Bozz Strategy

Booz Backtesting : Booz Backtesting is a method for analyzing the performance of your current trading strategy . Booz Backtesting aims to help you generate results and evaluate risk and return without risking real capital.

The Booz Backtesting is the Booz Super Swing Indicator equivalent but gives you the ability to backtest data on different charts.

This is an Indicator created for the purpose of identifying trends in Multiple Markets, it is based on Moving Average Crossover and extra features.

Swing Trading: This function allows you to navigate the entire trend until it is not strong enough, so you can compare it with fixed parameters such as Take Profit and Stop Loss.

Take Profit and Stop Loss function: With this function you will be able to choose the most optimal parameters and see in real time the results in order to choose the best combination of parameters.

Leverage : We have this function for the futures markets where you can check which is the most appropriate leverage for your operation.

Trend Filter: allows you to take multiple entries in the same direction of the market.

If the market crosses below the 200 moving average, it will take only short entries.

If the market crosses above the 200 moving average, it will take only long entries.

Timeframes

Charting from 1 Hour, 4 Hour, Daily, Weekly, Weekly

Markets :Booz Backtesting can be tested in Cryptocurrency, Stocks and Futures markets.

Background Color : at a glance, you can see what cycle the market is in.

Green background : Shows that the market is in a bullish cycle.

Red background: Shows that the market is in a bearish cycle.

Twitter

Website

Search in scripts for "backtest"

Heikin Ashi Candle Startegy for Long PositionThis strategy utilize Heikin-Ashi candlestick chart.

Heikin-Ashi technique is a Japanese candlestick-based technical trading tool that uses candlestick charts to represent and visualize market price data.

Heikin-Ashi candle is essentially taking an average of the movement.

There is a tendency with Heikin-Ashi for the candles to stay red during a downtrend and green during an uptrend.

This strategy only apply for long trading position.

The idea is trader will waiting 3 green candles for validation period (confirmation) before entering long position.

Different timeframe will result different result.

Number of validation period can be changed to see different result

This strategy has parameter for take profit percentage, trailing stop and stop loss.

User can set maximum active position to minimize risk and qty order.

This tool is useful for user who wants to backtest Heikin-Ashi trading strategy.

Script will emit alert when long position is opened and closed.

Warning of Backtesting

Backtesting is backward-looking. As the name implies, you are testing how something would have worked if you traded it perfectly in the past.

Past performance does not indicate future performance and you should not assume it does.

Backtesting assumes you never miss-fire, that you get in and out at the exactly perfect moment each time.

Backtesting assumes you have perfect liquidity, and your limit orders fill at a specific, pre-defined price every time (either the open, close, low, high, or some average of these).

Disclaimer

Do your own research and consider fundamental price of asset.

The indicators provided on this script is for educational purposes only.

Author does not offer advisory or brokerage services, nor does it recommend or advise users to buy or sell particular stocks or securities.

Please examined script and give feedback for further improvement.

Script are open to public, everyone see and clone source code or just apply to chart. Please make comment for improvement.

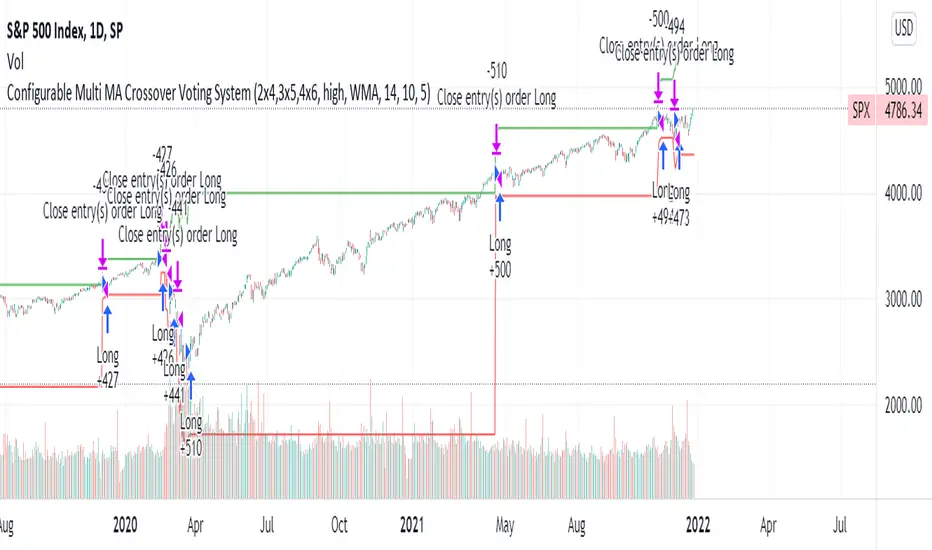

Configurable Multi MA Crossover Voting SystemThis strategy goes long when all fast moving averages that you have defined are above their counterpart slow moving averages.

Long position is closed when profit or loss target is hit and at least one of the fast moving averages is below its counterpart slow moving average.

The format of the config is simple. The format is : FASTxSLOW,FASTxSLOW,...

Example : If you want 2 moving averages fast=9,slow=14 and fast=20,slow=50 you define it like this : 9x14,20x50

Another example : 5x10,10x15,15x20 => means 3 moving average setups : first wih fast=5/slow=10, second with fast=10/slow=15, last with fast=15/slow=20

You can chose the type of moving average : SMA, WMA, VWMA (i got issues with EMA/RMA so i removed them)

You can chose the source of the moving average : high, close, hl2 etc.

You can chose the period on which ATR is calculated and ATR profit/loss factors.

Profit is calculated like : buy_price + atr_factor*atr

Loss is calculated like : buy_price - atr_factor*atr

Performance in backtest is variable depending on the timeframe, the options and the market.

Performance in backtest suggests it works better for higher timeframes like 1d, 4h etc.

Disclaimer

Please remember that past performance may not be indicative of future results.

Due to various factors, including changing market conditions, the strategy may no longer perform as well as in historical backtesting.

This post and the script don’t provide any financial advice.

[astropark] Moon Phases [strategy]Dear Followers,

today I'm glad to present you an indicator which calculates Moon Phases and let's you backtest the simplest strategy over it: buy/sell on full moon and do the opposite on new moon.

This is a public free indicator based on the public one by @paaax:

I added my usual backtesting logic, plus some more customization inputs for easy coloring.

The lower the timeframe you backtest on, the more backtesting data are effective.

Enjoy!

-- astropark

Buy and Hold entry finder StrategyHello everyone!

I proudly present the backtest Strategy Script for my "Buy and Hold entry finder" Script.

It basically shows you the outcome, if you would use my indicator in the past.

The buy signals are limited to 1 order per month.

Order Size: Allows you to choose, how much money you want to invest per month. (Please consider, it will only invest an x amount per Order, but it will not stack the amount you did not invest in an previous month ) (Example in my indicator)

Pyramiding: Just regulates, how often you can open an position.

Commission: Here you can set how much it will cost to open an position at your broker.

I coded a feature that allows you to set a Start Date and an End Date for your backtest. In the end of the backtest the script closes all positions.

If you got any question, feel free to ask in the comments or send me a message.

Sincerely, RS Titan.

Updated TurtlesThis script has been updated to prevent double orders (short/long) from occurring and modifying backtests results.

This is an update to the script that was written a few years ago to prevent double longs/shorts from occurring and skewin backtesting results. Check out the updated indicator here and let me know what you think.

I also added:

- date range inputs if you want to do some backtesting on a particular set of dates.

- the ability to toggle shorting

Noro's SILA v1.6L StrategyBacktesting

Backtesting (for all the time of existence of couple) only with software configurations to default (without optimization of parameters):

US = Uptrend-Sensivity

DS = Downtrend-Sensivity

It is recommended and by default:

- the normal market requires US=DS (for example US=5, DS=5)

- very bear market requires US DS, (for example US=5, DS=0)

- very bull market requires US DS, (US=0, DS=5)

Cryptocurrencies it is very bull market (US=0, DS=5)

Backtesting BTC/FIAT

D1 timeframe

identical parameters for all pairs

BTC/USD (Bitstamp) profit of +41805%

BTC/EUR (BTC-e) profit of +1147%

BTC/RUB (BTC-e) profit of +1162%

BTC/JPY (Bitflyer) profit of +215%

BTC/CNY (BTCChina) profit of 54948%

Backtesting ALTCOIN/BTC

D1 timeframe

identical parameters for all pairs

the exchange Poloniex

top-10 of cryptocurrencies on capitalization at the time of this text

NA = TradingView can't make backtest because of too low price of this cryptocurrency, or on the website there are no quotations of this cryptocurrency

ETH/BTC (Etherium) profit of +11690%

XRP/BTC (Ripple) loss of-100%

LTC/BTC (Litecoin) NA

ETC/BTC (Etherium Classic) profit of +214%

NEM/BTC loss of-49%

DASH/BTC profit of +106%

IOTA/BTC NA

XMR/BTC (Monero) profit of +96%

STRAT/BTC (Stratis) loss of-31%

ALTCOIN/ALTCOIN - not recomended

I don't need your money, I need reputation and likes.

Line Break StrategyLine Break Strategy

Entry rule:

Long on a bullish line and short on a bearish line.

Backtest:

Profit factors are shown below for three-line break.

Daily time frame, FXCM broker.

EURUSD: 1.267, USDJPY: 1.039, GBPUSD: -0.816, AUDUSD: -0.959

S&P500: -0.783, Nikkei225: 1.099

CrudeOil: 1.03, Gold: 1.196

BTCUSD: -0.883

Reference:

Steve Nison, Beyond Candlesticks - New Japanese Charting Techniques Revealed

Note:

This strategy doesn't work properly on the linebreak chart.

A good example is shown below. The entry prices are not always correct.

If you have signal, but the next candle moves in the opposite direction, the entry price is drawn at the Open of the new candle instead of the Close of the previous candle.

The results of backtest are unreliable due to this reason.

Outsidebar vs Insidebar, Illusion Strategy (by ChartArt)WARNING: This strategy does not work! Please don't trade with this strategy

I'm sharing this strategy for the following three educational reasons:

1. You can easily find 100% strategies, but if they only seem to work 100% on one asset, they actually don't work at all. Therefore never backtest your strategy only on one asset, especially forward testing is useless, because it tends to repeat the old patterns. Your strategy has to work on as many different assets as possible.

2. The pyramiding of orders can have an impact on the strategy. In this case if you manually change the strategy settings by increasing it from 1 to 100 pyramiding orders changes the percent profitable on "UKOIL" monthly from 100% to 90% profitable. On other assets you can see very different results. Allowing much more pyramiding orders in this case results in opening orders where the background color highlights appear.

3. The Tradingview backtest beta version currently does not close the last open trade during the backtest. In this case going long on "UKOIL" near the top in 2011 as this strategy did would result in a big loss in 2015. But since the trade is still open and not canceled out by a new short order it still appears as if this strategy works 100% profitable. Which it doesn't.

Smart Scalper Pro Template + VWAP

📌 Author

Garry Evans

Independent system developer focused on:

Risk-first automation

Market structure & liquidity behavior

Discipline, consistency, and capital preservation

“The edge isn’t the market — it’s the man who survives it.”

⚙️ Risk Management & Position Sizing

The script is built around capital protection, not signal frequency.

Risk logic includes:

Fixed or dynamic risk per trade

Market-adaptive position sizing

Session-based trade limits

Daily trade caps and auto-lockout protection

Volatility-aware sizing (futures & crypto)

⚠️ Profit is pursued only after risk is controlled.

📊 Track Record

Backtested across multiple market environments

Forward-tested and actively used by the author

Real-account trades are logged where platform rules allow

Results vary by market, timeframe, and user-defined risk settings.

🌍 Supported Markets

Designed to work across all liquid markets, including:

Stocks

Crypto (spot & futures)

Options (signal-based framework)

Futures (indices, metals, crypto futures)

The system adapts to volatility and structure — it is not market-specific.

⚖️ Leverage

Leverage is not required

If used, leverage is fully user-controlled

Risk logic scales exposure conservatively

No martingale.

No revenge sizing.

No over-exposure logic.

🧪 Backtesting

✔ Yes

Strategy logic has been backtested

Filters reduce chop, noise, and forced trades

Focus on drawdown control over curve-fitting

🛠 Support

✔ Yes

Direct author support

Ongoing improvements and updates

Feature refinement based on real usage and feedback

👥 Community

✔ Yes

Private user access

High-quality feedback environment

No public signal spam or hype-driven chat rooms

⏳ Trial Period

✔ Yes

Limited trial access available

Designed for evaluation only

Trial users do not receive full feature access

🚫 Who This Script Is NOT For

This system is not for:

Traders looking for guaranteed profits

Users expecting copy-paste “signal calls”

Over-leveraged gamblers

Those unwilling to follow risk rules

Anyone seeking overnight results

This is a discipline and automation tool, not a shortcut.

🧠 Final Positioning

This is not a signal service.

This is a risk-controlled execution framework designed to:

Enforce discipline

Reduce emotional trading

Protect capital during bad market conditions

Scale responsibly during favorable ones

Trend Following $ZEC - Multi-Timeframe Structure Filter + Revers# Trend Following CRYPTOCAP:ZEC - Strategy Guide

## 📊 Strategy Overview

Trend Following CRYPTOCAP:ZEC is an enhanced Turtle Trading system designed for cryptocurrency spot trading, combining Donchian Channel breakouts, multi-timeframe structure filtering, and ATR-based dynamic risk management for both long and short positions.

---

## 🎯 Core Features

1. Multi-Timeframe Structure Filtering

- Uses Swing High/Low to identify market structure

- Customizable structure timeframe (default: 1 minute)

- Only enters trades in the direction of the trend, avoiding counter-trend positions

2. Reverse Signal Exit

- No fixed stop-loss or fixed-period exits

- Exits only when a reverse entry signal triggers

- Maximizes trend profits, reduces premature exits

3. ATR Dynamic Pyramiding

- Adds positions when price moves 0.5 ATR in favorable direction

- Supports up to 2 units maximum (adjustable)

- Pyramid scaling to enhance profitability

4. Complete Risk Management

- Fixed position size (5000 USD per unit)

- Commission fee 0.06% (Binance spot rate)

- Initial capital 10,000 USD

---

## 📈 Trading Logic

Entry Conditions

✅ Long Entry:

- Close price breaks above 20-period high

- Structure trend is bullish (price breaks above Swing High)

✅ Short Entry:

- Close price breaks below 20-period low

- Structure trend is bearish (price breaks below Swing Low)

Add Position Conditions

- Long: Price rises ≥ 0.5 ATR

- Short: Price falls ≥ 0.5 ATR

- Maximum 2 units including initial entry

Exit Conditions

- Long Exit: When short entry signal triggers (price breaks 20-period low + structure turns bearish)

- Short Exit: When long entry signal triggers (price breaks 20-period high + structure turns bullish)

---

## ⚙️ Parameter Settings

Channel Settings

- Entry Channel Period: 20 (Donchian Channel breakout period)

- Exit Channel Period: 10 (reserved parameter, actually uses reverse signal exit)

ATR Settings

- ATR Period: 20

- Stop Loss ATR Multiplier: 2.0 (reserved parameter)

- Add Position ATR Multiplier: 0.5

Structure Filter

- Swing Length: 160 (Swing High/Low calculation period)

- Structure Timeframe: 1 minute (can change to 5/15/60, etc.)

Position Management

- Maximum Units: 2 (including initial entry)

- Capital Per Unit: 5000 USD

---

## 🎨 Visualization Features

Background Colors

- Light Green: Bullish structure

- Light Red: Bearish structure

- Dark Green: Long entry

- Dark Red: Short entry

Optional Display (Default: OFF)

- Entry/exit channel lines

- Structure high/low lines

- ATR stop-loss line

- Next add position indicator

- Entry/exit labels

---

## 📱 Alert Message Format

Strategy sends notifications on entry/exit with the following format:

- Entry: `1m Long EP:428.26`

- Add Position: `15m Add Long 2/2 EP:429.50`

- Exit: `1m Close Long Reverse Signal`

Where:

- `1m`/`15m` = Current chart timeframe

- `EP` = Entry Price

---

## 💰 Backtest Settings

Capital Allocation

- Initial Capital: 10,000 USD

- Per Entry: 5,000 USD (split into 2 entries)

- Leverage: 0x (spot trading)

Trading Costs

- Commission: 0.06% (Binance spot VIP0)

- Slippage: 0

---

## 🎯 Use Cases

✅ Best Scenarios

- Trending markets

- Moderate volatility assets

- 1-minute to 4-hour timeframes

⚠️ Not Suitable For

- Highly volatile choppy markets

- Low liquidity small-cap coins

- Extreme market conditions (black swan events)

---

## 📊 Usage Recommendations

Timeframe Suggestions

| Timeframe | Trading Style | Suggested Parameter Adjustment |

|-----------|--------------|-------------------------------|

| 1-5 min | Scalping | Swing Length 100-160 |

| 15-30 min | Short-term | Swing Length 50-100 |

| 1-4 hour | Swing Trading | Swing Length 20-50 |

Optimization Tips

1. Adjust swing length based on backtest results

2. Different coins may require different parameters

3. Recommend backtesting on 1-minute chart first before live trading

4. Enable labels to observe entry/exit points

---

## ⚠️ Risk Disclaimer

1. Past Performance Does Not Guarantee Future Results

- Backtest data is for reference only

- Live trading may be affected by slippage, delays, etc.

2. Market Condition Changes

- Strategy performs better in trending markets

- May experience frequent stops in ranging markets

3. Capital Management

- Do not invest more than you can afford to lose

- Recommend setting total capital stop-loss threshold

4. Commission Impact

- Frequent trading accumulates commission fees

- Recommend using exchange discounts (BNB fee reduction, etc.)

---

## 🔧 Troubleshooting

Q: No entry signals?

A: Check if structure filter is too strict, adjust swing length or timeframe

Q: Too many labels displayed?

A: Turn off "Show Labels" option in settings

Q: Poor backtest performance?

A:

1. Check if the coin is suitable for trend-following strategies

2. Adjust parameters (swing length, channel period)

3. Try different timeframes

Q: How to set alerts?

A:

1. Click "Alert" in top-right corner of chart

2. Condition: Select "Strategy - Trend Following CRYPTOCAP:ZEC "

3. Choose "Order filled"

4. Set notification method (Webhook/Email/App)

---

## 📞 Contact Information

Strategy Name: Trend Following CRYPTOCAP:ZEC

Version: v1.0

Pine Script Version: v6

Last Updated: December 2025

---

## 📄 Copyright Notice

This strategy is for educational and research purposes only.

All risks of using this strategy for live trading are borne by the user.

Commercial use without authorization is prohibited.

---

## 🎓 Learning Resources

To understand the strategy principles in depth, recommended reading:

- "The Complete TurtleTrader" - Curtis Faith

- "Trend Following" - Michael Covel

- TradingView Pine Script Official Documentation

---

Happy Trading! Remember to manage your risk 📈

Quasimodo Pattern Strategy Back Test [TradingFinder] QM Trading🔵 Introduction

The QM pattern, also known as the Quasimodo pattern, is one of the popular patterns in price action, and it is often used by technical analysts. The QM pattern is used to identify trend reversals and provides a very good risk-to-reward ratio. One of the advantages of the QM pattern is its high frequency and visibility in charts.

Additionally, due to its strength, it is highly profitable, and as mentioned, its risk-to-reward ratio is very good. The QM pattern is highly popular among traders in supply and demand, and traders also use this pattern.

The Price Action QM pattern, like other Price Action patterns, has two types: Bullish QM and Bearish QM patterns. To identify this pattern, you need to be familiar with its types to recognize it.

🔵 Identifying the QM Pattern

🟣 Bullish QM

In the bullish QM pattern, as you can see in the image below, an LL and HH are formed. As you can see, the neckline is marked as a dashed line. When the price reaches this range, it will start its upward movement.

🟣 Bearish QM

The Price Action QM pattern also has a bearish pattern. As you can see in the image below, initially, an HH and LL are formed. The neckline in this image is the dashed line, and when the LL is formed, the price reaches this neckline. However, it cannot pass it, and the downward trend resumes.

🔵 How to Use

The Quasimodo pattern is one of the clearest structures used to identify market reversals. It is built around the concept of a structural break followed by a pullback into an area of trapped liquidity. Instead of relying on lagging indicators, this pattern focuses purely on price action and how the market reacts after exhausting one side of liquidity. When understood correctly, it provides traders with precise entry points at the transition between trend phases.

🟣 Bullish Quasimodo

A bullish Quasimodo forms after a clear downtrend when sellers start losing control. The market continues to make lower lows until a sudden higher high appears, signaling that buyers are entering with strength. Price then pulls back to retest the previous low, creating what is known as the Quasimodo low.

This area often becomes the final trap for sellers before the market shifts upward. A visible rejection or displacement from this zone confirms bullish momentum. Traders usually place entries near this level, stops below the low, and targets at previous highs or the next resistance zone. Combining the setup with demand zones or Fair Value Gaps increases its accuracy.

🟣 Bearish Quasimodo

A bearish Quasimodo forms near the top of an uptrend when buyers begin to lose strength. The market continues to make higher highs until a sudden lower low breaks the bullish structure, showing that selling pressure is entering the market. Price then retraces upward to retest the previous high, forming the Quasimodo high, where breakout buyers are often trapped.

Once rejection appears at this level, it indicates a likely reversal. Traders can enter short near this area, with stop-losses placed above the high and targets near the next support or previous lows. The setup gains more reliability when aligned with supply zones, SMT divergence, or bearish Fair Value Gaps.

🔵 Setting

Pivot Period : You can use this parameter to use your desired period to identify the QM pattern. By default, this parameter is set to the number 5.

Take Profit Mode : You can choose your desired Take Profit in three ways. Based on the logic of the QM strategy, you can select two Take Profit levels, TP1 and TP2. You can also choose your take profit based on the Reward to Risk ratio. You must enter your desired R/R in the Reward to Risk Ratio parameter.

Stop Loss Refine : The loss limit of the QM strategy is based on its logic on the Head pattern. You can refine it using the ATR Refine option to prevent Stop Hunt. You can enter your desired coefficient in the Stop Loss ATR Adjustment Coefficient parameter.

Reward to Risk Ratio : If you set Take Profit Mode to R/R, you must enter your desired R/R here. For example, if your loss limit is 10 pips and you set R/R to 2, your take profit will be reached when the price is 20 pips away from your entry point.

Stop Loss ATR Adjustment Coefficient : If you set Stop Loss Refine to ATR Refine, you must adjust your loss limit coefficient here. For example, if your buy position's loss limit is at the price of 1000, and your ATR is 10, if you set Stop Loss ATR Adjustment Coefficient to 2, your loss limit will be at the price of 980.

Entry Level Validity : Determines how long the Entry level remains valid. The higher the level, the longer the entry level will remain valid. By default it is 2 and it can be set between 2 and 15.

🔵 Results

The following examples show the backtest results of the Quasimodo (QM) strategy in action. Each image is based on specific settings for the symbol, timeframe, and input parameters, illustrating how the QM logic can generate signals under different market conditions. The detailed configuration for each backtest is also displayed on the image.

⚠ Important Note : Even with identical settings and the same symbol, results may vary slightly across different brokers due to data feed variations and pricing differences.

Default Properties of Backtests :

OANDA:XAUUSD | TimeFrame: 5min | Duration: 1 Year :

BINANCE:BTCUSD | TimeFrame: 5min | Duration: 1 Year :

CAPITALCOM:US30 | TimeFrame: 5min | Duration: 1 Year :

NASDAQ:QQQ | TimeFrame: 5min | Duration: 5 Year :

OANDA:EURUSD | TimeFrame: 5min | Duration: 5 Year :

PEPPERSTONE:US500 | TimeFrame: 5min | Duration: 5 Year :

TMB Invest - Smart Money Concept StrategyEnglish:

**Quick Overview**

The "TMB_SMC_Strategy_v1.1.3" combines a classic trend filter using two EMAs with contrarian RSI entries and simple SMC elements (Fair Value Gaps & Order Blocks). Stop-loss and take-profit orders are volatility-adaptive and controlled via the ATR. An integrated dashboard displays the setup status, stop-loss/take-profit levels, entry reference, and trend, RSI, and ATR values.

---

## Operating Principle

1. **Trend Filter:** A fast EMA (default 50) is compared to a slow EMA (default 200). Trading occurs only in the direction of the trend: long in uptrends, short in downtrends.

2. **Timing via RSI:** Contrarian entries within the trend. Go long when the RSI is below a buy level (default 40); Short when the RSI is above a sell level (standard 60).

3. **Structure Check (SMC Proxy):** An "FVG Touch" serves as additional confirmation that an inefficient price zone has been tested. Order blocks are visualized for guidance but are not a direct entry trigger.

4. **Risk Management via ATR:** Stop-loss and take-profit levels are set as multipliers of the current ATR (e.g., SL = 1×ATR, TP = 2×ATR). This allows target and risk distances to adjust to market volatility.

5. **Simple Position Logic:** Only one position is held at a time (no pyramiding). After entry, stop and limit orders (bracket exit) are automatically placed.

---

## Input Values

* **EMA Fast / EMA Slow:** Lengths of the moving averages for the trend filter.

* **RSI Length / Levels:** Length of the RSI as well as buy and sell thresholds (contra signals within the trend direction).

* **Take Profit (RR) / Stop Loss (RR):** ATR multipliers for TP and SL.

* **Show FVGs & Order Blocks:** Toggles the visual SMC elements (zones/boxes) on or off.

--

## Signals & Execution

* **Long Setup:** Uptrend (fast EMA above slow EMA) **and** RSI below the buy level **and** a current FVG signal in a bullish direction.

* **Short Setup:** Downtrend (fast EMA below slow EMA) **and** RSI above the sell level **and** a current FVG touch in a bearish direction.

* **Entry & Exit:** If the setup is met, the market is entered; stop-loss/take-profit orders are placed immediately according to ATR multiples.

--

## Visualization

* **EMAs:** The fast and slow EMAs are plotted to illustrate the trend.

* **FVGs:** Fair Value Gaps are drawn as semi-transparent boxes in the trend color and projected slightly into the future.

* **Order Blocks:** Potential order block zones from the previous candle are visually highlighted (for informational purposes only).

---

## Integrated Dashboard

A compact table dashboard (bottom left) displays:

* Current **Setup Status** (Long/Short active, Long/Short ready, No Setup),

* **Stop-Loss**, **Take-Profit**, and **Entry Reference**,

* **Trend Status** (Bull/Bear/Sideways),

* **RSI Value**, and **ATR Value**.

Active long/short positions are highlighted in color (green/red).

--

## Practical Guide

1. **Place on Chart** and select the desired timeframe.

2. **Calibrate Parameters** (EMA lengths, RSI levels, ATR multipliers) to match the market and timeframe.

3. **Backtest** across different market phases; prioritize robustness over maximum curve fit.

4. **Fine-Tuning:**

* Shorter EMAs are often useful intraday (e.g., 20/100 or 34/144).

* Adjust RSI levels to market characteristics (45/55 for aggressive trading, 30/70 for conservative trading).

* Increase or decrease ATR multipliers depending on volatility/trading style.

--

## Notes, Limitations & Extensions

* **FVG Definition:** The FVG detection used here is intentionally simplified. Those who prefer a more rigorous approach can switch to a 3-candle definition and fill levels.

* **Order Blocks:** These primarily serve as a guide. Integration into entry/exit logic (e.g., retests) is possible as an extension.

* **Backtest Realism:** Fills may differ from the displayed closing price. For greater accuracy, intrabar backtests or an entry indicator based on the average position price are conceivable.

* **Alerts:** Currently, no alert conditions are defined; these can be added for long/short setups and status messages.

* **Position Management:** By default, no scaling is performed. Partial sales, trailing stops, or multiple entries can be added.

---

## Purpose & Benefits

The strategy offers a clear, modular framework: trend filter (direction), RSI contra timing (entry), SMC proxy via FVG Touch (structure), and ATR-based exits (risk adaptation). This makes it robust, easy to understand, and highly extensible—both for discretionary traders who appreciate visual SMC elements and for systematic testers who prefer a clean, parameterizable foundation.

RSI Momentum Trend MM with Risk Per Trade [MTF]This is a comprehensive and highly customizable trend-following strategy based on RSI momentum. The core logic identifies strong directional moves when the RSI crosses user-defined thresholds, combined with an EMA trend confirmation. It is designed for traders who want granular control over their strategy's parameters, from signal generation to risk management and exit logic.

This script evolves a simple concept into a powerful backtesting tool, allowing you to test various money management and trade management theories across different timeframes.

Key Features

- RSI Momentum Signals: Uses RSI crosses above a "Positive" level or below a "Negative" level to generate trend signals. An EMA filter ensures entries align with the immediate trend.

- Multi-Timeframe (MTF) Analysis: The core RSI and EMA signals can be calculated on a higher timeframe (e.g., using 4H signals to trade on a 1H chart) to align trades with the larger trend. This feature helps to reduce noise and improve signal quality.

Advanced Money Management

- Risk per Trade %: Calculate position size based on a fixed percentage of equity you want to risk per trade.

- Full Equity: A more aggressive option to open each position with 100% of the available strategy equity.

Flexible Exit Logic: Choose from three distinct exit strategies to match your trading style

- Percentage (%) Based: Set a fixed Stop Loss and Take Profit as a percentage of the entry price.

- ATR Multiplier: Base your Stop Loss and Take Profit on the Average True Range (ATR), making your exits adaptive to market volatility.

- Trend Reversal: A true trend-following mode. A long position is held until an opposite "Negative" signal appears, and a short position is held until a "Positive" signal appears. This allows you to "let your winners run."

Backtest Date Range Filter: Easily configure a start and end date to backtest the strategy's performance during specific market periods (e.g., bull markets, bear markets, or high-volatility periods).

How to Use

RSI Settings

- Higher Timeframe: Set the timeframe for signal calculation. This must be higher than your chart's timeframe.

- RSI Length, Positive above, Negative below: Configure the core parameters for the RSI signals.

Money Management

Position Sizing Mode

- Choose "Risk per Trade" to use the Risk per Trade (%) input for precise risk control.

- Choose "Full Equity" to use 100% of your capital for each trade.

- Risk per Trade (%): Define the percentage of your equity to risk on a single trade (only works with the corresponding sizing mode).

SL/TP Calculation Mode

Select your preferred exit method from the dropdown. The strategy will automatically use the relevant inputs (e.g., % values, ATR Multiplier values, or the trend reversal logic).

Backtest Period Settings

Use the Start Date and End Date inputs to isolate a specific period for your backtest analysis.

License & Disclaimer

© waranyu.trkm — MIT License.

This script is for educational purposes only and should not be considered financial advice. Trading involves significant risk, and past performance is not indicative of future results. Always conduct your own research and risk assessment before making any trading decisions.

EMA inFusion Pro - Multiple SourcesEMA Fusion Pro: Dynamic Trend & Momentum Strategy with Three Exit Modes

EMA Fusion Pro is a highly customizable, multi-exit trend-following strategy designed for traders who value both precision and flexibility. By leveraging exponential moving averages (EMA), average directional index (ADX), and volume analysis, this strategy aims to capture trending market moves while offering three distinct exit modes for optimal risk management across varying market conditions.

Strategy Overview

This strategy systematically identifies potential entry points using a moving average crossover with highly configurable data sources (including price, volume, rate of change, or their Heikin Ashi versions) and filters signal quality with ADX trend strength and volume spikes. Each trade is managed with one of three advanced exit methodologies—reverse signal, ATR-based stop/take profit, or fixed percentage—giving you the control to adapt your risk profile to different market regimes.

Key Features

Customizable EMA Source: Calculate the core trend-filtering EMA from price (default), volume, rate of change, or their Heikin Ashi counterparts for unique market perspectives.

Trend Filter with ADX: Confirm entries only when the trend is strong, as measured by the user-adjustable ADX threshold.

Volume Spike Confirmation: Optional filter to only take trades with above-average volume activity, reducing false signals.

Three Exit Modes:

Reverse Signal: Exit trades when a new, opposite entry signal occurs.

ATR-Based Stop/Take Profit: Dynamic risk management using multiples of the average true range (ATR) for both take profit and stop loss.

Percent-Based Stop/Take Profit: Fixed-percentage risk management with user-defined thresholds.

Visual Annotations: Signal markers, EMA line color-coded by source, trend background coloring, and optional ATR/percent-based TP/SL levels.

Info Panel: Real-time display of all core indicators, current trading mode, exit parameters, and position status for quick oversight.

How It Works

Entry Logic: A crossover signal (above/below the EMA) triggers a new entry, but only if both ADX trend strength and (optionally) volume spike conditions are met.

Exit Logic: Three selectable modes allow you to exit trades on reverse signals, at a dynamic ATR-based profit or loss, or at a fixed percentage gain/loss.

Flexible Data Analysis: The EMA source can be chosen from six options—standard price, volume, rate of change, or their Heikin Ashi variants—allowing experimentation with different market dimensions.

Risk Management: All exits are precisely controlled, either by the next opposing signal, by volatility-adjusted levels, or by fixed risk/reward ratios.

Backtest & Optimization: The strategy is fully backtestable within TradingView’s Strategy Tester, with adjustable parameters for optimization.

Customization & Usage

Indicator Source: Select your preferred data type for EMA calculation, opening the door to creative strategy variations (e.g., volume momentum, pure price trend, rate of change divergence).

Filter Toggles: Enable/disable ADX and volume filters as desired—useful for different market environments.

Exit Mode Selection: Switch between reverse, ATR, or percent-based exits with a single parameter—ideal for adapting to ranging vs. trending markets.

Visual Clarity: The EMA line color reflects its underlying source, and the info panel summarizes all critical values for easy monitoring.

Who Should Use This Strategy?

Trend Followers seeking to ride strong moves with multiple exit options.

Experienced Traders who want to experiment with different data types (volume, momentum, Heikin Ashi) for trend analysis.

Algorithmic Traders looking for a robust, flexible base to build upon with their own ideas.

Getting Started

Apply the script to your chart and review default settings.

Customize parameters—EMA length, ADX threshold, volume settings, exit type—as desired.

Backtest on multiple instruments and timeframes to evaluate performance.

Optimize filters, exit rules, and risk parameters for your preferred trading style.

Monitor with the real-time info panel and trade alerts.

Disclaimer

This script is for educational and entertainment purposes only. It is not financial advice. Past performance is not indicative of future results. Always conduct thorough testing and consider your risk tolerance before trading real capital.

— Happy Trading —

Feel free to adapt, share, and contribute to this open-source strategy!

EMD Trend [InvestorUnknown]EMD Trend is a dynamic trend-following indicator that utilizes Exponential Moving Deviation (EMD) to build adaptive channels around a selected moving average. Designed for traders who value responsive trend signals with built-in volatility sensitivity, this tool highlights directional bias, market regime shifts, and potential breakout opportunities.

How It Works

Instead of using standard deviation, EMD Trend employs the exponential moving average of the absolute deviation from a moving average—producing smoother, faster-reacting upper and lower bounds:

Bullish (Risk-ON Long): Price crosses above the upper EMD band

Bearish (Risk-ON Short): Price crosses below the lower EMD band

Neutral: Price stays within the channel, indicating potential mean reversion or low momentum

Trend direction is defined by price interaction with these bands, and visual cues (color-coded bars and fills) help quickly identify market conditions.

Features

7 Moving Average Types: SMA, EMA, HMA, DEMA, TEMA, RMA, FRAMA

Custom Price Source: Choose close, hl2, ohlc4, or others

EMD Multiplier: Controls the width of the deviation envelope

Bar Coloring: Candles change color based on current trend

Intra-bar Signal Option: Enables faster updates (with optional repainting)

Speculative Zones: Fills highlight aggressive momentum moves beyond EMD bounds

Backtest Mode

Switch to Backtest Mode for performance evaluation over historical data:

Equity Curve Plot: Compare EMD Trend strategy vs. Buy & Hold

Trade Metrics Table: View number of trades, win/loss stats, profits

Performance Metrics Table: Includes CAGR, Sharpe, max drawdown, and more

Custom Start Date: Select from which date the backtest should begin

Trade Sizing: Configure capital and trade percentage per entry

Signal Filters: Choose from Long Only, Short Only, or Both

Alerts

Built-in alerts let you automate entries, exits, and trend transitions:

LONG (EMD Trend) - Trend flips to Long

SHORT (EMD Trend) - Trend flips to Short

RISK-ON LONG - Price crosses above upper EMD band

RISK-OFF LONG - Price crosses back below upper EMD band

RISK-ON SHORT - Price crosses below lower EMD band

RISK-OFF SHORT - Price crosses back above lower EMD band

Use Cases

Trend Confirmation with volatility-sensitive boundaries

Momentum Entry Filtering via breakout zones

Mean Reversion Avoidance in sideways markets

Backtesting & Strategy Building with real-time metrics

Disclaimer

This indicator is intended for informational and educational purposes only. It does not constitute investment advice. Historical performance does not guarantee future results. Always backtest and use in simulation before live trading.

Best SMA FinderThis script, Best SMA Finder, is a tool designed to identify the most robust simple moving average (SMA) length for a given chart, based on historical backtest performance. It evaluates hundreds of SMA values (from 10 to 1000) and selects the one that provides the best balance between profitability, consistency, and trade frequency.

What it does:

The script performs individual backtests for each SMA length using either "Long Only" or "Buy & Sell" logic, as selected by the user. For each tested SMA, it computes:

- Total number of trades

- Profit Factor (total profits / total losses)

- Win Rate

- A composite Robustness Score, which integrates Profit Factor, number of trades (log-scaled), and win rate.

Only SMA configurations that meet the user-defined minimum trade count are considered valid. Among all valid candidates, the script selects the SMA length with the highest robustness score and plots it on the chart.

How to use it:

- Choose the strategy type: "Long Only" or "Buy & Sell"

- Set the minimum trade count to filter out statistically irrelevant results

- Enable or disable the summary stats table (default: enabled)

The selected optimal SMA is plotted on the chart in blue. The optional table in the top-right corner shows the corresponding SMA length, trade count, Profit Factor, Win Rate, and Robustness Score for transparency.

Key Features:

- Exhaustive SMA optimization across 991 values

- Customizable trade direction and minimum trade filters

- In-chart visualization of results via table and plotted optimal SMA

- Uses a custom robustness formula to rank SMA lengths

Use cases:

Ideal for traders who want to backtest and auto-select a historically effective SMA without manual trial-and-error. Useful for swing and trend-following strategies across different timeframes.

📌 Limitations:

- Not a full trading strategy with position sizing or stop-loss logic

- Only one entry per direction at a time is allowed

- Designed for exploration and optimization, not as a ready-to-trade system

This script is open-source and built entirely from original code and logic. It does not replicate any closed-source script or reuse significant external open-source components.

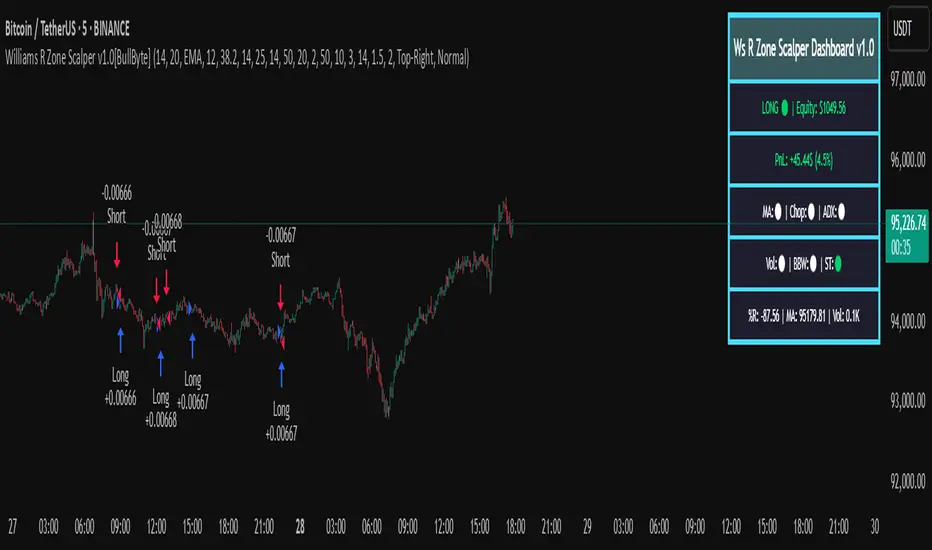

Williams R Zone Scalper v1.0[BullByte]Originality & Usefulness

Unlike standard Williams R cross-over scripts, this strategy layers five dynamic filters—moving-average trend, Supertrend, Choppiness Index, Bollinger Band Width, and volume validation —and presents a real-time dashboard with equity, PnL, filter status, and key indicator values. No other public Pine script combines these elements with toggleable filters and a custom dashboard. In backtests (BTC/USD (Binance), 5 min, 24 Mar 2025 → 28 Apr 2025), adding these filters turned a –2.09 % standalone Williams R into a +5.05 % net winner while cutting maximum drawdown in half.

---

What This Script Does

- Monitors Williams R (length 14) for overbought/oversold reversals.

- Applies up to five dynamic filters to confirm trend strength and volatility direction:

- Moving average (SMA/EMA/WMA/HMA)

- Supertrend line

- Choppiness Index (CI)

- Bollinger Band Width (BBW)

- Volume vs. its 50-period MA

- Plots blue arrows for Long entries (R crosses above –80 + all filters green) and red arrows for Short entries (R crosses below –20 + all filters green).

- Optionally sets dynamic ATR-based stop-loss (1.5×ATR) and take-profit (2×ATR).

- Shows a dashboard box with current position, equity, PnL, filter status, and real-time Williams R / MA/volume values.

---

Backtest Summary (BTC/USD(Binance), 5 min, 24 Mar 2025 → 28 Apr 2025)

• Total P&L : +50.70 USD (+5.05 %)

• Max Drawdown : 31.93 USD (3.11 %)

• Total Trades : 198

• Win Rate : 55.05 % (109/89)

• Profit Factor : 1.288

• Commission : 0.01 % per trade

• Slippage : 0 ticks

Even in choppy March–April, this multi-filter approach nets +5 % with a robust risk profile, compared to –2.09 % and higher drawdown for Williams R alone.

---

Williams R Alone vs. Multi-Filter Version

• Total P&L :

– Williams R alone → –20.83 USD (–2.09 %)

– Multi-Filter → +50.70 USD (+5.05 %)

• Max Drawdown :

– Williams R alone → 62.13 USD (6.00 %)

– Multi-Filter → 31.93 USD (3.11 %)

• Total Trades : 543 vs. 198

• Win Rate : 60.22 % vs. 55.05 %

• Profit Factor : 0.943 vs. 1.288

---

Inputs & What They Control

- wrLen (14): Williams R look-back

- maType (EMA): Trend filter type (SMA, EMA, WMA, HMA)

- maLen (20): Moving-average period

- useChop (true): Toggle Choppiness Index filter

- ciLen (12): CI look-back length

- chopThr (38.2): CI threshold (below = trending)

- useVol (true): Toggle volume-above-average filter

- volMaLen (50): Volume MA period

- useBBW (false): Toggle Bollinger Band Width filter

- bbwMaLen (50): BBW MA period

- useST (false): Toggle Supertrend filter

- stAtrLen (10): Supertrend ATR length

- stFactor (3.0): Supertrend multiplier

- useSL (false): Toggle ATR-based SL/TP

- atrLen (14): ATR period for SL/TP

- slMult (1.5): SL = slMult × ATR

- tpMult (2.0): TP = tpMult × ATR

---

How to Read the Chart

- Blue arrow (Long): Williams R crosses above –80 + all enabled filters green

- Red arrow (Short) : Williams R crosses below –20 + all filters green

- Dashboard box:

- Top : position and equity

- Next : cumulative PnL in USD & %

- Middle : green/white dots for each filter (green=passing, white=disabled)

- Bottom : Williams R, MA, and volume current values

---

Usage Tips

- Add the script : Indicators → My Scripts → Williams R Zone Scalper v1.0 → Add to BTC/USD chart on 5 min.

- Defaults : Optimized for BTC/USD.

- Forex majors : Raise `chopThr` to ~42.

- Stocks/high-beta : Enable `useBBW`.

- Enable SL/TP : Toggle `useSL`; stop-loss = 1.5×ATR, take-profit = 2×ATR apply automatically.

---

Common Questions

- * Why not trade every Williams R reversal?*

Raw Williams R whipsaws in sideways markets. Choppiness and volume filters reduce false entries.

- *Can I use on 1 min or 15 min?*

Yes—adjust ATR length or thresholds accordingly. Defaults target 5 min scalping.

- *What if all filters are on?*

Fewer arrows, higher-quality signals. Expect ~10 % boost in average win size.

---

Disclaimer & License

Trading carries risk of loss. Use this script “as is” under the Mozilla Public License 2.0 (mozilla.org). Always backtest, paper-trade, and adjust risk settings to your own profile.

---

Credits & References

- Pine Script v6, using TradingView’s built-in `ta.supertrend()`.

- TradingView House Rules: www.tradingview.com

Goodluck!

BullByte

Daily Bollinger Band StrategyOverview of the Daily Bollinger Band Strategy

1. Strategy Overview and Features

This strategy is a tool for backtesting a trading method that uses Bollinger Bands. It is *not* a tool for automated trading.

1-1. Main Display Items

The main chart displays the Bollinger Bands and the 200-day moving average.

It also shows the entry and exit points along with the position size (in units of 100 shares).

1-2. Summary of Trading Rules

For long (buy) strategies, the trade enters when the price crosses above the +1σ line of the Bollinger Bands, aiming to ride an upward trend. The position is exited when the price crosses below the middle band.

For short (sell) strategies, the trade enters when the price crosses below the -1σ line of the Bollinger Bands, aiming to ride a downward trend. The position is exited when the price crosses above the middle band.

1-3. Strategic Enhancements

The strategy uses the slope of the 200-day moving average to determine the trend direction and enter trades accordingly. This improves the win rate and payoff ratio.

Additionally, to reduce the probability of ruin, the risk per trade is limited to 1.0% of capital, and position sizing is adjusted using ATR (a volatility indicator).

2. Trading Rules

2-1. Chart Type

Only daily charts are used.

2-2. Indicators Used

(1) Bollinger Bands** (used for entry and exit signals)

- Period: Fixed at 80 days

- Upper and lower bands: Fixed at ±1σ

(2) Moving Average** (used to determine trend direction)

- Period: Fixed at 200 days

- Trend direction is judged based on whether the difference from the previous day is positive (upward) or negative (downward)

2-3. Buy Rules

Setup:

- Price crosses above the +1σ line from below

- Both the middle band and 200-day moving average are upward sloping

Entry:

- Buy at the next day’s market open using a market order

Exit:

- If the price crosses below the middle band, sell at the next day’s open using a market order

2-4. Sell Rules

Setup:

- Price crosses below the -1σ line from above

- Both the middle band and 200-day moving average are downward sloping

Entry:

- Sell at the next day’s market open using a market order

Exit:

- If the price crosses above the middle band, buy back at the next day’s open using a market order

2-5. Risk Management Rules

- Risk per trade: 1.0% of total capital (acceptable loss = capital × 1.0%)

- Position size: Acceptable loss ÷ 2ATR (rounded down to the nearest unit of 100 shares)

2-6. Other Notes

- No brokerage fees

- No pyramiding

- No partial exits

- No reverse positions (no “stop-and-reverse” trades)

3. Strategy Parameters

The following settings can be specified:

3-1. Period Settings

- Start date: Set the start date for the backtest period

- Stop date: Set the end date for the backtest period

3-2. Display of Trend and Signals

- Show trend: When checked, the background color of the bars is light red for an uptrend and light blue for a downtrend

- Show signal: When checked, entry and exit signals are displayed (note: signals are executed at the next day’s open, so there is a one-day lag in the display)

3-3. Capital Management Settings

- Funds: Capital available for trading (in JPY)

- Risk rate: Specify what percentage of the capital to risk per trade

Settings in the “Properties” tab are not used in this strategy.

4. Backtest Results (Example)

Here are the backtest results conducted by the author:

- Target Stocks: All components of the Nikkei 225

- Test Period: January 4, 2000 – December 30, 2024

- Data Points: 12,886

- Win Rate: 33.45%

- Net Profit: ¥82,132,380

- Payoff Ratio: 2.450

- Expected Value: ¥6,373.8

- Risk Rate: 1.0%

- Probability of Ruin: 0.00%

---

デイリー・ボリンジャーバンド・ストラテジーの概要

1. ストラテジーの概要と特徴

このストラテジーは、ボリンジャーバンドを使ったトレード手法のバックテストを行うツールです。自動売買を行うツールではありません。

1-1. 主な表示項目

メインチャートにボリンジャーバンドと 200日移動平均線を表示します。

また、エントリーと手仕舞いのタイミングと数量(100株単位)も表示されます。

1-2. トレードルールの概要

買い戦略の場合、ボリンジャーバンドの +1σ 超えでエントリーして上昇トレンドに乗り、ミドルバンドを割ったら決済します。

売り戦略の場合、ボリンジャーバンドの -1σ 割りでエントリーして下降トレンドに乗り、ミドルバンドを上抜けたら決済します。

1-3. ストラテジーの工夫点

200日移動平均線の傾きを見てトレンド方向にエントリーをしています。こうして勝率とペイオフレシオの成績を向上しています。

また、破産確率を抑えるために、リスク資金比率を 1.0% にして、ATR(ボラティリティ指標) を使って注文数を調整しています。

2. 売買ルール

2-1. 使用するチャート

日足チャートに限定します

2-2. 使用する指標

(1) ボリンジャーバンド(仕掛けと手仕舞いのシグナルに使用)

期間は80日に固定

上下バンドは ±1σ に固定

(2) 移動平均線(トレンドの方向を見るために使用)

期間は200日に固定

移動平均の値の前日との差がプラスのとき上向き、マイナスのとき下向きと判断

2-3. 買いのルール

セットアップ:ボリンジャーバンドの +1σ を価格が下から上に交差 かつ ミドルバンドと 200日移動平均線が上向き

仕掛け:翌日の寄り付きに成行で買う

手仕舞い:ボリンジャーバンドのミドルバンドを価格が上から下に交差したら、翌日の寄り付きに成行で売る

2-4. 売りのルール

セットアップ:ボリンジャーバンドの -1σ を価格が上から下に交差 かつ ミドルバンドと 200日移動平均線が下向き

仕掛け:翌日の寄り付きに成行で売る

手仕舞い:ボリンジャーバンドのミドルバンドを価格が下から上に交差したら、翌日の寄り付きに成行で買い戻す

2-5. 資金管理のルール

リスク資金比率:資産の 1.0%(許容損失 = 資産 × 1.0%)

注文数:許容損失 ÷ 2ATR(単元株数未満は切り捨て)

2-6. その他

仲介手数料:なし

ピラミッディング:なし

分割決済:なし

ドテン:しない

3. ストラテジーのパラメーター

次の項目が指定できます。

3-1. 期間の設定

Staer date : バックテストの検証期間の開始日を指定します

Stop date : バックテストの検証期間の終了日を指定します

3-2. トレンドとシグナルの表示

Show trend : チェックを入れると、バーの背景色が、トレンドが上昇のときは薄い赤で、下落のときは薄い青で表示されます

Show signal : チェックを入れると、エントリーと手仕舞いのシグナルを表示します(シグナルの出た翌日の寄り付きに売買をするので表示に1日のずれがあります)

3-3. 資金管理用の設定

Funds : トレード用の資金(円)

Risk rate : 許容損失を資金の何%にするかで指定します

「プロパティタブ」で設定する値は、このストラテジーでは有効ではありません。

4. バックテストの結果(例)

作者がバックテストを実施した結果をお知らせします。

対象銘柄:日経225構成銘柄すべて

対象期間:2000年1月4日~2024年12月30日

データ件数:12,886

勝率:33.45%

純利益:82,132,380

ペイオフレシオ:2.450

期待値:6,373.8

リスク資金比率:1.0%

破産確率:0.00%

Bull Flag (9:30-12:00 Only) [One-Liner Fix]🚀 Bull Flag Breakout Strategy | Intraday Momentum (9:30-12:00) 🔥📈

💡 Designed for Intraday Traders who love momentum breakouts and want to automate Bull Flag setups with volume confirmation! This strategy detects strong bullish moves, measures pullbacks, and triggers trades when the first candle makes a new high—ensuring maximum momentum.

⸻

🏆 Why This Strategy?

✅ Bull Flag Pattern Automation – No need to manually spot pullbacks! 🎯

✅ Smart Volume Confirmation – Only enter trades when breakout volume is strong! 📊

✅ Morning Session Focused (9:30 - 12:00 EST) – Trade when momentum is at its peak! ⏰

✅ Customizable ATR & Risk Settings – Adjust pullback %, stop-loss, and take-profit! 🛠️

✅ Backtest-Friendly – See how the strategy performs over time! 🔍

⸻

🎯 How It Works

📌 Step 1: Detects a Bullish Impulse Bar

🔹 Large green candle 🚀

🔹 Candle range > ATR multiplier

🔹 Volume > Average volume threshold

📌 Step 2: Confirms a Valid Pullback

🔸 Pullback must stay within % range of the impulse move 📉

🔸 If the pullback is too deep or takes too long, the setup is ignored ⛔

📌 Step 3: First Candle to Make a New High 📈

🔹 When a candle breaks the previous high and volume confirms, go long! 💰

🔹 Stop-Loss set at pullback low

🔹 Take-Profit at Risk:Reward (R:R) Target 🎯

⸻

🔥 Best For

💎 Scalpers & Day Traders – Capture short-term breakout momentum! ⚡

📊 Backtesters – Optimize ATR, volume, and pullback rules for best performance! 🧪

⏳ Morning Momentum Traders – Focus on 9:30-12:00 AM EST for higher probability setups!

⸻

🚨 Important Notes

🔹 This strategy is not financial advice! 📜

🔹 Always backtest & paper trade before using real money! 📉📈

🔹 Volatility varies – Customize settings based on your trading style! 🔧

🚀 Like this script? Give it a try & let us know how it works for you! 🔥👊

⸻

Ultimate Stochastics Strategy by NHBprod Use to Day Trade BTCHey All!

Here's a new script I worked on that's super simple but at the same time useful. Check out the backtest results. The backtest results include slippage and fees/commission, and is still quite profitable. Obviously the profitability magnitude depends on how much capital you begin with, and how much the user utilizes per order, but in any event it seems to be profitable according to backtests.

This is different because it allows you full functionality over the stochastics calculations which is designed for random datasets. This script allows you to:

Designate ANY period of time to analyze and study

Choose between Long trading, short trading, and Long & Short trading

It allows you to enter trades based on the stochastics calculations

It allows you to EXIT trades using the stochastics calculations or take profit, or stop loss, Or any combination of those, which is nice because then the user can see how one variable effects the overall performance.

As for the actual stochastics formula, you get control, and get to SEE the plot lines for slow K, slow D, and fast K, which is usually not considered.

You also get the chance to modify the smoothing method, which has not been done with regular stochastics indicators. You get to choose the standard simple moving average (SMA) method, but I also allow you to choose other MA's such as the HMA and WMA.

Lastly, the user gets the option of using a custom trade extender, which essentially allows a buy or sell signal to exist for X amount of candles after the initial signal. For example, you can use "max bars since signal" to 1, and this will allow the indicator to produce an extra sequential buy signal when a buy signal is generated. This can be useful because it is possible that you use a small take profit (TP) and quickly exit a profitable trade. With the max bars since signal variable, you're able to reenter on the next candle and allow for another opportunity.

Let me know if you have any questions! Please take a look at the performance report and let me know your thoughts! :)

Hyperbolic Tangent SuperTrend [InvestorUnknown]The Hyperbolic Tangent SuperTrend (HTST) is designed for technical analysis, particularly in markets with assets that have lower prices or price ratios. This indicator leverages the Hyperbolic Tangent Moving Average (HTMA), a custom moving average calculated using the hyperbolic tangent function, to smooth price data and reduce the impact of short-term volatility.

Hyperbolic Tangent Moving Average (HTMA):

The indicator's core uses a hyperbolic tangent function to calculate a smoothed average of the price. The HTMA provides enhanced trend-following capabilities by dampening the impact of sharp price swings and maintaining a focus on long-term market movements.

The hyperbolic tangent function (tanh) is commonly used in mathematical fields like calculus, machine learning and signal processing due to its properties of “squashing” inputs into a range between -1 and 1. The function provides a non-linear transformation that can reduce the impact of extreme values while retaining a certain level of smoothness.

tanh(x) =>

e_x = math.exp(x)

e_neg_x = math.exp(-x)

(e_x - e_neg_x) / (e_x + e_neg_x)

The HTMA is calculated by taking the difference between the price and its simple moving average (SMA), applying a multiplier to control sensitivity, and then transforming it using the hyperbolic tangent function.

htma(src, len, mul) =>

tanh_src = tanh((src - ta.sma(src, len)) * mul) * ta.stdev(src, len) + ta.sma(src, len)

htma = ta.sma(tanh_src, len)

Important Note: The Hyperbolic Tangent function becomes less accurate with very high prices. For assets priced above 100,000, the results may deteriorate, and for prices exceeding 1 million, the function may stop functioning properly. Therefore, this indicator is better suited for assets with lower prices or lower price ratios.

SuperTrend Calculation:

In addition to the HTMA, the indicator includes an Average True Range (ATR)-based SuperTrend calculation, which helps identify uptrends and downtrends in the market. The SuperTrend is adjusted dynamically using the HTMA to avoid false signals in fast-moving markets.

The ATR period and multiplier are customizable, allowing users to fine-tune the sensitivity of the trend signals.

pine_supertrend(src, calc_price, atrPeriod, factor) =>

atr = ta.atr(atrPeriod)

upperBand = src + factor * atr

lowerBand = src - factor * atr

prevLowerBand = nz(lowerBand )

prevUpperBand = nz(upperBand )

lowerBand := lowerBand > prevLowerBand or calc_price < prevLowerBand ? lowerBand : prevLowerBand

upperBand := upperBand < prevUpperBand or calc_price > prevUpperBand ? upperBand : prevUpperBand

int _direction = na

float superTrend = na

prevSuperTrend = superTrend

if na(atr )

_direction := 1

else if prevSuperTrend == prevUpperBand

_direction := calc_price > upperBand ? -1 : 1

else

_direction := calc_price < lowerBand ? 1 : -1

superTrend := _direction == -1 ? lowerBand : upperBand

Inbuilt Backtest Mode:

The HTST includes an inbuilt backtest mode that enables users to test the indicator's performance against historical data, similar to TradingView strategies.

The backtest mode allows you to compare the performance of different indicator settings with a simple buy and hold strategy to assess its effectiveness in different market conditions.

Hint Table for Display Modes:

The indicator includes a Hint Table that recommends the best pane to use for different display modes. For example, it suggests using the "Overlay" mode in the same pane as the price action, while the "Backtest Mode" is better suited for a separate pane. This ensures a more organized and clear visual experience.

The Hint Table appears as a small table at the bottom of the chart with easy-to-follow recommendations, ensuring the best setup for both visual clarity and indicator functionality.

With these features, the Hyperbolic Tangent SuperTrend Indicator offers traders a versatile and customizable tool for analyzing price trends while providing additional functionalities like backtesting and display mode hints for optimal usability.

Drip's 11am rule breakout/breakdown (OG)This indicator is based on Drippy2hard's 11:30 am (EST) rule.

In simple terms the rule states that:

If a trending stock makes a new high after 11:15-11:30am EST, there is a 75% chance of closing within 1% of High of day (HOD). Same applies for downtrend.

Please note:

Not all stocks will abide by this, this is backtested on stocks with avg daily volume > 2M and mostly mega cap stocks which have liquid option chains. The backtesting results show very promising results on $SPY/ $SPX so it is advised to trade $SPY/ $SPX using this indicator over any other stocks.

Although the name suggests 11 AM rule, the backtesting shows higher win rate for 11:30 AM so please select that option in the settings.

As always, no indicator is perfect and please follow your risk management and understand that indicators are tools to aid your trading and by no means they are supposed to work as intended in all scenarios

How the script works

1. A HOD/LOD zone is identified based on regular session (9:30am-11:30am) EST. Users can select cut off time to 11AM in the settings. These will be indicated on chart after 11/11:30pm depending on what user selected

2. If the stock breaks above the HOD and the ADX is showing strong momentum to upside then the candlesticks will start showing neon color, if the trend based on moving averages and candle closing is also bullish then the indicator will show trend arrows under the candle indicating to stay in the trade. Same applies for break below LOD, only the colors will change to represent downtrend.

3. An optional cloud is also shown if the trend is developed. The cloud can be used as trail stop or re entry point as long as it is displayed on chart

How to use the indicator in trading

In general, there are three scenarios which are trade worthy

1. If the stocks breaks out above the HOD zone and up trend develops or the stocks breaks below the LOD zone and downtrend develops. See images below

2. You can also use the LOD/HOD zone as demand/ supply if the Price action is range bound like this example below

Thanks for reading, please give thumbs up if you like using it! Please post comments on how to use it.