CGI - Option Premium Tracker [CE vs PE]## ⚡ CGI - Nifty Option Premium Tracker

**"Stop Switching Tabs. Decode the Institutional Battle."**

Trading Options in Nifty & BankNifty requires speed and clarity. Retail traders lose money because they look at the Spot Chart, but Big Players manipulate the **Premium Chart**.

The **CGI Premium Tracker** solves this. It plots both the **CALL (CE)** and **PUT (PE)** premium charts directly on a single screen, allowing you to spot the real winner in real-time.

---

### 🎯 Key Features (Free Version)

#### 1. ⚡ Dual-Chart Technology

* Visualize the **CE (Green Candles)** and **PE (Red Candles)** side-by-side.

* **The Logic:** If Spot is moving up, but the Call Premium isn't following (Divergence), it's a trap. This tool helps you see that instantly.

#### 2. 🐋 Operator Candle Detection

* **Blue Candles:** Highlight massive volume spikes (1.5x Average). This usually indicates "Smart Money" entering positions.

* **Yellow Candles:** Indicate extreme churn/panic.

#### 3. 🛡️ Institutional Anchors (Fresh AVWAP)

* Standard VWAP lags. Our **Fresh AVWAP** resets daily or at the first 15-minute close, showing you the *true* intraday average price where institutions defend their positions.

#### 4. 🚀 Scalper's EMA

* Includes the classic 8-EMA setup. A visual guide to stay in the trend as long as momentum holds.

---

### 🛠️ How to Use This Tool

1. **Select Your Strikes:** Go to settings and simply type the Strike name (e.g., `NIFTY24FEB26000CE`).

2. **Watch the Flow:** When Green Candles (CE) dominate Red Candles (PE) above the Anchors, the trend is real.

3. **Spot the Operator:** Watch for **Blue Candle** breakouts to identify where the momentum is starting.

---

### 🔓 Unlock Institutional Intelligence

This is the **Basic Visualization** tool.

Our **CGI Titanium Engine** (Invite-Only) is designed for professional analysis, adding:

* ✅ **Institutional Flow Ribbon:** Visualizes the dominant trend without the noise.

* ✅ **Trap Zone Detection:** Automatically highlights "Judas Swings" and fake-outs.

* ✅ **Market Consensus:** Advanced geometry to find high-probability reversal zones.

**👉 Check the Author Profile below to join the CGI Community!**

👇 **Drop a BOOST (Like) if this tool improved your screen setup!** 🚀

Optionstrading

Dynamic Strike Selection Indicator [ARJO]Dynamic Strike Selection Indicator

OVERVIEW

The Dynamic Strike Selection Indicator is a visual analysis tool designed for traders observing NSE (National Stock Exchange of India) instruments, particularly those interested in options. It displays a trend-based oscillator in the lower chart pane and automatically calculates option strike prices , presenting them in an easy-to-read table. The indicator helps users observe trend changes and understand how option strikes might be selected based on current market conditions.

IT has a dashboard that shows you:

Where the trend might be heading (through the oscillator)

What option strikes align with the current price level

When trend transitions occurred

CONCEPTS

This indicator combines several technical analysis concepts in a beginner-friendly format:

1. Trend Observation (Chandelier Exit)

The indicator uses a method called "Chandelier Exit" which observes price volatility to identify potential trend directions. When the indicator shows green, it suggests an upward trend pattern; red suggests a downward pattern. These are reference points, not predictions.

2. Smoothed Price Movement

Raw price data can be noisy. This indicator applies mathematical smoothing (called "Ehlers 2-Pole filter") to reduce short-term fluctuations, making it easier to observe the underlying trend direction.

3. Momentum Oscillator

The oscillator (displayed as bars and lines in the lower pane) shows the difference between smoothed price and its moving average. Positive values suggest upward momentum; negative values suggest downward momentum . This is similar to how MACD or LBR works.

4. Strike Price Calculation

For option traders , the indicator automatically calculates:

ATM (At-The-Money): The strike price closest to the current underlying price

OTM (Out-of-The-Money): Strike prices at a distance from ATM, based on your settings

These calculations use standard rounding methods based on each instrument's official strike interval.

FEATURES

Visual Components:

Color-Coded Oscillator: Green/teal for potential uptrend, purple/red for potential downtrend

Histogram Display: Visual bars showing momentum strength

Chandelier Exit Lines: Plotted on the main price chart as reference levels

Information Table: Displays calculated strikes, timestamps, and optional tracking data

Supported Instruments:

Major indices: NIFTY, BANKNIFTY

Popular stocks: RELIANCE, HDFCBANK, ICICIBANK, INFY, TCS, SBIN, and more

Any NSE instrument (using manual strike interval setting)

Flexible Configuration:

Choose between "Sell Mode" and "Buy Mode" perspectives

Customize strike interval for any instrument

Adjust sensitivity of trend detection

Modify visual appearance (colors, table position, text size)

Track entry prices and observe P&L calculations (for reference only)

Features:

Automatic strike interval detection for predefined instruments

Manual override option for custom requirements

Real-time option premium fetching (where available)

Timestamp recording of trend transitions

Active trade highlighting based on current trend

HOW TO USE

Step 1: Adding the Indicator

Open your TradingView chart with an NSE instrument (e.g., NIFTY, BANKNIFTY, or any stock)

Search for " Dynamic Strike Selection Indicator " in the Indicators menu

Click to add it to your chart

You'll see an oscillator appear in a pane below your price chart and a table in the corner

Step 2: Basic Settings

Click the settings (gear icon) on the indicator. Here are the key settings to understand:

Symbol Settings:

Symbol Source: Keep it on " Use Chart Symbol " to analyze whatever instrument is on your chart

Custom Symbol: Only change if you want to analyze a different instrument while viewing another chart

Expiry Date:

Set the expiry date of the option contracts you're observing

Use the dropdown menus for Day, Month, and Year

Example: For 30th January 2025, select Day: 30, Month: 01, Year: 25

Trade Entry (Optional):

Trade Mode: Choose "Sell" or "Buy" based on your observation perspective

Lot Size: Enter your intended lot size for P&L calculation reference

PUT/CALL Entry Price: Manually enter prices if you want to track reference P&L

OTM Strike Distance:

Default is 4 (means 4 strikes away from ATM)

Increase for further OTM strikes, decrease for closer strikes

Step 3: Understanding the Display

The Oscillator (Lower Pane):

Green/Teal Bars: Suggest bullish momentum characteristics

Purple/Red Bars: Suggest bearish momentum characteristics

Zero Line: The reference point - above suggests strength, below suggests weakness

Color Change: When the oscillator changes from red to green (or vice versa), it indicates a potential trend transition

Active Row Highlighting:

In Sell Mode: Green background on PUT row during uptrend, Red background on CALL row during downtrend

In Buy Mode: Green background on PUT row during downtrend, Red background on CALL row during uptrend

This helps you observe which strike aligns with the current trend direction

Visual Customization:

Change oscillator colors under "Color Settings"

Adjust table position, size, and transparency under "Table Settings"

Modify table colors to match your chart theme

NOTES FOR BEGINNERS

Start Simple: Use default settings first. Don't change too many parameters initially.

Paper Trade First: Observe the indicator for several days before considering any real trades. Note how often trend transitions occur and how strikes align.

Understand Your Instrument: Know the strike interval for your chosen stock/index. NIFTY/BANKNIFTY use 100, most stocks use 10, 20, or 50.

Timeframe Matters: The indicator behaves differently on different timeframes. A 5-minute chart will show more transitions than a 1-hour chart.

Use with Other Analysis: This indicator is one tool among many. Combine with price action, support/resistance, and volume analysis.

Don't Chase: Just because a transition occurs doesn't mean you must act. Observe the quality of the move.

Backtest Observations: Use TradingView's replay feature to observe how the indicator performed historically.

CONCLUSION

The Dynamic Strike Selection Indicator serves as an educational tool for observing trend-based oscillator patterns and understanding how option strikes might be mathematically selected based on current market conditions. It combines visual trend analysis with structured strike price calculations, helping users study the relationship between momentum patterns and option strike references.

The indicator is designed to enhance chart interpretation skills and provide transparency into strike selection methodologies. It does not predict future price movements or guarantee any outcomes. Users are encouraged to use it as one component of a broader analytical approach, always conducting independent research and maintaining realistic expectations about market analysis tools.

DISCLAIMER

This indicator is strictly for educational and analytical observation purposes. It is NOT a trading system, signal generator, or financial advisory service.

What This Indicator Does NOT Do:

Does not predict future price movements with certainty

Does not guarantee profitable trades or outcomes

Does not constitute financial, investment, or trading advice

Does not replace the need for independent research and analysis

Does not eliminate trading risks or ensure success

What You Must Understand:

All calculated strikes, P&L values, and trend observations are informational references only

Option trading involves substantial risk and can result in complete loss of invested capital

Past indicator performance does not predict future results

Trend transitions shown are historical observations, not predictions

The "active" highlighting is a visual reference tool, not a trade recommendation

Conduct thorough independent research before taking any trading decision. and consult qualified, licensed financial professionals for personalized advice.

The creator of this indicator is not a registered investment advisor, broker, or financial planner. This tool is provided "as is" without warranties of any kind. By using this indicator, you acknowledge that you understand these risks and limitations, and you agree that all trading decisions and their consequences are solely your responsibility. If you do not fully understand these risks or are unsure about options trading, do not use this indicator for live trading .

ATR + STRAT Dashboard (LAST + DIR + REV) + Est MovesATR + STRAT Dashboard is a multi-timeframe market structure indicator built around The Strat and ATR context. It summarizes higher-timeframe control (buyers vs sellers), highlights key Strat conditions (inside/outside/2-1-2 style transitions), and flags common reversal candles (hammer / shooting star style signals) to help spot potential turns. It also includes ATR-based context and estimated move guidance so you can quickly gauge whether price has “room” to run or is extended.

What it shows

MTF Dashboard: quick read of trend/control across multiple timeframes

Direction/Control: color-based bias (buyers vs sellers in charge)

Reversal Flags: highlights reversal-style candles for awareness (not guaranteed)

ATR Context + Estimated Moves: volatility-based framework for targets/expectations

Non-repainting HTF behavior: designed to use closed higher-timeframe bars to reduce repaint surprises

Note: This tool is for structure + context, not trade signals by itself. Always confirm with your plan/risk management.

Options Liquidity Meter (OLM)❓ The question behind this indicator

When trading options, it is common to experience situations where price moves in the expected direction, yet the option contract does not increase in value as anticipated.

This typically happens when one or more of the following conditions is missing:

Insufficient liquidity participation

Lack of volatility expansion

Weak or passive order flow

Options Liquidity Meter (OLM) was created to address this specific question:

“If price moves from here, are there conditions for option premiums to actually expand?”

🎯 What this indicator does

Options Liquidity Meter is a context tool, not a trading system.

It evaluates whether the current market environment is favorable for option premium expansion , based on three core engines:

Liquidity (Relative Volume)

Measures whether price movement is supported by meaningful participation.

Volatility State

Identifies compression, release, and expansion phases, where options tend to respond differently.

Order Flow Activity (OBV-based)

Acts as a proxy for active vs. passive participation, helping filter hollow moves.

These components are combined into a single, easy-to-read options context.

🟢🟡🔴 Options Context Output

The indicator displays one consolidated state:

RED — NO EXPANSION

Price may move, but option premiums often do not respond.

YELLOW — BUILDING

Liquidity or volatility is developing. Conditions are improving but not fully aligned.

GREEN — EXPANSION LIKELY

Liquidity, volatility expansion, and active flow are aligned.

This is a favorable environment for option premium expansion.

The same logic is reflected visually through the background color and summarized in the dashboard.

📊 How to read the dashboard

The dashboard shows:

Liquidity: LOW / OK / HIGH

Volatility: COMPRESSED / RELEASED / EXPANDING

Order Flow: FLAT / ACTIVE

Options Context: NO EXPANSION / BUILDING / EXPANSION LIKELY

Below, a Background Color Meaning section explains what each color represents, making the indicator intuitive and educational.

📍 Where to apply this indicator

Options Liquidity Meter must be applied to the underlying asset chart, such as:

Indices (SPY, SPX, QQQ, etc.)

Stocks

Futures

ETFs

It is not designed to be applied to option contracts themselves.

The indicator evaluates the market conditions of the underlying, which are the drivers that influence option premium behavior.

Contract selection (strike, delta, gamma, expiration) remains the trader’s responsibility.

🧠 How to use it

Use your own methodology to define:

Direction

Structure

Entries and exits

Use Options Liquidity Meter to evaluate:

Whether the current environment supports option premium expansion

If the context is RED, be cautious — price may move without rewarding options.

If the context is GREEN, the environment is statistically more favorable for options responsiveness.

🔗 Complementary tools

Options Liquidity Meter is designed to complement, not replace, other tools.

It works well alongside:

Opening Path Selector (EMA200 Context Tool)

For deciding which asset offers the cleanest directional context.

Multi-Tool VWAP + EMAs (Multi-Timeframe) + Key Levels

For in-chart structure, bias, and reference levels.

Each tool addresses a different stage of the decision process and can be used independently.

⚠️ Important notes

This indicator provides context only

It does not generate trading signals

No indicator guarantees results

Use at your own risk.

Max Pain Options [QuantLabs] v5 (Balanced)Institutional Grade Options Analysis: Max Pain, Gamma & Pin Risk

For years, TradingView users have been flying blind without access to Options Chain data. QuantLabs: Max Pain & Gamma Exposure changes that. This is not just a support/resistance indicator—it is a sophisticated, algorithmic model that reverse-engineers the incentives of Market Makers using synthetic Black-Scholes logic.

This tool visualizes the "invisible hand" of the market: the hedging requirements of large dealers who are forced to buy or sell to keep their books neutral.

CORE FEATURES:

🔴 Max Pain Gravity Model The bright red line represents the "Max Pain" strike—the price level where the maximum amount of Options Open Interest (Calls + Puts) expires worthless.

Theory: As OpEx (Expiration) approaches, Market Makers maximize profits by pinning the price to this level.

Strategy: Use this as a mean-reversion target. If price is far away, look for a snap-back to the red line.

🟣 Gamma Exposure Profiles (The Purple Lines) These neon histograms show you the estimated "Gamma Walls."

Long Gamma: Dealers trade against the trend (stabilizing price).

Short Gamma: Dealers trade with the trend (accelerating volatility).

Visual: The larger the purple bar, the harder it will be for price to break through that level.

