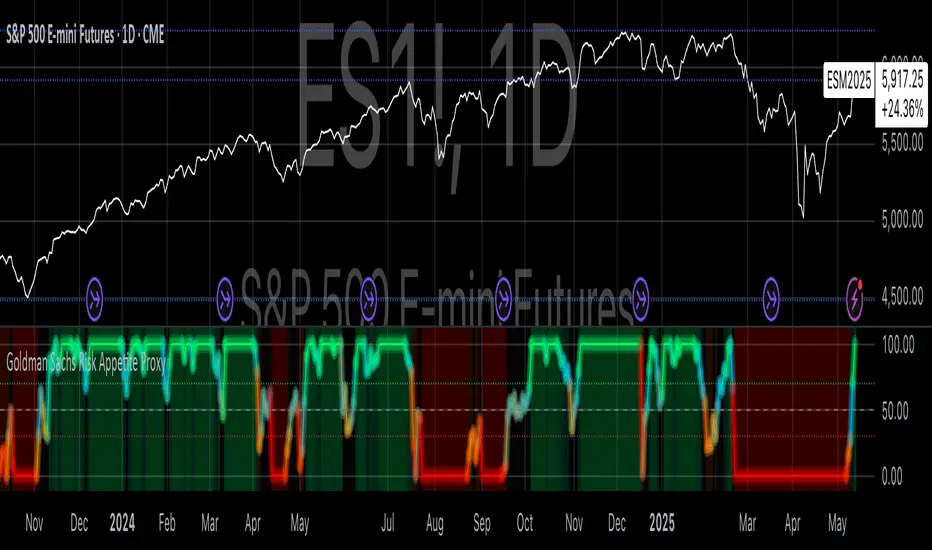

Goldman Sachs Risk Appetite ProxyRisk appetite indicators serve as barometers of market psychology, measuring investors' collective willingness to engage in risk-taking behavior. According to Mosley & Singer (2008), "cross-asset risk sentiment indicators provide valuable leading signals for market direction by capturing the underlying psychological state of market participants before it fully manifests in price action."

The GSRAI methodology aligns with modern portfolio theory, which emphasizes the importance of cross-asset correlations during different market regimes. As noted by Ang & Bekaert (2002), "asset correlations tend to increase during market stress, exhibiting asymmetric patterns that can be captured through multi-asset sentiment indicators."

Implementation Methodology

Component Selection

Our implementation follows the core framework outlined by Goldman Sachs research, focusing on four key components:

Credit Spreads (High Yield Credit Spread)

As noted by Duca et al. (2016), "credit spreads provide a market-based assessment of default risk and function as an effective barometer of economic uncertainty." Higher spreads generally indicate deteriorating risk appetite.

Volatility Measures (VIX)

Baker & Wurgler (2006) established that "implied volatility serves as a direct measure of market fear and uncertainty." The VIX, often called the "fear gauge," maintains an inverse relationship with risk appetite.

Equity/Bond Performance Ratio (SPY/IEF)

According to Connolly et al. (2005), "the relative performance of stocks versus bonds offers significant insight into market participants' risk preferences and flight-to-safety behavior."

Commodity Ratio (Oil/Gold)

Baur & McDermott (2010) demonstrated that "gold often functions as a safe haven during market turbulence, while oil typically performs better during risk-on environments, making their ratio an effective risk sentiment indicator."

Standardization Process

Each component undergoes z-score normalization to enable cross-asset comparisons, following the statistical approach advocated by Burdekin & Siklos (2012). The z-score transformation standardizes each variable by subtracting its mean and dividing by its standard deviation: Z = (X - μ) / σ

This approach allows for meaningful aggregation of different market signals regardless of their native scales or volatility characteristics.

Signal Integration

The four standardized components are equally weighted and combined to form a composite score. This democratic weighting approach is supported by Rapach et al. (2010), who found that "simple averaging often outperforms more complex weighting schemes in financial applications due to estimation error in the optimization process."

The final index is scaled to a 0-100 range, with:

Values above 70 indicating "Risk-On" market conditions

Values below 30 indicating "Risk-Off" market conditions

Values between 30-70 representing neutral risk sentiment

Limitations and Differences from Original Implementation

Proprietary Components

The original Goldman Sachs indicator incorporates additional proprietary elements not publicly disclosed. As Goldman Sachs Global Investment Research (2019) notes, "our comprehensive risk appetite framework incorporates proprietary positioning data and internal liquidity metrics that enhance predictive capability."

Technical Limitations

Pine Script v6 imposes certain constraints that prevent full replication:

Structural Limitations: Functions like plot, hline, and bgcolor must be defined in the global scope rather than conditionally, requiring workarounds for dynamic visualization.

Statistical Processing: Advanced statistical methods used in the original model, such as Kalman filtering or regime-switching models described by Ang & Timmermann (2012), cannot be fully implemented within Pine Script's constraints.

Data Availability: As noted by Kilian & Park (2009), "the quality and frequency of market data significantly impacts the effectiveness of sentiment indicators." Our implementation relies on publicly available data sources that may differ from Goldman Sachs' institutional data feeds.

Empirical Performance

While a formal backtest comparison with the original GSRAI is beyond the scope of this implementation, research by Froot & Ramadorai (2005) suggests that "publicly accessible proxies of proprietary sentiment indicators can capture a significant portion of their predictive power, particularly during major market turning points."

References

Ang, A., & Bekaert, G. (2002). "International Asset Allocation with Regime Shifts." Review of Financial Studies, 15(4), 1137-1187.

Ang, A., & Timmermann, A. (2012). "Regime Changes and Financial Markets." Annual Review of Financial Economics, 4(1), 313-337.

Baker, M., & Wurgler, J. (2006). "Investor Sentiment and the Cross-Section of Stock Returns." Journal of Finance, 61(4), 1645-1680.

Baur, D. G., & McDermott, T. K. (2010). "Is Gold a Safe Haven? International Evidence." Journal of Banking & Finance, 34(8), 1886-1898.

Burdekin, R. C., & Siklos, P. L. (2012). "Enter the Dragon: Interactions between Chinese, US and Asia-Pacific Equity Markets, 1995-2010." Pacific-Basin Finance Journal, 20(3), 521-541.

Connolly, R., Stivers, C., & Sun, L. (2005). "Stock Market Uncertainty and the Stock-Bond Return Relation." Journal of Financial and Quantitative Analysis, 40(1), 161-194.

Duca, M. L., Nicoletti, G., & Martinez, A. V. (2016). "Global Corporate Bond Issuance: What Role for US Quantitative Easing?" Journal of International Money and Finance, 60, 114-150.

Froot, K. A., & Ramadorai, T. (2005). "Currency Returns, Intrinsic Value, and Institutional-Investor Flows." Journal of Finance, 60(3), 1535-1566.

Goldman Sachs Global Investment Research (2019). "Risk Appetite Framework: A Practitioner's Guide."

Kilian, L., & Park, C. (2009). "The Impact of Oil Price Shocks on the U.S. Stock Market." International Economic Review, 50(4), 1267-1287.

Mosley, L., & Singer, D. A. (2008). "Taking Stock Seriously: Equity Market Performance, Government Policy, and Financial Globalization." International Studies Quarterly, 52(2), 405-425.

Oppenheimer, P. (2007). "A Framework for Financial Market Risk Appetite." Goldman Sachs Global Economics Paper.

Rapach, D. E., Strauss, J. K., & Zhou, G. (2010). "Out-of-Sample Equity Premium Prediction: Combination Forecasts and Links to the Real Economy." Review of Financial Studies, 23(2), 821-862.

스크립트에서 "N+credit最新动态"에 대해 찾기

Liquidity Stress Index SOFR - IORBLiquidity Stress Index (SOFR - IORB)

This indicator tracks the spread between the Secured Overnight Financing Rate (SOFR) and the Interest on Reserve Balances (IORB) set by the Federal Reserve.

A persistently positive spread may indicate funding stress or liquidity shortages in the repo market, as it suggests overnight lending rates exceed the risk-free rate banks earn at the Fed.

Useful for monitoring monetary policy transmission or market/liquidity stress.

SemaforThis is the 4 Level Semafor indicator with Daily Open Line and Average Session Range. Also on the chart is the EMA Ribbon indicator.

Credit to:

Devlucem for the Semafor indicator

Quantvue for the Average Session Range

Shusterivi for the Daily Open Line

MYNAMEISBRANDON for the EMA Ribbon

The Semafors are based on the ZigZag indicator and show higher highs/lower lows of a specified period, determined by the user and applied in settings.

The default periods I use are:

10 period (hidden on this chart)

50 period-blue dots

250 period-white dots

615 period-black dots

Just as the ZigZag indicator will recalculate so to will the semafors, as additional candles are built. The semafor indicator is never to be used as a stand alone signal. It must be combined with other indicators to be used effectively. What we look for are the semafor patterns of a large white dot followed by a 1st blue dot opposite of the white. Then a 2nd blue dot in agreement with the white dot. In theory, the 2nd blue dot is seen as confirmation of the establishment of the white semafor..

When combined with Daily Open Line, ADR (Average Sessions Range), EMA cross and VWAP anchored to your 250 semafors, your odds are greatly increased. Add to that the knowledge of basic market structure and the wisdom that comes from patience and you have a very powerful weapon.

The Daily Open...I trade the M1 chart and also draw a H4 Open Line on my chart for the smaller time frames. Price will tend to trade away from the Daily Open Line. In many cases until it reaches certain levels...Fib, Gann, ADR, etc., then runs through a pullback cycle. I like the ADR levels. The ADR can give clues when entering a consolidation phase, ie trading between the buy side and sell side 15% levels. Trading away from the Daily Open(or H4 open) along with breaking the 15% level, while in agreement with a semafor pattern is a good sign.

Add to that confluence the agreement of your MA cross and the 250 semafor Anchored VWAP and you have a solid signal to help determine your actions. This trend following layout will work on any time frame. I just really like the M1 for its precision, not for crazy back and forth all day. With the exception of some strong pull back signals, I don't enter any more trades on the M1 than on M5, 15 or 30.

This is based on and follows the teachings of Xard and his trading strategy. Just as I don't want to take anyone's credit for these indicators, I won't take credit for what I have been taught either.

The trader can obviously use their favorite MA cross indicator. But this one is visually beautiful AND displays the current time frame and 1 time frame higher on the chart...awesome!

Of note, I do run into trouble at times with the 615 period semafor. I have been told it is because TradingView has trouble with extended period indicators. As a matter of fact, I would like a much higher period for my biggest semafor. I would like it set at 1250, but that seems to be a no starter. If anyone has a solution, that would be welcomed news.

Best Buffett Ratio w/ Std-Dev Offset + Conditional PlotSummary:

This script provides a visually clear way to track the so-called “Buffett Ratio,”

a popular market valuation gauge which compares the total US stock market cap

to the country’s GDP. In addition, it plots a “hardcoded” long-term trend line,

along with fixed standard-deviation bands (in log space), and uses background colors

to signal potentially overvalued or undervalued zones.

What Is the Buffett Ratio?

Often credited to Warren Buffett, the Buffett Ratio (or Buffett Indicator) measures:

(Total US Stock Market Capitalization) / (US GDP)

• A higher ratio typically means equities are more expensive relative to the size of the economy.

• A lower ratio suggests equities may be more attractively valued compared to GDP.

Historically, the ratio has tended to drift upward over many decades,

as the US economy and stock markets grow, but it still oscillates around some trend over time.

How to Use

1) Add to Chart:

- In TradingView, simply apply the indicator (it internally fetches CRSPTM1 & GDP data).

