Daily Open Shift The "Daily Open Shift" System (V2.0)

1. The Setup (Indicators & Timeframe)

• Timeframe: 15-Minute Chart (Execution).

• Key Levels: Daily Open (DO) or New York Open (NYO).

• Trend Indicators:

o 24 & 42 EMA Ribbon (Exponential Moving Averages).

o 30-Minute Supertrend.

________________________________________

2. Phase 1: Establish The Bias (The Filter)

This is the V2 upgrade. We do not trade against the day's opening momentum.

1. Mark the Open: Draw a horizontal line at the Daily Open (00:00) or Session Open.

2. The "First 2H" Rule: Observe the price action for the first 2 hours after the open.

o First 2H are Green/Bullish? → You are LONG BIAS only for the rest of the session. (Ignore all sell signals).

o First 2H are Red/Bearish? → You are SHORT BIAS only for the rest of the session. (Ignore all buy signals).

________________________________________

3. Phase 2: The Signal (The Switch)

Wait for the chart to confirm your bias technically.

1. The Switch: Price must cross and close a 15M candle on the correct side of the Daily Open.

o Longs: Price switches from below to above DO.

o Shorts: Price switches from above to below DO.

2. Indicator Confluence:

o EMAs: Must be crossed in your direction (Green for Long, Red for Short).

o 30M Supertrend: Must match your direction.

________________________________________

4. Phase 3: The Entry (The Trigger)

We never chase the breakdown. We wait for the price to come to us.

1. The Pullback: Wait for the price to retrace and touch/wick into the 24/42 EMA Ribbon.

2. The Confirmation: Watch the candle that touches the EMA.

o It must reject the EMA (wick off it) and close respecting the trend.

o Do not enter if the candle closes forcefully through the EMA, breaking structure.

3. Execution: Enter Market Order immediately on that candle close.

________________________________________

5. Phase 4: Risk Management (The Math)

This is the V2 upgrade. We aim for higher profitability.

1. Stop Loss (SL):

o Longs: Placed strictly below the lowest EMA band.

o Shorts: Placed strictly above the highest EMA band.

o Logic: If price crosses the EMA band completely, the trend is dead. Get out.

2. Take Profit (TP):

o FIXED 3R (Reward = 3x Risk).

o Example: If Risk is $100, TP is set to make $300.

o Rule: Do not move the TP. Do not close early. Let the math play out.

________________________________________

Summary Checklist (Print This)

Time: Is the First 2H bias clear? (Green=Buy / Red=Sell)

Switch: Did price close above/below the Daily Open?

Trend: Are EMAs crossed and Supertrend agreeing?

Patience: Did I wait for the price to pull back to the EMA band?

Trigger: Did the candle close respecting the EMA?

Execution: Market Entry + Stop Loss behind EMA + Fixed 3R Target.

Mindset: Am I at "2/10" emotion? Set the trade and walk away.

Concept

Hybrid Trend-Following Inside Bar BreakoutHybrid Trend-Following Inside Bar Breakout Strategy

The Hybrid Trend-Following Inside Bar Breakout Strategy is a rule-based trading system designed to capture strong directional moves while controlling risk during uncertain market conditions. It combines trend-following, price action, and volatility-based risk management into a single robust framework.

Core Concept

The strategy trades inside bar breakouts only in the direction of the dominant market trend. Inside bars represent periods of consolidation, and when price breaks out of this consolidation in a trending market, it often leads to impulsive moves with favorable risk–reward characteristics.

Key Components

1. Trend Filter

Uses 50 EMA and 200 EMA to define the market trend.

Bullish bias: 50 EMA above 200 EMA

Bearish bias: 50 EMA below 200 EMA

This filter prevents counter-trend trades and improves trade quality.

2. Volatility Filter

Compares fast ATR (14) with slow ATR (50).

Trades are taken only when volatility is expanding or above a minimum threshold.

This avoids low-volatility, choppy market conditions.

3. Inside Bar Breakout

An inside bar forms when the current candle’s high is lower than the previous candle’s high and the low is higher than the previous candle’s low.

A trade is triggered only when price breaks above or below the inside bar range in the direction of the trend.

4. Candle Quality Filter

Requires a minimum body-to-range ratio, ensuring that the breakout candle has strong momentum and is not driven by weak wicks.

Risk Management & Trade Management

Stop Loss (SL)

Placed using ATR-based dynamic stops, adapting to current market volatility.

Prevents tight stops in volatile conditions and wide stops in calm markets.

Partial Profit Taking

50% of the position is exited at 1.5R, locking in profits early.

This reduces psychological pressure and improves equity stability.

Trailing Stop

After partial profit is taken, the remaining position is managed with an ATR-based trailing stop.

Allows the strategy to capture large trend moves while protecting gains.

