MTF Regime Filter II [CHE]Regime Filter II - Comprehensive Guide

Introduction

The "Regime Filter II " indicator is a tool designed to help traders identify market trends by smoothing price data and applying a color scheme to visualize bullish and bearish conditions. This guide provides a detailed explanation of the script's functionality, benefits, and how to use it effectively in TradingView.

Key Benefits

1. Trend Identification: Smooths price data to highlight underlying trends, making it easier for traders to spot potential buying or selling opportunities.

2. Visual Clarity: Uses distinct color schemes to differentiate between bullish and bearish market conditions, enhancing visual analysis.

3. Customization: Offers various settings to adjust smoothing and averaging lengths, choose between different color schemes, and set visibility for different timeframes.

4. Neutral Candle Option: Provides an option to display neutral candles for clearer visual representation when market conditions are neither strongly bullish nor bearish.

5. Timeframe Adaptability: Includes functions to determine appropriate step sizes based on different timeframes, ensuring the indicator remains accurate across various trading periods.

Script Breakdown

1. Indicator Declaration

The script starts by declaring itself as a TradingView indicator using the latest version of Pine Script. This sets up the framework for the indicator's functionality.

2. User Inputs for Smoothing and Averaging Lengths

The script allows users to input specific lengths for smoothing and averaging intervals. These inputs are crucial for determining how the price data is processed to identify trends. By adjusting these lengths, users can fine-tune the sensitivity of the indicator to market movements.

3. Color Scheme Selection

Users can choose between two color schemes: "Traditional" and "WT1 0 Rule". The selected color scheme will determine how the indicator colors the candles to represent bullish and bearish conditions. This customization enhances the visual appeal and usability of the indicator according to personal preferences.

4. Settings for Timeframe Visibility

The script includes settings that allow users to specify which timeframes the indicator should be visible on. This feature helps traders focus on the most relevant timeframes for their trading strategies. Additionally, users can set the number of recent candles to display, providing a clear view of the most recent market trends.

5. Color Definitions

The indicator defines specific colors for bearish and bullish candles. Bearish candles are colored red, while bullish candles are green. These color definitions are applied based on the selected color scheme and the calculated trend, providing a quick visual reference for market conditions.

6. Time Constants

To manage different timeframes effectively, the script uses constants that represent various time intervals in milliseconds, such as minutes, hours, and days. These constants are used to convert timeframes into a format that the script can work with to determine the appropriate step size for calculations.

7. Step Size Determination

The script includes a function that determines the step size based on the selected timeframe. This function ensures that the indicator adapts to different timeframes, maintaining its accuracy and relevance across various trading periods. The step size is calculated based on time intervals, and appropriate labels (like "60", "240", "1D") are assigned.

- For timeframes less than or equal to 1 minute, the step size is set to "60".

- For timeframes less than or equal to 5 minutes, the step size is set to "240".

- For timeframes less than or equal to 1 hour, the step size is set to "1D" (daily).

- For timeframes less than or equal to 4 hours, the step size is set to "3D" (three days).

- For timeframes less than or equal to 12 hours, the step size is set to "7D" (weekly).

- For timeframes less than or equal to 1 day, the step size is set to "1M" (monthly).

- For timeframes less than or equal to 1 week, the step size is set to "3M" (three months).

- For all other timeframes, the step size is set to "12M" (yearly).

8. Trend Calculation

The core of the indicator is its ability to calculate market trends. Here's a detailed breakdown of how the `calculateTrend` function works:

- Initialization: Variables for the middle price and scale, and summations of high/low prices and ranges, are initialized.

- Summation Loop: A loop runs over the smoothing length to calculate the sum of high and low prices and their range.

- Middle and Scale Calculation: The middle price is determined as the average of high/low sums, and the scale is calculated as a fraction of the average range.

- Normalization: The high, low, and close prices are normalized based on the middle price and scale.

- HT Calculation: The normalized prices are smoothed using a simple moving average (SMA).

- Frequency and Exponential Calculations: The frequency and related constants (a, c1, c2, c3) are calculated for further smoothing.

- Smoothed Moving Average (SMA): A smoothed moving average is computed using the HT values and exponential constants.

- WT1 and WT2 Calculation: The final smoothed values (WT1) and their average (WT2) are derived.

9. Color Application Based on Trend

Once the trend is calculated, the script applies the appropriate color to the candles based on the selected color scheme. This function ensures that the visual representation of the trend is consistent with the user’s preferences.

10. Label Plotting for Timeframes

If the option to display timeframe labels is enabled, the script plots labels on the chart to indicate the current timeframe. This feature helps users quickly identify which timeframe they are analyzing.

11. Shape Plotting Based on Trend and Color Scheme

The indicator plots shapes (squares) on the chart based on the calculated trend and selected color scheme. These shapes provide an additional visual cue for market conditions, enhancing the overall clarity of the indicator.

12. Neutral Candle Color Option

The script includes an option to set the color of neutral candles when market conditions are neither strongly bullish nor bearish. This option helps traders better visualize periods of market indecision.

Summary

The "Regime Filter II " is a powerful and customizable tool for traders, offering clear visual cues for market trends and adaptability to various timeframes. By smoothing price data and applying intuitive color schemes, it helps traders make more informed decisions. With features like adjustable smoothing lengths, multiple color schemes, and optional neutral candle displays, this indicator enhances market analysis and trading strategy development. By following this comprehensive guide, traders can effectively utilize the "Regime Filter II " indicator to enhance their market analysis and make more informed trading decisions.

Best regards

스크립트에서 "bear"에 대해 찾기

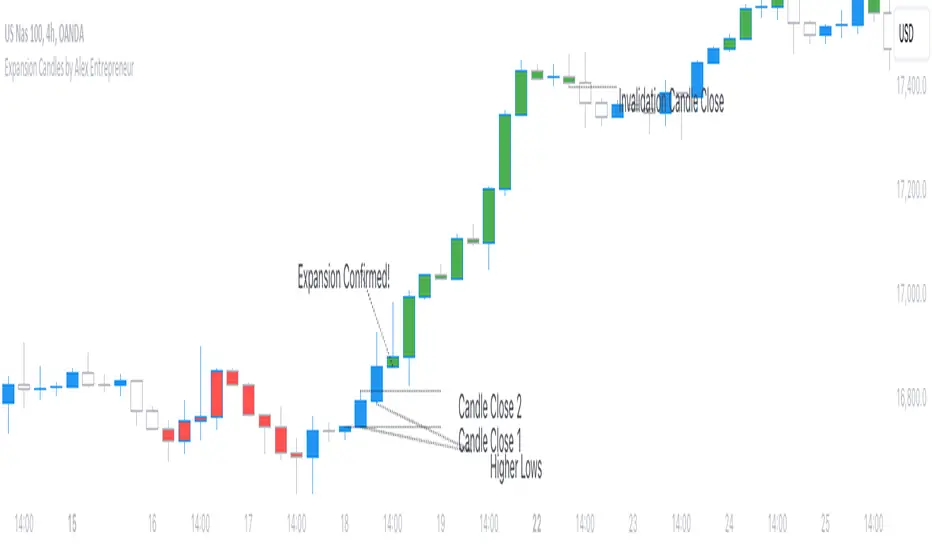

Expansion Candles by Alex EntrepreneurHey people! Thanks for using Expansion Candles. I designed this tool to help me identify price runs (expansions) based on consecutive bullish or bearish candle closes and then trade continuations on the lower timeframes. Here's what makes it awesome:

How Does It Work?

An “expansion” is confirmed after multiple closes above the previous candle’s high (in the bull case) or below the previous candle’s low (in the bear case) while also having a higher candle low than the previous candle (in the bull case) or having lower candle high that the previous candle (in the bear case). After an expansion is confirmed, then the indicator will be displayed on the next candle.

You can set the number of required candle closes that confirm an “expansion” by increasing or decreasing the "Required Candles For Valid Expansion" setting.

An expansion will continue until an “invalidation” event occurs this will cause the indicator to stop displaying.

This “invalidation” can either be a lower candle low than the previous candle (in the bull case) and a higher candle high than the previous candle (in the bear case), or a close below the previous candle’s low (in the bull case) or a close above the previous candle’s high (in the bear case).

You can choose whether you want to use candle highs and lows as invalidation or candle closes as invalidation by changing the “Invalidation Type” setting to either “Wick” or “Candle Close”.

