Séparateur H4 & DailyH4 & Daily Separator - TradingView Indicator

This Pine Script v6 indicator draws infinite vertical lines to mark H4 and Daily candle separations on your chart.

Features:

H4 Separations: Marks candles starting at 3am, 7am, 11am, 3pm, 7pm, and 11pm

Daily Separations: Marks candles starting at midnight (00:00)

Fully Customizable:

Toggle H4 and/or Daily lines independently

Choose line color, thickness (1-4), and style (Solid, Dotted, Dashed)

Control the number of visible vertical lines (1-500)

Use Case:

Perfect for traders who want to visualize higher timeframe separations while trading on lower timeframes. Helps identify H4 and Daily candle opens without switching charts.

Installation:

Simply copy the code into TradingView's Pine Editor and add it to your chart. All settings are adjustable in the indicator's settings panel.

스크립트에서 "daily"에 대해 찾기

SPY Daily Expected Move • Manual VIXSPY Daily Expected Move • Manual VIX — Description 📈🔥

This indicator calculates the daily expected move (EM) for SPY using a manual VIX input, then draws the projected high and low boundaries for the trading session.

It automatically retrieves the previous day’s closing price (or today’s open if you choose), then applies a volatility-based formula to estimate the range SPY is statistically likely to remain within. 📊

How the Expected Move Is Calculated 🧮

This indicator uses a simplified institutional volatility model:

\text{Expected % Move} = \frac{\text{VIX}}{\sqrt{252}}

This daily percentage is multiplied by your chosen baseline price:

📘 Previous Close (recommended — most accurate)

🌅 Today’s Open

✏️ Custom Price

And the script automatically plots:

🔼 Expected High

🔽 Expected Low

🏷️ Optional labels + info panel

Choosing the Correct Baseline 🎯

The baseline is one of the most important components of the expected move calculation.

Previous Day’s Close (Strongly Recommended) ✔️

Used by:

🏦 Market makers

🎛️ Options market makers

📐 Institutional volatility models

Expected move represents full-day implied volatility, making the previous close the mathematically correct anchor for SPY.

Using the VIX Input 🌡️

Enter the current VIX, taken from /VX futures or the ^VIX index.

⬆️ Higher VIX = larger expected move

⬇️ Lower VIX = tighter expected move

This lets you align SPY’s session range with real-time volatility conditions.

Recommended VIX-Based Multiplier Adjustments 🔧

The multiplier input allows you to fine-tune the expected move in different volatility regimes.

VIX Level Market Condition Recommended Multiplier

🟦 < 13 Very low volatility 0.9 — tight EM

🟩 13–18 Normal conditions 1.0 (default)

🟨 18–25 Elevated volatility 1.05 – 1.1

🟧 25–35 High volatility 1.2 – 1.3

🟥 > 35 Extreme volatility 1.4 – 1.6

These adjustments reflect how SPY’s actual intraday range stretches during higher volatility periods.

Why This Indicator Matters for SPY Traders 🚀

SPY is the most heavily traded ETF in the world, and market makers heavily rely on expected move to price options.

Because of that:

🧲 EM levels often act as dynamic support/resistance

📛 Breaks above/below EM can trigger gamma-driven trend days

🔄 Sweeps around EM frequently produce high-probability reversal zones

This indicator provides a statistically grounded framework that helps traders anticipate where SPY is most likely to:

move

stall

reverse

expand beyond expected range

All with clean, auto-updating levels that adjust daily based on your input of previous close price and the current VIX opening price.⚡📘

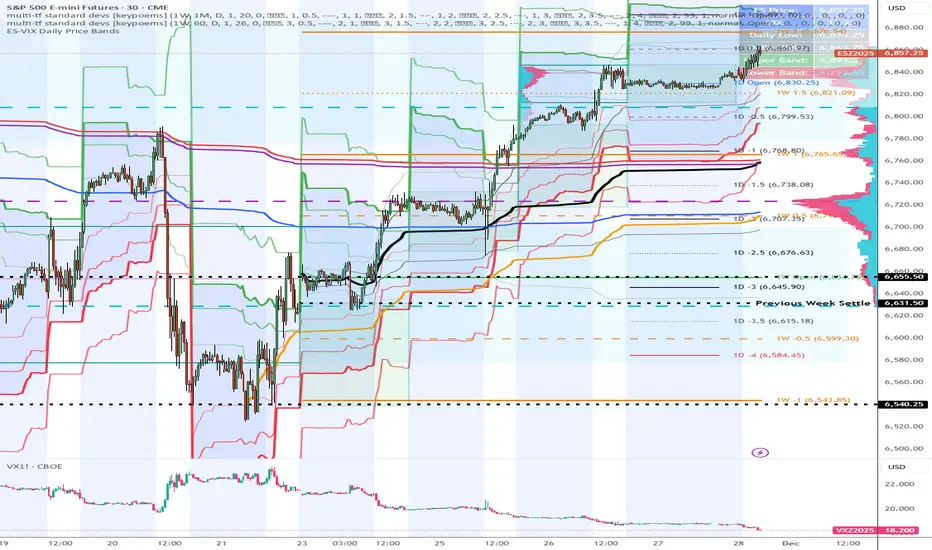

ES-VIX Daily Price Bands - Inner and OuterES-VIX Daily Price Bands

This indicator plots dynamic intraday price bands for ES futures based on real-time volatility levels measured by the VIX (CBOE Volatility Index). The bands evolve throughout the trading day, providing volatility-adjusted price targets.

Formulas:

Upper Band = Daily Low + (ES Price × VIX ÷ √252 ÷ 100)

Lower Band = Daily High - (ES Price × VIX ÷ √252 ÷ 100)

The calculation uses the square root of 252 (trading days per year) to convert annualized VIX volatility into an expected daily move, then scales it as a percentage adjustment from the current day's extremes.

