Trend Volatility Index (TVI)Trend Volatility Index (TVI)

A robust nonparametric oscillator for structural trend volatility detection

⸻

What is this?

TVI is a volatility oscillator designed to measure the strength and emergence of price trends using nonparametric statistics.

It calculates a U-statistic based on the Gini mean difference across multiple simple moving averages.

This allows for objective, robust, and unbiased quantification of trend volatility in tick-scale values.

⸻

What can it do?

• Quantify trend strength as a continuous value aligned with tick price scale

• Detect trend breakouts and volatility expansions

• Identify range-bound market states

• Detect early signs of new trends with minimal lag

⸻

What can’t it do?

• Predict future price levels

• Predict trend direction before confirmation

⸻

How it works

TVI computes a nonparametric dispersion metric (Gini mean difference) from multiple SMAs of different lengths.

As this metric shares the same dimension as price ticks, it can be directly interpreted on the chart as a volatility gauge.

The output is plotted using candlestick-style charts to enhance visibility of change rate and trend behavior.

⸻

Disclaimer

TVI does not predict price. It is a structural indicator designed to support discretionary judgment.

Trading carries inherent risk, and this tool does not guarantee profitability. Use at your own discretion.

⸻

Innovation

This indicator introduces a novel approach to trend volatility by applying U-statistics over time series

to produce a nonparametric, unbiased, and robust estimate of structural volatility.

日本語要約

Trend Volatility Index (TVI) は、ノンパラメトリックなU統計量(Gini平均差)を使ってトレンドの強度を客観的に測定することを目的に開発されたボラティリティ・オシレーターです。

ティック単位で連続的に変化し、トレンドのブレイク・レンジ・初動の予兆を定量的に検出します。

未来の価格や方向は予測せず、現在の構造的ばらつきだけをロバストに評価します。

지표 및 전략

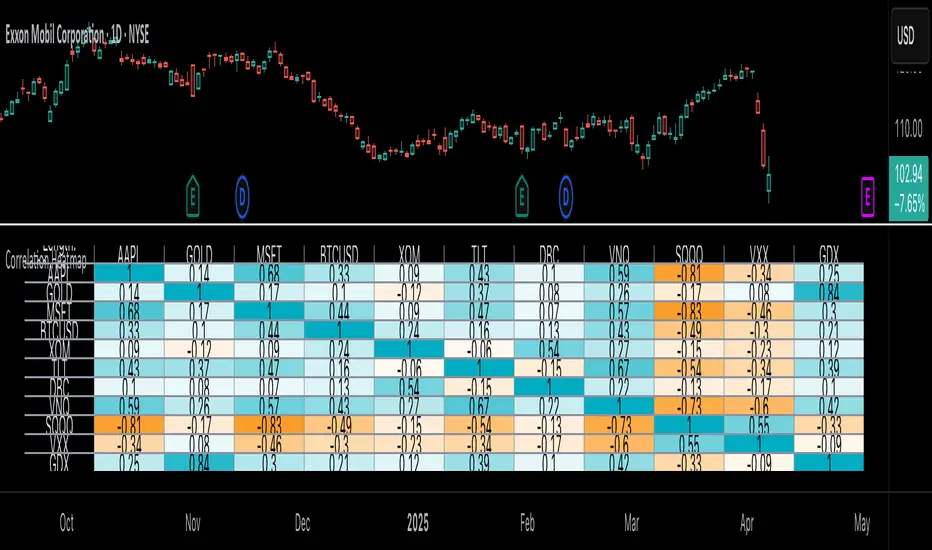

Cointegration Heatmap & Spread Table [EdgeTerminal]The Cointegration Heatmap is a powerful visual and quantitative tool designed to uncover deep, statistically meaningful relationships between assets.

Unlike traditional indicators that react to price movement, this tool analyzes the underlying statistical relationship between two time series and tracks when they diverge from their long-term equilibrium — offering actionable signals for mean-reversion trades .

What Is Cointegration?

Most traders are familiar with correlation, which measures how two assets move together in the short term. But correlation is shallow — it doesn’t imply a stable or predictable relationship over time.

Cointegration, however, is a deeper statistical concept: Two assets are cointegrated if a linear combination of their prices or returns is stationary , even if the individual series themselves are non-stationary.

Cointegration is a foundational concept in time series analysis, widely used by hedge funds, proprietary trading firms, and quantitative researchers. This indicator brings that institutional-grade concept into an easy-to-use and fully visual TradingView indicator.

This tool helps answer key questions like:

“Which stocks tend to move in sync over the long term?”

“When are two assets diverging beyond statistical norms?”

“Is now the right time to short one and long the other?”

Using a combination of regression analysis, residual modeling, and Z-score evaluation, this indicator surfaces opportunities where price relationships are stretched and likely to snap back — making it ideal for building low-risk, high-probability trade setups.

In simple terms:

Cointegrated assets drift apart temporarily, but always come back together over time. This behavior is the foundation of successful pairs trading.

How the Indicator Works

Cointegration Heatmap indicator works across any market supported on TradingView — from stocks and ETFs to cryptocurrencies and forex pairs.

You enter your list of symbols, choose a timeframe, and the indicator updates every bar with live cointegration scores, spread signals, and trade-ready insights.

Indicator Settings:

Symbol list: a customizable list of symbols separated by commas

Returns timeframe: time frame selection for return sampling (Weekly or Monthly)

Max periods: max periods to limit the data to a certain time and to control indicator performance

This indicator accomplishes three major goals in one streamlined package:

Identifies stable long-term relationships (cointegration) between assets, using a heatmap visualization.

Tracks the spread — the difference between actual prices and the predicted linear relationship — between each pair.

Generates trade signals based on Z-score deviations from the mean spread, helping traders know when a pair is statistically overextended and likely to mean revert.

The math:

Returns are calculated using spread tickers to ensure alignment in time and adjust for dividends, splits, and other inconsistencies.

For each unique pair of symbols, we perform a linear regression

Yt=α+βXt+ε

Then we compute the residuals (errors from the regression):

Spreadt=Yt−(α+βXt)

Calculate the standard deviation of the spread over a moving window (default: 100 samples) and finally, define the Cointegration Score:

S=1/Standard Deviation of Residuals

This means, the lower the deviation, the tighter the relationship, so higher scores indicate stronger cointegration.

Always remember that cointegration can break down so monitor the asset over time and over multiple different timeframes before making a decision.

How to use the indicator

The heatmap table:

The indicator displays 2 very important tables, one in the middle and one on the right side. After entering your symbols, the first table to pay attention to is the middle heatmap table.

Any assets with a cointegration value of 25% is something to pay attention to and have a strong and stable relationship. Anything below is weak and not tradable.

Additionally, the 40% level is another important line to cross. Assets that have a cointegration score of over 40% will most likely have an extremely strong relationship.

Think about it this way, the higher the percentage, the tighter and more statistically reliable the relationship is.

The spread table:

After finding a good asset pair using heatmap, locate the same pair in the spread table (right side).

Here’s what you’ll see on the table:

Spread: Current difference between the two symbols based on the regression fit

Mean: Historical average of that spread

Z-score: How far current spread is from the mean in standard deviations

Signal: Trade suggestion: Short, Long, or Neutral

Since you’re expecting mean reversion, the idea is that the spread will return to the average. You want to take a trade when the z-score is either over +2 or below -2 and exit when z-score returns to near 0.

You will usually see the trade suggestion on the spread chart but you can make your own decision based on your risk level.

Keep in mind that the Z-score for each pair refers to how off the first asset is from the mean compared to the second one, so for example if you see STOCKA vs STOCKB with a Z-score of -1.55, we are regressing STOCKB (Y) on STOCKA (X).

In this case, STOCKB is the quoted asset and STOCKA is the base asset.

In this case, this means that STOCKB is much lower than expected relative to STOCKA, so the trade would be a long position on stock B and short position on stock A.

