ORB with Alerts - Current Day OnlyORB with Alerts - Current Day Only

This script plots the Opening Range Breakout (ORB) levels and provides alerts when price breaks above or below the range. It is designed for intraday trading and resets daily.

How It Works:

The ORB time in settings should be set to 15 minutes.

The Session Time should be set to 09:30 - 09:45.

The script marks the high and low of the ORB period and tracks price action for breakouts.

Alerts trigger when price crosses above the ORB high or below the ORB low.

This tool helps traders identify breakout opportunities based on early price action, aiding in momentum-based strategies

스크립트에서 "daily"에 대해 찾기

Keltner Channel StrategyOverview

The Keltner Channel Strategy is a powerful trend-following and mean-reversion system that leverages the Keltner Channels, EMA crossovers, and ATR-based stop-losses to optimize trade entries and exits. This strategy has proven to be highly effective, particularly when applied to Gold (XAUUSD) and other commodities with strong trend characteristics.

📈 How It Works

This strategy incorporates two trading approaches: 1️⃣ Keltner Channel Reversal Trades – Identifies overbought and oversold conditions when price touches the outer bands.

2️⃣ Trend Following Trades – Uses the 9 EMA & 21 EMA crossover, with confirmation from the 50 EMA, to enter trades in the direction of the trend.

🔍 Entry & Exit Criteria

📊 Keltner Channel Entries (Reversal Strategy)

✅ Long Entry: When the price crosses below the lower Keltner Band (potential reversal).

✅ Short Entry: When the price crosses above the upper Keltner Band (potential reversal).

⏳ Exit Conditions:

Long positions close when price crosses back above the mid-band (EMA-based).

Short positions close when price crosses back below the mid-band (EMA-based).

📈 Trend Following Entries (Momentum Strategy)

✅ Long Entry: When the 9 EMA crosses above the 21 EMA, and price is above the 50 EMA (bullish momentum).

✅ Short Entry: When the 9 EMA crosses below the 21 EMA, and price is below the 50 EMA (bearish momentum).

⏳ Exit Conditions:

Long positions close when the 9 EMA crosses back below the 21 EMA.

Short positions close when the 9 EMA crosses back above the 21 EMA.

📌 Risk Management & Profit Targeting

ATR-based Stop-Losses:

Long trades: Stop set at 1.5x ATR below entry price.

Short trades: Stop set at 1.5x ATR above entry price.

Take-Profit Levels:

Long trades: Profit target 2x ATR above entry price.

Short trades: Profit target 2x ATR below entry price.

🚀 Why Use This Strategy?

✅ Works exceptionally well on Gold (XAUUSD) due to high volatility.

✅ Combines reversal & trend strategies for improved adaptability.

✅ Uses ATR-based risk management for dynamic position sizing.

✅ Fully automated alerts for trade entries and exits.

🔔 Alerts

This script includes automated TradingView alerts for:

🔹 Keltner Band touches (Reversal signals).

🔹 EMA crossovers (Momentum trades).

🔹 Stop-loss & Take-profit activations.

📊 Ideal Markets & Timeframes

Best for: Gold (XAUUSD), NASDAQ (NQ), Crude Oil (CL), and trending assets.

Recommended Timeframes: 15m, 1H, 4H, Daily.

⚡️ How to Use

1️⃣ Add this script to your TradingView chart.

2️⃣ Select a 15m, 1H, or 4H timeframe for optimal results.

3️⃣ Enable alerts to receive trade notifications in real time.

4️⃣ Backtest and tweak ATR settings to fit your trading style.

🚀 Optimize your Gold trading with this Keltner Channel Strategy! Let me know how it performs for you. 💰📊

Rolling Pivot PointsThe "Rolling Pivot Points" indicator, built in Pine Script (version 6) for TradingView, overlays dynamic pivot levels on a price chart. It calculates a 24-hour lookback period (length = 1440 / (timeframe.in_seconds() / 60)) using the prior period’s high, low, and close to determine a Pivot Point (vPP) and three resistance (vR1, vR2, vR3) and support (vS1, vS2, vS3) levels. Plotted lines include vPP (yellow), vR1 (red), and vS1 (blue) in a cross style, with a customizable reset time (default: 8 AM) to refresh levels daily.

The indicator updates at the specified resetTime (minute = 0), otherwise retaining prior levels, making it ideal for intraday traders. The averageDays input (default: 5) is present but unclear in function. Suited for identifying key price zones, it adapts across timeframes, offering a concise, color-coded tool for technical analysis on TradingView.

Premarket Gap MomoTrader(SC)🚀 Pre-Market Momentum Trader | Dynamic Position Sizing 🔥

📈 Trade explosive pre-market breakouts with confidence! This algorithmic strategy automatically detects high-momentum setups, dynamically adjusts position size, and ensures risk control with a one-trade-per-day rule.

⸻

🎯 Key Features

✅ Pre-Market Trading (4:00 - 9:30 AM EST) – Only trades during the most volatile session for early breakouts.