Features:

Real-time band calculation that updates throughout the trading session

Upper band (green) extends from the current day's low

Lower band (red) contracts from the current day's high

Inner upper band (green) at 50% of expected move

Inner lower band (red) at 50% of expected move

Middle Inner upper band (green) at 80% of expected move

Middle Inner lower band (red) at 80% of expected move

Outer upper band (green) at 150% of expected move

Outer lower band (red) at 150% of expected move

Shaded zone between bands for visual clarity

Information table displaying:

Current ES price and VIX level

Running daily high and low

Current upper and lower band values

ES-VIX Daily Price Bands - Inner bands (80% and 50%)ES-VIX Daily Price Bands

This indicator plots dynamic intraday price bands for ES futures based on real-time volatility levels measured by the VIX (CBOE Volatility Index). The bands evolve throughout the trading day, providing volatility-adjusted price targets.

Formulas:

Upper Band = Daily Low + (ES Price × VIX ÷ √252 ÷ 100)

Lower Band = Daily High - (ES Price × VIX ÷ √252 ÷ 100)

The calculation uses the square root of 252 (trading days per year) to convert annualized VIX volatility into an expected daily move, then scales it as a percentage adjustment from the current day's extremes.

Features:

Real-time band calculation that updates throughout the trading session

Upper band (green) extends from the current day's low

Lower band (red) contracts from the current day's high

Inner upper band (green) at 50% of expected move

Inner lower band (red) at 50% of expected move

Middle Inner upper band (green) at 80% of expected move

Middle Inner lower band (red) at 80% of expected move

Shaded zone between bands for visual clarity

Information table displaying:

Current ES price and VIX level

Running daily high and low

Current upper and lower band values

ES-VIX Daily Price Bands - Inner bandsES-VIX Daily Price Bands

This indicator plots dynamic intraday price bands for ES futures based on real-time volatility levels measured by the VIX (CBOE Volatility Index). The bands evolve throughout the trading day, providing volatility-adjusted price targets.

Formulas:

Upper Band = Daily Low + (ES Price × VIX ÷ √252 ÷ 100)

Lower Band = Daily High - (ES Price × VIX ÷ √252 ÷ 100)

The calculation uses the square root of 252 (trading days per year) to convert annualized VIX volatility into an expected daily move, then scales it as a percentage adjustment from the current day's extremes.

Features:

Real-time band calculation that updates throughout the trading session

Upper band (green) extends from the current day's low

Lower band (red) contracts from the current day's high

Inner upper band (green) at 50% of expected move

Inner lower band (red) at 50% of expected move

Shaded zone between bands for visual clarity

Information table displaying:

Current ES price and VIX level

Running daily high and low

Current upper and lower band values

ES-VIX Daily Price BandsES-VIX Daily Price Bands

This indicator plots dynamic intraday price bands for ES futures based on real-time volatility levels measured by the VIX (CBOE Volatility Index). The bands evolve throughout the trading day, providing volatility-adjusted price targets.

Formulas:

Upper Band = Daily Low + (ES Price × VIX ÷ √252 ÷ 100)

Lower Band = Daily High - (ES Price × VIX ÷ √252 ÷ 100)

The calculation uses the square root of 252 (trading days per year) to convert annualized VIX volatility into an expected daily move, then scales it as a percentage adjustment from the current day's extremes.

Features:

Real-time band calculation that updates throughout the trading session

Upper band (green) extends from the current day's low

Lower band (red) contracts from the current day's high

Shaded zone between bands for visual clarity

Information table displaying:

Current ES price and VIX level

Running daily high and low

Current upper and lower band values

ES-VIX Expected Daily MoveThis indicator calculates the expected daily price movement for ES futures based on current volatility levels as measured by the VIX (CBOE Volatility Index).

Formula:

Expected Daily Move = (ES Price × VIX Price) / √252 / 100

The calculation converts the annualized VIX volatility into an expected daily move by dividing by the square root of 252 (the approximate number of trading days per year).

Features:

Real-time calculation using current ES futures price and VIX level

Histogram visualization in a separate pane for easy trend analysis

Information table displaying:

Current ES futures price

Current VIX level

Expected daily move in points

Expected daily move as a percentage

Karapuz Daily Context EngineKarapuz Daily Context Engine is designed for traders who want to understand the day’s context in advance and see how the market shapes its structure even before European liquidity hits the chart. It blends Asian session analysis with fractal structure, helping you quickly grasp the market’s intraday dynamics and potential directional bias.

The indicator automatically highlights the Asian session, reads its range, and compares it to the previous one. Based on this comparison, it generates a color-coded state — a daily sentiment marker that instantly shows whether buyers or sellers are taking the initiative.

The Asia box fills with color one hour before the Frankfurt open, giving you early access to the emerging context and making this tool perfect for your morning preparation.

Fractals act as clean structural cues, helping you identify key local highs and lows without cluttering the chart.

Key Features:

Intelligent detection and analysis of the Asian session.

Color-based daily context generated by comparing the current and previous Asian ranges.

True daily context that refreshes every new trading day.

Early visualization — session shading appears 1 hour before Frankfurt opens.

Adjustable fractals (3/5 bars) for clean structural insights.

Minimalistic, sharp visual design optimized for fast chart reading.

For contact or questions, you can reach me on Telegram: @KarapuzGG

SPY Daily Gamma Levels [Manual Input With Alerts]Overview This indicator plots key options-based support and resistance levels (Gamma Exposure / GEX) directly on your chart. Unlike standard technical analysis, these levels (Call Wall, Gamma Flip, Put Support, and Volatility Trigger) represent where Market Makers are positioned, often acting as "magnets" or "repellents" for price action.

Important Note: TradingView Pine Script cannot currently access external options open interest data natively. Therefore, this is a Manual Input Indicator. You must update the four price levels in the settings each morning before the market opens.

Key Features:

4 Key Levels: Plots the Call Wall, Gamma Flip (Zero Gamma), Put Support, and Volatility Trigger.

Auto-Cleaning: Automatically deletes yesterday's lines to keep your chart clean; lines only show for the current session.

