uses it (step-by-step)

1. Add the indicator to a chart (any ticker / timeframe).

2. Open inputs and review the main groups: Order Block, Trendline, Signal Filters, Display.

3. Start with defaults (OB periods ≈ 7, ATR multiplier 0.5, volume threshold 1.2) and observe the dashboard on the last bar.

4. Walk the chart back in time (use the last-bar update behavior) and watch how signals, order blocks, trendlines, and the performance counters change.

5. Run the hands-on labs below to build intuition.

________________________________________

3) Main configurable inputs (what you can tweak)

• Order Block Relevant Periods (default ~7): number of consecutive candles used to define an order block.

• Min. Percent Move for Valid OB (threshold): minimum percent move required for a valid order block.

• Number of OB Channels: how many past order block lines to keep visible.

• Trendline Period (tl_period): pivot lookback for detecting highs/lows used to draw trendlines.

• Use Wicks for Trendlines: whether pivot uses wicks or body.

• Extension Bars: how far trendlines are projected forward.

• Use Volume Filter + Volume Threshold Multiplier (e.g., 1.2): requires volume to be greater than multiplier × average volume.

• Use ATR Filter + ATR Multiplier: require bar range > ATR × multiplier to filter noise.

• Show Targets / Table settings / Colors for visualization.

________________________________________

4) Core building blocks — what the script computes (plain language)

Price & trend:

• Spot / LTP: current close price.

• EMA 9 / 21 / 50: fast, medium, slow moving averages to define short/medium trend.

o trend_bullish: EMA9 > EMA21 > EMA50

o trend_bearish: EMA9 < EMA21 < EMA50

o trend_neutral: otherwise

Volatility & noise:

• ATR (14): average true range used for dynamic target and filter sizing.

• dynamic_zone = ATR × atr_multiplier: minimum bar range required for meaningful move.

• Annualized volatility: stdev of price changes × sqrt(252) × 100 — used to classify volatility (HIGH/MEDIUM/LOW).

Momentum & oscillators:

• RSI 14: overbought/oversold indicator (thresholds 70/30).

• MACD: EMA(12)-EMA(26) and a 9-period signal line; histogram used for momentum direction and strength.

• Momentum (ta.mom 10): raw momentum over 10 bars.

Mean reversion / band context:

• Bollinger Bands (20, 2σ): upper, mid, lower.

o price_position measures where price sits inside the band range as 0–100.

Volume metrics:

• avg_volume = SMA(volume, 20) and volume_spike = volume > avg_volume × volume_threshold

o volume_ratio = volume / avg_volume

Support & Resistance:

• support_level = lowest low over 20 bars

• resistance_level = highest high over 20 bars

• current_position = percent of price between support & resistance (0–100)

________________________________________

5) Order Block detection — concept & logic

What it tries to find: a bar (the base) followed by N candles in the opposite direction (a classical order block setup), with a minimum % move to qualify. The script records the high/low of the base candle, averages them, and plots those levels as OB channels.

How learners should think about it (conceptual):

1. An order block is a signature area where institutions (theory) left liquidity — often seen as a large bar followed by a sequence of directional candles.

2. This indicator uses a configurable number of subsequent candles to confirm that the pattern exists.

3. When found, it stores and displays the base candle’s high/low area so students can see how price later reacts to those zones.

Implementation note for learners: the tool keeps a limited history of OB lines (ob_channels). When new OBs exceed the count, the oldest lines are removed — good practice to avoid clutter.

________________________________________

6) Trendline detection — idea & interpretation

• The script finds pivot highs and lows using a symmetric lookback (tl_period and half that as right/left).

• It then computes a trendline slope from successive pivots and projects the line forward (extension_bars).

• Break detection: Resistance break = close crosses above the projected resistance line; Support break = close crosses below projected support.

Learning tip: trendlines here are computed from pivot points and time. Watch how changing tl_period (bigger = smoother, fewer pivots) alters the trendlines and break signals.

________________________________________

7) Signal generation & filters — step-by-step

1. Primary triggers: