Reset Strike Options-Type 1 [Loxx]In a reset call (put) option, the strike is reset to the asset price at a predetermined future time, if the asset price is below (above) the initial strike price. This makes the strike path-dependent. The payoff for a call at maturity is equal to max((S-X)/X, 0) where is equal to the original strike X if not reset, and equal to the reset strike if reset. Similarly, for a put, the payoff is max((X-S)/X, 0) Gray and Whaley (1997) x have derived a closed-form solution for such an option. For a call, we have

c = e^(b-r)(T2-T1) * N(-a2) * N(z1) * e^(-rt1) - e^(-rT2) * N(-a2)*N(z2) - e^(-rT2) * M(a2, y2; p) + (S/X) * e^(b-r)T2 * M(a1, y1; p)

and for a put,

p = e^(-rT2) * N(a2) * N(-z2) - e^(b-r)(T2-T1) * N(a2) * N(-z1) * e^(-rT1) + e^(-rT2) * M(-a2, -y2; p) - (S/X) * e^(b-r)T2 * M(-a1, -y1; p)

where b is the cost-of-carry of the underlying asset, a is the volatil- ity of the relative price changes in the asset, and r is the risk-free interest rate. X is the strike price of the option, r the time to reset (in years), and T is its time to expiration. N(x) and M(a, b; p) are, respec- tively, the univariate and bivariate cumulative normal distribution functions. The remaining parameters are p = (T1/T2)^0.5 and

a1 = (log(S/X) + (b+v^2/2)T1) / vT1^0.5 ... a2 = a1 - vT1^0.5

z1 = (b+v^2/2)(T2-T1)/v(T2-T1)^0.5 ... z2 = z1 - v(T2-T1)^0.5

y1 = log(S/X) + (b+v^2)T2 / vT2^0.5 ... y2 = y1 - vT2^0.5

b=r options on non-dividend paying stock

b=r-q options on stock or index paying a dividend yield of q

b=0 options on futures

b=r-rf currency options (where rf is the rate in the second currency)

Inputs

Asset price ( S )

Initial strike price ( X1 )

Extended strike price ( X2 )

Initial time to maturity ( t1 )

Extended time to maturity ( T2 )

Risk-free rate ( r )

Cost of carry ( b )

Volatility ( s )

Numerical Greeks or Greeks by Finite Difference

Analytical Greeks are the standard approach to estimating Delta, Gamma etc... That is what we typically use when we can derive from closed form solutions. Normally, these are well-defined and available in text books. Previously, we relied on closed form solutions for the call or put formulae differentiated with respect to the Black Scholes parameters. When Greeks formulae are difficult to develop or tease out, we can alternatively employ numerical Greeks - sometimes referred to finite difference approximations. A key advantage of numerical Greeks relates to their estimation independent of deriving mathematical Greeks. This could be important when we examine American options where there may not technically exist an exact closed form solution that is straightforward to work with. (via VinegarHill FinanceLabs)

Numerical Greeks Ouput

Delta

Elasticity

Gamma

DGammaDvol

GammaP

Vega

DvegaDvol

VegaP

Theta (1 day)

Rho

Rho futures option

Phi/Rho2

Carry

DDeltaDvol

Speed

Things to know

Only works on the daily timeframe and for the current source price.

You can adjust the text size to fit the screen

스크립트에서 "通达信+选股公式+换手率+0.5+源码"에 대해 찾기

Hurst Exponent Oscillator [PhenLabs]📊 Hurst Exponent Oscillator -

Version: PineScript™ v5

📌 Description

The Hurst Exponent Oscillator (HEO) by PhenLabs is a powerful tool developed for traders who want to distinguish between trending, mean-reverting, and random market behaviors with clarity and precision. By estimating the Hurst Exponent—a statistical measure of long-term memory in financial time series—this indicator helps users make sense of underlying market dynamics that are often not visible through traditional moving averages or oscillators.

Traders can quickly know if the market is likely to continue its current direction (trending), revert to the mean, or behave randomly, allowing for more strategic timing of entries and exits. With customizable smoothing and clear visual cues, the HEO enhances decision-making in a wide range of trading environments.

🚀 Points of Innovation

Integrates advanced Hurst Exponent calculation via Rescaled Range (R/S) analysis, providing unique market character insights.

Offers real-time visual cues for trending, mean-reverting, or random price action zones.

User-controllable EMA smoothing reduces noise for clearer interpretation.

Dynamic coloring and fill for immediate visual categorization of market regime.

Configurable visual thresholds for critical Hurst levels (e.g., 0.4, 0.5, 0.6).

Fully customizable appearance settings to fit different charting preferences.

🔧 Core Components

Log Returns Calculation: Computes log returns of the selected price source to feed into the Hurst calculation, ensuring robust and scale-independent analysis.

Rescaled Range (R/S) Analysis: Assesses the dispersion and cumulative deviation over a rolling window, forming the core statistical basis for the Hurst exponent estimate.

Smoothing Engine: Applies Exponential Moving Average (EMA) smoothing to the raw Hurst value for enhanced clarity.

Dynamic Rolling Windows: Utilizes arrays to maintain efficient, real-time calculations over user-defined lengths.

Adaptive Color Logic: Assigns different highlight and fill colors based on the current Hurst value zone.

🔥 Key Features

Visually differentiates between trending, mean-reverting, and random market modes.

User-adjustable lookback and smoothing periods for tailored sensitivity.

Distinct fill and line styles for each regime to avoid ambiguity.

On-chart reference lines for strong trending and mean-reverting thresholds.

Works with any price series (close, open, HL2, etc.) for versatile application.

🎨 Visualization

Hurst Exponent Curve: Primary plotted line (smoothed if EMA is used) reflects the ongoing estimate of the Hurst exponent.

Colored Zone Filling: The area between the Hurst line and the 0.5 reference line is filled, with color and opacity dynamically indicating the current market regime.

Reference Lines: Dash/dot lines mark standard Hurst thresholds (0.4, 0.5, 0.6) to contextualize the current regime.

All visual elements can be customized for thickness, color intensity, and opacity for user preference.

📖 Usage Guidelines

Data Settings

Hurst Calculation Length

Default: 100

Range: 10-300

Description: Number of bars used in Hurst calculation; higher values mean longer-term analysis, lower values for quicker reaction.

Data Source

Default: close

Description: Select which data series to analyze (e.g., Close, Open, HL2).

Smoothing Length (EMA)

Default: 5

Range: 1-50

Description: Length for smoothing the Hurst value; higher settings yield smoother but less responsive results.

Style Settings

Trending Color (Hurst > 0.5)

Default: Blue tone

Description: Color used when trending regime is detected.

Mean-Reverting Color (Hurst < 0.5)

Default: Orange tone

Description: Color used when mean-reverting regime is detected.

Neutral/Random Color

Default: Soft blue

Description: Color when market behavior is indeterminate or shifting.

Fill Opacity

Default: 70-80

Range: 0-100

Description: Transparency of area fills—higher opacity for stronger visual effect.

Line Width

Default: 2

Range: 1-5

Description: Thickness of the main indicator curve.

✅ Best Use Cases

Identifying if a market is regime-shifting from trending to mean-reverting (or vice versa).

Filtering signals in automated or systematic trading strategies.

Spotting periods of randomness where trading signals should be deprioritized.

Enhancing mean-reversion or trend-following models with regime-awareness.

⚠️ Limitations

Not predictive: Reflects current and recent market state, not future direction.

Sensitive to input parameters—overfitting may occur if settings are changed too frequently.

Smoothing can introduce lag in regime recognition.

May not work optimally in markets with structural breaks or extreme volatility.

💡 What Makes This Unique

Employs advanced statistical market analysis (Hurst exponent) rarely found in standard toolkits.

Offers immediate regime visualization through smart dynamic coloring and zone fills.

🔬 How It Works

Rolling Log Return Calculation:

Each new price creates a log return, forming the basis for robust, non-linear analysis. This ensures all price differences are treated proportionally.

Rescaled Range Analysis:

A rolling window maintains cumulative deviations and computes the statistical “range” (max-min of deviations). This is compared against the standard deviation to estimate “memory”.

Exponent Calculation & Smoothing:

The raw Hurst value is translated from the log of the rescaled range ratio, and then optionally smoothed via EMA to dampen noise and false signals.

Regime Detection Logic:

The smoothed value is checked against 0.5. Values above = trending; below = mean-reverting; near 0.5 = random. These control plot/fill color and zone display.

💡 Note:

Use longer calculation lengths for major market character study, and shorter ones for tactical, short-term adaptation. Smoothing balances noise vs. lag—find a best fit for your trading style. Always combine regime awareness with broader technical/fundamental context for best results.

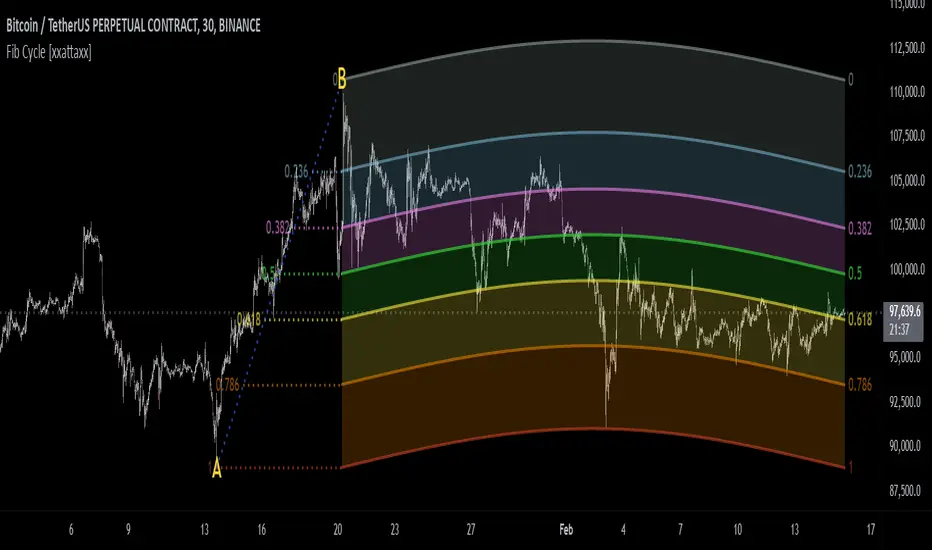

Fibonacci Cycle Finder🟩 Fibonacci Cycle Finder is an indicator designed to explore Fibonacci-based waves and cycles through visualization and experimentation, introducing a trigonometric approach to market structure analysis. Unlike traditional Fibonacci tools that rely on static horizontal levels, this indicator incorporates the dynamic nature of market cycles, using adjustable wavelength, phase, and amplitude settings to visualize the rhythm of price movements. By applying a sine function, it provides a structured way to examine Fibonacci relationships in a non-linear context.

Fibonacci Cycle Finder unifies Fibonacci principles with a wave-based method by employing adjustable parameters to align each wave with real-time price action. By default, the wave begins with minimal curvature, preserving the structural familiarity of horizontal Fibonacci retracements. By adjusting the input parameters, the wave can subtly transition from a horizontal line to a more pronounced cycle,visualizing cyclical structures within price movement. This projective structure extends potential cyclical outlines on the chart, opening deeper exploration of how Fibonacci relationships may emerge over time.

Fibonacci Cycle Finder further underscores a non-linear representation of price by illustrating how wave-based logic can uncover shifts that are missed by static retracement tools. Rather than imposing immediate oscillatory behavior, the indicator encourages a progressive approach, where the parameters may be incrementally modified to align wave structures with observed price action. This refinement process deepens the exploration of Fibonacci relationships, offering a systematic way to experiment with non-linear price dynamics. In doing so, it revisits fundamental Fibonacci concepts, demonstrating their broader adaptability beyond fixed horizontal retracements.

🌀 THEORY & CONCEPT 🌀

What if Fibonacci relationships could be visualized as dynamic waves rather than confined to fixed horizontal levels? Fibonacci Cycle Finder introduces a trigonometric approach to market structure analysis, offering a different perspective on Fibonacci-based cycles. This tool provides a way to visualize market fluctuations through cyclical wave motion, opening the door to further exploration of Fibonacci’s role in non-linear price behavior.

Traditional Fibonacci tools, such as retracements and extensions, have long been used to identify potential support and resistance levels. While valuable for analyzing price trends, these tools assume linear price movement and rely on static horizontal levels. However, market fluctuations often exhibit cyclical tendencies , where price follows natural wave-like structures rather than strictly adhering to fixed retracement points. Although Fibonacci-based tools such as arcs, fans, and time zones attempt to address these patterns, they primarily apply geometric projections. The Fibonacci Cycle Finder takes a different approach by mapping Fibonacci ratios along structured wave cycles, aligning these relationships with the natural curvature of market movement rather than forcing them onto rigid price levels.

Rather than replacing traditional Fibonacci methods, the Fibonacci Cycle Finder supplements existing Fibonacci theory by introducing an exploratory approach to price structure analysis. It encourages traders to experiment with how Fibonacci ratios interact with cyclical price structures, offering an additional layer of insight beyond static retracements and extensions. This approach allows Fibonacci levels to be examined beyond their traditional static form, providing deeper insights into market fluctuations.

📊 FIBONACCI WAVE IMPLEMENTATION 📊

The Fibonacci Cycle Finder uses two user-defined swing points, A and B, as the foundation for projecting these Fibonacci waves. It first establishes standard horizontal levels that correspond to traditional Fibonacci retracements, ensuring a baseline reference before wave adjustments are applied. By default, the wave is intentionally subtle— Wavelength is set to 1 , Amplitude is set to 1 , and Phase is set to 0 . In other words, the wave starts as “stretched out.” This allows a slow, measured start, encouraging users to refine parameters incrementally rather than producing abrupt oscillations. As these parameters are increased, the wave takes on more distinct sine and cosine characteristics, offering a flexible approach to exploring Fibonacci-based cyclicity within price action.

Three parameters control the shape of the Fibonacci wave:

1️⃣ Wavelength Controls the horizontal spacing of the wave along the time axis, determining the length of one full cycle from peak to peak (or trough to trough). In this indicator, Wavelength acts as a scaling input that adjusts how far the wave extends across time, rather than a strict mathematical “wavelength.” Lower values further stretch the wave, increasing the spacing between oscillations, while higher values compress it into a more frequent cycle. Each full cycle is divided into four quarter-cycle segments, a deliberate design choice to minimize curvature by default. This allows for subtle oscillations and smoother transitions, preventing excessive distortion while maintaining flexibility in wave projections. The wavelength is calculated relative to the A-B swing, ensuring that its scale adapts dynamically to the selected price range.

2️⃣ Amplitude Defines the vertical displacement of the wave relative to the baseline Fibonacci level. Higher values increase the height of oscillations, while lower values reduce the height, Negative values will invert the wave’s initial direction. The amplitude is dynamically applied in relation to the A-B swing direction, ensuring that an upward swing results in upward oscillations and a downward swing results in downward oscillations.

3️⃣ Phase Shifts the wave’s starting position along its cycle, adjusting alignment relative to the swing points. A phase of 0 aligns with a sine wave, where the cycle starts at zero and rises. A phase of 25 aligns with a cosine wave, starting at a peak and descending. A phase of 50 inverts the sine wave, beginning at zero but falling first, while a phase of 75 aligns with an inverted cosine , starting at a trough and rising. Intermediate values between these phases create gradual shifts in wave positioning, allowing for finer alignment with observed market structures.

By fine-tuning these parameters, users can adapt Fibonacci waves to better reflect observed market behaviors. The wave structure integrates with price movements rather than simply overlaying static levels, allowing for a more dynamic representation of cyclical price tendencies. This indicator serves as an exploratory tool for understanding potential market rhythms, encouraging traders to test and visualize how Fibonacci principles extend beyond their traditional applications.

🖼️ CHART EXAMPLES 🖼️

Following this downtrend, price interacts with curved Fibonacci levels, highlighting resistance at the 0.236 and 0.382 levels, where price stalls before pulling back. Support emerges at the 0.5, 0.618, and 0.786 levels, where price finds stability and rebounds

In this Fibonacci retracement, price initially finds support at the 1.0 level, following the natural curvature of the cycle. Resistance forms at 0.786, leading to a pullback before price breaks through and tests 0.618 as resistance. Once 0.618 is breached, price moves upward to test 0.5, illustrating how Fibonacci-based cycles may align with evolving market structure beyond static, horizontal retracements.

Following this uptrend, price retraces downward and interacts with the Fibonacci levels, demonstrating both support and resistance at key levels such as 0.236, 0.382, 0.5, and 0.618.

With only the 0.5 and 1.0 levels enabled, this chart remains uncluttered while still highlighting key price interactions. The short cycle length results in a mild curvature, aligning smoothly with market movement. Price finds resistance at the 0.5 level while showing strong support at 1.0, which follows the natural flow of the market. Keeping the focus on fewer levels helps maintain clarity while still capturing how price reacts within the cycle.

🛠️ CONFIGURATION AND SETTINGS 🛠️

Wave Parameters

Wavelength : Stretches or compresses the wave along the time axis, determining the length of one full cycle. Higher values extend the wave across more bars, while lower values compress it into a shorter time frame.

Amplitude : Expands or contracts the wave along the price axis, determining the height of oscillations relative to Fibonacci levels. Higher values increase the vertical range, while negative values invert the wave’s initial direction.

Phase : Offsets the wave along the time axis, adjusting where the cycle begins. Higher values shift the starting position forward within the wave pattern.

Fibonacci Levels

Levels : Enable or disable specific Fibonacci levels (0.0, 0.236, 0.382, 0.5, 0.618, 0.786, 1.0) to focus on relevant price zones.

Color : Modify level colors for enhanced visual clarity.

Visibility

Trend Line/Color : Toggle and customize the trend line connecting swing points A and B.

Setup Lines : Show or hide lines linking Fibonacci levels to projected waves.

A/B Labels Visibility : Control the visibility of swing point labels.

Left/Right Labels : Manage the display of Fibonacci level labels on both sides of the chart.

Fill % : Adjust shading intensity between Fibonacci levels (0% = no fill, 100% = maximum fill).

A and B Points (Time/Price):

These user-defined anchor points serve as the basis for Fibonacci wave calculations and can be manually set. A and B points can also be adjusted directly on the chart, with automatic synchronization to the settings panel, allowing for seamless modifications without needing to manually input values.

⚠️ DISCLAIMER ⚠️

The Fibonacci Cycle Finder is a visual analysis tool designed to illustrate Fibonacci relationships and serve as a supplement to traditional Fibonacci tools. While the indicator employs mathematical and geometric principles, no guarantee is made that its calculations will align with other Fibonacci tools or proprietary methods. Like all technical and visual indicators, the Fibonacci levels generated by this tool may appear to visually align with key price zones in hindsight. However, these levels are not intended as standalone signals for trading decisions. This indicator is intended for educational and analytical purposes, complementing other tools and methods of market analysis.

🧠 BEYOND THE CODE 🧠

Fibonacci Cycle Finder is the latest indicator in the Fibonacci Geometry Series. Building on the concepts of the Fibonacci Time-Price Zones and the Fibonacci 3-D indicators, this tool introduces a trigonometric approach to market structure analysis.

The Fibonacci Cycle Finder indicator, like other xxattaxx indicators , is designed to encourage both education and community engagement. Your feedback and insights are invaluable to refining and enhancing the Fibonacci Cycle Finder indicator. We look forward to the creative applications, observations, and discussions this tool inspires within the trading community.

Intramarket Difference Index StrategyHi Traders !!

The IDI Strategy:

In layman’s terms this strategy compares two indicators across markets and exploits their differences.

note: it is best the two markets are correlated as then we know we are trading a short to long term deviation from both markets' general trend with the assumption both markets will trend again sometime in the future thereby exhausting our trading opportunity.

📍 Import Notes:

This Strategy calculates trade position size independently (i.e. risk per trade is controlled in the user inputs tab), this means that the ‘Order size’ input in the ‘Properties’ tab will have no effect on the strategy. Why ? because this allows us to define custom position size algorithms which we can use to improve our risk management and equity growth over time. Here we have the option to have fixed quantity or fixed percentage of equity ATR (Average True Range) based stops in addition to the turtle trading position size algorithm.

‘Pyramiding’ does not work for this strategy’, similar to the order size input togeling this input will have no effect on the strategy as the strategy explicitly defines the maximum order size to be 1.

This strategy is not perfect, and as of writing of this post I have not traded this algo.

Always take your time to backtests and debug the strategy.

🔷 The IDI Strategy:

By default this strategy pulls data from your current TV chart and then compares it to the base market, be default BINANCE:BTCUSD . The strategy pulls SMA and RSI data from either market (we call this the difference data), standardizes the data (solving the different unit problem across markets) such that it is comparable and then differentiates the data, calling the result of this transformation and difference the Intramarket Difference (ID). The formula for the the ID is

ID = market1_diff_data - market2_diff_data (1)

Where

market(i)_diff_data = diff_data / ATR(j)_market(i)^0.5,

where i = {1, 2} and j = the natural numbers excluding 0

Formula (1) interpretation is the following

When ID > 0: this means the current market outperforms the base market

When ID = 0: Markets are at long run equilibrium

When ID < 0: this means the current market underperforms the base market

To form the strategy we define one of two strategy type’s which are Trend and Mean Revesion respectively.

🔸 Trend Case:

Given the ‘‘Strategy Type’’ is equal to TREND we define a threshold for which if the ID crosses over we go long and if the ID crosses under the negative of the threshold we go short.

The motivating idea is that the ID is an indicator of the two symbols being out of sync, and given we know volatility clustering, momentum and mean reversion of anomalies to be a stylised fact of financial data we can construct a trading premise. Let's first talk more about this premise.

For some markets (cryptocurrency markets - synthetic symbols in TV) the stylised fact of momentum is true, this means that higher momentum is followed by higher momentum, and given we know momentum to be a vector quantity (with magnitude and direction) this momentum can be both positive and negative i.e. when the ID crosses above some threshold we make an assumption it will continue in that direction for some time before executing back to its long run equilibrium of 0 which is a reasonable assumption to make if the market are correlated. For example for the BTCUSD - ETHUSD pair, if the ID > +threshold (inputs for MA and RSI based ID thresholds are found under the ‘‘INTRAMARKET DIFFERENCE INDEX’’ group’), ETHUSD outperforms BTCUSD, we assume the momentum to continue so we go long ETHUSD.

In the standard case we would exit the market when the IDI returns to its long run equilibrium of 0 (for the positive case the ID may return to 0 because ETH’s difference data may have decreased or BTC’s difference data may have increased). However in this strategy we will not define this as our exit condition, why ?

This is because we want to ‘‘let our winners run’’, to achieve this we define a trailing Donchian Channel stop loss (along with a fixed ATR based stop as our volatility proxy). If we were too use the 0 exit the strategy may print a buy signal (ID > +threshold in the simple case, market regimes may be used), return to 0 and then print another buy signal, and this process can loop may times, this high trade frequency means we fail capture the entire market move lowering our profit, furthermore on lower time frames this high trade frequencies mean we pay more transaction costs (due to price slippage, commission and big-ask spread) which means less profit.

By capturing the sum of many momentum moves we are essentially following the trend hence the trend following strategy type.

Here we also print the IDI (with default strategy settings with the MA difference type), we can see that by letting our winners run we may catch many valid momentum moves, that results in a larger final pnl that if we would otherwise exit based on the equilibrium condition(Valid trades are denoted by solid green and red arrows respectively and all other valid trades which occur within the original signal are light green and red small arrows).

another example...

Note: if you would like to plot the IDI separately copy and paste the following code in a new Pine Script indicator template.

indicator("IDI")

// INTRAMARKET INDEX

var string g_idi = "intramarket diffirence index"

ui_index_1 = input.symbol("BINANCE:BTCUSD", title = "Base market", group = g_idi)

// ui_index_2 = input.symbol("BINANCE:ETHUSD", title = "Quote Market", group = g_idi)

type = input.string("MA", title = "Differrencing Series", options = , group = g_idi)

ui_ma_lkb = input.int(24, title = "lookback of ma and volatility scaling constant", group = g_idi)

ui_rsi_lkb = input.int(14, title = "Lookback of RSI", group = g_idi)

ui_atr_lkb = input.int(300, title = "ATR lookback - Normalising value", group = g_idi)

ui_ma_threshold = input.float(5, title = "Threshold of Upward/Downward Trend (MA)", group = g_idi)

ui_rsi_threshold = input.float(20, title = "Threshold of Upward/Downward Trend (RSI)", group = g_idi)

//>>+----------------------------------------------------------------+}

// CUSTOM FUNCTIONS |

//<<+----------------------------------------------------------------+{

// construct UDT (User defined type) containing the IDI (Intramarket Difference Index) source values

// UDT will hold many variables / functions grouped under the UDT

type functions

float Close // close price

float ma // ma of symbol

float rsi // rsi of the asset

float atr // atr of the asset

// the security data

getUDTdata(symbol, malookback, rsilookback, atrlookback) =>

indexHighTF = barstate.isrealtime ? 1 : 0

= request.security(symbol, timeframe = timeframe.period,

expression = [close , // Instentiate UDT variables

ta.sma(close, malookback) ,

ta.rsi(close, rsilookback) ,

ta.atr(atrlookback) ])

data = functions.new(close_, ma_, rsi_, atr_)

data

// Intramerket Difference Index

idi(type, symbol1, malookback, rsilookback, atrlookback, mathreshold, rsithreshold) =>

threshold = float(na)

index1 = getUDTdata(symbol1, malookback, rsilookback, atrlookback)

index2 = getUDTdata(syminfo.tickerid, malookback, rsilookback, atrlookback)

// declare difference variables for both base and quote symbols, conditional on which difference type is selected

var diffindex1 = 0.0, var diffindex2 = 0.0,

// declare Intramarket Difference Index based on series type, note

// if > 0, index 2 outpreforms index 1, buy index 2 (momentum based) until equalibrium

// if < 0, index 2 underpreforms index 1, sell index 1 (momentum based) until equalibrium

// for idi to be valid both series must be stationary and normalised so both series hae he same scale

intramarket_difference = 0.0

if type == "MA"

threshold := mathreshold

diffindex1 := (index1.Close - index1.ma) / math.pow(index1.atr*malookback, 0.5)

diffindex2 := (index2.Close - index2.ma) / math.pow(index2.atr*malookback, 0.5)

intramarket_difference := diffindex2 - diffindex1

else if type == "RSI"

threshold := rsilookback

diffindex1 := index1.rsi

diffindex2 := index2.rsi

intramarket_difference := diffindex2 - diffindex1

//>>+----------------------------------------------------------------+}

// STRATEGY FUNCTIONS CALLS |

//<<+----------------------------------------------------------------+{

// plot the intramarket difference

= idi(type,

ui_index_1,

ui_ma_lkb,

ui_rsi_lkb,

ui_atr_lkb,

ui_ma_threshold,

ui_rsi_threshold)

//>>+----------------------------------------------------------------+}

plot(intramarket_difference, color = color.orange)

hline(type == "MA" ? ui_ma_threshold : ui_rsi_threshold, color = color.green)

hline(type == "MA" ? -ui_ma_threshold : -ui_rsi_threshold, color = color.red)

hline(0)

Note it is possible that after printing a buy the strategy then prints many sell signals before returning to a buy, which again has the same implication (less profit. Potentially because we exit early only for price to continue upwards hence missing the larger "trend"). The image below showcases this cenario and again, by allowing our winner to run we may capture more profit (theoretically).

This should be clear...

🔸 Mean Reversion Case:

We stated prior that mean reversion of anomalies is an standerdies fact of financial data, how can we exploit this ?

We exploit this by normalizing the ID by applying the Ehlers fisher transformation. The transformed data is then assumed to be approximately normally distributed. To form the strategy we employ the same logic as for the z score, if the FT normalized ID > 2.5 (< -2.5) we buy (short). Our exit conditions remain unchanged (fixed ATR stop and trailing Donchian Trailing stop)

🔷 Position Sizing:

If ‘‘Fixed Risk From Initial Balance’’ is toggled true this means we risk a fixed percentage of our initial balance, if false we risk a fixed percentage of our equity (current balance).

Note we also employ a volatility adjusted position sizing formula, the turtle training method which is defined as follows.

Turtle position size = (1/ r * ATR * DV) * C

Where,

r = risk factor coefficient (default is 20)

ATR(j) = risk proxy, over j times steps

DV = Dollar Volatility, where DV = (1/Asset Price) * Capital at Risk

🔷 Risk Management:

Correct money management means we can limit risk and increase reward (theoretically). Here we employ

Max loss and gain per day

Max loss per trade

Max number of consecutive losing trades until trade skip

To read more see the tooltips (info circle).

🔷 Take Profit:

By defualt the script uses a Donchain Channel as a trailing stop and take profit, In addition to this the script defines a fixed ATR stop losses (by defualt, this covers cases where the DC range may be to wide making a fixed ATR stop usefull), ATR take profits however are defined but optional.

ATR SL and TP defined for all trades

🔷 Hurst Regime (Regime Filter):

The Hurst Exponent (H) aims to segment the market into three different states, Trending (H > 0.5), Random Geometric Brownian Motion (H = 0.5) and Mean Reverting / Contrarian (H < 0.5). In my interpretation this can be used as a trend filter that eliminates market noise.

We utilize the trending and mean reverting based states, as extra conditions required for valid trades for both strategy types respectively, in the process increasing our trade entry quality.

🔷 Example model Architecture:

Here is an example of one configuration of this strategy, combining all aspects discussed in this post.

Future Updates

- Automation integration (next update)

Rolling Correlation with Bitcoin V1.1 [ADRIDEM]Overview

The Rolling Correlation with Bitcoin script is designed to offer a comprehensive view of the correlation between the selected ticker and Bitcoin. This script helps investors understand the relationship between the performance of the current ticker and Bitcoin over a rolling period, providing insights into their interconnected behavior. Below is a detailed presentation of the script and its unique features.

Unique Features of the New Script

Bitcoin Comparison : Allows users to compare the correlation of the current ticker with Bitcoin, providing an analysis of their relationship.

Customizable Rolling Window : Enables users to set the length for the rolling window, adapting to different market conditions and timeframes. The default value is 252 bars, which approximates one year of trading days, but it can be adjusted as needed.

Smoothing Option : Includes an option to apply a smoothing simple moving average (SMA) to the correlation coefficient, helping to reduce noise and highlight trends. The smoothing length is customizable, with a default value of 4 bars.

Visual Indicators : Plots the smoothed correlation coefficient between the current ticker and Bitcoin, with distinct colors for easy interpretation. Additionally, horizontal lines help identify key levels of correlation.

Dynamic Background Color : Adds dynamic background colors to highlight areas of strong positive and negative correlations, enhancing visual clarity.

Originality and Usefulness

This script uniquely combines the analysis of rolling correlation for a current ticker with Bitcoin, providing a comparative view of their relationship. The inclusion of a customizable rolling window and smoothing option enhances its adaptability and usefulness in various market conditions.

Signal Description

The script includes several features that highlight potential insights into the correlation between the assets:

Rolling Correlation with Bitcoin : Plotted as a red line, this represents the smoothed rolling correlation coefficient between the current ticker and Bitcoin.

Horizontal Lines and Background Color : Lines at -0.5, 0, and 0.5 help to quickly identify regions of strong negative, weak, and strong positive correlations.

These features assist in identifying the strength and direction of the relationship between the current ticker and Bitcoin.

Detailed Description

Input Variables

Length for Rolling Window (`length`) : Defines the range for calculating the rolling correlation coefficient. Default is 252.

Smoothing Length (`smoothing_length`) : The number of periods for the smoothing SMA. Default is 4.

Bitcoin Ticker (`bitcoin_ticker`) : The ticker symbol for Bitcoin. Default is "BINANCE:BTCUSDT".

Functionality

Correlation Calculation : The script calculates the daily returns for both Bitcoin and the current ticker and computes their rolling correlation coefficient.

```pine

bitcoin_close = request.security(bitcoin_ticker, timeframe.period, close)

bitcoin_dailyReturn = ta.change(bitcoin_close) / bitcoin_close

current_dailyReturn = ta.change(close) / close

rolling_correlation = ta.correlation(current_dailyReturn, bitcoin_dailyReturn, length)

```

Smoothing : A simple moving average is applied to the rolling correlation coefficient to smooth the data.

```pine

smoothed_correlation = ta.sma(rolling_correlation, smoothing_length)

```

Plotting : The script plots the smoothed rolling correlation coefficient and includes horizontal lines for key levels.

```pine

plot(smoothed_correlation, title="Rolling Correlation with Bitcoin", color=color.rgb(255, 82, 82, 50), linewidth=2)

h_neg1 = hline(-1, "-1 Line", color=color.gray)

h_neg05 = hline(-0.5, "-0.5 Line", color=color.red)

h0 = hline(0, "Zero Line", color=color.gray)

h_pos05 = hline(0.5, "0.5 Line", color=color.green)

h1 = hline(1, "1 Line", color=color.gray)

fill(h_neg1, h_neg05, color=color.rgb(255, 0, 0, 90), title="Strong Negative Correlation Background")

fill(h_neg05, h0, color=color.rgb(255, 165, 0, 90), title="Weak Negative Correlation Background")

fill(h0, h_pos05, color=color.rgb(255, 255, 0, 90), title="Weak Positive Correlation Background")

fill(h_pos05, h1, color=color.rgb(0, 255, 0, 90), title="Strong Positive Correlation Background")

```

How to Use

Configuring Inputs : Adjust the rolling window length and smoothing length as needed. Ensure the Bitcoin ticker is set to the desired asset for comparison.

Interpreting the Indicator : Use the plotted correlation coefficient and horizontal lines to assess the strength and direction of the relationship between the current ticker and Bitcoin.

Signal Confirmation : Look for periods of strong positive or negative correlation to identify potential co-movements or divergences. The background colors help to highlight these key levels.

This script provides a detailed comparative view of the correlation between the current ticker and Bitcoin, aiding in more informed decision-making by highlighting the strength and direction of their relationship.

Color Stochastic IndicatorThis Pine Script™ indicator, "Color Stochastic Indicator," is designed to visualize the stochastic oscillator with color-coded trends and shaded background levels, providing a clearer understanding of market trends and potential trading signals.

Key Features:

Customizable Parameters:

K Period: The period for the %K line in the stochastic calculation (default: 50).

D Period: The period for the %D line, which is the moving average of %K (default: 13).

Slowing: The slowing factor applied to the stochastic calculation (default: 2).

Smoothing: A factor for additional smoothing of the stochastic values (default: 1.0).

Use Crossover: Option to determine trend based on the crossover of %K and %D lines.

Display Levels: Option to show significant stochastic levels on the chart (0.2, 0.5, 0.8).

Price Field: Selection of the price field used in calculations.

Stoch Width: Line width for the %K line.

Signal Width: Line width for the %D line.

Background Colors:

Upper Level Background: Shaded area between 0.5 and 0.8 with a customizable color.