✅ Dynamic Position Sizing – Adapts trade size based on candle strength:

• ≥90% body → 100% position

• ≥85% body → 50% position

• ≥75% body → 25% position

✅ 1 Trade Per Day – Avoids overtrading by allowing only one high-quality trade daily.

✅ Momentum Protection – Stays in the trade as long as:

• Every candle remains green (no red candles).

• Each new candle has increasing volume (confirming strong buying).

✅ Automated Exit – Closes position if:

• A red candle appears.

• Volume fails to increase on a green candle.

⸻

🔍 How It Works

📌 Entry Conditions:

✔️ Candle gains ≥5% from previous close.

✔️ Candle is green & body size ≥75% of total range.

✔️ Volume >15K (confirming liquidity).

✔️ Occurs within pre-market session (4:00 - 9:30 AM EST).

✔️ Only the first valid trade of the day is taken.

📌 Exit Conditions:

❌ First red candle after entry → Exit trade.

❌ First green candle with lower volume → Exit trade.

⸻

🏆 Why Use This?

🔹 Eliminates Fake Breakouts – No trade unless volume & momentum confirm.

🔹 Prevents Overtrading – Restricts to one quality trade per day.

🔹 Adaptable to Any Market – Works on stocks, crypto, or forex.

🔹 Hands-Free Execution – No manual chart watching required!

⸻

🚨 Important Notes

📢 Not financial advice. Trading involves risk—always backtest & practice on paper trading before using real money.

📢 Enable pre-market data in your TradingView settings for accurate results.

📢 Optimized for 1-minute & 5-minute timeframes.

🔔 Like this strategy? Leave a comment, share your results, and don’t forget to hit Follow for more strategies! 🚀🔥

THE Bucknut test PARI (SPY)📌 THE Bucknut Test PARI – Market Momentum & Volatility Gauge

🔹 Description

THE Bucknut Test PARI Indicator is a momentum and volatility-based market gauge designed to provide clear, actionable insights on price movement. This indicator calculates a Price Action Relative Index (PARI) score to help traders evaluate risk and potential market reversals.

It utilizes exponential moving average (EMA)-based momentum, standard deviation volatility, and SPY correlation to generate a PARI score between 1-100. The score is then categorized into risk zones, helping traders identify when conditions are favorable for entries or caution is needed.

Ideal for intraday traders, options traders (including SPX 0DTE), and swing traders looking to gauge volatility-driven market shifts.

🔥 Features & Functionality

✅ Momentum Calculation via EMA Filtering – Ensures smooth, responsive signals.

✅ Volatility-Based Adjustments – Uses standard deviation-based volatility scaling.

✅ SPY Correlation Filtering – Helps align momentum signals with market sentiment.

✅ User-Defined Timeframe Settings – Adjusts dynamically based on selected time intervals.

✅ Customizable Risk Thresholds – Allows traders to define high-risk, neutral, and low-risk zones.

✅ Non-Repainting Algorithm – Ensures reliable, static signals without revision.

⚙️ Settings & Adjustments

Setting Default Value Description

Time Frame Mode "5m-15m" Choose between 1m-3m, 5m-15m, or 1H-Daily. Affects smoothing values.

Scaling Factor 10 Adjusts PARI score sensitivity. Higher values amplify movement.

Background Color Black Custom background for the indicator panel.

Background Transparency 85 Controls indicator panel opacity (0 = solid, 100 = invisible).

High-Risk Threshold 80 Above this level, market is in overbought/high-risk conditions.

Low-Risk Threshold 20 Below this level, market is oversold/low-risk for potential reversals.

Neutral Level 50 Middle ground where price action is balanced.

📈 How to Use THE Bucknut Test PARI

🔴 Above 80 (High-Risk Zone)

Market may be overheated, strong momentum may fade or reverse soon.

Caution with calls; potential put opportunities.

🟢 Below 20 (Low-Risk Zone)

Market is oversold, potential reversal or bounce incoming.

Consider long entries or avoiding shorts.

⚪ Between 20-80 (Neutral Zone)

Market is in equilibrium; follow primary trend direction.

No extreme risk, trend-following strategies preferred.

🔍 Example Use Cases

✔ Intraday Traders → Gauge market strength on short-term charts (1m-15m).

✔ SPX 0DTE Options Traders → Time high-confidence call/put setups.

✔ Swing Traders → Identify periods of excessive momentum or exhaustion.

Quarter Shift IdentifierQuarter Shift Identifier

This indicator helps traders and analysts identify significant price movements between quarters. It calculates the percentage change from the close of the previous quarter to the current price and signals when this change exceeds a 4% threshold.

