KillZones Hunt + Sessions [TradingFinder] Alert & Volume Ranges🟣 Introduction

🔵 Session

Financial markets are divided into various time segments, each with its own characteristics and activity levels. These segments are called sessions, and they are active at different times of the day.

The most important active sessions in financial markets are :

1. Asian Session

2. European Session

3. New York Session

The timing of these major sessions based on the UTC time zone is as follows :

1. Asian Session: 23:00 to 06:00

2. European Session: 07:00 to 16:30

3. New York Session: 13:00 to 22:00

Note

To avoid overlap between sessions and interference in kill zones, we have adjusted the session timings as follows :

• Asian Session: 23:00 to 06:00

• European Session: 07:00 to 14:25

• New York Session: 14:30 to 22:55

🔵 Kill Zones

Kill zones are parts of a session where trader activity is higher than usual. During these periods, trading volume increases and price fluctuations are more intense.

The timing of the major kill zones based on the UTC time zone is as follows :

• Asian Kill Zone: 23:00 to 03:55

• European Kill Zone: 07:00 to 09:55

• New York Morning Kill Zone: 14:30 to 16:55

• New York Evening Kill Zone: 19:30 to 20:55

This indicator focuses on tracking the kill zone and its range. For example, once a kill zone ends, the high and low formed during it remain unchanged.

If the price reaches the high or low of the kill zone while the session is still active, the corresponding line is not drawn any further. Based on this information, various strategies can be developed, and the most important ones are discussed below.

🟣 How to Use

There are three main ways to trade based on the kill zone :

• Kill Zone Hunt

• Breakout and Pullback to Kill Zone

• Trading in the Trend of the Kill Zone

🔵 Kill Zone Hunt

According to this strategy, once the kill zone ends and its high and low lines no longer change, if the price reaches one of these lines within the same session and is strongly rejected, a trade can be entered.

🔵 Breakout and Pullback to Kill Zone

According to this strategy, once the kill zone ends and its high and low lines no longer change, if the price breaks one of these lines strongly within the same session, a trade can be entered on the pullback to that level.

Trading in the Trend of the Kill Zone

We know that kill zones are areas where high-volume trading occurs and powerful trends form. Therefore, trades can be made in the direction of the trend. For example, when an upward trend dominates this area, you can enter a buy trade when the price reaches a demand order block.

🟣 Features

🔵 Alerts

You can set alerts to be notified when the price hits the high or low lines of the kill zone.

🔵 More Information

By enabling this feature, you can view information such as the time and trading volume within the kill zone. This allows you to compare the trading volume with the same period on the previous day or other kill zones.

🟣 Settings

Through the settings, you have access to the following options :

• Show or hide additional information

• Enable or disable alerts

• Show or hide sessions

• Show or hide kill zones

• Set preferred colors for displaying sessions

• Customize the time range of sessions

• Customize the time range of kill zones

스크립트에서 "价格在30元内股票"에 대해 찾기

KillZones & Sessions [TradingFinder] Volume | Asia, London & NY🔵 Introduction

🟣 Session

The forex market operates 24 hours a day, 5 days a week, with only Saturdays and Sundays being off; traders often focus on one of the forex trading sessions instead of trying to trade in all markets 24 hours a day.

Trading sessions are time intervals during which a specific financial market is active and trades are conducted. The Asia, London, and New York sessions are the most important trading sessions throughout the 24-hour period, during which a significant amount of money and liquidity enters the market.

🟣 Kill Zone

Traders in financial markets profit from the difference between the price at which they buy or sell and the current market price. Traders have different time horizons for trading.

Among these, some traders engage in daily or even hourly trading and must operate during times when the market has desirable trading volumes and significant price movements.

Kill zones are segments of a session with higher trading volumes and price fluctuations compared to the rest of the session.

🔵 How to Use

🟣 Session Time

The "Asia Session" consists of two sessions: "Sydney" and "Tokyo." The beginning of this session, according to the "UTC" time zone, is at 23:00 and ends at 06:00. Similarly, the beginning of the "Asia KillZone," according to the "UTC" time zone, is at 23:00, and it ends at 03:55.

The "London Session" consists of two sessions: "Frankfurt" and "London." The beginning of this session, according to the "UTC" time zone, is at 07:00, and it ends at 14:25. Similarly, the beginning of the "London KillZone," according to the "UTC" time zone, is at 07:00, and it ends at 09:55.

The beginning of the "New York am" session, according to the "UTC" time zone, is at 14:30, and it ends at 19:25. Similarly, the beginning of the "New York am KillZone," according to the "UTC" time zone, is at 14:30, and it ends at 16:55.

The beginning of the "New York pm" session, according to the "UTC" time zone, is at 19:30, and it ends at 22:55. Similarly, the beginning of the "New York pm KillZone," according to the "UTC" time zone, is at 19:30, and it ends at 20:55.

Important : To prevent session overlap, the working hours of each session have slightly changed.

🔵 Features

🟣 Simultaneous Session and Kill Zone

With this indicator, you can simultaneously view the kill zone and session. High and low lines are used to indicate sessions, while filled areas with color represent kill zones. If you do not want to see kill zones, you can turn off the display settings.

🟣 Candle, Time, and Volume

Using the "More Info" feature, you can see the number of candles, elapsed time, and traded volume within the colored filled area.

🔵 Settings

•Show More Info: To display "More Info," you need to turn on this feature and turn it off whenever you don't need it.

• You can also customize these settings for each session separately :

o Display or hide session.

o Choose session color.

o Set session time range.

o Display or hide kill zone.

o Set kill zone time range.

EMA Scalping StrategyEMA Slope Indicator Overview:

The indicator plots two exponential moving averages (EMAs) on the chart: a 9-period EMA and a 15-period EMA.

It visually represents the EMAs on the chart and highlights instances where the slope of each EMA exceeds a certain threshold (approximately 30 degrees).

Scalping Strategy:

Using the EMA Slope Indicator on a 5-minute timeframe for scalping can be effective, but it requires adjustments to account for the shorter time horizon.

Trend Identification: Look for instances where the 9-period EMA is above the 15-period EMA. This indicates an uptrend. Conversely, if the 9-period EMA is below the 15-period EMA, it suggests a downtrend.

Slope Analysis: Pay attention to the slope of each EMA. When the slope of both EMAs is steep (exceeds 30 degrees), it signals a strong trend. This can be a favorable condition for scalping as it suggests potential momentum.

Entry Points:

For Long (Buy) Positions: Consider entering a long position when both EMAs are sloping upwards strongly (exceeding 30 degrees) and the 9-period EMA is above the 15-period EMA. Look for entry points when price retraces to the EMAs or when there's a bullish candlestick pattern.

For Short (Sell) Positions: Look for opportunities to enter short positions when both EMAs are sloping downwards strongly (exceeding -30 degrees) and the 9-period EMA is below the 15-period EMA. Similar to long positions, consider entering on retracements or bearish candlestick patterns.

Exit Strategy: Use tight stop-loss orders to manage risk, and aim for small, quick profits. Since scalping involves short-term trading, consider exiting positions when the momentum starts to weaken or when the price reaches a predetermined profit target.

Risk Management:

Scalping involves high-frequency trading with smaller profit targets, so it's crucial to implement strict risk management practices. This includes setting stop-loss orders to limit potential losses and not risking more than a small percentage of your trading capital on each trade.

Backtesting and Optimization:

Before implementing the strategy in live trading, backtest it on historical data to assess its performance under various market conditions. You may also consider optimizing the strategy parameters (e.g., EMA lengths) to maximize its effectiveness.

Continuous Monitoring:

Keep a close eye on market conditions and adjust your strategy accordingly. Market dynamics can change rapidly, so adaptability is key to successful scalping.

NASDAQ 100 Peak Hours StrategyNASDAQ 100 Peak Hours Trading Strategy

Description

Our NASDAQ 100 Peak Hours Trading Strategy leverages a carefully designed algorithm to trade within specific hours of high market activity, particularly focusing on the first two hours of the trading session from 09:30 AM to 11:30 AM GMT-5. This period is identified for its increased volatility and liquidity, offering numerous trading opportunities.

The strategy incorporates a blend of technical indicators to identify entry and exit points for both long and short positions. These indicators include:

Exponential Moving Averages (EMAs) : A short-term 9-period EMA and a longer-term 21-period EMA to determine the market trend and momentum.

Relative Strength Index (RSI) : A 14-period RSI to gauge the market's momentum.

Average True Range (ATR) : A 14-period ATR to assess market volatility and to set dynamic stop losses and trailing stops.

Volume Weighted Average Price (VWAP) : To identify the market's average price weighted by volume, serving as a benchmark for the trading day.