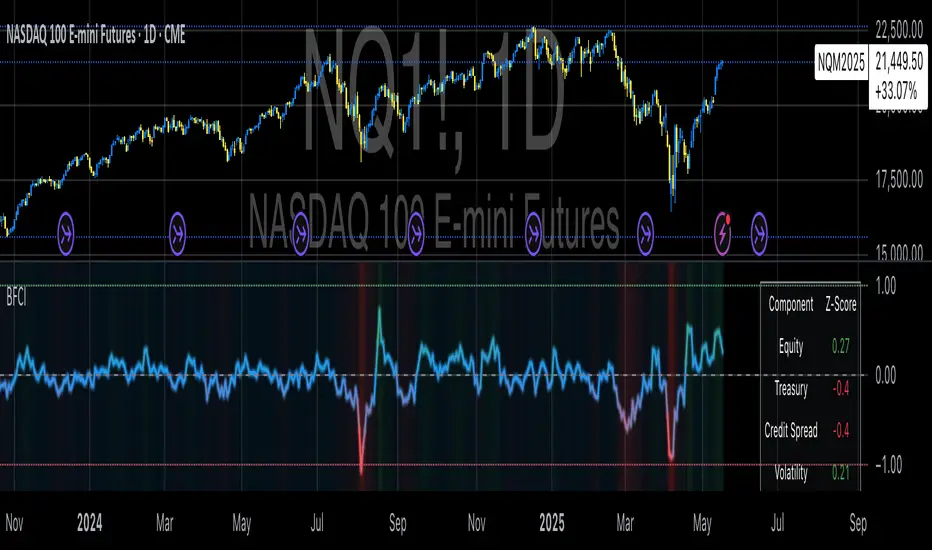

Bloomberg Financial Conditions Index (Proxy)The Bloomberg Financial Conditions Index (BFCI): A Proxy Implementation

Financial conditions indices (FCIs) have become essential tools for economists, policymakers, and market participants seeking to quantify and monitor the overall state of financial markets. Among these measures, the Bloomberg Financial Conditions Index (BFCI) has emerged as a particularly influential metric. Originally developed by Bloomberg L.P., the BFCI provides a comprehensive assessment of stress or ease in financial markets by aggregating various market-based indicators into a single, standardized value (Hatzius et al., 2010).

The original Bloomberg Financial Conditions Index synthesizes approximately 50 different financial market variables, including money market indicators, bond market spreads, equity market valuations, and volatility measures. These variables are normalized using a Z-score methodology, weighted according to their relative importance to overall financial conditions, and then aggregated to produce a composite index (Carlson et al., 2014). The resulting measure is centered around zero, with positive values indicating accommodative financial conditions and negative values representing tighter conditions relative to historical norms.

As Angelopoulou et al. (2014) note, financial conditions indices like the BFCI serve as forward-looking indicators that can signal potential economic developments before they manifest in traditional macroeconomic data. Research by Adrian et al. (2019) demonstrates that deteriorating financial conditions, as measured by indices such as the BFCI, often precede economic downturns by several months, making these indices valuable tools for predicting changes in economic activity.

Proxy Implementation Approach

The implementation presented in this Pine Script indicator represents a proxy of the original Bloomberg Financial Conditions Index, attempting to capture its essential features while acknowledging several significant constraints. Most critically, while the original BFCI incorporates approximately 50 financial variables, this proxy version utilizes only six key market components due to data accessibility limitations within the TradingView platform.

These components include:

Equity market performance (using SPY as a proxy for S&P 500)

Bond market yields (using TLT as a proxy for 20+ year Treasury yields)

Credit spreads (using the ratio between LQD and HYG as a proxy for investment-grade to high-yield spreads)

Market volatility (using VIX directly)

Short-term liquidity conditions (using SHY relative to equity prices as a proxy)

Each component is transformed into a Z-score based on log returns, weighted according to approximated importance (with weights derived from literature on financial conditions indices by Brave and Butters, 2011), and aggregated into a composite measure.

Differences from the Original BFCI

The methodology employed in this proxy differs from the original BFCI in several important ways. First, the variable selection is necessarily limited compared to Bloomberg's comprehensive approach. Second, the proxy relies on ETFs and publicly available indices rather than direct market rates and spreads used in the original. Third, the weighting scheme, while informed by academic literature, is simplified compared to Bloomberg's proprietary methodology, which may employ more sophisticated statistical techniques such as principal component analysis (Kliesen et al., 2012).

These differences mean that while the proxy BFCI captures the general direction and magnitude of financial conditions, it may not perfectly replicate the precision or sensitivity of the original index. As Aramonte et al. (2013) suggest, simplified proxies of financial conditions indices typically capture broad movements in financial conditions but may miss nuanced shifts in specific market segments that more comprehensive indices detect.

Practical Applications and Limitations

Despite these limitations, research by Arregui et al. (2018) indicates that even simplified financial conditions indices constructed from a limited set of variables can provide valuable signals about market stress and future economic activity. The proxy BFCI implemented here still offers significant insight into the relative ease or tightness of financial conditions, particularly during periods of market stress when correlations among financial variables tend to increase (Rey, 2015).

In practical applications, users should interpret this proxy BFCI as a directional indicator rather than an exact replication of Bloomberg's proprietary index. When the index moves substantially into negative territory, it suggests deteriorating financial conditions that may precede economic weakness. Conversely, strongly positive readings indicate unusually accommodative financial conditions that might support economic expansion but potentially also signal excessive risk-taking behavior in markets (López-Salido et al., 2017).

The visual implementation employs a color gradient system that enhances interpretation, with blue representing neutral conditions, green indicating accommodative conditions, and red signaling tightening conditions—a design choice informed by research on optimal data visualization in financial contexts (Few, 2009).

References

Adrian, T., Boyarchenko, N. and Giannone, D. (2019) 'Vulnerable Growth', American Economic Review, 109(4), pp. 1263-1289.

Angelopoulou, E., Balfoussia, H. and Gibson, H. (2014) 'Building a financial conditions index for the euro area and selected euro area countries: what does it tell us about the crisis?', Economic Modelling, 38, pp. 392-403.

Aramonte, S., Rosen, S. and Schindler, J. (2013) 'Assessing and Combining Financial Conditions Indexes', Finance and Economics Discussion Series, Federal Reserve Board, Washington, D.C.

Arregui, N., Elekdag, S., Gelos, G., Lafarguette, R. and Seneviratne, D. (2018) 'Can Countries Manage Their Financial Conditions Amid Globalization?', IMF Working Paper No. 18/15.

Brave, S. and Butters, R. (2011) 'Monitoring financial stability: A financial conditions index approach', Economic Perspectives, Federal Reserve Bank of Chicago, 35(1), pp. 22-43.

Carlson, M., Lewis, K. and Nelson, W. (2014) 'Using policy intervention to identify financial stress', International Journal of Finance & Economics, 19(1), pp. 59-72.

Few, S. (2009) Now You See It: Simple Visualization Techniques for Quantitative Analysis. Analytics Press, Oakland, CA.

Hatzius, J., Hooper, P., Mishkin, F., Schoenholtz, K. and Watson, M. (2010) 'Financial Conditions Indexes: A Fresh Look after the Financial Crisis', NBER Working Paper No. 16150.

Kliesen, K., Owyang, M. and Vermann, E. (2012) 'Disentangling Diverse Measures: A Survey of Financial Stress Indexes', Federal Reserve Bank of St. Louis Review, 94(5), pp. 369-397.

López-Salido, D., Stein, J. and Zakrajšek, E. (2017) 'Credit-Market Sentiment and the Business Cycle', The Quarterly Journal of Economics, 132(3), pp. 1373-1426.

Rey, H. (2015) 'Dilemma not Trilemma: The Global Financial Cycle and Monetary Policy Independence', NBER Working Paper No. 21162.

TASC 2025.06 Cybernetic Oscillator█ OVERVIEW

This script implements the Cybernetic Oscillator introduced by John F. Ehlers in his article "The Cybernetic Oscillator For More Flexibility, Making A Better Oscillator" from the June 2025 edition of the TASC Traders' Tips . It cascades two-pole highpass and lowpass filters, then scales the result by its root mean square (RMS) to create a flexible normalized oscillator that responds to a customizable frequency range for different trading styles.

█ CONCEPTS

Oscillators are indicators widely used by technical traders. These indicators swing above and below a center value, emphasizing cyclic movements within a frequency range. In his article, Ehlers explains that all oscillators share a common characteristic: their calculations involve computing differences . The reliance on differences is what causes these indicators to oscillate about a central point.

The difference between two data points in a series acts as a highpass filter — it allows high frequencies (short wavelengths) to pass through while significantly attenuating low frequencies (long wavelengths). Ehlers demonstrates that a simple difference calculation attenuates lower-frequency cycles at a rate of 6 dB per octave. However, the difference also significantly amplifies cycles near the shortest observable wavelength, making the result appear noisier than the original series. To mitigate the effects of noise in a differenced series, oscillators typically smooth the series with a lowpass filter, such as a moving average.