Key Features:

• Automatically detects quarter transitions

• Calculates quarter-to-quarter price changes

• Signals significant shifts when the change exceeds 4%

• Displays blue up arrows for bullish shifts and red down arrows for bearish shifts

How it works:

1. The script tracks the closing price of each quarter

2. When a new quarter begins, it calculates the percentage change from the previous quarter's close

3. If the change exceeds 4%, an arrow is plotted on the chart

This tool can be useful for:

• Identifying potential trend changes at quarter boundaries

• Analyzing seasonal patterns in price movements

• Supplementing other technical analysis tools for a comprehensive market view

Recommended Timeframes are Weekly and Daily.

Disclaimer:

This indicator is for informational and educational purposes only. It is not financial advice and should not be the sole basis for any investment decisions. Always conduct your own research and consider your personal financial situation before trading or investing. Past performance does not guarantee future results.

SOPR | QuantumResearchIntroducing Rocheur’s SOPR Indicator

The Spent Output Profit Ratio (SOPR) indicator by Rocheur is a powerful tool designed for analyzing Bitcoin market dynamics using on-chain data. By leveraging SOPR data and smoothing it through short- and long-term moving averages, this indicator provides traders with valuable insights into market behavior, helping them identify trends, reversals, and potential trading opportunities.

Understanding SOPR and Its Role in Trading

SOPR is a metric derived from on-chain data that measures the profit or loss of spent outputs on the Bitcoin network. It reflects the behavior of market participants based on the price at which Bitcoin was last moved. When SOPR is above 1, it indicates that outputs are being spent at a profit. Conversely, values below 1 suggest that outputs are being spent at a loss.

Rocheur’s SOPR indicator enhances this raw data by incorporating short-term and long-term smoothed trends, allowing traders to observe shifts in market sentiment and momentum.

How It Works

Data Source: The indicator uses SOPR data from Glassnode’s BTC_SOPR metric, updated daily.

Short-Term Trend (STH SOPR):

A Double Exponential Moving Average (DEMA) is applied over a customizable short-term length (default: 150 days).

This reflects recent market participant behavior.

Long-Term Trend (1-Year SOPR):

A Weighted Moving Average (WMA) is applied over a customizable long-term length (default: 365 days).

This captures broader market trends and investor behavior.

Trend Comparison:

Bullish Market: When STH SOPR exceeds the 1-year SOPR, the market is considered bullish.

Bearish Market: When STH SOPR falls below the 1-year SOPR, the market is considered bearish.

Neutral Market: When the two values are equal, the market is neutral.

Visual Representation

The indicator provides a color-coded visual representation for easy trend identification:

Green Bars: Indicate a bullish market where STH SOPR is above the 1-year SOPR.

Red Bars: Represent a bearish market where STH SOPR is below the 1-year SOPR.

Gray Bars: Show a neutral market condition where STH SOPR equals the 1-year SOPR.

The dynamic bar coloring allows traders to quickly assess the prevailing market sentiment and adjust their strategies accordingly.

Customization & Parameters

The SOPR Indicator offers several customizable settings to adapt to different trading styles and preferences:

Short-Term Length: Default set to 150 days, defines the smoothing period for the STH SOPR .

Long-Term Length: Default set to 365 days, defines the smoothing period for the 1-year SOPR.

Color Modes: Choose from seven distinct color schemes to personalize the indicator’s appearance.

Final Note

Rocheur’s SOPR Indicator is a unique tool that combines on-chain data with technical analysis to provide actionable insights for Bitcoin traders. Its ability to blend short- and long-term trends with a visually intuitive interface makes it an invaluable resource for navigating market dynamics. As with all indicators, backtesting and integration into a comprehensive strategy are essential for optimizing performance.

Bollinger Breakout Strategy with Direction Control [4H crypto]Bollinger Breakout Strategy with Direction Control - User Guide

This strategy leverages Bollinger Bands, RSI, and directional filters to identify potential breakout trading opportunities. It is designed for traders looking to capitalize on significant price movements while maintaining control over trade direction (long, short, or both). Here’s how to use this strategy effectively:

How the Strategy Works

Indicators Used:

Bollinger Bands:

A volatility-based indicator with an upper and lower band around a simple moving average (SMA). The bands expand or contract based on market volatility.

RSI (Relative Strength Index):

Measures momentum to determine overbought or oversold conditions. In this strategy, RSI is used to confirm breakout strength.

Trade Direction Control:

You can select whether to trade:

Long only: Buy positions.

Short only: Sell positions.

Both: Trade in both directions depending on conditions.

Breakout Conditions:

Long Trade:

The price closes above the upper Bollinger Band.

RSI is above the midline (50), confirming upward momentum.

The "Trade Direction" setting allows either "Long" or "Both."

Short Trade:

The price closes below the lower Bollinger Band.

RSI is below the midline (50), confirming downward momentum.

The "Trade Direction" setting allows either "Short" or "Both."

Risk Management:

Stop-Loss:

Long trades: Set at 2% below the entry price.

Short trades: Set at 2% above the entry price.

Take-Profit:

Calculated using a Risk/Reward Ratio (default is 2:1).

Adjust this in the strategy settings.

Inputs and Customization

Key Parameters:

Bollinger Bands Length: Default is 20. Adjust based on the desired sensitivity.