Key Features

Price Run Detection : Identify when price is expanding through consecutive bullish or bearish candle closes. You can chose whether a wick or opposite candle close finishes the run.

Timeframe Selection : Select your preferred timeframe for expansion candles and then view the indicator on lower timeframes for precise continuation entries.

Custom Display Options : Tailor the way expansions are shown on your chart. Choose your bullish and bearish colours and then display expansions as coloured candles, background colours, boxes, or arrows.

Sensitivity Adjustment : Adjust the indicator's sensitivity by changing the number of "Required Candles For Valid Expansion" to suit your analysis.

Set Alerts : Detect new bullish or bearish expansions in your favourite instruments with customisable alerts.

Best,

Alex Entrepreneur

Johnny's Adjusted BB Buy/Sell Signal"Johnny's Adjusted BB Buy/Sell Signal" leverages Bollinger Bands and moving averages to provide dynamic buy and sell signals based on market conditions. This indicator is particularly useful for traders looking to identify strategic entry and exit points based on volatility and trend analysis.

How It Works

Bollinger Bands Setup: The indicator calculates Bollinger Bands using a specified length and multiplier. These bands serve to identify potential overbought (upper band) or oversold (lower band) conditions.

Moving Averages: Two moving averages are calculated — a trend moving average (trendMA) and a long-term moving average (longTermMA) — to gauge the market's direction over different time frames.

Market Phase Determination: The script classifies the market into bullish or bearish phases based on the relationship of the closing price to the long-term moving average.

Strong Buy and Sell Signals: Enhanced signals are generated based on how significantly the price deviates from the Bollinger Bands, coupled with the average candle size over a specified lookback period. The signals are adjusted based on whether the market is bullish or bearish:

In bullish markets, a strong buy signal is triggered if the price significantly drops below the lower Bollinger Band. Conversely, a strong sell signal is activated when the price rises well above the upper band.

In bearish markets, these signals are modified to be more conservative, adjusting the thresholds for triggering strong buy and sell signals.

Features:

Flexibility: Users can adjust the length of the Bollinger Bands and moving averages, as well as the multipliers and factors that determine the strength of buy and sell signals, making it highly customizable to different trading styles and market conditions.

Visual Aids: The script vividly plots the Bollinger Bands and moving averages, and signals are visually represented on the chart, allowing traders to quickly assess trading opportunities:

Regular buy and sell signals are indicated by simple shapes below or above price bars.

Strong buy and sell signals are highlighted with distinctive colors and placed prominently to catch the trader's attention.

Background Coloring: The background color changes based on the market phase, providing an immediate visual cue of the market's overall sentiment.

Usage:

This indicator is ideal for traders who rely on technical analysis to guide their trading decisions. By integrating both Bollinger Bands and moving averages, it provides a multi-faceted view of market trends and volatility, making it suitable for identifying potential reversals and continuation patterns. Traders can use this tool to enhance their understanding of market dynamics and refine their trading strategies accordingly.

Delta ZigZag [LuxAlgo]The Delta ZigZag indicator is focused on volume analysis during the development of ZigZag lines. Volume data can be retrieved from a Lower timeframe (LTF) or real-time Tick data.

Our Delta ZigZag publication can be helpful in detecting indications of a trend reversal or potential weakening/strengthening of the trend.

This indicator by its very nature backpaints, meaning that the displayed components are offset in the past.

🔶 USAGE

The ZigZag line is formed by connecting Swings , which can be set by adjusting the Left and Right settings.

Left is the number of bars for evaluation at the left of the evaluated point.

Right is the number of bars for evaluation at the right of the evaluated point.

A valid Swing is a value higher or lower than the bars at the left/right .

A higher Left or Right set number will generally create broader ZigZag ( ZZ ) lines, while the drawing of the ZZ line will be delayed (especially when Right is set higher). On the other hand, when Right is set at 0, ZZ line are drawn quickly. However, this results in a hyperactive switching of the ZZ direction.

To ensure maximum visibility of values, we recommend using " Bars " from the " Bar's style " menu.

🔹 Volume examination

The script provides two options for Volume examination :

Examination per ZigZag line

Examination per bar

Bullish Volume is volume associated with a green bar ( close > open )

Bearish Volume is volume associated with a red bar ( close < open )

Neutral Volume (volume on a " close == open" bar) is not included in this publication.

🔹 Examination per ZigZag line

As long as the price moves in the same direction, the present ZZ line will continue. When the direction of the price changes, the bull/bear volume of the previous ZZ line is evaluated and drawn on the chart.

The ZZ line is divided into two parts: a bullish green line and a bearish red line.

The intercept of these two lines will depend on the ratio of bullish/bearish volume

This ratio is displayed at the intercept as % bullish volume (Settings -> Show % Bullish Volume)

* Note that we cannot draw between 2 bars. Therefore, if a ZZ line is only 1 bar long, the intercept will be at one of those 2 bars and not in between. The percentage can be helpful in interpreting bull/bear volume.

In the example above (2 most right labels), you can see that an overlap of 2 labels is prevented, ensuring the ability to evaluate the bullish % volume of the ZZ line .

The percentage will be colored green when more than 50%, red otherwise. The color will fade when the direction is contradictory; for example, 40% when the ZZ line goes up or 70% when the ZZ line falls.

More details can be visualized by enabling " Show " and choosing 1 of 3 options:

Average Volume Delta/bar

Average Volume/bar

Normalised Volume Delta

For both 'averages', the sum of " Volume "/" Volume Delta " of every bar on the ZZ line is divided by the number of bars (per ZZ line ).

The " Normalised Volume Delta " is calculated by dividing the sum of " Delta Volume " by the sum of " Volume " (neutral volume not included), which is displayed as a percentage.

All three options will display a label at the last point of the ZZ line and be coloured similarly: green when the ratio bullish/bearish volume of the ZZ line is bullish and red otherwise. Here, the colour also fades when it is bullish, but the ZZ line falls or when it is bearish with a rising ZZ line .

A tooltip at each label hints at the chosen option.

You can pick one of the options or combine them together.

🔹 Examination per bar

Besides information about what's happening during the ZZ line , information per bar can be visualized by enabling " Show Details " in Settings .

Split Volume per bar : show the sum of bullish (upV) and bearish (dnV) volume per bar

Volume (bar) : Total Volume per bar (bullish + bearish volume, neutral volume not included)

Δ Volume (bar) : Show Delta Volume (bullish - bearish volume)

🔹 Using Lower Timeframe Data

The ZigZag lines using LTF data are colored brighter. Also note the vertical line where the LTF data starts and the gap between ZZ lines with LTF data and without.

When " LTF " is chosen for the " Data from: " option in Settings , data is retrieved from Lower Timeframe bars (default 1 minute). When the LTF setting is higher than the current chart timeframe, the LTF period will automatically be adjusted to the current timeframe to prevent errors.

As there is a 100K limit to the number of LTF intrabars that can be analyzed by a script, this implies the higher the difference between LTF and current TF; the fewer ZZ lines will be seen.

🔹 Using real-time tick data

The principles are mostly the same as those of LTF data. However, in contrast with LTF data, where you already have LTF ZZ lines when loading the script, real-time tick data-based ZZ lines will only start after loading the chart.

Changing the settings of a ticker will reset everything. However, returning to the same settings/ticker would show the cached data again.

Here, you can see that changing settings reset everything, but returning after 2 minutes to the initial settings shows the cached data. Don't expect it to be cached for hours or days, though.

🔶 DETAILS

The timeframe used for LTF data should always be the same or lower than the current TF; otherwise, an error occurs. This snippet prevents the error and adjusts the LTF to the current TF when LTF is too high:

res = input.timeframe('1')

res := timeframe.from_seconds( math.min( timeframe.in_seconds(timeframe.period), timeframe.in_seconds(res) ) )

🔶 SETTINGS

Data from: LTF (Lower TimeFrame) or Ticks (Real-time ticks)

Res: Lower TimeFrame (only applicable when choosing LTF )

Option: choose " high/low " or " close " for Swing detection

🔹 ZigZag

Left: Lookback period for Swings

Right: Confirmation period after potential Swing

🔹 ZigZag Delta

Show % Bullish Volume : % bullish volume against total volume during the ZZ line

Show:

Average Volume Delta/bar

Average Volume/bar

Normalised Volume Delta

See USAGE for more information

🔹 Bar Data

Split Volume per bar: shows the sum of bullish ( upV ) and bearish ( dnV ) volume per bar

Volume (bar): Total Volume per bar (bullish + bearish volume, neutral volume not included)

Δ Volume (bar): Show Volume Delta (bullish - bearish volume)

TSF 20What kind of traders/investors are we?

We are trend followers. We look for assets that are outperforming the market. Our scripts are designed to be used on the higher timeframes (weekly/daily) to catch the large moves/trends in the market.

Our scripts have been designed to help you follow the trend in an asset.

What does this script do?

This script is designed to colour candles on a chart based on their position relative to two sets of Bollinger Bands. Here's a breakdown of how it functions:

Bollinger Bands Setup:

The script uses two sets of Bollinger Bands, both with a length of 20 and based on the closing prices of candles.

The first set of Bollinger Bands uses a standard deviation (StdDev) of 1.

The second set uses a standard deviation of 2.

Neither set of bands is displayed on the chart.

Coloring Candles:

Green Candle: A candle is coloured green if its close is above the upper Bollinger Band with StdDev 1 but below the upper Bollinger Band with StdDev 2. This indicates a moderately bullish sentiment.

Dark Green Candle: A candle is colored dark green when its close is above the upper Bollinger Band with StdDev 2. This implies a stronger bullish sentiment.

Red Candle: A candle is coloured red if its close is below the lower Bollinger Band with StdDev 1 but above the lower Bollinger Band with StdDev 2. This indicates a moderately bearish sentiment.

Dark Red Candle: A candle is colored dark red if its close is below the lower Bollinger Band with StdDev 2, indicating a stronger bearish sentiment.

Grey Candle: A candle is coloured grey if it closes between the upper and lower Bollinger Bands with StdDev 1. This usually signifies a neutral market condition or periods of consolidation.

In summary, this script is an analytical tool that visually represents the market's bullishness or bearishness relative to the Bollinger Bands, without displaying the bands themselves. It's designed to help investors quickly assess market conditions and sentiment based on the colour-coded representation of price action in relation to these volatility bands.

What makes this script unique?

Innovative Color-Coding System: Candles are colored in varying shades of green and red, providing an immediate visual cue about the market's bullish or bearish tendencies. A neutral grey is also used, offering a quick assessment of market indecision or consolidation phases.

Dual Bollinger Band Analysis: Utilizes two sets of Bollinger Bands (StdDev 1 and StdDev 2) to gauge market volatility and sentiment. This dual-band approach enhances the precision of sentiment analysis compared to using a single standard deviation.

Customizable and Non-Obtrusive: Designed to keep your charts clean and readable. The Bollinger Bands themselves are not displayed, reducing visual clutter and allowing for a focus on price action.

Versatile and Adaptable: Suitable for various trading styles and timeframes. Whether you are a short-term or long-term investor, this indicator can be seamlessly integrated into your analysis toolkit.

Valuable Addition to Market Analysis: Enhances traditional candlestick analysis and complements other technical indicators and strategies. It offers an additional layer of understanding market dynamics and can be used to confirm or question other signals.

How It Adds Value:

Enhanced Visual Analysis: By colour-coding candles based on Bollinger Band positioning, it simplifies the interpretation of market sentiment and volatility, making it easier to spot trends and reversals.

Strategic Decision Making: Helps traders make more informed decisions by clearly highlighting bullish and bearish strength, or lack thereof, in the market.

Time Efficiency: Reduces the time spent analyzing charts by providing an immediate visual representation of market conditions.

Originality: Offers a fresh perspective and an innovative approach to using Bollinger Bands, making it a unique addition to the community's toolbox.

Morning & Evening Star This Pine Script code is designed to identify Morning Star and Evening Star candlestick patterns on a chart. Here's how it works:

Calculate Candle Body and Wick Sizes: The script calculates the size of the candle body and wick based on the difference between the close and open prices, as well as the difference between the high and the maximum of the close and open prices.

Determine if the Candle is a Doji: It checks if the candle is a doji by comparing the size of the body to a fraction of the wick size. If the body size is less than or equal to 20% of the wick size, it is considered a doji.

Determine if the Current Candle is Bullish or Bearish: It checks if the current candle is bullish (close price is higher than open price) or bearish (close price is lower than open price).

Plot Shapes for Doji and Candles: It plots shapes on the chart to indicate buy and sell signals based on the presence of a doji and the formation of Morning Star or Evening Star patterns. These shapes are displayed below (for buy signals) or above (for sell signals) the respective candlesticks.

Combine this indicator with my support and resistance zones indicator for better results

Xen's Flag Pattern Scalper1. Input Parameters:

FlagLength: Determines the length of the flag pattern.

TakeProfit1Ratio, takeProfit2Ratio, takeProfit3Ratio: Define the ratios for calculating

the take-profit levels relative to the entry price.

RiskRewardRatio: Specifies the risk-reward ratio for calculating the stop-loss level

relative to the entry price.

2 Flag Conditions:

BullishFlag: Checks if the current bar meets the conditions for a bullish flag pattern. It

evaluates to true if the low of the current bar is lower than the low flagLength bars

ago, and the close of the current bar is higher than the high flagLength bars ago.

BearishFlag: Checks if the current bar meets the conditions for a bearish flag pattern. It evaluates to true if the high of the current bar is higher than the high flagLength bars

ago, and the close of the current bar is lower than the low flagLength bars ago.

3. Entry Price:

EntryPrice: Calculates the entry price based on whether a bullish or bearish flag

pattern is identified. For a bullish flag, the entry price is set to the low of the current bar.

For a bearish flag, the entry price is set to the high of the current bar.

4. Stop Loss:

StopLoss: Determines the stop-loss level based on the entry price and the specified

riskRewardRatio . For a bullish flag, the stop-loss level is calculated by subtracting the

difference between the high and low of the current bar multiplied by the riskRewardRatio from the low of the current bar. For a bearish flag, the stop-loss level

is calculated similarly but added to the high of the current bar.

5. Take Profit Levels:

Three take-profit levels ( takeProfit1, takeProfit2, takeProfit3 ) are calculated based on

the entry price, stop-loss level, and specified take-profit ratios ( takeProfit1Ratio,

takeProfit2Ratio, takeProfit3Ratio ).

6. Plotting Signals and Levels:

Bullish and bearish flag patterns are plotted using triangle shapes ( shape.triangleup for

bullish and shape.triangledown for bearish) above or below the bars, respectively.

Entry, stop-loss, and take-profit levels are plotted using horizontal lines ( line.new )

with different colors and styles. Entry and stop-loss levels are labeled with "Entry" and "SL",

respectively, while take-profit levels are labeled with "TP 1", "TP 2", and "TP 3".

The colors for bullish flags are white for entry, red for stop-loss, and green for take-profit levels. For bearish flags, the colors are the same, but the labels are plotted above the bars.

7. Label Placement:

Labels for entry, stop-loss, and take-profit levels are placed a distance of 4 bars to the right

of the entry price using bar_index + 4 .

This indicator is intended to help traders identify flag patterns on price charts and visualize potential entry, stop-loss, and take-profit levels associated with these patterns.

Please use risk management and when TP1 is hit, move stoploss to breakeven .

Relative Strength Scoring SystemRelative Strength Scoring System :

Important prerequisite :

This indicator can be loaded on any forex chart, i.e. a currency pair, but must not be loaded on any other asset due to certain market closures.

The chart timeframe must be less than or equal to the trading timeframe, which is the indicator's first parameter. A timeframe equal to that of the "Trading Timeframe" parameter is preferable.

Introduction :

This indicator measures the relative strength of a currency against all other currencies using spread formulas. It gives an indication of which currencies are bullish, neutral or bearish. The ultimate aim of this indicator is to find out which pair will generate a higher probability of gain than the others by pairing the most bullish pair with the most bearish pair.

Spread formulas :

To find the relative strength of a currency compared with others, we use the following spreads formulas :

USD = (FX:USDJPY/100+SAXO:USDEUR+FX:USDCHF+SAXO:USDGBP+FX:USDCAD+SAXO:USDAUD+FX_IDC:USDNZD)/7

JPY = (SAXO:JPYUSD/100+FX_IDC:JPYAUD/100+FX_IDC:JPYCAD/100+FX_IDC:JPYNZD/100+FX_IDC:JPYCHF/100+SAXO:JPYEUR/100+FX_IDC:JPYGBP/100)/7

CHF = (FX:CHFJPY/100+SAXO:CHFUSD+SAXO:CHFEUR+FX_IDC:CHFGBP+FX_IDC:CHFCAD+SAXO:CHFAUD+FX_IDC:CHFNZD)/7

EUR = (FX:EURJPY/100+FX:EURUSD+FX:EURCHF+FX:EURGBP+FX:EURCAD+FX:EURAUD+FX:EURNZD)/7

GBP = (FX:GBPJPY/100+FX:GBPUSD+FX:GBPCHF+SAXO:GBPEUR+FX:GBPCAD+FX:GBPAUD+FX:GBPNZD)/7

CAD = (FX:CADJPY/100+SAXO:CADUSD+FX:CADCHF+FX_IDC:CADGBP+SAXO:CADEUR+FX_IDC:CADAUD+FX_IDC:CADNZD)/7

AUD = (FX:AUDJPY/100+FX:AUDUSD+FX:AUDCHF+SAXO:AUDGBP+FX:AUDCAD+SAXO:AUDEUR+FX:AUDNZD)/7

NZD = (FX:NZDJPY/100+FX:NZDUSD+FX:NZDCHF+SAXO:NZDGBP+FX:NZDCAD+SAXO:NZDAUD+SAXO:NZDEUR)/7

CRYPTO = (BITSTAMP:BTCUSD+BITSTAMP:ETHUSD+BITSTAMP:LTCUSD+BITSTAMP:BCHUSD)/4

Timeframes :

As mentioned in the prerequisites, the chart timeframe must not be greater than the trading timeframe. The latter corresponds to the timeframe chosen by the trader to enter a position, and is the indicator's first parameter. Once this has been chosen, the algorithm selects the timeframes of the "Trend" and "Velocity" charts. Here's how it allocates them :

Trading TF => ("Velocity TF", "Trend TF")

"5min" => ("15min ", "60min")

"15min" => ("60min ", "4h")

"30min" => ("2h ", "8h")

"60min" => ("4h ", "12h")

"4h" => ("12h", "1D")

"6h" => ("1D", "3D")

"8h" => ("1D", "4D")

"12h" => ("2D", "1W")

"1D" => ("3D", "1W")

Trend Scoring System :

When the timeframe of the trend graph has been allocated, the algorithm will establish this graph's score using three criteria :

Trend chart pivot points: if the last two pivots, high and low, are increasing, the score is 1; if they are decreasing, the score is -1; else the score is 0.

SMA: if its slope is increasing with a candle strictly above the SMA value, the score is 1; if its slope is decreasing with a candle strictly below it, the score is -1; otherwise, it is 0.

MACD: if the MACD is positive, the score is 1, if it is negative, the score is -1; else it's 0.

We then sum the scores of these three criteria to find the trend score.

Velocity Scoring System :

In the same way, we analyze the score of the "velocity" graph with its corresponding timeframe using three criteria :

The EMA: if its slope is increasing with a candle strictly above the EMA value, the score is 1; if its slope is decreasing with a candle strictly below it, the score is -1; otherwise, it is 0.

The RSI: if the RSI's EMA has an increasing slope with an RSI strictly greater than the value of this EMA, the score is 1; and if the RSI's EMA has a decreasing slope with an RSI strictly less than this EMA, the score is -1; otherwise it is 0.

SAR parabolic: if the SAR is below the price, the score is 1; if it is above the price, the score is -1.

We then sum the scores of these three criteria to find the velocity score.

Relative Strength Scoring System :

Once the trend score and velocity score have been calculated, we determine the relative strength score of each currency using the following algorithm :

If trend score >=2 and velocity score >=2, the currency is bullish.

If trend score <=2 and velocity score <=2, currency is bearish

If (trendScore>=2 or velocityScore>=2) and (trendScore=1 or velocityScore=1) the currency is not yet bullish

If (trendScore<=2 or velocityScore<=2) and (trendScore=-1 or velocityScore=-1) the currency is not yet bearish.

Otherwise the currency is neutral

Parameters :

Trading Timeframe: the trading timeframe chosen by the trader for which he makes his position entry and exit decisions. Default is 1h

Pivot Legs: Parameter used for the chart "Trend" setting the pivot strength to the right and left of high/low. Default is 2

SMA Length: SMA length of the chart "Trend". Default is 20

MACD Fast Length: Length of the MACD fast SMA calculated on the chart "Trend". Default is 12

MACD Slow Length: Length of the MACD slow SMA calculated on the chart "Trend". Default is 26

MACD Signal Length: Length of the MACD signal SMA calculated on the chart "Trend". Default is 9

EMA Length: EMA length of the "Velocity" graph. Default is 13

RSI Length: RSI length of the "Velocity" graph. Default is 14

RSI EMA Length: Length of the RSI EMA. Default is 9

Parabolic SAR Start: Start of the SAR parabola in the "Velocity" graph. Default is 0.02

Parabolic SAR Increment: Increment of the SAR parabola in the "Velocity" graph. Default is 0.02

Parabolic SAR Max: Maximum of the SAR parabola in the "Velocity" graph. Default is 0.2

Conclusion :

This indicator has been designed to determine the relative strength of the major currencies against each other. The aim is to know which pair to trade at the right time in order to maximize the probability of a successful trade. For example, if the USD is bullish and the NZD bearish, we'll short the NZDUSD pair.

Enjoy this indicator and don't forget to take the trade ;)

Open Interest Inflows & Outflows [LuxAlgo]The Open Interest Inflows & Outflows indicator focuses on highlighting alterations in the overall count of active contracts associated with a specific financial instrument.

The indicator also includes an oscillator highlighting the price sentiment to use in conjunction with the open interest flow sentiment and also includes a rolling correlation of the open interest flow sentiment with a user-selected source.

🔶 USAGE

Open Interest (OI) indicates the total number of active contracts, encompassing both long and short positions, for a specific financial instrument at any given moment. This key indicator helps traders and analysts assess market activity and sentiment.

An increase in open interest generally indicates new money flowing into the market, suggesting increased activity and the potential for a trending market. Conversely, a decrease in open interest indicates that traders are closing their positions, suggesting less interest in that particular contract.

Open Interest Flow Sentiment assesses the correlation between the initiation of new positions (inflows) and the closure of existing positions (outflows) for a particular instrument. Positive values suggest a prevalence of inflows, while negative values signify a prevalence of outflows.

The magnitude of the deviation from zero reflects the extent of dominance, either in inflows or outflows.

Price Sentiment estimates the relationship between the strength of bulls (buyers) and bears (sellers) on an instrument. Positive values indicate higher bull power and negative values indicate higher bear power.

The correlation feature is a key component of the indicator and helps analyze the relationship between trading volume and Open Interest changes. If volume increases along with rising Open Interest, it supports the validity of the price trend.

A divergence between price movement, volume, and Open Interest may signal potential reversals.

🔶 DETAILS

This indicator, based on Dr. Alexander Elder's acclaimed Elder-Ray concept, aids traders in evaluating the strength of both bulls and bears by delving beneath the surface of the markets. It uncovers data not immediately apparent from a superficial glance at prices. The indicator comprises two components: Bull Power and Bear Power.

Considering that the high price of any candle signifies the maximum power of buyers and the low price represents the maximum power of sellers, Elder employs the 13-period Exponential Moving Average (EMA) to depict the average consensus of price value. Bull Power assesses whether buyers can drive prices above the average consensus of value, while Bear Power assesses whether sellers can push prices below this average.

Here are the formulas for Bull Power and Bear Power:

bull_power = high - ema(close, 13)

bear_power = low - ema(close, 13)

This concept is utilized to calculate Open Interest Flow Sentiment and Price Sentiment. The Open Interest Flow Sentiment estimates the relationship between new positions (inflows) and positions being closed (outflows), providing insights into market dynamics. The Price Sentiment, on the other hand, gauges the correlation between price movements and the Elder-Ray components, aiding traders in identifying potential shifts in market sentiment and momentum.

🔶 SETTINGS

🔹Open Interest Inflows & Outflows

OI Sentiment Correlation: toggles the visibility of Open Interest correlation with a variety of sources.

Money Flow Estimates: toggles the visibility of Money Flow Estimates calculated for the last bar.

🔹Style

OI Flow Sentiment: toggles the visibility of Open Interest Flow Sentiment, along with color customization options.

Price Sentiment: toggles the visibility of Price Sentiment, along with color customization options.

Correlation Colors: color customization option for the Correlation Area.

🔹Others

Smoothing: smoothing length applicable for Open Interest Flow Sentiment and Price Sentiment.