📦 Algorithmic "Pin Risk" Zones The dashed red box highlights the "Kill Zone." When price enters this area near expiration, volatility often dies as dealers pin the asset to kill retail premiums.

Warning: Do not expect breakouts while inside the Pin Zone.

📊 Institutional HUD A clean, non-intrusive dashboard provides real-time Greeks and risk analysis:

Pin Risk: High/Medium/Low probability of a pinned close.

Exp Mode: Detects if the market is in "Short Gamma" (Squeeze territory) or "Long Gamma" (Chop territory).

HOW IT WORKS (The Math): Since live options data is not available via Pine Script, this engine uses a proprietary Synthetic OI Distribution Model. It inputs Volume, Volatility (IV), and Time-to-Expiry into a modified Black-Scholes equation to probability-map where the heavy open interest likely sits.

SETTINGS & CUSTOMIZATION:

Responsiveness: Tuned for the "Goldilocks Zone" (Spread: 12, Decay: 22) to catch local liquidity walls without over-fitting.

Visuals: Designed for Dark Mode. High-contrast Neon aesthetics for maximum readability.

Round Strike Price, Levels Options Series➤ Strike Price Range Mode:

➤ Exact Strike Price Mode:

⭐ Overview and How It Works

Round Strike Price or Levels is a precision-focused visual tool designed for options and index traders.

It dynamically plots round strike levels around the current price and presents them either as:

⠀ — Exact strike prices, or

⠀ — Strike price ranges, where each zone represents the midpoint between two adjacent strikes.

The indicator continuously recalculates the base strike using the current price and aligns all surrounding levels using a fixed step size.

All lines and labels are updated only on the last bar for optimal performance and stability.

This makes StrikePrice ideal for:

🔹 Identifying key option strikes.

🔹 Visualizing price acceptance zones.

🔹 Understanding strike-to-strike movement during intraday trading.

⭐ Key Features and Functionality

Strike Price Range:

⠀ — Treats each pair of strike lines as a price zone.

⠀ — Labels are plotted at the midpoint between two lines.

⠀ — Last label is intentionally hidden (no upper range exists)

Exact Strike Price:

⠀ — Labels are plotted directly on each strike line.

⠀ — Useful for precise strike-based analysis.

Dynamic Base Calculation:

⠀ — Automatically snaps price to the nearest round strike.

⠀ — Re-centers the entire grid as price moves.

⠀ — No manual adjustment required.

Efficient Object Management:

⠀ — Uses persistent arrays for lines and labels.

⠀ — Objects are reused instead of recreated.

⠀ — Prevents flickering and avoids TradingView object limits.

🎨 Visualizations and User Experience

Clean horizontal strike grid with configurable:

⠀ — Line width, Line color, Line style (Solid / Dashed / Dotted), Extension direction (Left / Right / Both / None).

Labels are:

⠀ — Positioned to the right of price, Size-adjustable, Fully customizable in text color and background color.

Designed to stay visually clear even on:

⠀ — Fast-moving intraday charts, Options-focused layouts, Multi-indicator setups.

Tip: Increase Right Bars Margin in chart settings to give labels proper spacing.

⭐ Settings and Customization

🔹 Strike Settings:

⠀ — Step (points): Distance between adjacent strike levels (e.g., 50, 100)

⠀ — Levels per side: Number of strike levels plotted above and below the base.

⠀ — Strike Mode: Strike Price Range, Exact Strike Price.

🔹 Line Settings:

⠀ — Line width, Line color, Line style (Solid / Dashed / Dotted), Line extension direction.

🔹 Label Settings:

⠀ — Show / hide labels, Label distance (bars to the right), Label size, Label text color, Label background color.

All label properties are updated dynamically, allowing real-time UI tuning without reloading the script.

⭐ Uniqueness of the Concept:

Unlike generic round-number indicators, StrikePrice:

⠀ — Understands option-style strike structure.

⠀ — Separates range-based thinking from exact price levels.

⠀ — Uses midpoint logic to visualize strike-to-strike movement.

⠀ — Maintains strict performance discipline by updating only when necessary.

This makes it especially useful for:

⠀ • NIFTY / BANKNIFTY options.

⠀ • Index and futures traders.

⠀ • Intraday strike rotation analysis.

⠀ • Premium decay and range-bound setups.

🚀 Conclusion:

StrikePrice is a focused, professional-grade indicator for traders who think in strikes, ranges, and levels rather than arbitrary prices.

It offers:

⠀ • Clear structure

⠀ • Accurate strike alignment

⠀ • Clean visuals

⠀ • Zero repainting logic

ATM Pulse (Arjo)ATM Pulse (Arjo) — Real-Time ATM Options Sentiment & Trend Strength Indicator

Overview

ATM Pulse (Arjo) is an options analytics and trend overlay tool that automatically detects the At-The-Money (ATM) strike for NIFTY, BANKNIFTY , or any selected stock.

It merges Call–Put Volume Ratio (CPVR) sentiment analysis with a Chandelier Exit trend overlay to help traders visualize both market bias and trend direction in a single chart.

Concepts & Logic

ATM Auto Detection

The script calculates the current ATM strike by rounding the underlying’s price to the nearest strike interval (e.g., 50 for NIFTY, 100 for BANKNIFTY). It then requests live option-chain data for that strike.

Call–Put Volume Ratio (CPVR)

The Call-Put Volume Ratio (CPVR) is calculated as the call volume divided by the put volume.

CPVR > 1.25 → Bullish dominance (Calls stronger)

CPVR < 0.75 → Bearish dominance (Puts stronger)

0.75–1.25 → Neutral sentiment

This ratio helps interpret real-time option-market positioning.

Chandelier Exit Trend Overlay

Using Average True Range (ATR) , the overlay plots dynamic trailing stops and visual trend zones:

🟢 Green: Uptrend continuation zone

🔴 Red: Downtrend continuation zone

A color change signals possible momentum reversal.

Combination of CPVR and Chandelier Exit

CPVR gauges option-market sentiment

Chandelier Exit confirms price-action direction

When both align (e.g., bullish CPVR + green Chandelier zone), it strengthens directional conviction. Divergent readings may signal indecision or early reversals.

How to Use

Open any NIFTY, BANKNIFTY , or stocks chart.

Add ATM Pulse (Arjo) to the chart.

Select your expiry date — the script auto-detects the ATM strike and displays:

C: Call LTP

P: Put LTP

CPVR: Call/Put Volume Ratio label

Watch the Chandelier Exit colors:

🟢 Green = Bullish trend

🔴 Red = Bearish trend

Combine CPVR bias + trend color for confirmation.

If CPVR is above 1.25 and trend color green → More bullish activity (Calls stronger).

If CPVR is below 0.75, and trend color red→ More bearish activity (Puts stronger).

If CPVR is between 0.75 and 1.25 and the trend color is gray/mixed → Neutral

Practical Use Case

The script continuously updates the ATM strike, CPVR , and trend overlay in real time.

It provides a clear visual snapshot of how option volumes align with price momentum , ideal for intraday or short-term directional traders.

Disclaimer

This tool is for educational and analytical purposes only.

It does not provide financial advice or guaranteed trading signals.

Happy Trading. ARJO

Institutional Zones: Opening & Closing Trend HighlightsDescription / Content:

Track key institutional trading periods on Nifty/Bank Nifty charts with dynamic session zones:

Opening Volatility Zone: 9:15 AM – 9:45 AM IST (Green)

Closing Institutional Zone: 1:30 PM – 3:30 PM IST (Orange)

Both zones are bounded by the day’s high and low to help visualize institutional activity and price behavior.

Key Observations:

Breakout in both closing trend and opening trends often occurs on uptrending days.

Breakdown in both closing range and opening range usually happens on downside trending days.

Price opening above the previous closing trend is often a sign of a strong opening.

This script helps traders identify trend strength, breakout/breakdown zones, and institutional participation during critical market hours.

Disclaimer:

This indicator is for educational and informational purposes only. It is not a financial advice or recommendation to buy or sell any instrument. Always confirm with your own analysis before taking any trade.

Pine Script Features:

Dynamic boxes for opening and closing sessions

Boxes adjust to the day’s high and low

Optional labels at session start

Works on intraday charts (1m, 5m, 15m, etc.)

Usage Tip:

Use this indicator in combination with trend analysis and volume data to spot strong breakout/breakdown opportunities in Nifty and Bank Nifty.

Gamma Exposure Levels by OMG (Oh My Gamma)OMG (Oh My Gamma) - Daily GEX Levels

An operational framework for Gamma analysis with daily data.

Indicator's Purpose & Demo Data

This indicator plots key strategic levels derived from Gamma Exposure (GEX) analysis. It showcases the operational logic of OhMyGamma analytical engine.

IMPORTANT: The levels plotted by this public script are based on a past date's snapshot for demonstration purposes. They are not valid for live trading and will not update automatically.

The real edge comes from using the fresh data structure provided daily.

How to Read the Levels

This indicator is designed to provide actionable intelligence, not just data. Here's how to read it:

The Levels: Each line represents a key strategic zone (Zero Gamma, Call/Put Walls, etc.) where a market reaction is statistically probable due to dealer hedging flows.

Line Thickness = Strategic Importance: The thickness of each line directly corresponds to its strategic rating. Thicker, solid lines represent higher-conviction zones.

Labels & Tooltips: Hover over a level's label on your chart to see its full description, confluences, and strategic rating.

Pro Tip: The Power of Confluence

This indicator is not a standalone "system". It's an institutional-grade intelligence layer. Its predictive power increases exponentially when used to find confluence with your own analysis.

The highest-probability trades occur when a key Gamma level aligns with:

Price Action: Key support/resistance zones, order blocks, or liquidity pools.

Volumetric Indicators: High/Low Volume Nodes (HVN/LVN) from Volume Profile, VWAP, and Anchored VWAP.

Use these levels to confirm your setups and gain the conviction to act.

How to Get the Daily Updated Script

This indicator requires a new Pine Script code each day to load the current session's data.

To get the daily updated code feel free to visit www.ohmygamma.com

Feedback & Suggestions

This tool is built for the community. Suggestions for improvements and new features are highly welcome and help the project evolve. Feel free to get in touch via the contact form on the website.

Disclaimer: This tool is for informational and educational purposes only. Trading involves significant risk. The authors assume no responsibility for any trading decisions.

Options Max Pain Calculator [BackQuant]Options Max Pain Calculator

A visualization tool that models option expiry dynamics by calculating "max pain" levels, displaying synthetic open interest curves, gamma exposure profiles, and pin-risk zones to help identify where market makers have the least payout exposure.

What is Max Pain?

Max Pain is the theoretical expiration price where the total dollar value of outstanding options would be minimized. At this price level, option holders collectively experience maximum losses while option writers (typically market makers) have minimal payout obligations. This creates a natural gravitational pull as expiration approaches.

Core Features

Visual Analysis Components:

Max Pain Line: Horizontal line showing the calculated minimum pain level

Strike Level Grid: Major support and resistance levels at key option strikes

Pin Zone: Highlighted area around max pain where price may gravitate

Pain Heatmap: Color-coded visualization showing pain distribution across prices

Gamma Exposure Profile: Bar chart displaying net gamma at each strike level

Real-time Dashboard: Summary statistics and risk metrics

Synthetic Market Modeling**

Since Pine Script cannot access live options data, the indicator creates realistic synthetic open interest distributions based on configurable market parameters including volume patterns, put/call ratios, and market maker positioning.

How It Works

Strike Generation:

The tool creates a grid of option strikes centered around the current price. You can control the range, density, and whether strikes snap to realistic market increments.

Open Interest Modeling:

Using your inputs for average volume, put/call ratios, and market maker behavior, the indicator generates synthetic open interest that mirrors real market dynamics:

Higher volume at-the-money with decay as strikes move further out

Adjustable put/call bias to reflect current market sentiment

Market maker inventory effects and typical short-gamma positioning

Weekly options boost for near-term expirations

Pain Calculation:

For each potential expiry price, the tool calculates total option payouts:

Call options contribute pain when finishing in-the-money

Put options contribute pain when finishing in-the-money

The strike with minimum total pain becomes the Max Pain level

Gamma Analysis:

Net gamma exposure is calculated at each strike using standard option pricing models, showing where hedging flows may be most intense. Positive gamma creates price support while negative gamma can amplify moves.

Key Settings

Basic Configuration:

Number of Strikes: Controls grid density (recommended: 15-25)

Days to Expiration: Time until option expiry

Strike Range: Price range around current level (recommended: 8-15%)

Strike Increment: Spacing between strikes

Market Parameters:

Average Daily Volume: Baseline for synthetic open interest

Put/Call Volume Ratio: Market sentiment bias (>1.0 = bearish, <1.0 = bullish) It does not work if set to 1.0

Implied Volatility: Current option volatility estimate

Market Maker Factors: Dealer positioning and hedging intensity

Display Options:

Model Complexity: Simple (line only), Standard (+ zones), Advanced (+ heatmap/gamma)

Visual Elements: Toggle individual components on/off

Theme: Dark/Light mode

Update Frequency: Real-time or daily calculation

Reading the Display

Dashboard Table (Top Right):

Current Price vs Max Pain Level

Distance to Pain: Percentage gap (smaller = higher pin risk)

Pin Risk Assessment: HIGH/MEDIUM/LOW based on proximity and time

Days to Expiry and Strike Count

Model complexity level

Visual Elements:

Red Line: Max Pain level where payout is minimized

Colored Zone: Pin risk area around max pain

Dotted Lines: Major strike levels (green = support, orange = resistance)

Color Bar: Pain heatmap (blue = high pain, red = low pain/max pain zones)

Horizontal Bars: Gamma exposure (green = positive, red = negative)

Yellow Dotted Line: Gamma flip level where hedging behavior changes

Trading Applications

Expiration Pinning:

When price is near max pain with limited time remaining, there's increased probability of gravitating toward that level as market makers hedge their positions.

Support and Resistance:

High open interest strikes often act as magnets, with max pain representing the strongest gravitational pull.

Volatility Expectations:

Above gamma flip: Expect dampened volatility (long gamma environment)

Below gamma flip: Expect amplified moves (short gamma environment)

Risk Assessment:

The pin risk indicator helps gauge likelihood of price manipulation near expiry, with HIGH risk suggesting potential range-bound action.