Ehlers highlights an underlying issue with smoothing differenced data to create oscillators. He postulates that market data statistically follows a pink spectrum , where the amplitudes of cyclic components in the data are approximately directly proportional to the underlying periods. Specifically, he suggests that cyclic amplitude increases by 6 dB per octave of wavelength.

Because some conventional oscillators, such as RSI, use differencing calculations that attenuate cycles by only 6 dB per octave, and market cycles increase in amplitude by 6 dB per octave, such calculations do not have a tangible net effect on larger wavelengths in the analyzed data. The influence of larger wavelengths can be especially problematic when using these oscillators for mean reversion or swing signals. For instance, an expected reversion to the mean might be erroneous because oscillator's mean might significantly deviate from its center over time.

To address the issues with conventional oscillator responses, Ehlers created a new indicator dubbed the Cybernetic Oscillator. It uses a simple combination of highpass and lowpass filters to emphasize a specific range of frequencies in the market data, then normalizes the result based on RMS. The process is as follows:

Apply a two-pole highpass filter to the data. This filter's critical period defines the longest wavelength in the oscillator's passband.

Apply a two-pole SuperSmoother (lowpass filter) to the highpass-filtered data. This filter's critical period defines the shortest wavelength in the passband.

Scale the resulting waveform by its RMS. If the filtered waveform follows a normal distribution, the scaled result represents amplitude in standard deviations.

The oscillator's two-pole filters attenuate cycles outside the desired frequency range by 12 dB per octave. This rate outweighs the apparent rate of amplitude increase for successively longer market cycles (6 dB per octave). Therefore, the Cybernetic Oscillator provides a more robust isolation of cyclic content than conventional oscillators. Best of all, traders can set the periods of the highpass and lowpass filters separately, enabling fine-tuning of the frequency range for different trading styles.

█ USAGE

The "Highpass period" input in the "Settings/Inputs" tab specifies the longest wavelength in the oscillator's passband, and the "Lowpass period" input defines the shortest wavelength. The oscillator becomes more responsive to rapid movements with a smaller lowpass period. Conversely, it becomes more sensitive to trends with a larger highpass period. Ehlers recommends setting the smallest period to a value above 8 to avoid aliasing. The highpass period must not be smaller than the lowpass period. Otherwise, it causes a runtime error.

The "RMS length" input determines the number of bars in the RMS calculation that the indicator uses to normalize the filtered result.

This indicator also features two distinct display styles, which users can toggle with the "Display style" input. With the "Trend" style enabled, the indicator plots the oscillator with one of two colors based on whether its value is above or below zero. With the "Threshold" style enabled, it plots the oscillator as a gray line and highlights overbought and oversold areas based on the user-specified threshold.

Below, we show two instances of the script with different settings on an equities chart. The first uses the "Threshold" style with default settings to pass cycles between 20 and 30 bars for mean reversion signals. The second uses a larger highpass period of 250 bars and the "Trend" style to visualize trends based on cycles spanning less than one year:

Dynamic Volume Clusters with Retest Signals (Zeiierman)█ Overview

The Dynamic Volume Clusters with Retest Signals indicator is designed to detect key Volume Clusters and provide Retest Signals. This tool is specifically engineered for traders looking to capitalize on volume-based trends, reversals, and key price retest points.

The indicator seamlessly combines volume analysis, dynamic cluster calculations, and retest signal logic to present a comprehensive trading framework. It adapts to market conditions, identifying clusters of volume activity and signaling when the price retests critical zones.

█ How It Works

⚪ Volume Cluster Detection

The indicator dynamically calculates volume clusters by analyzing the highest and lowest price points within a specified lookback period.

Cluster Logic:

Bright Lines (Strong Red/Green):

These indicate that the price has frequently revisited these levels, creating a dense cluster.

Such areas serve as support or resistance, where significant historical trading has occurred, often acting as barriers to price movement.

Traders should consider these levels as potential reversal zones or consolidation points.

Faded or Darker Lines:

These lines indicate areas where the price has less historical activity, suggesting weaker clustering.

These zones have less market memory and are more likely to break, supporting trend continuation and rapid price movement.

⚪ Candle Color Logic (Market Memory)

Blue Candles (High Cluster Density):

Candles turn blue when the price has revisited a particular area many times.

This signals a highly clustered zone, likely to act as a barrier, creating consolidation or range phases.

These areas indicate strong market memory, potentially rejecting price attempts to break through.

Green or Red Candles (Low Cluster Density):

Once the price breaks out of these dense clusters, the candles turn green (bullish) or red (bearish).

This suggests the price has moved into a less clustered territory, where the path forward is clearer and trends are likely to extend without immediate resistance.

⚪ Retest Signal Logic

The indicator identifies critical retest points where the price crosses a cluster boundary and then reverses. These points are essential for traders looking to catch continuation or reversal setups.

⚪ Dynamic Price Clustering

The indicator dynamically adapts the clustering logic based on price movement and volume shifts.

Uses a dynamic moving average (VPMA) to maintain adaptive cluster levels.

Integrates a Kalman Filter for smoothing, reducing noise, and improving trend clarity.

Automatically updates as new data is received, keeping the clusters relevant in real-time.

█ How to Use

⚪ Trend Following & Reversal Detection

Use Retest signals to identify potential trend continuation or reversal points.

⚪ Trading Volume Clusters and Market Memory

Identify Key Zones:

Focus on bright, saturated cluster lines (strong red or green) as they indicate high market memory, where price has spent significant time in the past.

These zones are likely to exhibit a more choppy market. Apply range or mean reversion strategies.

Spot Potential Breakouts:

Faded or darker cluster lines indicate areas of low market memory, where the price has moved quickly and spent less time.

Use these areas to identify possible trend setups, as they represent lower resistance to price movement.

⚪ Interpreting Candle Colors for Market Phases

Blue Candles (High Cluster Density):

When candles turn blue, it signals that the price has revisited this area multiple times, creating a dense cluster.

These zones often trap price movement, leading to consolidations or range phases.

Use these areas as caution zones, where price can slow down or reverse.

Green or Red Candles (Low Cluster Density):

Once the price breaks out of these clustered zones, the candles turn green (bullish) or red (bearish), indicating lower market memory.

This signals a trend initiation with less immediate resistance, ideal for momentum and breakout trades.

Use these signals to identify emerging trends and ride the momentum.

█ Settings

Range Lookback Period: Sets the number of bars for calculating the range.

Zone Width (% of Range): Determines how wide the volume clusters are relative to the calculated range.

Volume Line Colors: Customize the appearance of bullish and bearish lines.

Retest Signals: Toggle the appearance of Triangle Up/Down retest markers.

Minimum Bars for Retest: Define the minimum number of bars required before a retest is valid.

Maximum Bars for Retest: Set the maximum number of bars within which a retest can occur.

Price Cluster Period: Adjusts the sensitivity of the dynamic clustering logic.

Cluster Confirmation: Controls how tightly the clusters respond to price action.

Price Cluster Start/Peak: Sets the minimum and maximum touches required to fully form a cluster.

-----------------

Disclaimer

The content provided in my scripts, indicators, ideas, algorithms, and systems is for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or a solicitation to buy or sell any financial instruments. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

Multi-Layer Volume Profile [BigBeluga]A powerful multi-resolution volume analysis tool that stacks multiple profiles of historical trading activity to reveal true market structure.

This indicator breaks down total and delta volume distribution across time at four adjustable depths — enabling traders to spot major POCs, volume shelves, and zones of price acceptance or rejection with unmatched clarity.

🔵 KEY FEATURES

Multi-Layer Volume Profiles:

Up to 4 separate volume profiles are stacked on the chart:

- Profile 1: Full period

- Profile 2: Half-length

- Profile 3: Quarter-length

- Profile 4: One-eighth-length

This layering helps traders assess confluence across different time horizons.

Custom Bin Resolution:

Each profile uses a customizable number of bins to control visual precision.

More bins = higher granularity, fewer bins = smoother profile.

Precise POC Highlighting:

The price level with the maximum traded volume in each profile is highlighted with a thick blue POC line.

This key level shows the most accepted price for each period.

Total and Delta Volume Labels:

- Total Volume: Displays cumulative volume over the profile period at the top of the profile box.

- Delta Volume: The difference between bullish and bearish volume is labeled at the base, showing directional pressure.

Positive delta = buyer dominance, negative delta = seller dominance.

Range Levels:

Each profile includes horizontal reference lines showing its high, low, bounds.

These edges often align with price reaction zones and become future resistance/support.

🔵 HOW IT WORKS

For each active profile, the indicator:

- Collects price range (highs/lows) across the selected `length`

- Divides this range into equal bins

- Assigns volume into bins based on candle close location

- Aggregates volume per bin to form the profile (polylines)

Separately tracks:

- Total volume (sum of all candles in range)

- Delta volume (sum of candle volumes: positive for bullish, negative for bearish closes)

Highlights the bin with maximum volume (POC)

and marks it with a thick blue line.

Adds auxiliary lines for high/low of each profile box

and total/delta volume tags with tooltips.

🔵 USAGE

Spot Acceptance Zones:

Thick, flat areas on the profile show where price stayed longest — ideal for building positions.

Identify Rejection Zones:

Thin volume areas signal price rejection and are often used for stop placement or entries.

Delta Confirmation:

Use strong positive/negative delta readings as directional bias confirmation for breakout trades.

Confluence Detection:

Watch for overlapping POCs between layers to identify extremely strong support/resistance zones.

🔵 CONCLUSION

Multi-Layer Volume Profile equips traders with a deeply layered market structure view.

Whether you're scalping intraday levels or analyzing macro support zones, the ability to stack volume perspectives, visualize directional delta, and anchor POCs provides an edge in anticipating market moves.

Use this tool to validate entries, confirm structure, and make more informed, volume-aware trading decisions.

pymath█ OVERVIEW

This library ➕ enhances Pine Script's built-in types (`float`, `int`, `array`, `array`) with mathematical methods, mirroring 🪞 many functions from Python's `math` module. Import this library to overload or add to built-in capabilities, enabling calls like `myFloat.sin()` or `myIntArray.gcd()`.

█ CONCEPTS

This library wraps Pine's built-in `math.*` functions and implements others where necessary, expanding the mathematical toolkit available within Pine Script. It provides a more object-oriented approach to mathematical operations on core data types.

█ HOW TO USE

• Import the library: i mport kaigouthro/pymath/1

• Call methods directly on variables: myFloat.sin() , myIntArray.gcd()

• For raw integer literals, you MUST use parentheses: `(1234).factorial()`.

█ FEATURES

• **Infinity Handling:** Includes `isinf()` and `isfinite()` for robust checks. Uses `POS_INF_PROXY` to represent infinity.

• **Comprehensive Math Functions:** Implements a wide range of methods, including trigonometric, logarithmic, hyperbolic, and array operations.

• **Object-Oriented Approach:** Allows direct method calls on `int`, `float`, and arrays for cleaner code.

• **Improved Accuracy:** Some functions (e.g., `remainder()`) offer improved accuracy compared to default Pine behavior.

• **Helper Functions:** Internal helper functions optimize calculations and handle edge cases.

█ NOTES

This library improves upon Pine Script's built-in `math` functions by adding new ones and refining existing implementations. It handles edge cases such as infinity, NaN, and zero values, enhancing the reliability of your Pine scripts. For Speed, it wraps and uses built-ins, as thy are fastest.

█ EXAMPLES

//@version=6

indicator("My Indicator")

// Import the library

import kaigouthro/pymath/1

// Create some Vars

float myFloat = 3.14159

int myInt = 10

array myIntArray = array.from(1, 2, 3, 4, 5)

// Now you can...

plot( myFloat.sin() ) // Use sin() method on a float, using built in wrapper

plot( (myInt).factorial() ) // Factorial of an integer (note parentheses)

plot( myIntArray.gcd() ) // GCD of an integer array

method isinf(self)

isinf: Checks if this float is positive or negative infinity using a proxy value.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) value to check.

Returns: (bool) `true` if the absolute value of `self` is greater than or equal to the infinity proxy, `false` otherwise.

method isfinite(self)

isfinite: Checks if this float is finite (not NaN and not infinity).

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The value to check.

Returns: (bool) `true` if `self` is not `na` and not infinity (as defined by `isinf()`), `false` otherwise.

method fmod(self, divisor)

fmod: Returns the C-library style floating-point remainder of `self / divisor` (result has the sign of `self`).

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) Dividend `x`.

divisor (float) : (float) Divisor `y`. Cannot be zero or `na`.

Returns: (float) The remainder `x - n*y` where n is `trunc(x/y)`, or `na` if divisor is 0, `na`, or inputs are infinite in a way that prevents calculation.

method factorial(self)

factorial: Calculates the factorial of this non-negative integer.

Namespace types: series int, simple int, input int, const int

Parameters:

self (int) : (int) The integer `n`. Must be non-negative.

Returns: (float) `n!` as a float, or `na` if `n` is negative or overflow occurs (based on `isinf`).

method isqrt(self)

isqrt: Calculates the integer square root of this non-negative integer (floor of the exact square root).

Namespace types: series int, simple int, input int, const int

Parameters:

self (int) : (int) The non-negative integer `n`.

Returns: (int) The greatest integer `a` such that a² <= n, or `na` if `n` is negative.

method comb(self, k)

comb: Calculates the number of ways to choose `k` items from `self` items without repetition and without order (Binomial Coefficient).

Namespace types: series int, simple int, input int, const int

Parameters:

self (int) : (int) Total number of items `n`. Must be non-negative.

k (int) : (int) Number of items to choose. Must be non-negative.

Returns: (float) The binomial coefficient nCk, or `na` if inputs are invalid (n<0 or k<0), `k > n`, or overflow occurs.

method perm(self, k)

perm: Calculates the number of ways to choose `k` items from `self` items without repetition and with order (Permutations).

Namespace types: series int, simple int, input int, const int

Parameters:

self (int) : (int) Total number of items `n`. Must be non-negative.

k (simple int) : (simple int = na) Number of items to choose. Must be non-negative. Defaults to `n` if `na`.

Returns: (float) The number of permutations nPk, or `na` if inputs are invalid (n<0 or k<0), `k > n`, or overflow occurs.

method log2(self)

log2: Returns the base-2 logarithm of this float. Input must be positive. Wraps `math.log(self) / math.log(2.0)`.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The input number. Must be positive.

Returns: (float) The base-2 logarithm, or `na` if input <= 0.

method trunc(self)

trunc: Returns this float with the fractional part removed (truncates towards zero).

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The input number.

Returns: (int) The integer part, or `na` if input is `na` or infinite.

method abs(self)

abs: Returns the absolute value of this float. Wraps `math.abs()`.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The input number.

Returns: (float) The absolute value, or `na` if input is `na`.

method acos(self)

acos: Returns the arccosine of this float, in radians. Wraps `math.acos()`. Input must be between -1 and 1.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The input number. Must be between -1 and 1.

Returns: (float) Angle in radians , or `na` if input is outside or `na`.

method asin(self)

asin: Returns the arcsine of this float, in radians. Wraps `math.asin()`. Input must be between -1 and 1.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The input number. Must be between -1 and 1.

Returns: (float) Angle in radians , or `na` if input is outside or `na`.

method atan(self)

atan: Returns the arctangent of this float, in radians. Wraps `math.atan()`.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The input number.

Returns: (float) Angle in radians , or `na` if input is `na`.

method ceil(self)

ceil: Returns the ceiling of this float (smallest integer >= self). Wraps `math.ceil()`.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The input number.

Returns: (int) The ceiling value, or `na` if input is `na` or infinite.

method cos(self)

cos: Returns the cosine of this float (angle in radians). Wraps `math.cos()`.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The angle in radians.

Returns: (float) The cosine, or `na` if input is `na`.

method degrees(self)

degrees: Converts this float from radians to degrees. Wraps `math.todegrees()`.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The angle in radians.

Returns: (float) The angle in degrees, or `na` if input is `na`.

method exp(self)

exp: Returns e raised to the power of this float. Wraps `math.exp()`.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The exponent.

Returns: (float) `e**self`, or `na` if input is `na`.

method floor(self)

floor: Returns the floor of this float (largest integer <= self). Wraps `math.floor()`.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The input number.

Returns: (int) The floor value, or `na` if input is `na` or infinite.

method log(self)

log: Returns the natural logarithm (base e) of this float. Wraps `math.log()`. Input must be positive.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The input number. Must be positive.

Returns: (float) The natural logarithm, or `na` if input <= 0 or `na`.

method log10(self)

log10: Returns the base-10 logarithm of this float. Wraps `math.log10()`. Input must be positive.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The input number. Must be positive.

Returns: (float) The base-10 logarithm, or `na` if input <= 0 or `na`.

method pow(self, exponent)

pow: Returns this float raised to the power of `exponent`. Wraps `math.pow()`.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The base.

exponent (float) : (float) The exponent.

Returns: (float) `self**exponent`, or `na` if inputs are `na` or lead to undefined results.

method radians(self)

radians: Converts this float from degrees to radians. Wraps `math.toradians()`.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The angle in degrees.

Returns: (float) The angle in radians, or `na` if input is `na`.

method round(self)

round: Returns the nearest integer to this float. Wraps `math.round()`. Ties are rounded away from zero.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The input number.

Returns: (int) The rounded integer, or `na` if input is `na` or infinite.

method sign(self)

sign: Returns the sign of this float (-1, 0, or 1). Wraps `math.sign()`.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The input number.

Returns: (int) -1 if negative, 0 if zero, 1 if positive, `na` if input is `na`.

method sin(self)

sin: Returns the sine of this float (angle in radians). Wraps `math.sin()`.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The angle in radians.

Returns: (float) The sine, or `na` if input is `na`.

method sqrt(self)

sqrt: Returns the square root of this float. Wraps `math.sqrt()`. Input must be non-negative.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The input number. Must be non-negative.

Returns: (float) The square root, or `na` if input < 0 or `na`.

method tan(self)

tan: Returns the tangent of this float (angle in radians). Wraps `math.tan()`.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The angle in radians.

Returns: (float) The tangent, or `na` if input is `na`.

method acosh(self)

acosh: Returns the inverse hyperbolic cosine of this float. Input must be >= 1.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The input number. Must be >= 1.

Returns: (float) The inverse hyperbolic cosine, or `na` if input < 1 or `na`.

method asinh(self)

asinh: Returns the inverse hyperbolic sine of this float.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The input number.

Returns: (float) The inverse hyperbolic sine, or `na` if input is `na`.

method atanh(self)

atanh: Returns the inverse hyperbolic tangent of this float. Input must be between -1 and 1 (exclusive).

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The input number. Must be between -1 and 1 (exclusive).

Returns: (float) The inverse hyperbolic tangent, or `na` if input is outside (-1, 1) or `na`.

method cosh(self)

cosh: Returns the hyperbolic cosine of this float.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The input number.

Returns: (float) The hyperbolic cosine, or `na` if input is `na`.

method sinh(self)

sinh: Returns the hyperbolic sine of this float.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The input number.

Returns: (float) The hyperbolic sine, or `na` if input is `na`.

method tanh(self)

tanh: Returns the hyperbolic tangent of this float.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The input number.

Returns: (float) The hyperbolic tangent, or `na` if input is `na`.

method atan2(self, dx)

atan2: Returns the angle in radians between the positive x-axis and the point (dx, self). Wraps `math.atan2()`.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The y-coordinate `y`.

dx (float) : (float) The x-coordinate `x`.

Returns: (float) The angle in radians , result of `math.atan2(self, dx)`. Returns `na` if inputs are `na`. Note: `math.atan2(0, 0)` returns 0 in Pine.

Optimization: Use built-in math.atan2()

method cbrt(self)

cbrt: Returns the cube root of this float.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The value to find the cube root of.

Returns: (float) The real cube root. Handles negative inputs correctly, or `na` if input is `na`.

method exp2(self)

exp2: Returns 2 raised to the power of this float. Calculated as `2.0.pow(self)`.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The exponent.

Returns: (float) `2**self`, or `na` if input is `na` or results in non-finite value.

method expm1(self)

expm1: Returns `e**self - 1`. Calculated as `self.exp() - 1.0`. May offer better precision for small `self` in some environments, but Pine provides no guarantee over `self.exp() - 1.0`.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The exponent.

Returns: (float) `e**self - 1`, or `na` if input is `na` or `self.exp()` is `na`.

method log1p(self)

log1p: Returns the natural logarithm of (1 + self). Calculated as `(1.0 + self).log()`. Pine provides no specific precision guarantee for self near zero.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) Value to add to 1. `1 + self` must be positive.

Returns: (float) Natural log of `1 + self`, or `na` if input is `na` or `1 + self <= 0`.

method modf(self)

modf: Returns the fractional and integer parts of this float as a tuple ` `. Both parts have the sign of `self`.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The number `x` to split.

Returns: ( ) A tuple containing ` `, or ` ` if `x` is `na` or non-finite.

method remainder(self, divisor)

remainder: Returns the IEEE 754 style remainder of `self` with respect to `divisor`. Result `r` satisfies `abs(r) <= 0.5 * abs(divisor)`. Uses round-half-to-even.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) Dividend `x`.

divisor (float) : (float) Divisor `y`. Cannot be zero or `na`.

Returns: (float) The IEEE 754 remainder, or `na` if divisor is 0, `na`, or inputs are non-finite in a way that prevents calculation.

method copysign(self, signSource)

copysign: Returns a float with the magnitude (absolute value) of `self` but the sign of `signSource`.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) Value providing the magnitude `x`.

signSource (float) : (float) Value providing the sign `y`.

Returns: (float) `abs(x)` with the sign of `y`, or `na` if either input is `na`.

method frexp(self)

frexp: Returns the mantissa (m) and exponent (e) of this float `x` as ` `, such that `x = m * 2^e` and `0.5 <= abs(m) < 1` (unless `x` is 0).

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The number `x` to decompose.

Returns: ( ) A tuple ` `, or ` ` if `x` is 0, or ` ` if `x` is non-finite or `na`.

method isclose(self, other, rel_tol, abs_tol)

isclose: Checks if this float `a` and `other` float `b` are close within relative and absolute tolerances.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) First value `a`.

other (float) : (float) Second value `b`.

rel_tol (simple float) : (simple float = 1e-9) Relative tolerance. Must be non-negative and less than 1.0.

abs_tol (simple float) : (simple float = 0.0) Absolute tolerance. Must be non-negative.

Returns: (bool) `true` if `abs(a - b) <= max(rel_tol * max(abs(a), abs(b)), abs_tol)`. Handles `na`/`inf` appropriately. Returns `na` if tolerances are invalid.

method ldexp(self, exponent)

ldexp: Returns `self * (2**exponent)`. Inverse of `frexp`.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) Mantissa part `x`.

exponent (int) : (int) Exponent part `i`.

Returns: (float) The result of `x * pow(2, i)`, or `na` if inputs are `na` or result is non-finite.

method gcd(self)

gcd: Calculates the Greatest Common Divisor (GCD) of all integers in this array.

Namespace types: array

Parameters:

self (array) : (array) An array of integers.

Returns: (int) The largest positive integer that divides all non-zero elements, 0 if all elements are 0 or array is empty. Returns `na` if any element is `na`.

method lcm(self)

lcm: Calculates the Least Common Multiple (LCM) of all integers in this array.

Namespace types: array

Parameters:

self (array) : (array) An array of integers.

Returns: (int) The smallest positive integer that is a multiple of all non-zero elements, 0 if any element is 0, 1 if array is empty. Returns `na` on potential overflow or if any element is `na`.

method dist(self, other)

dist: Returns the Euclidean distance between this point `p` and another point `q` (given as arrays of coordinates).

Namespace types: array

Parameters:

self (array) : (array) Coordinates of the first point `p`.

other (array) : (array) Coordinates of the second point `q`. Must have the same size as `p`.

Returns: (float) The Euclidean distance, or `na` if arrays have different sizes, are empty, or contain `na`/non-finite values.

method fsum(self)

fsum: Returns an accurate floating-point sum of values in this array. Uses built-in `array.sum()`. Note: Pine Script does not guarantee the same level of precision tracking as Python's `math.fsum`.

Namespace types: array

Parameters:

self (array) : (array) The array of floats to sum.

Returns: (float) The sum of the array elements. Returns 0.0 for an empty array. Returns `na` if any element is `na`.

method hypot(self)

hypot: Returns the Euclidean norm (distance from origin) for this point given by coordinates in the array. `sqrt(sum(x*x for x in coordinates))`.

