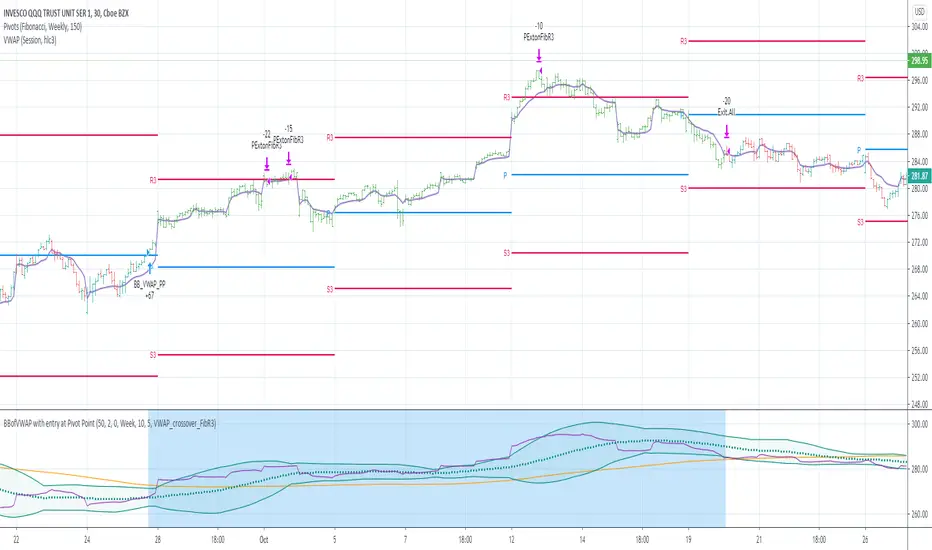

LCDT Trade Entry ToolLCDT Trade Entry Tool

Enter the Offset for the X Axis for the Entry Tool.

Enter the Offset for the Y Axis for the Entry Tool.

Enter the Price for your Stop Loss in $.

Enter your desired Risk Amount in $.

Enter the max amount of of Capital per Trade in $.

There are toggle buttons in the setup to reveal/remove more data in the label that pops up, as well as a toggle to make the text larger.

Pine Script® 인디케이터