Relative Falling three Methods IndicatorAbstract

This script measure the related speed between rising and falling.

This script can replace binary Falling Three Methods detector and, report continuous value and estimate potential trend direction.

My suggestion of using this script is combining it with trading emotion.

Introduction

Falling Three Methods (F3M) is a candlestick pattern.

Many trading courses say traders can regard it as predicting falling will continue.

However, it is not easy to see perfect Falling Three Methods pattern from charts.

Therefore, we need an alternative method to measure it.

We can use the observation that falling is faster than rising during those time.

When falling is faster than rising, some long ( buy , call , higher , upper ) position owners may worry the price will fall very much suddenly.

When rising is faster than falling, some traders may worry they may miss buy opportunities.

Computing Related Falling Three Methods Indicator

(1) The value of rising and falling

In this script, open price is replaced with previous close price.

If the previous price is equal to the close price, than both rising and falling are equal to high-low.

If the previous price is lower than the close price, than the falling value becomes smaller, high-close+previous-low.

If the previous price is higher than the close price, than the rising value becomes smaller, high-previous+close-low.

(2) Area of value (aov)

Area of value is equal to highest-lowest. The previous close price is included.

(3) Compute weight and filter noise

We need a threshold for the noise filter. The default setting is aov/length, where length means how many days are counted.

When a rising or falling value <= threshold, it is not counted.

When a rising or falling value > threshold, the counted value = original value - threshold

and its weight = min ( counted value , threshold )

(4) compute speed

Rising speed = sum ( counted rising value ) / sum ( rising weight )

Falling speed = sum ( counted falling value ) / sum ( falling weight )

(5) Final result

Final result = Rising speed / ( Rising speed + Falling speed ) * 100 - 50

I move the middle level to 0 because 0 axis is always visible unless you cannot see negative values or you cannot see positive values.

Parameters

Length : how many days are counted. The default value is 16 just because 16=4*4, using binary characteristic.

Multi : the multiplier of noise threshold. Threshold applied = default threshold * multi

src : current not used

Conclusion

Related Falling Three Methods Indicator can measure the related speed between rising and falling.

I hope this indicator can help us to evaluate the possibility of trend continue or reversal and potential breakout direction.

After all, we care how trading emotion control the price movement and therefore we can take advantage to it.

Reference

How to trade with Falling Three Methods pattern

How to trade with Related Strength Indicator

스크립트에서 "binary"에 대해 찾기

4 in 1 Stoch Indicators as used by HG (Stoch, SRSIx2, DMIStoch)By using this indicator you can better view the Stoch indicators used by this strategy which are:

- Stochastic (14,3,3)

- Stochastic RSI (14,14,3,3)

- Stochastic RSI (6,6,3,3)

- DMI Stochastic

This is best used alongside:

- Evan Cabral binary strategy 2

- Binary with Temito

The analisis is:

- When all lines in the indicator are above or below the overbough/oversold lines

- When the bollinger bands are broken

- A support or resistance is reached

That means a change of Trend.

Edge-Preserving FilterIntroduction

Edge-preserving smoothing is often used in image processing in order to preserve edge information while filtering the remaining signal. I introduce two concepts in this indicator, edge preservation and an adaptive cumulative average allowing for fast edge-signal transition with period increase over time. This filter have nothing to do with classic filters for image processing, those filters use kernels convolution and are most of the time in a spatial domain.

Edge Detection Method

We want to minimize smoothing when an edge is detected, so our first goal is to detect an edge. An edge will be considered as being a peak or a valley, if you recall there is one of my indicator who aim to detect peaks and valley (reference at the bottom of the post) , since this estimation return binary outputs we will use it to tell our filter when to stop filtering.

Filtering Increase By Using Multi Steps Cumulative Average

The edge detection is a binary output, using a exponential smoothing could be possible and certainly more efficient but i wanted instead to try using a cumulative average approach because it smooth more and is a bit more original to use an adaptive architecture using something else than exponential averaging. A cumulative average is defined as the sum of the price and the previous value of the cumulative average and then this result is divided by n with n = number of data points. You could say that a cumulative average is a moving average with a linear increasing period.

So lets call CMA our cumulative average and n our divisor. When an edge is detected CMA = close price and n = 1 , else n is equal to previous n+1 and the CMA act as a normal cumulative average by summing its previous values with the price and dividing the sum by n until a new edge is detected, so there is a "no filtering state" and a "filtering state" with linear period increase transition, this is why its multi-steps.

The Filter

The filter have two parameters, a length parameter and a smooth parameter, length refer to the edge detection sensitivity, small values will detect short terms edges while higher values will detect more long terms edges. Smooth is directly related to the edge detection method, high values of smooth can avoid the detection of some edges.

smooth = 200

smooth = 50

smooth = 3

Conclusion

Preserving the price edges can be useful when it come to allow for reactivity during important price points, such filter can help with moving average crossover methods or can be used as a source for other indicators making those directly dependent of the edge detection.

Rsi with a period of 200 and our filter as source, will cross triggers line when an edge is detected

Feel free to share suggestions ! Thanks for reading !

References

Peak/Valley estimator used for the detection of edges in price.

Momentum Strategy, rev.2This is a revised version of the Momentum strategy listed in the built-ins.

For more information check out this resource:

www.forexstrategiesresources.com

EMA Strong Trend MarketUse this indicator with my binary blast v2 indicator for getting good binary signals if combine. Don't call or put option when this signal comes in a bar while using previous indicator.

Heiken Ashi zero lag EMA v1.1 by JustUncleLI originally wrote this script earlier this year for my own use. This released version is an updated version of my original idea based on more recent script ideas. As always with my Alert scripts please do not trade the CALL/PUT indicators blindly, always analyse each position carefully. Always test indicator in DEMO mode first to see if it profitable for your trading style.

DESCRIPTION:

This Alert indicator utilizes the Heiken Ashi with non lag EMA was a scalping and intraday trading system

that has been adapted also for trading with binary options high/low. There is also included

filtering on MACD direction and trend direction as indicated by two MA: smoothed MA(11) and EMA(89).

The the Heiken Ashi candles are great as price action trending indicator, they shows smooth strong

and clear price fluctuations.

Financial Markets: any.

Optimsed settings for 1 min, 5 min and 15 min Time Frame;

Expiry time for Binary options High/Low 3-6 candles.

Indicators used in calculations:

- Exponential moving average, period 89

- Smoothed moving average, period 11

- Non lag EMA, period 20

- MACD 2 colour (13,26,9)

Generate Alerts use the following Trading Rules

Heiken Ashi with non lag dot

Trade only in direction of the trend.

UP trend moving average 11 period is above Exponential moving average 89 period,

Doun trend moving average 11 period is below Exponential moving average 89 period,

CALL Arrow appears when:

Trend UP SMA11>EMA89 (optionally disabled),

Non lag MA blue dot and blue background.

Heike ashi green color.

MACD 2 Colour histogram green bars (optional disabled).

PUT Arrow appears when:

Trend UP SMA11

Bollinger Bands NEW

var tradingview_embed_options = {};

tradingview_embed_options.width = 640;

tradingview_embed_options.height = 400;

tradingview_embed_options.chart = 's48QJlfi';

new TradingView.chart(tradingview_embed_options);

Vdub Binary Options SniperVX v1 by vdubus on TradingView.com

MLActivationFunctionsLibrary "MLActivationFunctions"

Activation functions for Neural networks.

binary_step(value) Basic threshold output classifier to activate/deactivate neuron.

Parameters:

value : float, value to process.

Returns: float

linear(value) Input is the same as output.

Parameters:

value : float, value to process.

Returns: float

sigmoid(value) Sigmoid or logistic function.

Parameters:

value : float, value to process.

Returns: float

sigmoid_derivative(value) Derivative of sigmoid function.

Parameters:

value : float, value to process.

Returns: float

tanh(value) Hyperbolic tangent function.

Parameters:

value : float, value to process.

Returns: float

tanh_derivative(value) Hyperbolic tangent function derivative.

Parameters:

value : float, value to process.

Returns: float

relu(value) Rectified linear unit (RELU) function.

Parameters:

value : float, value to process.

Returns: float

relu_derivative(value) RELU function derivative.

Parameters:

value : float, value to process.

Returns: float

leaky_relu(value) Leaky RELU function.

Parameters:

value : float, value to process.

Returns: float

leaky_relu_derivative(value) Leaky RELU function derivative.

Parameters:

value : float, value to process.

Returns: float

relu6(value) RELU-6 function.

Parameters:

value : float, value to process.

Returns: float

softmax(value) Softmax function.

Parameters:

value : float array, values to process.

Returns: float

softplus(value) Softplus function.

Parameters:

value : float, value to process.

Returns: float

softsign(value) Softsign function.

Parameters:

value : float, value to process.

Returns: float

elu(value, alpha) Exponential Linear Unit (ELU) function.

Parameters:

value : float, value to process.

alpha : float, default=1.0, predefined constant, controls the value to which an ELU saturates for negative net inputs. .

Returns: float

selu(value, alpha, scale) Scaled Exponential Linear Unit (SELU) function.

Parameters:

value : float, value to process.

alpha : float, default=1.67326324, predefined constant, controls the value to which an SELU saturates for negative net inputs. .

scale : float, default=1.05070098, predefined constant.

Returns: float

exponential(value) Pointer to math.exp() function.

Parameters:

value : float, value to process.

Returns: float

function(name, value, alpha, scale) Activation function.

Parameters:

name : string, name of activation function.

value : float, value to process.

alpha : float, default=na, if required.

scale : float, default=na, if required.

Returns: float

derivative(name, value, alpha, scale) Derivative Activation function.

Parameters:

name : string, name of activation function.

value : float, value to process.

alpha : float, default=na, if required.

scale : float, default=na, if required.

Returns: float

Whole NumbersThis is a simple indicator for the whole numbers.

It breaks down every pair for 10 pips.

Its also simple and nice to use

Stochastic with Outlier Labels/MTFTL;DR This indicator is an update to a simple stochastic ('Stoch_MTF' by binarytrader666) that provides a novel outlier highlighting feature

Improvements on stochastic:

1. Novel outlier highlighting that points out crosses that are the Nth consecutive cross or greater.

2. Allowing for multiple timeframes to be shown on the same chart

3. Highlighting/Labelling crosses and providing labels for alerts

A cross of the stochastics in the high or low zones establishes a trend. Successive crosses in the same region seem to indicate a continuation of that trend. The outlier functionality here provides a signal for when X number of crosses have been in the same trend, signaling further strength of that signal.

I also provided the necessary code for converting this to a strategy if you so wish at the bottom.

Linear Regression Trend Channel with Entries & AlertsPlease Use this Indicator If you understand the risk posed by linear regression trend channel

Features

Provides trend channel (best value for period is 40 on 5 minute timeframe

Provides BUY/SELL entries based on current channel

Provides custom color for channel

Best used with MattyPips strategy indicators

Risks : Please note, this script is the likes of Bollinger bands and poses a risk of falling in a trend range.

Entries may keep running on the same direction while the market is moving.

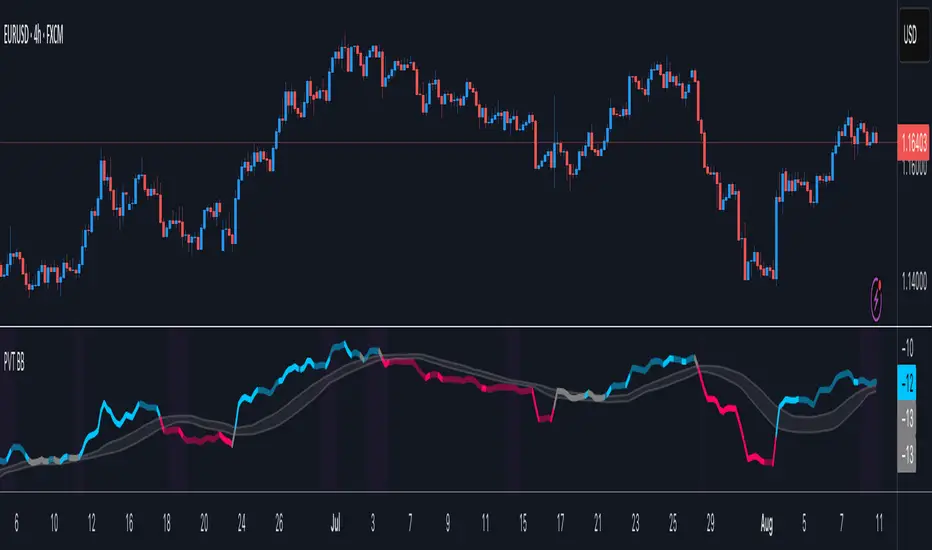

Price Volume Trend BBHey guys,

Ive been thinking about Price Volume Trend for a while and tried adding different moving averages to it, but seems its not as binary.

Therefore adding the bollinger bands as a no-trade-zone made it alot better. Indicator is pretty basic at the moment since I just implemented the idea but im planning to do some add-ons later on to make it easier to read.

Will keep you updated!

VEMA Band_v2 - 'Centre of GravityConcept taken from the MT4 indicator 'Centre of Gravity'except this one doesn't repaint.

Modified / BinaryPro 3 / Permanent Marker

Ema configuration instead of sma & centralised.

Vdub_Tetris_Stoch_V1Vdub_Tetris_Stoch_V1

A combination lower based indicators based on the period channel indicator Vdub_Tetris_V2

Blue line is more reactive fast moving, Red line in more accurate to highs / Lows with divergence.- Still testing

Code title error

Change % = Over Bought / Over Sold

Vdub Tetris_V2

Vdubus BinaryPro 2 /Tops&Bottoms

StochDM

SENTINEL CORE by Pipsomnian🛡️ Sentinel Core — Learning Mode (Structure & Probability Engine)

by Pipsomnian

Sentinel Core is the core structure and probability framework within the Sentinel ecosystem.

It is designed to help traders move beyond binary signals and learn how to grade market environments based on structure, momentum, and session quality.

This tool does not predict price.

It evaluates context.

🎯 What Sentinel Core Is

Sentinel Core is an EMA-structured learning and decision-grading indicator built to train:

• Trend alignment

• Pullback behavior

• Market structure continuation

• Session discipline (London & New York)

• Probability stacking

Instead of asking “Is there a signal?”,

Sentinel Core trains you to ask:

“How strong is this setup?”

🧠 The Scoring Concept

Each potential setup is evaluated using multiple structural components:

• EMA trend alignment

• Pullback to value

• Strong candle confirmation

• Market structure continuation

• Active trading session

The result is a setup quality grade:

• A+ → Full structural alignment

• B → Strong but incomplete alignment

Lower-quality environments are intentionally ignored.

This encourages patience, selectivity, and discipline.

🟢 Who Sentinel Core Is For

Sentinel Core is designed for traders who:

• Already understand basic EMA structure

• Want fewer, higher-quality setups

• Trade session-based markets (especially Gold)

• Value discipline over frequency

• Want to develop judgment, not dependency

🚫 What Sentinel Core Is NOT

Sentinel Core is not:

• A signal service

• An automated strategy

• A promise of profitability

• A replacement for risk management

• A shortcut to consistency

Execution, risk control, and psychology remain your responsibility.

⏱️ Recommended Use

• Timeframe: 5-Minute

• Markets: XAUUSD (Gold), major FX, liquid indices

• Sessions: London & New York

EMAs are used for structure and context, not prediction.

🧭 Position in the Sentinel Framework

• Sentinel Lite — Learn structure & discipline

• Sentinel Core — Grade probability & judgment

• Sentinel A+ — Refine timing & precision

• Sentinel Gold Standard — Execute with control

⚠️ Educational use only. No financial advice.

— Pipsomnian

Tanh Clamped Momentum Oscillator [Alpha Extract]A sophisticated momentum measurement system that combines dual EMA trend analysis with volatility-weighted pressure calculations, applying hyperbolic tangent normalization for bounded oscillator output with adaptive signal generation. Utilizing ATR-based volatility regime detection and candle pressure metrics, this indicator delivers institutional-grade momentum assessment with multi-tiered band structure and pulse-based envelope visualization. The system's tanh clamping methodology prevents extreme outliers while maintaining sensitivity to genuine momentum shifts, combined with histogram divergence detection and comprehensive alert framework for high-probability reversal and continuation signals.

🔶 Advanced Dual-Component Momentum Engine

Implements hybrid calculation combining EMA trend differential with candle pressure analysis, weighted by volatility regime assessment for context-aware momentum measurement. The system calculates fast and slow EMA difference normalized by ATR, measures intrabar pressure as close-open relative to range, applies volatility-based weighting between trend and pressure components, and produces composite raw momentum capturing both directional bias and internal candle dynamics.

// Core Momentum Framework

EMA_Fast = ta.ema(src, Fast_Length)

EMA_Slow = ta.ema(src, Slow_Length)

Trend = EMA_Fast - EMA_Slow

// Volatility Regime Detection

ATR_Short = ta.atr(ATR_Length)

ATR_Long = ta.atr(ATR_Length * 2)

Vol_Ratio = ATR_Short / ATR_Long

Vol_Weight = clamp((Vol_Ratio - 0.5) / 1.0, 0, 1)

// Pressure Component

Pressure = (close - open) / (high - low)

// Composite Momentum

Raw = Trend_Normalized * Vol_Weight + Pressure_Scaled * (1 - Vol_Weight)

🔶 Hyperbolic Tangent Normalization Framework

Features sophisticated tanh transformation that clamps raw momentum into bounded range while preserving proportional sensitivity across varying market conditions. The system applies safe exponential calculations with input capping to prevent overflow, computes hyperbolic tangent to compress extreme values while maintaining linearity near zero, and scales output by configurable factor creating oscillator with enhanced dynamic range and reduced outlier distortion.

// Tanh Clamping Logic

tanh(x) =>

x_clamped = clamp(x, -5.0, 5.0)

e = exp(2.0 * x_clamped)

(e - 1.0) / (e + 1.0)

Oscillator = tanh(Smoothed_Momentum / Clamp_Factor) * Scale

🔶 Volatility Regime Weighting System

Implements intelligent volatility assessment comparing short-term and long-term ATR to determine market regime, dynamically adjusting weight between trend and pressure components. The system calculates ATR ratio, normalizes to 0-1 range, and uses this weight factor to emphasize trend component during high-volatility regimes and pressure component during low-volatility consolidations, creating adaptive momentum sensitive to market microstructure.

🔶 Multi-Tiered Band Architecture

Provides comprehensive threshold structure with soft, hard, and maximum bands marking progressive momentum extremes for graduated overbought/oversold assessment. The system establishes configurable levels at soft zones (initial caution), hard zones (strong extreme), and maximum zones (critical overextension) with visual differentiation through line styles and background highlighting, enabling nuanced interpretation beyond binary extreme detection.

🔶 Pulse Envelope Visualization

Features dynamic envelope bands calculated from exponential moving average of absolute oscillator value, creating adaptive boundary that expands during momentum acceleration and contracts during deceleration. The system applies configurable length and width multiplier to pulse calculation, fills area between positive and negative pulse bounds with gradient coloring matching oscillator direction, providing visual context for momentum magnitude relative to recent activity.

🔶 Signal Line Integration Framework

Implements dual-mode signal line supporting both EMA and SMA smoothing of primary oscillator for crossover-based swing detection. The system calculates configurable-length moving average, generates histogram differential between oscillator and signal, applies additional smoothing to histogram for noise reduction, and uses crossovers/crossunders as momentum swing indicators distinguishing bullish and bearish momentum shifts.

🔶 Histogram Divergence Display

Creates column-style histogram visualization showing oscillator-signal differential with intensity-based coloring reflecting momentum acceleration or deceleration. The system plots histogram bars in bright colors when expanding (accelerating momentum) and faded colors when contracting (decelerating momentum), enabling instant visual identification of momentum divergences and convergences without numerical analysis.

🔶 Advanced Reversion Signal Logic

Generates overbought/oversold signals requiring both signal line crossover and extreme threshold breach for high-conviction reversal identification. The system triggers oversold when oscillator crosses above signal while below negative reversion level, triggers overbought when crossing below signal while above positive reversion level, and plots small circle markers at signal locations for clear visual confirmation of setup conditions.

🔶 Comprehensive Alert Framework

Provides six distinct alert conditions covering overbought/oversold reversions, midline trend changes, and oscillator-signal swings with configurable notification preferences. The system includes alerts for extreme reversions (OB/OS), zero-line crossovers (trend changes), and signal line crossovers (momentum swings), enabling traders to monitor critical oscillator events across multiple signal types without constant chart observation.

🔶 Adaptive Bar Coloring System

Implements four coloring modes including midline cross (trend direction), extremities (threshold breach), reversions (OB/OS signals), and slope (oscillator vs signal) for customizable visual integration. The system applies selected color scheme to candles providing chart-level momentum feedback, with option to disable coloring for minimal visual interference while maintaining oscillator pane analysis.

🔶 Performance Optimization Architecture

Utilizes efficient tanh calculation with safe clamping, streamlined EMA computations, and optimized ATR ratio processing for smooth real-time updates. The system includes intelligent null handling, minimal recalculation overhead through smart smoothing application, and configurable display toggles allowing users to disable unused visual elements for enhanced performance during extended historical analysis.

🔶 Why Choose Tanh-Clamped Momentum Oscillator ?

This indicator delivers sophisticated momentum analysis through hybrid trend-pressure calculation with volatility-adaptive weighting and hyperbolic tangent normalization. Unlike traditional momentum oscillators susceptible to extreme outlier distortion, the tanh clamping ensures bounded output while preserving sensitivity to genuine momentum shifts. The system's dual-component architecture combining directional trend with intrabar pressure, weighted by volatility regime assessment, creates context-aware momentum measurement that adapts to market microstructure. The multi-tiered band structure, pulse envelope visualization, and comprehensive signal framework make it essential for traders seeking nuanced momentum analysis with graduated extreme detection and high-probability reversal signals across cryptocurrency, forex, and equity markets.

ST | TTM SqueezeThis is a minimalist implementation of the classic "Squeeze" setup, designed to declutter your chart. Instead of complex histograms, this indicator focuses solely on the binary state of volatility compression.

How it works: It identifies periods where volatility contracts significantly, often preceding explosive moves.

TPOSmartMoneyLibLibrary "TPOSmartMoneyLib"

Library for TPO (Time Price Opportunity) and Smart Money concepts including session management, PDH/PDL detection, sweeping logic, and volume profile utilities

f_price_to_tick(p)

Convert price to tick

Parameters:

p (float) : Price value

Returns: Tick value

f_tick_to_row(t, row_ticks_in)

Convert tick to row

Parameters:

t (int) : Tick value

row_ticks_in (int) : Number of ticks per row

Returns: Row index

f_row_to_price(row, row_ticks_in)

Convert row to price (midpoint)

Parameters:

row (int) : Row index

row_ticks_in (int) : Number of ticks per row

Returns: Price at row midpoint

f_calc_row_ticks(natr_ref, row_gran_mult)

Calculate dynamic row size based on normalized ATR

Parameters:

natr_ref (float) : Daily normalized ATR reference value

row_gran_mult (float) : Row granularity multiplier

Returns: Number of ticks per row

f_more_transp_pct(c, pct)

Increase color transparency by percentage

Parameters:

c (color) : Input color

pct (float) : Percentage to increase transparency (0.0 to 1.0)

Returns: Color with increased transparency

f_dom_color(dom, buy_col, sell_col, gamma, transp_weak, transp_strong)

Calculate dominance color based on buy/sell ratio

Parameters:

dom (float) : Dominance ratio (-1 to 1, negative = sell, positive = buy)

buy_col (color) : Buy dominant color

sell_col (color) : Sell dominant color

gamma (float) : Gamma correction for color intensity

transp_weak (int) : Transparency for weak dominance

transp_strong (int) : Transparency for strong dominance

Returns: Blended color

f_sess_part(sess_str, get_start)

Parse session string to get start or end time

Parameters:

sess_str (string) : Session string in format "HHMM-HHMM"

get_start (bool) : True to get start time, false to get end time

Returns: Time string in HHMM format

f_hhmm_to_h(hhmm)

Convert HHMM string to hours

Parameters:

hhmm (string) : Time string in HHMM format

Returns: Hours (0-23)

f_hhmm_to_m(hhmm)

Convert HHMM string to minutes

Parameters:

hhmm (string) : Time string in HHMM format

Returns: Minutes (0-59)

f_prev_day_window_bounds(today_day_rth, win_start, win_end, session_tz)

Calculate previous day window bounds

Parameters:

today_day_rth (int) : Today's RTH start timestamp

win_start (string) : Window start time in HHMM format

win_end (string) : Window end time in HHMM format

session_tz (string) : Session timezone

Returns: Tuple of

f_default_session_colors()

Get default session colors

Returns: Array of 4 colors

f_session_names()

Get session names

Returns: Array of 4 session names

f_process_hl(arr, rng, keep_bars, lock_to_live)

Process high/low lines with sweeping detection

Parameters:

arr (array) : Array of HLLine objects

rng (float) : Price range for visibility filtering

keep_bars (int) : Maximum bars to keep lines

lock_to_live (bool) : Whether to lock line end to current bar

Returns: 0 (for chaining)

f_process_naked_lines(arr, calc_bars, bars_per_day, keep_to_day_end)

Process naked lines (POC/VAH/VAL) with sweeping detection

Parameters:

arr (array) : Array of NakedLine objects

calc_bars (int) : Maximum calculation bars

bars_per_day (int) : Bars per day for scope calculation

keep_to_day_end (bool) : Whether to extend to day end

Returns: 0 (for chaining)

f_update_pdhl_lines(pd_hl, pdh, pdl, new_day, pd_rng, bars_per_day, pdh_color, pdl_color)

Detect and create PDH/PDL lines

Parameters:

pd_hl (array) : Array to store HLLine objects

pdh (float) : Previous day high

pdl (float) : Previous day low

new_day (bool) : Whether it's a new day

pd_rng (float) : Price range for visibility

bars_per_day (int) : Bars per day

pdh_color (color) : PDH line color

pdl_color (color) : PDL line color

Returns: 0 (for chaining)

f_poc_from_vals(keys, vals)

Calculate POC from sorted keys and values

Parameters:

keys (array) : Sorted array of row keys

vals (array) : Array of volume values

Returns: POC row key

f_value_area(keys, vals, poc_key, va_pct)

Calculate Value Area from volume distribution

Parameters:

keys (array) : Sorted array of row keys

vals (array) : Array of volume values

poc_key (int) : POC row key

va_pct (float) : Value Area percentage (typically 0.70)

Returns: Tuple of

f_find_key_sorted(keys, target)

Find key in sorted array using binary search

Parameters:

keys (array) : Sorted array of keys

target (int) : Target key to find

Returns: Index of key, or -1 if not found

f_zscore_safe(x, len)

Safe z-score calculation using built-in functions

Parameters:

x (float) : Input series

len (int) : Lookback length

Returns: Z-score

HLLine

Represents a high/low line with sweeping detection

Fields:

ln (series line) : Line object

lb (series label) : Label object

lvl (series float) : Price level

startBar (series int) : Bar index where line starts

swept (series bool) : Whether the level has been swept

isHigh (series bool) : True if this is a high, false if low

col (series color) : Line color

NakedLine

Represents a naked POC/VAH/VAL line

Fields:

ln (series line) : Line object

lb (series label) : Label object

lvl (series float) : Price level

startBar (series int) : Bar index where line starts

swept (series bool) : Whether the level has been swept

sweptBar (series int) : Bar index where swept occurred

endBar (series int) : Bar index where line should end

Neeson Trend Price Oscillator Pulse EditionNeeson Trend Price Oscillator Pulse Edition: A Comprehensive Market Cycle Analysis Tool

Overview and Purpose

The Trend Price Oscillator Pulse Edition is a sophisticated technical analysis indicator designed to identify major market cycle tops and bottoms. This tool operates as a standalone oscillator in a subchart, providing clear visual signals of overbought and oversold conditions within the context of long-term market cycles. Developed for position traders and long-term investors, it focuses on capturing significant market turning points rather than short-term fluctuations.

Integration Rationale and Component Synergy

The indicator integrates three core analytical concepts into a cohesive system:

Detrended Price Oscillator (DPO) Foundation: Traditional DPO methodology isolates cyclical price movements by removing the underlying trend component. This creates a clearer view of oscillatory behavior without the distortion of long-term directional bias.

Normalization Framework: By converting raw DPO values to a standardized 0-100 scale, the indicator establishes consistent reference points for market extremes across different instruments and timeframes. This normalization enables meaningful comparison of oscillator readings regardless of absolute price levels.

Dynamic Threshold System: The implementation of adjustable threshold levels (default: 95% for overbought, 5% for oversold) creates adaptive boundaries that respond to changing market volatility and cycle characteristics.

These components work synergistically: The DPO extracts cyclical information from price action, the normalization process standardizes this information for consistent interpretation, and the threshold system provides actionable decision points based on historical extremes.

Operational Mechanism

The indicator calculates a detrended price value by comparing current price against a displaced moving average. This detrended value is then normalized against its historical range over a specified lookback period, transforming it into a percentage-based oscillator. A smoothing filter is applied to reduce noise and highlight significant movements.

The oscillator's movement through threshold zones generates four distinct market signals:

Entry into overbought territory (crossing above 95%)

Exit from overbought territory (crossing below 95%)

Entry into oversold territory (crossing below 5%)

Exit from oversold territory (crossing above 5%)

Each signal corresponds to a specific market condition hypothesis regarding institutional versus retail trader dynamics in major market cycles.

Practical Application Guidelines

Primary Use Cases:

Identification of potential major cycle turning points on weekly and monthly timeframes

Confirmation tool for existing trading strategies requiring cycle analysis

Risk management through recognition of extreme market conditions

Interpretation Framework:

Overbought Conditions (Oscillator ≥ 95%): Suggest potential selling pressure from major market participants. Consider reducing long exposure or implementing protective measures.

Oversold Conditions (Oscillator ≤ 5%): Indicate potential accumulation zones by institutional buyers. Consider establishing or adding to long positions using dollar-cost averaging strategies.

Threshold Crossings: Monitor for exits from extreme zones as potential confirmation that a cycle peak or trough may have formed.

Parameter Considerations:

Default parameters (548-period oscillator, 274-period offset, 1096-period lookback) are optimized for identifying major market cycles. Users may adjust these values for different market conditions or timeframes, though significant parameter changes will alter the indicator's sensitivity and signal frequency.

Originality and Distinctive Features

This implementation incorporates several innovative aspects:

Extended Cycle Focus: Unlike most oscillators designed for shorter timeframes, this tool employs exceptionally long calculation periods specifically for identifying primary market cycles.

Dynamic Normalization: The lookback-based normalization adapts to changing market conditions without requiring manual recalibration.

Multi-Signal Alert System: Four distinct alert conditions provide nuanced information about market state transitions rather than simple binary signals.

Integrated Risk Context: Each signal includes contextual information about potential market participant behavior, encouraging disciplined risk management.

Empirical Considerations and Limitations

The indicator provides probabilistic assessments based on historical price behavior, not predictive certainties. Market conditions may change, rendering historical patterns less reliable. Users should consider:

The indicator performs best in trending or cyclical markets; it may generate false signals during extended range-bound periods.

No technical indicator, including this one, can guarantee future market movements.

Proper position sizing and risk management should accompany all trading decisions, regardless of indicator signals.

Expected User Outcomes

When used as part of a comprehensive trading plan, this indicator can help users:

Identify potential reversal zones in major market cycles

Develop patience by focusing on significant rather than frequent trading opportunities

Maintain objective perspective during market extremes through quantitative assessment

Coordinate entry and exit timing with cycle analysis

The Trend Price Oscillator Pulse Edition represents a specialized tool for traders seeking to align their strategies with major market cycles through systematic analysis of price oscillation behavior relative to long-term trends.

Luminous Volume Flow [Pineify]Luminous Volume Flow

The Luminous Volume Flow is a specialized volume-based momentum oscillator designed to uncover the underlying buying and selling pressure within the market. Unlike traditional volume indicators that simply aggregate volume based on the close relative to the open, LVF analyzes intrabar dynamics—specifically the relationship between the close price and the high/low wicks—to estimate the dominance of buyers or sellers.

By smoothing this raw volume delta and applying a signal line, the LVF provides a clear visual representation of volume flow, helping traders identify trend strength, potential reversals, and momentum shifts with high-definition "luminous" visuals.

Key Features

Intrabar Pressure Analysis : Calculates buying and selling pressure based on wick dynamics and price polarity to provide a more granular view of market sentiment.

Multi-Type Smoothing : Offers selectable Moving Average types (SMA, EMA, RMA) for the main Flow Line to adapt to different market volatilities.

Luminous Visuals : Utilizes dynamic color gradients that brighten as momentum expands and darken as it contracts, offering immediate visual feedback on trend intensity.

Sentiment Cloud : Fills the area between the Flow and Signal lines to clearly visualize the prevailing bullish or bearish sentiment.

High-Contrast Signals : Optional high-contrast signal markers for clear crossover identification.

How It Works

The LVF operates on a multi-stage calculation process:

Pressure Calculation : The script compares the lower wick (Close - Low) against the upper wick (High - Close).

If the lower wick is longer, it suggests buying pressure (rejection of lower prices), and volume is assigned to Buy Pressure .

If the upper wick is longer, it suggests selling pressure (rejection of higher prices), and volume is assigned to Sell Pressure .

If equal, the Close > Open polarity is used as a tie-breaker.

Raw Delta : The difference between Buy and Sell Pressure is calculated to determine the net volume flow for the bar.

Flow Line : The Raw Delta is smoothed using a user-selected Moving Average (SMA, EMA, or RMA) over the Flow Length period. This creates the main oscillator line.

Signal Line : An EMA of the Flow Line is calculated to generate the Signal Line, similar to the MACD mechanic.

Histogram : The difference between the Flow Line and Signal Line determines the Histogram, which drives the "Luminous" color gradient logic.

Trading Ideas and Insights

Trend Confirmation : When the Flow Line is above the Signal Line and the Cloud is green, the bullish trend is supported by volume. Conversely, a red cloud indicates bearish volume dominance.

Momentum Crossovers : The triangle shapes indicate crossovers between the Flow and Signal lines. A triangle up (Green) suggests a potential bullish entry or invalidation of a short bias. A triangle down (Red) suggests a bearish turn.

Expansion vs. Contraction : Pay attention to the brightness of the histogram columns. Bright colors indicate expanding momentum (a strong move), while darker, fading colors suggest the move is losing steam, potentially preceding a consolidation or reversal.

How multiple components work together

This script combines the logic of Volume Delta analysis with Signal Line Crossover mechanics (popularized by MACD). By applying trend-following smoothing to raw volume data, we transform erratic volume spikes into a coherent flow. The "Luminous" visual layer is added to make the data interpretation intuitive—removing the need to mentally calculate the rate of change based on histogram height alone.

Unique Aspects

Adaptive Gradient Coloring : The histogram doesn't just show positive/negative values; it visually communicates the *acceleration* of the move via color intensity based on standard deviation.

Wick-Based Volume Attribution : Instead of a binary close-to-open comparison, LVF respects the price action within the candle (the wicks), acknowledging that a long lower wick on a red candle can actually represent significant buying interest.

How to Use

Add the indicator to your chart.

Adjust the Flow Length to match your trading timeframe (lower for scalping, higher for swing trading).

Select your preferred Smoothing Type (EMA is default and recommended for responsiveness).

Use the "Sentiment Cloud" filter: Look for long signals only when the cloud is green, and short signals when the cloud is red.

Monitor the Luminous Histogram for signs of exhaustion (colors fading) to manage exits.

Customization

Flow Length : Period for the main smoothing (Default: 14).

Signal Length : Period for the signal line (Default: 9).

Smoothing Type : Choose between SMA, EMA, or RMA.

Colors : Fully customizable colors for Bullish/Bearish phases and signals.

Chart Bars : Option to color the main chart candles based on the Flow direction.

Conclusion

The Luminous Volume Flow is a robust tool for traders who want to go beyond price action and understand the volume dynamics driving the market. By visualizing the flow of buying and selling pressure with advanced smoothing and reactive visuals, it provides a clearer picture of market sentiment than standard volume bars.