Our strategy uniquely applies a volatility filter using the ATR, ensuring trades are only executed in conditions that favor our setup. Additionally, we consider the direction of the EMAs to confirm the market's trend before entering trades.

Originality and Usefulness

This strategy stands out by combining these indicators within the NASDAQ 100's peak hours, exploiting the specific market conditions that prevail during these times. The inclusion of a volatility filter and dynamic stop-loss mechanisms based on the ATR provides a robust method for managing risk.

By focusing on the early trading hours, the strategy aims to capture the initial market movements driven by overnight news and the opening rush, often characterized by higher volatility. This approach is particularly useful for traders looking to maximize gains from short-term fluctuations while limiting exposure to longer-term market uncertainty.

Strategy Results

To ensure the strategy's effectiveness and reliability, it has undergone rigorous backtesting over a significant dataset to produce a sample size of more than 100 trades. This testing phase helps in identifying the strategy's potential in various market conditions, its consistency, and its risk-to-reward ratio.

Our backtesting adheres to realistic trading conditions, accounting for slippage and commission to reflect actual trading scenarios accurately. The strategy is designed with a conservative approach to risk management, advising not to risk more than 5-10% of equity on a single trade. The default settings in the script align with these principles, ensuring that users can replicate our tested conditions.

Using the Strategy

The strategy is designed for simplicity and ease of use:

Trade Hours : Focuses on 09:30 AM to 11:30 AM GMT-5, during the NASDAQ 100's peak activity hours.

Entry Conditions : Trades are initiated based on the alignment of EMAs, RSI, VWAP, and the ATR's volatility filter within the designated time frame.

Exit Conditions : Includes dynamic trailing stops based on ATR, a predefined time exit strategy, and a trend reversal exit condition for risk management.

This script is a powerful tool for traders looking to leverage the NASDAQ 100's peak hours, providing a structured approach to navigating the early market hours with a robust set of criteria for making informed trading decisions.

Auto-magnifier / quantifytools- Overview

Auto-magnifier shows a lower timeframe view of candles and volume bars inside any main timeframe candle by zooming into it. Candles and volume bars as they develop are shown chronologically from left to right. By default, magnifier is triggered when less than 3 candles are visible on the chart.

By default, 20 lower timeframe candles are displayed by splitting main timeframe into 20 parts. The amount of candles displayed is a target rate, meaning the script will use a lower timeframe that has the closest match to 20 candles and therefore will vary a bit. Users can override automatic timeframe calculation and opt in to display any specific lower timeframe or adjust amount of candles shown (e.g. 20 -> 30 candles) per each main timeframe candle.

Example

Main timeframe set to 30 minute, candles displayed set to 20 -> Magnifying using 2 minute candles (30 minute/20 candles = 1.5 min, rounded to 2 min)

Main timeframe set to 30 minute, override set to 5 minutes -> Displaying 5 minute candles

Size of volume bars is calculated using relative volume (volume relative to volume SMA20), lowest bar representing relative volume values of under or equal to 1x the moving average and from there onwards progressively growing.

- Limitations and considerations

Amount of candles shown might flow over from the background on smaller screen sizes, in which case you would want to decrease the amount shown. Opposite is true for bigger screens, this value can be increased as more candles fit.

This indicator involves a lot of tricks with text elements to make it work automatically by zooming in. Size of wicks, bodies and volume bars are calculated by adding more text elements on big candles and less text elements on smaller candles. This means the displayed candles won't be a 100% match, but a rather a fair representation of the view, e.g. candle is green = lower timeframe candle is green, candle has a big wick = lower timeframe candle has a big wick (but not a 100% match).

Example

Magnified lower timeframe chart vs. Actual lower timeframe chart

Most mismatch will be found on the price levels where lower timeframe candles are shown, which is sacrificed for the sake of getting a better readability on the overall shape of lower timeframe price action. Users can alternatively optimize calculations for more accuracy, giving a better representation of the price levels where candles truly originated. This typically comes with the cost of worse readability however.

Example

Optimized for readability vs. Optimized for accuracy

- Visuals

All visual elements are fully customizable.

Sessions Lite [TradingFinder] New York, London, Asia, NYSE Forex🔵 Introduction

A trading session is one of the basic concepts in the financial market that refers to specific time periods. In fact, a session means hours during the day and night, during which traders in a certain part of the world conduct their transactions.

Although the "Forex" and "CFDs" market is open 24 hours a day and it is possible to trade in it, but in some hours the activity in this market decreases so much that many traders prefer not to trade and only watch the market. On the other hand, there are specific times when the market is very busy and dynamic, and many traders tend to trade during these hours of the day and night.

Trading sessions are usually divided into three main categories, which are "Asian", "European" and "North American" sessions. These trading sessions are also called the "Tokyo", "London" and "New York" sessions, respectively. But they also categorized these sessions in more detailed ways such as "Sydney session", "Shanghai session" or "NYSE session".

🔵 Tokyo trading session (Asian session)

After the weekend that happens on Saturday and Sunday, the Forex market starts with the Asian session. In this continent, most of the transactions are done in the Tokyo session, and for this reason, it is usually called the Asian session or the Tokyo session. However, other countries such as Australia, China and Singapore also do a lot of trading in this session.

The Tokyo session has a lower volume of transactions compared to the London and New York sessions, and therefore the liquidity is lower. In this session, most of the Forex currency pairs move in a price range. For this reason, different people use the ups and downs with the trading strategy in the range and get profit.

The low liquidity of the Tokyo session means that trading spreads are also higher during these hours. Besides, most of the transactions of this session are done in the early hours and at the same time as the planned news release.

In the Tokyo or Asia session, the best currency pairs to trade are the "Japanese yen", the "Australian dollar", and the "New Zealand dollar".

"Nikkei" index is also a good option for trading. If you trade in the Tokyo session, you should also be aware of the release of economic news and data from Australian, New Zealand and Japanese financial institutions.

🔵 London trading session (European session)

After the Asian session, it is time for the European session. In this period of time, transactions are very large and many European markets are involved. However, the European session is usually known as the London session.

Because of its specific time zone, London is not only known as the Forex trading center in Europe, but it is also known as the Forex trading center in the world. The London session overlaps with two other major trading sessions in the world, Asia and America. This means that most of the Forex transactions are done in this session. According to the latest statistics, 32% of Forex transactions are related to the London session, which shows that about a third of the activity performed in Forex takes place during this period.

This will increase the volume of Forex transactions and increase liquidity. An event that causes the spread of transactions to decrease. Of course, high liquidity also leads to greater volatility, which is desirable for many traders.

In the European session, the pound and euro currencies and the "DAX", "FTSE100", and "CAC40" indices are known as the best tradable assets. Also, traders of this session should pay attention to the news and data published by the "European Central Bank" and the "Bank of England". The news of countries like Germany, France and Italy are also very important.

🔵 American trading session (New York session)

When the New York session begins, several hours have passed since the end of the Tokyo session, but the European session is in the middle. In this session, they usually affect the financial activities carried out in America, but they also affect other countries such as Canada, Mexico and several South American countries.

The "US dollar" and stock indices such as "S&P", "Dow Jones" and "Nasdaq" are the most important assets that are traded in this session.

The early hours of the American session have a lot of liquidity and volatility due to the overlap with the European session, but with the end of the European session, the activity in the American session also decreases.

You can trade all major Forex currency pairs in the New York trading session. In this session, the "Federal Reserve", as the most important central bank in the world, is the institution that you should pay attention to its news and data.

The trading session indicator is an analytical tool in the financial markets that is used to display and analyze specific trading periods during a day. These indicators are generally useful for determining support and resistance levels during any trading session and for detecting different trading patterns.

For example, usually these indicators display the open and close price levels, the highest and lowest prices during a trading session. Also, you may notice various price patterns such as price channels, price phase phases and market trend changes during different trading sessions using these indicators.

🔵 cause of construction

In particular, the session light indicator version is designed and built for those traders who use many different tools on their chart at the same time. These traders can include "Volume Traders", "ICT traders", "Day Traders" and... These individuals can use "Session Lite" without disturbing the display of their other trading tools such as "Order Blocks", "Liquidity", "Zigzag", "FVG" etc.

But in general, there are several reasons for making tools like trading session indicators in financial markets, some of which include the following :

1. Analysis of specific time frames : Some traders and investors like to consider specific time frames for price analysis and review. For example, analyzing price changes during each trading session can help analyze trading patterns and identify trading opportunities.

2. Recognize different price patterns : Different price patterns may be observed during trading sessions. Trading session indicators can help to make better trading decisions by analyzing these patterns and their strengths and weaknesses.

3. Identifying Support and Resistance Levels : These tools may help to identify support and resistance levels during any trading session which can be helpful in deciding whether to enter or exit the market.

🔵 How to use

The Session Lite indicator displays 8 sessions by default. Asia session, Sydney session, Tokyo session, Shanghai session, Europe session, London session, New York session and New York Stock Exchange (NYSE) session are the sessions that are displayed.

You can activate or deactivate the display of each session by using the tick button next to the name of each session.

Two gray vertical dashes are also displayed by default, which indicate the beginning of the European session and the New York session. This feature is available for all sessions, but it is enabled by default only for these two sessions, and you can activate it for the rest of the session. You can enable or disable the display of this line by using the Start Session tick key.

Likewise, the information table is displayed by default, which includes the open or closed information of each session and the start and end times of each session. These timings are based on the UTC time zone.

Accordingly, the schedule of trading sessions is as follows :

Asia session from 23:00 to 06:00

Sydney session from 23:00 to 05:00

Tokyo session from 00:00 to 00:06

Shanghai session from 01:30 to 06:57

European session from 07:00 to 16:30

London session from 08:00 to 16:30

New York session from 13:00 to 22:00

New York Stock Exchange (NYSE) session from 14:30 to T 22:00

Important note : the beginning of the European session coincides with the opening of the Frankfurt market.

🔵 Settings

• In the settings section, there are customization capabilities according to the type of use of each user. The settings related to showing or not showing the box of each session, the start indicator of each session, setting the start and end time of the session and choosing the desired color to display each session are among the things that can be set from this section.

• At the end of the settings, you will see the "Info Table" option; By disabling this option, the "sessions" clock table displayed on the upper right side will be disabled.

Cycles 90mThe cycles are separated by vertical lines. The first cycle (Q1) is marked with a red line because it is a manipulative cycle where you should not open positions. Other cycles are green (Q2, Q3, Q4).

You can add the time of the current candle, its size and position on the chart in the settings

The time is highlighted in red in the timeframes 9:30-9:40, 10:00-10:10, 11:00-11:30, 15:30-15:40, 16:00-16:10, 17:00-17:10, 17:30-17:40, as price movements are most often expected during these timeframes.

The cycle lines automatically disappear if you open a timeframe above M15

VWAP, MFI, RSI with S/R StrategyBest for 0dte/intraday trading on AMEX:SPY with 1 minute chart

Strategy Concept

This strategy aims to identify potential reversal points in a price trend by combining momentum indicators (RSI and MFI), volume-weighted price (VWAP), and recent price action trends. It looks for conditions where the price is poised to change direction, either bouncing off a support level in a potential uptrend or falling from a resistance level in a potential downtrend.

By incorporating both price level analysis (support/resistance) and momentum indicators, the strategy seeks to increase the likelihood of identifying significant trend reversals, taking into consideration both recent price movements and the current price's position relative to historical highs and lows.

VWAP (Volume-Weighted Average Price)

VWAP acts as a benchmark to determine the general market trend. It's an average price weighted by volume.

A price above VWAP is often considered bullish, and a price below VWAP is seen as bearish.

MFI (Money Flow Index) and RSI (Relative Strength Index) Parameters

MFI is a volume-weighted RSI, used to identify overbought (above 70) or oversold (below 30) conditions.

RSI is a momentum indicator that measures the magnitude of recent price changes to identify overbought or oversold conditions, similar to MFI.

The script uses standard overbought (70) and oversold (30) thresholds for both MFI and RSI.

Trend Check Function

The function trendCheck analyzes the past pastBars candles to count how many were bullish (closing price higher than the opening price) and bearish.

This function is used to assess the recent trend direction.

Support and Resistance Detection

The script calculates the highest high (highestHigh) and lowest low (lowestLow) over the last lookbackSR (50) periods to identify potential support and resistance levels.

isNearSupport and isNearResistance are conditions to check if the current price is within 0.08% of these identified levels, indicating proximity to support or resistance.

Buy and Sell Logic

Buy Signal:

The RSI crosses over the oversold threshold (30).

The MFI is also below its oversold level (30).

The current price is above the VWAP.

The recent trend (past 20 bars) has been predominantly bearish.

The price is near the identified support level.

Sell Signal:

The RSI crosses under the overbought threshold (70).

The MFI is above its overbought level (70).

The current price is below the VWAP.

The recent trend has been predominantly bullish.

The price is near the identified resistance level.

Market Trend Indicator (FinnoVent)The Market Trend Indicator (FinnoVent) is a comprehensive trading tool designed to provide clear visual cues for market trends on TradingView charts. This indicator combines the principles of Exponential Moving Averages (EMAs), Bollinger Bands, the Average Directional Index (ADX), and the Relative Strength Index (RSI) to offer a nuanced view of market movements.

How It Works:

Trend Identification with EMAs: The indicator uses two EMAs (3-period and 30-period) to identify the primary trend. An upward trend is signaled when the 3-period EMA crosses above the 30-period EMA, while a downward trend is indicated when the 3-period EMA crosses below the 30-period EMA.

Sideways Market Detection: To identify sideways trends, the indicator employs Bollinger Bands, ADX, and RSI. A sideways (or consolidating) market condition is identified when:

The price is between the middle 60% of the Bollinger Bands (avoiding the top and bottom 20%).

The ADX is below 30, indicating a lack of a strong trend.

The RSI is between 40 and 60, suggesting a neutral market momentum.

Visual Representation:

Bar Colors: The indicator colors the price bars on the chart based on the identified trend:

Green Bars: Indicate an upward trend.

Red Bars: Indicate a downward trend.

Grey Bars: Indicate a sideways or consolidating market.

How to Use:

Trend Following: Use the colored bars as a guide for trend following. Green bars suggest a potential entry for a long position, while red bars may indicate opportunities for short positions.

Sideways Market Caution: Grey bars signal a sideways market. In such conditions, traders might exercise caution and avoid trend-following strategies, as the market lacks a clear direction.

Complementary Analysis: While the Market Trend Indicator (FinnoVent) provides valuable insights, it's recommended to use it in conjunction with other forms of analysis (like fundamental analysis, other technical indicators, or price action) for comprehensive decision-making.

Suitable for: This indicator is versatile and can be applied to various timeframes and trading instruments, including stocks, forex, commodities, and indices.

Important Notes:

The indicator is designed to minimize repainting but always consider the latest data for the most accurate analysis.

Like all indicators, it is not foolproof. It works best when combined with a solid trading plan and risk management strategies.

Machine Learning: MFI Heat Map [YinYangAlgorithms]Overview:

MFI Heat Maps are a visually appealing way to display the values of 29 different MFIs at the same time while being able to make sense of it. Each plot within the Indicator represents a different MFI value. The higher you get up, the longer the length that was used for this MFI. This Indicator also features the use of Machine Learning to help balance the MFI levels. It doesn’t solely rely upon Machine Learning but instead incorporates a growing length MFI averaged with the Machine Learning MFI at any given index.

For instance, say we are calculating the 10th plot from the bottom, the MFI would be an average of:

MFI(source, 11)

Machine Learning MFI at Index of 10

We do it this way as they both help smooth each other out without relying solely on just one calculation method.

Due to plot limitations, you are capped at 28 Plot Amounts within this indicator, but that is still quite a bit of information you can glean from a Heat Map.

The Machine Learning used in this indicator is of the K-Nearest Neighbor (KNN). It uses a Fast and Slow MFI calculation then sorts through them over Machine Learning Length and calculates the differences between them. It then slices off KNN length to create our Max/Min Distances allotted. It adds the average between Fast and Slow MFIs to a Viable Distances array if their distances are within the KNN Min/Max distance. It then averages all distances in the Viable Distances array and returns the result.

The result of the KNN Function is saved to another ML Data array whose length is that of Plot Amount (Heat Map Size). This way each Index of the ML Data array can be indexed according to the Heat Map Size.

The Average of the ML Data array is the MFI line (white) that you’ll see plotted on the Indicator. There is also the SMA of the MFI Average (orange) which is likewise plotted. These plots allow you to visualize where the ML MFI is sitting and can potentially be useful for seeing when the MFI Average and SMA cross over and under each other.

We’ve heard many people talk highly of RSI, but sadly not too many even refer to MFI. MFI oftentimes may be overlooked, especially with new traders who may not even know what it is. Essentially MFI is an RSI but it also incorporates Volume into its calculations, which in our opinion leads to a more accurate reading; afterall, what is price movement without Volume.

Tutorial:

You may be thinking, this Indicator looks appealing to the eye, but how do I benefit from it trading wise?

Before we get into our visual examples, let's talk briefly about what makes Heat Maps in general a useful tool for trading. Heat Maps give us the ability to visualize and understand lots of data while removing the clutter. We can understand the data of 29 different MFIs without having to look at and decipher 29 different MFI plots. When you overlay too many MFI lines on top of each other, they can be very difficult to read and oftentimes end up actually hindering your Technical Analysis. For this reason, we have a simple solution to this problem; Heat Maps. This MFI Heat Map allows you to easily know (in a relative %) what the MFI level is for varying lengths. For Instance, the First (bottom) plot indexes an MFI of (K(0) (loop of Plot Amount) + Smoothing Length (default 1)) = 1. Since this is indexing (usually) a very low length, it will change much quicker. Whereas the Last (top) plot indexes an MFI of (K(27) (loop of Plot Amount) + Smoothing Length (default 1)) = 28. This is indexing a much higher length of MFI which results in the MFI the higher you go up in the Heat Map to move much slower.

Heat Maps give us the ability to see changes happening over multiple MFIs at the same time, which can be very useful for seeing shifts in MFI / Momentum. Remember, MFI incorporates Volume, so even if the price goes up a lot, if there was low volume, the MFI won’t move as much as an RSI would. However, likewise, if there is high volume but low price movement, the MFI will move slightly more than the RSI.

Heat Maps change color based on their MFI level. If the MFI is >= 90 it is HOT (red), if the MFI <= 9 it is COLD (teal, think of ICE). Green represents an MFI of 50-59 and Dark Blue represents an MFI of 40-49. Green and Dark blue are the most common colors as all the others are more ‘Extreme’ MFI levels.

Okay, time to get to the Examples :

Since there is so much going on in Heat Maps, we’ve decided to focus this tutorial to this specific area and talk about individual locations before talking about it as a whole.

If you refer to the example above where there are 2 white circles; these white circles are highlighting a key location you’ll be wanting to identify within your Heat Maps, many things are happening here:

The MFI crossed over the SMA (bullish).

The Heat Map started changing from mid/dark Blue (30-50 MFI) to Green (50-59 MFI) around the midline (the 50% dashed like).

The Lower levels of the Heat Map are turning Yellow/Orange/Red (60-100 MFI).

The Upper Levels of the Heat Map are still Light Blue - Green (10-50 MFI).

The 4 Key points above, all point towards potential Bullish Momentum changes. You’re likely wondering, but why? Let's discuss about each one in more specific detail:

1. The MFI crossed over the SMA (bullish): What this tells us is that the current MFI Average is now greater than its average over the last (default) 16 bars. This means there's been a large amount of Money Flow (Price and Volume) recently (subjectively based on the last (default) 16 average). This is one of the leading Bullish / Bearish signals you will see within this Indicator. You can enable Signals within the Settings and/or even add Alerts for when these crossings occur.

2. The Heat Map started changing from mid/dark Blue (30-50 MFI) to Green (50-59 MFI) around the midline (the 50% dashed like): This shows us that the index’s in the mid (if using all 28 heat map plots it would be at 14) has already received some of this momentum change. If you look at the second white circle (right), you’ll also notice the higher MFI plot indexes are also green. This is because since their length is long they still have some momentum and strength from the first white circle (left). Just because the first white circle failed in its bullish push, doesn’t mean it didn’t achieve momentum that would later on help to push the price up.

3. The Lower levels of the Heat Map are turning Yellow/Orange/Red (60-100 MFI): It occurred somewhat in the left white circle, but mainly in the right white circle. This shows us the MFI is very high on the lower lengths, this may lead to the current, middle and higher length MFIs following suit soon. Remember it has to work its way up, the higher levels can’t go red unless the lower levels go red first and the higher levels can also lag quite a bit behind and take awhile to catch up, this is normal, expected and meant to happen. Vice versa is also true with getting higher levels to go cold (light teal (think of ICE)).

4. The Upper Levels of the Heat Map are still Light Blue - Green (10-50 MFI): You might think at first that this is a bad thing, but it's not! Remember you want to be Fearful when others are Greedy and Greedy when others are Fearful! You don’t want to buy when the higher levels have a high MFI, you want to buy when you see the momentum pushing up in the lower MFI levels (getting yellow/orange/red in the low levels) while it is still Cold in the higher levels (BLUE OR GREEN, nothing higher than green as it is already slightly too high). There will be many times that it is Yellow or possibly Orange in the high levels and the bullish push still happens, but this is much more risky! The key to trading is to minimize risks while maximizing potential.

Hopefully now you’re getting an idea of how to spot potential bullish momentum changes, but what about bearish momentum changes? Technically they are the exact opposite, so we don’t need to go into as much detail, but lets still take a look at a few examples:

In the example above we marked the 3 times where it was displaying overly bullish characteristics. We marked the bullish momentum occurring with arrows. If you look closely at the start of the arrow to where it finishes, you’ll notice how the heat (HOT)(RED) works its way up from the lower levels to the higher levels. We then see the MFI to SMA cross under. In all 3 of these examples the heat made it all the way to the top of the chart. These are all very bearish signals that represent a bearish momentum movement that may occur soon.

Also, please note, the level the MFI is at DOES matter! That line isn’t there simply for you to see when there are crosses over and under. The MFI is considered to be Overbought when it is greater than 70 (the upper white dashed line, it is just formatted to be on a different scale cause there are 28 plots, but it represents 70). The MFI is considered to be Oversold when it is less than 30 (the lower white dashed line).

If we look to the left a little here where a big drop in price occurred shortly after our MFI and SMA crossed, would we have been able to identify it using the Heat Maps? Likely, No. There was some color change in the lower levels a few bars prior that went yellow/orange/red but before this cross happened they all went back to Dark Blue. In the middle section when the cross happened it was only Green and Yellow and in the upper section we are Blue. This would be a very risky trade to go on as the only real Bearish Indication was the MFI to SMA cross under. Remember, you want to reduce risk, you don’t want to simply trade on everytime the MFI and SMA cross each other or you’ll be getting yourself into many risky trades based on false signals.

Based on what you’ve learned above, can you see the signs that are indicating where this white circle may have potential for a bullish momentum change?

Now that we are more zoomed in, you may also be noticing there are colors to the price bars. This can be disabled in the settings, but just so you know what they mean, let’s zoom in a little more and talk about it.

We’ve condensed the Indicator a bit so you can see the bars better here. The colors that are displayed on these bars are the Heat Map value for your MFI (the white line in the Indicator). This way you can better see when the Price is Hot and Cold. As you may see while looking, the colors generally go from cold to hot when bullish momentum is happening and hot to cold when bearish momentum is happening. We don’t recommend solely looking at the bars as indicators to MFI momentum change, as seeing the Heat Map will give you much more data; however it can be nice to see the Heat Map projected on the bars rather than trying to eyeball it yourself or hover over each bar specifically to see their levels.

We will conclude our Tutorial here. Hopefully this has given you some insight to how useful Heat Maps can be and why it works well with a Machine Learning (KNN) Model applied to the MFI.

PLEASE NOTE: You can adjust the line width for the Heat Map within the settings. If you condense the Indicator a lot or have a small screen, likely use a length of 1-2. If you have it stretched out or a large screen, a length of 2-3 will work nice. You just don’t want to have the lines overlapping or it defeats the purpose of a Heat Map. Also, the bigger the linewidth, generally you’ll want to increase the Transparency within the Settings also as it can get quite bright and hurt your eyes over time.

Settings:

MFI:

Show MFI and SMA Crossing Signals: MFI and SMA Crossing is one of the leading Bullish and Bearish Signals in this Indicator. You can also add alerts for these signals.

Plot Amount: How many plots are used in this Heat Map. (2 - 28).

Source: The Source to use in all MFI calculations.

Smooth Initial MFI Length: How much to smooth the Fast and Slow MFI calculation by. 1 = No smoothing.

MFI SMA Length: What length we smooth the MFI Average over to get our MFI SMA.

Machine Learning:

Average MFI data by adding a lookback to the Source: While populating our Heat Map with the MFI's, should use use the Source each MFI Length increase or should we also lookback a Source each MFI Length Increase.

KNN Distance Requirement: To be a valid KNN, it needs to abide by a Distance calculation. Generally only Max is used, but you can change it if it suits your trading style better.

Machine Learning Length: How much ML data should we store? The longer the length generally the smoother the result; which may not be as accurate for something like a Heat Map, so keeping this relatively low may lead to more accurate results.

KNN Length: How many KNN are used in the slice to calculate max/min distance allowed.

Fast Length: Fast MFI length used in KNN to calculate distances by comparing its distance with the Slow MFI Length.

Slow Length: Slow MFI length used in KNN to calculate distances by comparing its distance with the Fast MFI Length.

Smoothing Length: When populating our Heat Map, at what length do we start our MFI calculations with (A Higher value with result in a slower and more smoothed MFI / Heat Map).

Colors:

Change Bar Color: Change bar colors to MFI Avg Color.

Heat Map Transparency: If there isn't any transparency it can be a little hard on the eyes. The Greater the Line Width, generally the more transparency you'll want for your eyes.

Line Width: Set how wide the Heat Map lines are

MFI 90-100 Color: Color when the MFI is between these levels.

MFI 80-89 Color: Color when the MFI is between these levels.

MFI 70-79 Color: Color when the MFI is between these levels.

MFI 60-69 Color: Color when the MFI is between these levels.

MFI 50-59 Color: Color when the MFI is between these levels.

MFI 40-49 Color: Color when the MFI is between these levels.

MFI 30-39 Color: Color when the MFI is between these levels.

MFI 20-29 Color: Color when the MFI is between these levels.

MFI 10-19 Color: Color when the MFI is between these levels.

MFI 0-100 Color: Color when the MFI is between these levels.

If you have any questions, comments, ideas or concerns please don't hesitate to contact us.

HAPPY TRADING!

Machine Learning: Support and Resistance [YinYangAlgorithms]Overview:

Support and Resistance is normally based upon Pivot Points and Highest Highs and Lowest Lows. Many times coders even incorporate Volume, RSI and other factors into the equation. However there may be a downside to doing a pure technical approach based on historical levels. We live in a time where Machine Learning is becoming more and more used; thus we have decided to create a Machine Learning Support and Resistance Projection based Indicator. Rather than using traditional Support and Resistance calculations using historical data, we have taken a rather different approach. This Indicator instead attempts to Predict and Project where Support and Resistance locations will be based on a Machine Learning Model using a form of KNN (k-Nearest Neighbors).

Since this indicator creates a Projection of where it deems Support and Resistance will be, it has the ability to move its Support and Resistance before the price even gets to it if it believes it will surpass its projections. This may create a more accurate placement of Support and Resistance as they’re not based on historical levels.

This Indicator does not Repaint.

How it works:

This Indicator makes its projections based on the source you provide (by default close) of the previous bar and submits the source, RSI and EMA to our Projection Function to get its projection of the current bar.

The Projection function essentially calculates potential movement after finding the differences between the source the MA from the current bar, previous bar and average over the span of Machine Learning Length.

Potential movement is defined as:

Average Difference + Average(Machine Learning Average, Average Last Distance)

Average Difference: (Absolute value of Current Source - Current MA) - (Absolute value of Machine Learning Average - Machine Learning MA)

Average Last Distance: Average(Current Source - Current MA, Previous Source - Previous MA)

It then predicts the next bars directional movement (bullish or bearish bar) using several factors:

Previous Source > Previous MA

Current Source - Current MA > Average Source - Average MA

Current RSI > Previous RSI

Current RSI > 30 and Previous RSI <= 30

Current RSI < 70 and Previous RSI >= 70

This helps us to predict the direction the next bar may move.

We then calculate a multiplier that we apply to our Potential Movement value to get our final result which is our Current Bars Close Projection.

Our multiplier is calculated using:

(Current RSI > 30 and Previous RSI <= 30) OR (Current RSI < 70 and Previous RSI >= 70)

Current Source - Current MA > Previous Source - Previous MA

We then create an array and fill it with the previous X projections (Machine Learning Length) and send it to another function. This function, if told to, will sort the data accordingly and then output the KNN average of the length given.

We calculate and plot various KNN lengths to create different Zones:

Strong Support: Length of 2 but sort the data Ascending (low to high)

Strong Resistance: Length of 2 but sort the data Descending (high to low)

Support: Length of Machine Length Length / 10 or Min of 2 sorted by Ascending

Resistance: Length of Machine Length Length / 10 or Min of 2 sorted by Descending

There are also 4 other plots you may be wondering what they are, there is your AVG, VWMA, Long Term Memory and Current Projection.

By default your Current Projection is disabled in settings but you can enable it if you are curious to see how the projections for each close are calculated. It is, however, not a crucial point of interest (white line).

The average is simply the average value of the Machine Learning Data (purple line).

The VWMA is a VWMA calculation applied to our Data over a length specified in settings (by default 1)(blue line). The VWMA is crucial when combined with the Avg as they can cross over and under each other. These crosses represent potential Bullish and Bearish zones.

Lastly, but certainly not least, we have the Long Term Memory (maroon line). The Long Term Memory can be displayed either as an ‘Average’, ‘Hard Line’ or ‘None’. The Long Term Average is only updated every Machine Learning Length Bar Index’s and is populated with the average of the Machine Learning Data. For Instance, if Machine Learning Length is set to 100, the Long Term Memory is only updated every 100 bars, and since its length is the same as the Machine Learning Length, that means its data is composed of 10,000 bars worth of data. The Long Term Memory may be very beneficial for determining where Support and Resistance lie over the Long Term within a Machine Learning Algorithm. When set to ‘Average’ it plots the connection lines diagonally, and although they may be more visually appealing, they’re less useful when it comes to actually seeing support and resistance as generally speaking, support and resistance lie on the horizontal. When set to ‘Hard Line’ the Long Term Memory is connected with hard lines and holds the price value until the next time it is updated. This makes it much more useful for potentially identifying Support and Resistance.

Tutorial:

Here is an overview of what the Indicator looks like, now let's start to dissect it.

In the example above we can see how all of the lines between the Major Support and Resistance zones may act as BOTH Support and Resistance depending on which side the price is currently on. In the circle on the left, we can see how it can fluctuate between the two. If you look at the circle on the right, we can see how the Average line acts as a strong support before it fails to maintain it. Generally speaking, most Support and Resistance locations may potentially fail to hold after 3 tests, as the Average did in this example.

As you can see, the Support and Resistance doesn’t wait to be tested before adjusting, which is why there are 2 lines which create their zones. The inner line is the Support/Resistance and the outer line is the Strong Support/Resistance. The Yellow Circle shows the inner line was able to calculate the moving resistance correctly and then adjusted accordingly as it was projecting the price to keep increasing. However, if you look at the White Circle, you can see that since there was first a crash, and then parabolic movement, that the inner zone could not move and predict the resistance as well as the outer zone could.

We consider the price to be ‘Overvalued’ when it is above the VWMA (blue line) and ‘Undervalued’ when it is below the VWMA. It is considered ‘fair’ price when it is within the VWMA to Average zone (between the blue and purple lines). If you look at the example above, you’ll notice where the two yellow circles are, it is not only considered ‘Overvalued’, but it then proceeds to ride the inner resistance line upwards. This is common when the market is overly bullish and vice versa when it is bearish. Please keep in mind, although it is common, it doesn’t mean a correction can’t happen.

In this example above we look at the last bull run that may have started due to the halving. This bull run was very bullish as you can see in the example above. The price was constantly sitting within the Resistance Zone and the VWMA that was very close to it was constantly acting as a Support. Naturally, due to the Algorithm used in this Indicator, as the momentum starts to slow down, the VWMA (blue line) will start to space out more and more from the Resistance Zone. This doesn’t mean the momentum is gone, it just means it may be slowing down.

Unfortunately we have to study the Bear Market with a different perspective than the Bull Market. However, there are still some similarities within the two. If you refer to the example above and the previous example, you can clearly see that the Bull Market loves to stay with the Resistance Zone and use the VWMA as a Support. However, the Bear Market does not. This is a normal occurrence, however we can see from the example above you may see a correction / horizontal movement when the Outer Support Line is touched. If you look at all 3 yellow circles, the Outer Support Line was touched, then either a small correction or horizontal consolidation occurred.

We will conclude our Tutorial here, hopefully you’ll be able to benefit from a moving Support and Resistance calculated with Machine Learning that projects its locations, rather than using traditional calculations.

Settings:

Source: This source is the base for all our calculations

Machine Learning Length: How much projection data are we storing and using to make calculations.

Smoothing Length: We need to smooth calculations such as RSI, EMA and VWMA. What length are we smoothing it with?

VWMA ML Projection Length: How far into our Machine Learning data should we average for our VWMA. Please note the 'Smoothing Length' is still applied here after getting the Projection Average.

Long Term Memory: Long term memory has the same storage length but is only updated once per Machine Learning Length. For instance, if Machine Learning Length is 100, it will save the Average of our data once every 100 bars. This means its memory is an average of 10,000 bars of Machine Learning. 'Average' connects its values diagonally whereas 'Hard Line' holds its value until it changes.

Use Average Last Distance In Potential Movement: This can help accuracy but generally also displaces the Support and Resistance by projecting it further.

Show Current Projection: Projections occur for each bar, and our Machine Learning utilizes these projections by storing and evaluating them. This toggle will display the Current Projection Line which is used to create all our Projections.

If you have any questions, comments, ideas or concerns please don't hesitate to contact us.

HAPPY TRADING!

Nadaraya-Watson Envelope: Modified by YosietRange Filter indicator based on the LuxAlgo Nadaraya-Watson Envelope () indicator adding the SMA 30 high and SMA 7 low to predict the changes of the trends lines price.

WARNING: This indicator, as the same as the original, repaints the chart and could affect the exact values of the prices.

SMA Low 7 was identified using tensorflowJS years ago as accurate and abstract rsi indicator

SMA High 30 was identified using tensorflowJS years ago as accurate and strong trend line

This two SMAs were added to the original indicator Nadaraya-Watson to predict the exact points where the price will change direction or will re-test the trend to continue on.

The signals will act as the Williams Fractals, replacing the original signals of the indicator.

For those ICT/SMC traders, the bands and SMAs can toggle off in the settings of this indicator.

SETTINGS

Can set the source of the UPPER band indivuadilly

Can set the source of the LOWER band indivuadilly

Can toggle the visibility of the bands, this will not affect the calculations

Can toggle the visibility of SMAs

ALERTS AND SIGNALS

When the SMA LOW 7 cross under or over the bands, will trigger a signal orange

When the SMA 30 High cross over the upper band, will trigger a short signal purpple

HOW TO USE IT

If the both signals appears (sma 7 low and sma 30 high) crossing the upper band at the same point, this means that the price will drop strongly.

If the sma 7 low cross signal (orange triangle) appears under the price and lower band, means that the price will go up.

The separation of the signals from the chart will suggest the force of the movement. While more distance be, strongest reaction of the price.

DISCLAIMER : This indicator or script does not imply or constitute financial advice, investment advice, trading advice or any other type of advice or recommendation by and for TradingView. Use it at your own risk and your own decision.

Multi-Timeframe Trend Detector [Alifer]Here is an easy-to-use and customizable multi-timeframe visual trend indicator.

The indicator combines Exponential Moving Averages (EMA), Moving Average Convergence Divergence (MACD), and Relative Strength Index (RSI) to determine the trend direction on various timeframes: 15 minutes (15M), 30 minutes (30M), 1 hour (1H), 4 hours (4H), 1 day (1D), and 1 week (1W).

EMA Trend : The script calculates two EMAs for each timeframe: a fast EMA and a slow EMA. If the fast EMA is greater than the slow EMA, the trend is considered Bullish; if the fast EMA is less than the slow EMA, the trend is considered Bearish.

MACD Trend : The script calculates the MACD line and the signal line for each timeframe. If the MACD line is above the signal line, the trend is considered Bullish; if the MACD line is below the signal line, the trend is considered Bearish.

RSI Trend : The script calculates the RSI for each timeframe. If the RSI value is above a specified Bullish level, the trend is considered Bullish; if the RSI value is below a specified Bearish level, the trend is considered Bearish. If the RSI value is between the Bullish and Bearish levels, the trend is Neutral, and no arrow is displayed.

Dashboard Display :

The indicator prints arrows on the dashboard to represent Bullish (▲ Green) or Bearish (▼ Red) trends for each timeframe.

You can easily adapt the Dashboard colors (Inputs > Theme) for visibility depending on whether you're using a Light or Dark theme for TradingView.

Usage :

You can adjust the indicator's settings such as theme (Dark or Light), EMA periods, MACD parameters, RSI period, and Bullish/Bearish levels to adapt it to your specific trading strategies and preferences.

Disclaimer :

This indicator is designed to quickly help you identify the trend direction on multiple timeframes and potentially make more informed trading decisions.

You should consider it as an extra tool to complement your strategy, but you should not solely rely on it for making trading decisions.

Always perform your own analysis and risk management before executing trades.

The indicator will only show a Dashboard. The EMAs, RSI and MACD you see on the chart image have been added just to demonstrate how the script works.

DETAILED SCRIPT EXPLANATION

INPUTS:

theme : Allows selecting the color theme (options: "Dark" or "Light").

emaFastPeriod : The period for the fast EMA.

emaSlowPeriod : The period for the slow EMA.

macdFastLength : The fast length for MACD calculation.

macdSlowLength : The slow length for MACD calculation.

macdSignalLength : The signal length for MACD calculation.

rsiPeriod : The period for RSI calculation.

rsiBullishLevel : The level used to determine Bullish RSI condition, when RSI is above this value. It should always be higher than rsiBearishLevel.

rsiBearishLevel : The level used to determine Bearish RSI condition, when RSI is below this value. It should always be lower than rsiBullishLevel.

CALCULATIONS:

The script calculates EMAs on multiple timeframes (15-minute, 30-minute, 1-hour, 4-hour, daily, and weekly) using the request.security() function.

Similarly, the script calculates MACD values ( macdLine , signalLine ) on the same multiple timeframes using the request.security() function along with the ta.macd() function.

RSI values are also calculated for each timeframe using the request.security() function along with the ta.rsi() function.

The script then determines the EMA trends for each timeframe by comparing the fast and slow EMAs using simple boolean expressions.

Similarly, it determines the MACD trends for each timeframe by comparing the MACD line with the signal line.

Lastly, it determines the RSI trends for each timeframe by comparing the RSI values with the Bullish and Bearish RSI levels.

PLOTTING AND DASHBOARD:

Color codes are defined based on the EMA, MACD, and RSI trends for each timeframe. Green for Bullish, Red for Bearish.

A dashboard is created using the table.new() function, displaying the trend information for each timeframe with arrows representing Bullish or Bearish conditions.

The dashboard will appear in the top-right corner of the chart, showing the Bullish and Bearish trends for each timeframe (15M, 30M, 1H, 4H, 1D, and 1W) based on EMA, MACD, and RSI analysis. Green arrows represent Bullish trends, red arrows represent Bearish trends, and no arrows indicate Neutral conditions.

INFO ON USED INDICATORS:

1 — EXPONENTIAL MOVING AVERAGE (EMA)

The Exponential Moving Average (EMA) is a type of moving average (MA) that places a greater weight and significance on the most recent data points.

The EMA is calculated by taking the average of the true range over a specified period. The true range is the greatest of the following:

The difference between the current high and the current low.

The difference between the previous close and the current high.

The difference between the previous close and the current low.

The EMA can be used by traders to produce buy and sell signals based on crossovers and divergences from the historical average. Traders often use several different EMA lengths, such as 10-day, 50-day, and 200-day moving averages.

The formula for calculating EMA is as follows:

Compute the Simple Moving Average (SMA).

Calculate the multiplier for weighting the EMA.

Calculate the current EMA using the following formula:

EMA = Closing price x multiplier + EMA (previous day) x (1-multiplier)

2 — MOVING AVERAGE CONVERGENCE DIVERGENCE (MACD)

The Moving Average Convergence Divergence (MACD) is a popular trend-following momentum indicator used in technical analysis. It helps traders identify changes in the strength, direction, momentum, and duration of a trend in a financial instrument's price.

The MACD is calculated by subtracting a longer-term Exponential Moving Average (EMA) from a shorter-term EMA. The most commonly used time periods for the MACD are 26 periods for the longer EMA and 12 periods for the shorter EMA. The difference between the two EMAs creates the main MACD line.

Additionally, a Signal Line (usually a 9-period EMA) is computed, representing a smoothed version of the MACD line. Traders watch for crossovers between the MACD line and the Signal Line, which can generate buy and sell signals. When the MACD line crosses above the Signal Line, it generates a bullish signal, indicating a potential uptrend. Conversely, when the MACD line crosses below the Signal Line, it generates a bearish signal, indicating a potential downtrend.

In addition to the MACD line and Signal Line crossovers, traders often look for divergences between the MACD and the price chart. Divergence occurs when the MACD is moving in the opposite direction of the price, which can suggest a potential trend reversal.

3 — RELATIVE STRENGHT INDEX (RSI):

The Relative Strength Index (RSI) is another popular momentum oscillator used by traders to assess the overbought or oversold conditions of a financial instrument. The RSI ranges from 0 to 100 and measures the speed and change of price movements.

The RSI is calculated based on the average gain and average loss over a specified period, commonly 14 periods. The formula involves several steps:

Calculate the average gain over the specified period.

Calculate the average loss over the specified period.

Calculate the relative strength (RS) by dividing the average gain by the average loss.