Alerts Included: Built-in alert conditions allow you to set notifications when price crosses the Gamma Flip or breaks the Vol Trigger.

Customization: Fully customizable colors and line styles.

Best Practices:

Timeframe: Works best on 15-minute charts for trend identification and 5-minute charts for entry execution.

Strategy:

Above Gamma Flip: Market generally stabilizes; dealers buy dips.

Below Gamma Flip: Volatility expands; dealers sell rips.

Below Vol Trigger: "Danger Zone" – expect accelerated selling pressure.

How to Get the Data (The AI Workflow)

Since these numbers change daily, I use Google Gemini to fetch the data and remind me every morning. Here is how you can set up the same automated workflow:

1. The Prompt You can ask Gemini (or your preferred AI) the following prompt manually each morning:

"Find the daily SPY Call Wall, Gamma Flip, Put Support, and Vol Trigger levels for today to input into my TradingView indicator."

2. Automating the Routine I have set up a scheduled daily reminder with Gemini. To do this yourself, simply ask Gemini:

"Can you schedule a daily task to search for these SPY Gamma levels and send them to me every morning at 8:00 AM?"

3. Updating the Chart

Receive the notification from the AI.

Open the Indicator Settings in TradingView.

Type in the new numbers.

The chart updates instantly.

Disclaimer: This tool is for educational purposes only. Gamma levels are estimates based on Open Interest and Dealer Gamma exposure models. Always manage your risk.

ORB + Fair Value Gaps (FVG/iFVG) Suite with Daily 50% MidlineA complete smart-money–focused price-action toolkit combining the New York Open Range Breakout (ORB), ICT-style Fair Value Gaps, Inverted FVGs, and a dynamic Daily 50% Midline.

Designed for traders who want a clean, fast, and highly visual way to track liquidity, imbalances, and intraday directional bias.

📌 Key Features

1. NY Session ORB (09:30–09:45 New York Time)

Automatically plots:

ORB High

ORB Low

Labels for ORB high/low

Optional 5-minute chart restriction

Lines extend forward for easy reference

Used to identify breakout conditions, liquidity sweeps, and directional bias into the morning session.

📌 2. ICT-Style Fair Value Gaps (FVGs)

Full automated detection of bullish & bearish FVGs based on the classic 3-candle displacement structure:

Bullish FVG: high < low

Bearish FVG: low > high

Each FVG is drawn as a box with:

Custom colour

Custom border style (solid, dashed, dotted)

Automatic extension to the right until filled

Optional size text showing the gap in points (font size/colour adjustable)

Adjustable max lookback for performance

📌 3. Inverted FVGs (iFVGs)

Once price fully fills an FVG, it automatically becomes an iFVG, shown with:

Custom iFVG colour

Custom border style

Extension to the right

Once price trades through the zone from the opposite side, the iFVG is considered “consumed” and:

It stops extending

And optionally auto-deletes based on user settings

This makes it easy to track meaningful imbalances that turn into liquidity pockets.

📌 4. “Show Only After ORB” Filter

Optionally hide all FVGs/iFVGs formed before the ORB completes.

This is especially useful for intraday strategies focused on NY session structure only.

📌 5. Daily 50% Midline (OHLC Midpoint)

A dynamic, always-updating midpoint of the current daily candle:

Mid = (Daily High + Daily Low) / 2

Features:

Custom colour

Dashed styling

Extends left and right as a horizontal ray

Updates live as the daily candle forms

Great for bias filters, mean reversion, and daily liquidity zones.

📌 6. Performance-Optimized (Fast!)

Built with:

Fully configurable max lookback

Memory-efficient arrays

Auto-cleaning of old FVG/iFVG objects

Lightweight daily midline recalculation

This allows extremely fast rendering even on 1-minute charts.

📌 7. Alerts

Includes a clean alert condition:

Price returned to a Fair Value Gap

Works for both bullish and bearish FVG revisits.

🎯 Who This Indicator Is For

This tool is ideal for traders who use:

ICT / SMC concepts

Liquidity-based trading

ORB strategies

Imbalance-driven price action

Intraday or NY session-focused setups

Futures, crypto, forex, and equities

🎁 Summary

This indicator gives you:

A clean ORB framework

Automatic, dynamic FVG and iFVG analysis

Real-time daily candle context

Customizable visuals

Powerful session filtering

Efficient performance

All in one clean, intuitive package built for real-time decision making.

RSI Arrow Signals (Daily & Weekly)📘 Indicator Overview

This indicator identifies oversold conditions using RSI on two higher timeframes and plots visual signals directly on the chart. It is designed for traders who want to track multi-timeframe RSI exhaustion without switching charts.

🔍 How It Works

1. Daily RSI Signal (Orange Arrow)

The script pulls Daily RSI using request.security().

When the Daily RSI closes at 30 or below, an orange upward arrow is displayed beneath the bar.

2. Weekly RSI Signal (Red Arrow)

The script also retrieves Weekly RSI.

When the Weekly RSI closes at 30 or below, a red upward arrow appears beneath the bar.

Both signals use confirmed candle data to reduce repainting.

🎯 Purpose

This tool highlights potential oversold reversal zones across two key timeframes.

It helps traders quickly identify moments when price may be stretched to the downside on Daily or Weekly context

⚙️ Features

Multi-timeframe RSI (Daily & Weekly)

Color-coded arrow signals for quick visual recognition

Optional alert conditions for automated notifications

Works on any chart timeframe via request.security()

Repaint-safe (no lookahead_on)

📌 Important Notes

Signals only appear after the Daily or Weekly candle closes.

This indicator is not a buy/sell system; it serves as a market condition signal.

Use together with your own risk management and additional confluence.

*this indicator is helped by GPT

SVE Daily ATR + SDTR Context BandsSVE Daily ATR + SDTR Context Bands is a free companion overlay from The Volatility Engine™ ecosystem.

It plots daily ATR-based expansion levels and a Standardized Deviation Threshold Range (SDTR) to give traders a clean, quantitative view of where intraday price sits relative to typical daily movement and volatility extremes.