🔶 RELATED SCRIPTS

Open-Interest-Chart

Liquidation-Estimates

Thanks to our community for recommending this script. For more conceptual scripts and related content, we welcome you to explore by visiting >>> LuxAlgo-Scripts .

Reversal and Breakout Signals [AlgoAlpha]🚀🌟 Introducing the Reversal and Breakout Signals by AlgoAlpha 🌟🚀

This innovative tool is crafted to enhance your chart analysis by identifying potential reversal and breakout opportunities directly on your charts. It's designed with both novice and experienced traders in mind, providing intuitive visual cues for better decision-making. Let's dive into the key features and how it operates:

### Key Features:

🔶 Dynamic Period Settings: Customize the sensitivity of the indicator with user-defined periods for both the indicator and volume strength.

📊 Volume Threshold: Set a threshold to define what constitutes strong volume, enabling the identification of significant market movements.

💡 Trend Coloring: Option to color candles during trends, making it easier to visualize bullish and bearish market conditions.

🌈 Customizable Visuals: Choose your preferred colors for bullish, bearish, and breakout signals, personalizing the chart to your liking.

🚨 Advanced Alert System: Configure alerts for reversal and breakout signals, ensuring you never miss a potential trading opportunity.

### How to Use:

To maximize the effectiveness of the Reversal and Breakout Signals tool, follow these steps:

1. 🔧 Set Up Your Preferences:

- Adjust the Indicator Period and Volume Strength Period to match the timeframe of your trading strategy. This fine-tuning allows the indicator to better align with your specific market analysis needs.

- Define the Strong Volume Threshold to distinguish between ordinary and significant volume movements. This helps in identifying breakout or reversal signals with higher confidence.

2. 🎨 Customize Visuals:

- Choose colors for Bullish , Bearish , and Breakout Signals to visually differentiate between different types of market activities. This customization facilitates quicker decision-making while scanning charts.

3. 🔍 Reversal Signals:

- Bullish Reversal : Look for a triangle below the bar indicating a potential upward movement. It's identified when the price dips below the lower level but closes above it, suggesting a rejection of lower prices.

- Bearish Reversal : A triangle above the bar signals a potential downward movement. This occurs when the price spikes above the upper level but closes below, indicating a rejection of higher prices.

4. 📈 Trend and Breakout Signals:

- Diamonds represent breakout signals. A bullish breakout is marked below the bar when the price closes above the upper level, suggesting strong buying pressure. Conversely, a bearish breakout above the bar indicates strong selling pressure as the price closes below the lower level.

- The tool also features a Trend Tracker that highlights the current market trend using the Hull Moving Average (HMA). This can help you stay aligned with the overall market direction for your trades.

By integrating these steps into your trading strategy, the Reversal and Breakout Signals tool can provide actionable insights to help identify potential entry and exit points, enhancing your trading decisions with visual cues and alerts for market reversals and breakouts.

### How It Works:

The core logic revolves around calculating weighted moving averages of high and low prices over a user-defined period, identifying the highest and lowest points within this period to establish potential breakout or breakdown levels while reducing the amount of noise, hence the use of moving averages.

1. Weighted Moving Averages Calculation:

sh = ta.wma(high, len)

sl = ta.wma(low, len)

h = ta.highest(sh, len)

l = ta.lowest(sl, len)

2. Breakout and Reversal Detection:

The script then employs logic to detect bullish and bearish breakouts and reversals based on the closing price's position relative to these levels, combined with volume analysis to confirm the strength of the move.

if not (h < h or h > h )

hstore := h

if not (l < l or l > l )

lstore := l

bullishbreakout := (breakout or ((breakout or breakout or breakout or breakout ) and candledir == 1)) and strongvol and not (bullishbreakout or bullishbreakout or bullishbreakout )

bearishbreakout := (breakdown or ((breakdown or breakdown or breakdown or breakdown ) and candledir == -1)) and strongvol and not (bearishbreakout or bearishbreakout or bearishbreakout )

3. Visual Indicators and Alerts:

Visual cues such as triangle shapes for reversals and diamonds for breakouts, along with colored bars, make it easy to spot these opportunities. Additionally, alerts can be set up for these events, ensuring traders can react promptly to potential trading setups.

plotshape(bullishrej and not (state ==- 1) ? low * 0.9995 : na, " Bullish Reversal ", shape.triangleup, location.belowbar, color.new(green, 0), size = size.tiny, text = "𝓡", textcolor = color.gray)

plotshape(bearishrej and not (state == 1) ? high * 1.0005 : na, " Bearish Reversal ", shape.triangledown, location.abovebar, color.new(red, 0), size = size.tiny, text = "𝓡", textcolor = color.gray)

plotshape(bullishbreakout ? low * 0.999 : na, " Bullish Breakout ", shape.diamond, location.belowbar, color.new(yellow, 0), size = size.tiny, text = "𝓑", textcolor = color.gray)

plotshape(bearishbreakout ? high * 1.001 : na, " Bearish Breakout ", shape.diamond, location.abovebar, color.new(yellow, 0), size = size.tiny, text = "𝓑", textcolor = color.gray)

This script is a versatile tool designed to aid in the identification of key reversal and breakout points, helping traders to make informed decisions based on technical analysis. Its customization options allow for a tailored analysis experience, fitting the unique needs and strategies of each trader.

Supertrend with Target Price & ATREE [SS]Hey everyone,

Releasing this supertrend mashup indicator.

This is your basic supertrend, but with two additions:

1. The integration of the ATREE technical probability modeller; and

2. The use of ATR price targets for crossovers

ATREE

ATREE stands for Advanced Technical Range Expectancy Estimator. It has its very own indicator available here . If you are not that familiar with it, I would suggest heading over to that page and reading about it, because it gives you the in-depth details.

But for a recap, ATREE uses technical indicators such as RSI, Stochastics or Z-Score to predict the likely sentiment, whether it be bullish or bearish. The indicator allows you to select the ATREE model type and supports 3 separate probability models based on either:

1. RSI

2. Stochastics; or

3. Z-Score

If you want to know which model is most effective for the ticker and timeframe you are using, you can launch up the native ATREE indicator and review the backtesting results to ascertain which model performs optimally for that particular ticker on that particular timeframe.

When ATREE assesses the sentiment as bearish, you will get a red fill. When it assesses the sentiment as bullish, you will get a green fill. This will help you adjust your bias to focus on either dip buying or rip shorting.

The ATREE timeframe is also customizable, so you can pull data from higher timeframes than you are on.

ATR Price Targets

As with my EMA 9/21 crossover with the target price, this is essentially the same concept. When the trend shifts to bullish or bearish, bull and bear targets will be printed so you know where to look for potential reversal and you can also set realistic target prices if you are scalping or day trading.

Supertrend

The last and base feature is the supertrend. The supertrend settings are customizeable.

It will provide a green line for uptrend and a redline for downtrend, the basic supertrend functionality.

And that's the indicator!

Let me know what you think and hope you enjoy!

Safe trades as always!

Squeeze Momentum TD - A Revisited Version of the TTM SqueezeDescription:

The "Squeeze Momentum TD" is our unique take on the highly acclaimed TTM Squeeze indicator, renowned in the trading community for its efficiency in pinpointing market momentum. This script is a tribute and an extension to the foundational work laid by several pivotal figures in the trading industry:

• John Carter, for his creation of the TTM Squeeze and TTM Squeeze Pro, which revolutionized the way traders interpret volatility and momentum.

• Lazybear, whose original interpretation of the TTM Squeeze, known as the "Squeeze Momentum Indicator", provided an invaluable foundation for further development.

• Makit0, who evolved Lazybear's script to incorporate enhancements from the TTM Squeeze Pro, resulting in the "Squeeze PRO Arrows".

Our script, "Squeeze Momentum TD", represents a custom version developed after reviewing all variations of the TTM Squeeze indicator. This iteration focuses on a distinct visualization approach, featuring an overlay band on the chart for an user-friendly experience. We've distilled the essence of the TTM Squeeze and its advanced version, the TTM Squeeze Pro, into a form that emphasizes intuitive usability while retaining comprehensive analytical depth.

Features:

-Customizable Bollinger Bands and Keltner Channels: These core components of the TTM Squeeze.

-Dynamic Squeeze Conditions: Ranging from No Squeeze to High Compression.

-Momentum Oscillator: A linear regression-based momentum calculation, offering clear insights into market trends.