Best Practices

Setup Recommendations

Start with Model Complexity set to "Standard"

Use realistic strike ranges (8-12% for most assets)

Set put/call ratio based on current market sentiment

Adjust implied volatility to match current levels

Interpretation Guidelines:

Small distance to pain + short time = high pin probability

Large gamma bars indicate key hedging levels to monitor

Heatmap intensity shows strength of pain concentration

Multiple nearby strikes can create wider pin zones

Update Strategy:

Use "Daily" updates for cleaner visuals during trading hours

Switch to "Every Bar" for real-time analysis near expiration

Monitor changes in max pain level as new options activity emerges

Important Disclaimers

This is a modeling tool using synthetic data, not live market information. While the calculations are mathematically sound and the modeling realistic, actual market dynamics involve numerous factors not captured in any single indicator.

Max pain represents theoretical minimum payout levels and suggests where natural market forces may create gravitational pull, but it does not guarantee price movement or predict exact expiration levels. Market gaps, news events, and changing volatility can override these dynamics.

Use this tool as additional context for your analysis, not as a standalone trading signal. The synthetic nature of the data makes it most valuable for understanding market structure and potential zones of interest rather than precise price prediction.

Technical Notes

The indicator uses established option pricing principles with simplified implementations optimized for Pine Script performance. Gamma calculations use standard financial models while pain calculations follow the industry-standard definition of minimized option payouts.

All visual elements use fixed positioning to prevent movement when scrolling charts, and the tool includes performance optimizations to handle real-time calculation without timeout errors.

Implied Volatility RangeThe Implied Volatility Range is a forward-looking tool that transforms option market data into probability ranges for future prices. Based on the lognormal distribution of asset prices assumed in modern option pricing models, it converts the implied volatility curve into a volatility cone with dynamic labels that show the market’s expectations for the price distribution at a specific point in time. At the selected future date, it displays projected price levels and their percentage change from today’s close across 1, 2, and 3 standard deviation (σ) ranges:

1σ range = ~68.2% probability the price will remain within this range.

2σ range = ~95.4% probability the price will remain within this range.

3σ range = ~99.7% probability the price will remain within this range.

What makes this indicator especially useful is its ability to incorporate implied volatility skew. When only ATM IV (%) is entered, the indicator displays the standard Black–Scholes lognormal distribution. By adding High IV (%) and Low IV (%) values tied to strikes above and below the current price, the indicator interpolates between these inputs to approximate the implied volatility skew. This adjustment produces a market-implied probability distribution that indicates whether the option market is leaning bullish or bearish, based on the data entered in the menu:

ATM IV (%) = Implied volatility at the current spot price (at-the-money).

High IV (%) = Implied volatility at a strike above the current spot price.

High Strike = Strike price corresponding to the High IV input (OTM call).

Low IV (%) = Implied volatility at a strike below the current spot price.

Low Strike = Strike price corresponding to the Low IV input (OTM put).

Expiration (Day, Month, Year) = Option expiration date for the projection.

Once these inputs are entered, the indicator calculates implied probability ranges and, if both High IV and Low IV values are provided, adjusts for skew to approximate the option market’s distribution. If no implied volatility data is supplied, the indicator defaults to a lognormal distribution based on historical volatility, using past realized volatility over the same forward horizon. This keeps the tool functional even without implied volatility inputs, though in that case the output represents only an approximation of ATM IV, not the actual market view.

In summary, the Implied Volatility Range is a powerful tool that translates implied volatility inputs into a clear and practical estimate of the market’s expectations for future prices. It allows traders to visualize the probability of price ranges while also highlighting directional bias, a dimension often difficult to interpret from traditional implied volatility charts. It should be emphasized, however, that this tool reflects only the market’s expectations at a specific point in time, which may change as new information and trading activity reshape implied volatility.

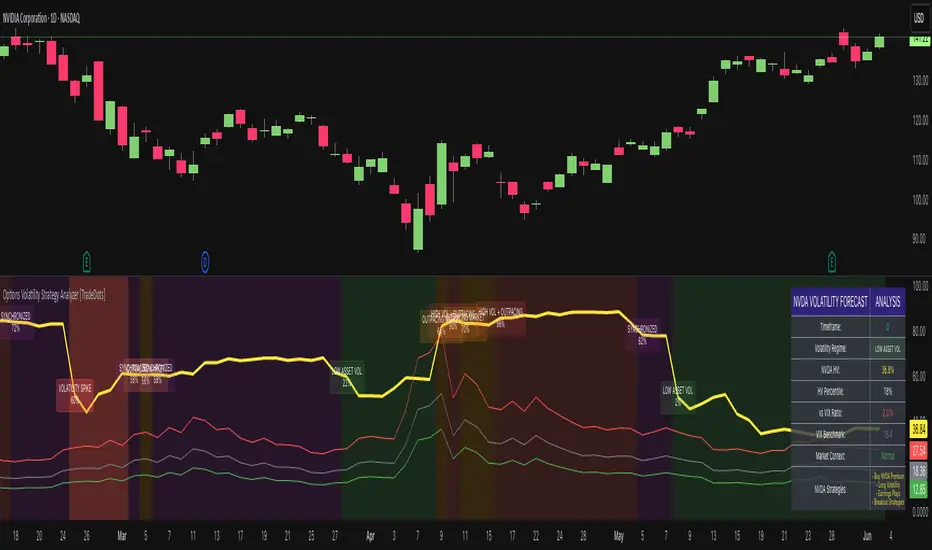

Options Volatility Strategy Analyzer [TradeDots]The Options Volatility Strategy Analyzer is a specialized tool designed to help traders assess market conditions through a detailed examination of historical volatility, market benchmarks, and percentile-based thresholds. By integrating multiple volatility metrics (including VIX and VIX9D) with color-coded regime detection, the script provides users with clear, actionable insights for selecting appropriate options strategies.

📝 HOW IT WORKS

1. Historical Volatility & Percentile Calculations

Annualized Historical Volatility (HV): The script automatically computes the asset’s historical volatility using log returns over a user-defined period. It then annualizes these values based on the chart’s timeframe, helping you understand the asset’s typical volatility profile.

Dynamic Percentile Ranks: To gauge where the current volatility level stands relative to past behavior, historical volatility values are compared against short, medium, and long lookback periods. Tracking these percentile ranks allows you to quickly see if volatility is high or low compared to historical norms.

2. Multi-Market Benchmark Comparison

VIX and VIX9D Integration: The script tracks market volatility through the VIX and VIX9D indices, comparing them to the asset’s historical volatility. This reveals whether the asset’s volatility is outpacing, lagging, or remaining in sync with broader market volatility conditions.

Market Context Analysis: A built-in term-structure check can detect market stress or relative calm by measuring how VIX compares to shorter-dated volatility (VIX9D). This helps you decide if the present environment is risk-prone or relatively stable.

3. Volatility Regime Detection

Color-Coded Background: The analyzer assigns a volatility regime (e.g., “High Asset Vol,” “Low Asset Vol,” “Outpacing Market,” etc.) based on current historical volatility percentile levels and asset vs. market ratios. A color-coded background highlights the regime, enabling traders to quickly interpret the market’s mood.

Alerts on Regime Changes & Spikes: Automated alerts warn you about any significant expansions or contractions in volatility, allowing you to react swiftly in changing conditions.

4. Strategy Forecast Table

Real-Time Strategy Suggestions: At the close of each bar, an on-chart table generates suggested options strategies (e.g., selling premium in high volatility or buying premium in low volatility). These suggestions provide a quick summary of potential tactics suited to the current regime.

Contextual Market Data: The table also displays key statistics, such as VIX levels, asset historical volatility percentile, or ratio comparisons, helping you confirm whether volatility conditions warrant more conservative or more aggressive strategies.

🛠️ HOW TO USE

1. Select Your Timeframe: The script supports multiple timeframes. For short-term trading, intraday charts often reveal faster shifts in volatility. For swing or position trading, daily or weekly charts may be more stable and produce fewer false signals.

2. Check the Volatility Regime: Observe the background color and on-chart labels to identify the current regime (e.g., “HIGH ASSET VOL,” “LOW VOL + LAGGING,” etc.).

3. Review the Forecast Table: The table suggests strategy ideas (e.g., iron condors, long straddles, ratio spreads) depending on whether volatility is elevated, subdued, or spiking. Use these as a starting point for designing trades that match your risk tolerance.

4. Combine with Additional Analysis: For optimal results, confirm signals with your broader trading plan, technical tools (moving averages, price action), and fundamental research. This script is most effective when viewed as one component in a comprehensive decision-making process.

❗️LIMITATIONS

Directional Neutrality: This indicator analyzes volatility environments but does not predict price direction (up/down). Traders must combine with directional analysis for complete strategy selection.

Late or Missed Signals: Since all calculations require a bar to close, sharp intrabar volatility moves may not appear in real-time.

False Positives in Choppy Markets: Rapid changes in percentile ranks or VIX movements can generate conflicting or premature regime shifts.

Data Sensitivity: Accuracy depends on the availability and stability of volatility data. Significant gaps or unusual market conditions may skew results.

Market Correlation Assumptions: The system assumes assets generally correlate with S&P 500 volatility patterns. May be less effective for:

Small-cap stocks with unique volatility drivers

International stocks with different market dynamics

Sector-specific events disconnected from broad market

Cryptocurrency-related assets with independent volatility patterns

RISK DISCLAIMER

Options trading involves substantial risk and is not suitable for all investors. Options strategies can result in significant losses, including the total loss of premium paid. The complexity of options strategies requires thorough understanding of the risks involved.

This indicator provides volatility analysis for educational and informational purposes only and should not be considered as investment advice. Past volatility patterns do not guarantee future performance. Market conditions can change rapidly, and volatility regimes may shift without warning.

No trading system can guarantee profits, and all trading involves the risk of loss. The indicator's regime classifications and strategy suggestions should be used as part of a comprehensive trading plan that includes proper risk management, directional analysis, and consideration of broader market conditions.

Opening Range Breakout (ORB)This is an Opening Range Break indicator. Best if used on a 5 minute chart. It plots the opening 30 minutes high and low of a ticker. (meaning mostly for stocks, options, etfs) and then it alerts a buy signal upon break of opening high and a sell signal upon break of opening low. This is a day trading type of indicator and there is a new opening range everyday.

Monthly Options Expiration 2025Monthly Options Expiration 2025

Plots the monthly options expiration dates in advance for the year 2025.

Happy trading and all the best.

Option Time ValueThis TradingView script calculates and visualizes the time value of an option (Call or Put) based on its market price and intrinsic value. The time value represents the premium paid for the option above its intrinsic value, and it is a key metric for analyzing the cost of holding an option.

This script is suitable for traders analyzing options on indices or stocks, such as the NIFTY 50, and supports both Call and Put options. By dynamically extracting the strike price and option type from the input symbol, it adapts seamlessly to the selected instrument.

Key Features:

Dynamic Instrument Selection:

Users can input the underlying asset (e.g., NSE:NIFTY) and the specific option instrument (e.g., NSE:NIFTY250327C24000 for a Call or NSE:NIFTY250327P24000 for a Put).

Automatic Option Type Detection:

The script detects whether the option is a Call or a Put by parsing the input symbol for the characters "C" (Call) or "P" (Put).

Dynamic Strike Price Extraction:

The strike price is dynamically extracted from the input option symbol, eliminating the need for hardcoding and reducing user errors.

Key Metrics Plotted:

Time Value: The premium paid above the intrinsic value, plotted in blue.

Intrinsic Value: The calculated intrinsic value of the option, plotted in green.

Seamless Integration:

Designed for ease of use and integration into existing TradingView setups.

Automatically adjusts to the timeframe and pricing data of the selected instruments.

Options Cumulative Chart AnalysysThis Pine Script is a comprehensive tool designed for traders analyzing options data on TradingView. It aggregates multiple symbols to calculate and visualize cumulative performance, providing essential insights for decision-making.

Key Features:

Symbol and Strike Price Configuration:

Supports up to four configurable symbols (e.g., NIFTY options).

Allows defining buy/sell actions, quantities, and entry premiums for each symbol.

Customizable Chart Display:

Plot candlesticks and line charts for cumulative data.

Configurable Exponential Moving Averages (EMAs) for technical analysis.

Entry and price lines with customizable colors.

Timeframe Management:

Supports higher timeframe (HTF) candles.

Ensures compatibility with the current chart timeframe to maintain accuracy.

Dynamic Coloring and Visualization:

Red, green, and gray color schemes for body and wicks of candlesticks based on price movements.

Customizable positive and negative color schemes.

Table for Data Representation:

Displays an info table showing symbols, quantities, entry prices, and latest traded prices (LTP).

Adjustable table position, overlay, and styling.

Premium and Profit/Loss Calculations:

Calculates cumulative open, high, low, and close prices considering premiums and quantities.

Tracks the profit and loss dynamically based on cumulative premiums and market prices.

Alerts and Notifications:

Alerts triggered on specific conditions, such as when the profit/loss turns negative.

Modular Functions:

Functions for calculating high/low/open/close values, combining premiums, and drawing candlesticks.

Utilities for symbol management and security requests.

Custom Settings:

Includes a wide range of input options for customization:

Timeframes, EMA lengths, colors, table configurations, and more.

Error Handling:

Validates timeframe inputs to ensure compatibility and prevent runtime errors.

This script is designed for advanced traders looking for a customizable tool to analyze cumulative options data efficiently. By leveraging its modular design and visual elements, users can make informed trading decisions with a holistic view of market movements.

Rolling Straddle PremiumScript is Basically intended to provide insight's on the Rolling Straddle premium for the selected index based on the input settings.

Important thing to consider for the script to work seamlessly:

Specify the LTP in the input field (need not be very accurate)

Specify the Expiry Date for the Option Strike.

Ensure Profile matches to the chart script (Index Script)

Note: Zones marked in Blue, is the max level that indicator can track the option prices. beyond which it may fail to track, during such time consider reloading the indicator with Latest LTP .

Labels on the chart indicate that If i had shorted the Straddle, what would be my current position of that Straddle. however the rational behind shorting is only the pivot high points (not sure if this is right or wrong! )

Note On Labels: Labels are delayed basis the pivot point candles specified in the indicator settings.

EN: Entry Price (Straddle Premium) of the Strike Specified.

Cur: Current Price ( Current Straddle Premium ) of the Strike Specified.

SH: Max Straddle Premium ( Increase in Premium ) since position is active.

SL: Min Straddle Premium ( Premium Erosion ) since position is active.

Theta Shield | Flux Charts💎 GENERAL OVERVIEW

Introducing our new Theta Shield indicator! Theta is the options risk factor concerning how fast there is a decline in the value of an option over time. This indicator aims to help the trader avoid sideways market phases in the current ticker, to minimize the risk of theta decay. For more information, please check the "How Does It Work" section.

Features of the new Theta Shield Indicator :

Foresight Of Accumulation Zones

Decrease Risk Of Theta Decay

Clear "Valid" & "Non-Valid" Signals

Validness Trail

Alerts

📌 HOW DOES IT WORK ?

In options trading, theta is defined as the rate of decline in the value of an option due to the passage of time. Traders want to avoid this kind of decay in the value of an option. One of the best ways to avoid it is not holding an option contract when the market is going sideways. This indicator uses a stochastic oscillator to try to get a foresight of sideways markets, warning the trader to not hold an option contract while the price is in a range.

The indicator starts by calculating the stochastic value using close, high & low prices of the candlesticks. Then a stoch threshold & a theta length are determined depending on the option contract type defined by the user in the settings of the indicator. Each candlestick that falls above or below the stoch threshold value is counted, and a "theta valid strength" is calculated using the counted candlesticks, which has a value between -100 & 100. Here is the formula of the "theta valid strength" value :

f_lin_interpolate(float x0, float x1, float y0, float y1, float x) =>

y0 + (x - x0) * (y1 - y0) / (x1 - x0)

thetaValid = Total Candlesticks That Fall Above & Below The Threshold In Last "Theta Length" bars.

thetaValidStrength = f_lin_interpolate(0, thetaLength, -100, 100, thetaValid)

Then a trail is rendered, and "Valid" & "Non-Valid" signals are given using this freshly calculated strength value. Valid means that the indicator currently thinks that no accumulation will happen in the near future, so the option positions in the current ticker are protected from the theta decay. Non-Valid means that the indicator thinks the ticker has entered the accumulation phase, so holding any option position is not recommended, as they may be affected by the theta decay.

🚩 UNIQUENESS

This indicator offers a unique way to avoid theta decay in options trading. It uses a stochastic oscillator and thresholds to calculate a "theta strength" value, which is used for rendering validness signals and a trail. Traders can follow the valid & non-valid signals when deciding to hold their options position or not. The indicator also has an alerts feature, so you can get notified when a ticker is about to enter a range, or when it's about to get out of it.

⚙️ SETTINGS

1. General Configuration

Contract Type -> You can set the option contract type here. The indicator will adjust itself to get a better foresight depending on the contract length.

2. Style

Fill Validness -> Will render a trail based on "theta strength" value.

DEVPRO TradingDEVPRO Trading system comprises of the following:

D - Double (EMA and VWAP)

E - EMA

V - VWAP (current and previous day ending VWAP level)

P - Standard Pivot Point

R - RSI (Multi-time frame table is added at the top and traders can add standard RSI 14 as an additional non-overlay indicator)

O - OI data (not available for options trading in TV but trader can always check in their broker terminal)

Double EMA have been color coded in red and green for bullish and bearish trends.

Candles are colored for bullish (green), sideways (grey) and bearish (red) phases.

Setup to be traded with monthly options for stocks and weekly options for indices.

Bullish Setup:

RSI greater than 50

Current candle close above VWAP and previous day closing VWAP

Current candle close above daily Pivot

For option buying (Call option OI should be falling below its moving average 20 meaning short covering)

For option selling (Put option OI should be rising above its moving average 20 meaning Put writers confidence is increasing)

Book partial qty profits at R1/R2/R3 and/or exit completely on Doji candle low break

Bearish Setup:

RSI less than 50

Current candle close below VWAP and previous day closing VWAP

Current candle close below daily Pivot

For option buying (Put option OI should be falling below its moving average 20 meaning short covering)

For option selling (Call option OI should be rising above its moving average 20 meaning Call writers confidence is increasing)

Book partial qty profits at S1/S2/S3 and/or exit completely on Doji candle high break

BUY/SELL + ADVANCE DECLINEThis script is a custom trading view indicator that helps to identify potential buy and sell signals based on the RSI (Relative Strength Index) and SMA (Simple Moving Average) indicators. The script also identifies potential reversals using a combination of RSI and price action. It plots buy, sell, and reversal signals on the chart along with an SMA line. Additionally, it provides alerts based on the buy, sell, and reversal conditions.

Changes made to the original script:

Fixed the undeclared identifier 'c' error by calculating the difference between the current closing price and the previous closing price: c = close - close .

Added an "ADD Value Floating Label" to the chart. The label shows the difference between the current and previous closing prices (ADD value) along with a "Bullish" or "Bearish" indicator based on the value of 'c'. The label is positioned at the top right of the visible chart area and remains static.

Here's a summary of the major components of the script:

Input settings: Define the input parameters for RSI and SMA.

Calculation of RSI and SMA: Compute the RSI and SMA values based on the input parameters.

Color definitions: Define colors for different conditions and levels.

Condition definitions: Define various conditions for buy, sell, reversal, and other criteria.

Buy and sell conditions: Determine buy and sell signals based on RSI, SMA, and price action.

Reversal conditions: Identify potential reversals using RSI and price action.

Plot signals: Display buy, sell, and reversal signals on the chart.

Bar colors: Color the bars based on the identified signals.

Plot SMA: Display the SMA line on the chart.

Alert conditions: Set up alerts for buy, sell, and reversal conditions.

ADD Value Floating Label: Add a label to the chart showing the ADD value and a "Bullish" or "Bearish" indicator.

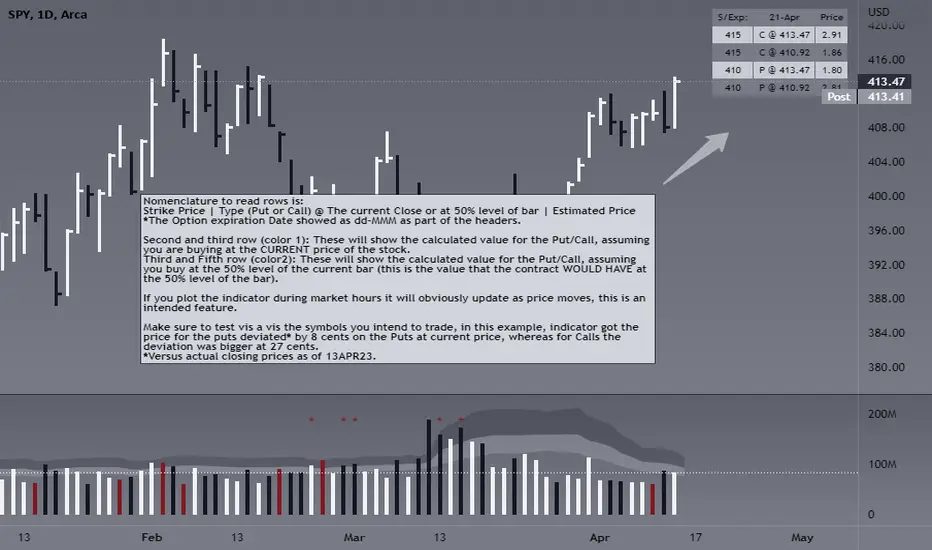

Automated Option Price - Black-Scholes modelPlease make sure you are plotting this indicator on DAILY bars, not doing so will lead to unintended results. Also, make sure that you keep up to date the Risk-free interest rate, which you can consult (for U.S.) on ycharts.com.

This is an indicator that is meant to be used for Options Day Trading, but it can be useful for mid-term or leaps for I also enabled the possibility for user to input manually the Strike and Expiration date. I based the calculation on the Black-Scholes model. Variables included in the calculation are:

-Stock price (S): The current price of the underlying asset (e.g., a stock).

-Strike price (K): The predetermined price at which the option can be exercised.

-Time to expiration (T): The time remaining until the option expires, expressed as a fraction of a year.

-Volatility (σ): The annualized standard deviation of the stock's returns, which is a measure of the stock's price fluctuations.

-Risk-free interest rate (r): The annualized return on a risk-free investment, often approximated by the yield on a government bond.

The only variable I excluded from the original model was the Dividend yield (q).

U S E R I N P U T S:

1. AUTOMATIC calculations enabled:

i) Strike price (K):

Automatically calculate the strike price for both call and put options based on the stock's closing price. The logic follows a set of rules to determine the strike prices which will usually be Out-of-the-Money (OTM):

-If the stock's closing price is between 1 and 60, the call strike price is rounded up to the nearest whole number, while the put strike price is rounded down to the nearest whole number.

-If the stock's closing price is between 60 and 90, the call strike price is rounded up to the nearest whole number and increased by 1, while the put strike price is rounded down to the nearest whole number and decreased by 1.

-If the stock's closing price is between 90 and 120, the call strike price is rounded up to the nearest whole number and increased by 2, while the put strike price is rounded down to the nearest whole number and decreased by 2.

-If the stock's closing price is above 120, the call strike price is rounded up to the nearest multiple of 5, while the put strike price is rounded down to the nearest multiple of 5.

By applying these rules, I just tried to ensure that the automatically calculated strike prices are tailored to the stock's price range, allowing for more accurate option pricing calculations.

ii) Time to expiration (T):

The indicator will consider this week’s expiration contracts (Friday) only when the current day/bar = Monday. If Tuesday or older it will consider the expiration date of the next week’s Friday (because we are not Theta gamblers, right?).

If you are not comfortable with above for whatever reason, you can always…

2. Enter inputs MANUALLY

First make sure you UNTICK the boxes for automatic calculation.

i) Strike price (K) – Self-explanatory

ii) Time to expiration (T) – Just make sure that the horizon you are inputting matches with the next parameter (e.g. you would not input a Monthly risk-free interest rate for a Leap).

iii) Risk-free interest rate (r) – You can pull this data from the web. Here’s the link I used to define the value that this indicator was launched with:

ycharts.com

Don’t get obsessed with updating this daily if you are using this for day trading, you will notice that weekly may be more than enough.

V O L A T I L I T Y

Not option to manually input Volatility so I’ll explain how it is calculated in this script:

I considered two measures of volatility; one is derived calculating the annualized volatility using the standard deviation of daily returns and the second one is the ATR-based annualized volatility. I then used a ‘combined’ approach with the harmonic mean and the arithmetic mean of these results which can help account for the variability in the option prices calculated with different volatility estimates, which can be more robust when dealing with outliers or skewed data. I back tested with some samples of actual option prices and found that this approach is the one that got results closer to the actual bids.

T A B L E

Nomenclature to read rows is:

Option Strike Price | Type of Option (Put or Call) @ The current Close or at 50% level of bar | Estimated Price

*The Option expiration Date showed as dd-MMM as part of the headers.

Second and third row (color 1): These will show the calculated value for the Put/Call, assuming you are buying at the CURRENT price of the stock.

Third and Fifth row (color2): These will show the calculated value for the Put/Call, assuming you buy at the 50% level of the current bar (this is the value that the contract WOULD HAVE at the 50% level of the bar).

If you plot the indicator during market hours it will obviously update as price moves, this is an intended feature.

L I M I T A T I O N S

The Black-Scholes model, like many other models, has its limitations and will oftentimes provide inaccurate option prices in all market conditions. High volatility events, such as earnings announcements, can lead to significant price fluctuations that are not fully captured by the model.

The model assumes that the stock price follows a continuous random walk with constant volatility, but in reality, volatility can change over time, and stock prices can exhibit jumps, especially around significant events like earnings announcements. This can cause the model to underestimate the true option price in such situations.

Please make sure that you first back test on the symbols you trade to ensure the information presented by this indicator will suit your trading strategy. You will find that the delta between the proposed price of the indicator versus the actual price may differ significantly in some symbols while for others it will be very close. For instance, today (13APR23), the prices for AMD, DIS, AAPL (puts only), were very close to actual bids, whereas TSLA differ significantly (but then again, take a look at the calendar and this last symbol is having earnings next week which may add a premium to the contracts)… I am sure you will get your own conclusions and applicable use cases based on the data you test with.

As always, be wise and methodical on the investment or trading decisions you make!

Options Price CalculatorIn the team, we continue to explore and expand the boundaries of TradingView.

For now, there is not much an options trader can do with options in TradingView.

We wanted to change that and created a simple option pricer.

You can set up in parameters a set of strikes, implied volatility, and days to expiry.

The indicators will take a risk-free rate from US01Y and the underlying price from your current chart.

It will compute prices and greeks for both put and call options.

Thanks to @MUQWISHI for helping code it.

Disclaimer

Please remember that past performance may not indicate future results.

Due to various factors, including changing market conditions, the strategy may no longer perform as well as in historical backtesting.

This post and the script don’t provide any financial advice.

Higher Time Frame Average True RangesPurpose: This script will help an options trader asses risk and determine good entry and exit strategies

Background Information: The true range is the greatest of: current high minus the current low; the absolute value of the current high minus the previous close; and the absolute value of the current low minus the previous close. The Average True Range (ATR) is a 14-day moving average of the true range. Traders use the ATR indicator to assess volatility in stocks and decide when to enter and exit trades. It is important to note the limitations of using True Range and ATR: These indications cannot tell you the direction of your options trade (call vs. put) and they cannot tell you whether a particular trend is about to reverse. However, it can be used to assess if volatility has peaked for a particular direction and time period.

How this script works: This indicator calculates true range for the daily (DTR), weekly (WTR), and monthly (MTR) time frames and compares it to the Average True Range (ATR) for each of those time frames (DATR, WATR, and MATR). The comparison is displayed into a colored table in the upper right-hand corner of the screen. When a daily, weekly, or monthly true range reaches 80% of its respective ATR, the row for that time frame will turn Orange indicating medium risk for staying in the trade. If the true range goes above 100% of the respective ATR, then the row will turn Red indicating high risk for staying in the trade. When the row for a time period turns red, volatility for the time period has likely peaked and traders should heavily consider taking profits. It is important to note these calculations start at different times for each time frame: Daily (Today’s Open), Weekly (Monday’s Open), Monthly (First of the Month’s Open). This means if it’s the 15th of the month then the Monthly True Range is being calculated for the trading days in the first half of the month (approximately 10 trade days).

The script also plots three sets of horizontal dotted lines to visually represent the ATR for each time period. Each set is generated by adding and subtracting the daily, weekly, and monthly ATRs from that time periods open price. For example, the weekly ATR is added and subtracted from Mondays open price to visually represent the true range for that week. The DATR is represented by red lines, the WATR is represented by the green lines, and the MATR is represented by the blue lines. These plots could also be used to assess risk as well.

How to use this script: Use the table to assess risk and determine potential exit strategies (Green=Low Risk, Orange=Medium Risk, Red=High Risk. Use the dotted lines to speculate what a stock’s price could be in a given time period (Daily=Red, Weekly=Green, and Monthly=Blue). And don’t forget the true range’s calculation and plots starts at the beginning of each time period!