Lower Level Background: Shaded area between 0.2 and 0.5 with a customizable color.

Color-Coded Trends:

Wait (Gray): Neutral state when no clear trend is detected.

Uptrend (Green): Indicates a potential buying signal.

Downtrend (Red): Indicates a potential selling signal.

Signal Line (Blue): Represents the %D line for clearer signal identification.

Alerts:

Customizable alerts trigger when the trend changes, providing timely notifications for potential trade opportunities.

How It Works:

Stochastic Calculation:

The %K line is calculated based on the selected K Period.

The %D line is a simple moving average (SMA) of the %K line over the D Period.

Additional smoothing is applied to both %K and %D lines using the specified Smoothing factor.

Fisher Transform:

The script applies a Fisher transform to the smoothed %K values, enhancing the clarity of trend signals.

Trend Determination:

If Use Crossover is enabled, the trend is determined based on the crossover of smoothed %K and %D lines.

If Use Crossover is disabled, the trend is determined based on whether the smoothed %K value is above or below 0.5.

Background Shading:

Fixed background colors are applied using hline and fill functions, highlighting the specified levels on the chart (0.2, 0.5, 0.8).

Plotting:

The smoothed %K line is plotted with color coding based on its value relative to the %D line and threshold levels.

The %D line is plotted for reference.

How to Use:

Adding the Indicator:

Copy and paste the provided Pine Script™ code into a new indicator script in TradingView.

Save and add the indicator to your desired chart.

Configuring Parameters:

Adjust the input parameters (K Period, D Period, Slowing, etc.) according to your trading strategy and preferences.

Enable or disable the Use Crossover option based on whether you prefer trend determination by crossover or threshold.

Interpreting Signals:

Observe the color-coded %K line to identify potential buy (green) and sell (red) signals.

Use the shaded background areas to quickly assess overbought (0.5 to 0.8) and oversold (0.2 to 0.5) conditions.

Monitor alerts for trend changes to take timely trading actions.

Alerts Setup:

Set up custom alerts based on the provided alert conditions to receive notifications when the trend changes.

Originality:

This script combines the stochastic oscillator with color-coding and background shading for enhanced visualization.

It introduces a unique Fisher transform application to the smoothed %K values.

The crossover and threshold-based trend determination options provide flexibility for different trading strategies.

Customizable alert messages help traders stay informed about trend changes in real time.

By incorporating these features, the "Color Stochastic Indicator" offers a comprehensive tool for traders seeking to leverage stochastic analysis with improved clarity and actionable insights.

Trend Channels [Cryptoverse]This Indicator dynamically generates and displays on the chart Trend Channels with the pivot points it determines in each market and in each time period. The type of price used to determine the pivot points and create the channels is optional (e.g. close or high, low).

It will help you identify your entry points and stop zones and help you take positions, but it does not contain any buy and sell signals or trading strategies. It creates more successful channels on higher timeframes.

Usage Settings:

---------------------------------------------------

General Settings:

Pivot Period: This field determines how many candles before and after a candle will be counted as a peak or bottom in order to determine the peaks and troughs on the chart.

Trend Channels are created by calculating the Pivot points according to the period set here. (Default value: 6)

Top Pivot Source: Determines which value of the related candle the top pivot points will be based on.

Bottom Pivot Source: Determines which value of the related candle the lower pivot points will be based on.

(Default: closing)

Trend Channels Settings:

Show All Trend Lines: Allows you to show or hide trend channels.

Hide Old Trend Lines: If you activate it, it allows you to hide the channels created in the past other than the current trend channels.

Hide 0.5 Lines: Allows you to hide lines at the Fibonacci 0.5 level.

Hide 0.236 Lines: Allows to hide lines at Fibonacci 0.236 level.

Hide 0.786 Lines: Allows to hide lines at Fibonacci 0.786 level.

Helper Line Format: Allows the helper line that converts a trend line into a channel to be drawn based on percentage or price.

*Note:* When using large time intervals by choosing percentages, there may be situations where the helper lines do not provide full parallels.

Up Trend Color: Indicates the outer color of the Up Trend channel.

Down Trend Color: Indicates the outer color of the Descending Trend channel.

0.5 Trend Color: Specifies the color of the fibonacci 0.5 line drawn for all channels.

0.236 Trend Color: Specifies the color of the fibonacci 0.5 line drawn for all channels.

0.786 Trend Color: Sets the color of the fibonacci 0.5 line drawn for all channels.

Trend Channel Width: Determines the thickness of the channel lines.

Trend Channel Style: Determines the style of the channel lines.

Custom Fib by Dr. MauryaThis indicator is based on purely Fibonacci levels.

How it works:

Let's first understand the Fibonacci levels.

The main Fibonacci numbers are 0, 0.236, 0.392, 0.5, 0.618, 0.764, 1 whereas 0 equal to low and 1 equal to high.

As the market is moving in any direction, new lows or new highs are developing and hence Fibonacci levels are also changing throughout the time.

Sometime market retraces from various levels like 0.5, 0.618/0.382(mirror value), 0.762/0.236 (mirror value).

Retracement : The three mid-level 0.382, 0.5 and 0.618 are act as a retracement or like pivot levels for market. These levels are filled with green and red colors to attention the buyers and sellers to take a trade either side if any candlestick pattern are observed at these levels.

one direction trend takes support of 0.236/0.786(mirror value) (blue line in chart)

Sometime buy/sell on dip levels are happen at 0.762/0.392 (mirror value).

Targets: Target could be Fibonacci extension level lowest targets (1, 1.18, 1.23,), medium targets (1.39, 1.5, 1.61) and large target (2.0, 2.5.2.61, 3.0) as depended on your study volume levels and trend strength.

Stoploss: You can choose any preceding lines for stoploss: e.g. if you enter long on 0.618 or 0.5 levels you can set SL on 0.762

Previous day three mid-point 0.382, 0.5, 0.618 (filled with red and green color) as well as high and low could also act as resistance or support levels for current day market.

Lets understand the Input section of indicator

The first input section allowed to choose where you want to start developing Fibonacci : select session for intraday then weekly, monthly and yearly options are available.

Now you can set any Fibonacci levels (as you wish) you can set upto 20 levels.

By default, total 7 Fibonacci levels are plotted (0, 0.236, 0.392, 0.618, 0.762 and 1.

Further you can set Fibonacci extension level for long side (1.18, 1.23, 1.39, 1.5, 1.61, 2 etc).

You must be careful when you enter Fibonacci extension level lower side (short side). You need to enter value -0.5 (equal to 1.5 for long). -0.618 (equal to 1.618 for long), -1(equal to 2.0 for long).

You can fill color between any two adjacent lines from style sections.

You can also select labels from input tab if you want to see Fibonacci numbers on chart as labels.

You can also shift the labels from current bar to desired offset bar by changing the value in input section.

Conclusion

This indicator is highly customisable developing Fibonacci levels because everyone and different scripts works on different fib levels.

This indicator keeps the Fibonacci levels at a particular time and it plots only new lines when new low or high established without affecting the previous Fibonacci levels. Overall, as the market moves, you will find the trending plot goes which side.

Public Sentiment Oscillator This is a combination of 9 common use indicators turned into on single oscillator. These indicators are: 200 day moving average cross, 9/12 ema cross, 13/48 sma cross, rsi, stochastic, mfi, cci, macd, and open close trend. I have weighted the scores to be pretty even so that its balances each indicator in the sum. Because of the odd number of indicators, I have decided to normalized the score to 10. I think this has the effect of making it easier to read.

The score definition: oc_trend > 0 ? 1 : 0, fast_e > slow_e ? 1 : 0, fast_s > slow_s ? 1 : 0, rsi < 30 ? 0 : rsi > 30 and rsi < 70 ? 0.5 : rsi > 70 ? 1 : 0, macd1 > macd2 ? 0.5 : macd1 < macd2 ? 0 : 0, (hist >=0 ? (hist < hist ? 0.5 : 0.25) : (hist < hist ? 0.25 : 0)), stoch < 20 ? 0 : stoch > 20 and stoch < 80 ? 0.5 : stoch > 80 ? 1 : 0, source > ma200 ? 1 : ex <= ma200 ? 0 : 0, mfi < 20 ? 0 : mfi > 20 and mfi < 80 ? 0.5 : mfi > 80 ? 1 : 0, cci < -100 ? 0 : cci > -100 and cci < 100 ? 0.5 : cci > 100 ? 1 : 0

I hope you find this useful in your trades. Enjoy!