Multiplier: Default is 2.0. Higher values widen the bands; lower values narrow them.

RSI Length: Default is 14, which is standard for RSI.

Risk/Reward Ratio: Default is 2.0. Increase for more aggressive profit targets, decrease for conservative exits.

Trade Direction:

Options: "Long," "Short," or "Both."

Example: Set to "Long" in a bullish market to focus only on buy trades.

How to Use This Strategy

Adding the Strategy:

Paste the script into TradingView’s Pine Editor and add it to your chart.

Setting Parameters:

Adjust the Bollinger Band settings, RSI, and Risk/Reward Ratio to fit the asset and timeframe you're trading.

Analyzing Signals:

Green line (Upper Band): Signals breakout potential for long trades.

Red line (Lower Band): Signals breakout potential for short trades.

Blue line (Basis): Central Bollinger Band (SMA), helpful for understanding price trends.

Testing the Strategy:

Use the Strategy Tester in TradingView to backtest performance on your chosen asset and timeframe.

Optimizing for Assets:

Forex pairs, cryptocurrencies (like BTC), or stocks with high volatility are ideal for this strategy.

Works best on higher timeframes like 4H or Daily.

Best Practices

Combine with Volume: Confirm breakouts with increased volume for higher reliability.

Avoid Sideways Markets: Use additional trend filters (like ADX) to avoid trades in low-volatility conditions.

Optimize Parameters: Regularly adjust the Bollinger Bands multiplier and RSI settings to match the asset's behavior.

By utilizing this strategy, you can effectively trade breakouts while maintaining flexibility in trade direction. Adjust the parameters to match your trading style and market conditions for optimal results!

Honest Volatility Grid [Honestcowboy]The Honest Volatility Grid is an attempt at creating a robust grid trading strategy but without standard levels.

Normal grid systems use price levels like 1.01;1.02;1.03;1.04... and place an order at each of these levels. In this program instead we create a grid using keltner channels using a long term moving average.

🟦 IS THIS EVEN USEFUL?

The idea is to have a more fluid style of trading where levels expand and follow price and do not stick to precreated levels. This however also makes each closed trade different instead of using fixed take profit levels. In this strategy a take profit level can even be a loss. It is useful as a strategy because it works in a different way than most strategies, making it a good tool to diversify a portfolio of trading strategies.

🟦 STRATEGY

There are 10 levels below the moving average and 10 above the moving average. For each side of the moving average the strategy uses 1 to 3 orders maximum (3 shorts at top, 3 longs at bottom). For instance you buy at level 2 below moving average and you increase position size when level 6 is reached (a cheaper price) in order to spread risks.

By default the strategy exits all trades when the moving average is reached, this makes it a mean reversion strategy. It is specifically designed for the forex market as these in my experience exhibit a lot of ranging behaviour on all the timeframes below daily.

There is also a stop loss at the outer band by default, in case price moves too far from the mean.

What are the risks?

In case price decides to stay below the moving average and never reaches the outer band one trade can create a very substantial loss, as the bands will keep following price and are not at a fixed level.

Explanation of default parameters

By default the strategy uses a starting capital of 25000$, this is realistic for retail traders.

Lot sizes at each level are set to minimum lot size 0.01, there is no reason for the default to be risky, if you want to risk more or increase equity curve increase the number at your own risk.

Slippage set to 20 points: that's a normal 2 pip slippage you will find on brokers.

Fill limit assumtion 20 points: so it takes 2 pips to confirm a fill, normal forex spread.

Commission is set to 0.00005 per contract: this means that for each contract traded there is a 5$ or whatever base currency pair has as commission. The number is set to 0.00005 because pinescript does not know that 1 contract is 100000 units. So we divide the number by 100000 to get a realistic commission.

The script will also multiply lot size by 100000 because pinescript does not know that lots are 100000 units in forex.

Extra safety limit

Normally the script uses strategy.exit() to exit trades at TP or SL. But because these are created 1 bar after a limit or stop order is filled in pinescript. There are strategy.orders set at the outer boundaries of the script to hedge against that risk. These get deleted bar after the first order is filled. Purely to counteract news bars or huge spikes in price messing up backtest.

🟦 VISUAL GOODIES

I've added a market profile feature to the edge of the grid. This so you can see in which grid zone market has been the most over X bars in the past. Some traders may wish to only turn on the strategy whenever the market profile displays specific characteristics (ranging market for instance).

These simply count how many times a high, low, or close price has been in each zone for X bars in the past. it's these purple boxes at the right side of the chart.

🟦 Script can be fully automated to MT5

There are risk settings in lot sizes or % for alerts and symbol settings provided at the bottom of the indicator. The script will send alert to MT5 broker trying to mimic the execution that happens on tradingview. There are always delays when using a bridge to MT5 broker and there could be errors so be mindful of that. This script sends alerts in format so they can be read by tradingview.to which is a bridge between the platforms.

Use the all alert function calls feature when setting up alerts and make sure you provide the right webhook if you want to use this approach.

