FlowFusion Money Flow — FP + VWAP Drift + PVT (−100..+100)Title (ASCII only)

FlowFusion Money Flow — Flow Pressure + Rolling VWAP Drift + PVT (Normalized −100..+100)

Short Description

Original money-flow oscillator combining Flow Pressure, Rolling VWAP Drift, and PVT Momentum into one normalized score (−100..+100) with a signal line, thresholds, optional component plots, and ready-made alerts.

Full Description (meets “originality & usefulness”)

What’s original

FlowFusion Money Flow is not a generic mashup. It builds a single score from three complementary, volume-aware components that target different facets of order flow:

Flow Pressure (FP) — In-bar directional drive scaled by relative volume.

Drive

=

close

−

open

max

(

high

−

low

,

tick

)

∈

=

max(high−low, tick)

close−open

∈ .

Relative Volume

=

volume

average volume over

𝑓

𝑝

𝐿

𝑒

𝑛

=

average volume over fpLen

volume

.

𝐹

𝑃

𝑟

𝑎

𝑤

=

Drive

×

RelVol

FP

raw

=Drive×RelVol then squashed (softsign) to

.

Why it belongs: distinguishes real pushes (big body and big volume) from noise.

Rolling VWAP Drift — Direction of VWAP itself over a rolling window, normalized by ATR.

𝑉

𝑊

𝐴

𝑃

𝑡

=

∑

(

𝑇

𝑃

×

𝑉

𝑜

𝑙

)

∑

𝑉

𝑜

𝑙

VWAP

t

=

∑Vol

∑(TP×Vol)

over vwapLen.

Drift

=

𝑉

𝑊

𝐴

𝑃

𝑡

−

𝑉

𝑊

𝐴

𝑃

𝑡

−

1

𝐴

𝑇

𝑅

=

ATR

VWAP

t

−VWAP

t−1

→ squashed to

.

Why it belongs: persistent VWAP movement signals sustained accumulation/distribution.

PVT Momentum — Price-Volume Trend standardized (z-score) and squashed.

𝑃

𝑉

𝑇

𝑡

=

𝑃

𝑉

𝑇

𝑡

−

1

+

𝑉

𝑜

𝑙

×

Δ

𝐶

𝑙

𝑜

𝑠

𝑒

𝐶

𝑙

𝑜

𝑠

𝑒

𝑡

−

1

PVT

t

=PVT

t−1

+Vol×

Close

t−1

ΔClose

.

𝑧

=

𝑃

𝑉

𝑇

−

SMA

(

𝑃

𝑉

𝑇

)

StDev

(

𝑃

𝑉

𝑇

)

z=

StDev(PVT)

PVT−SMA(PVT)

→ squashed to

.

Why it belongs: captures volume-weighted trend pressure without relying on price alone.

Composite score:

Score

=

𝑤

𝐹

𝑃

⋅

𝐹

𝑃

+

𝑤

𝑉

𝑊

𝐴

𝑃

⋅

𝑉

𝑊

𝐴

𝑃

_

𝐷

𝑟

𝑖

𝑓

𝑡

+

𝑤

𝑃

𝑉

𝑇

⋅

𝑃

𝑉

𝑇

_

𝑀

𝑜

𝑚

𝑤

𝐹

𝑃

+

𝑤

𝑉

𝑊

𝐴

𝑃

+

𝑤

𝑃

𝑉

𝑇

Score=

w

FP

+w

VWAP

+w

PVT

w

FP

⋅FP+w

VWAP

⋅VWAP_Drift+w

PVT

⋅PVT_Mom

with a Signal = SMA(Score, sigLen). Thresholds mark strong accumulation/distribution zones.

How it works (step-by-step)

Compute FP, VWAP Drift, PVT Momentum.

Normalize each to the same

scale.

Weighted average → FlowFusion Score.

Smooth with a Signal line to reduce whipsaw.

Optional background shading when Score exceeds thresholds.

How to use

Direction filter:

Score > 0 favors longs; Score < 0 favors shorts.

Momentum turns:

Score crosses above Signal → setup for long; below → setup for short.

Strength zones:

Above Upper Threshold (default +40) = strong buy pressure; below Lower (−40) = strong sell pressure.

Confluence:

Best near S/R, trendlines, or HTF bias. For scalping on 1–5m, consider sigLen 9–13 and thresholds ±40 to ±50.

Alerts included: zero cross, zone entries, and Score/Signal crossovers.

Inputs (key)

fpLen (20): relative-volume lookback for Flow Pressure.

vwapLen (34): rolling VWAP window.

pvtLen (50): PVT z-score window.

sigLen (9): Signal smoothing.

Weights: wFP, wVWAP, wPVT to bias the blend.

Thresholds: upperBand / lowerBand (defaults +40/−40).

Display: toggle component plots and background shading.

Best practices

Trending markets: increase wVWAP (VWAP Drift) or widen thresholds.

Ranging markets: increase wFP and wPVT; take quicker profits.

News: wait for bar close confirmation or reduce size.

Data quality: use consistent volume feeds (especially in crypto).

Limitations

Oscillators can stay extreme in strong trends; use structure/trend filters.

Volume anomalies (illiquid pairs, API glitches) can distort signals—sanity-check with another venue when possible.

Disclaimer

This indicator is for educational purposes only and is not financial advice. Trading involves risk; past performance does not guarantee future results. Always paper-trade first and use appropriate risk controls.

M-oscillator

SMC Zones & Confirmations with Filters [PersianDev]these zones filtered by confirmations. confirmations are with filters.

Nearest Rank For Loop - [JTCAPITAL]Nearest Rank For Loop is used for trend-following using the median of the data.

The indicator works by calculating in the following steps:

1. The median is calculated using the ranking length of the source and using "percentile nearest rank" to determine the middle value. This is done with the original length and the length devided by 3, averaged out to eliminate false signals from extremely fast and temporary market movements.

2. Over the length of the loop values get added based on the median being higher than the previous median.

3. The results of the for loop segment get smoothed out using an EMA.

--Buy and sell conditions--

-When the for loop values get above the long threshold we enter a buying condition, we dont exit the buying condition until the for loop values get below the short condition. Which signals a short.

-When the values stay between the thresholds the signal doesnt change. This and smoothing out the for loop values is used to eliminate false signals as much as possible.

--Features and Parameters--

-Allows the changing of the length of the ranking (median)

-Allows the usage of different sources

-Allows changing of the paramaters over the start and end of the for loop segment

-Allows changing the thresholds for longs and shorts

-Allows changing the parameter for the smoothing using an EMA

--Details--

Both the wide thresholds and the use of an EMA over the for loop values are used to eliminate as much false signals as possible. Aswell as deviding the length by 3 and taking the average from the medians. From testing this indicator we have found that using a very small value for the shorting gives the overall best performance. Since a fast market move wont immediately trigger a false signal, but it also wont massively delay entries and exits.

It is recommended to change the parameter settings for different asset classes and timeframes based off volatility and fast and confusing market movements.

Enjoy!

Big Mo’s Glaskugel — Macro Drawdown Risk (v1.1.2)What it does / what you see

An at-a-glance drawdown-risk oscillator that blends several macro US signals.

• A smooth, color-blended line (green→orange→red) shows the scaled risk score (0–100).

• Subtle shading marks “re-steepen warning windows” (starts when the yield curve re-steepens after an inversion; ends on normalization/cool-down).

• A compact status table summarizes: overall risk level, Yield Curve (10y–3m), Credit Stress (Baa–10y), Economy (LEI), and Valuation (CAPE).

Data used & why

Yield Curve (10y–3m) — FRED:T10Y3M. Inversions and subsequent re-steepens often precede recessions/equity drawdowns.

Credit Stress — FRED:BAA10Y vs its 1-year average (deviation in bps). Widening credit spreads flag tightening financial conditions.

Economy (LEI) — ECONOMICS:USLEI. 6-month annualized growth below a cutoff highlights macro deterioration.

Valuation (CAPE) — SHILLER_PE_RATIO_MONTH. Elevated valuations can amplify downside risk.

VIX spikes — optional boost that recognizes sudden risk repricings.

Important disclaimer

This is not a reliable or predictive indicator in all regimes. No guarantees or warranties of any kind are provided. It is not financial advice. Signals can be early, late, or wrong.

That said, it leans on well-studied warning factors (yield-curve dynamics, credit spreads, LEI weakness, valuation extremes) that have flagged major market downturns in the past.

Key customization / tweaks

Weights for each component (Yield, Credit, LEI, VIX, CAPE).

Thresholds: yield inversion months, re-steepen lookback, credit-stress bps, LEI cutoff, CAPE level, VIX spike levels.

Re-steepen boost: enable/disable, base points, half-life decay.

Shading behavior: cool-down bars to “unwarn,” max warning duration, only shade when risk ≠ green.

Scaling & smoothing: dynamic rolling max, EMA length, yellow/red thresholds.

Status table: position, and a snapshot mode to view values at a chosen historical time.

Standardized Cumulative Deltas [LuxAlgo]The Standardized Cumulative Deltas tool allows traders to compare the cumulative standardized open-close difference for up to 10 different tickers, allowing them to visualize the general sentiment for all selected tickers.

These results allow the construction of two areas showing the average or extreme bullish and bearish cumulative change for all enabled tickers, providing a summarized view of the overall ticker group sentiment.

🔶 USAGE

This tool is meant to give a full picture of the individuals and/or overall selected tickers, and unlike classical indicators, the displayed series of values is not meant to be directly interpreted over time.

Given the selected lookback period, a majority of observations being above 0 indicate an overall bullish market for the asset.

By default, the auto lookback period feature is enabled, allowing the tool to use all the visible bars for its calculations. Traders can also set the lookback period manually. The above chart uses a fixed lookback period of 500.

Up to 10 tickers can be used. While major cryptocurrencies are set by default, the users can set a specific basket of assets, such as US equities, forex pairs, commodities, etc.

🔹 Densities

The provided areas, here called densities, can be used to get an overall sentiment of the selected tickers. The upper density (bullish) processes positive deltas, while the lower one (bearish) processes negative ones.

Interpretation is subject to the selected "Density Mode".

Average: Densities track the average bullish/bearish cumulative deltas for the selected tickers. For example, a more prominent bullish density would indicate that, on average, cumulative deltas were positive across the tickers.

Envelope: Densities track the extreme values made by bullish/bearish cumulative deltas for the selected tickers. Here, a more prominent density would indicate more volatile bullish/bearish movements, depending on the density.

🔹 Dashboard

The tool features a dashboard with active tickers and their respective colors for traders' convenience.

🔶 DETAILS

🔹 Densities

Densities are obtained by applying a forward-backward exponential moving average on the average, or the highest/lowest cumulative series, depending on the selected Density Mode.

The resulting densities are smoothed by the "Smoothing" parameter located in the Settings panel, with higher values returning smoother envelopes with less variability.

Do note that the smoothing method used here is subject to repainting.

🔶 SETTINGS

Lookback: Select the lookback period and enable/disable the Auto Lookback feature

Tickers: Enable/disable and select up to 10 tickers and their colors

Density Mode: Determine how densities are calculated

🔹 Dashboard

Show Dashboard: Enable/disable the dashboard

Position: Select the dashboard position

Size: Select the dashboard size

🔹 Style

Density: Enable/disable the density areas

Bullish Density: Select the color of the top density area

Bearish Density: Select the color of the bottom density area

Smoothing: Select the smoothing constant for the EMA calculation

Adaptive Valuation [BackQuant]Adaptive Valuation

What this is

A composite, zero-centered oscillator that standardizes several classic indicators and blends them into one “valuation” line. It computes RSI, CCI, Demarker, and the Price Zone Oscillator, converts each to a rolling z-score, then forms a weighted average. Optional smoothing, dynamic overbought and oversold bands, and an on-chart table make the inputs and the final score easy to inspect.

How it works

Components

• RSI with its own lookback.

• CCI with its own lookback.

• DM (Demarker) with its own lookback.

• PZO (Price Zone Oscillator) with its own lookback.

Standardization via z-score

Each component is transformed using a rolling z-score over lookback bars:

z = (value − mean) ÷ stdev , where the mean is an EMA and the stdev is rolling.

This puts all inputs on a comparable scale measured in standard deviations.

Weighted blend

The z-scores are combined with user weights w_rsi, w_cci, w_dm, w_pzo to produce a single valuation series. If desired, it is then smoothed with a selected moving average (SMA, EMA, WMA, HMA, RMA, DEMA, TEMA, LINREG, ALMA, T3). ALMA’s sigma input shapes its curve.

Dynamic thresholds (optional)

Two ways to set overbought and oversold:

• Static : fixed levels at ob_thres and os_thres .

• Dynamic : ±k·σ bands, where σ is the rolling standard deviation of the valuation over dynLen .

Bands can be centered at zero or around the valuation’s rolling mean ( centerZero ).

Visualization and UI

• Zero line at 0 with gradient fill that darkens as the valuation moves away from 0.

• Optional plotting of band lines and background highlights when OB or OS is active.

• Optional candle and background coloring driven by the valuation.

• Summary table showing each component’s current z-score, the final score, and a compact status.

How it can be used

• Bias filter : treat crosses above 0 as bullish bias and below 0 as bearish bias.

• Mean-reversion context : look for exhaustion when the valuation enters the OB or OS region, then watch for exits from those regions or a return toward 0.

• Signal confirmation : use the final score to confirm setups from structure or price action.

• Adaptive banding : with dynamic thresholds, OB and OS adjust to prevailing variability rather than relying on fixed lines.

• Component tuning : change weights to emphasize trend (raise DM, reduce RSI/CCI) or range behavior (raise RSI/CCI, reduce DM). PZO can help in swing environments.

Why z-score blending helps

Indicators often live on different scales. Z-scoring places them on a common, unitless axis, so a one-sigma move in RSI has comparable influence to a one-sigma move in CCI. This reduces scale bias and allows transparent weighting. It also facilitates regime-aware thresholds because the dynamic bands scale with recent dispersion.

Inputs to know

• Component lookbacks : rsilb, ccilb, dmlb, pzolb control each raw signal.

• Standardization window : lookback sets the z-score memory. Longer smooths, shorter reacts.

• Weights : w_rsi, w_cci, w_dm, w_pzo determine each component’s influence.

• Smoothing : maType, smoothP, sig govern optional post-blend smoothing.

• Dynamic bands : dyn_thres, dynLen, thres_k, centerZero configure the adaptive OB/OS logic.

• UI : toggle the plot, table, candle coloring, and threshold lines.

Reading the plot

• Above 0 : composite pressure is positive.

• Below 0 : composite pressure is negative.

• OB region : valuation above the chosen OB line. Risk of mean reversion rises and momentum continuation needs evidence.

• OS region : mirror logic on the downside.

• Band exits : leaving OB or OS can serve as a normalization cue.

Strengths

• Normalizes heterogeneous signals into one interpretable series.

• Adjustable component weights to match instrument behavior.

• Dynamic thresholds adapt to changing volatility and drift.

• Transparent diagnostics from the on-chart table.

• Flexible smoothing choices, including ALMA and T3.

Limitations and cautions

• Z-scores assume a reasonably stationary window. Sharp regime shifts can make recent bands unrepresentative.

• Highly correlated components can overweight the same effect. Consider adjusting weights to avoid double counting.

• More smoothing adds lag. Less smoothing adds noise.

• Dynamic bands recalibrate with dynLen ; if set too short, bands may swing excessively. If too long, bands can be slow to adapt.

Practical tuning tips

• Trending symbols: increase w_dm , use a modest smoother like EMA or T3, and use centerZero dynamic bands.

• Choppy symbols: increase w_rsi and w_cci , consider ALMA with a higher sigma , and widen bands with a larger thres_k .

• Multiday swing charts: lengthen lookback and dynLen to stabilize the scale.

• Lower timeframes: shorten component lookbacks slightly and reduce smoothing to keep signals timely.

Alerts

• Enter and exit of Overbought and Oversold, based on the active band choice.

• Bullish and bearish zero crosses.

Use alerts as prompts to review context rather than as stand-alone trade commands.

Final Remarks

We created this to show people a different way of making indicators & trading.

You can process normal indicators in multiple ways to enhance or change the signal, especially with this you can utilise machine learning to optimise the weights, then trade accordingly.

All of the different components were selected to give some sort of signal, its made out of simple components yet is effective. As long as the user calibrates it to their Trading/ investing style you can find good results. Do not use anything standalone, ensure you are backtesting and creating a proper system.

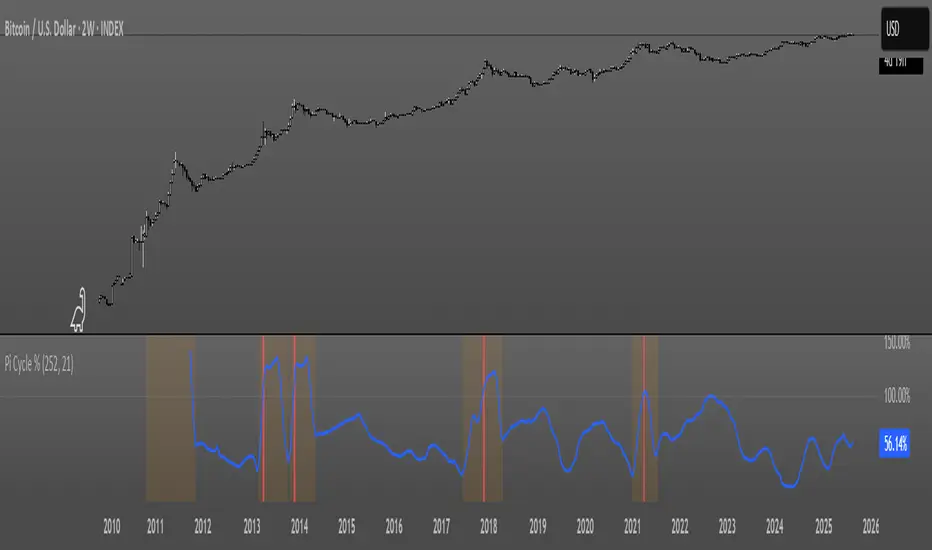

Pi Cycle OscillatorThis oscillator combines the Pi Cycle Top indicator with a percentile-based approach to create a more precise and easy to read market timing tool.

Instead of waiting for moving average crossovers, it shows you exactly how close you are to a potential market top.

Orange background means you should start preparing for a potential top and look into taking profits.

Red background means that the crossover has happened on the original Pi Cycle Indicator and that you should have already sold everything. (Crossover of the gray line aka 100)

Thank you

Bollinger Band Width Percentile - The_Caretaker

Pi Cycle Top - megasyl20

SMC - Institutional Confidence Oscillator [PhenLabs]📊 Institutional Confidence Oscillator

Version: PineScript™v6

📌 Description

The Institutional Confidence Oscillator (ICO) revolutionizes market analysis by automatically detecting and evaluating institutional activity at key support and resistance levels using our own in-house detection system. This sophisticated indicator combines volume analysis, volatility measurements, and mathematical confidence algorithms to provide real-time readings of institutional sentiment and zone strength.

Using our advanced thin liquidity detection, the ICO identifies high-volume, narrow-range bars that signal institutional zone formation, then tracks how these zones perform under market pressure. The result is a dual-wave confidence oscillator that shows traders when institutions are actively defending price levels versus when they’re abandoning positions.

The indicator transforms complex institutional behavior patterns into clear, actionable confidence percentiles, helping traders align with smart money movements and avoid common retail trading pitfalls.

🚀 Points of Innovation

Automated thin liquidity zone detection using volume threshold multipliers and zone size filtering

Dual-sided confidence tracking for both support and resistance levels simultaneously

Sigmoid function processing for enhanced mathematical accuracy in confidence calculations

Real-time institutional defense pattern analysis through complete test cycles

Advanced visual smoothing options with multiple algorithmic methods (EMA, SMA, WMA, ALMA)

Integrated momentum indicators and gradient visualization for enhanced signal clarity

🔧 Core Components

Volume Threshold System: Analyzes volume ratios against baseline averages to identify institutional activity spikes

Zone Detection Algorithm: Automatically identifies thin liquidity zones based on customizable volume and size parameters

Confidence Lifecycle Engine: Tracks institutional defense patterns through complete observation windows

Mathematical Processing Core: Uses sigmoid functions to convert raw market data into normalized confidence percentiles

Visual Enhancement Suite: Provides multiple smoothing methods and customizable display options for optimal chart interpretation

🔥 Key Features

Auto-Detection Technology: Automatically scans for institutional zones without manual intervention, saving analysis time

Dual Confidence Tracking: Simultaneously monitors both support and resistance institutional activity for comprehensive market view

Smart Zone Validation: Evaluates zone strength through volume analysis, adverse excursion measurement, and defense success rates

Customizable Parameters: Extensive input options for volume thresholds, observation windows, and visual preferences

Real-Time Updates: Continuously processes market data to provide current institutional confidence readings

Enhanced Visualization: Features gradient fills, momentum indicators, and information panels for clear signal interpretation

🎨 Visualization

Dual Oscillator Lines: Support confidence (cyan) and resistance confidence (red) plotted as percentage values 0-100%

Gradient Fill Areas: Color-coded regions showing confidence dominance and strength levels

Reference Grid Lines: Horizontal markers at 25%, 50%, and 75% levels for easy interpretation

Information Panel: Real-time display of current confidence percentiles with color-coded dominance indicators

Momentum Indicators: Rate of change visualization for confidence trends

Background Highlights: Extreme confidence level alerts when readings exceed 80%

📖 Usage Guidelines

Auto-Detection Settings

Use Auto-Detection

Default: true

Description: Enables automatic thin liquidity zone identification based on volume and size criteria

Volume Threshold Multiplier

Default: 6.0, Range: 1.0+

Description: Controls sensitivity of volume spike detection for zone identification, higher values require more significant volume increases

Volume MA Length

Default: 15, Range: 1+

Description: Period for volume moving average baseline calculation, affects volume spike sensitivity

Max Zone Height %

Default: 0.5%, Range: 0.05%+

Description: Filters out wide price bars, keeping only thin liquidity zones as percentage of current price

Confidence Logic Settings

Test Observation Window

Default: 20 bars, Range: 2+

Description: Number of bars to monitor zone tests for confidence calculation, longer windows provide more stable readings

Clean Break Threshold

Default: 1.5 ATR, Range: 0.1+

Description: ATR multiple required for zone invalidation, higher values make zones more persistent

Visual Settings

Smoothing Method

Default: EMA, Options: SMA/EMA/WMA/ALMA

Description: Algorithm for signal smoothing, EMA responds faster while SMA provides more stability

Smoothing Length

Default: 5, Range: 1-50

Description: Period for smoothing calculation, higher values create smoother lines with more lag

✅ Best Use Cases

Trending market analysis where institutional zones provide reliable support/resistance levels

Breakout confirmation by validating zone strength before position entry

Divergence analysis when confidence shifts between support and resistance levels

Risk management through identification of high-confidence institutional backing

Market structure analysis for understanding institutional sentiment changes

⚠️ Limitations

Performs best in liquid markets with clear institutional participation

May produce false signals during low-volume or holiday trading periods

Requires sufficient price history for accurate confidence calculations

Confidence readings can fluctuate rapidly during high-impact news events

Manual fallback zones may not reflect actual institutional activity

💡 What Makes This Unique

Automated Detection: First Pine Script indicator to automatically identify thin liquidity zones using sophisticated volume analysis

Dual-Sided Analysis: Simultaneously tracks institutional confidence for both support and resistance levels

Mathematical Precision: Uses sigmoid functions for enhanced accuracy in confidence percentage calculations

Real-Time Processing: Continuously evaluates institutional defense patterns as market conditions change

Visual Innovation: Advanced smoothing options and gradient visualization for superior chart clarity

🔬 How It Works

1. Zone Identification Process:

Scans for high-volume bars that exceed the volume threshold multiplier

Filters bars by maximum zone height percentage to identify thin liquidity conditions

Stores qualified zones with proximity threshold filtering for relevance

2. Confidence Calculation Process:

Monitors price interaction with identified zones during observation windows

Measures volume ratios and adverse excursions during zone tests

Applies sigmoid function processing to normalize raw data into confidence percentiles

3. Real-Time Analysis Process:

Continuously updates confidence readings as new market data becomes available

Tracks institutional defense success rates and zone validation patterns

Provides visual and numerical feedback through the oscillator display

💡 Note:

The ICO works best when combined with traditional technical analysis and proper risk management. Higher confidence readings indicate stronger institutional backing but should be confirmed with price action and volume analysis. Consider using multiple timeframes for comprehensive market structure understanding.

Moving Average Adaptive RSI [BackQuant]Moving Average Adaptive RSI

What this is

A momentum oscillator that reshapes classic RSI into a zero-centered column plot and makes it adaptive. It builds RSI from two parts:

• A sensitivity window that scans several recent bars to capture the strongest up and down impulses.

• A selectable moving average that smooths those impulses before computing RSI.

The output ranges roughly from −100 to +100 with 0 as the midline, with optional extra smoothing and built-in divergence detection.

How it works

Impulse extraction

• For each bar the script inspects the last rsi_sen bars and collects upward and downward price changes versus the current price.

• It keeps the maximum upward change and maximum downward change from that window, emphasizing true bursts over single-bar noise.

MA-based averaging

• The up and down impulse series are averaged with your chosen MA over rsi_len bars.

• Supported MA types: SMA, EMA, DEMA, WMA, HMA, SMMA (RMA), TEMA.

Zero-centered RSI transform

• RS = UpMA ÷ DownMA, then mapped to a symmetric scale: 100 − 200 ÷ (1 + RS) .

• Above 0 implies positive momentum bias. Below 0 implies negative momentum bias.

Optional extra smoothing

• A second smoothing pass can be applied to the final oscillator using smoothing_len and smooth_type . Toggle with “Use Extra Smoothing”.

Visual encoding

• The oscillator is drawn as columns around the zero line with a gradient that intensifies toward extremes.

• Static bands mark 80 to 100 and −80 to −100 for extreme conditions.

Key inputs and what they change

• Price Source : input series for momentum.

• Calculation Period (rsi_len) : primary averaging window on up and down components. Higher = smoother, slower.

• Sensitivity (rsi_sen) : how many recent bars are scanned to find max impulses. Higher = more responsive to bursts.

• Calculation Type (ma_type) : MA family that shapes the core behavior. HMA or DEMA is faster, SMA or SMMA is slower.

• Smoothing Type and Length : optional second pass to calm noise on the final output.

• UI toggles : show or hide the oscillator, candle painting, and extreme bands.

Reading the oscillator

• Midline cross up (0) : momentum bias turning positive.

• Midline cross down (0) : momentum bias turning negative.

• Positive territory :

– 0 to 40: constructive but not stretched.

– 40 to 80: strong momentum, continuation more likely.

– Above 80: extreme risk of mean reversion grows.

• Negative territory : mirror the same levels for the downside.

Divergence detection

The script plots four divergence types using pivot highs and lows on both price and the oscillator. Lookbacks are set by lbL and lbR .

• Regular bullish : price lower low, oscillator higher low. Possible downside exhaustion.

• Hidden bullish : price higher low, oscillator lower low. Bias to trend continuation up.

• Regular bearish : price higher high, oscillator lower high. Possible upside exhaustion.

• Hidden bearish : price lower high, oscillator higher high. Bias to trend continuation down.

Labels: ℝ for regular, ℍ for hidden. Green for bullish, red for bearish.

Candle coloring

• Optional bar painting: green when the oscillator is above 0, red when below 0. This is for visual scanning only.

Strengths

• Adaptive sensitivity via a rolling impulse window that responds to genuine bursts.

• Configurable MA core so you can match responsiveness to the instrument.

• Zero-centered scale for simple regime reads with 0 as a clear bias line.

• Built-in regular and hidden divergence mapping.

• Flexible across symbols and timeframes once tuned.

Limitations and cautions

• Trends can remain extended. Treat extremes as context rather than automatic reversal signals.

• Divergence quality depends on pivot lookbacks. Short lookbacks give more signals with more noise. Long lookbacks reduce noise but add lag.

• Double smoothing can delay zero-line transitions. Balance smoothness and timeliness.

Practical usage ideas

• Regime filter : only take long setups from your separate method when the oscillator is above 0, shorts when below 0.

• Pullback confirmation : in uptrends, look for dips that hold above 0 or turn up from 0 to 40. Reverse for downtrends.

• Divergence as a heads-up : wait for a zero-line cross or a price trigger before acting on divergence.

• Sensitivity tuning : start with rsi_sen 2 to 5 on faster timeframes, increase slightly on slower charts.

Alerts

• MA-A RSI Long : oscillator crosses above 0.

• MA-A RSI Short : oscillator crosses below 0.

Use these as bias or timing aids, not standalone trade commands.

Settings quick reference

• Calculation : Price Source, Calculation Type, Calculation Period, Sensitivity.

• Smoothing : Smoothing Type, Smoothing Length, Use Extra Smoothing.

• UI : Show Oscillator, Paint Candles, Show Static High and Low Levels.

• Divergences : Pivot Lookback Left and Right, Div Signal Length, Show Detected Divergences.

Final thoughts

This tool reframes RSI by extracting strong short-term impulses and averaging them with a moving-average model of your choice, then presenting a zero-centered output for clear regime reads. Pair it with your structure, risk and execution process, and tune sensitivity and smoothing to the market you trade.

SExI - Super Exhaustion Indicator [Da_Prof]As we know, the RSI can remain at "overbought" or "oversold" levels for long periods of time while the price continues in that direction. The SExI (Super Exhaustion Indicator) is an indicator designed to help detect exhaustion of strong moves.

The SExI is a combination of the RSI and "upper" Aroon. For the indicator to trigger, the RSI has to be above or below a top/bottom trigger line when the Aroon has had a set number of drives up or down correspondingly. An Aroon top drive is defined as the Aroon hitting 100% on the current candle when the previous candle was below 100%. An Aroon bottom drive is defined as the Aroon hitting 0% on the current candle when the previous candle was above 0%. Consecutive top or bottom drives are counted and exhaustion triggers when these drives hit a setpoint (default is 5 drives = the Aroon exhaustion trigger). When Aroon exhaustion is triggered and the RSI is correspondingly above/below a trigger line, the overall indicator signals exhaustion. There are two lines for bottoms and tops, one each for a "normal" trigger and and an "extreme" trigger.

The Aroon drives are visualized at the top and bottom of the indicator. The RSI is plotted as a line that crosses top and bottom trigger lines. There are extreme trigger values for both the bottom and top exhaustion triggers.

--Da_Prof

EMA Range OscillatorEMA Range Oscillator (ERO) - User Guide

Overview

The EMA Range Oscillator (ERO) is a technical indicator that measures the distance between two Exponential Moving Averages (EMAs) and the distance between price and EMA. It normalizes these distances into a 0-100 range, helping traders identify trend strength, market momentum, and potential reversal points.

Components

Main Line

Green Line: EMA20 > EMA50 (Uptrend)

Red Line: EMA20 < EMA50 (Downtrend)

Histogram

White Histogram: Price distance from EMA20

Key Levels

Upper Level (80): High divergence zone

Middle Level (50): Neutral zone

Lower Level (20): Low divergence zone

Parameters

ParameterDefaultDescriptionFast EMA20Short-term EMA periodSlow EMA50Long-term EMA periodNormalization Period100Lookback period for scalingUpper80Upper threshold levelLower20Lower threshold level

How to Read the Indicator

High Values (Above 80)

Strong trend in progress

EMAs are widely separated

High momentum

Potential overbought/oversold conditions

Watch for possible trend exhaustion

Low Values (Below 20)

Consolidation phase

EMAs are close together

Low volatility

Potential breakout setup

Range-bound market conditions

Middle Zone (20-80)

Normal market conditions

Moderate trend strength

Balanced momentum

Look for directional clues from color changes

cd_RSI_Divergence_CxGeneral:

The Relative Strength Index (RSI) is a momentum oscillator widely used by traders in price analysis. In addition to showing overbought/oversold zones, divergences between RSI and price are also tracked to identify trading opportunities.

The general consensus is that oscillators alone are not sufficient for entries and should be evaluated together with multiple confirmations.

This oscillator is designed as an additional confirmation/compatible tool for strategies that already use higher time frame (HTF) sweeps and lower time frame (LTF) confirmations such as Change in State Delivery (CISD) or Change of Character (CHOCH).

Features:

While RSI oscillators are commonly displayed in line format (classic), this indicator also offers candlestick-style visualization.

Depending on the selected source, period length, and EMA length, RSI can be displayed as lines and/or candlesticks.

Divergence detection & tracking:

Price and RSI values are monitored on the chosen higher time frame (from the menu) to determine highs and lows. For divergence display, the user can choose between two modes:

1- Alignment with HTF Sweep

2- All

1 - Alignment with HTF Sweep:

First, the price must sweep the previous high/low of the candle on the HTF (i.e., break it) but fail to continue in that direction and return inside (sweep).

If this condition is met, RSI values are checked:

If price makes a high sweep but RSI fails to make a new high → divergence is confirmed.

If price makes a low sweep but RSI fails to make a new low → divergence is confirmed.

Divergence is then displayed on the chart.

2 - All:

In this mode, sweep conditions are ignored. Divergence is confirmed if:

Price makes a new high on HTF but RSI does not.

RSI makes a new high on HTF but price does not.

Price makes a new low on HTF but RSI does not.

RSI makes a new low on HTF but price does not.

Menu & Settings:

RSI visualization (source + period length + EMA period length)

Option to choose classic/candlestick style display

Color customization

Higher time frame selection

Adjustable HTF boxes and table display

Final notes:

This oscillator is designed as an additional confirmation tool for strategies based on HTF sweep + LTF CISD/CHOCH confirmation logic. The chosen HTF in the oscillator should match the time frame where sweeps are expected.

Divergence signals from this oscillator alone will not make you profitable.

For spot trades, monitoring sweeps and divergences on higher time frames is more suitable (e.g., Daily–H1 / Weekly–H4).

My personal usage preferences:

Entry TF: 3m

HTF bias: Daily + H1

Sweep + CISD: 30m / 3m

Market Structure: 3m

RSI divergence: HTF = 30m

If all of them align bullish or bearish ( timeframe alignment ), I try to take the trade.

I’d be glad to hear your feedback and suggestions for improvement.

Happy trading!

Dual Stochastic with Trend FilterThe "Dual Stochastic with Trend Filter" is an oscillator indicator designed to provide clearer, trend-aligned trading signals. It uses two distinct stochastic oscillators to identify potential entry points and incorporates an optional EMA-based trend filter to ensure that you are trading in the direction of the broader market momentum.

How It Works and How to Use It

This indicator combines two key technical analysis concepts: momentum (via stochastics) and trend (via moving averages).

Core Components:

Dual Stochastic Oscillators:

Signal Line 1 (Blue): A standard stochastic oscillator.

Signal Line 2 (Red): A second stochastic oscillator, often using a different source (like hlcc4) to provide a smoother, more reliable signal.

A buy signal is generated when the Blue Line (d1) crosses above the Red Line (d2).

A sell signal is generated when the Blue Line (d1) crosses below the Red Line (d2).

Trend Filter (Optional):

This feature uses a fast and a slow Exponential Moving Average (EMA) to determine the overall market trend.

When the fast EMA is above the slow EMA, the background will turn green, indicating an uptrend.

When the fast EMA is below the slow EMA, the background will turn red, indicating a downtrend.

This filter can be toggled on or off in the indicator settings.

How to Use:

With Trend Filter Enabled (Recommended):

Long (Buy) Entry: Look for a green triangle buy signal (▲). This signal only appears when:

The Blue Signal Line crosses above the Red Signal Line.

The market is in a confirmed uptrend (green background).

Short (Sell) Entry: Look for a red triangle sell signal (▼). This signal only appears when:

The Blue Signal Line crosses below the Red Signal Line.

The market is in a confirmed downtrend (red background).

Exit Signal:

A yellow circle (●) appears to suggest closing an open trade. This signal is triggered for a long position if either the stochastics have a bearish cross or the trend flips to a downtrend. Conversely, for a short position, it's triggered by a bullish stochastic cross or a trend flip to an uptrend.

With Trend Filter Disabled:

If you turn off the "Use Trend Filter" option, the indicator will function as a simple dual stochastic crossover system.

A green triangle (▲) will appear every time the Blue Line crosses above the Red Line.

A red triangle (▼) will appear every time the Blue Line crosses below the Red Line.

The background coloring and exit signals based on trend flips will be deactivated. This mode is more sensitive but may produce more false signals in choppy markets.

Key Visuals:

Blue Line: The primary signal line.

Red Line: The secondary, often smoother, signal line.

Green Triangle (▲): Bullish entry signal.

Red Triangle (▼): Bearish entry signal.

Yellow Circle (●): Suggested trade exit/stop.

Green/Red Background: Visual confirmation of the current uptrend or downtrend.

By filtering stochastic signals with the dominant trend, this indicator helps traders avoid common pitfalls like entering short positions during a strong uptrend or buying into a bearish market. This alignment of momentum and trend is key to improving signal quality.

Disclaimer

This indicator is provided for educational and informational purposes only and should not be considered as financial advice or a recommendation to buy or sell any asset. All trading and investment decisions are your own sole responsibility.

Trading financial markets involves a high level of risk, and you may lose more than your initial investment. Past performance is not indicative of future results. The signals generated by this indicator are not guaranteed to be accurate, and you should always use this tool in conjunction with other forms of analysis and sound risk management practices.

Before using this indicator in a live trading environment, it is strongly recommended that you backtest it thoroughly and practice with it on a demo account. The author is not responsible for any financial losses you may incur from using this script.

BTC Dominance & Price RSI Analyzer by Sajad BagheriThis indicator analyzes the Relative Strength Index (RSI) for three key cryptocurrency metrics:

Bitcoin Price (BTC/USDT)

Bitcoin Dominance (BTC.D)

Tether Dominance (USDT.D)

It provides a comprehensive view of market momentum by displaying three RSI lines in a single pane, allowing traders to identify overbought and oversold conditions across these important metrics simultaneously.

Constance Brown Composite Index EnhancedWhat This Indicator Does

Implements Constance Brown's copyrighted Composite Index formula (1996) from her Master's thesis - a breakthrough oscillator that solves the critical problem where RSI fails to show divergences in long-horizon trends, providing early warning signals for major market reversals.

The Problem It Solves

Traditional RSI frequently fails to display divergence signals in Global Equity Indexes and long-term charts, leaving asset managers without warning of major price reversals. Brown's research showed RSI failed to provide divergence signals 42 times across major markets - failures that would have been "extremely costly for asset managers."

Key Components

Composite Line: RSI Momentum (9-period) + Smoothed RSI Average - the core breakthrough formula

Fast/Slow Moving Averages: Trend direction confirmation (13/33 periods default)

Bollinger Bands: Volatility envelope around the composite signal

Enhanced Divergence Detection: Significantly improved trend reversal timing vs standard RSI

Research-Proven Performance

Based on Brown's extensive study across 6 major markets (1919-2015):

42 divergence signals triggered where RSI showed none

33 signals passed with meaningful reversals (78% success rate)

Only 5 failures - exceptional performance in monthly/2-month timeframes

Tested on: German DAX, French CAC 40, Shanghai Composite, Dow Jones, US/Japanese Government Bonds

New Customization Features

Moving Average Types: Choose SMA or EMA for fast/slow lines

Optional Fills: Toggle composite and Bollinger band fills on/off

All Periods Adjustable: RSI length, momentum, smoothing periods

Visual Styling: Customize colors and line widths in Style tab

Default Settings (Original Formula)

RSI Length: 14

RSI Momentum: 9 periods

RSI MA Length: 3

SMA Length: 3

Fast SMA: 13, Slow SMA: 33

Bollinger STD: 2.0

Applications

Long-term investing: Monthly/2-month charts for major trend changes

Elliott Wave analysis: Maximum displacement at 3rd-of-3rd waves, divergence at 5th waves

Multi-timeframe: Pairs well with MACD, works across all timeframes

Global markets: Proven effective on equities, bonds, currencies, commodities

Perfect for serious traders and asset managers seeking the proven mathematical edge that traditional RSI cannot provide.

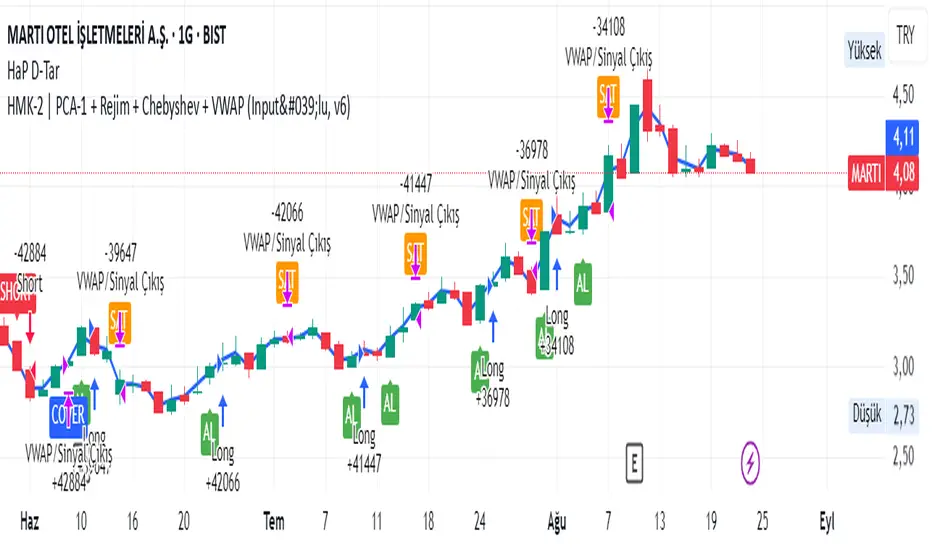

HMK-2 | PCA-1 + Rejim + Chebyshev + VWAP (Input'lu, v6)📌 HMK-2 | PCA-1 + Regime + Chebyshev + VWAP Strategy

1️⃣ Core Structure

Instead of relying on a single indicator, this system uses the Z-Score normalized average of three oscillators (RSI, MFI, ROC).

Signal (PCA-1):

RSI(14), MFI(14), ROC(5) → each is converted into a z-score.

Their average becomes the “composite signal,” our PCA-1 value.

Trend direction: If the Z-score EMA is rising → trend UP. If falling → trend DOWN.

2️⃣ Side Filters

Regime Filter (ADX + EMA)

ADX is calculated manually.

If ADX > 20 → trend exists → a 50-period EMA of this value smooths it.

This turns “trend regime” into a probability between 0–1.

Chebyshev Filter

A return series is checked against mean ± k*sigma bands.

If the return is within this band → valid signal. Extreme moves are filtered out.

VWAP Filter

Long trades: price must be above VWAP.

Short trades: price must be below VWAP.

Trades are only taken on the correct side of institutional cost averages.

3️⃣ Entry Conditions

Long:

PCA-1 signal crosses above threshold.

Trend Up + Regime OK + Chebyshev OK + Above VWAP.

Short:

PCA-1 signal crosses below threshold.

Trend Down + Regime OK + Chebyshev OK + Below VWAP.

4️⃣ Exit Mechanism

Main Exit: ATR-based stop/target.

Stop = entry price – ATR × (SL factor).

Take profit = entry price + ATR × (TP factor).

Additional Exit:

If price crosses to the opposite side of VWAP.

If PCA-1 signal crosses zero.

👉 Prevents trades from being locked, makes exits adaptive.

5️⃣ Labels / Visualization

AL / SHORT → entry points.

SAT / COVER → exit points.

VWAP line plotted in blue.

🧩 Strategy Features

Optimizable parameters:

Z-window (zWin)

Threshold

Chebyshev factor

ATR stop/target multipliers

This system works with:

Disciplined core (PCA-1 signal)

Triple protection (Regime + Chebyshev + VWAP)

Adaptive exits (ATR + VWAP/signal cross)

👉 Not a “single-indicator robot,” but a multi-filtered trade direction engine.

💡 Final Note

This is a base model of the system — open for further development.

I’ve shared the logic to give you a roadmap.

If you spot errors, fix them → that’s how you’ll improve it.

Don’t waste time asking me questions — refine and build it better yourselves.

Wishing you profitable trades. Stay well 🙏

Relative Weighted Rate of Change (WROC) vs Nifty 50Relative Weighted Rate of Change (WROC) vs Nifty 50

Donchian Squeeze Oscillator# Donchian Squeeze Oscillator (DSO) - User Guide

## Overview

The Donchian Squeeze Oscillator is a technical indicator designed to identify periods of low volatility (squeeze) and high volatility (expansion) in financial markets by measuring the distance between Donchian Channel bands. The indicator normalizes this measurement to a 0-100 scale, making it easy to interpret across different timeframes and instruments.

## How It Works

The DSO calculates the width of Donchian Channels as a percentage of the middle line, smooths this data, and then normalizes it using historical highs and lows over a specified lookback period. The result is inverted so that:

- **High values (80+)** = Narrow channels = Low volatility = Squeeze

- **Low values (20-)** = Wide channels = High volatility = Expansion

## Key Parameters

### Core Settings

- **Donchian Channel Period (20)**: The number of bars used to calculate the highest high and lowest low for the Donchian Channels

- **Smoothing Period (5)**: Applies moving average smoothing to reduce noise in the oscillator

- **Normalization Lookback (200)**: Historical period used to normalize the oscillator between 0-100

### Threshold Levels

- **Over Squeeze (80)**: Values above this level indicate strong squeeze conditions

- **Over Expansion (20)**: Values below this level indicate strong expansion conditions

## Reading the Indicator

### Color Coding

- **Red Line**: Squeeze condition (above 80 threshold) - Markets are consolidating

- **Orange Line**: Neutral/trending condition with upward momentum

- **Green Line**: Expansion condition or downward momentum

### Visual Elements

- **Red Dashed Line (80)**: Squeeze threshold - potential breakout zone

- **Gray Dotted Line (50)**: Middle line - neutral zone

- **Green Dashed Line (20)**: Expansion threshold - high volatility zone

- **Red Background**: Highlights active squeeze periods

## Trading Applications

### 1. Breakout Trading

- **Setup**: Wait for DSO to reach 80+ (squeeze zone)

- **Entry**: Look for breakouts when DSO starts declining from squeeze levels

- **Logic**: Prolonged low volatility often precedes significant price movements

### 2. Volatility Cycle Trading

- **Squeeze Phase**: DSO > 80 - Prepare for potential breakout

- **Breakout Phase**: DSO declining from 80 - Trade the direction of breakout

- **Expansion Phase**: DSO < 20 - Expect trend continuation or reversal

### 3. Trend Confirmation

- **Orange Color**: Suggests bullish momentum during expansion

- **Green Color**: Suggests bearish momentum or consolidation

- Use in conjunction with price action for trend confirmation

## Best Practices

### Timeframe Selection

- **Higher Timeframes (Daily, 4H)**: More reliable signals, fewer false breakouts

- **Lower Timeframes (1H, 15M)**: More frequent signals but higher noise

- **Multi-timeframe Analysis**: Confirm squeeze on higher TF, enter on lower TF

### Parameter Optimization

- **Volatile Markets**: Increase Donchian period (25-30) and smoothing (7-10)

- **Range-bound Markets**: Decrease Donchian period (15-20) for more sensitivity

- **Trending Markets**: Use longer normalization lookback (300-400)

### Signal Confirmation

Always combine DSO signals with:

- **Price Action**: Support/resistance levels, chart patterns

- **Volume**: Confirm breakouts with increasing volume

- **Other Indicators**: RSI, MACD, or momentum oscillators

## Alert System

The indicator includes built-in alerts for:

- **Squeeze Started**: When DSO crosses above the squeeze threshold

- **Expansion Started**: When DSO crosses below the expansion threshold

## Common Pitfalls to Avoid

1. **False Breakouts**: Don't trade every squeeze - wait for confirmation

2. **Parameter Over-optimization**: Stick to default settings initially

3. **Ignoring Market Context**: Consider overall market conditions and news

4. **Single Indicator Reliance**: Always use additional confirmation tools

## Advanced Tips

- Monitor squeeze duration - longer squeezes often lead to bigger moves

- Look for squeeze patterns at key support/resistance levels

- Use DSO divergences with price for potential reversal signals

- Combine with Bollinger Band squeezes for enhanced accuracy

## Conclusion

The Donchian Squeeze Oscillator is a powerful tool for identifying volatility cycles and potential breakout opportunities. Like all technical indicators, it should be used as part of a comprehensive trading strategy rather than as a standalone signal generator. Practice with the indicator on historical data before implementing it in live trading to understand its behavior in different market conditions.

EMA Oscillator [Alpha Extract]A precision mean reversion analysis tool that combines advanced Z-score methodology with dual threshold systems to identify extreme price deviations from trend equilibrium. Utilizing sophisticated statistical normalization and adaptive percentage-based thresholds, this indicator provides high-probability reversal signals based on standard deviation analysis and dynamic range calculations with institutional-grade accuracy for systematic counter-trend trading opportunities.

🔶 Advanced Statistical Normalization

Calculates normalized distance between price and exponential moving average using rolling standard deviation methodology for consistent interpretation across timeframes. The system applies Z-score transformation to quantify price displacement significance, ensuring statistical validity regardless of market volatility conditions.

// Core EMA and Oscillator Calculation

ema_values = ta.ema(close, ema_period)

oscillator_values = close - ema_values

rolling_std = ta.stdev(oscillator_values, ema_period)

z_score = oscillator_values / rolling_std

🔶 Dual Threshold System

Implements both statistical significance thresholds (±1σ, ±2σ, ±3σ) and percentage-based dynamic thresholds calculated from recent oscillator range extremes. This hybrid approach ensures consistent probability-based signals while adapting to varying market volatility regimes and maintaining signal relevance during structural market changes.

// Statistical Thresholds

mild_threshold = 1.0 // ±1σ (68% confidence)

moderate_threshold = 2.0 // ±2σ (95% confidence)

extreme_threshold = 3.0 // ±3σ (99.7% confidence)

// Percentage-Based Dynamic Thresholds

osc_high = ta.highest(math.abs(z_score), lookback_period)

mild_pct_thresh = osc_high * (mild_pct / 100.0)

moderate_pct_thresh = osc_high * (moderate_pct / 100.0)

extreme_pct_thresh = osc_high * (extreme_pct / 100.0)

🔶 Signal Generation Framework

Triggers buy/sell alerts when Z-score crosses extreme threshold boundaries, indicating statistically significant price deviations with high mean reversion probability. The system generates continuation signals at moderate levels and reversal signals at extreme boundaries with comprehensive alert integration.

// Extreme Signal Detection

sell_signal = ta.crossover(z_score, selected_extreme)

buy_signal = ta.crossunder(z_score, -selected_extreme)

// Dynamic Color Coding

signal_color = z_score >= selected_extreme ? #ff0303 : // Extremely Overbought

z_score >= selected_moderate ? #ff6a6a : // Overbought

z_score >= selected_mild ? #b86456 : // Mildly Overbought

z_score > -selected_mild ? #a1a1a1 : // Neutral

z_score > -selected_moderate ? #01b844 : // Mildly Oversold

z_score > -selected_extreme ? #00ff66 : // Oversold

#00ff66 // Extremely Oversold

🔶 Visual Structure Analysis

Provides a six-tier color gradient system with dynamic background zones indicating mild, moderate, and extreme conditions. The histogram visualization displays Z-score intensity with threshold reference lines and zero-line equilibrium context for precise mean reversion timing.

snapshot

4H

1D

🔶 Adaptive Threshold Selection

Features intelligent threshold switching between statistical significance levels and percentage-based dynamic ranges. The percentage system automatically adjusts to current volatility conditions using configurable lookback periods, while statistical thresholds maintain consistent probability-based signal generation across market cycles.

🔶 Performance Optimization

Utilizes efficient rolling calculations with configurable EMA periods and threshold parameters for optimal performance across all timeframes. The system includes comprehensive alert functionality with customizable notification preferences and visual signal overlay options.

🔶 Market Oscillator Interpretation

Z-score > +3σ indicates statistically significant overbought conditions with high reversal probability, while Z-score < -3σ signals extreme oversold levels suitable for counter-trend entries. Moderate thresholds (±2σ) capture 95% of normal price distributions, making breaches statistically significant for systematic trading approaches.

snapshot

🔶 Intelligent Signal Management

Automatic signal filtering prevents false alerts through extreme threshold crossover requirements, while maintaining sensitivity to genuine statistical deviations. The dual threshold system provides both conservative statistical approaches and adaptive market condition responses for varying trading styles.

Why Choose EMA Oscillator ?

This indicator provides traders with statistically-grounded mean reversion analysis through sophisticated Z-score normalization methodology. By combining traditional statistical significance thresholds with adaptive percentage-based extremes, it maintains effectiveness across varying market conditions while delivering high-probability reversal signals based on quantifiable price displacement from trend equilibrium, enabling systematic counter-trend trading approaches with defined statistical confidence levels and comprehensive risk management parameters.

Reverse RSI Signals [AlgoAlpha]🟠 OVERVIEW

This script introduces the Reverse RSI Signals system, an original approach that inverts traditional RSI values back into price levels and then overlays them directly on the chart as dynamic bands. Instead of showing RSI in a subwindow, the script calculates the exact price thresholds that correspond to common RSI levels (30/70/50) and displays them as upper, lower, and midline bands. These are further enhanced with an adaptive Supertrend filter and divergence detection, allowing traders to see overbought/oversold zones translated into actionable price ranges and trend signals. The script combines concepts of RSI inversion, volatility envelopes, and divergence tracking to provide a context-driven tool for spotting reversals and regime shifts.

🟠 CONCEPTS

The script relies on inverting RSI math: by solving for the price that would yield a given RSI level, it generates real chart levels tied to oscillator conditions. These RSI-derived price bands act like support/resistance, adapting each bar as RSI changes. On top of this, a Supertrend built around the RSI midline introduces directional bias, switching regimes when the midline is breached. Regular bullish and bearish divergences are detected by comparing RSI pivots against price pivots, highlighting early reversal conditions. This layered approach means the indicator is not just RSI on price but a hybrid of oscillator translation, volatility-tracking midline envelopes, and divergence analysis.

🟠 FEATURES

Inverted RSI bands: upper (70), lower (30), and midline (50), smoothed with EMA for noise reduction.

Supertrend overlay on the RSI midline to confirm regime direction (bullish or bearish).

Gradient-filled zones between outer and inner RSI bands to visualize proximity and exhaustion.

Non-repainting bullish and bearish divergence markers plotted directly on chart highs/lows.

🟠 USAGE

Apply the indicator to any chart and use the plotted RSI price bands as adaptive support/resistance. The midline defines equilibrium, while upper and lower bands represent classic RSI thresholds translated into real price action. In bullish regimes (green candles), long trades are stronger when price approaches or bounces from the lower band; in bearish regimes (red candles), shorts are favored near the upper band. Divergence markers (▲ for bullish, ▼ for bearish) flag potential reversal points early. Traders can combine the band proximity, divergence alerts, and Supertrend context to time entries, exits, or to refine ongoing trend trades. Adjust smoothing and Supertrend ATR settings to match the volatility of the instrument being analyzed.

ATAI Volume Pressure Analyzer V 1.0 — Pure Up/DownATAI Volume Pressure Analyzer V 1.0 — Pure Up/Down

Overview

Volume is a foundational tool for understanding the supply–demand balance. Classic charts show only total volume and don’t tell us what portion came from buying (Up) versus selling (Down). The ATAI Volume Pressure Analyzer fills that gap. Built on Pine Script v6, it scans a lower timeframe to estimate Up/Down volume for each host‑timeframe candle, and presents “volume pressure” in a compact HUD table that’s comparable across symbols and timeframes.

1) Architecture & Global Settings

Global Period (P, bars)

A single global input P defines the computation window. All measures—host‑TF volume moving averages and the half‑window segment sums—use this length. Default: 55.

Timeframe Handling

The core of the indicator is estimating Up/Down volume using lower‑timeframe data. You can set a custom lower timeframe, or rely on auto‑selection:

◉ Second charts → 1S

◉ Intraday → 1 minute

◉ Daily → 5 minutes

◉ Otherwise → 60 minutes

Lower TFs give more precise estimates but shorter history; higher TFs approximate buy/sell splits but provide longer history. As a rule of thumb, scan thin symbols at 5–15m, and liquid symbols at 1m.

2) Up/Down Volume & Derived Series

The script uses TradingView’s library function tvta.requestUpAndDownVolume(lowerTf) to obtain three values:

◉ Up volume (buyers)

◉ Down volume (sellers)

◉ Delta (Up − Down)

From these we define:

◉ TF_buy = |Up volume|

◉ TF_sell = |Down volume|

◉ TF_tot = TF_buy + TF_sell

◉ TF_delta = TF_buy − TF_sell

A positive TF_delta indicates buyer dominance; a negative value indicates selling pressure. To smooth noise, simple moving averages of TF_buy and TF_sell are computed over P and used as baselines.

3) Key Performance Indicators (KPIs)

Half‑window segmentation

To track momentum shifts, the P‑bar window is split in half:

◉ C→B: the older half

◉ B→A: the newer half (toward the current bar)

For each half, the script sums buy, sell, and delta. Comparing the two halves reveals strengthening/weakening pressure. Example: if AtoB_delta < CtoB_delta, recent buying pressure has faded.

[ 4) HUD (Table) Display /i]

Colors & Appearance

Two main color inputs define the theme: a primary color and a negative color (used when Δ is negative). The panel background uses a translucent version of the primary color; borders use the solid primary color. Text defaults to the primary color and flips to the negative color when a block’s Δ is negative.

Layout

The HUD is a 4×5 table updated on the last bar of each candle:

◉ Row 1 (Meta): indicator name, P length, lower TF, host TF

◉ Row 2 (Host TF): current ↑Buy, ↓Sell, ΔDelta; plus Σ total and SMA(↑/↓)

◉ Row 3 (Segments): C→B and B→A blocks with ↑/↓/Δ

◉ Rows 4–5: reserved for advanced modules (Wings, α/β, OB/OS, Top

5) Advanced Modules

5.1 Wings

“Wings” visualize volume‑driven movement over C→B (left wing) and B→A (right wing) with top/bottom lines and a filled band. Slopes are ATR‑per‑bar normalized for cross‑symbol/TF comparability and converted to angles (degrees). Coloring mirrors HUD sign logic with a near‑zero threshold (default ~3°):

◉ Both lines rising → blue (bullish)

◉ Both falling → red (bearish)

◉ Mixed/near‑zero → gray

Left wing reflects the origin of the recent move; right wing reflects the current state.

5.2 α / β at Point B

We compute the oriented angle between the two wings at the midpoint B:

β is the bottom‑arc angle; α = 360° − β is the top‑arc angle.

◉ Large α (>180°) or small β (<180°) flags meaningful imbalance.

◉ Intuition: large α suggests potential selling pressure; small β implies fragile support. HUD cells highlight these conditions.

5.3 OB/OS Spike

OverBought/OverSold (OB/OS) labels appear when directional volume spikes align with a 7‑oscillator vote (RSI, Stoch, %R, CCI, MFI, DeMarker, StochRSI).

◉ OB label (red): unusually high sell volume + enough OB votes

◉ OS label (teal): unusually high buy volume + enough OS votes

Minimum votes and sync window are user‑configurable; dotted connectors can link labels to the candle wick.

5.4 Top3 Volume Peaks

Within the P window the script ranks the top three BUY peaks (B1–B3) and top three SELL peaks (S1–S3).

◉ B1 and S1 are drawn as horizontal resistance (at B1 High) and support (at S1 Low) zones with adjustable thickness (ticks/percent/ATR).

◉ The HUD dedicates six cells to show ↑/↓/Δ for each rank, and prints the exact High (B1) and Low (S1) inline in their cells.

6) Reading the HUD — A Quick Checklist

◉ Meta: Confirm P and both timeframes (host & lower).

◉ Host TF block: Compare current ↑/↓/Δ against their SMAs.

◉ Segments: Contrast C→B vs B→A deltas to gauge momentum change.

◉ Wings: Right‑wing color/angle = now; left wing = recent origin.

◉ α / β: Look for α > 180° or β < 180° as imbalance cues.

◉ OB/OS: Note labels, color (red/teal), and the vote count.

◉Top3: Keep B1 (resistance) and S1 (support) on your radar.

Use these together to sketch scenarios and invalidation levels; never rely on a single signal in isolation.

[ 7) Example Highlights (What the table conveys) /i]

◉ Row 1 shows the indicator name, the analysis length P (default 55), and both TFs used for computation and display.

◉ B1 / S1 blocks summarize each side’s peak within the window, with Δ indicating buyer/seller dominance at that peak and inline price (B1 High / S1 Low) for actionable levels.

◉ Angle cells for each wing report the top/bottom line angles vs. the horizontal, reflecting the directional posture.

◉ Ranks B2/B3 and S2/S3 extend context beyond the top peak on each side.

◉ α / β cells quantify the orientation gap at B; changes reflect shifting buyer/seller influence on trend strength.

Together these visuals often reveal whether the “wings” resemble a strong, upward‑tilted arm supported by buyer volume—but always corroborate with your broader toolkit

8) Practical Tips & Tuning

◉ Choose P by market structure. For daily charts, 34–89 bars often works well.

◉ Lower TF choice: Thin symbols → 5–15m; liquid symbols → 1m.

◉ Near‑zero angle: In noisy markets, consider 5–7° instead of 3°.

◉ OB/OS votes: Daily charts often work with 3–4 votes; lower TFs may prefer 4–5.

◉ Zone thickness: Tie B1/S1 zone thickness to ATR so it scales with volatility.

◉ Colors: Feel free to theme the primary/negative colors; keep Δ<0 mapped to the negative color for readability.

Combine with price action: Use this indicator alongside structure, trendlines, and other tools for stronger decisions.

Technical Notes

Pine Script v6.

◉ Up/Down split via TradingView/ta library call requestUpAndDownVolume(lowerTf).

◉ HUD‑first design; drawings for Wings/αβ/OBOS/Top3 align with the same sign/threshold logic used in the table.

Disclaimer: This indicator is provided solely for educational and analytical purposes. It does not constitute financial advice, nor is it a recommendation to buy or sell any security. Always conduct your own research and use multiple tools before making trading decisions.

Advanced Trend Momentum [Alpha Extract]The Advanced Trend Momentum indicator provides traders with deep insights into market dynamics by combining exponential moving average analysis with RSI momentum assessment and dynamic support/resistance detection. This sophisticated multi-dimensional tool helps identify trend changes, momentum divergences, and key structural levels, offering actionable buy and sell signals based on trend strength and momentum convergence.

🔶 CALCULATION

The indicator processes market data through multiple analytical methods:

Dual EMA Analysis: Calculates fast and slow exponential moving averages with dynamic trend direction assessment and ATR-normalized strength measurement.

RSI Momentum Engine: Implements RSI-based momentum analysis with enhanced overbought/oversold detection and momentum velocity calculations.

Pivot-Based Structure: Identifies and tracks dynamic support and resistance levels using pivot point analysis with configurable level management.

Signal Integration: Combines trend direction, momentum characteristics, and structural proximity to generate high-probability trading signals.

Formula:

Fast EMA = EMA(Close, Fast Length)

Slow EMA = EMA(Close, Slow Length)

Trend Direction = Fast EMA > Slow EMA ? 1 : -1

Trend Strength = |Fast EMA - Slow EMA| / ATR(Period) × 100

RSI Momentum = RSI(Close, RSI Length)

Momentum Value = Change(Close, 5) / ATR(10) × 100

Pivot Support/Resistance = Dynamic pivot arrays with configurable lookback periods

Bullish Signal = Trend Change + Momentum Confirmation + Strength > 1%

Bearish Signal = Trend Change + Momentum Confirmation + Strength > 1%

🔶 DETAILS

Visual Features:

Trend EMAs: Fast and slow exponential moving averages with dynamic color coding (bullish/bearish)

Enhanced RSI: RSI oscillator with color-coded zones, gradient fills, and reference bands at overbought/oversold levels

Trend Fill: Dynamic gradient between EMAs indicating trend strength and direction

Support/Resistance Lines: Horizontal levels extending from pivot-based calculations with configurable maximum levels

Momentum Candles: Color-coded candlestick overlay reflecting combined trend and momentum conditions

Divergence Markers: Diamond-shaped signals highlighting bullish and bearish momentum divergences

Analysis Table: Real-time summary of trend direction, strength percentage, RSI value, and momentum reading

Interpretation:

Trend Direction: Bullish when Fast EMA crosses above Slow EMA with strength confirmation

Trend Strength > 1%: Strong trending conditions with institutional participation

RSI > 70: Overbought conditions, potential selling opportunity

RSI < 30: Oversold conditions, potential buying opportunity

Momentum Divergence: Price and momentum moving opposite directions signal potential reversals

Support/Resistance Proximity: Dynamic levels provide optimal entry/exit zones

Combined Signals: Trend changes with momentum confirmation generate high-probability opportunities

🔶 EXAMPLES

Trend Confirmation: Fast EMA crossing above Slow EMA with trend strength exceeding 1% and positive momentum confirms strong bullish conditions.

Example: During institutional accumulation phases, EMA crossovers with momentum confirmation have historically preceded significant upward moves, providing optimal long entry points.

15min

4H

Momentum Divergence Detection: RSI reaching overbought levels while momentum decreases despite rising prices signals potential trend exhaustion.

Example: Bearish divergence signals appearing at resistance levels have marked major market tops, allowing traders to secure profits before corrections.

Support/Resistance Integration: Dynamic pivot-based levels combined with trend and momentum signals create high-probability trading zones.

Example: Bullish trend changes occurring near established support levels offer optimal risk-reward entries with clearly defined stop-loss levels.

Multi-Dimensional Confirmation: The indicator's combination of trend, momentum, and structural analysis provides comprehensive market validation.

Example: When trend direction aligns with momentum characteristics near key structural levels, the confluence creates institutional-grade trading opportunities with enhanced probability of success.

🔶 SETTINGS

Customization Options:

Trend Analysis: Fast EMA Length (default: 12), Slow EMA Length (default: 26), Trend Strength Period (default: 14)

Support & Resistance: Pivot Length for level detection (default: 10), Maximum S/R Levels displayed (default: 3), Toggle S/R visibility

Momentum Settings: RSI Length (default: 14), Oversold Level (default: 30), Overbought Level (default: 70)

Visual Configuration: Color schemes for bullish/bearish/neutral conditions, transparency settings for fills, momentum candle overlay toggle

Display Options: Analysis table visibility, divergence marker size, alert system configuration

The Advanced Trend Momentum indicator provides traders with comprehensive insights into market dynamics through its sophisticated integration of trend analysis, momentum assessment, and structural level detection. By combining multiple analytical dimensions into a unified framework, this tool helps identify high-probability opportunities while filtering out market noise through its multi-confirmation approach, enabling traders to make informed decisions across various market cycles and timeframes.