Reset Strike Options-Type 2 (Gray Whaley) [Loxx]For a reset option type 2, the strike is reset in a similar way as a reset option 1. That is, the strike is reset to the asset price at a predetermined future time, if the asset price is below (above) the initial strike price for a call (put). The payoff for such a reset call is max(S - X, 0), and max(X - S, 0) for a put, where X is equal to the original strike X if not reset, and equal to the reset strike if reset. Gray and Whaley (1999) have derived a closed-form solution for the price of European reset strike options. The price of the call option is then given by (via "The Complete Guide to Option Pricing Formulas")

c = Se^(b-r)T2 * M(a1, y1; p) - Xe^(-rT2) * M(a2, y2; p) - Se^(b-r)T1 * N(-a1) * N(z2) * e^-r(T2-T1) + Se^(b-r)T2 * N(-a1) * N(z1)

p = Se^(b-r)T1 * N(a1) * N(-z2) * e^-r(T2-T1) + Se^(b-r)T2 * N(a1) * N(-z1) + Xe^(-rT2) * M(-a2, -y2; p) - Se^(b-r)T2 * M(-a1, -y1; p)

where b is the cost-of-carry of the underlying asset, a is the volatility of the relative price changes in the asset, and r is the risk-free interest rate. K is the strike price of the option, T1 the time to reset (in years), and T2 is its time to expiration. N(x) and M(a,b; p) are, respectively, the univariate and bivariate cumulative normal distribution functions. Further

a1 = (log(S/X) + (b+v^2/2)T1) / v*T1^0.5 ... a2 = a1 - v*T1^0.5

z1 = ((b+v^2/2)(T2-T1)) / v*(T2-T1)^0.5 ... z2 = z1 - v*(T2-T1)^0.5

y1 = (log(S/X) + (b+v^2/2)T1) / v*T1^0.5 ... y2 = a1 - v*T1^0.5

and p = (T1/T2)^0.5. For reset options with multiple reset rights, see Dai, Kwok, and Wu (2003) and Liao and Wang (2003).

Inputs

Asset price ( S )

Strike price ( K )

Reset time ( T1 )

Time to maturity ( T2 )

Risk-free rate ( r )

Cost of carry ( b )

Volatility ( s )

Numerical Greeks or Greeks by Finite Difference

Analytical Greeks are the standard approach to estimating Delta, Gamma etc... That is what we typically use when we can derive from closed form solutions. Normally, these are well-defined and available in text books. Previously, we relied on closed form solutions for the call or put formulae differentiated with respect to the Black Scholes parameters. When Greeks formulae are difficult to develop or tease out, we can alternatively employ numerical Greeks - sometimes referred to finite difference approximations. A key advantage of numerical Greeks relates to their estimation independent of deriving mathematical Greeks. This could be important when we examine American options where there may not technically exist an exact closed form solution that is straightforward to work with. (via VinegarHill FinanceLabs)

Numerical Greeks Outputs

Delta D

Elasticity L

Gamma G

DGammaDvol

GammaP G

Vega

DvegaDvol

VegaP

Theta Q (1 day)

Rho r

Rho futures option r

Phi/Rho2

Carry

DDeltaDvol

Speed

Strike Delta

Strike gamma

Things to know

Only works on the daily timeframe and for the current source price.

You can adjust the text size to fit the screen

Variable Purchase Options [Loxx]Handley (2001) describes how to value variable purchase options (VPO). A VPO is basically a call option, but where the number of underlying shares is stochastic rather than fixed, or more precisely, a deterministic function of the asset price. The strike price of a VPO is typically a fixed discount to the underlying share price at maturity. The payoff at maturity is equal to max , where N is the number of shares. VPOs may be an interesting tool for firms that need to raise capital relatively far into the future at a given time. The number of underlying shares N is decided on at maturity and is equal to

N = X / St(1 -D)

where X is the strike price, ST is the asset price at maturity, and D is the fixed discount expressed as a proportion 0 > D < 1. The number of shares is in this way a deterministic function of the asset price. Further, the number of shares is often subjected to a minimum and maximum. In this case, we will limit the minimum number of shares to Nmin = X / U(1 -D) if, the asset price at maturity is above a predefined level U at maturity. Similarly, we will reach the maximum number of shares A T = x if the stock price at maturity is equal Nmax = X / L(1 -D) or lower than a predefined level L. Based on Handley (2001), we get the following closed-form solution: (via "The Complete Guide to Option Pricing Formulas")

c = XD / 1-D e^-rT + Nmin(Se^(b-r)T * N(d1) - Ue^-rT * N(d2))

- Nmax(Le^-rT * N(-d4) - Se^(b-r)T * N(-d3))

+ Nmax(L(1-D)e^-rT * N(-d6) - Se^(b-r)T * N(-d5))

where

d1 = (log(S/U) + (b+v^2/2)T) / vT^0.5 ... d2 = d1 - vT^0.5

d3 = (log(S/L) + (b+v^2/2)T) / vT^0.5 ... d4 = d3 - vT^0.5

d5 = (log(S/L(1-D)) + (b+v^2/2)T) / vT^0.5 ... d6 = d5 - vT^0.5

Inputs

Asset price (S)

Strike price (K)

Discount %

Lower bound

Upper bound

Time to maturity

Risk-free rate (r) %

Cost of carry (b) %

Volatility (v) %

Things to know

Only works on the daily timeframe and for the current source price.

You can adjust the text size to fit the screen

American Approximation Bjerksund & Stensland 2002 [Loxx]American Approximation Bjerksund & Stensland 2002 is an American Options pricing model. This indicator also includes numerical greeks. You can compare the output of the American Approximation to the Black-Scholes-Merton value on the output of the options panel.

The Bjerksund & Stensland (2002) Approximation

The Bjerksund and Stensland (2002) approximation divides the time to maturity into two parts, each with a separate flat exercise boundary. It is thus a straightforward generalization of the Bjerksund-Stensland 1993 algorithm. The method is fast and efficient and should be more accurate than the Barone-Adesi and Whaley (1987) and the Bjerksund and Stensland (1993b) approximations. The algorithm requires an accurate cumulative bivariate normal approximation. Several approximations that are described in the literature are not sufficiently accurate, but the Genze algorithm works.

C = alpha2*S^B - alpha2*phi(S, t1, B, I2, I2)

+ phi(S, t1, I2, I2) - phi(S, t1, I, I1, I2)

- X*phi(S, t1, 0, I2, I2) + X*phi(S, t1, 0, I1, I2)

+ alpha1*phi(X, t1, B, I1, I2) - alpha1*psi*St, T, B, I1, I2, I1, t1)

+ psi(S, T, 1, I1, I2, I1, t1) - psi(S, T, 1, X, I2, I1, t1)

- X*psi(S, T, 0, I1, I2, I1, t1) + psi(S, T, 0 ,X, I2, I1, t1)

where

alpha1 = (I1 - X)*I1^-B

alpha2 = (I2 - X)*I2^-B

B = (1/2 - b/v^2) + ((b/v^2 - 1/2)^2 + 2*(r/v^2))^0.5

The function psi(S, T, y, H, I) is given by

psi(S, T, gamma, H, I) = e^lambda * S^gamma * (N(-d) - (I/S)^k * N(-d2))

d = (log(S/H) + (b + (gamma - 1/2) * v^2) * T) / (v * T^0.5)

d2 = (log(I^2/(S*H)) + (b + (gamma - 1/2) * v^2) * T) / (v * T^0.5)

lambda = -r + gamma * b + 1/2 * gamma * (gamma - 1) * v^2

k = 2*b/v^2 + (2 * gamma - 1)

and the trigger price I is defined as

I1 = B0 + (B(+infi) - B0) * (1 - e^h1)

I2 = B0 + (B(+infi) - B0) * (1 - e^h2)

h1 = -(b*t1 + 2*v*t1^0.5) * (X^2 / ((B(+infi) - B0))*B0)

h2 = -(b*T + 2*v*T^0.5) * (X^2 / ((B(+infi) - B0))*B0)

t1 = 1/2 * (5^0.5 - 1) * T

B(+infi) = (B / (B - 1)) * X

B0 = max(X, (r / (r - b)) * X)

Moreover, the function psi(S, T, gamma, H, I2, I1, t1) is given by

psi(S, T, gamma, H, I2, I1, t1, r, b, v) = e^(lambda * T) * S^gamma * (M(-e1, -f1, rho) - (I2/S)^k * M(-e2, -f2, rho)

- (I1/S)^k * M(-e3, -f3, -rho) + (I1/I2)^k * M(-e4, -f4, -rho))

where (see screenshot for e and f values)

b=r options on non-dividend paying stock

b=r-q options on stock or index paying a dividend yield of q

b=0 options on futures

b=r-rf currency options (where rf is the rate in the second currency)

Inputs

S = Stock price.

K = Strike price of option.

T = Time to expiration in years.

r = Risk-free rate

c = Cost of Carry

V = Variance of the underlying asset price

cnd1(x) = Cumulative Normal Distribution

cbnd3(x) = Cumulative Bivariate Normal Distribution

nd(x) = Standard Normal Density Function

convertingToCCRate(r, cmp ) = Rate compounder

Numerical Greeks or Greeks by Finite Difference

Analytical Greeks are the standard approach to estimating Delta, Gamma etc... That is what we typically use when we can derive from closed form solutions. Normally, these are well-defined and available in text books. Previously, we relied on closed form solutions for the call or put formulae differentiated with respect to the Black Scholes parameters. When Greeks formulae are difficult to develop or tease out, we can alternatively employ numerical Greeks - sometimes referred to finite difference approximations. A key advantage of numerical Greeks relates to their estimation independent of deriving mathematical Greeks. This could be important when we examine American options where there may not technically exist an exact closed form solution that is straightforward to work with. (via VinegarHill FinanceLabs)

Things to know

Only works on the daily timeframe and for the current source price.

You can adjust the text size to fit the screen

Modified Bachelier Option Pricing Model w/ Num. Greeks [Loxx]Modified Bachelier Option Pricing Model w/ Num. Greeks is an adaptation of the Modified Bachelier Option Pricing Model in Pine Script. The following information is an except from Espen Gaarder Haug's book "Option Pricing Formulas".

Before Black Scholes Merton

The curious reader may be asking how people priced options before the BSM breakthrough was published in 1973. This section offers a quick overview of some of the most important precursors to the BSM model. As early as 1900, Louis Bachelier published his now famous work on option pricing. In contrast to Black, Scholes, and Merton, Bachelier assumed a normal distribution for the asset price—in other words, an arithmetic Brownian motion process:

dS = sigma * dz

Where S is the asset price and dz is a Wiener process. This implies a positive probability for observing a negative asset price—a feature that is not popular for stocks and any other asset with limited liability features.

The current call price is the expected price at expiration. This argument yields:

c = (S - X)*N(d1) + v * T^0.5 * n(d1)

and for a put option we get

p = (S - X)*N(-d1) + v * T^0.5 * n(d1)

where

d1 = (S - X) / (v * T^0.5)

Modified Bachelier Model

By using the arguments of BSM but now with arithmetic Brownian motion (normal distributed stock price), we can easily correct the Bachelier model to take into account the time value of money in a risk-neutral world. This yields:

c = S * N(d1) - Xe^-rT * N(d1) + v * T^0.5 * n(d1)

p = Xe^-rT * N(-d1) - S * N(-d1) + v * T^0.5 * n(d1)

d1 = (S - X) / (v * T^0.5)

Inputs

S = Stock price.

X = Strike price of option.

T = Time to expiration in years.

r = Risk-free rate

v = Volatility of the underlying asset price

cnd (x) = The cumulative normal distribution function

nd(x) = The standard normal density function

Numerical Greeks or Greeks by Finite Difference

Analytical Greeks are the standard approach to estimating Delta, Gamma etc... That is what we typically use when we can derive from closed form solutions. Normally, these are well-defined and available in text books. Previously, we relied on closed form solutions for the call or put formulae differentiated with respect to the Black Scholes parameters. When Greeks formulae are difficult to develop or tease out, we can alternatively employ numerical Greeks - sometimes referred to finite difference approximations. A key advantage of numerical Greeks relates to their estimation independent of deriving mathematical Greeks. This could be important when we examine American options where there may not technically exist an exact closed form solution that is straightforward to work with. (via VinegarHill FinanceLabs)

Things to know

Volatility for this model is price, so dollars or whatever currency you're using. Historical volatility is also reported in currency.

There is no dividend adjustment input

Only works on the daily timeframe and for the current source price.

CNS - Multi-Timeframe Bollinger Band OscillatorMy hope is to optimize the settings for this indicator and reintroduce it as a "strategy" with suggested position entry and exit points shown in the price pane.

I’ve been having good results setting the “Bollinger Band MA Length” in the Input tab to between 5 and 10. You can use the standard 20 period, but your results will not be as granular.

This indicator has proven very good at finding local tops and bottoms by combining data from multiple timeframes. Use BB timeframes that are lower than the timeframe you are viewing in your price pane.

The default settings work best on the weekly timeframe, but can be adjusted for most timeframes including intraday.

Be cognizant that the indicator, like other oscillators, does occasionally produce divergences at tops and bottoms.

Any feedback is appreciated.

Overview

This indicator is an oscillator that measures the normalized position of the price relative to Bollinger Bands across multiple timeframes. It takes the price's position within the Bollinger Bands (calculated on different timeframes) and averages those positions to create a single value that oscillates between 0 and 1. This value is then plotted as the oscillator, with reference lines and colored regions to help interpret the price's relative strength or weakness.

How It Works

Bollinger Band Calculation:

The indicator uses a custom function f_getBBPosition() to calculate the position of the price within Bollinger Bands for a given timeframe.

Price Position Normalization:

For each timeframe, the function normalizes the price's position between the upper and lower Bollinger Bands.

It calculates three positions based on the high, low, and close prices of the requested timeframe:

pos_high = (High - Lower Band) / (Upper Band - Lower Band)

pos_low = (Low - Lower Band) / (Upper Band - Lower Band)

pos_close = (Close - Lower Band) / (Upper Band - Lower Band)

If the upper band is not greater than the lower band or if the data is invalid (e.g., na), it defaults to 0.5 (the midline).

The average of these three positions (avg_pos) represents the normalized position for that timeframe, ranging from 0 (at the lower band) to 1 (at the upper band).

Multi-Timeframe Averaging:

The indicator fetches Bollinger Band data from four customizable timeframes (default: 30min, 60min, 240min, daily) using request.security() with lookahead=barmerge.lookahead_on to get the latest available data.

It calculates the normalized position (pos1, pos2, pos3, pos4) for each timeframe using f_getBBPosition().

These four positions are then averaged to produce the final avg_position:avg_position = (pos1 + pos2 + pos3 + pos4) / 4

This average is the oscillator value, which is plotted and typically oscillates between 0 and 1.

Moving Averages:

Two optional moving averages (MA1 and MA2) of the avg_position can be enabled, calculated using simple moving averages (ta.sma) with customizable lengths (default: 5 and 10).

These can be potentially used for MA crossover strategies.

What Is Being Averaged?

The oscillator (avg_position) is the average of the normalized price positions within the Bollinger Bands across the four selected timeframes. Specifically:It averages the avg_pos values (pos1, pos2, pos3, pos4) calculated for each timeframe.

Each avg_pos is itself an average of the normalized positions of the high, low, and close prices relative to the Bollinger Bands for that timeframe.

This multi-timeframe averaging smooths out short-term fluctuations and provides a broader perspective on the price's position within the volatility bands.

Interpretation

0.0 The price is at or below the lower Bollinger Band across all timeframes (indicating potential oversold conditions).

0.15: A customizable level (green band) which can be used for exiting short positions or entering long positions.

0.5: The midline, where the price is at the average of the Bollinger Bands (neutral zone).

0.85: A customizable level (orange band) which can be used for exiting long positions or entering short positions.

1.0: The price is at or above the upper Bollinger Band across all timeframes (indicating potential overbought conditions).

The colored regions and moving averages (if enabled) help identify trends or crossovers for trading signals.

Example

If the 30min timeframe shows the close at the upper band (position = 1.0), the 60min at the midline (position = 0.5), the 240min at the lower band (position = 0.0), and the daily at the upper band (position = 1.0), the avg_position would be:(1.0 + 0.5 + 0.0 + 1.0) / 4 = 0.625

This value (0.625) would plot in the orange region (between 0.85 and 0.5), suggesting the price is relatively strong but not at an extreme.

Notes

The use of lookahead=barmerge.lookahead_on ensures the indicator uses the latest available data, making it more real-time, though its effectiveness depends on the chart timeframe and TradingView's data feed.

The indicator’s sensitivity can be adjusted by changing bb_length ("Bollinger Band MA Length" in the Input tab), bb_mult ("Bollinger Band Standard Deviation," also in the Input tab), or the selected timeframes.

Multi-Timeframe Bollinger BandsMy hope is to optimize the settings for this indicator and reintroduce it as a "strategy" with suggested position entry and exit points shown in the price pane.

I’ve been having good results setting the “Bollinger Band MA Length” in the Input tab to between 5 and 10. You can use the standard 20 period, but your results will not be as granular.

This indicator has proven very good at finding local tops and bottoms by combining data from multiple timeframes. Use timeframes that are lower than the timeframe you are viewing in your price pane. Be cognizant that the indicator, like other oscillators, does occasionally produce divergences at tops and bottoms.

Any feedback is appreciated.

Overview

This indicator is an oscillator that measures the normalized position of the price relative to Bollinger Bands across multiple timeframes. It takes the price's position within the Bollinger Bands (calculated on different timeframes) and averages those positions to create a single value that oscillates between 0 and 1. This value is then plotted as the oscillator, with reference lines and colored regions to help interpret the price's relative strength or weakness.

How It Works

Bollinger Band Calculation:

The indicator uses a custom function f_getBBPosition() to calculate the position of the price within Bollinger Bands for a given timeframe.

Price Position Normalization:

For each timeframe, the function normalizes the price's position between the upper and lower Bollinger Bands.