Almost every setting in this indicator has a tooltip added to it. So if any setting is not clear hover over the (?) icon on the right of the setting.

ICT Professional Accumulation DistributionICT Professional Accumulation Distribution (ICT AD) provides a x-ray view into market accumulation and distribution. You can literally see the institutions at work.

The indicator consists of two cumulative lines derived from:

Cumulative change from open to close

Cumulative change from previous close to new open

By overlaying these two cumulative lines, you can detect real meaningful divergence that is narrative based not mathematically derived. You're seeing the real works of algorithms in play working in this area.

These divergences are only useful at extremes (topping or bottoming formations), not while trending. It will probably confirm your suspicion about making a important high or low.

This works on all timeframes but is most impactful on the daily.

How to use:

Method 1:

Enable the option for "Show Open vs Close."

Calculate the shift by subtracting the "Open vs Close" line value from the ICT Accumulation/Distribution (AD) line value.

Look for divergences between the two cumulative lines.

Method 2:

Switch the chart's display mode to "Line View" (representing the Open vs Close).

look for divergences between the line chart and the ICT AD line.

MTF SqzMom [tradeviZion]Credits:

John Carter for creating the TTM Squeeze and TTM Squeeze Pro.

Lazybear for the original interpretation of the TTM Squeeze: Squeeze Momentum Indicator.

Makit0 for evolving Lazybear's script by incorporating TTM Squeeze Pro upgrades – Squeeze PRO Arrows.

MTF SqzMom - Multi-Timeframe Squeeze & Momentum Tool

MTF SqzMom is a tool designed to help traders easily monitor squeeze and momentum signals across multiple timeframes in a simple, organized format. Built using Pine Script 5, it ensures that data remains consistent, even when switching between different time intervals on the chart.

Key Features:

Multi-Timeframe Monitoring: Track squeeze and momentum signals across various timeframes, all in one view. This includes key timeframes like 1-minute, 5-minute, hourly, and daily.

Dynamic Table Display: A color-coded table that automatically adjusts based on the selected timeframes, offering a clear view of market conditions.

Alerts for Key Market Events: Get notifications when a squeeze starts or fires across your chosen timeframes, so you can stay informed without needing to monitor the chart continuously.

Customizable Appearance: Tailor the look of the table by selecting colors for squeeze levels and momentum shifts, and choose the best position on your chart for easy access.

How It Works:

MTF SqzMom is based on the concept of the squeeze, which signals periods of lower volatility where price breakouts may occur. The tool tracks this by monitoring the contraction of Bollinger Bands within Keltner Channels. Along with this, it provides momentum analysis to help you gauge the potential direction of the market after a squeeze.

Squeeze Conditions: The script tracks four levels of squeeze conditions (no squeeze, low, mid, and high), each represented by a different color in the table.

Momentum Analysis: Momentum is visually represented by colors indicating four stages: up increasing, up decreasing, down increasing, and down decreasing. This color coding helps you quickly assess whether the market is gaining or losing momentum.

Using Alerts:

You can enable two types of alerts: when a squeeze starts (indicating consolidation) and when a squeeze fires (indicating a breakout). These alerts cover all timeframes you’ve selected, so you never miss important signals.

How to Set It Up:

1. Enable Alerts in Settings: Turn on "Alert for Squeeze Start" and "Alert for Squeeze Fire" in the settings.

2. Add Alerts to Your Chart:

Click the three dots next to the indicator name.

Select "Add alert on tradeviZion - MTF SqzMom."

3. Customize and Save: Adjust alert options, choose your notification type, and click "Create."

Why Use MTF SqzMom ?

Consistent Data: The tool ensures that squeeze and momentum data remain consistent, even when you switch between chart intervals.

Real-Time Alerts: Stay updated with alerts for squeeze conditions without needing to constantly watch the chart.

Simple to Use, Customizable to Fit: You can easily adjust the table’s look and choose the timeframes and colors that best suit your trading style.

Acknowledgment:

While this tool builds on the TTM Squeeze concept developed by John Carter of Simpler Trading, it offers added flexibility through multi-timeframe analysis, alerts, and customizability to make monitoring market conditions more accessible.

Multi-time Frame Trend DirectionThis is a multi-time frame trend direction indicator. It indicates whether the trend is ascending or descending across multiple time frames: 5M, 15M, 30M, 1H, 4H, and Daily.

The logic is based on the positions of EMA12 and EMA26.

These EMAs are smoothed with an SMA.

Why 12 and 26, and why are they smoothed with 9?

As you might surmise, these parameters are derived from the MACD.

I recommend not altering the parameters, but the choice is yours. Enjoy.

Donchian Quest Research// =================================

Trend following strategy.

// =================================

Strategy uses two channels. One channel - for opening trades. Second channel - for closing.

Channel is similar to Donchian channel, but uses Close prices (not High/Low). That helps don't react to wicks of volatile candles (“stop hunting”). In most cases openings occur earlier than in Donchian channel. Closings occur only for real breakout.