-User-Defined Color Schemes: Personalize your experience with adjustable colors for bands and plot shapes.

-Advanced Alert System: Alerts for key market shifts like Bull Watch Out, Bear Watch Out, and Momentum shifts.

-Adaptive Band Widths: Modify the band widths to suit your preference.

How to use it?

• Transition from Light Green to Dark Green: Indicates a potential end to the bullish momentum. This 'Bull Watch Out' signal suggests that traders should be cautious about continuing bullish trends.

• Transition from Light Red to Dark Red: Signals that the bearish momentum might be fading, triggering a 'Bear Watch Out' alert. It's a hint for traders to be wary of ongoing bearish trends.

• Shift from Dark Green to Light Green: This change suggests an increase in bullish momentum. It's an indicator for traders to consider bullish positions.

• Change from Dark Red to Light Red: Implies that bearish momentum is picking up. Traders might want to explore bearish strategies under this condition.

• Rapid Change from Light Red to Light Green: This swift shift indicates a quick transition from bearish to bullish sentiment. It's a strong signal for traders to consider switching to bullish positions.

• Quick Shift from Light Green to Light Red: Demonstrates a speedy change from bullish to bearish momentum. It suggests that traders might want to adjust their strategies to align with the emerging bearish trend.

Acknowledgements:

Special thanks to Beardy_Fred for the significant contributions to the development of this script. This work stands as a testament to the collaborative spirit of the trading community, continuously evolving to meet the demands of diverse trading strategies.

Disclaimer:

This script is provided for educational and informational purposes only. Users should conduct their own due diligence before making any trading decisions.

Trend Change IndicatorThe Trend Change Indicator is an all-in-one, user-friendly trend-following tool designed to identify bullish and bearish trends in asset prices. It features adjustable input values and a built-in alert system that promptly notifies investors of potential shifts in both short-term and long-term price trends. This alert system is crucial for helping less active investors correctly position themselves ahead of major trend shifts and assists in risk management after a trend is established. It's important to note that this indicator is most effective with assets that historically exhibit strong trends.

At the heart of this tool is the interaction between the 30-day and 60-day Exponential Moving Averages (EMA). A bullish trend is indicated in green when the 30-day EMA is above the 60-day EMA, while a bearish trend is signaled in red when the 30-day EMA is below the 60-day EMA. The appearance of gray alerts users to potential shifts in the current trend as the EMAs converge, falling below the Average True Range (ATR) safety margin. This analysis is conducted across both hourly and daily timeframes, with the 4-hour timeframe providing early signals for daily trend changes. The band visually represents the interaction between the daily EMAs and is also displayed in the second row of the table, with the first row showing the same EMA interaction on the 4-hour timeframe.

This indicator also includes a 140-day (20-week) Simple Moving Average (SMA), visually represented by a line with predictive dots. This feature significantly enhances the investor's ability to understand long-term trends in asset prices, offering forward-looking insights by projecting the SMA value 10 days into the future. The value of this forecast lies in interpreting the slope of the dots; upward trending dots suggest a bullish underlying trend, while downward trending dots indicate a bearish trend. Generally, prices above the SMA signal bullishness, and prices below indicate bearishness.

In summary, the Trend Change Indicator is a comprehensive solution for identifying price trends and managing risk. Its intuitive, color-coded design makes it an indispensable tool for traders and investors who aim to be well-positioned ahead of trend shifts and manage risk once a trend has been established. While it has proven historically valuable in trending markets such as cryptocurrencies, tech stocks, and commodities, it is advisable to use this indicator in conjunction with other technical analysis tools for a more comprehensive and well-rounded decision-making process.

Machine Learning: STDEV Oscillator [YinYangAlgorithms]This Indicator aims to fill a gap within traditional Standard Deviation Analysis. Rather than its usual applications, this Indicator focuses on applying Standard Deviation within an Oscillator and likewise applying a Machine Learning approach to it. By doing so, we may hope to achieve an Adaptive Oscillator which can help display when the price is deviating from its standard movement. This Indicator may help display both when the price is Overbought or Underbought, and likewise, where the price may face Support and Resistance. The reason for this is that rather than simply plotting a Machine Learning Standard Deviation (STDEV), we instead create a High and a Low variant of STDEV, and then use its Highest and Lowest values calculated within another Deviation to create Deviation Zones. These zones may help to display these Support and Resistance locations; and likewise may help to show if the price is Overbought or Oversold based on its placement within these zones. This Oscillator may also help display Momentum when the High and/or Low STDEV crosses the midline (0). Lastly, this Oscillator may also be useful for seeing the spacing between the High and Low of the STDEV; large spacing may represent volatility within the STDEV which may be helpful for seeing when there is Momentum in the form of volatility.

Tutorial:

Above is an example of how this Indicator looks on BTC/USDT 1 Day. As you may see, when the price has parabolic movement, so does the STDEV. This is due to this price movement deviating from the mean of the data. Therefore when these parabolic movements occur, we create the Deviation Zones accordingly, in hopes that it may help to project future Support and Resistance locations as well as helping to display when the price is Overbought and Oversold.

If we zoom in a little bit, you may notice that the Support Zone (Blue) is smaller than the Resistance Zone (Orange). This is simply because during the last Bull Market there was more parabolic price deviation than there was during the Bear Market. You may see this if you refer to their values; the Resistance Zone goes to ~18k whereas the Support Zone is ~10.5k. This is completely normal and the way it is supposed to work. Due to the nature of how STDEV works, this Oscillator doesn’t use a 1:1 ratio and instead can develop and expand as exponential price action occurs.

The Neutral (0) line may also act as a Support and Resistance location. In the example above we can see how when the STDEV is below it, it acts as Resistance; and when it’s above it, it acts as Support.

This Neutral line may also provide us with insight as towards the momentum within the market and when it has shifted. When the STDEV is below the Neutral line, the market may be considered Bearish. When the STDEV is above the Neutral line, the market may be considered Bullish.

The Red Line represents the STDEV’s High and the Green Line represents the STDEV’s Low. When the STDEV’s High and Low get tight and close together, this may represent there is currently Low Volatility in the market. Low Volatility may cause consolidation to occur, however it also leaves room for expansion.

However, when the STDEV’s High and Low are quite spaced apart, this may represent High levels of Volatility in the market. This may mean the market is more prone to parabolic movements and expansion.

We will conclude our Tutorial here. Hopefully this has given you some insight into how applying Machine Learning to a High and Low STDEV then creating Deviation Zones based on it may help project when the Momentum of the Market is Bullish or Bearish; likewise when the price is Overbought or Oversold; and lastly where the price may face Support and Resistance in the form of STDEV.

If you have any questions, comments, ideas or concerns please don't hesitate to contact us.

HAPPY TRADING!

Trend Strength Over TimeThe script serves as an indicator designed to assess and visualize trend strength and Volume strength over time. It employs a variety of calculations and conditions to offer insights into both bullish and bearish market trends. Let's explore the key conceptual elements of the code.

Trend Strength Conditions:

The script defines conditions to assess trend strength based on a comparison between each calculated percentile value and the highest high (bullish) or lowest low (bearish). Separate conditions are established for each percentile length, allowing for a nuanced understanding of trend dynamics across different timeframes.

Counting Bull and Bear Trends:

To quantify the strength of bullish and bearish trends, the script maintains counts for the number of conditions that are true for each. This count-based approach provides a quantitative measure of trend strength.

Weak Bull and Bear Counts:

Recognizing that trends are not always clear-cut, the script introduces the concept of weak trends. It counts instances where the percentiles fall between the highest high and lowest low, indicating a potential weakening of the prevailing trend.

Bull and Bear Strength:

Bull and bear strengths are calculated based on the counts, with adjustments made for weak trends. This step provides a more nuanced and comprehensive assessment of trend strength by considering both strong and weak signals.

Current Trend Value:

The culmination of these calculations is the determination of the current trend value. This value represents the balance between bullish and bearish forces, offering a dynamic indicator of the market's prevailing sentiment.

Volume Strength Calculation:

In addition to price-based indicators, the script incorporates volume strength as a crucial element. This is calculated using the simple moving averages (SMAs) of volume over different lengths, normalized relative to the SMA over a length of 144. Volume strength adds a layer of confirmation or divergence to the price-based trend analysis.

Color Change:

To facilitate quick and intuitive interpretation, the script dynamically changes the color of the plotted line on the chart based on the current trend value. Green indicates a bullish trend, red indicates a bearish trend, and blue suggests a neutral or indecisive market.