This module is designed as an SVE-compatible context layer—using discrete, RTH-aligned daily zones, expected-move bands, and a standardized volatility shell—so traders can build situational awareness even without the full SPX Volatility Engine™ (SVE).

It does not generate trade signals.

Its sole purpose is to provide a clear volatility framework you can combine with your own structure, Fibonacci, or signal logic (including SVE, if you use it).

🔍 What It Shows

* Daily ATR Bands (expHigh / expLow)

- Expected high/low based on smoothed daily ATR

- Updates at the RTH open

* Daily SDTR Bands (expHighSDTR / expLowSDTR)

- Standard deviation threshold range for volatility extremes

- Helps identify overextended conditions

Discrete RTH-aligned Zones

- Bands reset cleanly at each RTH session

No continuous carry-over from prior days

Daily ATR & SDTR stats label

Quick-reference box showing current ATR and SDTR values

🎯 Purpose

This tool helps traders:

- Gauge intraday context relative to expected daily movement

- Assess volatility state (quiet, normal, expanded, extreme)

- Identify likely exhaustion or expansion zones

- Frame intraday price action inside daily volatility rails

- Support decision-making with objective context rather than emotion

It complements any strategy and works on any intraday timeframe.

⚙️ Inputs

- ATR Lookback (default: 20 days)

- RTH Session Times

- SDTR Lookback

- Show/Hide Daily Stats Label

🧩 Part of the SVE Ecosystem

This module is part of the broader SPX Volatility Engine™ framework.

The full SVE system includes:

- Composite signal scoring

- Volatility compression logic

- Histogram slope and momentum analysis

- Internals (VIX / VVIX / TICK)

- Structural zone awareness

- Real-time bias selection

- High-clarity decision support

⚠️ Disclaimer

This tool is provided for educational and informational purposes only.

No performance claims are made or implied.

Not investment advice.

Average Daily Range DashboardThis script displays a non-intrusive ADR (Average Daily Range) dashboard designed to assist traders in monitoring real-time range expansion throughout the trading session. It compares the current day's high-low range to the average daily range calculated over a user-defined number of previous completed days (default: 5).

The tool provides a numerical ADR score (0–5) based on how much of the average daily range has been filled. It also includes optional visual cues and narrative descriptions to help contextualize current price behavior.

📘 Key Features:

Calculates ADR using fully completed daily bars (excluding the current session)

Tracks the current session’s intraday range live (high to low)

Outputs a score from 0 (low range expansion) to 5 (ADR fully filled or exceeded)

Optional alerts when ADR thresholds are crossed (e.g., 60%, 100%)

Displays optional debug values: ADR value, today’s range, session high/low

Customizable table position, size, colors, and visibility settings

🧮 Formula Transparency:

ADR = Simple Moving Average of (Daily High - Low) over the last N completed days

Intraday Range = Real-time (Session High - Session Low)

ADR Score is derived by comparing current range to ADR:

score = floor((sessionRange / adr) * 5), capped at 5

⚠️ Disclaimer:

This tool does not provide buy/sell signals, trading advice, or predictive forecasts. It is intended for educational and informational purposes only. Users should independently verify all data and apply their own analysis. Past performance of any range behavior is not indicative of future results.

ATR Daily (Classic vs Robust, NY-Fix, Spike Control)📘 What this indicator does

This tool provides an advanced view of daily market volatility by comparing two versions of the Average True Range (ATR):

• Classic ATR — standard Wilder smoothing

• Robust ATR — uses median-based filtering and spike-control logic to reduce distortion from abnormal candles

Both values are calculated using daily data aligned to the New York trading session, so volatility resets at the same moment each institutional trading day begins. This keeps readings consistent across crypto, forex and stocks, even on intraday charts.

⚙️ How it works (in simple terms)

The script evaluates each True Range (TR) value relative to a median-based threshold:

• Abnormally large ranges are either clamped to a limit or excluded from updating ATR

• A hard cap prevents single spikes from inflating the entire indicator

• The result is a smoother and more realistic representation of daily volatility

This allows ATR to reflect typical market behaviour instead of rare one-off events.

📊 What appears on the chart

• Two daily ATR lines (Classic and Robust)

• Histogram showing the percentage of daily range already completed

• Red bars when price exceeds 100% of daily ATR

• A data table with volatility metrics

• Background highlights on days with extreme values

💡 How traders can use it

• Identify when a market has already completed most of its typical daily move

• Compare Classic vs Robust ATR to spot news-driven distortion

• Use Robust ATR for more stable stop-loss and take-profit logic

• Track volatility expansion or contraction across sessions

⚙️ Key settings

Setting Purpose

ATR period Standard smoothing length (default 14)

Robust mode Clamp, Freeze or Off

MAD multiplier Sensitivity to outliers

Cap × median(TR) Maximum allowed spike size

Base for passed ATR Which ATR is used to measure daily %

Freeze weekends Keeps ATR unchanged on Sat/Sun

🧩 Unique concept

Unlike typical ATR indicators, this one combines robust statistics (median + MAD) with session-based fixation. ATR values update only once per New York session, creating stable volatility measurements that match institutional timing.

🔒 Source code

The script is published with protected source code to preserve its statistical structure and prevent unauthorized modification.

🧭 Summary

ATR Daily (Classic vs Robust, NY-Fix) provides a clearer and more reliable view of daily volatility.

It helps determine whether the market is still in the early phase of its daily range or already exhausted.

% Levels from previous Daily Close % Levels from Previous Close

This indicator plots up to three customizable percentage bands above and below the previous day's close, providing a clear visual reference for intraday price action relative to yesterday’s session.

Concept

Inspired by volatility studies (such as the SqueezeMetrics research showing that most SPX sessions close within ±1%), this tool helps traders visualize statistically relevant daily ranges.

The levels remain fixed for the entire day — they only update once a new daily session begins — allowing for consistent reference points throughout intraday trading.

Features

Up to three percentage levels (configurable in settings)

Static daily bands anchored to the previous close

Optional shaded zones between upper and lower levels

Optional midline showing the exact previous close

Works on any symbol and timeframe

Use cases

Identify high-probability daily range boundaries

Combine with VWAP or volume profile to locate confluence zones

Define structured intraday risk/reward targets

Analyze volatility expansion versus mean reversion

Note

Some CFD symbols may use a different daily session close compared to the underlying cash index.

For best accuracy, use the same session settings as the instrument you trade.

ICT Daily Wick QuadrantsICT DAILY WICK QUADRANTS

Inspired by ICT's teachings, this indicator allows you to view previous daily wicks (adjustable ratio to body threshold) on any timeframe chart, both at their origin and conveniently ahead of price.

Color coding, day of week labels, and directional arrows allow you to easily identify and visualize any notable daily candles wick in order to anticipate potential price behavior at that qaudrant. Keeping your chart clean and free of clutter is important.

Thanks to a great idea by @fadizeidan aka (fadi), the lines will remain muted to an adjustable degree according to a user adjusted distance of price. This will only highlight levels nearby and relevant to current price action, while fading out more distant levels. Of course this is optional and adjustable.

Each daily candle wick label contains options to show the percentage (0%,25%,50%,75%,100%), the direction of the candle (arrow up for up close, arrow down for down close), the open, close, lower quadrant, mid, upper quadrant, and high/low of that candle, and the day of the week. There is also a set of labels with the same option

Vwap Daily By SamsungTitle

Daily VWAP with Historical Lookback (Logic Fix)

Description

This script calculates and plots the daily Volume-Weighted Average Price (VWAP), an essential tool for intraday traders.

What makes this indicator special is its robust plotting logic. Unlike many simple VWAP scripts that struggle to show data for previous days, this version includes a crucial fix that allows you to reliably display historical VWAP lines for as many days back as you need. This allows for more comprehensive backtesting and analysis of how price has interacted with the VWAP on previous trading days.

This is an indispensable tool for traders who use VWAP as a dynamic level of support/resistance, a benchmark for trade execution quality, or a gauge of the day's trend.

Key Features

Historical VWAP Display: Easily plot VWAP for multiple past days on your chart. Simply set the number of lookback days in the settings.

Accurate Daily Calculation: The VWAP calculation correctly resets at the beginning of each new trading session (00:00 server time).

Fully Customizable: You have full control over the appearance of the VWAP line, including its color, width, and style (Solid or Stepped).

Robust Plotting Engine: This script solves the common Pine Script issue where conditionally plotted historical lines fail to render. It works reliably on all intraday timeframes.

Built-in Debug Mode: For advanced users or those curious about the inner workings, a comprehensive debug mode can be enabled to display raw VWAP values, cumulative volume, and timeframe warnings.

How to Use

Add the "Daily VWAP with Historical Lookback" indicator to your chart.

IMPORTANT: Make sure you are on an intraday timeframe (e.g., 1H, 30M, 15M, 5M, 1M). This indicator is designed for intraday analysis and will display a warning if used on a daily or higher timeframe.

Open the indicator's settings.

In the "VWAP Settings" tab, adjust the "Lookback Days to Display" to set how many previous days of VWAP you want to see. (e.g., 0 for today only, 1 for today and yesterday, 10 for the last 10 days).

Customize the line's appearance in the "Line Style" tab.

The "Logic Fix" Explained (For Developers)

A common challenge in Pine Script is conditionally plotting data for historical bars. Many scripts attempt this by dynamically changing the plot color to na (transparent) for bars that shouldn't be displayed. This method is often unreliable and can result in the entire plot failing to render.

This script employs a more robust and standard approach: manipulating the data series itself.

The Problem: plot(vwap, color = shouldPlot ? color.red : na) can be buggy.

The Solution: plot(shouldPlot ? vwap : na, color = color.red) is reliable.

Instead of changing the color, we create a new data series (plotVwap). This series contains the vwapValue only on the bars that meet our date criteria. On all other bars, its value is na (Not a Number). The plot() function is designed to handle na values by simply "lifting the pen," creating a clean break in the line. This ensures that the VWAP is drawn only for the selected days, with 100% reliability across all historical data.

Settings Explained

Lookback Days to Display: Sets the number of past days (from the last visible bar) for which to display the VWAP.

Line Color, Width, and Style: Standard cosmetic settings for the VWAP line.

Enable Debug Mode (Master Switch): Toggles all debugging features on or off. It is enabled by default to help new users.

Display Debug: Cumulative Volume: When enabled, it shows the daily cumulative volume in a gray area on a separate pane.

Display Debug: Raw VWAP Value: When enabled, it plots the raw, unfiltered VWAP calculation for all days on the chart, helping to verify the core logic.

This script is provided for educational and informational purposes. Trading involves significant risk. Always conduct your own research and analysis before making any trading decisions.

If you find this script useful, a 'Like' is always appreciated! Happy trading

Weekly & Daily Key LevelsWeekly & Daily Key Levels Indicator

This is a multi-timeframe support and resistance indicator that displays critical weekly and daily price levels for A+ -grade trading decisions.