// =================================

Strategy waits for beginning of trend - when price breakout of channel. Default length of both channels = 50 candles.

Conditions of trading:

- Open Long: If last Close = max Close for 50 closes.

- Close Long: If last Close = min Close for 50 closes.

- Open Short: If last Close = min Close for 50 closes.

- Close Short: If last Close = max Close for 50 closes.

// =================================

Color of lines:

- black - channel for opening trade.

- red - channel for closing trade.

- yellow - entry price.

- fuchsia - stoploss and breakeven.

- vertical green - go Long.

- vertical red - go Short.

- vertical gray - close in end, don't trade anymore.

// =================================

Order size calculated with ATR and volatility.

You can't trade 1 contract in BTC and 1 contract in XRP - for example. They have different price and volatility, so 1 contract BTC not equal 1 contract XRP.

Script uses universal calculation for every market. It is based on:

- Risk - USD sum you ready to loss in one trade. It calculated as percent of Equity.

- ATR indicator - measurement of volatility.

With default setting your stoploss = 0.5 percent of equity:

- If initial capital is 1000 USD and used parameter "Permit stop" - loss will be 5 USD (0.5 % of equity).

- If your Equity rises to 2000 USD and used parameter "Permit stop"- loss will be 10 USD (0.5 % of Equity).

// =================================

This Risk works only if you enable “Permit stop” parameter in Settings.

If this parameter disabled - strategy works as reversal strategy:

⁃ If close Long - channel border works as stoploss and momentarily go Short.

⁃ If close Short - channel border works as stoploss and momentarily go Long.

Channel borders changed dynamically. So sometime your loss will be greater than ‘Risk %’. Sometime - less than ‘Risk %’.

If this parameter enabled - maximum loss always equal to 'Risk %'. This parameter also include breakeven: if profit % = Risk %, then move stoploss to entry price.

// =================================

Like all trend following strategies - it works only in trend conditions. If no trend - slowly bleeding. There is no special additional indicator to filter trend/notrend. You need to trade every signal of strategy.

Strategy gives many losses:

⁃ 30 % of trades will close with profit.

⁃ 70 % of trades will close with loss.

⁃ But profit from 30% will be much greater than loss from 70 %.

Your task - patiently wait for it and don't use risky setting for position sizing.

// =================================

Recommended timeframe - Daily.

// =================================

Trend can vary in lengths. Selecting length of channels determine which trend you will be hunting:

⁃ 20/10 - from several days to several weeks.

⁃ 20/20 or 50/20 - from several weeks to several months.

⁃ 50/50 or 100/50 or 100/100 - from several months to several years.

// =================================

Inputs (Settings):

- Length: length of channel for trade opening/closing. You can choose 20/10, 20/20, 50/20, 50/50, 100/50, 100/100. Default value: 50/50.

- Permit Long / Permit short: Longs are most profitable for this strategy. You can disable Shorts and enable Longs only. Default value: permit all directions.

- Risk % of Equity: for position sizing used Equity percent. Don't use values greater than 5 % - it's risky. Default value: 0.5%.

⁃ ATR multiplier: this multiplier moves stoploss up or down. Big multiplier = small size of order, small profit, stoploss far from entry, low chance of stoploss. Small multiplier = big size of order, big profit, stop near entry, high chance of stoploss. Default value: 2.

- ATR length: number of candles to calculate ATR indicator. It used for order size and stoploss. Default value: 20.

- Close in end - to close active trade in the end (and don't trade anymore) or leave it open. You can see difference in Strategy Tester. Default value: don’t close.

- Permit stop: use stop or go reversal. Default value: without stop, reversal strategy.

// =================================

Properties (Settings):

- Initial capital - 1000 USD.

- Script don't uses 'Order size' - you need to change 'Risk %' in Inputs instead.

- Script don't uses 'Pyramiding'.

- 'Commission' 0.055 % and 'Slippage' 0 - this parameters are for crypto exchanges with perpetual contracts (for example Bybit). If use on other markets - set it accordingly to your exchange parameters.

// =================================

Big dataset used for chart - 'BITCOIN ALL TIME HISTORY INDEX'. It gives enough trades to understand logic of script. It have several good trends.