Plotting:

The script uses the plot function to visually present the calculated trend strength and volume strength on the chart. This visual representation aids traders in making informed decisions based on the identified trends and their strengths.

Volume Strength: A Detailed Explanation

In the context of the provided script, volume strength is a critical component used to assess the strength of a market trend. It provides insights into the level of participation and commitment of market participants, offering a complementary perspective to traditional price-based indicators. Let's delve into the concept and practical applications of volume strength.

Calculation of Volume Strength:

The script calculates volume strength by considering the simple moving averages (SMAs) of volume over different time periods (13, 21, 34, 55, 89). These individual SMAs are then normalized relative to the SMA over a more extended period of 144. The weights assigned to each SMA in the calculation are defined in the variable VCF (Volume Correction Factor).

Calculation of Volume Strength with Weights: The weights assigned to each SMA in this calculation are crucial for emphasizing the significance of shorter-term volume movements relative to a longer-term baseline.

Interpretation of Weights:

The choice of weights reflects the relative importance of shorter-term volume movements compared to longer-term trends. In this script, shorter-term SMAs (13, 21, 34, 55, 89) are assigned decreasing weights, while the longer-term SMA (144) serves as the baseline.

Shorter-term SMAs with higher weights may have a more immediate impact on the volume strength calculation. This implies that recent changes in volume carry more weight in assessing the current market conditions.

The decreasing weights for shorter-term SMAs might indicate that, as the timeframe lengthens, the significance of recent volume movements diminishes in relation to the longer-term trend. This approach allows for a focus on both short-term volatility and longer-term stability in volume patterns.

The purpose of normalization is to emphasize the current volume's significance in comparison to its historical context. This can help identify abnormal volume spikes or sustained increases in trading activity, which may indicate the strength or weakness of a trend.

Interpretation and Practical Use:

Confirmation of Trend:

Rising volume during an uptrend can validate the strength of the upward movement, suggesting that a significant number of market participants are actively buying. Conversely, decreasing volume during an uptrend might indicate weakening interest and a potential reversal.

In a downtrend, increasing volume on downward price movements reinforces the strength of the trend. A decrease in volume during a downtrend may suggest a potential weakening or exhaustion of the downward momentum.

Divergence Analysis:

Divergence occurs when there is a disagreement between the price movement and the corresponding volume. For example, if prices are rising but volume is declining, it could signal a lack of conviction in the upward movement, and a reversal might be imminent.

Conversely, if prices are falling, but volume is decreasing as well, it might suggest that the downward momentum is losing steam, and a potential reversal or consolidation could be on the horizon.

In conclusion, volume strength analysis provides traders with a powerful tool to gauge the conviction behind price movements. By incorporating volume data into the technical analysis, one can make more informed decisions, enhance trend identification, and improve risk management strategies.

Liquidations Meter [LuxAlgo]The Liquidation Meter aims to gauge the momentum of the bar, identify the strength of the bulls and bears, and more importantly identify probable exhaustion/reversals by measuring probable liquidations.

🔶 USAGE

This tool includes many features related to the concept of liquidation. The two core ones are the liquidation meter and liquidation price calculator, highlighted below.

🔹 Liquidation Meter

The liquidation meter presents liquidations on the price chart by measuring the highest leverage value of longs and shorts that have been potentially liquidated on the last chart bar, hence allowing traders to:

gauge the momentum of the bar.

identify the strength of the bulls and bears.

identify probable reversal/exhaustion points.

Liquidation of low-leveraged positions can be indicative of exhaustion.

🔹 Liquidation Price Calculator

A liquidation price calculator might come in handy when you need to calculate at what price level your leveraged position in Crypto, Forex, Stocks, or any other asset class gets liquidated to add a protective stop to mitigate risk. Monitoring an open position gets easier if the trader can calculate the total risk in order for them to choose the right amount of margin and leverage.

Liquidation price is the distance from the trader's entry price to the price where trader's leveraged position gets liquidated due to a loss. As the leverage is increased, the distance from trader's entry price to the liquidation price shrinks.

While you have one or several trades open you can quickly check their liquidation levels and determine which one of the trades is closest to their liquidation price.

If you are a day trader that uses leverage and you want to know which trade has the best outlook you can calculate the liquidation price to see which one of the trades looks best.

🔹 Dashboard

The bar statistics option enables measuring and presenting trading activity, volatility, and probable liquidations for the last chart bar.

🔶 DETAILS

It's important to note that liquidation price calculator tool uses a formula to calculate the liquidation price based on the entry price + leverage ratio.

Other factors such as leveraged fees, position size, and other interest payments have been excluded since they are variables that don’t directly affect the level of liquidation of a leveraged position.

The calculator also assumes that traders are using an isolated margin for one single position and does not take into consideration the additional margin they might have in their account.

🔹Liquidation price formula

the liquidation distance in percentage = 100 / leverage ratio

the liquidation distance in price = current asset price x the liquidation distance in percentage

the liquidation price (longs) = current asset price – the liquidation distance in price

the liquidation price (shorts) = current asset price + the liquidation distance in price

or simply

the liquidation price (longs) = entry price * (1 – 1 / leverage ratio)

the liquidation price (shorts) = entry price * (1 + 1 / leverage ratio)

Example:

Let’s say that you are trading a leverage ratio of 1:20. The first step is to calculate the distance to your liquidation point in percentage.

the liquidation distance in percentage = 100 / 20 = 5%

Now you know that your liquidation price is 5% away from your entry price. Let's calculate 5% below and above the entry price of the asset you are currently trading. As an example, we assume that you are trading bitcoin which is currently priced at $35000.

the liquidation distance in price = $35000 x 0.05 = $1750

Finally, calculate liquidation prices.

the liquidation price (longs) = $35000 – $1750 = $33250

the liquidation price (short) = $35000 + $1750 = $36750

In this example, short liquidation price is $36750 and long liquidation price is $33250.

🔹How leverage ratio affects the liquidation price

The entry price is the starting point of the calculation and it is from here that the liquidation price is calculated, where the leverage ratio has a direct impact on the liquidation price since the more you borrow the less “wiggle-room” your trade has.

An increase in leverage will subsequently reduce the distance to full liquidation. On the contrary, choosing a lower leverage ratio will give the position more room to move on.

🔶 SETTINGS

🔹Liquidations Meter

Base Price: The option where to set the reference/base price.

🔹Liquidation Price Calculator

Liquidation Price Calculator: Toggles the visibility of the calculator. Details and assumptions made during the calculations are stated in the tooltip of the option.

Entry Price: The option where to set the entry price, a value of 0 will use the current closing price. Details are given in the tooltip of the option.

Leverage: The option where to set the leverage value.

Show Calculated Liquidation Prices on the Chart: Toggles the visibility of the liquidation prices on the price chart.

🔹Dashboard

Show Bar Statistics: Toggles the visibility of the last bar statistics.

🔹Others

Liquidations Meter Text Size: Liquidations Meter text size.

Liquidations Meter Offset: Liquidations Meter offset.

Dashboard/Calculator Placement: Dashboard/calculator position on the chart.

Dashboard/Calculator Text Size: Dashboard text size.

🔶 RELATED SCRIPTS

Here are some of the scripts that are related to the liquidation and liquidity concept, for more and other conceptual scripts you are kindly invited to visit LuxAlgo-Scripts .

Liquidation-Levels

Liquidations-Real-Time

Buyside-Sellside-Liquidity

TPG.Buy sell RSI Scapl XAUThis is a tool that is widely used

Especially for Overbought and Oversold systems, but I have made some changes in this indicator,

How to use it...