What It Does:

Weekly Levels:

Current Weekly Open (purple) - Key pivot for the week

Previous Weekly High/Low (green/red) - Major support/resistance zones

Previous Weekly Close (gray) - Institutional reference point

Mid-Week Level (orange) - 50% retracement level between weekly high/low

Gap Zones - Visual highlighting of weekly gaps with fill tracking

Daily Levels:

Previous Day Open, High, Low, Close - Essential intraday reference points

Previous Day VWAP (Volume Weighted Average Price) - Institution money flow level

Key Features:

Support/Resistance Zones:

Adjustable zone width around weekly high/low

Color-coded fills (green resistance, red support)

Helps identify optimal entry/exit ranges vs precise lines

Gap Analysis:

Automatic weekly gap detection

Visual gap fill zones (lime = gap up, orange = gap down)

Gap fill tracking and alerts

Real-Time Analysis Table:

Current price position vs all weekly levels

Current price position vs all daily levels

Trading bias indicators (BULLISH/BEARISH/NEUTRAL)

Gap status monitoring

Smart Alerts:

Weekly high/low breakouts

Daily high/low breakouts

Weekly open and mid-level crosses

Gap fills

VWAP crosses

Best Use Cases:

Swing Trading: Use weekly levels for major support/resistance and trade direction

Day Trading: Combine daily levels with weekly context for high-probability setups

Institutional Trading: VWAP and weekly open are key levels where smart money operates

Gap Trading: Track and trade gap fill scenarios

Multi-Timeframe Analysis: See the "big picture" structure on any timeframe

Settings:

Toggle individual level displays

Adjustable zone widths

Customizable alerts

Clean visual presentation that doesn't clutter charts

Adjustments settings based on your trading style. Works on all instruments and timeframes. I am open to any suggested improvements.

Average Daily Range [Blaz]Version 1.0 – Published October 2025: Initial release

1. Overview & Purpose

The Average Daily Range is an advanced volatility assessment tool designed to give traders a clear, real-time view of the market's expected daily movement. It calculates the average range between daily highs and lows over a user-defined historical period and projects this average onto the current trading session.

By visualising the potential high and low boundaries for the day, this indicator assists in setting realistic profit targets, managing risk effectively, and identifying when price action is becoming overextended relative to its recent volatility profile. It is an essential tool for day traders and swing traders across all markets, including Forex, Stocks, Crypto, Futures, and Commodities.

2. Core Functionality & Key Features

The indicator provides a dynamic, multi-faceted analysis of daily volatility:

Historical ADR Calculation: Automatically computes the Average Daily Range based on the specified number of previous trading days (configurable from 1 to 20).

Real-Time Range Tracking: Monitors and displays the current day's live price range as it develops.

Percentage Used Metric: Shows the percentage of the historical ADR that the current day's range has already consumed, providing an immediate gauge of remaining volatility potential.

Remaining Range Projection: Visually highlights the potential upward and downward movement remaining to meet the average range, displayed as semi-transparent areas on the chart.

Daily Open Reference: Plots customisable vertical separation lines and horizontal price lines at the daily open to clearly anchor the current session's price action.

3. Visual Components & Analytical Insights

A fully configured Average Daily Range setup displays several key analytical components that work together to provide a comprehensive volatility overview.

3.1. Information Table

A highly customizable data table provides a concise summary of all critical metrics at a glance:

Historical Ranges: Displays the individual daily ranges for the selected lookback period.

ADR Value: The calculated average range.

Today's Range: The live, developing range for the current session.

% Used: A colour-coded percentage (turning orange upon exceeding 100% and red upon exceeding 150%) showing how much of the average volatility has been consumed.

3.2. Visual Range Projections

Remaining Range Zones: When the current day's range is below the historical average, semi-transparent zones extend from the current day's extreme high and low, illustrating the additional movement required to reach the ADR. This provides an instant visual cue for potential target zones.

Daily Open Markers: Clean, customisable lines mark the start of each trading day (vertical line) and the daily open price (horizontal line), helping to contextualise intraday price moves.

4. Input Parameters and Settings

4.1. General Settings

Lookback: Set the number of days used to calculate the Average Daily Range (1-20).

Set Alert: Configure alerts to be notified when the current day's range consumes a significant portion (e.g., 100% or more) of the historical ADR.

4.2. Table Customization

Visibility & Style: Toggle the table and historical data on/off. Fully customise the header and body colours, text colours, border style, and font sizes.

Placement & Orientation: Precisely position the table anywhere on the chart (Top/Bottom/Centre, Left/Right) and choose between Horizontal or Vertical layout to best suit your chart layout.

4.3. Visual Style Controls

Remaining Range: Toggle the projection zones on/off and customise their colour and transparency.

Daily Open Markers: Independently control the visibility, colour, style, and width of the daily separation line and the open price line.

5. Protected Logic & Original Design

The Average Daily Range indicator incorporates proprietary logic for efficiently tracking intraday extremes, managing historical data arrays, and dynamically rendering visual elements. The closed-source nature of this tool protects the author's original code structure and optimisation techniques, particularly the real-time area fill projection logic for the remaining daily range and the dynamic table management system. This ensures the indicator remains performant and reliable while being freely accessible to the entire TradingView community.

6. Disclaimer & Terms of Use

This indicator, titled Average Daily Range , has been independently developed by the author. The code and its structural logic are original and were written entirely from scratch to reflect a unique and efficient approach to volatility analysis. The internal mechanics were written from scratch and are not based on any publicly available script or third-party code.

This tool is provided solely for educational and informational purposes. It is not intended as financial advice, investment guidance, or a specific recommendation to buy or sell any financial instrument. The indicator is designed to assist with technical analysis based on volatility but does not guarantee accuracy or profitability.

Trading financial markets involves significant risk, including the possibility of loss of capital. By using this indicator, you acknowledge and accept that you are solely responsible for any decisions you make and for all trading outcomes. No part of this script should be considered a signal or assurance of success in the market.

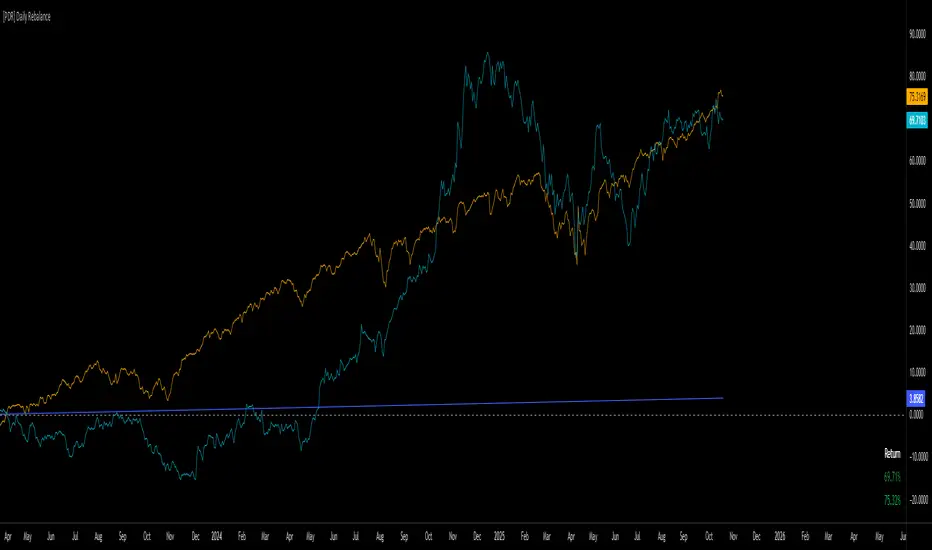

[PDR] Daily Rebalance█ OVERVIEW

This indicator is a powerful portfolio backtesting tool designed to simulate the performance of a static-weight, daily rebalancing strategy. It allows you to define a portfolio of up to 10 assets, set their target weights, and track its cumulative return against a user-defined benchmark and a risk-free rate.

The core of the script is its daily rebalancing logic, which calculates and logs every trade needed to bring the portfolio back to its target allocations at the close of each day. This provides a transparent and detailed view of how a static portfolio would have performed historically, including the impact of trading costs.

█ KEY FEATURES

Daily Rebalancing: Simulates a portfolio that is rebalanced at the close of every day to maintain target asset allocations.

Customizable Portfolio: Configure up to 10 different assets with specific weights. If all weights are left at 0, the script automatically creates an equal-weight portfolio from the selected assets.

Performance Comparison: Plots the portfolio's equity curve against a user-defined benchmark (e.g., SET:SET50 ) and a risk-free return, allowing for easy relative performance analysis.

Realistic Simulation: Accounts for trading costs like broker commission and minimum lot sizes for more accurate and grounded backtesting results.

Detailed Performance Metrics: An on-chart table displays real-time statistics, including Current Drawdown, Max Drawdown, and Total Return for both your portfolio and the benchmark.

Trade-by-Trade Logs: For full transparency, every rebalancing trade (BUY/SELL), including shares, price, notional value, and fees, is logged in the Pine Logs panel.

█ HOW TO USE

**Apply to a Daily Chart:** This script is designed to work exclusively on the daily ( 1D ) timeframe. Applying it to any other timeframe will result in a runtime error.

**Configure Settings:** Open the indicator's settings. Set your `Initial Capital`, `Start Time`, and the `Benchmark` symbol you wish to compare against.

**Define Your Assets:** In the 'Assets' group, check the box to enable each asset you want to include, select the symbol, and define its target `Weight (%)`.

**Set Trading Costs:** Adjust the `Broker Commission (%)` and `Minimal Buyable Lot` to match your expected trading conditions.

**Analyze the Results:** The performance curves are plotted in the indicator pane below your main chart. The key metrics table is displayed on the bottom-right of your chart.

**View Rebalancing Trades:** This is a crucial step for understanding the simulation. To see the detailed daily trades, you **must** open the **Pine Logs**. You can find this panel at the bottom of your TradingView window, next to the "Pine Editor" and "Strategy Tester" tabs. The logs provide a complete breakdown of every rebalancing action.

█ DISCLAIMER

This is a backtesting and simulation tool, not a trading signal generator. Its purpose is for research and performance analysis. Past performance is not indicative of future results. Always conduct your own research before making any investment decisions.

ATR DAILY PROGRESSION)Indicator: ATR Daily Progression — Final Compact Edition

1. Indicator Objective

The ATR Daily Progression indicator measures the progression of intraday volatility as a percentage of the daily Average True Range (ATR).

It provides a quick visual overview of whether the market has reached or exceeded its average daily range of movement.

This helps traders avoid entering low-probability continuation trades once the day’s ATR is already completed.

2. Visual Presentation

Horizontal bar ranging from 0% to 150% of the ATR.

Green color up to 100%, then red beyond that point.

Main ticks: 0, 25, 50, 75, 90, 100, and 150%.

Full-height white vertical lines at 0%, 100%, and 150%.

A floating badge displaying the current ATR completion percentage, always visible.

Compact Height mode enabled by default for optimal visual integration.

3. Key Features

Function Description

Precise alignment The transition from green to red occurs exactly after the 100% tick.

Audio & visual alerts Triggered at 75%, 90%, 100%, and 150%.

Session flash effects The filled bar blinks when the ATR is reached (100%) or exceeded (150%).

Dynamic badge Displays the current ATR %, green before 100%, red after.

Compact layout Three-line table format for better chart integration.

4. Recommended Settings

ATR Length (Daily): 14

Bar width (steps): 32–40 (depending on chart size)

Always green below 100%: enabled

Show floating % badge: enabled

Compact Height: enabled by default

Flash at 75% and 90%: enabled

Flash at 100% and 150%: enabled

5. Strategic Use

The ATR Done Today is a visual discipline tool designed to help traders:

Identify when the market has likely completed its daily move.

Avoid late-session counter-trend trades.

Visualize volatility compression or expansion.

Determine optimal times to take profits or pause trading.

Anchored VWAP Close-Above Alert (Daily)This indicator is a daily anchored VWAP (Volume-Weighted Average Price) tracker that alerts you when price closes above a key pivot line you’ve defined — either dynamically (anchored VWAP from a date like 9/5) or statically (a fixed level like 126.65).

Here’s how each piece works:

1. The anchor date

You give it a date — say September 5, 2025. The script starts calculating VWAP from that day forward. That line represents the average price buyers and sellers have transacted at since that anchor. It’s a kind of “fair-value line” for that period.

2. The logic

Every bar after that date, it adds up (price × volume) and divides by total volume — giving a running VWAP from that starting point. You can instead lock it to a flat number (like 126.65) if you don’t want it recalculating.

3. The alert trigger

Once per day — when the daily candle closes — it checks:

“Did price close above my watched line?”

If yes, it fires an alert (and can draw a label) to tell you that the day’s candle reclaimed that level.

4. The why

That kind of move — a daily close reclaiming a major anchored VWAP — often signals a shift in sentiment or trend strength. Traders watch it to confirm rebounds or invalidations of downside moves.

So in your context:

You anchored to 9/5 (the downside pivot).

You want to know if price closes back above that VWAP (~126.65).

If it does, the alert lights up — confirming the “reclaim” you mentioned in your note.

It’s basically your guard dog for the daily close reclaim.

Crash Survival Indicator (SPX, Weekly/Daily)Short description

SPX-focused risk context tool using 30WMA/ATR/ADX and distance to 30WMA, with optional Hindenburg-Omen breadth and macro add-ons. Weekly is primary; Daily provides early-warning. Educational only.

Full description (English first)

What it is

Crash Survival Indicator (CSI) is a rules-based risk context indicator for the S&P 500 index (SPX). It helps keep decisions data-driven during stress by combining four weekly conditions into a weighted risk score and presenting them in a readable dashboard. Optional breadth (Hindenburg Omen cluster proxy) and macro add-ons give additional context. This is not a buy/sell system.

Why it’s original and useful

Weekly core with confirmation: Four classic conditions (30WMA regime, ATR(14) trend, ADX(14) > 20 & rising, and % distance from 30WMA) feed a 0–100 score. A 2-of-3 gate (WMA down / ATR up / ADX>20↑) must confirm before “Danger,” reducing false spikes.

Daily Early-Warning: A separate daily preview flags conditions approaching the Danger threshold (with a streak filter). It’s a heads-up only, not a timeframe switch.

Scope control to avoid confusion: Signals (labels/alerts) are restricted to SPX on Weekly/Daily by design. The dashboard can be shown SPX-only or on all symbols (configurable).

Clarity for all users: Beginner card view (plain badges) and Pro table view (detailed chips) improve readability without hiding logic.

How it works (mechanics)

Weekly core (primary frame)

30WMA regime: price vs 30-week WMA; IN/OUT labels on crosses.

ATR(14): rising ATR counts as volatility stress.

ADX(14): risk weight when ADX > 20 and rising.

Distance to 30WMA: % deviation flags potential overheat.

Scoring & thresholds: Weighted sum → Caution ≥ 40, Danger ≥ 60 (defaults). Danger also requires the 2-of-3 gate above.

Daily Early-Warning: Uses daily versions of the same ideas to detect near-Danger conditions with a streak requirement (heads-up only).

Optional breadth (Hindenburg Omen proxy): Elevated new highs and new lows while the NYSE Composite is above its 50DMA, with deteriorating breadth momentum; requires cluster confirmation to reduce noise.

Optional macro add-ons: VIX regime, DXY strength, credit stress (HYG/LQD vs MA), and TNX trend each add adjustable weights.

Inputs (overview)

Scope & Mode: SPX primary/alt tickers; signal restriction to SPX + Weekly/Daily; dashboard visibility (SPX-only vs all symbols); Beginner or Pro display.

Label Policy: Weekly-only / Weekly-core + Daily-early (default) / All (W/D); lookback windows and minimum bar gaps to prevent clutter.

Scoring: Weights for 30WMA down, ATR up, ADX>20↑, Overheat; Caution/Danger thresholds; Overheat % (distance).

Hindenburg Omen (optional): NYSE Composite and High/Low/AD series; cluster requirement.

Macro add-ons (optional): Symbols + weights for VIX, DXY, HYG, LQD, TNX.

Early Warning (Daily): Near-Danger buffer and streak length.

Visuals & Alerts: Background shading, labels on/off, font size, dashboard position, runtime

alerts.

Alerts (contextual; not trade signals)

OUT — 30WMA Down Break (Weekly)

IN — 30WMA Reclaim (Weekly)

Risk ≥ Danger + 2-of-3 Gate

Hindenburg Omen Cluster detected

Early Warning (Daily near Danger, streak)

Alerts provide context only. They are not buy/sell instructions.

Intended use and limitations

Use the Weekly panel for decisions; treat Daily Early-Warning as a heads-up.

Best used as risk framing alongside your own process (position sizing, liquidity, event risk).

Breadth/macro inputs depend on your data source; if unavailable, keep add-ons off.

No forward-looking data or lookahead; designed to avoid repainting.

Disclaimer

For educational purposes only. Not financial advice, not an investment recommendation, and not a solicitation to buy or sell any security. Past performance does not guarantee future results. Users are solely responsible for their decisions and regulatory compliance.

Optional Korean addendum (append after English)

한국어 안내 요약: 본 지표는 위기 상황에서 감정보다 데이터를 우선할 수 있도록 리스크 맥락을 제공합니다. 주봉이 핵심, 일봉은 조기경보(Heads-up)이며, 매수/매도 신호가 아닙니다. 심프님의 프로토타입 철학을 살리되 SPX 한정 신호, 라벨/알림 정책, 선택형 오멘/매크로 기능, 초보/프로 대시보드 등 가독성을 개선했습니다. 투자 판단과 책임은 전적으로 사용자에게 있습니다.

Privacy & format

Visibility: Public

Source: Protected (no source disclosure), compliant with Publishing Rules

Language: English title & description first; Korean addendum optional

Screenshot guidance (for your gallery)

Weekly SPX showing dashboard at “Danger” with an OUT label.

Weekly SPX with Hindenburg Omen Cluster label and shaded background.

Daily SPX with Early-Warning label as weekly approaches Danger.

Beginner vs Pro dashboard comparison on SPX.

Author certification (paste if needed)

I certify this publication contains no promotions, links, or solicitations, complies with TradingView House Rules and Script Publishing Rules, uses Pine v5, and is intended solely for educational purposes with no performance claims.