// =================================

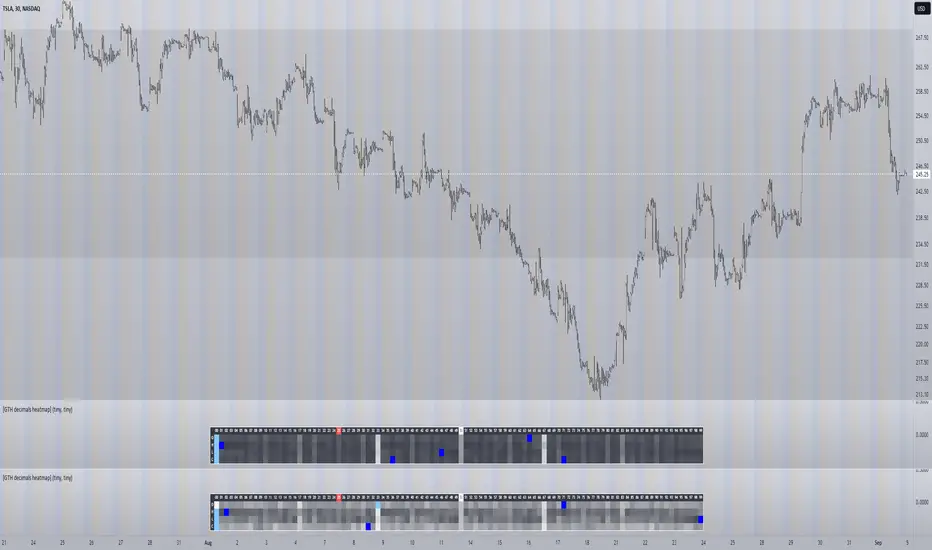

[GTH decimals heatmap] (wide screen advised)Preface

I share my personal general view on indicators below; skip ahead to the Description below if you are not interested.

It is my personal conviction that most - if not all - indicators rely mainly on trader's belief that they work, and in a feedback system like free markets they might become a self-fulfilling prophecy as a result, if (!) a big part of the traders believes in it, because some famous trader releases an indicator, or such person's public statement goes viral.

One of those voodoo indicators is the famous "follow-through day". There is zero statistical evidence for its validity, beyond the validity of a statement like "If it's bright at day it's usually the sun shining". The uselessness was proven exactly on its inventor's YT channel, Investors Business Daily. According to the examiner, its inventor William J. O'Neil himself could not explain the values used for this indicator. It might have been an incidental observation at some point without general validity. A.k.a "curve fitting". Still, it's being used by many today.

Another one of those indicators is the three points reversal on the S&P 500 Volatility Index (VIX) which allegedly might potentially maybe indicate a possible shift in trend. Both indicators share an immediately problematic feature: They use absolute values. Nothing is ever absolute in a highly subjective and emotionally driven game like the markets where a lot of money can be made and lost.

Most indicators can not produce additional information since they can only re-pack price/volume action. Many times an interpretion of the distance between price and a moving average and/or the slope of a moving average deliver very similar - if not better - results than MACD, RSI etc., especially with standard settings, the origin of which are usually unknown (always a warning sign). Very few indicators can deliver information which is otherwise hard to quantify, e. g. market noise (Kaufman's Efficiency Ratio or Price Density) or volatility, standard deviation etc.

It is common knowledge that trading the markets is a game of probability. No indicator works all the time (or at all, see above). In order to make decisions based on any indicator, the probability for its validity and the conditions under which validity seemed to have occurred, must be known. Otherwise it is just coffee grounds reading under the illusion of adding to the edge, when in fact it is only adding to the trees, making it even harder to see the forest.

Description

A common belief is that whole or half-dollar prices tend to be attraction points in price action, so a number of traders include those into decision making. But are they really...?

Spoiler Alert:

Generally, it is safe to say that for the big majority of stocks there is very thin evidence for it. It depends vastly on the asset, the timeframe used and the market period (pre/post/main trading times). If at all, there seems to be an above random but still thin evidence for whole prices being significant attraction points. Interesting/surprising patterns are visible on many stocks/timeframes/session periods, though.

The screenshot shows TSLA, 30m timeframe, two heatmaps added. The top one shows pre/post-market data only, the bottom one main market data only. The cyan fields indicate the strongest occurrence, the dark blue fields indicate the weakest occurrence of open/high/low/close prices at the respective decimal. The red field indicates the current/last price decimal.

Clearly, TSLA displays a strong pre-market attraction for .00, followed by .33 and .67 and .50. This pattern of thirds seems to be a unique feature of TSLA. In the main trading session it is being diluted by a more random distribution.

Other interesting equities to examine:

SPY: No significant pattern on any timeframe!

META: Generally weak patterns on all timeframes, but interestingly on the 1D there is evidence for less randomness on O and H, more on L and most on C.

AAPL: 1D, foggy attraction areas around .35 and .12. Whole price is no attraction area at all! Very weak attraction around .73.

AMD: Strong pattern on D, W, M, attraction areas around 1/16th intervals. No patterns on lower timeframes.

AMZN: Significant differences between pre/post and main session. Strong 1/16th pattern below D in pre/post.

TAOP: Strong 1/5th pattern on all timeframes.

Read the tool tips and go explore!

EMA 9/21 with Target Price [SS]Hey everyone,

Coming back with my EMA 9/21 indicator.

My original one was removed a long time ago because I didn't really realize that there were already plenty of similar indicators (my bad!) but this one is my unique, Steversteves edition haha.

About the Indicator:

Essentially, it just combines the 2 only EMA's I ever really use (the 9 and 21) with an ATR based analysis to calculate the average range a ticker undergoes after an EMA 9 / 21 Cross-over and Cross-under.