Calculate the RSI using the following formula: RSI = 100 - (100 / (1 + RS))

The RSI oscillates between 0 and 100, where readings above 70 are considered overbought, suggesting that the price may have risen too far and could be due for a correction. Readings below 30 are considered oversold, suggesting that the price may have dropped too much and could be due for a rebound.

Traders often use the RSI to identify potential trend reversals. For example, when the RSI crosses above 30 from below, it may indicate the start of an uptrend, and when it crosses below 70 from above, it may indicate the start of a downtrend. Additionally, traders may look for bullish or bearish divergences between the RSI and the price chart, similar to the MACD analysis, to spot potential trend changes.

Swing Action PriceEnglish:

**Description of "Swing Action Price" TradingView Script**

"Swing Action Price" is a custom technical indicator designed to identify swing highs and swing lows in a financial market. The script calculates and plots various lines on the chart to visualize these swing points. Swing highs are points where the price has made a local peak, while swing lows are points where the price has made a local trough.

The indicator displays the following lines on the chart:

1. Dotted lines representing each individual swing high and swing low identified on different timeframes (10, 30, 60, 100, 150, 200, 700, and 1000 bars).

2. Dotted lines representing the most recent swing high and swing low for the current bar.

How the indicator works:

1. The script uses historical price data to calculate swing highs and swing lows based on specific conditions.

2. For each of the mentioned timeframes, the indicator identifies the highest high and lowest low within a defined number of bars (10, 30, 60, etc.).

3. Once a new swing high or swing low is identified, the corresponding dotted lines are drawn on the chart, extending from the previous swing point to the current one.

The "Swing Action Price" indicator can be used by traders to visually identify key support and resistance levels in the market. It helps them recognize potential trend reversals or continuation points, which may be valuable for making trading decisions.

Please note that trading indicators should always be used in conjunction with other technical and fundamental analysis tools to make informed trading choices. The "Swing Action Price" indicator is offered under the Mozilla Public License 2.0, and the developer's username is "damianjorgeportillo."

Remember that past performance is not indicative of future results, and it's essential to exercise caution and apply risk management strategies when trading financial markets.

/******************************/

Spanish:

**Descripción del Script "Swing Action Price" en TradingView**

"Swing Action Price" es un indicador técnico personalizado diseñado para identificar máximos y mínimos en un mercado financiero. El script calcula y muestra diversas líneas en el gráfico para visualizar estos puntos de inflexión. Los máximos se producen cuando el precio alcanza un pico local, mientras que los mínimos ocurren cuando el precio alcanza un valle local.

El indicador muestra las siguientes líneas en el gráfico:

1. Líneas punteadas que representan cada máximo y mínimo individual identificado en diferentes marcos de tiempo (10, 30, 60, 100, 150, 200, 700 y 1000 barras).

2. Líneas punteadas que representan el máximo y mínimo más reciente para la barra actual.

Cómo funciona el indicador:

1. El script utiliza datos históricos de precios para calcular los máximos y mínimos en función de ciertas condiciones.

2. Para cada uno de los marcos de tiempo mencionados, el indicador identifica el máximo más alto y el mínimo más bajo dentro de un número específico de barras (10, 30, 60, etc.).

3. Una vez que se identifica un nuevo máximo o mínimo, se dibujan las líneas punteadas correspondientes en el gráfico, extendiéndose desde el punto de inflexión anterior hasta el actual.

El indicador "Swing Action Price" puede ser utilizado por traders para identificar visualmente niveles clave de soporte y resistencia en el mercado. Ayuda a reconocer posibles puntos de inversión o continuación de tendencia, lo que puede ser valioso para tomar decisiones comerciales.

Por favor, ten en cuenta que los indicadores de trading siempre deben utilizarse junto con otras herramientas de análisis técnico y fundamental para tomar decisiones comerciales informadas. El indicador "Swing Action Price" se ofrece bajo la Licencia Pública de Mozilla 2.0, y el nombre de usuario del desarrollador es "damianjorgeportillo".

Recuerda que el rendimiento pasado no garantiza resultados futuros, y es esencial ser cauteloso y aplicar estrategias de gestión de riesgos al operar en los mercados financieros.

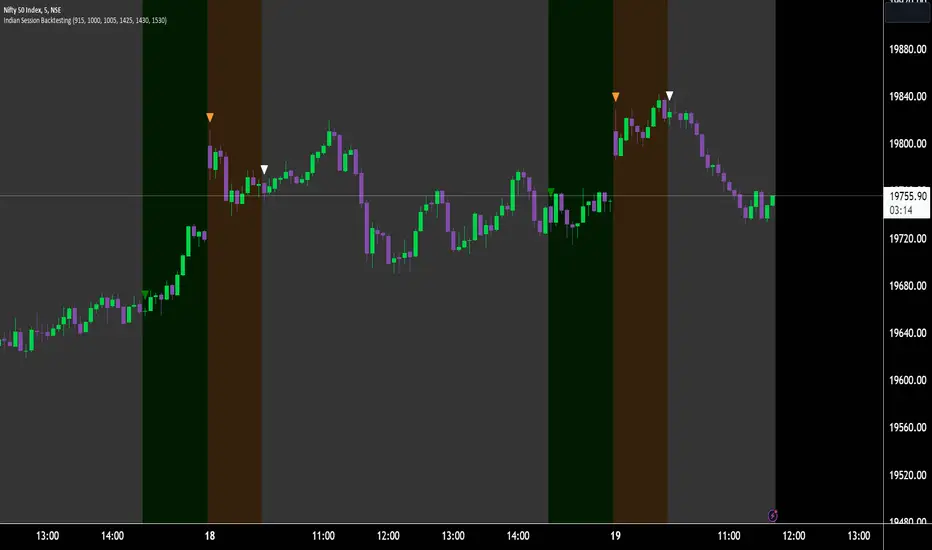

Indian Market Sessions for BacktestingThis indicator is designed to increase the quality of your backtesting in the Indian Market.

NSE & BSE run from 9:15 am IST to 3:30 pm IST.

Naturally different times have different kinds of volatility.

On your chart you will find premarked -

Saffron - 9:15 am to 10:30 am - Opening Session - High Volatility Observed Historically

White - 10:35 am to 2:25 pm - Middle Session - Lower Volatility Observed Historically

Green - 2:30 pm to 3:30 pm - Closing Session - Medium to High Volatility Observed Historically

You will also find the start of each session marked with an arrow.

Feel free to change the times from the input settings and the color and visibility from the style settings.

_______________

Usage:

When you backtest any strategies, say moving average crossovers, also mark the sessions in your sheet which will help you further increase accuracy.

Feel free to drop your doubts in the comments.

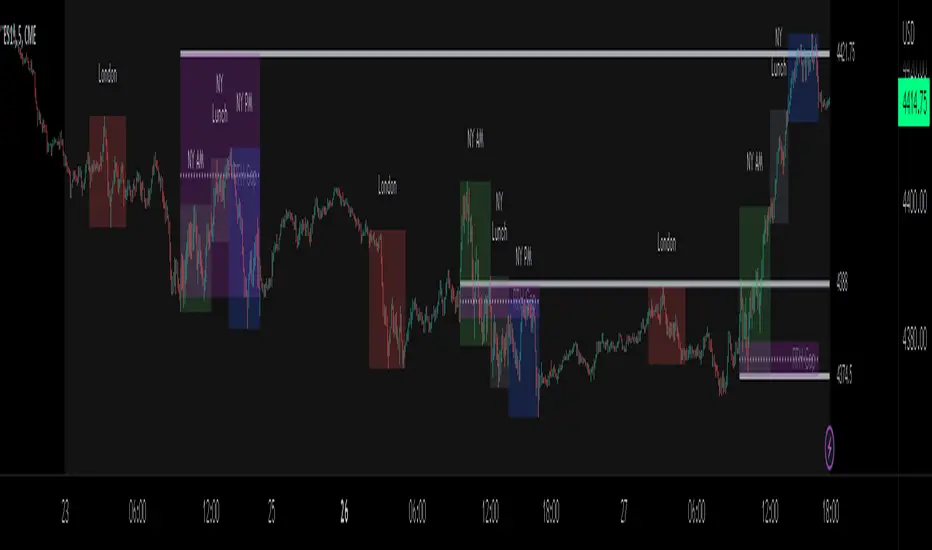

ICT Sessions_One Setup for Life [MK]The script plots the High/Low of the following trading sessions:

London - 02:00-05:00

NY AM - 09:30-12:00

New York Lunch - 12:00-13:30

New York PM - 13:30-16:00

Due to the high level of liquidity (resting orders), highs and lows of these sessions may be used as buy/sell areas and also as profit target areas. Typically, buy orders would be initiated below a session low and sell orders would be initiated above a

session high.

The script also plots 'RTH (Regular Trading Hours) Opening Gaps'. The RTH gaps are drawn from the closing price of regular trading at 16:15 (EST) to the open price of regular trading at 09:30 (EST). Gaps can be areas that traders might anticipate to be filled at some time in the future. A gap 'midline' is available if needed and yesterday RTH close line can be shown and extended to the current bar.

This script is simply a means to draw boxes around certain areas/periods on the charts. It is in no way a trading strategy and users should spend much time to study the concept and should also perform extensive back-testing before taking any trades.

By setting the lookback value to a much higher value then the default of 6, users can utilise the script to perform their own backtesting studies.

The above chart shows the default setup of the indicator. Note that the user has to choose how far (in days) to lookback and draw the sessions/gaps.

It is also possible to show the session high//low lines and extend them to the current bar time. If this is used it is advised to keep the lookback period as low as possible to ensure charts stay clean/uncluttered.

All boxes/lines styles/colors are fully customisable.

MA Slope : New Method1 . Introduction

Hello, traders.

This indicator is designed to measure the slope of a moving average line.

I imagine many of you who use Pine Script have struggled with this; measuring the slope of a moving average line can be quite challenging.

Firstly, this is because while the x-axis is fixed to the 'number of candles', the price scale on the y-axis can be adjusted freely.

Secondly, while the concept of differentiation could simplify the measurement process, the resulting value will differ from the conventional derivative we are familiar with since 'delta x' is fixed to '1'.

Consequently, I've put a lot of thought into how to configure the x-axis and y-axis in order to measure a slope that aligns with our perception of 'slope'.

After some reflection, I, like many others, realized that many people measure the slope based on the pivot of the moving average line.

This indicator is the product of that reflection.

2. Description

A. Setting

First, select the moving average line for which you want to check the slope. While SMA is commonly used, T3 is set as the default because it best visualizes the slope.

If you check 'Show MA Slope Average Pivot Range?' in the input window, it displays the average of the recent 30 slope pivot highs and pivot lows.

In other words, it shows 'On average, this level of slope was produced in the recent 30 waves.'

B. Usage

A cross from 0 in the slope indicates a 'reversal in the slope of the curve', which is the most crucial value when observing the slope.

Thus, fundamentally, it's important to look at the points where the slope becomes "0". Furthermore, when the slope starts to curve after rising, it signifies a change in acceleration, suggesting an imminent slope reversal.

(Note that acceleration was omitted from the indicator representation due to its tendency to overly complicate the data.)

While a shorter length of the moving average line may provide more useful slope data for actual trading, a less smooth moving average line may cross around 0 too often, making it less useful.

Therefore, it's crucial to adjust the 'Smoothing Length' in the input values to find a value that you believe is appropriate.

3. Conclusion

I always contemplate how to find a value in Pine Script that is similar to the perceived slope.

I made this script thinking that it might be a novel approach, but there are still many areas that need improvement.

If you have any innovative ideas about the slope, please feel free to provide feedback anytime.

Thank you.

--------

1. 서론

트레이더 여러분 안녕하세요. 이 지표는 이동평균선의 기울기를 측정하는 지표입니다.

아마 파인스크립트를 다루는 많은 분들이 같은 고민을 하셨을 것 같은데, 이동평균선의 기울기를 측정하는 것은 매우 어렵습니다.

그 이유로 첫번째는 x축은 '캔들 갯수'로 고정되어있는 반면, y축의 가격 스케일은 유동적으로 바꿀 수 있기 때문입니다.

두번째로는, 미분 개념을 이용하면 훨씬 수월하게 구할 수 있을테지만, 델타x가 '1'로 고정되어있기 때문에 우리가 알고있는 미분과 다른 값이 나옵니다.

따라서 x축과 y축을 어떻게 하면 실제 우리가 인식하는 '기울기'에 가깝도록 구성할 수 있을지에 대해 고민해보았습니다.

고민해본 결과 저 역시 그러하고, 많은 사람들이 이동평균선의 피벗을 기준으로 기울기를 측정한다는 사실을 알게되었습니다.

이 지표는 그 고민의 결과물입니다.

2. 내용 설명

A. 셋팅

먼저, 기울기를 확인하고싶은 이동평균선을 선택해주세요.

일반적으로 SMA를 많이 보시겠지만, T3가 기울기로 표현할 때 가장 아름다운 모습이 나오기 때문에 기본 설정을 T3로 설정했습니다.

Input창에 있는 'Show MA Slope Average Pivot Range?'를 체크하면, 최근 30개의 기울기 피벗 하이와 피벗 로우의 평균을 보여줍니다.

즉, '평균적으로, 최근 30개의 파동에서는 이 정도의 기울기가 만들어졌다'라는 것을 보여줍니다

B. 사용법

기울기가 0에서 크로스 된다는 것은, "곡선의 기울기가 반전"된다는 것이기에 기울기를 봄에 있어서 가장 중요한 값입니다. 따라서 가장 기본적으로는, 기울기가 "0"이 되는 곳을 보는 것이 중요하고

또 기울기가 올라갔다 꺾이기 시작할 때는, 가속도가 바뀌고 있다는 뜻이므로, 곧 기울기가 반전될 것을 의미합니다.

(다만 가속도를 지표로 표현하기엔, 너무나도 데이터가 지저분해져서 생략하였습니다)

이동평균선의 길이를 짧게 할수록 더 실제 트레이딩에 유용한 기울기 데이터를 얻을 수 있으나,

부드럽지 못한 이동평균선은 기울기가 0 근처에서 크로스 되는 모습이 지나치게 많이 나올 것이기에 유용하지 않을 수 있습니다.

따라서, input값에 있는 'Smoothing Length'를 조절해가면서 자신이 생각하기에 맞는 값을 고르는 것이 중요합니다.

3. 맺음말

파인스크립트에서 어떻게하면 실제 인식하는 기울기와 유사한 값을 찾을 수 있을까를 항상 고민합니다. 나름 새로운 접근방법이라 생각해서 이렇게 스크립트로 만들었으나, 여전히 아쉬운 부분이 많이 존재합니다.

기울기에 대한 좋은 아이디어가 있다면 언제든 피드백 해주세요.

감사합니다.

Volume-Weighted RSI with Adaptive SmoothingThis indicator is designed to provide traders with insights into the relative strength of a security by incorporating volume-weighted elements, effectively combining the concepts of Relative Strength Index (RSI) and volume-weighted averages to generate meaningful trading signals.

The indicator calculates the traditional RSI, which measures the speed and change of price movements, as well as the volume-weighted RSI, which considers the influence of trading volume on price action. It then applies adaptive smoothing to the volume-weighted RSI, allowing for customization of the smoothing process. The resulting smoothed volume-weighted RSI is plotted alongside the original RSI, providing traders with a comprehensive view of the price strength dynamics.

The line coloration in this indicator is designed to provide visual cues about the relationship between the RSI and the volume-weighted RSI. When the RSI line is above or equal to the volume-weighted RSI line, it suggests a potentially bullish condition with positive market momentum. In such cases, the line is colored lime. Conversely, when the RSI line (fuchsia) is below the volume-weighted RSI line, it indicates a potentially bearish condition with negative market momentum. The line color is set to fuchsia. By observing the line color, traders can quickly assess the relative strength between the RSI and the volume-weighted RSI, aiding their decision-making process.

The bar color and background color further enhance the visual interpretation of the indicator. The bar color reflects the RSI's relationship with the volume-weighted RSI and the predefined thresholds. If the RSI line is above both the volume-weighted RSI line and the overbought threshold (70), the bar color is set to lime, indicating a potentially overbought condition. Conversely, if the RSI line is below both the volume-weighted RSI line and the oversold threshold (30), the bar color is set to fuchsia, suggesting a potentially oversold condition. When the RSI line is between these two thresholds, the bar color is set to yellow, indicating a neutral or intermediate state. The background color, displayed with a semi-transparent shade, provides additional context by reflecting the prevailing market conditions. It turns lime if the volume-weighted RSI is above the overbought threshold, fuchsia if below the oversold threshold, and yellow if it falls between these two thresholds. This coloration scheme aids traders in quickly assessing market conditions and potential trading opportunities.

Calculations:

-- RSI Calculation : The traditional RSI is calculated based on the price movements of the asset. The up and down movements are determined, and exponential moving averages are used to smooth the values. The RSI value ranges from 0 to 100, with levels above 70 indicating overbought conditions and levels below 30 indicating oversold conditions.