2) Tweak Inputs:

- Log Offset for 1σ: Adjust how wide the ±1σ/±2σ bands appear around the trend.

- Anchor Points: Edit startYear , endYear , startRatio , endRatio

if you want a different slope or different “fair value” anchors.

3) Interpretation:

- If the indicator is above +2σ (red line) , it’s historically “very expensive,”

often leading to lower future returns over the long term.

- If it’s below –2σ (green line) , it’s historically “deep undervaluation,”

often pointing to better future returns over time.

- The intermediate zones show degrees of mild over- or undervaluation.

How This Script Works

1) Buffett Ratio Calculation:

- The script requests data from TradingView’s built-in CRSPTM1 index (total US market cap).

- It also requests US GDP data via request.economic("US", "GDP") .

- If GDP data is missing, the ratio becomes na on that bar.

2) Hardcoded Trend Line:

- Rather than a rolling average, the script uses two “anchors” (e.g. 1950 → 0.30 ratio, 2024 → 1.25 ratio)

and solves for a single log-growth rate to produce a steady upward slope.

3) Fixed Standard Deviations in Log Space:

- The script takes the log of the trend line, then applies a fixed offset for ±1σ and ±2σ,

creating proportional bands that do not “expand/contract” from a rolling window.

4) Conditional Plotting:

- The script only begins plotting once the Buffett Ratio actually has data (around 2011).

5) Color-Coded Zones:

- Above +2σ: red background (historically very expensive)

- Between +1σ and +2σ: yellow background (moderately expensive)

- Between –1σ and +1σ: no background color (around normal)

- Between –2σ and –1σ: aqua background (moderately undervalued)

- Below –2σ: green background (historically deep undervaluation)

Final Notes

• Data Limitations: US GDP data and CRSPTM1 only go back so far, so this starts around 2011.

• Long-Term vs. Short-Term: Best viewed on monthly/quarterly charts and interpreted over years.

• Tuning: If you believe structural changes have shifted the ratio’s fair slope,

adjust the code’s anchors or log offsets.

Enjoy, and use responsibly!

Financial Crisis Predictor - Doomsday ClockThe **Financial Crisis Predictor - Doomsday Clock** is a composite indicator that evaluates multiple market conditions to determine financial risk levels. It combines four key metrics: market volatility (via VIX), yield curve spread, stock market momentum, and credit risk (via high-yield spread). Each metric contributes to a weighted "risk score," scaled between 0 and 100, which helps gauge the probability of a financial crisis. Here's a breakdown of how it works:

### 1. **Market Volatility (VIX)**

- **How it's measured:**

- Uses the VIX index, which represents expected market volatility.

- Applies two exponential moving averages (EMAs) to smooth out the data—one fast and one slow.

- Triggers a signal if the fast EMA crosses above the slow EMA and VIX exceeds a defined threshold (default is 30).

- **Weighting:**

- Contributes up to 35% of the total risk score when active.

### 2. **Yield Curve Spread**

- **How it's measured:**

- Takes the difference between the yields of 10-year and 2-year U.S. Treasury bonds (inversion indicates recession risk).

- If the spread drops below a certain threshold (default is 0.2), it signals a potential recession.

- **Weighting:**

- Contributes up to 25% of the risk score.

### 3. **Stock Market Momentum**

- **How it's measured:**

- Analyzes the S&P 500 (SPY) using a 20-day EMA for price momentum.

- Checks for a cross under the 20-day EMA and if the 5-day rate of change (ROC) is less than -2.

- This combination signals bearish market momentum.

- **Weighting:**

- Contributes up to 20% of the risk score.

### 4. **Credit Risk (High Yield Spread)**

- **How it's measured:**

- Assesses high-yield corporate bond spreads using EMAs, similar to the VIX logic.

- A crossover of the fast EMA above the slow EMA combined with spreads exceeding a defined threshold (default is 5.0) indicates increased credit risk.

- **Weighting:**

- Contributes up to 20% of the total risk score.

### 5. **Risk Score Calculation**

- The final **risk score** ranges from 0 to 100 and is calculated using the weighted sum of the four indicators.

- The score is smoothed to minimize false signals and maintain stability.

### 6. **Risk Zones**

- **Extreme Risk:** If the risk score is ≥ 75, indicating a severe crisis warning.

- **High Risk:** If the risk score is between 15 and 75, signaling heightened risk.

- **Moderate Risk:** If the risk score is between 10 and 15, representing potential concerns.

- **Low Risk:** If the risk score is < 10, suggesting stable conditions.

### 7. **Visual & Alerts**

- The indicator plots the risk score on a chart with color-coded backgrounds to indicate risk levels: green (low), yellow (moderate), orange (high), and red (extreme).

- Alert conditions are set for each risk zone, notifying users when the risk level transitions into a higher zone.

This indicator aims to quickly detect potential financial crises by aggregating signals from key market factors, making it a versatile tool for traders, analysts, and risk managers.

Butterfly Harmonic Pattern [TradingFinder] Harmonic Detector🔵 Introduction

The Butterfly Harmonic Pattern is a sophisticated and highly regarded tool in technical analysis, utilized by traders to identify potential reversal points in the financial markets. This pattern is distinguished by its reliance on Fibonacci ratios and geometric configurations, which aid in predicting price movements with remarkable precision.

The origin of the Butterfly Harmonic Pattern can be traced back to the pioneering work of Bryce Gilmore, who is credited with discovering this pattern. Gilmore's extensive research and expertise in Fibonacci ratios laid the groundwork for the identification and application of this pattern in technical analysis.

The Butterfly pattern, like other harmonic patterns, is based on the principle that market movements are not random but follow specific structures and ratios.

The pattern is characterized by a distinct "M" shape in bullish scenarios and a "W" shape in bearish scenarios, each indicating a potential reversal point. These formations are identified by specific Fibonacci retracement and extension levels, making the Butterfly pattern a powerful tool for traders seeking to capitalize on market turning points.

The precise nature of the Butterfly pattern allows for the accurate prediction of target prices and the establishment of strategic entry and exit points, making it an indispensable component of a trader's analytical arsenal.

Bullish :

Bearish :

🔵 How to Use

Like other harmonic patterns, the Butterfly pattern is categorized based on how it forms at the end of an uptrend or downtrend. Unlike the Gartley and Bat patterns, the Butterfly pattern, similar to the Crab pattern, forms outside the wave 3 range at the end of a rally.

🟣 Types of Butterfly Harmonic Patterns

🟣 Bullish Butterfly Pattern

This pattern forms at the end of a downtrend and leads to a trend reversal from a downtrend to an uptrend.

🟣 Bearish Butterfly Pattern

In contrast to the Bullish Butterfly pattern, this pattern forms at the end of an uptrend and warns analysts of a trend reversal to a downtrend. In this case, traders are encouraged to shift their trading stance from buy trades to sell trades.

Advantages and Limitations of the Butterfly Pattern in Technical Analysis :

The Butterfly pattern is considered one of the precise and stable tools in financial market analysis. However, it is always important to pay special attention to the advantages and limitations of each pattern.

Here, we review the advantages and disadvantages of using the Butterfly harmonic pattern :

The main advantage of the Butterfly pattern is providing very accurate signals.

Using Fibonacci golden ratios and geometric rules, the Butterfly pattern identifies patterns accurately and systematically. (This high accuracy significantly helps investors in making trading decisions.)

Identifying this pattern requires expertise and experience in technical analysis.

Recognizing the Butterfly pattern might be complex for beginner traders. (Correct identification of the pattern necessitates mastery over geometric principles and Fibonacci ratios.)

The Butterfly harmonic pattern might issue false trading signals. (Traders usually combine the Butterfly pattern with other technical tools to confirm buy and sell signals.)

🔵 Setting

🟣 Logical Setting

ZigZag Pivot Period : You can adjust the period so that the harmonic patterns are adjusted according to the pivot period you want. This factor is the most important parameter in pattern recognition.

Show Valid Forma t: If this parameter is on "On" mode, only patterns will be displayed that they have exact format and no noise can be seen in them. If "Off" is, the patterns displayed that maybe are noisy and do not exactly correspond to the original pattern.

Show Formation Last Pivot Confirm : if Turned on, you can see this ability of patterns when their last pivot is formed. If this feature is off, it will see the patterns as soon as they are formed. The advantage of this option being clear is less formation of fielded patterns, and it is accompanied by the latest pattern seeing and a sharp reduction in reward to risk.

Period of Formation Last Pivot : Using this parameter you can determine that the last pivot is based on Pivot period.

🟣 Genaral Setting

Show : Enter "On" to display the template and "Off" to not display the template.

Color : Enter the desired color to draw the pattern in this parameter.

LineWidth : You can enter the number 1 or numbers higher than one to adjust the thickness of the drawing lines. This number must be an integer and increases with increasing thickness.

LabelSize : You can adjust the size of the labels by using the "size.auto", "size.tiny", "size.smal", "size.normal", "size.large" or "size.huge" entries.

🟣 Alert Setting

Alert : On / Off

Message Frequency : This string parameter defines the announcement frequency. Choices include: "All" (activates the alert every time the function is called), "Once Per Bar" (activates the alert only on the first call within the bar), and "Once Per Bar Close" (the alert is activated only by a call at the last script execution of the real-time bar upon closing). The default setting is "Once per Bar".

Show Alert Time by Time Zone : The date, hour, and minute you receive in alert messages can be based on any time zone you choose. For example, if you want New York time, you should enter "UTC-4". This input is set to the time zone "UTC" by default.

Scalper's Volatility Filter [QuantraSystems]Scalpers Volatility Filter

Introduction

The 𝒮𝒸𝒶𝓁𝓅𝑒𝓇'𝓈 𝒱𝑜𝓁𝒶𝓉𝒾𝓁𝒾𝓉𝓎 𝐹𝒾𝓁𝓉𝑒𝓇 (𝒮𝒱𝐹) is a sophisticated technical indicator, designed to increase the profitability of lower timeframe trading.

Due to the inherent decrease in the signal-to-noise ratio when trading on lower timeframes, it is critical to develop analysis methods to inform traders of the optimal market periods to trade - and more importantly, when you shouldn’t trade.

The 𝒮𝒱𝐹 uses a blend of volatility and momentum measurements, to signal the dominant market condition - trending or ranging.

Legend

The 𝒮𝒱𝐹 consists of a signal line that moves above and below a central zero line, serving as the indication of market regime.

When the signal line is positioned above zero, it indicates a period of elevated volatility. These periods are more profitable for trading, as an asset will experience larger price swings, and by design, trend-following indicators will give less false signals.

Conversely, when the signal line moves below zero, a low volatility or mean-reverting market regime dominates.

This distinction is critical for traders in order to align strategies with the prevailing market behaviors - leveraging trends in volatile markets and exercising caution or implementing mean-reversion systems in periods of lower volatility.

Case Study

Here we can see the indicator's unique edge in action.

Out of the four potential long entries seen on the chart - displayed via bar coloring, two would result in losses.

However, with the power of the 𝒮𝒱𝐹 a trader can effectively filter false signals by only entering momentum-trades when the signal line is above zero.

In this small sample of four trades, the 𝒮𝒱𝐹 increased the win rate from 50% to 100%

Methodology

The methodology behind the 𝒮𝒱𝐹 is based upon three components:

By calculating and contrasting two ATR’s, the immediate market momentum relative to the broader, established trend is calculated. The original method for this can be credited to the user @xinolia

A modified and smoothed ADX indicator is calculated to further assess the strength and sustainability of trends.

The ‘Linear Regression Dispersion’ measures price deviations from a fitted regression line, adding further confluence to the signals representation of market conditions.

Together, these components synthesize a robust, balanced view of market conditions, enabling traders to help align strategies with the prevailing market environment, in order to potentially increase expected value and win rates.

[blackcat] L2 Fibonacci BandsThe concept of the Fibonacci Bands indicator was described by Suri Dudella in his book "Trade Chart Patterns Like the Pros" (Section 8.3, page 149). These bands are derived from Fibonacci expansions based on a fixed moving average, and they display potential areas of support and resistance. Traders can utilize the Fibonacci Bands indicator to identify key price levels and anticipate potential reversals in the market.

To calculate the Fibonacci Bands indicator, three Keltner Channels are applied. These channels help in determining the upper and lower boundaries of the bands. The default Fibonacci expansion levels used are 1.618, 2.618, and 4.236. These levels act as reference points for traders to identify significant areas of support and resistance.

When analyzing the price action, traders can focus on the extreme Fibonacci Bands, which are the upper and lower boundaries of the bands. If prices trade outside of the bands for a few bars and then return inside, it may indicate a potential reversal. This pattern suggests that the price has temporarily deviated from its usual range and could be due for a correction.

To enhance the accuracy of the Fibonacci Bands indicator, traders often use multiple time frames. By aligning short-term signals with the larger time frame scenario, traders can gain a better understanding of the overall market trend. It is generally advised to trade in the direction of the larger time frame to increase the probability of success.

In addition to identifying potential reversals, traders can also use the Fibonacci Bands indicator to determine entry and exit points. Short-term support and resistance levels can be derived from the bands, providing valuable insights for trade decision-making. These levels act as reference points for placing stop-loss orders or taking profits.

Another useful tool for analyzing the trend is the slope of the midband, which is the middle line of the Fibonacci Bands indicator. The midband's slope can indicate the strength and direction of the trend. Traders can monitor the slope to gain insights into the market's momentum and make informed trading decisions.

The Fibonacci Bands indicator is based on the concept of Fibonacci levels, which are support or resistance levels calculated using the Fibonacci sequence. The Fibonacci sequence is a mathematical pattern that follows a specific formula. A central concept within the Fibonacci sequence is the Golden Ratio, represented by the numbers 1.618 and its inverse 0.618. These ratios have been found to occur frequently in nature, architecture, and art.

The Italian mathematician Leonardo Fibonacci (1170-1250) is credited with introducing the Fibonacci sequence to the Western world. Fibonacci noticed that certain ratios could be calculated and that these ratios correspond to "divine ratios" found in various aspects of life. Traders have adopted these ratios in technical analysis to identify potential areas of support and resistance in financial markets.

In conclusion, the Fibonacci Bands indicator is a powerful tool for traders to identify potential reversals, determine entry and exit points, and analyze the overall trend. By combining the Fibonacci Bands with other technical indicators and using multiple time frames, traders can enhance their trading strategies and make more informed decisions in the market.

Fisher+ [OSC]The Fisher Transform Indicator is classified as an oscillator, meaning that its value swings above and below a central point. This characteristic allows traders to identify overbought and oversold conditions, providing potential clues about market reversals. As mentioned previously, it is an oscillator so the strength of the move is displayed by how long the fisher line stays above/below zero. Indicator can be used to aid in confluence near supply/demand zones.

White Line = Fisher

Red/Blue Line = Moving Average

--Changes color whether fisher line is above/below the MA

Red/Blue Shaded Line = Moving Average

--Changes color based on a smoothing factor

Red/Blue Shaded Fill = Asset in Overbought/Oversold Conditions

Red/Blue Circles = Asset in Extreme Overbought/Oversold Conditions

Red/Blue Triangles = MACD Signals Below/Above "0"

Divergence Labels = Asset Signaling Divergence

The moving average line will turn red/blue as long as the fisher line is below/above the moving average. The shaded MA line will switch colors based on if it is moving in an up/down trend. The MA can also be used as a signal and treated similar to an oscillator. Market trending conditions will either keep the MA below/above the dashed zero line.

MACD code credited to LazyBear's MACD Leader indicator. It is used to filter out/confirm any signals such as divergences. As long as the MACD Leader line is above both the MACD line and signal lines then it'll signal with with a triangle. MACD divergences will be added at a later time.

SOLANA Performance & Volatility Analysis BB%Overview:

The script provides an in-depth analysis of Solana's performance and volatility. It showcases Solana's price, its inverse relationship, its own volatility, and even juxtaposes it against Bitcoin's 24-hour historical volatility. All of these are presented using the Bollinger Bands Percentage (BB%) methodology to normalise the price and volatility values between 0 and 1.

Key Components:

Inputs:

SOLANA PRICE (SOLUSD): The price of Solana.

SOLANA INVERSE (SOLUSDT.3S): The inverse of Solana's price.

SOLANA VOLATILITY (SOLUSDSHORTS): Volatility for Solana.

BITCOIN 24 HOUR HISTORICAL VOLATILITY (BVOL24H): Bitcoin's volatility over the past 24 hours.

BB Calculations:

The script uses the Bollinger Bands methodology to calculate the mean (SMA) and the standard deviation of the prices and volatilities over a certain period (default is 20 periods). The calculated upper and lower bands help in normalising the values to the range of 0 to 1.

Normalised Metrics Plotting:

For better visualisation and comparative analysis, the normalised values for:

Solana Price

Solana Inverse

Solana Volatility

Bitcoin 24hr Volatility

are plotted with steplines.

Band Plotting:

Bands are plotted at 20%, 40%, 60%, and 80% levels to serve as reference points. The area between the 40% and 60% bands is shaded to highlight the median region.

Colour Coding:

Different colours are used for easy differentiation:

Solana Price: Blue

Solana Inverse: Red

Solana Volatility: Green

Bitcoin 24hr Volatility: White

Licence & Creator:

The script adheres to the Mozilla Public Licence 2.0 and is credited to the author, "Volatility_Vibes".

Works well with Breaks and Retests with Volatility Stop

Feigenbaum ProjectionsThe theory of price delivery per Feigenbaum projections is credited to TRSTNGLRD, this indicator aims to aid traders from all backgrounds to utilize projections for determination of potential future price moves.

What follows is the simplest description of where to anchor the projection:

As price delivers and clears higher high (buy side liquidity) then reverses to clear most recent low (sell side liquidity), this becomes the anchorage point for the Feigenbaum projection and is referred to as perturbation. The start and end points for the projection should be only those candle bodies that wholly exist within the range within the high and low that were cleared by the perturbation, this range of candle bodies is to be considered the "initial condition". Structure that appears as a broadening formation is one such price delivery occurrence that can be utilized with these projections.

The projected zones are all pre-configured by TRSTNs specifications per Feigenbaum but can be adjusted if the need arises.

Price is expected to expand beyond the initial condition and into the negative and positive target zones, accuracy diminishes with further expansion and reevaluation should occur when a new perturbation is discovered.

It's recommended to explore various timeframes to find a perturbation by which to anchor the next Feigenbaum projection.

I'll do my best to update this description with time as more discoveries are made and TRSTNGLRD provides more guidance and feedback on this indicator.

Pythagorean Moving Averages (and more)When you think of the question "take the mean of this dataset", you'd normally think of using the arithmetic mean because usually the norm is equal to 1; however, there are an infinite number of other types of means depending on the function norm (p).

Pythagoras' is credited for the main types of means: his harmonic mean, his geometric mean, and his arithmetic mean:

Harmonic Average (p = -1):

- Take the reciprocal of all the numbers in the dataset, add them all together, divide by the amount of numbers added together, then take the reciprocal of the final answer.

Geometric Average (p = 0):

- Multiply all the numbers in the dataset, then take the nth root where n is equal to the amount of number you multiplied together.

Arithmetic Mean (p = 1):

- Add all the numbers in the dataset, then divide by the amount of numbers you added by.

A couple other means included in this script were the quadratic mean (p = 2) and the cubic mean (p = 3).

Quadratic Mean (p = 2):

- Square every number in the dataset, then divide by the amount of numbers your added by, then take the square root.

Cubic Mean (p = 3):

- Cube every number in the dataset, then divide by the amount of numbers you added by, then take the cube root.

There are an infinite number of means for every scenario of p, but they begin to follow a pattern after p = 3.

Read more:

www.cs.uni.edu

en.wikipedia.org

en.wikipedia.org

Note : I added the functions for the quadratic mean and cubic mean, but since market charts don't have those types of graphs, the functions don't usually work. It's the same reason why sometimes you'll see the harmonic average not working.

Disclaimer : This is not financial or mathematical advice, please look for someone certified before making any decisions.

VP and POCThis code is credited to juliangonzaconde. Have taken his help to modify his beautiful creation.

Volume profile is a key study when comes to understanding the auction trading process. Volume Profiles will show you exactly how much volume, as well as relative volume, occurred at each price as well as the exact number of contracts for the entire session. It is a visualization tool to understand the high activity zone and low activity zone.

Volume profile measures the confidence of the traders in the market. From short term trading perspective monitoring the developing volume profile in realtime make more sense to track current market participation behavior to take better trading decisions.

Hope this helps you in trading on daily timeframe.

Happy Trading.

Market Trend using First Derivative of MAs + Volatility Based on Smooth First Derivative Indicator by tbiktag

Volatility also from another public TV script, forgot which one though, sorry if this is yours and I haven't credited your work, let me know if it is and I'll reference it properly.

About this indicator:

Estimates whether market is trending up, down or sideways by adding the slope (first derivatives) of a fast & slow MA. Uptrend = Green, Downtrend = Red, Sideways = Yellow

Uses a minimum slope percentile to determine threshold for uptrend, downtrend & sideways. Definitely adjust this when changing timeframes, for BTCUSD at 1 hour timeframe a value of 25 is decent

Also has a measure of Volatility if you're into that

Explanation of inputs:

Bandwidth - for derivative function

Fastma - period for fast Moving Average

Slowma - period for slow Moving Average

Derivmalength - smooths out the signal, reducing single contrasting bars, but delays the signal. Use 1 if don't want to use

V length - ema of volatility if you want to smooth it

Min Slope Percentile - slope should exceed this percentile to be classified as uptrend (green) or downtrend (red) anything in this bottom percentile will be considered sideways

Mine Slope Lookback Period - # of bars back to calculate Slope Percentile

Coinbase to Binance premium indicator/strategy

1) Offers bar/ma chart of premium

2) Offers different trading strats based on premium(ma cross, premium value cross, smoothed premium value cross)

supersmoother code credited to someone else from tradingview

Momentum Acceleration by DGTItalian physicist Galileo Galilei is usually credited with being the first to measure speed by considering the distance covered and the time it takes. Galileo defined speed as the distance covered during a period of time. In equation form, that is v = Δd / Δt where v is speed, Δd is change in distance, and Δt is change in time. The Greek symbol for delta, a triangle (Δ), means change.

Is the speed getting faster or slower?

Acceleration will be the answer, acceleration is defined as the rate of change of speed over a set period of time, meaning something is getting faster or slower. Mathematically expressed, acceleration denoted as a is a = Δv / Δt , where Δv is the change in speed and Δt is the change in time.

How to apply in trading

Lets think about Momentum, Rate of Return, Rate of Change all are calculated in almost same approach with Speed

Momentum measures change in price over a specified time period,

Rate of Change measures percent change in price over a specified time period,

Rate of Return measures the net gain or loss over a specified time period,

And Speed measures change in distance over a specified time period

So we may state that measuring the change in distance is also measuring the change in price over a specified time period which is length, hence

speed can be calculated as (source – source )/length and acceleration becomes (speed – speed )/length

In this study acceleration is used as signal line and result plotted as arrows demonstrating bull or bear direction where direction changes can be considered as trading setups

Just a little fun, since we deal with speed the short name of the study is named after famous cartoon character Speedy Gonzales

Trading success is all about following your trading strategy and the indicators should fit within your trading strategy, and not to be traded upon solely

Disclaimer: The script is for informational and educational purposes only. Use of the script does not constitutes professional and/or financial advice. You alone the sole responsibility of evaluating the script output and risks associated with the use of the script. In exchange for using the script, you agree not to hold dgtrd TradingView user liable for any possible claim for damages arising from any decision you make based on use of the script

JSun - Guppy Multiple Moving AverAgeThe Guppy Multiple Moving Average (GMMA) is a technical indicator that identifies changing trends, breakouts, and trading opportunities in the price of an asset by combining two groups of moving averages (MA) with different time periods. There is a short-term group of MAs, and a long-term group of MA. Both contain six MAs, for a total of 12. The term gets its name from Daryl Guppy, an Australian trader who is credited with its development.

Key Takeaways:

1. The Gruppy Multiple Moving Average (GMMA) is applied as an overlay on the price chart of an asset.

2. The short-term MAs are typically set at 3, 5, 8, 10, 12, and 15 periods. The longer-term MAs are typically set at 30, 35, 40, 45, 50, and 60.

3. When the short-term group of averages moves above the longer-term group, it indicates a price uptrend in the asset could be emerging.

4. When the short-term group falls below the longer-term group of MAs, a price downtrend in the asset could be starting.

5. When there is lots of separation between the MAs, this helps confirm the price trend in the current direction.

6. If both groups become compressed with each other, or crisscross, it indicates the price has paused and a price trend reversal is possible.

7. Traders often trade in the direction the longer-term MA group is moving, and use the short-term group for trade signals to enter or exit.

strategy of RSI with trendlines and S/RBefore I go through this chart I want to acknowledge the great programmers who spent much of their time and effort to assist many TV users and traders.

Thank you to LunaOwl for the RSI American lines her script made me realize the need to have trendlines, supports, and resistance on RSI charts.

Also, a copy of Lij_MC code from was taken which had been credited to Duyck. Thank you Duyck.

The BB was copied from morpheus747

As I researched different strategies one strategy seemed to assist the trader for entry and exits. It was the combination of Support and resistance on the RSI. In addition, diagonal lines (Recently introduced in pine script V4) assists in the direction and reversals that may occur. What is supplied is only a graphical representation and no trade entry or exit points are selected.

On the chart you can use;

• RSI line or bar;

• Bollinger High / Low support line;

• Diagonal trend lines. A primary and a secondary group of trendlines; and

• Trendline candle highlighter.

I am hoping people with great skills could assist to develop this to the next level.

I hope this graphical strategy may help until further development. Enjoy.

Derivative Oscillator Cu [ID: AC-P]The "AC-P" version of the Derivative Oscillator is my personal customized version of Constance Brown's Derivative Oscillator (using Everget's implementation of it as the base), with the the following modifications and additions:

VWAP Indication - option to show whether the price input option is above or below the Daily VWAP (red triangles = price input is below vwap, green triangles = price input is above vwap)

Bullish and Bearish phases from shayankm's Waddah Attar Explosion V2 () is included as indication dots (bullish = blue dots, bearish = yellow dots) below/above the Derivative Oscillator histogram

Coral Trend from Lazybear () is included as indication dots (red/green dots below/above the Derivative Oscillator histogram

Input source options for vwap, Waddah components (MACD, Bollinger Upper/Lower)

Centerline option for Coral trend, and Horizontal center option for the Derivative Oscillator with circle indication (optional - provided as option for flexibility in use with overlaying with other indicators)

This indicator is a hybrid, with a combination of leading indicators and lagging trending indicators combined into one. Specifically, a few of the other indicators I use are lacking in the momentum and trend department, and this is one of the indicators I use to address that:

VWAP provides trend information on lower timeframes from a high timeframe interval (D)

Coral Trend provides additional confirmation to VWAP trend wise, and is adjustable

Waddah Attar Explosion provides a third level of confirmation for trending moves, taking into account shorter and longer timeframes (FastEMA and SlowEMA parameters).

Script base for the Derivative Oscillator is credited to Everget () and LazyBear ().

Source attribution to Constance Brown for the Derivative Oscillator formula/indicator:

// Brown, Constance.

// Reference 1: “The Derivative Oscillator: a New Approach to an Old Problem,” Journal of Technical Analysis (Winter-Spring 1994) 45–61.

// Reference 2: Technical Analysis for the Trading Professional. New York, NY: McGraw-Hill, 1999.

Information on the Derivative Oscillator:

www.investopedia.com

Bitcoin Stock to Flow Multiplethis study plots the price of btc over the Stock to Flow Model value

idea credited to: 100trillionUSD

my data is a bit off compared to the original source but overall it seems correct

Stock to Flowthis study gives the option to plot the stock to flow

OR the number of blocks per month. (you must edit the code by deleting the //)

it should be used only on the monthly timeframe

idea credited to:

medium.com

Ighodalo Gold - CRT (Candles are ranges theory)This indicator is designed to automatically identify and display CRT (Candles are Ranges Theory) Candles on your chart. It draws the high and low of the identified range and extends them until price breaks out, providing clear levels of support and resistance.

The Candles are Ranges Theory (CRT) concept was originally developed and shared by a trader named Romeotpt (Raid). All credit for the trading methodology goes to him. This indicator simply makes spotting these specific candles easier.

What is a CRT Candle & How Is It Used?

A CRT candle is a single candle that has both the highest high AND the lowest low over a user-defined period. It is identified by analysing a block of recent candles and finding the one candle that contains the entire price range of that block.

Once a CRT candle is formed, its high and low act as an accumulation range.

A break above or below this range is the manipulation phase.

A reclaim of the range (price closing back inside) signifies a potential distribution phase.

On higher timeframes, this sequence can be interpreted as:

Candle 1: Accumulation

Candle 2: Manipulation

Candle 3: Distribution

Reversal (Turtle Soup):

A sweep of the high or low, followed by a quick reclaim (price closing back inside the range), can signify a reversal. According to the theory’s originator, Romeo, this reversal pattern is called “turtle soup.”

After a bearish reversal at the high, the target becomes the CRT low.

After a bullish reversal at the low, the target becomes the CRT high.

How to Use This Indicator

The indicator is flexible and can be adapted to your trading style. The most important settings are:

Max Lookback Period: Number of past candles ("n") the indicator checks within to find a CRT.

CRT Timeframe:

Select a timeframe (e.g., 1H): The indicator will look at the higher timeframe you selected and plot the most recent CRT range from that timeframe onto your current chart. This is useful for multi-timeframe analysis.

Enable Overlapping CRTs:

False (unchecked): Shows only one active CRT range at a time. The indicator won’t look for a new one until the current range is broken.

True (checked): Constantly searches for and displays all CRT ranges it finds, allowing multiple ranges to appear on the chart simultaneously.

Disclaimer & Notes

-This is a visualisation tool and not a standalone trading signal. Always use it alongside your own analysis and risk management strategy.

-All credit for the "Candles are Ranges Theory" (CRT) concept goes to its creator, Romeotpt (Raid).

"On the journey to the opposite side of the range, price often provides multiple turtle soup entry opportunities. Follow their footprints." — Raid, 2025

Contract Interest Turnover T3 [T69]Overview

--------

Contract Interest Turnover (CIT) estimates how “churny” a crypto derivatives market is by comparing the amount traded in a bar to the base stock of outstanding contracts (open interest). It normalizes both Volume and Open Interest (OI) by Price (Close), then plots a Turnover Rate = (Volume/Close) ÷ (OI/Close) as colored columns. Higher values = faster contract recycling (strong momentum / hype potential).

Features

--------

- Auto-fetch OI: Pulls OI via request.security(_OI, …) when the exchange/symbol exposes an OI stream on TradingView.

- Price-normalized comparison: Converts both Volume and OI into comparable notional terms by dividing each by Close.

- Turnover columns with threshold: Color the columns green once Turnover ≥ your set threshold; gray otherwise.

- Status-line readouts: Displays normalized Volume and OI values for quick sanity checks.

- Crypto-aware timeframe: Uses chart TF for crypto; forces daily OI when not crypto to avoid noisy intraday pulls.

How to Use

----------

1. Add the script on a perpetual/futures symbol that has OI on TradingView (e.g., BTC perps where an _OI feed exists).

2. Watch the Turnover Rate bars: spikes above your threshold flag sessions where contracts are actively flipping.

3. Interpret spikes as a signal of movement or activity — it does not specify price direction, only that the market is engaged and contracts are being traded more intensely than usual.

Configuration

-------------

- Interest Turnover Threshold (default 1.0): colors columns green when Turnover ≥ threshold. Tune per market’s typical churn profile.

Under the Hood (Formulas & Logic)

---------------------------------

- Fetch OI

oiClose ← request.security(ticker.standard(syminfo.tickerid) + "_OI", timeframe, close) with ignore_invalid_symbol = true.

If none is found, the script throws a clear runtime error.

- Normalize to price

vol_norm = volume / close

oi_norm = oiClose / close

This converts both to a common notional basis so their ratio is meaningful even as price changes.

- Turnover Rate

turnover = vol_norm / oi_norm

Interpretation: fraction/multiples of the outstanding contract base traded in the bar. Color = green if turnover ≥ threshold.

Why Open Interest ≈ “Float” Proxy

---------------------------------

In stocks, float ≈ shares the public can trade. In derivatives, there are no “shares,” so Open Interest acts as the live stock of active contracts. It’s the best proxy for “what’s available in play” because it counts open positions that persist across bars. Using Volume ÷ OI mirrors stock float-turnover logic: how fast the tradable base is being recycled each period.

Why Normalize by Price

----------------------

Derivatives volume and OI may be reported in contracts, not notional value. One contract’s economic weight changes with price (especially on inverse contracts). Dividing both Volume and OI by Close:

- Puts them on a comparable notional footing.

- Prevents false spikes purely from price moves.

- Makes Turnover comparable across time even as price trends.

Advanced Tips

-------------

- Calibrate threshold: Start from the 80th–90th percentile of the last 60–90 bars of Turnover; set the threshold a touch below that to surface early heat.

- Add OI-delta: Layer an OI change histogram (current − prior) to separate new positioning from pure churn.

- Linear vs inverse: For linear (USDT-margined) contracts, the normalization still works and keeps visuals consistent; for inverse, it’s essential.

Limitations

-----------

- Data availability: Works only if your symbol exposes an _OI feed on TradingView; otherwise it errors out.

- Exchange conventions: Volume units differ by venue (contracts, coin, notional). Normalization mitigates, but cross-symbol comparisons still need caution.

- Intrabar gaps: OI is typically end-of-bar; rapid intrabar shifts won’t appear until the bar closes.

Notes

-----

- Designed primarily for crypto derivatives. For non-crypto, the script blanks OI to avoid misleading plots and uses a daily TF when needed.

Credit

------

- Concept & data: Built for TradingView data feeds.

- Acknowledgment: Credit to TradingView default indicator as requested.

- Source: This write-up reflects the logic present in your uploaded script.

Disclaimer

----------

Markets move; indicators simplify. Use with position sizing, hard stops, and catalyst awareness. The Turnover Rate flags activity, not direction.