Namespace types: array

Parameters:

self (array) : (array) Array of coordinates defining the point.

Returns: (float) The Euclidean norm, or 0.0 if the array is empty. Returns `na` if any element is `na` or non-finite.

method prod(self, start)

prod: Calculates the product of all elements in this array.

Namespace types: array

Parameters:

self (array) : (array) The array of values to multiply.

start (simple float) : (simple float = 1.0) The starting value for the product (returned if the array is empty).

Returns: (float) The product of array elements * start. Returns `na` if any element is `na`.

method sumprod(self, other)

sumprod: Returns the sum of products of values from this array `p` and another array `q` (dot product).

Namespace types: array

Parameters:

self (array) : (array) First array of values `p`.

other (array) : (array) Second array of values `q`. Must have the same size as `p`.

Returns: (float) The sum of `p * q ` for all i, or `na` if arrays have different sizes or contain `na`/non-finite values. Returns 0.0 for empty arrays.

Best SMA FinderThis script, Best SMA Finder, is a tool designed to identify the most robust simple moving average (SMA) length for a given chart, based on historical backtest performance. It evaluates hundreds of SMA values (from 10 to 1000) and selects the one that provides the best balance between profitability, consistency, and trade frequency.

What it does:

The script performs individual backtests for each SMA length using either "Long Only" or "Buy & Sell" logic, as selected by the user. For each tested SMA, it computes:

- Total number of trades

- Profit Factor (total profits / total losses)

- Win Rate

- A composite Robustness Score, which integrates Profit Factor, number of trades (log-scaled), and win rate.

Only SMA configurations that meet the user-defined minimum trade count are considered valid. Among all valid candidates, the script selects the SMA length with the highest robustness score and plots it on the chart.

How to use it:

- Choose the strategy type: "Long Only" or "Buy & Sell"

- Set the minimum trade count to filter out statistically irrelevant results

- Enable or disable the summary stats table (default: enabled)

The selected optimal SMA is plotted on the chart in blue. The optional table in the top-right corner shows the corresponding SMA length, trade count, Profit Factor, Win Rate, and Robustness Score for transparency.

Key Features:

- Exhaustive SMA optimization across 991 values

- Customizable trade direction and minimum trade filters

- In-chart visualization of results via table and plotted optimal SMA

- Uses a custom robustness formula to rank SMA lengths

Use cases:

Ideal for traders who want to backtest and auto-select a historically effective SMA without manual trial-and-error. Useful for swing and trend-following strategies across different timeframes.

📌 Limitations:

- Not a full trading strategy with position sizing or stop-loss logic

- Only one entry per direction at a time is allowed

- Designed for exploration and optimization, not as a ready-to-trade system

This script is open-source and built entirely from original code and logic. It does not replicate any closed-source script or reuse significant external open-source components.

Bitcoin Monthly Seasonality [Alpha Extract]The Bitcoin Monthly Seasonality indicator analyzes historical Bitcoin price performance across different months of the year, enabling traders to identify seasonal patterns and potential trading opportunities. This tool helps traders:

Visualize which months historically perform best and worst for Bitcoin.

Track average returns and win rates for each month of the year.

Identify seasonal patterns to enhance trading strategies.

Compare cumulative or individual monthly performance.

🔶 CALCULATION

The indicator processes historical Bitcoin price data to calculate monthly performance metrics

Monthly Return Calculation

Inputs:

Monthly open and close prices.

User-defined lookback period (1-15 years).

Return Types:

Percentage: (monthEndPrice / monthStartPrice - 1) × 100

Price: monthEndPrice - monthStartPrice

Statistical Measures

Monthly Averages: ◦ Average return for each month calculated from historical data.

Win Rate: ◦ Percentage of positive returns for each month.

Best/Worst Detection: ◦ Identifies months with highest and lowest average returns.

Cumulative Option

Standard View: Shows discrete monthly performance.

Cumulative View: Shows compounding effect of consecutive months.

Example Calculation (Pine Script):

monthReturn = returnType == "Percentage" ?

(monthEndPrice / monthStartPrice - 1) * 100 :

monthEndPrice - monthStartPrice

calcWinRate(arr) =>

winCount = 0

totalCount = array.size(arr)

if totalCount > 0

for i = 0 to totalCount - 1

if array.get(arr, i) > 0

winCount += 1

(winCount / totalCount) * 100

else

0.0

🔶 DETAILS

Visual Features

Monthly Performance Bars: ◦ Color-coded bars (teal for positive, red for negative returns). ◦ Special highlighting for best (yellow) and worst (fuchsia) months.

Optional Trend Line: ◦ Shows continuous performance across months.

Monthly Axis Labels: ◦ Clear month names for easy reference.

Statistics Table: ◦ Comprehensive view of monthly performance metrics. ◦ Color-coded rows based on performance.

Interpretation

Strong Positive Months: Historically bullish periods for Bitcoin.

Strong Negative Months: Historically bearish periods for Bitcoin.

Win Rate Analysis: Higher win rates indicate more consistently positive months.

Pattern Recognition: Identify recurring seasonal patterns across years.

Best/Worst Identification: Quickly spot the historically strongest and weakest months.

🔶 EXAMPLES

The indicator helps identify key seasonal patterns

Bullish Seasons: Visualize historically strong months where Bitcoin tends to perform well, allowing traders to align long positions with favorable seasonality.

Bearish Seasons: Identify historically weak months where Bitcoin tends to underperform, helping traders avoid unfavorable periods or consider short positions.

Seasonal Strategy Development: Create trading strategies that capitalize on recurring monthly patterns, such as entering positions in historically strong months and reducing exposure during weak months.

Year-to-Year Comparison: Assess how current year performance compares to historical seasonal patterns to identify anomalies or confirmation of trends.

🔶 SETTINGS

Customization Options

Lookback Period: Adjust the number of years (1-15) used for historical analysis.

Return Type: Choose between percentage returns or absolute price changes.

Cumulative Option: Toggle between discrete monthly performance or cumulative effect.

Visual Style Options: Bar Display: Enable/disable and customize colors for positive/negative bars, Line Display: Enable/disable and customize colors for trend line, Axes Display: Show/hide reference axes.

Visual Enhancement: Best/Worst Month Highlighting: Toggle special highlighting of extreme months, Custom highlight colors for best and worst performing months.

The Bitcoin Monthly Seasonality indicator provides traders with valuable insights into Bitcoin's historical performance patterns throughout the year, helping to identify potentially favorable and unfavorable trading periods based on seasonal tendencies.

Market Manipulation Index (MMI)The Composite Manipulation Index (CMI) is a structural integrity tool that quantifies how chaotic or orderly current market conditions are, with the aim of detecting potentially manipulated or unstable environments. It blends two distinct mathematical models that assess price behavior in terms of both structural rhythm and predictability.

1. Sine-Fit Deviation Model:

This component assumes that ideal, low-manipulation price behavior resembles a smooth oscillation, such as a sine wave. It generates a synthetic sine wave using a user-defined period and compares it to actual price movement over an adaptive window. The error between the real price and this synthetic wave—normalized by price variance—forms the Sine-Based Manipulation Index. A high error indicates deviation from natural rhythm, suggesting structural disorder.

2. Predictability-Based Model:

The second component estimates how well current price can be predicted using recent price lags. A two-variable rolling linear regression is computed between the current price and two lagged inputs (close and close ). If the predicted price diverges from the actual price, this error—also normalized by price variance—reflects unpredictability. High prediction error implies a more manipulated or erratic environment.

3. Adaptive Mechanism:

Both components are calculated using an adaptive smoothing window based on the Average True Range (ATR). This allows the indicator to respond proportionally to market volatility. During high volatility, the analysis window expands to avoid over-sensitivity; during calm periods, it contracts for better responsiveness.

4. Composite Output:

The two normalized metrics are averaged to form the final CMI value, which is then optionally smoothed further. The output is scaled between 0 and 1:

0 indicates a highly structured, orderly market.

1 indicates complete structural breakdown or randomness.

Suggested Interpretation:

CMI < 0.3: Market is clean and structured. Trend-following or breakout strategies may perform better.

CMI > 0.7: Market is structurally unstable. Choppy price action, fakeouts, or manipulative behavior may dominate.