I have set it as the default setting

- RSI Length: 6 (<10 for scalping - 5m-15m)

- Overbought: 70

- Oversold: 30

What is unique about this tool?

we can see 3 conditions:

1) RSI Overbought / Oversold with Bullish Engulfing / Bearish Engulfing

2) RSI Overbought / Oversold with Hammer and Shooting Star

3) RSI Overbought / Oversold with 2 Bullish Bars / 2 Bearish Bars

4) RSI Overbought / Oversold with All Patterns at the same time

When the RSI reaches its Oversold line, the code will wait for Bullish Engulfing pattren, when oversold and Bullish engulfing matched, This indicator will generate a buy signal when the condition is met,

and same as for Bear market, When the RSI reaches its Overbought line, the code will wait for Bearish Engulfing pattren, This indicator will generate a sell/exit signal when the condition is met,

2nd condition is that a Hammer candle will be waited for when RSI touches the Overbought line, for Bullish Move

and Shooting Star candle will be waited for when RSI touches the Overbought line, for Bullish Move, for Bearish Move

3rd Condition is also the same as Condition 1 and Condition 2,

When the RSI reaches its Oversold line, the code will wait for 2 Bullish Bars, when oversold and 2 Bullish Bars matched then this indicator will generate a buy signal, and same as for Bear market,

When the RSI reaches its Overbought line, the code will wait for 2 Bearish Bars, when overbought and 2 Bearish Bars matched then this indicator will generate a Sell signal,

4th Condition is that we can use All Conditions at the same time,

- Bullish Engulfing / Bearish Engulfing

- Hammer and Shooting Star

- 2 Bullish Bars / 2 Bearish Bars

MADALGO`s Enhanced OBV DivergencesDescription:

MADALGO's Enhanced OBV Divergences indicator is a unique tool designed for traders to visualize the divergences between price action and On Balance Volume (OBV), a fundamental aspect often indicative of underlying strength or weakness in the market. By keenly identifying these divergences, traders are better positioned to anticipate potential trend reversals or trend continuations, making this script an invaluable addition to their technical analysis toolkit.

This script meticulously scans for both regular and hidden bullish/bearish divergences, providing a comprehensive view of market sentiment. The core of this indicator is built around the OBV, which cumulatively adds or subtracts volume based on the price movement per period, thus providing a running total of volume and portraying the force behind the price movements.

The regular divergences are classic indicators of a potential reversal in the current trend, while hidden divergences are often indicative of trend continuation. These divergences are pinpointed based on the relative positions of the OBV and price highs/lows, over customizable lookback periods and within specified lookback ranges.

Features:

Regular and Hidden Divergences: Clearly marked bullish and bearish divergences provide insights into potential market turning points.

On Balance Volume (OBV) Line: Visualize the continuous flow of buying and selling pressure, enabling the identification of accumulation or distribution phases essential for understanding the market's strength or weakness.

Moving Average of OBV: An optional feature to smooth the OBV line, aiding in the identification of the overarching trend.

Dynamic Statistics Label: A floating label provides real-time updates on essential statistics like the Rate of Percentage Change (RPC) of OBV, the last divergences, and bars since the last divergences.

Inputs:

Pivot Lookback Right and Pivot Lookback Left: Define the lookback periods for identifying pivot points in the OBV line.

Max of Lookback Range and Min of Lookback Range: Define the range for considering divergences.

RPC Period: Defines the period for calculating the Rate of Percentage Change of the OBV.

MA Period: Defines the period for the optional moving average of the OBV.

Plot Bullish, Plot Hidden Bullish, Plot Bearish, Plot Hidden Bearish: Toggle visibility of respective divergences.

Plot Moving Average: Toggle visibility of the OBV moving average.

Usage:

Add the script to your TradingView chart.

Tailor the input parameters in the settings panel to align with your analysis requirements.

The divergences, OBV line, and optional moving average will be plotted on your chart, with a dynamic label displaying real-time statistics.

Set up alerts to be notified of identified divergences, enabling timely decision-making.

Alerts:

Regular bullish/bearish divergence in OBV found: Triggered when a regular bullish or bearish divergence is identified.

Hidden bullish/bearish divergence in OBV found: Triggered when a hidden bullish or bearish divergence is identified.

Underlying Concepts:

The OBV Divergences indicator is rooted in the principle that volume precedes price movement. When prices are rising with increased volume, it suggests that buying pressure is prevailing and may lead to continued upward momentum. Conversely, rising prices with decreasing volume might indicate a lack of buying conviction and could signal a potential price reversal. The identification of divergences between price and OBV can therefore serve as a powerful signal for traders. These examples can be seen below in the image

The Moving Average of the OBV further aids in understanding the prevailing trend by smoothing out the OBV line, providing a clearer picture of the market's longer-term momentum. The Rate of Percentage Change (RPC) provides insight into the momentum of volume, offering an additional layer of analysis. Together, these additional features enhance the core OBV analysis, enabling a more nuanced understanding of volume dynamics fundamental for making more informed trading decisions.

License:

This Source Code Form is subject to the terms of the Mozilla Public License, v. 2.0. If a copy of the MPL was not distributed with this file, you can obtain one at Mozilla Public License 2.0.

TrendLine CrossThis indicator "TrendLine Cross", is designed to plot trend lines so you can spot potential trend reversal points on the charts. The main function is to draw several lines on the chart and identify the crossings between these lines, which can be significant indicators for trading. The lines are based on different periods which can be changed in the settings tabs.

Let's see the characteristics of the trend lines:

_Low Line Color(Green Line): This line connects the lowest point of low prices in the "low_time" period with the lowest point of low prices in the "high_time" period. Indicates a possible short-term support level on the chart.

_Liquidity Up Line Color (Golden Line): This line connects the lowest point of low prices in the "low_time" period with the highest point of low prices in the same period. It represents a liquidity zone and an important resistance in the chart.

_Lower Line Color (Blue Line): This horizontal line connects the lowest point of low prices in the "LowerLine_period" with the lowest point of low prices in the "high_time" period. Indicates a possible long-term support level.

_Upper Line Colorr: This line represents a connection between the highest points of the "high_time" period and the lowest point of the "LowerLine_period". Indicates a possible long-term resistance level.

_Up Line Color (Red Line): This line connects the highest point of high prices in the "high_time" period with the highest point of high prices in the "LowerLine_period". It represents a possible long-term resistance level.

_Liquidity Down Line Color(Golden Line): This line connects the highest point of high prices in the "high_time" period with the highest point of low prices in the "low_time" period. It represents a liquidity point and an important support zone.

The indicator becomes particularly interesting when the lines make crossings. These crossovers could suggest a potential trend change in the market. For example:

Change from Bearish to Bullish: If the "long-term" line (black) crosses the "short- or long-term" line (green or blue) from top to bottom, it could indicate a shift from a bearish to a bullish market , suggesting the opportunity for long positions.

_Changing from Bullish to Bearish: If the "long-term" line (blue) crosses the "short-term" line (red or black) from bottom to top, it could indicate a shift from a bullish to a bearish market, suggesting the opportunity for short positions.

Generally speaking, crossings between these lines can be key points of interest for traders, as they can signal significant changes in price direction.

Volatility Adjusted Composite RSI with SMA and EMA SignalsOverview

The script "VAC - RSI with SMA and EMA Signals" combines the traditional Relative Strength Index (RSI) with Time-based RSI (T-RSI), and adjusts it for volatility to create a Composite RSI (C-RSI). The script further uses Simple Moving Average (SMA) and Exponential Moving Average (EMA) to generate signals for potential trading opportunities. In the "VAC - RSI with SMA and EMA Signals" script, the combination of price, time, and volatility works as follows:

Price: The script calculates the traditional RSI based on price changes over a specified period.

Time: Alongside the price-based RSI, a Time-based RSI (T-RSI) is calculated, which considers the number of upward and downward closes over the same period.

Volatility: Volatility is integrated into the Composite RSI (C-RSI) by adjusting it with a Z-score based on a standard deviation of closing prices.

These three factors work together to create a more holistic and robust indicator.

How can it be used?

This script is used to identify potential overbought and oversold conditions in the market. It plots the VAC-RSI, SMA, and EMA on a chart, along with overbought and oversold levels, providing visual signals to the trader. When the EMA is below the SMA, it is a bullish signal, and vice versa for a bearish signal.

Default Values for Different Inputs:

Price RSI Weightage (%): 65

Unified Period for RSI & T-RSI: 14

C-RSI SMA Period: 13

C-RSI EMA Period: 33

C-RSI Bull Trend Support: 35

C-RSI Bear Trend Resistance: 65

Use Volatility Adjusted C-RSI (VAC-RSI): true

Standard Deviation Period: 14

Volatility Scaling Factor (α): 5

These values can be adjusted according to the trading strategy to optimize the signals for different assets or timeframes.

Strategies this Can be Used for:

The script can be used in various trading strategies including:

Trend Following: By observing the crosses of EMA and SMA, traders can follow the trend.

Reversion to the Mean: Using the overbought and oversold levels to identify potential reversal points.

Breakout: Identifying breakout points using the Bull and Bear Market Support and Resistance levels.

Comparison with the Standard Indicator: