Velocity SmartMoney Engine work - Delta Exchange📈 Velocity SmartMoney Engine

Adaptive Breakout & Order Block Strategy with Dynamic Risk Control

---

🔍 Overview

The Velocity SmartMoney Engine is a next-generation trading strategy that fuses Smart Money breakout logic , Order Block structure detection , and Supertrend-based directional filtering into one precision-built system.

It identifies institutional-level breakouts , manages positions with ATR-based adaptive risk , and executes disciplined exits using stop-loss, trailing stop, and profit target logic.

Designed for swing and short-term system traders, this strategy performs excellently on BTC, ETH, NIFTY, BANKNIFTY, Gold, and major FX pairs — best on 15m to 4h timeframes .

---

⚙️ Core Components

1️⃣ Smart Money Breakout Logic

Detects real breakouts using dynamic support/resistance pivots.

Confirms entries only during strong volatility bursts.

Avoids false breakouts in sideways markets.

2️⃣ Order Block Gap Detection

Finds institutional imbalance zones (Smart Money footprints).

Bullish gaps = Long bias; Bearish gaps = Short bias.

Works with candle confirmation and momentum validation.

3️⃣ Supertrend Directional Filter

Trades only in direction of Supertrend bias.

Exits instantly when Supertrend flips.

Prevents entries against dominant trend.

4️⃣ ATR-Based Risk & Volatility Filter

Uses ATR × multiplier for adaptive stop sizing.

Volatility filter ensures trades trigger only during active markets.

Avoids whipsaw zones.

---

💰 Position Management

Stop-Loss: Adaptive ATR-based.

Take-Profit: Default 5% target (editable input).

Trailing Stop: Auto-adjusts to lock profits.

No-Exit Hold: Hold position for defined candles before exits.

Supertrend Flip Exit: Instant trend-based closure.

---

🧠 Built-In Trade Discipline

One-trade-per-bar guard prevents duplicate entries.

Volatility-weighted breakout validation.

Clean and conflict-free exit hierarchy.

---

🎯 Key Features

✅ Smart Money breakout + Order Block fusion

✅ Supertrend-based trend confirmation

✅ ATR dynamic stop + 5% profit target

✅ Adaptive trailing logic

✅ One-trade-per-bar control

✅ Works across Crypto, Indices, FX, Commodities

✅ Ideal for 1h–4h swing setups

---

📊 Recommended Settings

Parameter | Typical Value | Purpose

--- | --- | ---

Levels Period | 20 | Pivot lookback for S/R zones

Volatility Filter | 20–40 | Filters out low-momentum areas

ATR Multiplier | 1.5 | Adjust stop size by volatility

Supertrend Length | 10 | ATR period for trend bias

Supertrend Multiplier | 3.0 | Supertrend sensitivity

Target Profit | 5% | Default take-profit level

---

⚡ Suggested Use

• Best suited for swing entries on 1H / 4H charts .

• Combine with session filters or trend confluence for automation.

• Ideal as a base module for TradingView + Broker integrations .

---

🧩 Disclaimer

This script is for educational purposes only .

Past performance does not guarantee future returns.

Use responsibly. The developer assumes no liability for financial losses.

---

💬 Community & Access

Developed by: Shubham Singh

Version: Velocity SmartMoney Engine v1.0

For premium modules & automation: DM "Velocity Access" on chat to request access.

---

© 2025 Velocity SmartMoney Engine — All Rights Reserved

스크립트에서 "bar"에 대해 찾기

FVG Strategy with One Trade Per Hour and Tick-based TP/SLThis strategy hunts for Fair Value Gaps (FVGs)—three-bar displacement gaps that mark imbalances where price moved so fast it left a “void.” It detects bullish (green) and bearish (red) FVGs on the chart timeframe or a higher timeframe you choose via the Timeframe input. Each detected zone is stored and optionally drawn as a box (static or “dynamic” that tightens with price). A simple threshold lets you filter out tiny gaps: either set a fixed percent (Threshold %) or let the script estimate it automatically. As price trades later, the engine watches for interaction with any stored zone.

Entries are taken on a touch/retest of the zone: buy when price intersects a green (bullish) FVG; short when it intersects a red (bearish) FVG. Risk management is manual and straightforward—your stop loss and take profit are set in ticks, placed off the signal bar’s close. To avoid over-trading, there’s a cap of one trade per hour (it resets when the clock hour changes). In short, it’s an intraday “gap fill / bounce” system: identify an imbalance, wait for price to revisit it, and take a directional trade with fixed tick targets and stops.

PSAR with ATR Trailing Stop + SMA Filter📈 Strategy Overview: PSAR + 6×ATR Trailing Stop with SMA Filter

This strategy is built around the principle of “Cut the losers, let the winners run” — a disciplined, trend-following approach that combines the Parabolic SAR indicator with dynamic risk management and a Simple Moving Average (SMA) trend filter.

🔍 Strategy Logic

Trend Filter Trades are only taken in the direction of the prevailing trend, defined by a user-selected SMA (default: 100).

✅ Long trades only when price is above the SMA

✅ Short trades only when price is below the SMA

Entry Signal: A trade is triggered when the Parabolic SAR flips to the opposite side of the price bars, signaling a potential trend reversal.

Stop Loss: The stop loss is dynamically set at 6×ATR from the entry price. This adapts to market volatility and is recalculated every bar — effectively acting as a trailing stop.

Exit Logic: There is no fixed take profit. The trade remains open until the trailing stop is hit — allowing winners to run and losers to be cut quickly.

Risk Management: Each trade risks 0.5% of total equity, ensuring consistent position sizing and capital preservation.

📊 Visual Elements

PSAR dots mark trend direction changes

SMA line shows the broader trend filter

Trailing stop crosses (with 50% opacity) indicate the current stop level without cluttering the chart

⚙️ Customizable Inputs

PSAR parameters: Start, Increment, Maximum

ATR length and multiplier

SMA length

Risk percentage per trade

This strategy is ideal for traders who want to stay aligned with the trend, automate disciplined exits, and avoid emotional decision-making. Clean, simple, and powerful.

Wishing you calm and successful trades!

量化多空策略 4H趋势+15M进场(高胜率高R:R·完整报警版)这是一套结合多周期结构(4小时趋势 + 15分钟入场)的量化交易策略,

核心理念是「顺势而为 + 动量二次确认 + 高R:R风险控制」。

策略特点:

• 使用 4H EMA 趋势判定方向

• 结合 15m RSI + MACD 动量信号确认入场

• 二次确认(2~3 根内突破 + 动量共振)过滤假信号

• 自适应止盈止损(基于 ATR 和 ADX)

• 全自动计算 R:R、冷却周期、成交量放大过滤

适用场景

• 加密货币(BTC、ETH、SOL、BNB 等)

• 黄金 / 外汇 / 指数CFD

• 15m~1h短线趋势盯盘

• 适合希望提高信号质量、过滤假突破的交易者

注意事项

• 该策略为研究与教学用途,不构成投资建议

• 实盘前请先在回测与模拟盘验证参数

• 适度调整「确认根数」「R:R」「ADX阈值」以适应不同市场波动性

This is a multi-timeframe quantitative trading strategy combining the 4-hour trend with 15-minute entry signals.

Its core philosophy is “Trend following + Momentum confirmation + High R:R risk control.”

Key Features

• Uses 4H EMA structure to determine market trend

• Combines 15m RSI + MACD momentum for entry confirmation

• Dual confirmation within 2–3 bars (breakout + momentum alignment) to filter false signals

• Adaptive take-profit and stop-loss based on ATR and ADX

• Automatically calculates Risk/Reward ratio, cooldown period, and volume expansion filters

Best Use Cases

• Cryptocurrencies (BTC, ETH, SOL, BNB, etc.)

• Gold / Forex / Index CFDs

• Short-term trend tracking (15m–1h)

• Traders aiming to improve signal quality and avoid false breakouts

Notes

• This strategy is for research and educational purposes only — not financial advice.

• Always backtest and paper trade before live deployment.

• Adjust confirmation bars, R:R ratio, and ADX threshold to suit different market volatilities.

US/SPY- Financial Regime Index Swing Strategy Credits: concept inspired by EdgeTools Bloomberg Financial Conditions Index (Proxy)

Improvements: eight component basket, inverse volatility weights, winsorization option( statistical technique used to limit the influence of outliers in a dataset by replacing extreme values with less extreme ones, rather than removing them entirely), slope and price gates, exit guards, table and gradients.

Summary in one paragraph

A macro regime swing strategy for index ETFs, futures, FX majors, and large cap equities on daily calculation with optional lower time execution. It acts only when a composite Financial Conditions proxy plus slope and an optional price filter align. Originality comes from an eight component macro basket with inverse volatility weights and winsorized return z scores that produce a portable yardstick.

Scope and intent

Markets: SPY and peers, ES futures, ACWI, liquid FX majors, BTC, large cap equities.

Timeframes: calculation daily by default, trade on any chart.

Default demo: SPY on Daily.

Purpose: convert broad financial conditions into clear swing bias and exits.

Originality and usefulness

Unique fusion: return z scores for eight liquid proxies with inverse volatility weighting and optional winsorization, then slope and price gates.

Failure mode addressed: false starts in chop and early shorts during easy liquidity.

Testability: all knobs are inputs and the table shows components and weights.

Portable yardstick: z scores center at zero so thresholds transfer across symbols.

Method overview in plain language

Base measures

Return basis: natural log return over a configurable window, standardized to a z score. Winsorization optional to cap extremes.

Components

EQ US and EQ GLB measure equity tone.

CREDIT uses LQD over HYG. Higher credit quality outperformance is risk off so sign is flipped after z score.

RATES2Y uses two year yield, sign flipped.

SLOPE uses ten minus two year yield spread.

USD uses DXY, sign flipped.

VOL uses VIX, sign flipped.

LIQ uses BIL over SPY, sign flipped.

Each component is smoothed by the composite EMA.

Fusion rule

Weighted sum where weights are equal or inverse volatility with exponent gamma, normalized to percent so they sum to one.

Signal rule

Long when composite crosses up the long threshold and its slope is positive and price is above the SMA filter, or when composite is above the configured always long floor.

Short when composite crosses down the short threshold and its slope is negative and price is below the SMA filter.

Long exit on cross down of the long exit line or on a fresh short signal.

Short exit on cross up of the short exit line or on a fresh long signal, or when composite falls below the force short exit guard.

What you will see on the chart

Markers on suggestion bars: L for long, S for short, LX and SX for exits.

Reference lines at zero and soft regime bands at plus one and minus one.

Optional background gradient by regime intensity.

Compact table with component z, weight percent, and composite readout.

Table fields and quick reading guide

Component: EQ US, EQ GLB, CREDIT, RATES2Y, SLOPE, USD, VOL, LIQ.

Z: current standardized value, green for positive risk tone where applicable.

Weight: contribution percent after normalization.

Composite: current index value.

Reading tip: a broadly green Z column with slope positive often precedes better long context.

Inputs with guidance

Setup

Calc timeframe: default Daily. Leave blank to inherit chart.

Lookback: 50 to 1500. Larger length stabilizes regimes and delays turns.

EMA smoothing: 1 to 200. Higher smooths noise and delays signals.

Normalization

Winsorize z at ±3: caps extremes to reduce one off shocks.

Return window for equities: 5 to 260. Shorter reacts faster.

Weighting

Weight lookback: 20 to 520.

Weight mode: Equal or InvVol.

InvVol exponent gamma: 0.1 to 3. Higher compresses noisy components more.

Signals

Trade side: Long Short or Both.

Entry threshold long and short: portable z thresholds.

Exit line long and short: soft exits that give back less.

Slope lookback bars: 1 to 20.

Always long floor bfci ≥ X: macro easy mode keep long.

Force short exit when bfci < Y: macro stress guard.

Confirm

Use price trend filter and Price SMA length.

View

Glow line and Show component table.

Symbols

SPY ACWI HYG LQD VIX DXY US02Y US10Y BIL are defaults and can be changed.

Realism and responsible publication

No performance claims. Past is not future.

Shapes can move intrabar and settle on close.

Execution is on standard candles only.

Honest limitations and failure modes

Major economic releases and illiquid sessions can break assumptions.

Very quiet regimes reduce contrast. Use longer windows or higher thresholds.

Component proxies are ETFs and indexes and cannot match a proprietary FCI exactly.

Strategy notice

Orders are simulated on standard candles. All security calls use lookahead off. Nonstandard chart types are not supported for strategies.

Entries and exits

Long rule: bfci cross above long threshold with positive slope and optional price filter OR bfci above the always long floor.

Short rule: bfci cross below short threshold with negative slope and optional price filter.

Exit rules: long exit on bfci cross below long exit or on a short signal. Short exit on bfci cross above short exit or on a long signal or on force close guard.

Position sizing

Percent of equity by default. Keep target risk per trade low. One percent is a sensible starting point. For this example we used 3% of the total capital

Commisions

We used a 0.05% comission and 5 tick slippage

Legal

Education and research only. Not investment advice. Test in simulation first. Use realistic costs.

Aurum DCX AVE Gold and Silver StrategySummary in one paragraph

Aurum DCX AVE is a volatility break strategy for gold and silver on intraday and swing timeframes. It aligns a new Directional Convexity Index with an Adaptive Volatility Envelope and an optional USD/DXY bias so trades appear only when direction quality and expansion agree. It is original because it fuses three pieces rarely combined in one model for metals: a convexity aware trend strength score, a percentile based envelope that widens with regime heat, and an intermarket DXY filter.

Scope and intent

• Markets. Gold and silver futures or spot, other liquid commodities, major indices

• Timeframes. Five minutes to one day. Defaults to 30min for swing pace

• Default demo used in this publication. TVC:GOLD on 30m

• Purpose. Enter confirmed volatility breaks while muting chop using regime heat and USD bias

• Limits. This is a strategy. Orders are simulated on standard candles only

Originality and usefulness

• Unique fusion. DCX combines DI strength with path efficiency and curvature. AVE blends ATR with a high TR percentile and widens with DCX heat. DXY adds an intermarket bias

• Failure mode addressed. False starts inside compression and unconfirmed breakouts during USD swings

• Testability. Each component has a named input. Entry names L and S are visible in the list of trades

• Portable yardstick. Weekly ATR for stops and R multiples for targets

• Open source. Method and implementation are disclosed for community review

Method overview in plain language

You score direction quality with DCX, size an adaptive envelope with a blend of ATR and a high TR percentile, and only allow breaks that clear the band while DCX is above a heat threshold in the same direction. An optional DXY filter favors long when USD weakens and short when USD strengthens. Orders are bracketed with a Weekly ATR stop and an R multiple target, with optional trailing to the envelope.

Base measures

• Range basis. True Range and ATR over user windows. A high TR percentile captures expansion tails used by AVE

• Return basis. Not required

Components

• Directional Convexity Index DCX. Measures directional strength with DX, multiplies by path efficiency, blends a curvature term from acceleration, scales to 0 to 100, and uses a rise window

• Adaptive Volatility Envelope AVE. Midline ALMA or HMA or EMA plus bands sized by a blend of ATR and a high TR percentile. The blend weight follows volatility of volatility. Band width widens with DCX heat

• DXY Bias optional. Daily EMA trend of DXY. Long bias when USD weakens. Short bias when USD strengthens

• Risk block. Initial stop equals Weekly ATR times a multiplier. Target equals an R multiple of the initial risk. Optional trailing to AVE band

Fusion rule

• All gates must pass. DCX above threshold and rising. Directional lead agrees. Price breaks the AVE band in the same direction. DXY bias agrees when enabled

Signal rule

• Long. Close above AVE upper and DCX above threshold and DCX rising and plus DI leads and DXY bias is bearish

• Short. Close below AVE lower and DCX above threshold and DCX falling and minus DI leads and DXY bias is bullish

• Exit and flip. Bracket exit at stop or target. Optional trailing to AVE band

Inputs with guidance

Setup

• Symbol. Default TVC:GOLD (Correlation Asset for internal logic)

• Signal timeframe. Blank follows the chart

• Confirm timeframe. Default 1 day used by the bias block

Directional Convexity Index

• DCX window. Typical 10 to 21. Higher filters more. Lower reacts earlier

• DCX rise bars. Typical 3 to 6. Higher demands continuation

• DCX entry threshold. Typical 15 to 35. Higher avoids soft moves

• Efficiency floor. Typical 0.02 to 0.06. Stability in quiet tape

• Convexity weight 0..1. Typical 0.25 to 0.50. Higher gives curvature more influence

Adaptive Volatility Envelope

• AVE window. Typical 24 to 48. Higher smooths more

• Midline type. ALMA or HMA or EMA per preference

• TR percentile 0..100. Typical 75 to 90. Higher favors only strong expansions

• Vol of vol reference. Typical 0.05 to 0.30. Controls how much the percentile term weighs against ATR

• Base envelope mult. Typical 1.4 to 2.2. Width of bands

• Regime adapt 0..1. Typical 0.6 to 0.95. How much DCX heat widens or narrows the bands

Intermarket Bias

• Use DXY bias. Default ON

• DXY timeframe. Default 1 day

• DXY trend window. Typical 10 to 50

Risk

• Risk percent per trade. Reporting field. Keep live risk near one to two percent

• Weekly ATR. Default 14. Basis for stops

• Stop ATR weekly mult. Typical 1.5 to 3.0

• Take profit R multiple. Typical 1.5 to 3.0

• Trail with AVE band. Optional. OFF by default

Properties visible in this publication

• Initial capital. 20000

• Base currency. USD

• request.security lookahead off everywhere

• Commission. 0.03 percent

• Slippage. 5 ticks

• Default order size method percent of equity with value 3% of the total capital available

• Pyramiding 0

• Process orders on close ON

• Bar magnifier ON

• Recalculate after order is filled OFF

• Calc on every tick OFF

Realism and responsible publication

• No performance claims. Past results never guarantee future outcomes

• Shapes can move while a bar forms and settle on close

• Strategies use standard candles for signals and orders only

Honest limitations and failure modes

• Economic releases and thin liquidity can break assumptions behind the expansion logic

• Gap heavy symbols may prefer a longer ATR window

• Very quiet regimes can reduce signal contrast. Consider higher DCX thresholds or wider bands

• Session time follows the exchange of the chart and can change symbol to symbol

• Symbol sensitivity is expected. Use the gates and length inputs to find stable settings

Open source reuse and credits

• None

Mode

Public open source. Source is visible and free to reuse within TradingView House Rules

Legal

Education and research only. Not investment advice. You are responsible for your decisions. Test on historical data and in simulation before any live use. Use realistic costs.

Moon Phases + Blood MoonWhat it is

This is a simple, time-based strategy that goes long on full moons and exits on the next new moon, while visually highlighting historically known “Blood Moon” (total lunar eclipse) dates. It’s built for exploratory testing of lunar timing effects on price, not for predictive claims.

Why it’s useful / originality

Most lunar scripts only mark phases. This one (1) computes lunar phases on the chart, (2) normalizes and flags Blood Moon days from a curated list, and (3) turns the phase changes into an executable strategy with clear, reproducible entry/exit rules and a configurable start date—so traders can quickly evaluate whether a lunar timing overlay adds any edge on their market/timeframe.

How it works (concept)

Moon phase detection: Uses Julian date conversion and standard astronomical approximations to determine the most recent phase change at each bar. The script classifies phase turns as +1 = New Moon and –1 = Full Moon, tracking the latest valid time to avoid lookahead.

Blood Moon tagging: A built-in array of UTC timestamps (total lunar eclipses) is date-matched to the current session and marked as “Blood Moon” when a full moon coincides with a listed date.

Signals & trades

Plot circles above/below bars: New Moon (above), Full Moon (below), Blood Moon (below, red).

Entry: Long at Full Moon once the bar time ≥ the user’s Start date.

Exit: Close the long on the next New Moon.

How to use

Add to your chart (non-monthly timeframes only).

Optionally adjust the Start date (default: 2001-12-31 UTC) to control the backtest window.

Use the color inputs to style New Moon / Full Moon / Blood Moon markers.

Evaluate performance on liquid symbols and timeframes that provide a sufficient number of phase cycles.

Default / publish settings

Initial capital: $10,000 (suggested)

Commission: 0.05% per trade (suggested)

Slippage: 1 tick (suggested)

Position sizing: TradingView strategy defaults (no leverage logic is added).

Timeframes: Intraday/Daily/Weekly supported. Monthly is blocked by design.

Chart type: Use standard chart types only (no Heikin Ashi, Renko, Kagi, P&F, Range) for signals/backtests.

Reading the chart

New Moon: soft gray circle above bars.

Full Moon: soft yellow circle below bars.

Blood Moon (if date-matched): soft red circle below bars.

The script also ensures symbol/timeframe context is visible—keep your chart clean so the markers are easy to interpret.

Limitations & important notes

This is a time-based heuristic. It does not forecast price and does not repaint via lookahead tricks; it avoids future leakage by anchoring to the last known phase time at each bar.

No non-standard chart signals. Using non-standard charts can produce unrealistic results.

Strategy properties like commission/slippage materially affect results—please set them to realistic values.

Backtests should include a large sample (ideally >100 trades over many cycles) to make statistics meaningful.

Past performance does not guarantee future results.

Open-source reuse / credits

Uses standard, public-domain techniques for Julian date conversion and lunar-phase approximations.

Blood Moon dates are incorporated as a hard-coded list for convenience; you may extend or adjust this list as needed.

No third-party proprietary code is reused.

Changelog / versioning

v1: Initial public release on Pine v6 with phase detection, Blood-Moon tagging, and a minimal long-only phase strategy.

Twisted Forex's Doji + Area StrategyTitle

Twisted Forex’s Doji + Area Strategy

Description

What this strategy does

This strategy looks for doji candles forming inside or near supply/demand areas . Areas are built from swing pivots and sized with ATR, then tracked for retests (“confirmations”). When a doji prints close to an area and quality checks pass, the strategy places a trade with the stop beyond the doji and a configurable R:R target.

How areas (zones) are built

• Swings are detected with a user-set pivot length.

• Each swing spawns a horizontal area centered at the pivot price with half-height = zoneHalfATR × ATR .

• Duplicates are de-duplicated by center distance (ATR-scaled).

• Areas fade when broken beyond a buffer or after an optional age (expiry).

• Retests are recorded when price touches and then bounces away from the area; repeated reactions increase the zone’s “strength”.

Signal logic (summary)

Doji detection: strict or loose body criteria with optional minimum wick fractions and ATR-scaled minimum range.

Proximity: price must be inside/near a supply or demand area (proxATR × ATR).

Side resolution: overlap is resolved by (a) which side price penetrates more, (b) fast/slow EMA trend, or (c) nearest distance. Optional “previous candle flip” can bias long after a bearish candle and short after a bullish one.

Optional 1-bar confirmation: the bar after the doji must close away from the area by confirmATR × ATR .

Quality filter (Off/Soft/Strict): four checks—(i) wick rejection past the edge, (ii) doji closes in an edge “band” of the area, (iii) fresh touch (cooldown), (iv) approach impulse over a short lookback. In Strict , thresholds auto-tighten.

Orders & exits

• Long: stop below doji low minus buffer; Short: above doji high plus buffer.

• Target = rrMultiple × risk distance .

• Pyramiding is off by default.

Position sizing

You can size from the script or from Strategy Properties:

• Script-driven (default): set Position sizing = “Risk % of equity” and choose riskPercent (e.g., 1.0%). The script applies safe floors/rounding (FX micro-lots by default) so quantity never rounds to zero.

• Properties-driven : toggle Use TV Properties → Order size ON, then pick “Percent of equity” in Properties (e.g., 1%). The header includes safe defaults so trades still place.

Key inputs to explore

• Zone building : pivotLen, zoneHalfATR, minDepartureATR, expiryBars, breakATR, leftBars, dedupeATR.

• Doji & proximity : strictDoji, dojiBodyFrac, minWickFrac, minRangeATR, proxATR, minBarsBetween.

• Overlap resolution : usePenetration, useTrend (EMA 21/55), “previous candle flip”, needNextBarConf & confirmATR.

• Quality : qualityMode (Off/Soft/Strict), minQualPass/kStrict, wickPenATR, edgeBandFrac, approachLookback, approachMinATR, freshTouchBars.

• Zone strength gating : minStrengthSoft / minStrengthStrict.

• HTF confluence (optional) : useHTFTrend (HTF EMA 34/89) and/or useHTFZoneProx (HTF swing bands).

Tips to make it cleaner / higher quality

• Turn needNextBarConf ON and use confirmATR = 0.10–0.15 .

• Increase approachMinATR (e.g., 0.35–0.45) to require a stronger pre-touch impulse.

• Raise minStrengthSoft/Strict (e.g., 4–6) so only well-reacted zones can signal.

• Use signalsOnlyConfirmed ON if you prefer trades only from zones with retests (the script falls back gracefully when none exist yet).

• Nudge proxATR to 0.5–0.6 to demand tighter proximity to the level.

• Optional: enable useHTFTrend to filter counter-trend setups.

Default settings used in this publication

• Initial capital: 100,000 (illustrative).

• Slippage: 1 tick; Commission: 0% (you can raise commission if you prefer—spread is partly modeled by slippage).

• Sizing: Risk % of equity via inputs; riskPercent = 1.0% ; FX uses micro-lot floors by default.

• Quality: Off by default (Soft/Strict available).

• HTF trend gate: Off by default.

Backtesting notes

For a meaningful sample size, test on liquid symbols/timeframes that yield 100+ trades (e.g., majors on 5–15m over 1–2 years). Backtests are modelled and broker costs/spread vary—validate on your feed and forward-test.

How to read the chart

Shaded bands are supply (above) and demand (below). Brighter bands are the nearest K per side (visual aid). BUY/SELL labels mark entries; colored dots show entry/SL/TP levels. You can hide zones or unconfirmed zones for a cleaner view.

Disclaimer

This is educational material, not financial advice. Trading involves risk. Always test and size responsibly.

Trend-Following & Breakout — Index Quant Strategy (NASDAQ)📈 Trend-Following & Breakout — Index Quant Strategy (NASDAQ & S&P 500)

Type: Invite-only strategy

Markets: NASDAQ 100 (NAS100 / US100 / NQ), S&P 500 (US500 / SPX), and other major equity indices.

🧠 Concept: Continuous trend model combining EWMAC (trend-following) and Donchian (breakout) signals, scaled by forecast strength and portfolio risk.

⚙️ Execution: Rebalances only on decision-bar closes, using hysteresis and a no-trade band to reduce churn.

📊 Default bias: Long-only — aligned with equity index drift.

🧩 How it works

• EWMAC Trend: Difference between fast and slow EMAs, normalized by an EWMA of absolute returns.

• Donchian Breakout: Distance beyond a 200-bar channel (Strict mode) or relative z-score position within it.

• Forecast combination: Weighted sum of trend and breakout points, clamped to ± capPoints.

• Hysteresis: Prevents quick sign flips near zero forecast.

• Risk scaling: Maps forecast strength to position size using equity × risk budget × ATR-based stop distance.

• Rebalance: Executes only if the required quantity change exceeds the Δqty threshold; can optionally block increases on Sundays (for CFDs).

⚙️ Default parameters

Deployed on NQ / US100 / NAS100 on Daily Timeframe

• Decision timeframe = 360 min (other options from 1 min to 1 week).

• Trend (EWMAC): Fast = 64, Slow = 256, Vol Norm = 32, Weight = 0.8.

• Breakout (Donchian): Length = 200, Mode = Strict, Weight = 0.2.

• Forecast scaling: ptsPerSigma = 1.0, capPoints = 10.

• Risk % per rebalance = 4 % of equity.

• ATR stop: ATR(14) × 1.0.

• No-trade band (Δqty) = 4 units.

• Hysteresis = 2 forecast points.

• Bias = Long-only (Neutral / Long-bias 50 % optional).

• Skip Sunday increases = false (default).

📋 Backtest properties (documented)

• Initial capital = 100 000 USD.

• Commission = 0.20 % per trade.

• Pyramiding = 10.

• Calc on every tick = false.

• Point value = 1 (for NAS100 CFD).

• No financing or slippage modeled.

• If using CFDs, account for overnight funding.

• On futures (NQ / ES), carry is implicit.

📊 Typical behaviour

• Many small scratches, a few large winners.

• Performs best during multi-week / multi-month trends.

• Underperforms in tight or volatile ranges.

• Average hold ≈ 30 – 90 days in historical tests.

💡 Risk and performance guide (illustrative)

Sharpe ≈ 1.25

Sortino ≈ 1.10 – 1.30

Max drawdown ≈ –18 % to –25 %

Annual volatility ≈ 24 – 28 %

CAGR ≈ 50 – 60 % (at 4 % risk)

Edge ratio ≈ 5 (MFE / MAE)

Historical backtests only — past performance does not guarantee future results.

🌍 Intended markets and timeframes

Optimized for NASDAQ 100 and S&P 500; also effective on similar indices (DAX, Dow Jones, FTSE).

Best on Daily or higher timeframes.

Aligns with long-term index drift — suitable for long-bias systematic trend portfolios.

⚠️ Limitations

• Backtests exclude CFD funding costs.

• Trend models will have losing streaks in range-bound markets.

• Designed for experienced traders seeking systematic exposure.

🔑 Requesting access

Send a private TradingView message to with the text:

“Request access to Trend-Following & Breakout — Index Quant Strategy.”

Access is granted only on explicit request.

For further information, see my TradingView Signature.

🆕 Release notes (v1.0)

• Initial release (360 min TF): EWMAC 64/256 + Donchian 200 Strict.

• Risk 4 %, ATR × 1.0, Long-only bias, hysteresis 2 pts, Δqty ≥ 4.

• Developed for NASDAQ 100 and S&P 500 indices.

• Implements continuous risk-scaled positioning and no-trade band logic.

🧾 Originality statement

This strategy is original work built entirely from TradingView built-ins (EMA, ATR, Highest, Lowest).

It does not reuse open-source invite-only code.

Any future reuse of open scripts will be done with explicit permission and credit.

Kootch Moon Phase Strategy🌙 Moon Phases Equity Strategy

This strategy explores the relationship between lunar cycles and equity price action.

It is based on a simple idea: markets may respond differently around New Moons and Full Moons.

🛠 How it works

• New Moon → Long Entry

The strategy enters a long position at the first bar after a New Moon event.

• Full Moon → Exit

The strategy closes the long position at the first bar after the following Full Moon.

• Optional Filters

• 200-day Moving Average (on by default): only take longs in bullish regimes.

• ATR-based Stops & Targets: risk management can be added with configurable multiples of ATR.

• Minimum Gap: ensures a cooldown period between trades to avoid clustering.

• Position Sizing: by default, trades risk a configurable % of equity (set to 35%).

📊 Notes

• This script is designed for equities (stocks, ETFs).

• It is a long-only system by default. If you enable “Always Flip,” the script will alternate long/short each lunar phase, but that is more experimental.

• Results can vary widely depending on the underlying asset. Trending stocks (e.g., AMZN, AAPL, SPY) tend to perform better with the long-only mode.

• Risk/Reward tracking in R-multiples is included for more consistent performance evaluation.

⚠️ Disclaimer

This strategy is for educational and research purposes only. It does not guarantee profitability and should not be used as financial advice. Past performance does not indicate future results. Always backtest on your preferred instruments and use sound risk management.

SRFRZ EMA Crossover with RSI StrategySRFRZ EMA Crossover with RSI Strategy

1. Overview

Strategy Name: SRFRZ EMA Crossover with RSI Strategy

Summary: A trend-following strategy designed for Indian stock and index markets, operating on any timeframe (optimized for 1H or 4H charts). It combines a 9-period and 21-period EMA crossover with RSI confirmation to identify high-probability long entries during the Indian trading session (9:15 AM–3:25 PM IST). Backtested with a fixed 20% capital allocation per trade, 3% stop loss, and 50% take profit, it aims for consistent returns in trending markets.

Intended Audience: Intermediate traders familiar with EMA and RSI, seeking automated signals for Indian markets.

2. How It Works (Core Logic)

Entry Conditions (Long/Buy Signal):

Primary Trigger: A "Golden Cross" occurs when the 9-period EMA crosses above the 21-period EMA, signaling bullish momentum.

RSI Confirmation: RSI (14-period) must be above 55, or cross above 55, to confirm strong momentum.

Trend Filter: The 9-period EMA must remain above the 21-period EMA for delayed RSI-triggered entries.

Session Filter: Trades are only executed during the Indian market session (9:15 AM–3:25 PM IST, Monday–Friday).

Exit Conditions:

Take Profit (TP): Fixed at 50% above the entry price (e.g., entry at ₹100, TP at ₹150).

Stop Loss (SL): Fixed at 3% below the entry price (e.g., entry at ₹100, SL at ₹97).

Indicator-Based Exit: Close the position if a "Death Cross" occurs (21-period EMA crosses above 9-period EMA).

Position Sizing: Allocates 20% of initial capital (₹100,000 default) per trade, calculated as (initial_capital * 0.20) / entry_price.

3. Key Indicators & Parameters

Primary Indicators:

EMA (9-period): Fast-moving average to capture short-term trends (plotted in blue).

EMA (21-period): Slower-moving average for trend confirmation (plotted in red).

RSI (14-period): Measures momentum, with a threshold of 55 for bullish confirmation (plotted in purple).

Customizable Settings in Pine Script:

initial_capital: Default ₹100,000 (adjust based on your account size).

qty_percent: Default 20% of capital per trade (adjust for risk tolerance).

sl_percent: Default 3% stop loss (adjust for volatility).

tp_percent: Default 50% take profit (adjust for reward targets).

session_time: Default "0915-1525:1234567" (Indian session, adjustable for other markets).

Default Values: Optimized for Indian stocks/indices (e.g., NIFTY 50) on 1H or 4H charts.

Risk Management:

Always use the built-in 3% stop loss.

Avoid trading during major news events (e.g., RBI announcements), as Pine Script cannot filter these.

Risk only 20% of capital per trade to diversify exposure.

Pro Tips:

Combine with support/resistance levels for manual confirmation.

Test on a demo account to validate performance on your chosen asset.

Monitor RSI for overbought conditions (>70) to anticipate reversals.

4. Visuals on Chart

Plotted Indicators:

Blue line: 9-period EMA.

Red line: 21-period EMA.

Purple line: RSI (14-period) in a separate pane.

Trade Signals:

Green triangle (below bar): Long entry.

Red triangle (above bar): Long exit (via TP, SL, or Death Cross).

5. Disclaimer & Notes

Risk Warning: Past performance is not indicative of future results. Trading involves significant risk. This strategy is for educational purposes only and is not financial advice.

Customization: The script is open-source (modify freely). Fork it to add short-selling logic or additional filters.

Note: The strategy avoids trades during non-session hours but cannot filter news events. Manually check economic calendars.

Add the script to your chart and adjust inputs (e.g., capital, TP/SL percentages).

Enable alerts for "Long Entry" and "Long Exit TP/SL" or "EMA Exit" to automate signals.

Optionally, connect to a broker via webhooks for auto-trading (consult your broker’s API).

Elliott Wave Auto + Fib Targets + Scalper Strategy (Fixed)// Elliott Wave Auto + Fib Targets + Scalper Strategy

//

// Fixed by expert trader:

// - Replaced table with label-based visualization to avoid 'Column 2 is out of table bounds' error.

// - Uses label.new to display buy/sell signal counts in top-right corner, mimicking table layout.

// - Fixed array.sum() error: Replaced invalid range-based array.sum() with custom sum_array_range() function.

// - Removed barstate usage to fix 'Undeclared identifier barstate' error.

// - Replaced barstate.isconfirmed with true (process every bar).

// - Replaced barstate.isfirstconfirmed with bar_index == 0 (first bar).

// - Replaced strategy.alert with label.new for long/short entry signals (buy/sell markers).

// - Fixed array index out-of-bounds: Protected array.get() calls with size checks.

// - Fixed pyramiding: Set constant pyramiding=4 (max 5 entries); use allow_pyramiding to limit entries.

// - Fixed default_qty_value: Set constant default_qty_value=100.0; use entry_size_pct to scale qty.

// - Replaced alertcondition with labels for Elliott Wave patterns.

// - Fixed partial exits: 50% at TP1 with fixed SL, 50% at TP2 with fixed SL or trailing.

// - Fixed Elliott Wave pivot indexing for alternating H/L check.

// - Ensured proper position sizing and exit logic.

Alpha SignalsThis strategy is designed to highlight potential short-term market setups using a fast and slow EMA crossover system on a 5-minute chart. It provides visual signals directly on the chart to help traders observe trend changes and potential entry points.

Key Features:

EMA Crossover Entries – The strategy enters long trades when the fast EMA crosses above the slow EMA and short trades when the fast EMA crosses below the slow EMA.

Time-Based Exits – Trades are automatically closed after a configurable number of bars to manage exposure.

Visual Alerts – Buy and sell signals are displayed as labels directly on the chart for easy interpretation.

Configurable Settings – Users can adjust fast and slow EMA lengths as well as the exit bar count to suit their trading preferences.

Usage:

Suitable for short-term traders focusing on the NQ1 futures contract or other instruments with similar volatility.

Can be used for observation, back testing, or as a confirmation tool alongside other strategies.

Does not guarantee profitability; intended for educational purposes and strategy testing only.

EMA Crossover Cloud w/Range-Bound FilterA focused 1-minute EMA crossover trading strategy designed to identify high-probability momentum trades while filtering out low-volatility consolidation periods that typically result in whipsaw losses. Features intelligent range-bound detection and progressive market attention alerts to help traders manage focus and avoid overtrading during unfavorable conditions.

Key Features:

EMA Crossover Signals: 10/20 EMA crossovers with volume surge confirmation (1.3x 20-bar average)

Range-Bound Filter: Automatically detects when price is consolidating in tight ranges (0.5% threshold) and blocks trading signals during these periods

Progressive Consolidation Stages: Visual alerts progress through Range Bound (red) → Coiling (yellow) → Loading (orange) → Trending (green) to indicate market compression and potential breakout timing

Market Attention Gauge: Helps manage focus between active trading and other activities with states: Active (watch close), Building (check frequently), Quiet (check occasionally), Dead (handle other business)

Smart RSI Exits: Cloud-based and RSI extreme level exits with conservative stop losses

Dual Mode Operation: Separate settings allow full backtesting performance while providing visual stay-out warnings for manual trading

How to Use:

Entry Signals: Trade aqua up-triangles (long) and orange down-triangles (short) when they appear with volume confirmation

Stay-Out Warnings: Ignore gray "RANGE" triangles - these indicate crossovers during range-bound periods that should be avoided

Monitor Top-Right Display:

Range: Current 60-bar dollar range

Attention: Market activity level for focus management

Status: Consolidation stage (trade green/yellow, avoid red, prepare for orange)

Position Sizing: Default 167 shares per signal, optimized for the crossover frequency

Alerts: Enable consolidation stage alerts and market attention alerts for automated notifications

Recommended Settings:

Timeframe: 1-minute charts

Symbol: Optimized for volatile stocks like TSLA

"Apply Filter to Backtest": Keep OFF for realistic backtesting, ON to see filtered results

Risk Management:

The strategy includes built-in overtrading protection by identifying and blocking trades during low-volatility periods. The progressive consolidation alerts help identify when markets are "loading" for significant moves, allowing traders to position appropriately for higher-probability setups.

CoinGpt NQ策略# CoinGpt NQ 策略(MACD·多因子·可金字塔)

## 概述

**CoinGpt NQ策略**是一套面向 **纳指期货 NQ(建议:`CME_MINI:NQ1!`)30 分钟** 的可运行交易策略。

核心以 **MACD 趋势动量** 为骨架,叠加 **EMA 趋势过滤**、**可选金字塔加仓**、**三种出场模式(固定 TP/SL、追踪、追踪+TP)** 与 **风控上限**,提供三套一键预设(Balanced / Trend / Scalper),满足不同市场状态与风险偏好。

> 适配:期货/连续合约;仅做多(本脚本版本)。

> 时间框架:**30m**(可在“仅在 30m 生效”开关控制)。

---

## 进场逻辑

* **信号触发**:`MACD 上穿 Signal`(并要求直方图连续上升 2 根)。

* **趋势过滤**:价格位于 `EMA(p_emaLen)` 上方,且 `MACD>0 & Signal>0`(可关闭)。

* **时间框架限制**:默认仅在 30m 有效(可关闭)。

## 出场逻辑

* **固定 TP/SL**:按百分比计算限价止盈与止损。

* **追踪止盈**:默认以 **ATR 偏移** 跟踪;

* **追踪 + TP**:在拖尾的同时设置上沿 TP。

* **反向保护**:`MACD 下穿 Signal` 时市价平仓。

> 出场模式在输入项 **「出场模式」** 选择:

> `Auto(by preset) / Fixed TP/SL / Trailing / Trailing + TP`

---

## 金字塔加仓(可选)

* 仅在已有多单且不利回撤达到阈值时触发;

* 最多 `p_maxAdds` 层;每层在 **上次加仓价** 基础上按 `p_addStep%` 回撤触发;

* 目的:**拉低均价、提高持仓性价比**;采用小步长、有限层数控制回撤风险。

---

## 风险管理

* **当日最大亏损**:`strategy.risk.max_intraday_loss(p_maxDailyDD, %权益)`

* **单笔头寸上限**:`strategy.risk.max_position_size(p_posCapPct)`

* **订单量**(策略属性):默认 **90% 权益**。

* 实盘更建议:Balanced≈**40%**、Trend≈**35%**、Scalper≈**30%**(在“策略属性 → 订单大小”中调整)。

---

## 三套预设(参数一键生效)

| 预设 | MACD(fast/slow/signal) | 趋势EMA | 金字塔 | 加仓步长 | 固定TP/SL(%) | 追踪(ATR倍数) | 单笔上限 | 当日亏损 |

| ---------------- | ---------------------- | ----- | --- | ----- | ----------------- | --------- | ---- | ---- |

| **Balanced(默认)** | 8 / 21 / 5 | 233 | 2 层 | 0.12% | TP 0.22 / SL 0.15 | 1.2× | 50% | 1.5% |

| **Trend** | 10 / 24 / 7 | 200 | 3 层 | 0.10% | TP 0.25 / SL 0.18 | 1.6× | 45% | 1.2% |

| **Scalper** | 6 / 19 / 4 | 100 | 关闭 | —— | TP 0.18 / SL 0.12 | 1.3× | 35% | 1.0% |

> 说明:

>

> * Balanced:均衡型,适合多数时期;

> * Trend:顺势拉伸,持仓更久、盈亏比更高;

> * Scalper:快进快出、高胜率、不过度叠仓。

---

## 使用建议

1. **品种/周期**:`CME_MINI:NQ1!`(或当季主力合约),**30m**。

2. **手续费**:本策略默认 **1 USD/合约**(在“策略属性”可按实盘成本调整)。

3. **成交精度**:建议在“策略属性 → 高级设置”勾选 **Bar Magnifier**,提升限价/拖尾成交模拟精度。

4. **仓位**:策略默认 90% 仅为展示;回测与实盘更建议 **30%\~40% 权益**。

5. **风险**:金字塔仅做轻量、有限层数;若市场极端震荡,适当降低单笔上限与当日亏损阈值。

---

## 输入项(TradingView 右侧面板)

* **参数预设**:`Balanced / Trend / Scalper`

* **仅在 30m 周期生效**:开/关

* **出场模式**:`Auto(by preset) / Fixed TP/SL / Trailing / Trailing + TP`

> 其余细节参数由预设自动注入,无需手动繁杂调整,**开箱即用**。

---

## 注意事项

* 本脚本为研究与教育用途,不构成投资建议。期货与杠杆交易风险高,请在可承受范围内使用。

* 预设适配历史统计特征,未来表现不保证;建议结合自身风控与账户规模,先小仓/纸面验证。

* 仅做多版本;若需要双向(多空)或加入 RTH(美股盘中)/HTF(更高周期确认)等扩展,请在评论区留言。

---

**作者注**:

* 本策略在 Pine v6 编写,避免了常见的 v6 语法踩坑(如 `strategy.risk.max_position_size()` 仅 1 参、`plot` 标题需常量、追踪需成对参数 `trail_price + trail_offset` 等)。

* 欢迎在评论区反馈你的回测截图(区间、手续费、订单量),我会根据数据给出更贴合你的参数档。

# CoinGpt NQ Strategy (MACD · Multi-Factor · Optional Pyramiding)

## Overview

**CoinGpt NQ Strategy** is a ready-to-trade system for **Nasdaq-100 futures (NQ; recommended: `CME_MINI:NQ1!`) on the 30-minute timeframe**.

It uses **MACD momentum** as the backbone, adds an **EMA trend filter**, optional **pyramiding**, and **three exit modes** (Fixed TP/SL, Trailing, Trailing+TP) with built-in risk caps. Three one-click presets—**Balanced / Trend / Scalper**—cover different regimes and risk appetites.

> Instruments: futures / continuous contract

> Direction: **Long-only** (this script version)

> Timeframe: **30m** (toggleable)

---

## Entry

* **Trigger:** `MACD` line crossing **above** `Signal`.

* **Trend filter (optional):** price above `EMA(p_emaLen)` and `MACD > 0 & Signal > 0`.

* **Timeframe guard:** by default, signals are valid on **30m** only.

## Exit

* **Fixed TP/SL:** percentage-based limit and stop.

* **Trailing:** ATR-based trailing offset (or percent).

* **Trailing + TP:** trailing stop **and** a take-profit cap.

* **Protective flip:** when `MACD` crosses **below** `Signal`, close the long.

> Choose exit mode in **Inputs → “Exit Mode”**:

> `Auto(by preset) / Fixed TP/SL / Trailing / Trailing + TP`.

---

## Pyramiding (optional)

* Adds only **against adverse pullbacks** from the last add price.

* Up to `p_maxAdds` layers; each layer triggers at `p_addStep%` pullback from the **previous add**.

* Goal: **improve average price** with **small steps & limited layers** to keep drawdowns controlled.

---

## Risk Management

* **Daily loss cap:** `strategy.risk.max_intraday_loss(p_maxDailyDD, % of equity)`.

* **Per-trade size cap:** `strategy.risk.max_position_size(p_posCapPct)`.

* **Order size (strategy properties):** default **90% of equity** (for display).

* Practical suggestion: Balanced ≈ **40%**, Trend ≈ **35%**, Scalper ≈ **30%** (set in Strategy Properties → Order size).

---

## Presets (one-click)

| Preset | MACD (fast/slow/signal) | Trend EMA | Pyramiding | Add Step | Fixed TP/SL (%) | Trailing (ATR) | Pos Cap | Daily DD |

| ---------------------- | ----------------------- | --------- | ---------- | -------- | ------------------------- | -------------- | ------- | -------- |

| **Balanced (default)** | 8 / 21 / 5 | 233 | 2 layers | 0.12% | TP **0.22** / SL **0.15** | **1.2×** | **50%** | **1.5%** |

| **Trend** | 10 / 24 / 7 | 200 | 3 layers | 0.10% | TP **0.25** / SL **0.18** | **1.6×** | **45%** | **1.2%** |

| **Scalper** | 6 / 19 / 4 | 100 | Off | — | TP **0.18** / SL **0.12** | **1.3×** | **35%** | **1.0%** |

> **Balanced:** all-weather, stable.

> **Trend:** holds longer and targets higher R multiples.

> **Scalper:** quick in/out, higher hit-rate, no stacking.

---

## Usage Tips

1. **Symbol/TF:** `CME_MINI:NQ1!`, **30m**.

2. **Fees:** default **\$1 per contract** (adjust to your broker in Strategy Properties).

3. **Execution realism:** enable **Bar Magnifier** (Strategy Properties → Advanced) for more accurate limit/trailing fills.

4. **Sizing:** the script defaults to 90% only to showcase behavior—use **30–40%** in realistic tests.

5. **Pyramiding:** keep layers small & capped. In choppy regimes, reduce `p_posCapPct` and `p_maxDailyDD`.

---

## Inputs (right-panel)

* **Param Preset:** `Balanced / Trend / Scalper`

* **30m-only:** on/off

* **Exit Mode:** `Auto(by preset) / Fixed TP/SL / Trailing / Trailing + TP`

> All other parameters are pre-wired by the chosen preset for **plug-and-play** operation.

---

## Notes & Disclaimer

* Educational use only—**not** financial advice. Futures and leverage carry substantial risk.

* Presets reflect historical characteristics; **future performance is not guaranteed**. Start small or paper trade first.

* This version is **long-only**; if you need a two-sided (long & short) variant or extras (RTH/HTF filters), leave a comment.

---

**Author Notes**

* Written in **Pine v6** with common pitfalls avoided (e.g., `strategy.risk.max_position_size()` takes **one** arg, `plot` titles are **const strings**, trailing requires `trail_price + trail_offset`).

* Share your backtest screenshots (period, fees, order size) and I can suggest **tighter, data-driven knobs** for your setup.

TheWave + Supertrend Hybrid w/ Signals• Green triangle below bar → Long entry signal

• Red triangle above bar → Short entry signal

• Small lime cross above/below → Take-profit hit

• Small maroon cross above/below → Stop-loss hit

• SMA5 and Supertrend lines for trend context

This version makes all entries and exits visually obvious while keeping the hybrid TheWave + Supertrend logic intact.

Turtle 20-Day Breakout + ATR (v6 Clean)20-bar breakout entries

ATR protective stops

Classic 10-bar opposite breakout exits

Proper plotting of breakout levels and stops

Signals on chart

Alert conditions in global scop

Intraday Alpha Pro - ORB + Trend/MomentumOverview

This is a pure intraday trading strategy designed for active traders seeking to capitalize on short-term price movements using two complementary modules: Opening Range Breakout (ORB) and Trend/Momentum. The strategy operates strictly within a user-defined trading session, automatically flattening all positions at session end to avoid overnight carry. It employs a points-based exit system with a trailing stop that activates only after the target is reached, ensuring disciplined risk management. Optional Martingale position sizing is included for users who prefer aggressive scaling after losses.Key Features Pure Intraday, No Carry: Trades are confined to a user-defined session (default: 9:15 AM–3:25 PM, Monday–Sunday). All positions are closed at session end.

Non-Repainting: Entries are evaluated only on confirmed bar closes (barstate.isconfirmed), ensuring no lookahead or repainting.

Dual Signal Modules: Opening Range Breakout (ORB): Captures breakouts above/below the high/low of a user-defined opening range (default: 9:15 AM–9:30 AM).

Trend/Momentum: Combines EMA (9/21) crossovers, RSI filters, volume confirmation, and an optional 200-period MA trend filter for robust trend-following signals.

Points-Based Exits: Uses fixed stop-loss (slPoints, default 16 points) and take-profit (tpPoints, default 32 points) distances. Once the take-profit level is reached, a trailing stop (trailDistPts, default 10 points) activates, ratcheting monotonically to lock in gains.

Martingale Sizing (Optional): Allows position size increases after losses (up to maxQtyInput) with a reset option after wins.

Cooldown Period: Prevents immediate re-entries after exits using a configurable cooldown (cooldownBars).

Flexible Inputs: Toggle long/short entries, enable/disable ORB or Trend/Momentum modules, and customize all parameters (e.g., MA lengths, RSI thresholds, volume multiplier).

Visuals & Alerts: Plots ORB high/low lines and moving averages (9, 21, 200). Includes alerts for long/short entries and end-of-day flattening.

How It Works Session Management: Trades only within the specified tradeSes (default: 9:15 AM–3:25 PM). The ORB module uses a separate orbSes (default: 9:15 AM–9:30 AM) to calculate breakout levels. Positions are closed automatically at session end.

Entry Conditions: ORB: Long when price closes above the ORB high after the ORB session ends; short when price closes below the ORB low.

Trend/Momentum: Long on fast MA (default EMA 9) crossing above slow MA (default EMA 21), with RSI above rsiBuy (default 55), volume exceeding volMult (default 1.5x prior bar), and price above the 200-period MA (if enabled). Shorts use the inverse.

Exit Logic: Stop-loss is set at entry price ± slPoints.

Take-profit is monitored using a running high/low since entry. Once price moves tpPoints in profit, the stop trails at trailDistPts behind the current price, adjusting only in the favorable direction (never loosening).

Exits use strategy.exit with stop only (no limit orders).

Position Sizing: Default size is baseQtyInput (minimum 1 contract). With useMartingale enabled, size increases by martingaleFactor after a loss, capped at maxQtyInput. If resetOnWin is true, size resets to baseQtyInput after a winning trade.

Cooldown: After an exit, no new trades are allowed for cooldownBars to prevent overtrading.

Futures-Safe Volume: Volume filter accommodates markets with missing or zero volume data (e.g., futures), ensuring signals aren’t blocked unnecessarily.

Inputs Trading Session: tradeSes (e.g., "0915-1525:1234567") and orbSes (e.g., "0915-0930:1234567").

Toggles: enableLong, enableShort, useORB, useTrendMom, useTrendFilter (200-MA).

Trend/Momentum: maType (EMA/SMA), fastLen (9), slowLen (21), trendLen (200), rsiLen (14), rsiBuy (55), rsiSell (45), volMult (1.5).

Exits: slPoints (16), tpPoints (32), trailDistPts (10).

Martingale: useMartingale, baseQtyInput, maxQtyInput, martingaleFactor, resetOnWin.

Cooldown: cooldownBars (1).

Legacy (Ignored): tp1RR, tp2RR, tp3RR, tp1Pct, tp2Pct, tp3Pct, stepTrail for backward compatibility.

Usage Notes Best suited for liquid, intraday markets (e.g., futures like ES, NQ, or forex pairs).

Adjust slPoints, tpPoints, and trailDistPts to match instrument volatility.

Use useMartingale cautiously, as it increases risk after losses.

Ensure tradeSes and orbSes align with your market’s trading hours.

Alerts can be set for long/short entries and EOD flattening.

The strategy avoids lookahead and repainting, ensuring reliability in live trading.

Risk Warning

Trading involves significant risk. Backtest thoroughly and use appropriate risk management. The Martingale option can amplify losses if not carefully monitored. Past performance is not indicative of future results.

FVG Ultra Assertive - Individual Filters (mtbr)FVG Ultra Assertive - Individual Filters (mtbr)

What this script offers:

This strategy detects and highlights FVGs (Fair Value Gaps) on the chart, providing traders with a visual and systematic approach to identify potential price inefficiencies. The script plots bullish and bearish FVG zones using customizable boxes and labels, allowing users to easily spot high-probability trading areas. In addition, it opens and closes simulated trades based on the detected FVGs, enabling full backtesting and strategy performance evaluation. It integrates multiple independent filters to validate the strength of each FVG signal before entering a trade.

How it works:

The script identifies:

Bullish FVGs when the current low is higher than the high of two bars ago.

Bearish FVGs when the current high is lower than the low of two bars ago.

Once an FVG is detected, it applies three optional independent filters:

GAP/ATR Filter:

Measures the FVG size relative to the Average True Range (ATR). Only gaps exceeding a user-defined multiple of ATR are considered valid.

Support/Resistance (S/R) Filter:

Uses pivot points to check if the FVG overlaps with recent high/low pivot levels within a tolerance percentage. This ensures the gap aligns with meaningful market levels.

Stochastic Filter:

Applies a stochastic oscillator to confirm momentum. Bullish FVGs are validated when stochastic values are oversold, and bearish FVGs when overbought.

After passing the selected filters, the strategy opens trades:

LONG FVG for bullish signals (buy)

SHORT FVG for bearish signals (sell)

The strategy automatically closes positions when an opposite signal appears, generating a backtest report with trades, profits, and statistics. The final bullish or bearish FVG signals are plotted as colored boxes on the chart with labels “BULL FVG” or “BEAR FVG” for immediate visual reference.

How to configure it for use:

Use GAP/ATR Filter: Enable or disable the ATR-based filter and adjust the ATR period (ATR Length) and minimum gap multiplier (Minimum Gap x ATR).

Use S/R Filter: Enable or disable the pivot-based S/R filter. Configure the pivot lookback periods (Pivot Left and Pivot Right) and the tolerance percentage (Gap Tolerance %).

Use Stochastic Filter: Enable or disable stochastic confirmation. Adjust the K and D lengths (Stoch K Length and Stoch D Length) and the overbought/oversold thresholds (Stoch Overbought and Stoch Oversold).

Colors: Customize the colors for bullish and bearish FVGs (FVG Bull and FVG Bear) to match your chart preferences.

Usage Tips:

Apply this strategy to any timeframe; shorter timeframes generate more frequent FVGs, while higher timeframes highlight stronger gaps.

Combine FVG signals with other technical analysis tools for better trade confirmation.

Use the box and label visualization to quickly scan charts for trade opportunities without cluttering the chart.

The strategy’s trades (LONG and SHORT) provide backtesting results and performance statistics for each signal.

3-Candle Reversal Pattern-vahid2star3-Candle Reversal Zones + Hammer Confirmation (with Risk Management & Alerts)

This script combines 3-candle reversal detection, hammer confirmations, and smart demand/supply zone plotting into a single tool designed for both discretionary and automated traders.

🔍 Core Logic

3-Candle Reversal Pattern

Candle-1: Strong move in one direction (big body).

Candle-2: Doji-like candle (high shadow/body ratio).

Candle-3: Reversal candle in the opposite direction (large body relative to Candle-2).

A gap after Candle-3 is required for extra confirmation.

Hammer Confirmation (Hammer-1 & Hammer-2)

After a valid 3-candle setup, the script searches for a hammer pattern near the zone.

Hammer-1: Draws a box directly on the hammer range if followed by a strong confirming candle.

Hammer-2: If another hammer forms after the confirmation candle and holds for N bars (configurable), a second hammer box is drawn.

Demand & Supply Zones

For bullish setups, a demand zone is created from the Candle-2 low to the Candle-1 low.

For bearish setups, a supply zone is created from the Candle-2 high to the Candle-1 high.

Zones extend to the right until price interacts with them.

🛠 Filters & Quality Controls

Trend filter (optional):

Only draw zones if price respects higher-timeframe EMA200 slope and LTF EMA alignment.

Market structure filter:

Require higher-high / higher-low (for bullish) or lower-high / lower-low (for bearish).

ATR filter:

Zones must have a minimum height relative to ATR.

Overlap control:

Avoid drawing zones that overlap too heavily with existing ones.

Cooldown:

Restrict consecutive zones of the same type within a user-defined bar distance.

🎯 Risk Management & Strategy

Dynamic position sizing:

Trade size is automatically calculated from account equity, risk %, and leverage.

Stop-loss & Take-profit:

SL placed just beyond the zone ± buffer ticks.

TP automatically set at user-defined Reward:Risk ratio (e.g., 3:1).

Capital protection:

Trades respect max leverage and risk per position settings.

⚡ Alerts

The script provides one-time alerts for each zone:

🔔 First Touch Alert → Triggered when price first touches a demand, supply, or hammer box.

Each zone only fires one alert, avoiding duplicates on re-touch or trade exit.

📊 Visuals

Demand zones: Green boxes.

Supply zones: Red boxes.

Hammer boxes: Blue (bullish) / Orange (bearish).

Used zones: Greyed out after price fills them.

Outcomes: Zones change to green if TP is hit, red if SL is hit.

Optional labels mark “Bullish zone ✓”, “Bearish zone ✓”, “Hammer-1 ✓”, or “Hammer-2 ✓” when confirmed.

🔧 Settings Overview

Core pattern ratios (C1/C2, C3/C2 size multipliers).

Doji definition (shadow/body ratio).

Hammer search depth, confirmation delay, and strictness.

Risk % per trade, leverage cap, stop buffer, RR ratio.

Visual styling (colors, max box count, labels).

Trend, structure, ATR, overlap, and cooldown filters.

Option to disable orders (use as indicator + alerts only).

⚠️ Disclaimer

This script is a technical analysis tool intended for educational purposes.

It does not guarantee profits. Use proper risk management and test thoroughly before applying in live trading.

✨ With its combination of 3-candle reversals, hammer confirmations, and smart filtering, this script is designed to reduce noise, highlight high-probability zones, and give traders both visual structure and actionable alerts.

MACD StrategyOverview

The "MACD Strategy" is a straightforward trading strategy tested for BTCUSDT Futures on the 1-minute timeframe, leveraging the Moving Average Convergence Divergence (MACD) indicator to identify momentum-based buy and sell opportunities. Developed with input from expert trading analyst insights, this strategy combines technical precision with risk management, making it suitable for traders of all levels on platforms like TradingView. It focuses on capturing trend reversals and momentum shifts, with clear visual cues and automated alerts for seamless integration with trading bots (e.g., Bitget webhooks).

#### How It Works

This strategy uses the MACD indicator to generate trading signals based on momentum and trend direction:

- **Buy Signal**: Triggered when the MACD line crosses above the signal line, and the MACD histogram turns positive (above zero). This suggests increasing bullish momentum.

- **Sell Signal**: Triggered when the MACD line crosses below the signal line, and the MACD histogram turns negative (below zero), indicating growing bearish momentum.

Once a signal is detected, the strategy opens a position (long for buy, short for sell) with a position size calculated based on your risk tolerance. It includes a stop-loss to limit losses and a take-profit to lock in gains, both dynamically adjusted using the Average True Range (ATR) for adaptability to market volatility.

#### Key Features

- **MACD-Based Signals**: Relies solely on MACD for entry points, plotted in a separate pane for clear momentum analysis.

- **Risk Management**: Automatically calculates position size based on a percentage of your account balance and sets stop-loss and take-profit levels using ATR multipliers and a risk:reward ratio.

- **Visual Feedback**: Plots entry, stop-loss, and take-profit lines on the chart with labeled markers for easy tracking.

- **Alerts**: Includes Bitget webhook-compatible alerts for automated trading, notifying you of buy and sell signals in real-time.

#### Input Parameters

- **Account Balance**: Default 10000 – Set your initial trading capital to determine position sizing.

- **MACD Fast Length**: Default 12 – The short-term EMA period for MACD sensitivity.

- **MACD Slow Length**: Default 26 – The long-term EMA period for MACD calculation.

- **MACD Signal Length**: Default 9 – The smoothing period for the signal line.

- **Risk Per Trade (%)**: Default 3.0 – The percentage of your account balance risked per trade (e.g., 3% of 10000 = 300).

- **Risk:Reward Ratio**: Default 3.0 – The ratio of potential profit to risk (e.g., 3:1 means risking 1 to gain 3).

- **SL Multiplier**: Default 1.0 – Multiplies ATR to set the stop-loss distance (e.g., 1.0 x ATR).

- **TP Multiplier**: Default 3.0 – Multiplies ATR to set the take-profit distance, adjusted by the risk:reward ratio.

- **Line Length (bars)**: Default 25 – Duration in bars for displaying trade lines on the chart.

- **Label Position**: Default 'left' – Position of text labels (left or right) relative to trade lines.

- **ATR Period**: Default 14 – The number of periods for calculating ATR to measure volatility.

#### How to Use

1. **Add to Chart**: Load the "MACD Strategy" as a strategy and the "MACD Indicator" as a separate indicator on your TradingView chart (recommended for BTCUSDT Futures on the 1-minute timeframe).

2. **Customize Settings**: Adjust the input parameters based on your risk tolerance and market conditions. For BTCUSDT Futures, consider reducing `Risk Per Trade (%)` during high volatility (e.g., 1%) or increasing `SL Multiplier` for wider stops.

3. **Visual Analysis**: Watch the main chart for trade entry lines (green for buy, red for sell), stop-loss (red), and take-profit (green) lines with labels. Use the MACD pane below to confirm momentum shifts.

4. **Set Alerts**: Create alerts in TradingView for "Buy Signal" and "Sell Signal" to automate trades via Bitget webhooks.

5. **Backtest and Optimize**: Test the strategy on historical BTCUSDT Futures 1-minute data to fine-tune parameters. The short timeframe requires quick execution, so monitor closely for slippage or latency.

#### Tips for Success

- **Market Conditions**: This strategy performs best in trending markets on the 1-minute timeframe. Avoid choppy conditions where MACD crossovers may produce false signals.

- **Risk Management**: Start with the default 3% risk per trade and adjust downward (e.g., 1%) during volatile periods like BTCUSDT news events. The 3:1 risk:reward ratio targets consistent profitability.

- **Timeframe**: Optimized for 1-minute charts; switch to 5-minute or 15-minute for less noise if needed.

- **Confirmation**: Cross-check MACD signals with price action or support/resistance levels for higher accuracy on BTCUSDT Futures.

#### Limitations

- This strategy relies solely on MACD, so it may lag in fast-moving or sideways markets. Consider adding a secondary filter (e.g., RSI) if needed.

- Stop-loss and take-profit are ATR-based and may need adjustment for BTCUSDT Futures’ high volatility, especially during leverage trading.

#### Conclusion

The "MACD Strategy" offers a simple yet effective way to trade momentum shifts using the MACD indicator, tested for BTCUSDT Futures on the 1-minute timeframe, with robust risk management and visual tools. Whether you’re scalping crypto futures or exploring short-term trends, this strategy provides a solid foundation for automated or manual trading. Share your feedback or customizations in the comments, and happy trading!

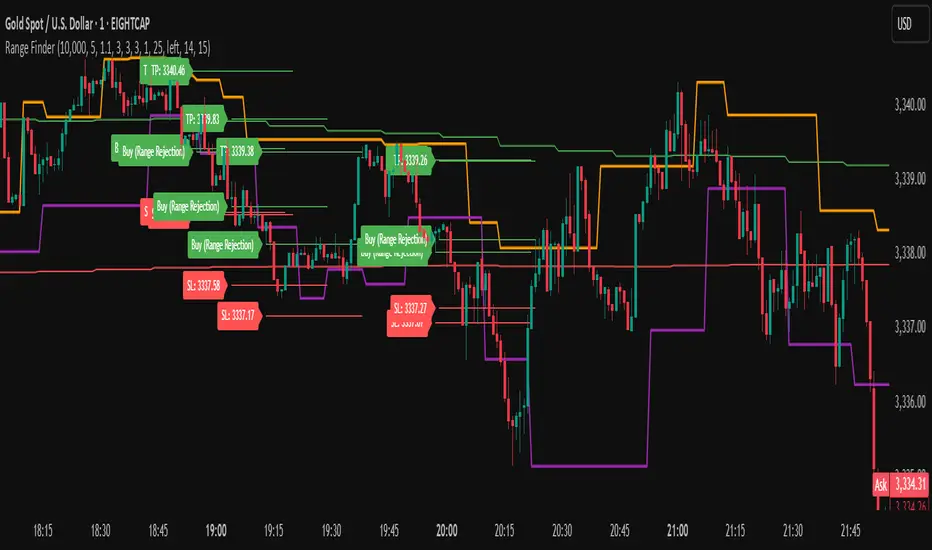

Range FinderRange Finder Strategy for TradingView

Overview

The Range Finder Strategy is a sophisticated trading system designed for forex and cryptocurrency markets, leveraging dynamic range detection, wick-based rejection patterns, and EMA confluence to execute high-probability trades. This strategy identifies key price ranges using pivot points and triggers trades when price rejects from these boundaries with significant wick formations, aligning with the broader market trend as confirmed by EMA crossovers. It incorporates robust risk management, customizable parameters, and visual aids for clear trade visualization, making it suitable for both manual and automated trading on platforms like Bitget via webhook alerts.

Strategy Components

1. Dynamic Range Detection

Pivot Points: The strategy identifies range boundaries using pivot highs and lows, calculated with a user-defined Pivot Length (default: 5 bars left/right). These pivots mark significant swing points, defining the upper (range high) and lower (range low) boundaries of the price range.

Visualization: The range high is plotted as an orange line, and the range low as a purple line, using a broken line style (plot.style_linebr) to show only confirmed pivot levels, providing a clear visual of the trading range.

2. Wick-Based Rejection Pattern

Wick Detection: The strategy looks for rejection candles at the range boundaries, characterized by significant wicks. A wick is considered valid if its size is at least the user-defined Wick to Body Ratio (default: 1.1, or 10% larger than the candle body).

Sell Signal: Triggered when the high exceeds the range high, the candle closes bearish (close < open), and the upper wick meets the ratio requirement.

Buy Signal: Triggered when the low falls below the range low, the candle closes bullish (close > open), and the lower wick meets the ratio requirement.

Purpose: These wicks indicate strong rejection at key levels, often signaling a reversal back into the range, providing high-probability entry points.

3. EMA Trend Confirmation

EMA Calculation: Uses two Exponential Moving Averages (EMAs) calculated on a user-selectable timeframe (default: 5-minute):

EMA 200: Long-term trend indicator (plotted in red).

EMA 50: Short-term trend indicator (plotted in green).

Crossover Logic:

A bullish trend is confirmed when the EMA 50 crosses above the EMA 200 (ema_trend_up = true).

A bearish trend is confirmed when the EMA 50 crosses below the EMA 200 (ema_trend_down = true).

Confluence Requirement: Trades are only executed when the wick rejection aligns with the EMA trend (e.g., sell signals require close < ema200 and bearish trend; buy signals require close > ema200 and bullish trend).

4. Risk Management

Position Sizing: Calculated based on the user-defined Account Balance (default: $10,000) and Risk Per Trade (default: 2%). The position size is determined as risk_amount / stop_distance, where stop_distance is derived from the Average True Range (ATR, default period: 14).

Stop Loss (SL): Set using an ATR-based multiplier (SL Multiplier, default: 9.0). For sells, SL is placed above the high; for buys, below the low.

Take Profit (TP): Set using an ATR-based multiplier (TP Multiplier, default: 6.0) scaled by the Risk:Reward Ratio (default: 6.0), ensuring a favorable reward-to-risk profile.

Example: For a $10,000 account with 2% risk, if ATR is 0.5, the position size is 400 units, with SL and TP dynamically adjusted to market volatility.

5. Trade Execution

Sell Entry: Triggered on a wick rejection above the range high, with bearish EMA confluence (ema_trend_down and close < ema200). Enters a short position with calculated SL and TP.

Buy Entry: Triggered on a wick rejection below the range low, with bullish EMA confluence (ema_trend_up and close > ema200). Enters a long position with calculated SL and TP.

Exit Logic: Uses strategy.exit to set SL and TP levels, closing trades when either is hit.

6. Visual Feedback

Lines and Labels: Upon trade entry, the strategy plots:

Red SL line and label (e.g., "SL: 123.45").

Green TP line and label (e.g., "TP: 120.00").

Entry line (red for sell, green for buy) labeled with "Sell (Range Rejection)" or "Buy (Range Rejection)".

Customization: Users can adjust the Line Length (default: 25 bars) for how long lines persist and Label Position (left or right) for optimal chart visibility.

7. Alert Conditions

Webhook Integration: Generates alerts for Bitget webhook integration, providing JSON-formatted messages with trade details (action, contracts, market position, size, price, symbol, and timestamp).

Usage: Traders can set up automated trading by connecting these alerts to trading bots or platforms supporting webhooks.

Close Above/Below Prev 2 Candle Strategy (Any Timeframe)Title: Close Above/Below Previous 2 Candle Strategy (Any Timeframe)

Description:

This strategy identifies potential breakout and trend continuation signals by analyzing the closing price relative to the highs and lows of the previous two candles. It works on any chart timeframe, making it versatile for intraday, swing, and daily trading.

How it works:

Long Entry (Bullish Signal): Triggered when the current candle closes above the highs of the previous two candles.

Short Entry (Bearish Signal): Triggered when the current candle closes below the lows of the previous two candles.

Visual Indicators:

Green triangles above the bar indicate bullish signals.

Red triangles below the bar indicate bearish signals.

Strategy Features:

Works on any timeframe, from 1-minute charts to daily/weekly charts.

Configurable risk/reward ratio for automatic stop-loss and take-profit levels.

Alerts trigger immediately when the condition is met, helping traders react to potential breakouts.

Provides clean visual signals for easy chart reading and decision-making.

Benefits:

Reduces noise by focusing on candle close confirmations.

Versatile and suitable for intraday, swing, and long-term trading.

Easy to combine with other indicators or strategies.