CMI 0.3–0.7: Transitional zone. Caution or reduced risk may be warranted.

This indicator is designed to serve as a contextual filter, helping traders assess whether current market conditions are conducive to structured strategies, or if discretion and defense are more appropriate.

Dual-Phase Trend Regime Oscillator (Zeiierman)█ Overview

Trend Regime: Dual-Phase Oscillator (Zeiierman) is a volatility-sensitive trend classification tool that dynamically switches between two oscillators, one optimized for low volatility, the other for high volatility.

By analyzing standard deviation-based volatility states and applying correlation-derived oscillators, this indicator reveals not only whether the market is trending but also what kind of trend regime it is in —Bullish or Bearish —and how that regime reacts to market volatility.

█ Its Uniqueness

Most trend indicators assume a static market environment; they don't adjust their logic when the underlying volatility shifts. That often leads to false signals in choppy conditions or late entries in trending phases.

Trend Regime: Dual-Phase Oscillator solves this by introducing volatility-aware adaptability. It switches between a slow, stable oscillator in calm markets and a fast, reactive oscillator in volatile ones, ensuring the right sensitivity at the right time.

█ How It Works

⚪ Volatility State Engine

Calculates returns-based volatility using standard deviation of price change

Smooths the current volatility with a moving average

Builds a volatility history window and performs median clustering to determine typical "Low" and "High" volatility zones

Dynamically assigns the chart to one of two internal volatility regimes: Low or High

⚪ Dual Oscillators

In Low Volatility, it uses a Slow Trend Oscillator (longer lookback, smoother)

In High Volatility, it switches to a Fast Trend Oscillator (shorter lookback, responsive)

Both oscillators use price-time correlation as a measure of directional strength

The output is normalized between 0 and 1, allowing for consistent interpretation

⚪ Trend Regime Classification

The active oscillator is compared to a neutral threshold (0.5)

If above: Bullish Regime, if below: Bearish Regime, else: Neutral

The background and markers update to reflect regime changes visually

Triangle markers highlight bullish/bearish regime shifts

█ How to Use

⚪ Identify Current Trend Regime

Use the background color and chart table to immediately recognize whether the market is trending up or down.

⚪ Trade Regime Shifts

Use triangle markers (▲ / ▼) to spot fresh regime entries, which are ideal for confirming breakouts within trends.

⚪ Pullback Trading

Look for pullbacks when the trend is in a stable condition and the slow oscillator remains consistently near the upper or lower threshold. Watch for moments when the fast oscillator retraces back toward the midline, or slightly above/below it — this often signals a potential pullback entry in the direction of the prevailing trend.

█ Settings Explained

Length (Slow Trend Oscillator) – Used in calm conditions. Longer = smoother signals

Length (Fast Trend Oscillator) – Used in volatile conditions. Shorter = more responsive

Volatility Refit Interval – Controls how often the system recalculates Low/High volatility levels

Current Volatility Period – Lookback used for immediate volatility measurement

Volatility Smoothing Length – Applies an SMA to the raw volatility to reduce noise

-----------------

Disclaimer

The content provided in my scripts, indicators, ideas, algorithms, and systems is for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or a solicitation to buy or sell any financial instruments. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

Nasan Risk Score & Postion Size Estimator** THE RISK SCORE AND POSITION SIZE WILL ONLY BE CALCUTAED ON DIALY TIMEFRAME NOT IN OTHER TIMEFRAMES.

The typically accepted generic rule for risk management is not to risk more than 1% - 2 % of the capital in any given trade. It has its own basis however it does not take into account the stocks historic & current performance and does not consider the traders performance metrics (like win rate, profit ratio).

The Nasan Risk Score & Position size calculator takes into account all the listed parameters into account and estimates a Risk %. The position size is calculated using the estimated risk % , current ATR and a dynamically adjusted ATR multiple (ATR multiple is adjusted based on true range's volatility and stocks relative performance).

It follows a series of calculations:

Unadjusted Nasan Risk Score = (Min Risk)^a + b*

Min Risk = ( 5 year weighted avg Annual Stock Return - 5 year weighted avg Annual Bench Return) / 5 year weighted avg Annual Max ATR%

Max Risk = ( 5 year weighted avg Annual Stock Return - 5 year weighted avg Annual Bench Return) / 5 year weighted avg Annual Min ATR%

The min and max return is calculated based on stocks excess return in comparison to the Benchmark return and adjusted for volatility of the stock.

When a stock underperforms the benchmark, the default is, it does not calculate a position size , however if we opt it to calculate it will use 1% for Min Risk% and 2% for Max Risk% but all the other calculations and scaling remain the same.

Rationale:

Stocks outperforming their benchmark with lower volatility (ATR%) score higher.

A stock with high returns but excessive volatility gets penalized.

This ensures volatility-adjusted performance is emphasized rather than absolute returns.

Depending on the risk preference aggressive or conservative

Aggressive Risk Scaling: a = max (m, n) and b = min (m, n)

Conservative Scaling: a = min (m, n) and b = max (m, n)

where n = traders win % /100 and m = 1 - (1/ (1+ profit ratio))

A default of 50% is used for win factor and 1.5 for profit ratio.

Aggressive risk scaling increases exposure when the strategy's strongest factor is favorable.

Conservative risk scaling ensures more stable risk levels by focusing on the weaker factor.

The Unadjusted Nasan risk is score is further refined based on a tolerance factor which is based on the stocks maximum annual drawdown and the trader's maximum draw down tolerance.

Tolerance = /100

The correction factor (Tolerance) adjusts the risk score based on downside risk. Here's how it works conceptually:

The formula calculates how much the stock's actual drawdown exceeds your acceptable limit.

If stocks maximum Annual drawdown is smaller than Trader's maximum acceptable drawdown % , this results in a positive correction factor (indicating the drawdown is within your acceptable range and increases the unadjusted score.

If stocks maximum Annual drawdown exceeds Trader's maximum acceptable drawdown %, the correction factor will decrease (indicating that the downside risk is greater than what you are comfortable with, so it will adjust the risk exposure).

Once the Risk Score (numerically equal to Risk %) The position size is calculated based on the current market conditions.

Nasan Risk Score (Risk%) = Unadjusted Nasan Risk Score * Tolerance.

Position Size = (Capital * Risk% )/ ATR-Multiplier * ATR

The ATR Multiplier is dynamically adjusted based on the stocks recent relative performance and the variability of the true range itself. It would range between 1 - 3.5.

The multiplier widens when conditions are not favorable decreasing the position size and increases position size when conditions are favorable.

This Calculation /Estimate Does not give you a very different result than the arbitrary 1% - 2%. However it does fine tune the % based on sock performance, traders performance and tolerance level.

NIG Probability TableNormal-Inverse Gaussian Probability Table

This indicator implements the Normal-Inverse Gaussian (NIG) distribution to estimate the likelihood of future price based on recent market behavior.

📊 Key Features:

- Estimates the parameters (α: tail heaviness, β: skewness, δ: scale, μ: location)

of the NIG distribution using a sliding window over log returns.

- Uses a numerically approximated version of the modified Bessel function (K₁)

to calculate the NIG probability density function (PDF).

- Normalizes the total probability across all bins to ensure the values are interpretable.

- Displays a dynamic probability table showing the chance of future returns falling into each bin.

⚠️ Notes:

- This is a real-time approximation. The Bessel function and posterior inference are simplified.

- Tail probabilities and shape parameters are sensitive to the window size and input settings.

- Useful for risk analysis, option overlays, and strategy filters.

Log-Normal Price ForecastLog-Normal Price Forecast

This Pine Script creates a log-normal forecast model of future price movements on a TradingView chart, based on historical log returns. It plots expected price trajectories and bands representing different levels of statistical deviation.

Parameters

Model Length – Number of bars used to calculate average and standard deviation of log returns (default: 100).

Forecast Length – Number of bars into the future for which the forecast is projected (default: 100, max: 500).

Volatility SMA Length – The smoothing length for the standard deviation (default: 20).

Confidence Intervals – Confidence intervals for price bands (default: 95%, 99%, 99.9%).

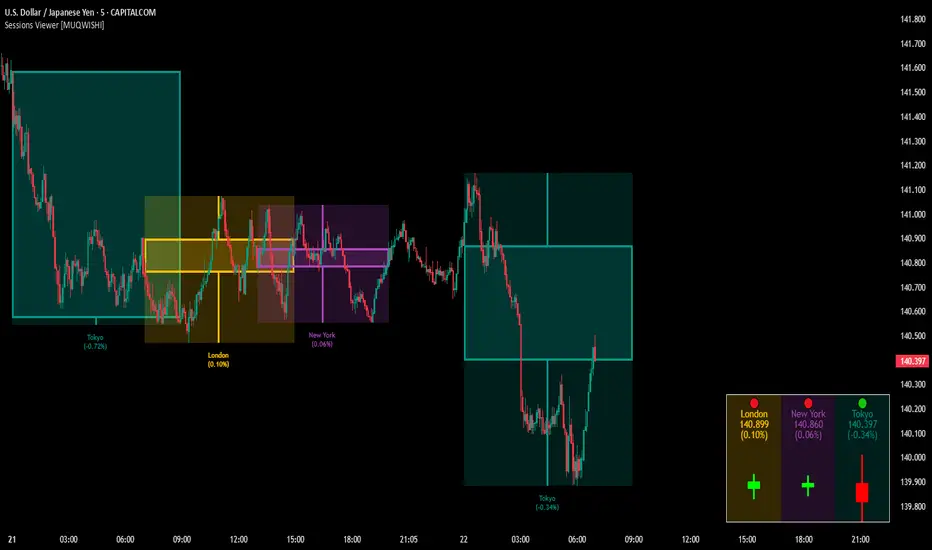

Market Sessions & Viewer Panel [By MUQWISHI]▋ INTRODUCTION :

The “Market Sessions & Viewer Panel” is a clean and intuitive visual indicator tool that highlights up to four trading sessions directly on the chart. Each session is fully customizable with its name, session time, and color. It also generates a panel that provides a quick-glance summary of each session’s candle/bar shape, helping traders gain insight into the volatility across all trading sessions.

_______________________

▋ OVERVIEW:

_______________________

▋ CREDIT:

This indicator utilizes the “ Timezone — Library ”. A huge thanks to @n00btraders for effort and well-organized work.

_______________________

▋ SESSION PANEL:

The Session Panel allows traders to visually compare session volatility using a candlestick/bar pattern.

Each bar represents the price action during a session and includes the session status, session name, closing price, change(%) from open, and a tooltip that reveals detailed OHLC and volume when hovered over.

Chart Type:

It offers two styles Bar or Candle to display based on traders’ preference

Sorting:

Allowing to arrange session candles/bars based on…

—Left to Right: The most recently opened on the left, moving backward in time to the right.

—Right to Left: The most recently opened on the right, moving backward in time to the left.

—Default: Arrange sessions in the user-defined input order.

_______________________

▋ CHART VISUALIZATION:

The chart visualization highlights each trading session using color-coded backgrounds in two selectable drawing styles that span their respective active timeframes. Each session block provides session’s name, close price, and change from open.

Chart Type: Candle

Chart Type: Box

Extra Drawing Feature:

This feature may not exist in other indicators within the same category, it extends the session block drawing to the projected end of the session. This's done through estimation based on historical data; however, it doesn’t function fully on seconds-based timeframes due to drawing limitations.

_______________________

▋ INDICATOR SETTINGS:

Section(1): Sessions

(1) Universal Timezone.

(2) Each Session: Enable/Disable, Name, Color, and Time.

Section(2): Session Panel

(1) Show/Hide Session Panel.

(2) Chart Type: Candle/Bar.

(3) Bar’s Up/Down color.

(4) Width and Height of the bar.

(5) Location of Session Panel on chat.

(6) Sort: Left to Right (most recent session is placed on the left), Right to Left (most recent session is placed on the right), and Default (as input arrangement).

Section(3): Chart Visualization

(1) Show/Hide Chart Block Visualization.

(2) Draw Shape: Box/Candle.

(3) Border Style and Size.

(4) Label Styling includes location, size, and some essential selectable infos.

Please let me know if you have any questions

Elastic Volume-Weighted Student-T TensionOverview

The Elastic Volume-Weighted Student-T Tension Bands indicator dynamically adapts to market conditions using an advanced statistical model based on the Student-T distribution. Unlike traditional Bollinger Bands or Keltner Channels, this indicator leverages elastic volume-weighted averaging to compute real-time dispersion and location parameters, making it highly responsive to volatility changes while maintaining robustness against price fluctuations.

This methodology is inspired by incremental calculation techniques for weighted mean and variance, as outlined in the paper by Tony Finch:

📄 "Incremental Calculation of Weighted Mean and Variance" .

Key Features

✅ Adaptive Volatility Estimation – Uses an exponentially weighted Student-T model to dynamically adjust band width.

✅ Volume-Weighted Mean & Dispersion – Incorporates real-time volume weighting, ensuring a more accurate representation of market sentiment.

✅ High-Timeframe Volume Normalization – Provides an option to smooth volume impact by referencing a higher timeframe’s cumulative volume, reducing noise from high-variability bars.

✅ Customizable Tension Parameters – Configurable standard deviation multipliers (σ) allow for fine-tuned volatility sensitivity.

✅ %B-Like Oscillator for Relative Price Positioning – The main indicator is in form of a dedicated oscillator pane that normalizes price position within the sigma ranges, helping identify overbought/oversold conditions and potential momentum shifts.

✅ Robust Statistical Foundation – Utilizes kurtosis-based degree-of-freedom estimation, enhancing responsiveness across different market conditions.

How It Works

Volume-Weighted Elastic Mean (eμ) – Computes a dynamic mean price using an elastic weighted moving average approach, influenced by trade volume, if not volume detected in series, study takes true range as replacement.

Dispersion (eσ) via Student-T Distribution – Instead of assuming a fixed normal distribution, the bands adapt to heavy-tailed distributions using kurtosis-driven degrees of freedom.

Incremental Calculation of Variance – The indicator applies Tony Finch’s incremental method for computing weighted variance instead of arithmetic sum's of fixed bar window or arrays, improving efficiency and numerical stability.

Tension Calculation – There are 2 dispersion custom "zones" that are computed based on the weighted mean and dynamically adjusted standard student-t deviation.

%B-Like Oscillator Calculation – The oscillator normalizes the price within the band structure, with values between 0 and 1:

* 0.00 → Price is at the lower band (-2σ).

* 0.50 → Price is at the volume-weighted mean (eμ).

* 1.00 → Price is at the upper band (+2σ).

* Readings above 1.00 or below 0.00 suggest extreme movements or possible breakouts.

Recommended Usage

For scalping in lower timeframes, it is recommended to use the fixed α Decay Factor, it is in raw format for better control, but you can easily make a like of transformation to N-bar size window like in EMA-1 bar dividing 2 / decayFactor or like an RMA dividing 1 / decayFactor.

The HTF selector catch quite well Higher Time Frame analysis, for example using a Daily chart and using as HTF the 200-day timeframe, weekly or monthly.

Suitable for trend confirmation, breakout detection, and mean reversion plays.

The %B-like oscillator helps gauge momentum strength and detect divergences in price action if user prefer a clean chart without bands, this thanks to pineScript v6 force overlay feature.

Ideal for markets with volume-driven momentum shifts (e.g., futures, forex, crypto).

Customization Parameters

Fixed α Decay Factor – Controls the rate of volume weighting influence for an approximation EWMA approach instead of using sum of series or arrays, making the code lightweight & computing fast O(1).

HTF Volume Smoothing – Instead of a fixed denominator for computing α , a volume sum of the last 2 higher timeframe closed candles are used as denominator for our α weight factor. This is useful to review mayor trends like in daily, weekly, monthly.

Tension Multipliers (±σ) – Adjusts sensitivity to dispersion sigma parameter (volatility).

Oscillator Zone Fills – Visual cues for price positioning within the cloud range.

Posible Interpretations

As market within indicators relay on each individual edge, this are just some key ideas to glimpse how the indicator could be interpreted by the user:

📌 Price inside bands – Market is considered somehow "stable"; price is like resting from tension or "charging batteries" for volume spike moves.

📌 Price breaking outer bands – Potential breakout or extreme movement; watch for reversals or continuation from strong moves. Market is already in tension or generating it.

📌 Narrowing Bands – Decreasing volatility; expect contraction before expansion.

📌 Widening Bands – Increased volatility; prepare for high probability pull-back moves, specially to the center location of the bands (the mean) or the other side of them.