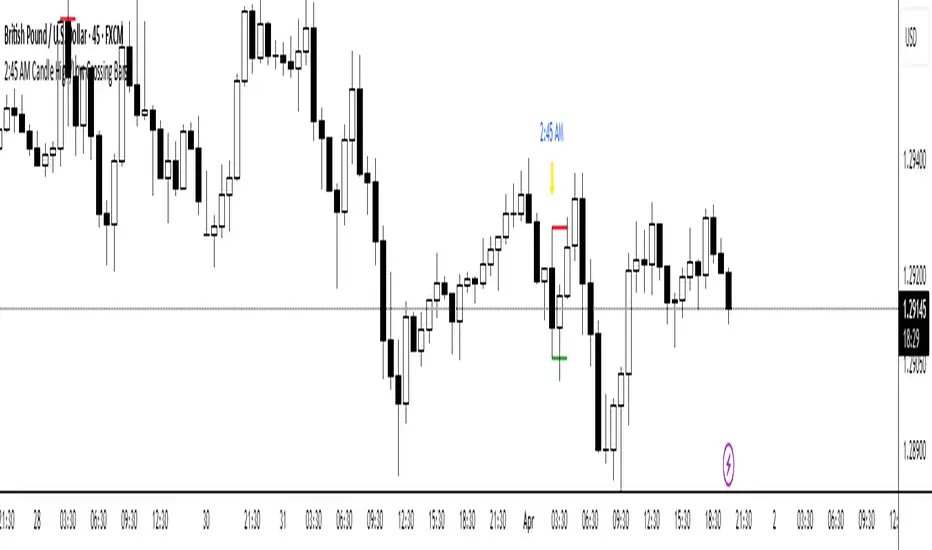

2:45 AM Candle High/Low Crossing Bars2:45 AM Candle High/Low Crossing Bars is an indicator that focuses on the trading view 2:45am NY TIME high and low indicating green for buy and red bars for sell, with the 2:45am new york time highlight/ If the next candle sweeps the low we buy while if it sweeps the high we sell, all time zoon must be the new York UTC time.

스크립트에서 "45美元兑换人民币+最新汇率"에 대해 찾기

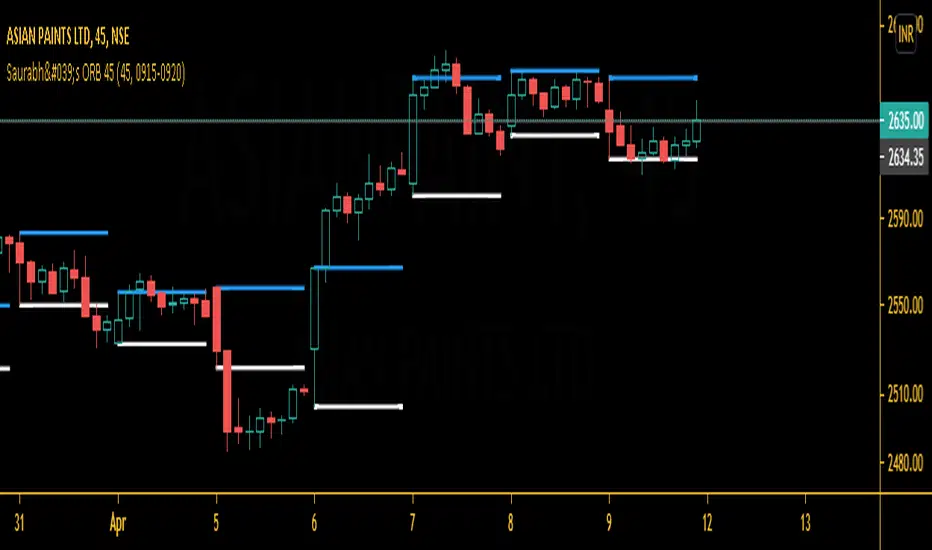

Saurabh's ORB 45This is indicator is all about opening range breakout on 45 mins charts.

|

|

|

|

|

which can be useful to day trader as a breakout strategy following the trend. Useful in 45 mins charts. Also, you may change the time frame from settings according to your likes.

Give thumbs up if you like it.

Vertical Lines @ Hour & :45vertical lines at hour and 45 past each hour

when manipulation is most likely to happen

Opening Range Breakout (9:30 - 9:45 EST)Here's a Pine Script (v5) for TradingView that plots the Opening Range Breakout (ORB) lines from 9:30 AM to 9:45 AM EST on a 15-minute chart.

It draws a green line at the high of the opening range and a red line at the low, both extending through the rest of the day.

RSI Chart Bars 8 55 45Dear Traders

This RSI 8 period made for perfect entry for Long and Short for Intraday/Scalping in any time frame, when RSI 8 crossed above 55 the Candle charged to White then you can go for Long/Buy and when crossed below 45 the Candle changed to Yellow so you can go for Short/Sell, it working in any time frame.

Thanks & Regards

Nesan

Phil's 45 EMA Scalper - Buy / Sell with Alertsgives buy / sell alert when candle closes above or below 45 EMA respectively.

EMA 9/45/90/180Easy script:

*4 EMAs : 9/45/90/180. You can change it if you want.

*Color change on crossover with close: Gives u an idea of the trend and mobile resistance/supports.

Let me know any suggestion!

Thx, bye.

Guppy MMA 3, 5, 8, 10, 12, 15 and 30, 35, 40, 45, 50, 60Guppy Multiple Moving Average

Short Term EMA 3, 5, 8, 10, 12, 15

Long Term EMA 30, 35, 40, 45, 50, 60

Use for SFTS Class

Quarterly Cycle Theory with DST time AdjustedThe Quarterly Theory removes ambiguity, as it gives specific time-based reference points to look for when entering trades. Before being able to apply this theory to trading, one must first understand that time is fractal:

Yearly Quarters = 4 quarters of three months each.

Monthly Quarters = 4 quarters of one week each.

Weekly Quarters = 4 quarters of one day each (Monday - Thursday). Friday has its own specific function.

Daily Quarters = 4 quarters of 6 hours each = 4 trading sessions of a trading day.

Sessions Quarters = 4 quarters of 90 minutes each.

90 Minute Quarters = 4 quarters of 22.5 minutes each.

Yearly Cycle: Analogously to financial quarters, the year is divided in four sections of three months each:

Q1 - January, February, March.

Q2 - April, May, June (True Open, April Open).

Q3 - July, August, September.

Q4 - October, November, December.

S&P 500 E-mini Futures (daily candles) — Monthly Cycle.

Monthly Cycle: Considering that we have four weeks in a month, we start the cycle on the first month’s Monday (regardless of the calendar Day):

Q1 - Week 1: first Monday of the month.

Q2 - Week 2: second Monday of the month (True Open, Daily Candle Open Price).

Q3 - Week 3: third Monday of the month.

Q4 - Week 4: fourth Monday of the month.

S&P 500 E-mini Futures (4 hour candles) — Weekly Cycle.

Weekly Cycle: Daye determined that although the trading week is composed by 5 trading days, we should ignore Friday, and the small portion of Sunday’s price action:

Q1 - Monday.

Q2 - Tuesday (True Open, Daily Candle Open Price).

Q3 - Wednesday.

Q4 - Thursday.

S&P 500 E-mini Futures (1 hour candles) — Daily Cycle.

Daily Cycle: The Day can be broken down into 6 hour quarters. These times roughly define the sessions of the trading day, reinforcing the theory’s validity:

Q1 - 18:00 - 00:00 Asia.

Q2 - 00:00 - 06:00 London (True Open).

Q3 - 06:00 - 12:00 NY AM.

Q4 - 12:00 - 18:00 NY PM.

S&P 500 E-mini Futures (15 minute candles) — 6 Hour Cycle.

6 Hour Quarters or 90 Minute Cycle / Sessions divided into four sections of 90 minutes each (EST/EDT):

Asian Session

Q1 - 18:00 - 19:30

Q2 - 19:30 - 21:00 (True Open)

Q3 - 21:00 - 22:30

Q4 - 22:30 - 00:00

London Session

Q1 - 00:00 - 01:30

Q2 - 01:30 - 03:00 (True Open)

Q3 - 03:00 - 04:30

Q4 - 04:30 - 06:00

NY AM Session

Q1 - 06:00 - 07:30

Q2 - 07:30 - 09:00 (True Open)

Q3 - 09:00 - 10:30

Q4 - 10:30 - 12:00

NY PM Session

Q1 - 12:00 - 13:30

Q2 - 13:30 - 15:00 (True Open)

Q3 - 15:00 - 16:30

Q4 - 16:30 - 18:00

S&P 500 E-mini Futures (5 minute candles) — 90 Minute Cycle.

Micro Cycles: Dividing the 90 Minute Cycle yields 22.5 Minute Quarters, also known as Micro Sessions or Micro Quarters:

Asian Session

Q1/1 18:00:00 - 18:22:30

Q2 18:22:30 - 18:45:00

Q3 18:45:00 - 19:07:30

Q4 19:07:30 - 19:30:00

Q2/1 19:30:00 - 19:52:30 (True Session Open)

Q2/2 19:52:30 - 20:15:00

Q2/3 20:15:00 - 20:37:30

Q2/4 20:37:30 - 21:00:00

Q3/1 21:00:00 - 21:23:30

etc. 21:23:30 - 21:45:00

London Session

00:00:00 - 00:22:30 (True Daily Open)

00:22:30 - 00:45:00

00:45:00 - 01:07:30

01:07:30 - 01:30:00

01:30:00 - 01:52:30 (True Session Open)

01:52:30 - 02:15:00

02:15:00 - 02:37:30

02:37:30 - 03:00:00

03:00:00 - 03:22:30

03:22:30 - 03:45:00

03:45:00 - 04:07:30

04:07:30 - 04:30:00

04:30:00 - 04:52:30

04:52:30 - 05:15:00

05:15:00 - 05:37:30

05:37:30 - 06:00:00

New York AM Session

06:00:00 - 06:22:30

06:22:30 - 06:45:00

06:45:00 - 07:07:30

07:07:30 - 07:30:00

07:30:00 - 07:52:30 (True Session Open)

07:52:30 - 08:15:00

08:15:00 - 08:37:30

08:37:30 - 09:00:00

09:00:00 - 09:22:30

09:22:30 - 09:45:00

09:45:00 - 10:07:30

10:07:30 - 10:30:00

10:30:00 - 10:52:30

10:52:30 - 11:15:00

11:15:00 - 11:37:30

11:37:30 - 12:00:00

New York PM Session

12:00:00 - 12:22:30

12:22:30 - 12:45:00

12:45:00 - 13:07:30

13:07:30 - 13:30:00

13:30:00 - 13:52:30 (True Session Open)

13:52:30 - 14:15:00

14:15:00 - 14:37:30

14:37:30 - 15:00:00

15:00:00 - 15:22:30

15:22:30 - 15:45:00

15:45:00 - 15:37:30

15:37:30 - 16:00:00

16:00:00 - 16:22:30

16:22:30 - 16:45:00

16:45:00 - 17:07:30

17:07:30 - 18:00:00

S&P 500 E-mini Futures (30 second candles) — 22.5 Minute Cycle.

Relative Strength Index With Range ZoneRSI (Relative Strength Index) with 45-55 Range Zone

1. Introduction and Historical Background

The Relative Strength Index (RSI) is a momentum indicator developed in 1978 by J. Welles Wilder Jr. It measures the speed and magnitude of price changes to assess overbought and oversold conditions of an asset. This widely used oscillator ranges between 0 and 100.

Historically, the RSI was mainly used to detect trend reversals by identifying extreme levels: above 70 (overbought) and below 30 (oversold). However, its application has evolved, and new approaches refine its interpretation, such as adding a 45-55 neutral zone to identify consolidation (range) periods.

2. RSI Calculation

The RSI is calculated using the following formula:

RSI=100−(1001+RS)RSI=100−(1+RS100)

Where:

RS=Average gain over N periodsAverage loss over N periodsRS=Average loss over N periodsAverage gain over N periods

• RS (Relative Strength) is the ratio between the average gains and the average losses over N periods (typically 14 periods).

• Gains and losses are calculated based on daily price variations.

Example calculation with a 14-day period:

1. Compute daily gains and losses.

2. Take an exponential or simple moving average of these values over 14 days.

3. Apply the formula to get the RSI value.

3. Classic RSI Usage

The RSI is typically interpreted as follows:

• RSI > 70: Overbought → Possible correction or bearish reversal.

• RSI < 30: Oversold → Possible rebound or bullish reversal.

• RSI between 50 and 70: Bullish momentum.

• RSI between 30 and 50: Bearish momentum.

4. Adding the 45-55 Zone to Identify Range Phases

Adding a neutral zone between 45 and 55 helps identify consolidation periods, when price moves sideways without a strong trend.

• RSI between 45 and 55: The market is in a range, meaning neither buyers nor sellers dominate.

• RSI breaking out of this zone:

o Above 55: Indicates the start of a bullish trend.

o Below 45: Indicates the start of a bearish trend.

This zone is particularly useful for:

• Avoiding false signals by waiting for trend confirmation.

• Identifying ranging markets, favoring range trading strategies (buying at support, selling at resistance).

• Filtering trend-based entries, waiting for the RSI to exit the 45-55 zone.

5. Trading Strategies Using RSI with the 45-55 Range Zone

1. Range Trading:

• When the RSI oscillates between 45 and 55, it signals a lack of strong trend.

• Strategy:

o Identify a support and resistance level.

o Buy near support when the RSI touches 45.

o Sell near resistance when the RSI touches 55.

2. Breakout Trading:

• If the RSI exits the 45-55 zone:

o Above 55 → Buy (start of a bullish trend).

o Below 45 → Sell (start of a bearish trend).

• This breakout can be used as a confirmed entry signal.

3. Confirmation with Divergences:

• A bullish divergence (price making lower lows while RSI makes higher lows) is more relevant if the RSI moves above 55.

• A bearish divergence (price making higher highs while RSI makes lower highs) is stronger if the RSI drops below 45.

6. Conclusion

The RSI is a powerful tool for analyzing price momentum. Adding a 45-55 zone enhances its usage by clearly distinguishing:

• Consolidation phases (range markets).

• Trend beginnings when RSI breaks out of this range.

This approach improves RSI reliability by filtering out false signals and allowing traders to adapt their strategy based on market conditions.

Gann RetracementThe indicator is based on W. D. Gann's method of retracement studies. Gann looked at stock retracement action in terms of Halves (1/2), Thirds (1/3, 2/3), Fifths (1/5, 2/5, 3/5, and 4/5) and more importantly the Eighths (1/8, 2/8, 3/8, 4/8, 5/8, 6/8, and 7/8). Needless to say, {2, 3, 5, 8} are the only Fibonacci numbers between 1 to 10. These ratios can easily be visualized in the form of division of a Circle as follows :

Divide the circle in 12 equal parts of 30 degree each to produce the Thirds :

30 x 4 = 120 is 1/3 of 360

30 x 8 = 240 is 2/3 of 360

The 30 degree retracement captures fundamental geometric shapes like a regular Triangle (120-240-360), a Square (90-180-270-360), and a regular Hexagon (60-120-180-240-300-360) inscribed inside of the circle.

Now, divide the circle in 10 equal parts of 36 degree each to produce the Fifths :

36 x 2 = 72 is 1/5 of 360

36 x 4 = 144 is 2/5 of 360

36 x 6 = 216 is 3/5 of 360

36 x 8 = 288 is 4/5 of 360

where, (72-144-216-288-360) is a regular Pentagon.

Finally, divide the circle in 8 equal parts of 45 degree each to produce the Eighths :

45 x 1 = 45 is 1/8 of 360

45 x 2 = 90 is 2/8 of 360

45 x 3 = 135 is 3/8 of 360

45 x 4 = 180 is 4/8 of 360

45 x 5 = 225 is 5/8 of 360

45 x 6 = 270 is 6/8 of 360

45 x 7 = 315 is 7/8 of 360

where, (45-90-135-180-225-270-315-360) is a regular Octagon.

How to Use this indicator ?

The indicator generates Gann retracement levels between any two significant price points, such as a high and a low.

Input :

Swing High (significant high price point, such as a top)

Swing Low (significant low price point, such as a bottom)

Degree (degree of retracement)

Output :

Gann retracement levels (color coded as follows) :

Swing High and Swing Low (BLUE)

50% retracement (ORANGE)

Retracements between Swing Low and 50% level (RED)

Retracements between 50% level and Swing High (LIME)

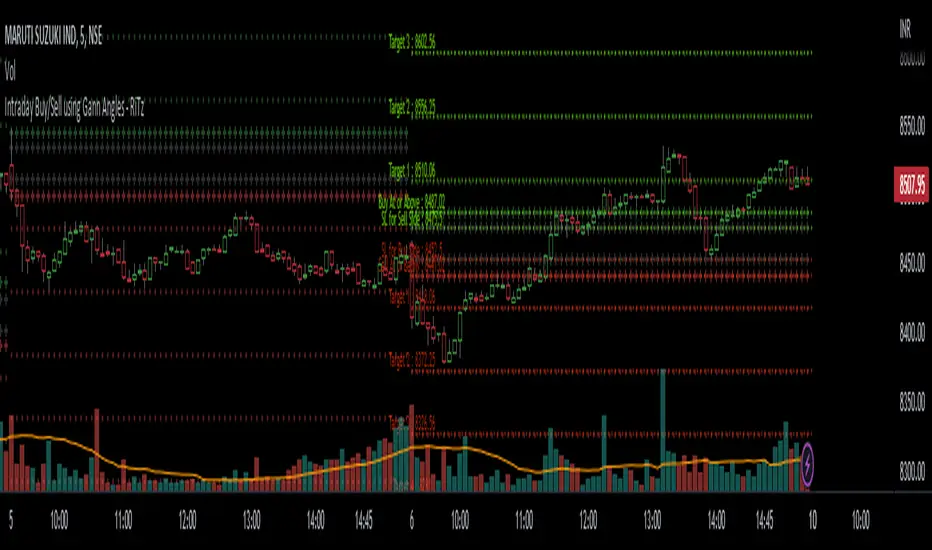

Intraday Buy/Sell using Gann Angles - RiTzIntraday Buy/Sell Levels using Gann Angles based on Todays Open/previous Day High/Low/Close prices

How to use this :

The Buy/Sell levels will be calculated on 1 of 4 things (you can choose any one which you prefer)

1. Todays Open price

2. Previous Day High

3. Previous Day Low

4. Previous Day Close

The Buy/Sell levels will be displayed in these ways

1. In a Table

2. on the Chart

You can turn them on/off according to your preference!

I can't seem to find the original documentation or a link to it.

i have it's excel file, in which we have to enter following data :

1. Todays Open price

2. Previous Day High

3. Previous Day Low

4. Previous Day Close

and the buy/sell levels are calculated by using the above data in following manner :

Based On Today's Opening Price

(lets call it TDO)

Degree's````````````````` Degree Factor```````````````````````` Buy````````````````````````` Sell

11.25```````````````````` =degree/180=11.25/180=0.0625````````` =(sqrt(TDO)-0.0625)^2``````` =(sqrt(TDO)+0.0625)^2````` SL

22.5````````````````````` =degree/180=22.5/180=0.125``````````` =(sqrt(TDO)+0.125)^2```````` =(sqrt(TDO)-0.125)^2`````` Buy/Sell At

45``````````````````````` =degree/180=45/180=0.25`````````````` =(sqrt(TDO)+0.25)^2````````` =(sqrt(TDO)-0.25)^2``````` Target-1

90``````````````````````` =degree/180=90/180=0.5``````````````` =(sqrt(TDO)+0.5)^2`````````` =(sqrt(TDO)-0.5)^2```````` Target-2

135`````````````````````` =degree/180=135/180=0.75````````````` =(sqrt(TDO)+0.75)^2````````` =(sqrt(TDO)-0.75)^2``````` Target-3

180`````````````````````` =degree/180=180/180=1```````````````` =(sqrt(TDO)+1)^2```````````` =(sqrt(TDO)-1)^2`````````` Target-4

225`````````````````````` =degree/180=225/180=1.25````````````` =(sqrt(TDO)+1.25)^2````````` =(sqrt(TDO)-1.25)^2``````` Target-5

270`````````````````````` =degree/180=270/180=1.5`````````````` =(sqrt(TDO)+1.5)^2`````````` =(sqrt(TDO)-1.5)^2```````` Target-6

315`````````````````````` =degree/180=315/180=1.75````````````` =(sqrt(TDO)+1.75)^2````````` =(sqrt(TDO)-1.75)^2``````` Target-7

360`````````````````````` =degree/180=360/180=2```````````````` =(sqrt(TDO)+2)^2```````````` =(sqrt(TDO)-2)^2`````````` Target-8

sqrt = square root

TDO = Today's Opening Price

PDH = Previous Days High

PDL = Previous Days Low

PDC = Previous Days Close

Based On Previous Days High Price

(lets call it PDH)

Degree's````````````````` Degree Factor```````````````````````` Buy````````````````````````` Sell

11.25```````````````````` =degree/180=11.25/180=0.0625````````` =(sqrt(PDH)-0.0625)^2``````` =(sqrt(PDH)+0.0625)^2````` SL

22.5````````````````````` =degree/180=22.5/180=0.125``````````` =(sqrt(PDH)+0.125)^2```````` =(sqrt(PDH)-0.125)^2`````` Buy/Sell At

45``````````````````````` =degree/180=45/180=0.25`````````````` =(sqrt(PDH)+0.25)^2````````` =(sqrt(PDH)-0.25)^2``````` Target-1

90``````````````````````` =degree/180=90/180=0.5``````````````` =(sqrt(PDH)+0.5)^2`````````` =(sqrt(PDH)-0.5)^2```````` Target-2

135`````````````````````` =degree/180=135/180=0.75````````````` =(sqrt(PDH)+0.75)^2````````` =(sqrt(PDH)-0.75)^2``````` Target-3

180`````````````````````` =degree/180=180/180=1```````````````` =(sqrt(PDH)+1)^2```````````` =(sqrt(PDH)-1)^2`````````` Target-4

225`````````````````````` =degree/180=225/180=1.25````````````` =(sqrt(PDH)+1.25)^2````````` =(sqrt(PDH)-1.25)^2``````` Target-5

270`````````````````````` =degree/180=270/180=1.5`````````````` =(sqrt(PDH)+1.5)^2`````````` =(sqrt(PDH)-1.5)^2```````` Target-6

315`````````````````````` =degree/180=315/180=1.75````````````` =(sqrt(PDH)+1.75)^2````````` =(sqrt(PDH)-1.75)^2``````` Target-7

360`````````````````````` =degree/180=360/180=2```````````````` =(sqrt(PDH)+2)^2```````````` =(sqrt(PDH)-2)^2`````````` Target-8

Based On Previous Days Low Price

(lets call it PDL)

Degree's````````````````` Degree Factor```````````````````````` Buy````````````````````````` Sell

11.25```````````````````` =degree/180=11.25/180=0.0625````````` =(sqrt(PDL)-0.0625)^2``````` =(sqrt(PDL)+0.0625)^2````` SL

22.5````````````````````` =degree/180=22.5/180=0.125``````````` =(sqrt(PDL)+0.125)^2```````` =(sqrt(PDL)-0.125)^2`````` Buy/Sell At

45``````````````````````` =degree/180=45/180=0.25`````````````` =(sqrt(PDL)+0.25)^2````````` =(sqrt(PDL)-0.25)^2``````` Target-1

90``````````````````````` =degree/180=90/180=0.5``````````````` =(sqrt(PDL)+0.5)^2`````````` =(sqrt(PDL)-0.5)^2```````` Target-2

135`````````````````````` =degree/180=135/180=0.75````````````` =(sqrt(PDL)+0.75)^2````````` =(sqrt(PDL)-0.75)^2``````` Target-3

180`````````````````````` =degree/180=180/180=1```````````````` =(sqrt(PDL)+1)^2```````````` =(sqrt(PDL)-1)^2`````````` Target-4

225`````````````````````` =degree/180=225/180=1.25````````````` =(sqrt(PDL)+1.25)^2````````` =(sqrt(PDL)-1.25)^2``````` Target-5

270`````````````````````` =degree/180=270/180=1.5`````````````` =(sqrt(PDL)+1.5)^2`````````` =(sqrt(PDL)-1.5)^2```````` Target-6

315`````````````````````` =degree/180=315/180=1.75````````````` =(sqrt(PDL)+1.75)^2````````` =(sqrt(PDL)-1.75)^2``````` Target-7

360`````````````````````` =degree/180=360/180=2```````````````` =(sqrt(PDL)+2)^2```````````` =(sqrt(PDL)-2)^2`````````` Target-8

Based On Previous Days Close Price

(lets call it PDC)

Degree's````````````````` Degree Factor```````````````````````` Buy````````````````````````` Sell

11.25```````````````````` =degree/180=11.25/180=0.0625````````` =(sqrt(PDC)-0.0625)^2``````` =(sqrt(PDC)+0.0625)^2````` SL

22.5````````````````````` =degree/180=22.5/180=0.125``````````` =(sqrt(PDC)+0.125)^2```````` =(sqrt(PDC)-0.125)^2`````` Buy/Sell At

45``````````````````````` =degree/180=45/180=0.25`````````````` =(sqrt(PDC)+0.25)^2````````` =(sqrt(PDC)-0.25)^2``````` Target-1

90``````````````````````` =degree/180=90/180=0.5``````````````` =(sqrt(PDC)+0.5)^2`````````` =(sqrt(PDC)-0.5)^2```````` Target-2

135`````````````````````` =degree/180=135/180=0.75````````````` =(sqrt(PDC)+0.75)^2````````` =(sqrt(PDC)-0.75)^2``````` Target-3

180`````````````````````` =degree/180=180/180=1```````````````` =(sqrt(PDC)+1)^2```````````` =(sqrt(PDC)-1)^2`````````` Target-4

225`````````````````````` =degree/180=225/180=1.25````````````` =(sqrt(PDC)+1.25)^2````````` =(sqrt(PDC)-1.25)^2``````` Target-5

270`````````````````````` =degree/180=270/180=1.5`````````````` =(sqrt(PDC)+1.5)^2`````````` =(sqrt(PDC)-1.5)^2```````` Target-6

315`````````````````````` =degree/180=315/180=1.75````````````` =(sqrt(PDC)+1.75)^2````````` =(sqrt(PDC)-1.75)^2``````` Target-7

360`````````````````````` =degree/180=360/180=2```````````````` =(sqrt(PDC)+2)^2```````````` =(sqrt(PDC)-2)^2`````````` Target-8

example based On Today's Opening Price = 4339

Degree's```````` Degree Factor```````` Buy`````````` Sell

11.25``````````` 0.0625``````````````` 4330.77`````` 4347.24```````` SL

22.5```````````` 0.125```````````````` 4355.48`````` 4322.55```````` Buy/Sell At

45`````````````` 0.25````````````````` 4372.00`````` 4306.13```````` Target-1

90`````````````` 0.5`````````````````` 4405.12`````` 4273.38```````` Target-2

135````````````` 0.75````````````````` 4438.37`````` 4240.76```````` Target-3

180````````````` 1```````````````````` 4471.74`````` 4208.26```````` Target-4

225````````````` 1.25````````````````` 4505.24`````` 4175.88```````` Target-5

270````````````` 1.5`````````````````` 4538.86`````` 4143.64```````` Target-6

315````````````` 1.75````````````````` 4572.61`````` 4111.51```````` Target-7

360````````````` 2```````````````````` 4606.48`````` 4079.52```````` Target-8

Note : ignore the '`' , inserted them to fill up the spaces , it was looking very weird!, tried to fix it as much as I can.

Note :- Please correct me if I'm wrong , as I've already mentioned I don't have it's original documentation.

if anyone can find it or already has it then please feel free to share it.

9:45am NIFTY TRADINGTime Frame: 15 Minutes | Reference Candle Time: 9:45 AM IST | Valid Trading Window: 3 Hours

📌 Introduction

This document outlines a structured trading strategy for NIFTY & BANKNIFTY Options based on a 15-minute timeframe with a 9:45 AM IST reference candle. The strategy incorporates technical indicators, probability analysis, and strict trading rules to optimize entries and exits.

📊 Core Features

1. Reference Time Trading System

9:45 AM IST Candle acts as the reference for the day.

All signals (Buy/Sell/Reversal) are generated based on price action relative to this candle.

The valid trading window is 3 hours after the reference candle.

2. Signal Generation Logic

Signal Condition

Buy (B) Price breaks above reference candle high with confirmation

Sell (S) Price breaks below reference candle low with confirmation

Reversal (R) Early trend reversal signal (requires strict confirmation)

3. Probability Analysis System

The strategy calculates Win Probability (%) using 4 components:

Component Weight Calculation

Body Win Probability 30% Based on candle body strength (body % of total range)

Volume Win Probability 30% Current volume vs. average volume strength

Trend Win Probability 40% EMA crossover + RSI momentum alignment

Composite Probability - Weighted average of all 3 components

Probability Color Coding:

🟢 Green (High Probability): ≥70%

🟠 Orange (Medium Probability): 50-69%

🔴 Red (Low Probability): <50%

4. Timeframe Enforcement

Strictly 15-minute charts only (no other timeframes allowed).

System auto-disables signals if the wrong timeframe is selected.

📈 Technical Analysis Components

1. EMA System (Trend Analysis)

Short EMA (9) – Fast trend indicator

Middle EMA (20) – Intermediate trend

Long EMA (50) – Long-term trend confirmation

Rules:

Buy Signal: Price > 9 EMA > 20 EMA > 50 EMA (Bullish trend)

Sell Signal: Price < 9 EMA < 20 EMA < 50 EMA (Bearish trend)

2. Multi-Timeframe RSI (Momentum)

5M, 15M, 1H, 4H, Daily RSI values are compared for divergence/confluence.

Overbought (≥70) / Oversold (≤30) conditions help in reversal signals.

3. Volume Analysis

Volume Strength (%) = (Current Volume / Avg. Volume) × 100

Strong Volume (>120% Avg.) confirms breakout/breakdown.

4. Body Percentage (Candle Strength)

Body % = (Close - Open) / (High - Low) × 100

Strong Bullish Candle: Body > 60%

Strong Bearish Candle: Body < 40%

📊 Visual Elements

1. Information Tables

Reference Data Table (9:45 AM Candle High/Low/Close)

RSI Values Table (5M, 15M, 1H, 4H, Daily)

Signal Legend (Buy/Sell/Reversal indicators)

2. Chart Overlays

Reference Lines (9:45 AM High & Low)

EMA Lines (9, 20, 50)

Signal Labels (B, S, R)

3. Color Coding

High Probability (Green)

Medium Probability (Orange)

Low Probability (Red)

⚠️ Important Usage Guidelines

✅ Best Practices:

Trade only within the 3-hour window (9:45 AM - 12:45 PM IST).

Wait for confirmation (closing above/below reference candle).

Use probability score to filter high-confidence trades.

❌ Avoid:

Trading outside the 15-minute timeframe.

Ignoring volume & RSI divergence.

Overtrading – Stick to 1-2 high-probability setups per day.

🎯 Conclusion

This NIFTY Trading Strategy is optimized for 15-minute charts with a 9:45 AM IST reference candle. It combines EMA trends, RSI momentum, volume analysis, and probability scoring to generate high-confidence signals.

🚀 Key Takeaways:

✔ Reference candle defines the day’s bias.

✔ Probability system filters best trades.

✔ Strict 15M timeframe ensures consistency.

Happy Trading! 📈💰

BioSwarm Imprinter™BioSwarm Imprinter™ — Agent-Based Consensus for Traders

What it is

BioSwarm Imprinter™ is a non-repainting, agent-based sentiment oscillator. It fuses many short-to-medium lookback “opinions” into one 0–100 consensus line that is easy to read at a glance (50 = neutral, >55 bullish bias, <45 bearish bias). The engine borrows from swarm intelligence: many simple voters (agents) adapt their influence over time based on how well they’ve been predicting price, so the crowd gets smarter as conditions change.

Use it to:

• Detect emerging trends sooner without overreacting to noise.

• Filter mean-reversion vs continuation opportunities.

• Gate entries with a confidence score that reflects both strength and persistence of the move.

• Combine with your execution tools (VWAP/ORB/levels) as a state filter rather than a trade signal by itself.

⸻

Why it’s different

• Swarm learning: Each agent improves or decays its “fitness” depending on whether its vote matched the next bar’s direction. High-fitness agents matter more; weak agents fade.

• Multi-horizon by design: The crowd is composed of fixed, simple lookbacks spread from lenMin to lenMax. You get a blended, robust view instead of a single fragile parameter.

• Two complementary lenses: Each agent evaluates RSI-style balance (via Wilder’s RMA) and momentum (EMA deviation). You decide the weight of each.

• No repaint, no MTF pitfalls: Everything runs on the chart’s timeframe with bar-close confirmation; no request.security() or forward references.

• Actionable UI: A clean consensus line, optional regime background, confidence heat, and triangle markers when thresholds are crossed.

⸻

What you see on the chart

• Consensus line (0–100): Smoothed to your preference; color/area makes bull/bear zones obvious.

• Regime coloring (optional): Light green in bull zone, light red in bear zone; neutral otherwise.

• Confidence heat: A small gauge/number (0–100) that combines distance from neutral and recent persistence.

• Markers (optional): Triangles when consensus crosses up through your bull threshold (e.g., 55) or down through your bear threshold (e.g., 45).

• Info panel (optional): Consensus value, regime, confidence, number of agents, and basic diagnostics.

⸻

How it works (under the hood)

1. Horizon bins: The range is divided into numBins. Each bin has a fixed, simple integer length (crucial for Pine’s safety rules).

2. Per-bin features (computed every bar):

• RSI-style balance using Wilder’s RMA (not ta.rsi()), then mapped to −1…+1.

• Momentum as (close − EMA(L)) / EMA(L) (dimensionless drift).

3. Agent vote: For its assigned bin, an agent forms a weighted score: score = wRSI*RSI_like + wMOM*Momentum. A small dead-band near zero suppresses chop; votes are +1/−1/0.

4. Fitness update (bar close): If the agent’s previous vote agreed with the next bar’s direction, multiply its fitness by learnGain; otherwise by learnPain. Fitness is clamped so it never explodes or dies.

5. Consensus: Weighted average of all votes using fitness as weights → map to 0–100 and smooth with EMA.

Why it doesn’t repaint:

• No future references, no MTF resampling, fitness updates only on confirmed bars.

• All TA primitives (RMA/EMA/deltas) are computed every bar unconditionally.

⸻

Signals & confidence

• Bullish bias: consensus ≥ bullThr (e.g., 55).

• Bearish bias: consensus ≤ bearThr (e.g., 45).

• Confidence (0–100):

• Distance score: how far consensus is from 50.

• Momentum score: how strong the recent change is versus its recent average.

• Combined into a single gate; start filtering entries at ≥60 for higher quality.

Tip: For range sessions, raise thresholds (60/40) and increase smoothing; for momentum sessions, lower smoothing and keep thresholds at 55/45.

⸻

Inputs you’ll actually tune

• Agents & horizons:

• N_agents (e.g., 64–128)

• lenMin / lenMax (e.g., 6–30 intraday, 10–60 swing)

• numBins (e.g., 12–24)

• Weights & smoothing:

• wRSI vs wMOM (e.g., 0.7/0.3 for FX & indices; 0.6/0.4 for crypto)

• deadBand (0.03–0.08)

• consSmooth (3–8)

• Thresholds & hygiene:

• bullThr/bearThr (55/45 default)

• cooldownBars to avoid signal spam

⸻

Playbooks (ready-to-use)

1) Breakout / Trend continuation

• Timeframe: 15m–1h for day/swing.

• Filter: Take longs only when consensus > 55 and confidence ≥ 60.

• Execution: Use your ORB/VWAP/pullback trigger for entry. Trail with swing lows or 1.5×ATR. Exit on a close back under 50 or when a bearish signal prints.

2) Mean reversion (fade)

• When: Sideways days or low-volatility clusters.

• Setup: Increase deadBand and consSmooth.

• Signal: Bearish fades when consensus rolls over below ≈55 but stays above 50; bullish fades when it rolls up above ≈45 but stays below 50.

• Targets: The neutral zone (~50) as the first take-profit.

3) Multi-TF alignment

• Keep BioSwarm on 1H for bias, execute on 5–15m:

• Only take entries in the direction of the 1H consensus.

• Skip counter-bias scalps unless confidence is very low (explicit mean-reversion plan).

⸻

Integrations that work

• DynamoSent Pro+ (macro bias): Only act when macro bias and swarm consensus agree.

• ORB + Session VWAP Pro: Trade London/NY ORB breakouts that retest while consensus >55 (long) or <45 (short).

• Levels/Orderflow: BioSwarm is your “go / no-go”; execution stays with your usual triggers.

⸻

Quick start

1. Drop the indicator on a 1H chart.

2. Start with: N_agents=64, lenMin=6, lenMax=30, numBins=16, deadBand=0.06, consSmooth=5, thresholds 55/45.

3. Trade only when confidence ≥ 60.

4. Add your favorite execution tool (VWAP/levels/OR) for entries & exits.

⸻

Non-repainting & safety notes

• No request.security(); no hidden lookahead.

• Bar-close confirmation for fitness and signals.

• All TA calls are unconditional (no “sometimes called” warnings).

• No series-length inputs to RSI/EMA — we use RMA/EMA formulas that accept fixed simple ints per bin.

⸻

Known limits & tips

• Too many signals? Raise deadBand, increase consSmooth, widen thresholds to 60/40.

• Too few signals? Lower deadBand, reduce consSmooth, narrow thresholds to 53/47.

• Over-fitting risk: Keep learnGain/learnPain modest (e.g., ×1.04 / ×0.96).

• Compute load: Large N_agents × numBins is heavier; scale to your device.

⸻

Example recipes

EURUSD 1H (swing):

lenMin=8, lenMax=34, numBins=16, wRSI=0.7, wMOM=0.3, deadBand=0.06, consSmooth=6, thr=55/45

Buy breakouts when consensus >55 and confidence ≥60; confirm with 5–15m pullback to VWAP or level.

SPY 15m (US session):

lenMin=6, lenMax=24, numBins=12, consSmooth=4, deadBand=0.05

On trend days, stay with longs as long as consensus >55; add on shallow pullbacks.

BTC 1H (24/7):

Increase momentum weight: wRSI=0.6, wMOM=0.4, extend lenMax to ~50. Use dynamic stops (ATR) and partials on strong verticals.

⸻

Final word

BioSwarm is a state engine: it tells you when the market is primed to continue or mean-revert. Pair it with your entries and risk framework to turn that state into trades. If you’d like, I can supply a companion strategy template that consumes the consensus and back-tests the three playbooks (Breakout/Fade/Flip) with standard risk management.

VWAP For Loop [BackQuant]VWAP For Loop

What this tool does—in one sentence

A volume-weighted trend gauge that anchors VWAP to a calendar period (day/week/month/quarter/year) and then scores the persistence of that VWAP trend with a simple for-loop “breadth” count; the result is a clean, threshold-driven oscillator plus an optional VWAP overlay and alerts.

Plain-English overview

Instead of judging raw price alone, this indicator focuses on anchored VWAP —the market’s average price paid during your chosen institutional period. It then asks a simple question across a configurable set of lookback steps: “Is the current anchored VWAP higher than it was i bars ago—or lower?” Each “yes” adds +1, each “no” adds −1. Summing those answers creates a score that reflects how consistently the volume-weighted trend has been rising or falling. Extreme positive scores imply persistent, broad strength; deeply negative scores imply persistent weakness. Crossing predefined thresholds produces objective long/short events and color-coded context.

Under the hood

• Anchoring — VWAP using hlc3 × volume resets exactly when the selected period rolls:

Day → session change, Week → new week, Month → new month, Quarter/Year → calendar quarter/year.

• For-loop scoring — For lag steps i = , compare today’s VWAP to VWAP .

– If VWAP > VWAP , add +1.

– Else, add −1.

The final score ∈ , where N = (end − start + 1). With defaults (1→45), N = 45.

• Signal logic (stateful)

– Long when score > upper (e.g., > 40 with N = 45 → VWAP higher than ~89% of checked lags).

– Short on crossunder of lower (e.g., dropping below −10).

– A compact state variable ( out ) holds the current regime: +1 (long), −1 (short), otherwise unchanged. This “stickiness” avoids constant flipping between bars without sufficient evidence.

Why VWAP + a breadth score?

• VWAP aggregates both price and volume—where participants actually traded.

• The breadth-style count rewards consistency of the anchored trend, not one-off spikes.

• Thresholds give you binary structure when you need it (alerts, automation), without complex math.

What you’ll see on the chart

• Sub-pane oscillator — The for-loop score line, colored by regime (long/short/neutral).

• Main-pane VWAP (optional) — Even though the indicator runs off-chart, the anchored VWAP can be overlaid on price (toggle visibility and whether it inherits trend colors).

• Threshold guides — Horizontal lines for the long/short bands (toggle).

• Cosmetics — Optional candle painting and background shading by regime; adjustable line width and colors.

Input map (quick reference)

• VWAP Anchor Period — Day, Week, Month, Quarter, Year.

• Calculation Start/End — The for-loop lag window . With 1→45, you evaluate 45 comparisons.

• Long/Short Thresholds — Default upper=40, lower=−10 (asymmetric by design; see below).

• UI/Style — Show thresholds, paint candles, background color, line width, VWAP visibility and coloring, custom long/short colors.

Interpreting the score

• Near +N — Current anchored VWAP is above most historical VWAP checkpoints in the window → entrenched strength.

• Near −N — Current anchored VWAP is below most checkpoints → entrenched weakness.

• Between — Mixed, choppy, or transitioning regimes; use thresholds to avoid reacting to noise.

Why the asymmetric default thresholds?

• Long = score > upper (40) — Demands unusually broad upside persistence before declaring “long regime.”

• Short = crossunder lower (−10) — Triggers only on downward momentum events (a fresh breach), not merely being below −10. This combination tends to:

– Capture sustained uptrends only when they’re very strong.

– Flag downside turns as they occur, rather than waiting for an extreme negative breadth.

Tuning guide

Choose an anchor that matches your horizon

– Intraday scalps : Day anchor on intraday charts.

– Swing/position : Month or Quarter anchor on 1h/4h/D charts to capture institutional cycles.

Pick the for-loop window

– Larger N (bigger end) = stronger evidence requirement, smoother oscillator.

– Smaller N = faster, more reactive score.

Set achievable thresholds

– Ensure upper ≤ N and lower ≥ −N ; if N=30, an upper of 40 can never trigger.

– Symmetric setups (e.g., +20/−20) are fine if you want balanced behavior.

Match visuals to intent

– Enabling VWAP coloring lets you see regime directly on price.

– Background shading is useful for discretionary reading; turn it off for cleaner automation displays.

Playbook examples

• Trend confirmation with disciplined entries — On Month anchor, N=45, upper=38–42: when the long regime engages, use pullbacks toward anchored VWAP on the main pane for entries, with stops just beyond VWAP or a recent swing.

• Downside transition detection — Keep lower around −8…−12 and watch for crossunders; combine with price losing anchored VWAP to validate risk-off.

• Intraday bias filter — Day anchor on a 5–15m chart, N=20–30, upper ~ 16–20, lower ~ −6…−10. Only take longs while score is positive and above a midline you define (e.g., 0), and shorts only after a genuine crossunder.

Behavior around resets (important)

Anchored VWAP is hard-reset each period. Immediately after a reset, the series can be young and comparisons to pre-reset values may span two periods. If you prefer within-period evaluation only, choose end small enough not to bridge typical period length on your timeframe, or accept that the breadth test intentionally spans regimes.

Alerts included

• VWAP FL Long — Fires when the long condition is true (score > upper and not in short).

• VWAP FL Short — Fires on crossunder of the lower threshold (event-driven).

Messages include {{ticker}} and {{interval}} placeholders for routing.

Strengths

• Simple, transparent math — Easy to reason about and validate.

• Volume-aware by construction — Decisions reference VWAP, not just price.

• Robust to single-bar noise — Needs many lags to agree before flipping state (by design, via thresholds and the stateful output).

Limitations & cautions

• Threshold feasibility — If N < upper or |lower| > N, signals will never trigger; always cross-check N.

• Path dependence — The state variable persists until a new event; if you want frequent re-evaluation, lower thresholds or reduce N.

• Regime changes — Calendar resets can produce early ambiguity; expect a few bars for the breadth to mature.

• VWAP sensitivity to volume spikes — Large prints can tilt VWAP abruptly; that behavior is intentional in VWAP-based logic.

Suggested starting profiles

• Intraday trend bias : Anchor=Day, N=25 (1→25), upper=18–20, lower=−8, paint candles ON.

• Swing bias : Anchor=Month, N=45 (1→45), upper=38–42, lower=−10, VWAP coloring ON, background OFF.

• Balanced reactivity : Anchor=Week, N=30 (1→30), upper=20–22, lower=−10…−12, symmetric if desired.

Implementation notes

• The indicator runs in a separate pane (oscillator), but VWAP itself is drawn on price using forced overlay so you can see interactions (touches, reclaim/loss).

• HLC3 is used for VWAP price; that’s a common choice to dampen wick noise while still reflecting intrabar range.

• For-loop cap is kept modest (≤50) for performance and clarity.

How to use this responsibly

Treat the oscillator as a bias and persistence meter . Combine it with your entry framework (structure breaks, liquidity zones, higher-timeframe context) and risk controls. The design emphasizes clarity over complexity—its edge is in how strictly it demands agreement before declaring a regime, not in predicting specific turns.

Summary

VWAP For Loop distills the question “How broadly is the anchored, volume-weighted trend advancing or retreating?” into a single, thresholded score you can read at a glance, alert on, and color through your chart. With careful anchoring and thresholds sized to your window length, it becomes a pragmatic bias filter for both systematic and discretionary workflows.

15-Minute ORB by @RhinoTradezOverview

Hey traders, ready to jump on the morning breakout train? The 15-Minute ORB by @RhinoTradez

is your go-to pal for rocking the Opening Range Breakout (ORB) scene, zeroing in on the first 15 minutes of the U.S. market day—9:30 to 9:45 AM Eastern Time. Picture this: sleek orange lines mark the high and low of that opening rush, but they only hang out during regular trading hours (9:30 AM-4:00 PM ET) and reset fresh each day—no old baggage here! Built in Pine Script v6 for that cutting-edge feel, it’s loaded with breakout signals and alerts to keep your trading game strong—ideal for SPY, QQQ, or any ticker you love.

Crafted by @RhinoTradez

to fuel your daily grind—let’s hit those breakouts running!

What It Does

The ORB strategy is all about that early market spark: the 9:30-9:45 AM range sets the battlefield, and breakouts signal the charge. Here’s the rundown:

Captures the Range : Snags the high and low from the 9:30-9:45 AM ET candle—U.S. market kickoff, locked in.

Daily Refresh : Wipes yesterday’s lines at 9:30 AM ET each day—today’s all that matters.

Regular Hours Focus : Orange lines shine from 9:45 AM to 4:00 PM ET, vanishing outside those hours.

Breakout Signals : Green triangles for upside breaks, red for downside, all within regular hours.

Alerts You : Chimes in with “Price broke above 15-min ORB High: 597” (or below the low) when the move hits.

It’s your morning breakout blueprint—simple, focused, and trader-ready.

Functionality Breakdown:

15-Minute ORB Snap:

Locks the high and low of the 9:30-9:45 AM ET candle on a 15-minute chart (EST/EDT auto-adjusted).

Resets daily at 9:30 AM ET—yesterday’s range is outta here.

Regular Hours Only:

Lines glow from 9:45 AM to 4:00 PM ET, keeping pre-market and after-hours clean.

Breakout Flags:

Marks price busting above the ORB high (green triangle below bar) or below the low (red triangle above), only during 9:30 AM-4:00 PM.

Alert Action:

Drops a custom alert with the breakout price (e.g., “Price broke below 15-min ORB Low: 594”)—stay in the know, hands-free.

Customization Options

Keep it chill with one slick tweak:

ORB Line Color : Starts at orange—vibrant and trader-cool! Flip it to blue, purple, or any shade you dig in the settings. Make it yours.

How to Use It

Pop It On: Add it to a 15-minute chart—SPY, QQQ, or your hot pick works like a dream.

Time It Right: Set your chart to “America/New_York” time (Chart Settings > Time Zone) to sync with 9:30 AM ET.

Choose Your Color: Dive into the indicator settings and pick your ORB line color—orange kicks it off, but you’re in charge.

Set Alerts: Right-click the indicator, add an alert with “Any alert() function call,” and catch breakouts live.

Ride the Wave: Green triangle? Upward vibe. Red? Downside alert. Mix with volume or candles for extra punch.

Pro Tips

15-Minute Only : Tailored for that 9:30-9:45 AM ET candle—other timeframes won’t sync up.

Daily Reset : Lines refresh at 9:30 AM ET—always today’s play.

Breakout Boost : High volume or RSI can seal the deal on those triangle signals.

No Clutter : Lines stick to 9:30 AM-4:00 PM ET—your chart stays tidy.

Brought to you by @RhinoTradez

in Pine Script v6, this ORB script’s your morning breakout wingman. Slap it on, pick a color, and let’s chase those moves together! Happy trading!

USD Session 8FX - LDN & NY (TF-invariant, Live + Table)What changed

Flexible session window

Removed the old fixed NY end-time selector.

Added new inputs so you can pick start time and length:

London: ldnStartSel (default 08:00) and ldnLenSel with options 45/60/90 minutes.

New York: nyStartSel (default 15:30) and nyLenSel with options 45/60/90 minutes.

The session string used by time(refTF, sess, tz) is now built dynamically as "HHMM-HHMM" from start + length (e.g., 1530-1630).

The label shown in the table (winTxt) auto-formats to HH:MM–HH:MM.

New time helpers

addMinutesHHMM() computes the end time from a "HHMM" start plus a minute length.

makeSess() produces the session string "HHMM-HHMM".

prettySess() converts "HHMM-HHMM" → "HH:MM-HH:MM".

(Kept on one line to avoid the “end of line without line continuation” error.)

Stability & UI fixes

Main table now uses table.new(f_pos(tablePos), ...) directly (no undeclared pos variable).

Trade Gate panel uses a properly initialized gatePosEnum before table.new(...) (fixes “Undeclared identifier”).

Minor cleanups; no logic changes.

What did NOT change

Scoring logic: returns → optional ATR normalization → weights → anti-USD vs USD-base averages → final score.

Thresholds: minAbsScore and live intrath alerts are unchanged.

VWAP Gate logic is the same (price vs VWAP consistency depending on USD Strong/Weak).

Freeze/Lock of values at session end is unchanged.

Alerts (session close bias, live threshold cross, and “Entry hint”) are unchanged.

Why this helps (practical impact)

Longer windows (e.g., NY 60/90, LDN 60/90) usually make the score more robust, filtering noise and reducing false signals—at the cost of a slightly slower signal.

You can now A/B test:

London: 45 vs 60 vs 90

New York: 45 vs 60 vs 90

without touching anything else; the indicator adapts automatically.

How to use

Choose Session (London / New York).

Set the start and length for that session.

The background highlight, the winTxt, and the entry/exit logic all follow the dynamic window.

Quick tips to reduce false signals

Try NY 60 or NY 90 and LDN 60 when volatility is choppy.

Keep ATR normalization ON (useATRnorm = true) for more comparable returns.

Consider raising minAbsScore slightly (e.g., from 0.12 → 0.15–0.20) if you still see noise.

Use the VWAP Gate panel: only act when Bias OK and at least one of the Top-3 pairs shows VWAP OK.

If you want, I can add quick presets (buttons) to jump between LDN 45/60/90 and NY 45/60/90, or plot two Scores side by side for direct comparison.

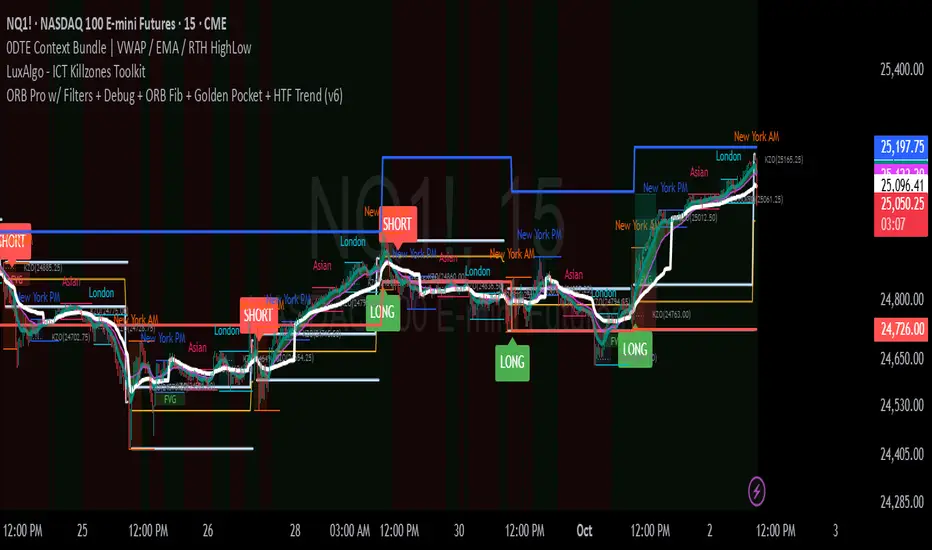

ORB Pro w/ Filters + Debug + ORB Fib + Golden Pocket + HTF Trend🚀 ORB Pro – Advanced Opening Range Breakout System

A professional ORB indicator with built-in filters, retest confirmation, EMA/HTF trend alignment, and automatic risk/reward targets. Designed to eliminate false breakouts and give traders clean LONG/SHORT signals with Fibonacci and debug overlays for maximum precision.

This script is an advanced Opening Range Breakout (ORB) system designed for futures, indices, and options traders who want more precision, cleaner entries, and higher win probability. It combines classic ORB logic with modern filters, Fibonacci confluence, and higher-timeframe trend confirmation.

The indicator automatically:

Plots the ORB box based on user-defined NY session times (default: 9:30–9:45 EST).

Generates long/short signals when price breaks the ORB range, with optional conditions like:

Candle close outside the range

Retest confirmation (with tolerance %)

Volume spike validation

EMA trend alignment

Higher-timeframe EMA slope alignment

Cooldown filters to prevent over-trading

Integrates Fibonacci retracements & extensions from the ORB box for confluence levels.

Includes Golden Pocket (0.5–0.618) retests for precision entries

Risk/Reward visualization — automatically plots stop loss and take profit levels based on user-defined R:R or fixed % levels.

Debug mode overlay to show why a signal is blocked (e.g., low volume, ORB too small, too late, wrong trend).

This tool is built for scalpers, day traders, and 0DTE options traders who need both flexibility and discipline.

⚙️ Inputs & Features

ORB Settings

ORB Start & End Time (NY) → Default: 9:30–9:45

Require Candle Close → Ensures breakouts are confirmed, not wick traps.

Retest Confirmation → Optional retest before entry (tolerance % adjustable).

Filters

Volume Spike → Validates breakouts only with above-average volume.

EMA Trend Filter → Confirms trade direction with EMA slope.

Higher Timeframe Trend → Optional (e.g., 15m ORB with 1h EMA alignment).

Cooldown Bars → Prevents consecutive false signals.

ORB Size Filter → Blocks signals when ORB is too small/too large.

Fibonacci Levels

Retracements: 0.236, 0.382, 0.5, 0.618, 0.786

Extensions: 1.272, 1.618

Golden Pocket Retest filter for high-probability trades

Risk Management

R:R Stops/Targets → Automatically plots SL/TP levels.

Custom Stop % / Take Profit % if not using R:R

Debug Overlay → Explains why signals are blocked

🧑💻 How to Use

Load the indicator on your chart (works best on 1m, 5m, and 15m).

Adjust ORB window (default 9:30–9:45 EST).

Select filters (candle close, retest, volume, EMA, HTF trend).

Watch for Long/Short labels outside ORB box with filters aligned.

Manage trades using plotted SL/TP levels or your own Webull/R:R calculator.

✅ Best Use Cases

Futures (NQ1!, ES1!)

ETFs (QQQ, SPY, IWM)

0DTE Options Trading

Scalping around market open

⚠️ Disclaimer

This tool is for educational purposes only. It does not constitute financial advice. Trading carries risk, and past performance does not guarantee future results. Always test on paper trading before using real capital.

-----------------------------------------

ORB Pro w/ Filters + Debug + ORB Fib + Golden Pocket + HTF Trend

A professional Opening Range Breakout (ORB) toolkit designed for intraday traders who want precision entries, risk-managed exits, and layered confirmation filters. Built for futures, stocks, and ETFs (e.g. NQ, ES, QQQ).

🔎 Core Logic

This script plots and trades breakouts from the Opening Range (9:30 – 9:45 NY time), then applies multiple confirmation filters before signaling a LONG or SHORT setup:

ORB Box: Defines the first 15 minutes of market activity (customizable).

Breakout Candle Confirmation: Requires a candle close outside the ORB box.

Retest Confirmation: Price must retest the ORB edge within tolerance before triggering.

Trend Filter: EMA confirmation to align trades with intraday trend.

Higher-Timeframe Trend Filter: Optional (default: 45-minute EMA) to avoid countertrend trades.

Fibonacci Levels: Auto-plot retracements (0.236 → 0.786) for confluence and trade management.

Golden Pocket Retest (Optional): Adds an extra precision filter at 0.5–0.618 retracement.

⚙️ Default Settings (Optimized for Beginners)

These are the pre-configured inputs so traders can load and trade immediately:

ORB Session: 9:30 – 9:45 NY

✅ Require Candle Close Outside ORB

✅ Require Retest Confirmation (tolerance 0.333%)

❌ Require Volume Spike (off by default, optional toggle)

✅ Require EMA Trend (50 EMA intraday)

✅ Require Higher-TF Trend (45m, EMA 21)

❌ Higher-TF EMA slope required (off)

✅ Cooldown Between Signals (10 bars)

ORB % Range: Min 0.3%, Max 0.5%

Max Minutes After ORB: 180

✅ ORB-based Risk/Reward Stops & Targets (default: 2R)

Stop Loss: 0.5% (if not R:R)

Take Profit: 1% (if not R:R)

✅ Debug Overlay (shows why signals are blocked)

✅ Fibonacci Retracements Plotted

❌ Extensions (off by default, toggle if needed)

✅ Golden Pocket Retest available, tolerance 0.11 (optional)

📈 Signals

Green "LONG" Label: Valid breakout above ORB with trend confirmation.

Red "SHORT" Label: Valid breakdown below ORB with trend confirmation.

Blocked (debug text): Signal suppressed by filters (low volume, too late, no retest, etc.).

🎯 Trade Management

Default R:R is 2:1 (stop at ORB edge, TP projected).

For manual trading (e.g., Webull, IBKR), you can use the plotted TP/SL boxes directly.

Fibonacci + Golden Pocket give additional profit-taking levels and retest filters.

✅ Best Practices

Use 15m chart for main ORB entries.

Confirm direction with HTF trend (45m EMA by default).

Avoid signals blocked by “Low Volume” or “Too Late” (debug helps identify).

Adjust ORB % range for asset volatility (tight for ETFs, wider for futures).

🚀 Why ORB Pro?

This is more than a standard ORB indicator. It’s a professional breakout system with filters designed to avoid false breakouts, automatically handle risk/reward, and guide traders with clear visual signals. Perfect for both systematic day traders and discretionary scalpers who want structure and confidence.

👉 Recommended starting point:

Load defaults → trade the 15m ORB with EMA + HTF filters on → let the script handle retests and stop/target placement.

Confluence Engine Confluence Engine is a practical, non-repainting decision aid that scores market conditions from −100…+100 by combining six proven modules: Trend, Momentum, Volatility, Volume, Structure, and an HTF confirmation. It’s designed for crypto, forex, indices, and stocks, and it fires entries only on confirmed bar closes.

What’s inside

Trend: EMA 20/50/200 alignment plus a Supertrend/KAMA toggle (you choose the baseline).

Momentum: RSI + MACD with confirmed-pivot divergence detection.

Volatility: ATR% and Bollinger Band width vs its average to favor expansion over chop.

Volume: OBV-style cumulative flow slope + volume surge vs SMA×multiplier.

Market Structure: Confirmed pivots, BOS (break of structure) and CHOCH (change of character).

HTF Filter: Closed higher-timeframe context via request.security(..., barmerge.gaps_on, barmerge.lookahead_off).

Why it does not repaint

Signals are computed and plotted on closed bars only.

Pivots/divergences use confirmed pivot points (no forward look).

HTF series are fetched with lookahead_off and use the last closed HTF bar in realtime.

No future bar references are used for entries or alerts.

How to use (3 steps)

Pick a timeframe pair: use a 4–6× HTF multiplier (5m→30m, 15m→1h, 1h→4h, 4h→1D, 1D→1W).

Trade with the HTF: take longs only when the HTF filter is bullish; shorts only when bearish.

Prefer expansion: act when BB width > its average and ATR% is elevated; skip most signals in compression.

Suggested presets (start here)

Crypto (BTC/ETH): 15m→1h, 1h→4h. stLen=10, stMult=3.0, bbLen=20, surgeMul=1.8–2.2, thresholds +40 / −40 (intraday can try +35 / −35).

Forex majors: 15m→1h, 1h→4h. stLen=10–14, stMult=2.5–3.0, surgeMul=1.5–1.8, thresholds +35 / −35 (swing: +45 / −45).

US equities (liquid): 5m→30m/1h, 15m→1h/2h. stMult=3.0–3.5, surgeMul=1.6–2.0, thresholds +45 / −45 to reduce chop.

Indices (ES/NQ): 5m→30m, 15m→1h. Defaults are fine; start at +40 / −40.

Gold/Oil: 15m→1h, 1h→4h. Thresholds +35 / −35, surgeMul=1.6–1.9.

Inputs (plain English)

Use Supertrend (off = KAMA): choose the trend baseline.

EMA Fast/Mid/Slow: 20/50/200 by default for classic stack.

RSI/MACD + divergence pivots: momentum and exhaustion context.

ATR Length & BB Length: volatility regime detection.

Volume SMA & Surge Multiplier: defines “meaningful” volume spikes.

Pivot left/right & “Confirm BOS/CHOCH on Close”: structure strictness.

Enable HTF & Higher Timeframe: confirms the lower timeframe direction.

Thresholds (+long / −short): when the score crosses these, you get signals.

Signals & alerts (IDs preserved)

Entry shapes plot at bar close when the score crosses thresholds.

Alerts you can enable:

CONFLUENCE LONG — long entry signal

CONFLUENCE SHORT — short entry signal

BULLISH BIAS — score turned positive

BEARISH BIAS — score turned negative

Best practices

Focus on signals with HTF agreement and volatility expansion; require volume participation (surge or rising OBV slope) for higher quality.

Raise thresholds (+45/−45 or +50/−50) to reduce whipsaws in choppy sessions.

Lower thresholds (+35/−35) only if you also require volatility/volume filters.

Performance & scope

Works across crypto/FX/equities/indices; no broker data or special feeds required.

No repainting by design; signals/alerts are computed on closed bars.

As with any tool, results vary by regime; always combine with risk management.

Disclosure

This script is for educational purposes only and is not financial advice. Trading involves risk. Test on historical data and paper trade before using live.

F&O Time Zones – Final Fixed📌 This indicator highlights high-probability intraday time zones used in Indian F&O (Futures & Options) strategies. Ideal for scalping, breakout setups, and trap avoidance.

🕒 Covered Time Zones:

• 9:15 – 9:21 AM → Flash Trades (first 1-minute volatility)

• 9:21 – 9:30 AM → Smart Money Trap (VWAP fakeouts)

• 9:30 – 9:50 AM → Fake Breakout Zone

• 9:50 – 10:15 AM → Institutional Entry Timing

• 10:15 – 10:45 AM → VWAP Range Scalps

• 10:45 – 11:15 AM → Second Trap Zone

• 11:15 – 1:00 PM → Trend Continuation Window

• 1:00 – 1:45 PM → Volatility Compression

• 1:45 – 2:15 PM → Institutional Exit Phase 1

• 2:15 – 2:45 PM → Trend Acceleration / Reversals

• 2:45 – 3:15 PM → Expiry Scalping Zone

• 3:15 – 3:30 PM → Dead Zone (square-off time)

🔧 Features:

✓ Clean vertical lines per zone

✓ Optional label positions (top or bottom)

✓ Adjustable line style, width, and color

🧠 Best used on: NIFTY, BANKNIFTY, FINNIFTY (5-min or lower)

---

🔒 **Disclaimer**:

This script is for **educational purposes only**. It is not financial advice. Trading involves risk. Please consult a professional or do your own research before taking any positions.

—

👤 Script by: **JoanJagan**

🛠️ Built in Pine Script v5

0830-0845 High/Low Marker (Accurate Start + History)This indicator marks the high and low of the 15-minute candle between 08:30 and 08:45 (local time) of the trading session. The high and low are tracked dynamically, with the lines drawn once the 08:45 candle closes.

Key Features:

Session-based Tracking: Automatically tracks and records the high and low of the 15-minute period starting at 08:30 and ending at 08:45.

Excludes 08:45 High : If a high is created exactly at 08:45, the indicator will ignore it and use the highest value before 08:45, ensuring it only references the price action during the specified window.

Line Extension : The high and low lines are drawn and extended to the right for a user-defined number of bars, making them visible beyond the session's close.

Customizable Parameters : Adjust the start and end times of the session, line colors, and line width to fit your preferences.

Use Case :

Ideal for traders who focus on the price action during the early part of the trading session (08:30 to 08:45) and want to track significant levels of support and resistance from that period.

The extended lines help identify potential price zones for the rest of the session or the trading day.