It calculates three positions based on the high, low, and close prices of the requested timeframe:

pos_high = (High - Lower Band) / (Upper Band - Lower Band)

pos_low = (Low - Lower Band) / (Upper Band - Lower Band)

pos_close = (Close - Lower Band) / (Upper Band - Lower Band)

If the upper band is not greater than the lower band or if the data is invalid (e.g., na), it defaults to 0.5 (the midline).

The average of these three positions (avg_pos) represents the normalized position for that timeframe, ranging from 0 (at the lower band) to 1 (at the upper band).

Multi-Timeframe Averaging:

The indicator fetches Bollinger Band data from four customizable timeframes (default: 30min, 60min, 240min, daily) using request.security() with lookahead=barmerge.lookahead_on to get the latest available data.

It calculates the normalized position (pos1, pos2, pos3, pos4) for each timeframe using f_getBBPosition().

These four positions are then averaged to produce the final avg_position:avg_position = (pos1 + pos2 + pos3 + pos4) / 4

This average is the oscillator value, which is plotted and typically oscillates between 0 and 1.

Moving Averages:

Two optional moving averages (MA1 and MA2) of the avg_position can be enabled, calculated using simple moving averages (ta.sma) with customizable lengths (default: 5 and 10).

These can be potentially used for MA crossover strategies.

What Is Being Averaged?

The oscillator (avg_position) is the average of the normalized price positions within the Bollinger Bands across the four selected timeframes. Specifically:It averages the avg_pos values (pos1, pos2, pos3, pos4) calculated for each timeframe.

Each avg_pos is itself an average of the normalized positions of the high, low, and close prices relative to the Bollinger Bands for that timeframe.

This multi-timeframe averaging smooths out short-term fluctuations and provides a broader perspective on the price's position within the volatility bands.

Interpretation

0.0 The price is at or below the lower Bollinger Band across all timeframes (indicating potential oversold conditions).

0.15: A customizable level (green band) which can be used for exiting short positions or entering long positions.

0.5: The midline, where the price is at the average of the Bollinger Bands (neutral zone).

0.85: A customizable level (orange band) which can be used for exiting long positions or entering short positions.

1.0: The price is at or above the upper Bollinger Band across all timeframes (indicating potential overbought conditions).

The colored regions and moving averages (if enabled) help identify trends or crossovers for trading signals.

Example

If the 30min timeframe shows the close at the upper band (position = 1.0), the 60min at the midline (position = 0.5), the 240min at the lower band (position = 0.0), and the daily at the upper band (position = 1.0), the avg_position would be:(1.0 + 0.5 + 0.0 + 1.0) / 4 = 0.625

This value (0.625) would plot in the orange region (between 0.85 and 0.5), suggesting the price is relatively strong but not at an extreme.

Notes

The use of lookahead=barmerge.lookahead_on ensures the indicator uses the latest available data, making it more real-time, though its effectiveness depends on the chart timeframe and TradingView's data feed.

The indicator’s sensitivity can be adjusted by changing bb_length ("Bollinger Band MA Length" in the Input tab), bb_mult ("Bollinger Band Standard Deviation," also in the Input tab), or the selected timeframes.

Multi-Timeframe Bollinger Band PositionBeta version.

My hope is to optimize the settings for this indicator and reintroduce it as a "strategy" with suggested position entry and exit points shown in the price pane.

Any feedback is appreciated.

Overview

This indicator is an oscillator that measures the normalized position of the price relative to Bollinger Bands across multiple timeframes. It takes the price's position within the Bollinger Bands (calculated on different timeframes) and averages those positions to create a single value that oscillates between 0 and 1. This value is then plotted as the oscillator, with reference lines and colored regions to help interpret the price's relative strength or weakness.

How It Works

Bollinger Band Calculation:

The indicator uses a custom function f_getBBPosition() to calculate the position of the price within Bollinger Bands for a given timeframe.

Price Position Normalization:

For each timeframe, the function normalizes the price's position between the upper and lower Bollinger Bands.

It calculates three positions based on the high, low, and close prices of the requested timeframe:

pos_high = (High - Lower Band) / (Upper Band - Lower Band)

pos_low = (Low - Lower Band) / (Upper Band - Lower Band)

pos_close = (Close - Lower Band) / (Upper Band - Lower Band)

If the upper band is not greater than the lower band or if the data is invalid (e.g., na), it defaults to 0.5 (the midline).

The average of these three positions (avg_pos) represents the normalized position for that timeframe, ranging from 0 (at the lower band) to 1 (at the upper band).

Multi-Timeframe Averaging:

The indicator fetches Bollinger Band data from four customizable timeframes (default: 30min, 60min, 240min, daily) using request.security() with lookahead=barmerge.lookahead_on to get the latest available data.

It calculates the normalized position (pos1, pos2, pos3, pos4) for each timeframe using f_getBBPosition().

These four positions are then averaged to produce the final avg_position:avg_position = (pos1 + pos2 + pos3 + pos4) / 4

This average is the oscillator value, which is plotted and typically oscillates between 0 and 1.

Moving Averages:

Two optional moving averages (MA1 and MA2) of the avg_position can be enabled, calculated using simple moving averages (ta.sma) with customizable lengths (default: 5 and 10).

These can be potentially used for MA crossover strategies.

What Is Being Averaged?

The oscillator (avg_position) is the average of the normalized price positions within the Bollinger Bands across the four selected timeframes. Specifically:It averages the avg_pos values (pos1, pos2, pos3, pos4) calculated for each timeframe.

Each avg_pos is itself an average of the normalized positions of the high, low, and close prices relative to the Bollinger Bands for that timeframe.

This multi-timeframe averaging smooths out short-term fluctuations and provides a broader perspective on the price's position within the volatility bands.

Interpretation:

0.0 The price is at or below the lower Bollinger Band across all timeframes (indicating potential oversold conditions).

0.15: A customizable level (green band) which can be used for exiting short positions or entering long positions.

0.5: The midline, where the price is at the average of the Bollinger Bands (neutral zone).

0.85: A customizable level (orange band) which can be used for exiting long positions or entering short positions.

1.0: The price is at or above the upper Bollinger Band across all timeframes (indicating potential overbought conditions).

The colored regions and moving averages (if enabled) help identify trends or crossovers for trading signals.

Example:

If the 30min timeframe shows the close at the upper band (position = 1.0), the 60min at the midline (position = 0.5), the 240min at the lower band (position = 0.0), and the daily at the upper band (position = 1.0), the avg_position would be:(1.0 + 0.5 + 0.0 + 1.0) / 4 = 0.625

This value (0.625) would plot in the orange region (between 0.85 and 0.5), suggesting the price is relatively strong but not at an extreme.

Notes:

The use of lookahead=barmerge.lookahead_on ensures the indicator uses the latest available data, making it more real-time, though its effectiveness depends on the chart timeframe and TradingView's data feed.

The indicator’s sensitivity can be adjusted by changing bb_length ("Bollinger Band MA Length" in the Input tab), bb_mult ("Bollinger Band Standard Deviation," also in the Input tab), or the selected timeframes.

Active PMI Support/Resistance Levels [EdgeTerminal]The PMI Support & Resistance indicator revolutionizes traditional technical analysis by using Pointwise Mutual Information (PMI) - a statistical measure from information theory - to objectively identify support and resistance levels. Unlike conventional methods that rely on visual pattern recognition, this indicator provides mathematically rigorous, quantifiable evidence of price levels where significant market activity occurs.

- The Mathematical Foundation: Pointwise Mutual Information

Pointwise Mutual Information measures how much more likely two events are to occur together compared to if they were statistically independent. In our context:

Event A: Volume spikes occurring (high trading activity)

Event B: Price being at specific levels

The PMI formula calculates: PMI = log(P(A,B) / (P(A) × P(B)))

Where:

P(A,B) = Probability of volume spikes occurring at specific price levels

P(A) = Probability of volume spikes occurring anywhere

P(B) = Probability of price being at specific levels

High PMI scores indicate that volume spikes and certain price levels co-occur much more frequently than random chance would predict, revealing genuine support and resistance zones.

- Why PMI Outperforms Traditional Methods

Subjective interpretation: What one trader sees as significant, another might ignore

Confirmation bias: Tendency to see patterns that confirm existing beliefs

Inconsistent criteria: No standardized definition of "significant" volume or price action

Static analysis: Doesn't adapt to changing market conditions

No strength measurement: Can't quantify how "strong" a level truly is

PMI Advantages:

✅ Objective & Quantifiable: Mathematical proof of significance, not visual guesswork

✅ Statistical Rigor: Levels backed by information theory and probability

✅ Strength Scoring: PMI scores rank levels by statistical significance

✅ Adaptive: Automatically adjusts to different market volatility regimes

✅ Eliminates Bias: Computer-calculated, removing human interpretation errors

✅ Market Structure Aware: Reveals the underlying order flow concentrations

- How It Works

Data Processing Pipeline: