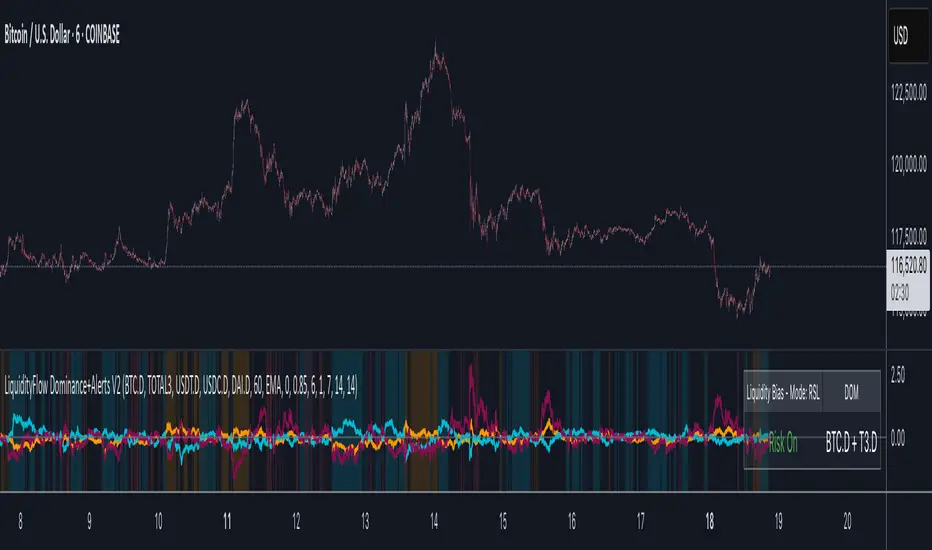

LiquidityFlow Dominance+Alerts (btc.d, T3, Stables)LiquidityFlow Dominance+Alerts: Overview & Usage Guide

Overview

The LiquidityFlow Dominance+Alerts indicator provides a dynamic view of liquidity flow across Bitcoin, Altcoins, and Stablecoins, helping track liquidity shifts and identify market sentiment. By integrating moving averages, custom alerts, and thresholds for extreme outliers, this indicator helps to anticipate bullish and bearish shifts in liquidity and alert market tops and bottoms.

Key features include:

1. Liquidity Flow Monitoring : Track liquidity flow across Bitcoin (BTC), Altcoins (TOTAL3), and Stablecoins (USDT, USDC, DAI).

2. Custom Alerts : Set alerts for key liquidity shifts and extreme conditions in Stablecoin dominance, both with static and moving average (MA)-based calculations.

3. Moving Averages : Use Simple, Exponential, or Weighted Moving Averages to smooth out market data for more reliable signals.

4. Outlier Detection : Identify potential tops and bottoms using thresholds for Stablecoin dominance, with alerts for extreme movements.

Functionality

Data Inputs and Key Metrics

- Symbols Monitored:

- Bitcoin Dominance (BTC.D)

- Altcoin Market Cap (TOTAL3)

- Stablecoins (USDT.D, USDC.D, DAI.D)

- Liquidity Flow Conditions:

- Track percentage changes in dominance across sectors to detect liquidity flow into Bitcoin, Altcoins, or Stablecoins.

- Custom Metrics:

- Liquidity Flow Index: BTC Dominance minus Stablecoin Dominance.

- Liquidity Flow Ratio: BTC Dominance divided by the combined dominance of Stablecoins and Altcoins.

Moving Average Integration

- Select from SMA, EMA, or WMA to apply moving averages to the dominance metrics. Moving averages help smooth out short-term volatility and provide more consistent signals.

- Moving averages are applied to each sector (BTC, Altcoins, and Stablecoins) and compared to their previous period values to determine shifts in liquidity.

Alerts and Thresholds

- % Change Lookback Period: Adjust the lookback period to align with the timeframe of your chart. Shorter timeframes may require a lower lookback period, while higher timeframes may benefit from longer periods.

- Stables Bull/Bear % for Alerts: Set a threshold for when Stablecoin dominance becomes a bullish or bearish signal relative to BTC and Altcoins. A higher threshold may be used in volatile markets to filter out noise.

- Extreme Outliers Detection: Use the **Stables Up/Down Extreme Threshold** to identify potential market tops or bottoms when Stablecoin dominance deviates significantly from historical trends. The **Extreme Lookback Period** controls the time window for detecting these anomalies.

How to Use the Indicator

Adjusting the % Change Lookback Period

- The `% Change Lookback Period` should be adjusted based on your chart’s timeframe. For example, a shorter period (e.g., 7) works well for intraday charts, while longer periods (e.g., 14) might be more suitable for daily or weekly charts.

Setting Thresholds for Alerts

- Stables Bull/Bear % for Alerts: Adjust this setting to define when Stablecoin dominance triggers bullish or bearish alerts. A value like 1% could be a good starting point for most market conditions but can be fine-tuned based on volatility.

- Extreme Lookback Period: Define the lookback period for detecting extreme moves in Stablecoin dominance. This will help identify major tops and bottoms in the market. For shorter-term trades, consider using a shorter extreme lookback (e.g., 7-10 periods).

Alerts for Liquidity Shifts

- The indicator supports alerts for key liquidity shifts, which are useful for staying ahead of market movements. Alerts can be set to notify you when liquidity moves into:

- Bitcoin: Indicating a potential bullish trend for Bitcoin.

- Altcoins: Signaling altcoins are bullish.

- Stablecoins: Suggesting a risk-off environment or market correction.

Extreme Alerts for Stables

- Extreme Up/Down Alerts: These are triggered when Stablecoin dominance crosses extreme thresholds. For example, if Stablecoin dominance rises more than 14% over a set period, it could signal a market top, while a significant drop could indicate a market bottom.

Moving Average Calculations

- In addition to static percentage changes, moving averages can be applied to smooth out dominance values. The type and length of the moving average can be customized:

- SMA (Simple Moving Average): Best for smoothing out volatility in a linear way.

- EMA (Exponential Moving Average): More responsive to recent data, making it useful in faster markets.

- WMA (Weighted Moving Average): Emphasizes more recent data, but less reactive than the EMA.

Additional Usage Tips:

- Background Colors: The indicator visually highlights the dominant liquidity flow:

- Orange: Liquidity is shifting toward Bitcoin.

- Aqua: Liquidity is flowing into Altcoins.

- Red: Liquidity is moving into Stablecoins.

Pine Script® 인디케이터