You can see the major example being in the chart above. I use this for dramatic effect as SPY just happened to have topped at the second expected bull target on the daily. But obviously the intention for this indicator is to be used on the smaller timeframes. Let's take a look at some examples with various tickers.

TSLA:

So let's just use the previous day as example (which was Friday). If we look to the chart below:

TSLA did an EMA 9/21 crossover (bullish) in premarket. This put the immediate TP at 234.59. If we play out the chart:

We shot right to it at open.

We then did a cross under with a TP of 225.93, but that was not realized as the sentiment was too bullish. We then cross back over to the upside, putthing next TP at 238.88 which was realized:

NVDA:

On Friday, NVDA was a bit of a mess, lots of whipsaw off open. But once we finally had a cross under with 3 consecutive closes below the EMA9/21 on the 5 minute chart, it solidified the likelihood of a short:

And this was the result:

We came down to the first target, held it actually as support before finally crossing back over, setting the next TP at 475.05. We got 3 consecutive closes above the EMA 9/21, so let's see what happened:

Nothing really, we closed before we got there, but we did make progress towards it.

And last but not least SPY:

We opened the day with a bullish crossover and 3 consecutive closes above the EMA9/21, making our TP 441.38 (chart above). Let's see what happened:

We came just shy of it after the fed release volatility slammed it down, where we got a crossunder (bearish) to a TP of 436.21:

This ended up playing out, we did get a bullish crossover later in the day and so let's see what happened then:

So those are the real examples, most recent examples of trading using this. They are not all perfect, which is intentional because you need to use a bit of your own analysis, of course, when you are using this type of strategy or indicator. The EMA 9/21 is not sufficient generally on its own, but it is very helpful to gauge the immediate PA and whether the expected move aligns with your overall thesis on the day in terms of realistic target prices.

Customizability:

In terms of the customizability, this is a very basic indicator aside from the assessment of ranges. So there really is not a lot to customize.

You can toggle off and on the labels if you do not want them, you can also adjust the lookback length for the ATR assessment. The lookback length is defaulted to 500, I do really highly suggest you leave it at 500 because this has worked well for me and in back-testing, it has performed above my own expectations.

But, that said, you can take this and back-test as you wish with whatever parameters you feel are most appropriate. I haven't back-tested this on every stock known to man, my go to's are SPY, QQQ, sometimes MSFT and so it works well on those. But perhaps some others will have differing results.

Final Thoughts:

That is the indicator in a nutshell! It is really self explanatory and its likely a strategy most of you already know. This just helps to add realistic price targets and context to those cross-overs and cross-unders.

It also works fine on larger timeframes. We can see it on the 1 hour with MSFT:

On the 2 hour hour with QQQ:

And I am sure you can find other examples!

That's it everyone, safe trades!

D-Bot Alpha RSI Breakout StrategyHello dear Traders,

Here is a simple yet effective strategy to use, for best profit higher time frame, such as daily.

Structure of the code

The code defines inputs for SMA (simple moving average) length, RSI (relative strength index) length, RSI entry level, RSI stop loss level, and RSI take profit level. The default values of these variables can be customized as per the user's preferences.

The script calculates SMA and RSI based on the input parameters and the closing price of the asset.

Trading logic

This strategy allows the placement of a long position when:

The RSI crosses above the RSI entry level and

The close price is above the SMA value.

After entering a long position, it applies a trailing stop mechanism. The stop price is updated to the close price if the close price is lower than the last close price.

The script closes the long position when:

RSI falls below the stop loss level.

RSI reaches or exceeds the take profit level.

If the trailing stop is activated (once RSI reaches or exceeds the take profit level), the closing price falls below the trailing stop level.

Strengths

The strategy includes mechanisms for entering a position, taking profit, and stopping losses, which are fundamental aspects of a trading strategy.

It applies a trailing stop mechanism that allows to capture further gains if the price keeps increasing while protecting from losses if the price starts to decrease.

Weaknesses

This strategy only contemplates long positions. Depending on the market situation, the strategy may miss opportunities for short selling when the market is on a downward trend.

The choice of the fixed RSI entry, stop loss, and take profit levels may not be ideal for all market conditions or assets. It might benefit from a more adaptive mechanism that adjusts these levels according to market volatility or trend.

The strategy doesn't factor in trading costs (such as spread or commission), which could have a significant impact on the net profit, especially if the user is trading with a high frequency or in a low liquidity market.

How to trade with this strategy

Given these parameters and the strategy outlined by the code, the trader would enter a long position when the RSI crosses above the RSI entry level (default 34) and the closing price is above the SMA value (SMA calculated with default period of 200). The trader would exit the position when either the RSI falls below the RSI stop loss level (default 30), or RSI rises above the RSI take profit level (default 50), or when the trailing stop is hit.

Remember "The strategies I have prepared are entirely for educational purposes and should not be considered as investment advice. Support your trades using other tools. Wishing everyone profitable trades..."