Cooldown Mechanism

After a losing trade, the system enters a cooldown period and skips a fixed number of bars.

This helps avoid revenge trading and overtrading during unfavorable market phases.

Why This Strategy Works

Trades only high-probability breakouts in trending markets

Adapts automatically to changing volatility

Combines price action precision with systematic risk control

Designed for consistent performance over long historical periods

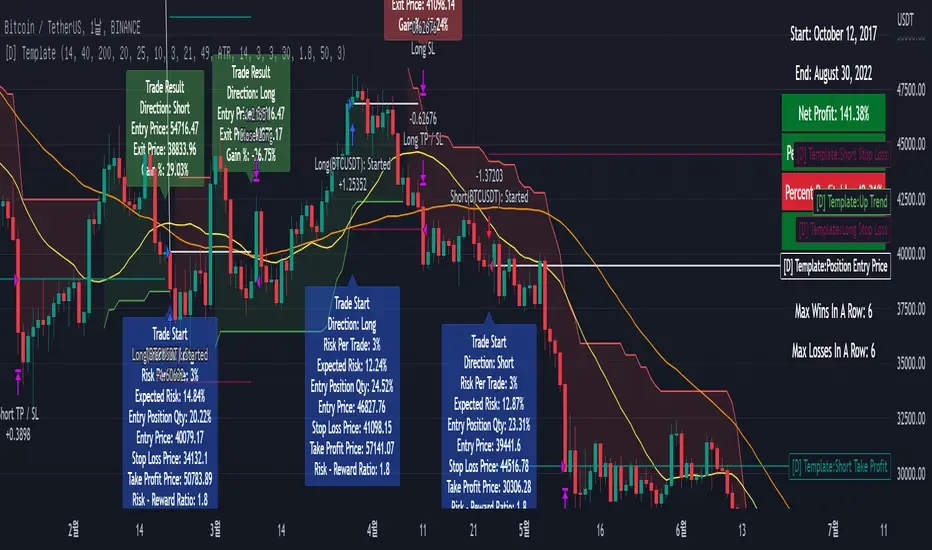

XAUUSD 1m SMC Zones (BOS + Flexible TP Modes + Trailing Runner)//@version=6

strategy("XAUUSD 1m SMC Zones (BOS + Flexible TP Modes + Trailing Runner)",

overlay = true,

initial_capital = 10000,

pyramiding = 10,

process_orders_on_close = true)

//━━━━━━━━━━━━━━━━━━━

// 1. INPUTS

//━━━━━━━━━━━━━━━━━━━

// TP / SL

tp1Pips = input.int(10, "TP1 (pips)", minval = 1)

fixedSLpips = input.int(50, "Fixed SL (pips)", minval = 5)

runnerRR = input.float(3.0, "Runner RR (TP2 = SL * RR)", step = 0.1, minval = 1.0)

// Daily risk

maxDailyLossPct = input.float(5.0, "Max daily loss % (stop trading)", step = 0.5)

maxDailyProfitPct = input.float(20.0, "Max daily profit % (stop trading)", step = 1.0)

// HTF S/R (1H)

htfTF = input.string("60", "HTF timeframe (minutes) for S/R block")

// Profit strategy (Option C)

profitStrategy = input.string("Minimal Risk | Full BE after TP1", "Profit Strategy", options = )

// Runner stop mode (your option 4)

runnerStopMode = input.string( "BE only", "Runner Stop Mode", options = )

// ATR trail settings (only used if ATR mode selected)

atrTrailLen = input.int(14, "ATR Length (trail)", minval = 1)

atrTrailMult = input.float(1.0, "ATR Multiplier (trail)", step = 0.1, minval = 0.1)

// Pip size (for XAUUSD: 1 pip = 0.10 if tick = 0.01)

pipSize = syminfo.mintick * 10.0

tp1Points = tp1Pips * pipSize

slPoints = fixedSLpips * pipSize

baseQty = input.float (1.0, "Base order size" , step = 0.01, minval = 0.01)

//━━━━━━━━━━━━━━━━━━━

// 2. DAILY RISK MANAGEMENT

//━━━━━━━━━━━━━━━━━━━

isNewDay = ta.change(time("D")) != 0

var float dayStartEquity = na

var bool dailyStopped = false

equityNow = strategy.initial_capital + strategy.netprofit

if isNewDay or na(dayStartEquity)

dayStartEquity := equityNow

dailyStopped := false

dailyPnL = equityNow - dayStartEquity

dailyPnLPct = dayStartEquity != 0 ? (dailyPnL / dayStartEquity) * 100.0 : 0.0

if not dailyStopped

if dailyPnLPct <= -maxDailyLossPct

dailyStopped := true

if dailyPnLPct >= maxDailyProfitPct

dailyStopped := true

canTradeToday = not dailyStopped

//━━━━━━━━━━━━━━━━━━━

// 3. 1H S/R ZONES (for direction block)

//━━━━━━━━━━━━━━━━━━━

htOpen = request.security(syminfo.tickerid, htfTF, open)

htHigh = request.security(syminfo.tickerid, htfTF, high)

htLow = request.security(syminfo.tickerid, htfTF, low)

htClose = request.security(syminfo.tickerid, htfTF, close)

// Engulf logic on HTF

htBullPrev = htClose > htOpen

htBearPrev = htClose < htOpen

htBearEngulf = htClose < htOpen and htBullPrev and htOpen >= htClose and htClose <= htOpen

htBullEngulf = htClose > htOpen and htBearPrev and htOpen <= htClose and htClose >= htOpen

// Liquidity sweep on HTF previous candle

htSweepHigh = htHigh > ta.highest(htHigh, 5)

htSweepLow = htLow < ta.lowest(htLow, 5)

// Store last HTF zones

var float htResHigh = na

var float htResLow = na

var float htSupHigh = na

var float htSupLow = na

if htBearEngulf and htSweepHigh

htResHigh := htHigh

htResLow := htLow

if htBullEngulf and htSweepLow

htSupHigh := htHigh

htSupLow := htLow

// Are we inside HTF zones?

inHtfRes = not na(htResHigh) and close <= htResHigh and close >= htResLow

inHtfSup = not na(htSupLow) and close >= htSupLow and close <= htSupHigh

// Block direction against HTF zones

longBlockedByZone = inHtfRes // no buys in HTF resistance

shortBlockedByZone = inHtfSup // no sells in HTF support

//━━━━━━━━━━━━━━━━━━━

// 4. 1m LOCAL ZONES (LIQUIDITY SWEEP + ENGULF + QUALITY SCORE)

//━━━━━━━━━━━━━━━━━━━

// 1m engulf patterns

bullPrev1 = close > open

bearPrev1 = close < open

bearEngulfNow = close < open and bullPrev1 and open >= close and close <= open

bullEngulfNow = close > open and bearPrev1 and open <= close and close >= open

// Liquidity sweep by previous candle on 1m

sweepHighPrev = high > ta.highest(high, 5)

sweepLowPrev = low < ta.lowest(low, 5)

// Local zone storage (one active support + one active resistance)

// Quality score: 1 = engulf only, 2 = engulf + sweep (we only trade ≥2)

var float supLow = na

var float supHigh = na

var int supQ = 0

var bool supUsed = false

var float resLow = na

var float resHigh = na

var int resQ = 0

var bool resUsed = false

// New resistance zone: previous bullish candle -> bear engulf

if bearEngulfNow

resLow := low

resHigh := high

resQ := sweepHighPrev ? 2 : 1

resUsed := false

// New support zone: previous bearish candle -> bull engulf

if bullEngulfNow

supLow := low

supHigh := high

supQ := sweepLowPrev ? 2 : 1

supUsed := false

// Raw "inside zone" detection

inSupRaw = not na(supLow) and close >= supLow and close <= supHigh

inResRaw = not na(resHigh) and close <= resHigh and close >= resLow

// QUALITY FILTER: only trade zones with quality ≥ 2 (engulf + sweep)

highQualitySup = supQ >= 2

highQualityRes = resQ >= 2

inSupZone = inSupRaw and highQualitySup and not supUsed

inResZone = inResRaw and highQualityRes and not resUsed

// Plot zones

plot(supLow, "Sup Low", color = color.new(color.lime, 60), style = plot.style_linebr)

plot(supHigh, "Sup High", color = color.new(color.lime, 60), style = plot.style_linebr)

plot(resLow, "Res Low", color = color.new(color.red, 60), style = plot.style_linebr)

plot(resHigh, "Res High", color = color.new(color.red, 60), style = plot.style_linebr)

//━━━━━━━━━━━━━━━━━━━

// 5. MODERATE BOS (3-BAR FRACTAL STRUCTURE)

//━━━━━━━━━━━━━━━━━━━

// 3-bar swing highs/lows

swHigh = high > high and high > high

swLow = low < low and low < low

var float lastSwingHigh = na

var float lastSwingLow = na

if swHigh

lastSwingHigh := high

if swLow

lastSwingLow := low

// BOS conditions

bosUp = not na(lastSwingHigh) and close > lastSwingHigh

bosDown = not na(lastSwingLow) and close < lastSwingLow

// Zone “arming” and BOS validation

var bool supArmed = false

var bool resArmed = false

var bool supBosOK = false

var bool resBosOK = false

// Arm zones when first touched

if inSupZone

supArmed := true

if inResZone

resArmed := true

// BOS after arming → zone becomes valid for entries

if supArmed and bosUp

supBosOK := true

if resArmed and bosDown

resBosOK := true

// Reset BOS flags when new zones are created

if bullEngulfNow

supArmed := false

supBosOK := false

if bearEngulfNow

resArmed := false

resBosOK := false

//━━━━━━━━━━━━━━━━━━━

// 6. ENTRY CONDITIONS (ZONE + BOS + RISK STATE)

//━━━━━━━━━━━━━━━━━━━

flatOrShort = strategy.position_size <= 0

flatOrLong = strategy.position_size >= 0

longSignal = canTradeToday and not longBlockedByZone and inSupZone and supBosOK and flatOrShort

shortSignal = canTradeToday and not shortBlockedByZone and inResZone and resBosOK and flatOrLong

//━━━━━━━━━━━━━━━━━━━

// 7. ORDER LOGIC – TWO PROFIT STRATEGIES

//━━━━━━━━━━━━━━━━━━━

// Common metrics

atrTrail = ta.atr(atrTrailLen)

// MINIMAL MODE: single trade, BE after TP1, optional trailing

// HYBRID MODE: two trades (Scalp @ TP1, Runner @ TP2)

// Persistent tracking

var float longEntry = na

var float longTP1 = na

var float longTP2 = na

var float longSL = na

var bool longBE = false

var float longRunEntry = na

var float longRunTP1 = na

var float longRunTP2 = na

var float longRunSL = na

var bool longRunBE = false

var float shortEntry = na

var float shortTP1 = na

var float shortTP2 = na

var float shortSL = na

var bool shortBE = false

var float shortRunEntry = na

var float shortRunTP1 = na

var float shortRunTP2 = na

var float shortRunSL = na

var bool shortRunBE = false

isMinimal = profitStrategy == "Minimal Risk | Full BE after TP1"

isHybrid = profitStrategy == "Hybrid | Scalp TP + Runner TP"

//━━━━━━━━━━ LONG ENTRIES ━━━━━━━━━━

if longSignal

if isMinimal

longEntry := close

longSL := longEntry - slPoints

longTP1 := longEntry + tp1Points

longTP2 := longEntry + slPoints * runnerRR

longBE := false

strategy.entry("Long", strategy.long)

supUsed := true

supArmed := false

supBosOK := false

else if isHybrid

longRunEntry := close

longRunSL := longRunEntry - slPoints

longRunTP1 := longRunEntry + tp1Points

longRunTP2 := longRunEntry + slPoints * runnerRR

longRunBE := false

// Two separate entries, each 50% of baseQty (for backtest)

strategy.entry("LongScalp", strategy.long, qty = baseQty * 0.5)

strategy.entry("LongRun", strategy.long, qty = baseQty * 0.5)

supUsed := true

supArmed := false

supBosOK := false

//━━━━━━━━━━ SHORT ENTRIES ━━━━━━━━━━

if shortSignal

if isMinimal

shortEntry := close

shortSL := shortEntry + slPoints

shortTP1 := shortEntry - tp1Points

shortTP2 := shortEntry - slPoints * runnerRR

shortBE := false

strategy.entry("Short", strategy.short)

resUsed := true

resArmed := false

resBosOK := false

else if isHybrid

shortRunEntry := close

shortRunSL := shortRunEntry + slPoints

shortRunTP1 := shortRunEntry - tp1Points

shortRunTP2 := shortRunEntry - slPoints * runnerRR

shortRunBE := false

strategy.entry("ShortScalp", strategy.short, qty = baseQty * 50)

strategy.entry("ShortRun", strategy.short, qty = baseQty * 50)

resUsed := true

resArmed := false

resBosOK := false

//━━━━━━━━━━━━━━━━━━━

// 8. EXIT LOGIC – MINIMAL MODE

//━━━━━━━━━━━━━━━━━━━

// LONG – Minimal Risk: 1 trade, BE after TP1, runner to TP2

if isMinimal and strategy.position_size > 0 and not na(longEntry)

// Move to BE once TP1 is touched

if not longBE and high >= longTP1

longBE := true

// Base SL: BE or initial SL

float dynLongSL = longBE ? longEntry : longSL

// Optional trailing after BE

if longBE

if runnerStopMode == "Structure trail" and not na(lastSwingLow) and lastSwingLow > longEntry

dynLongSL := math.max(dynLongSL, lastSwingLow)

if runnerStopMode == "ATR trail"

trailSL = close - atrTrailMult * atrTrail

dynLongSL := math.max(dynLongSL, trailSL)

strategy.exit("Long Exit", "Long", stop = dynLongSL, limit = longTP2)

// SHORT – Minimal Risk: 1 trade, BE after TP1, runner to TP2

if isMinimal and strategy.position_size < 0 and not na(shortEntry)

if not shortBE and low <= shortTP1

shortBE := true

float dynShortSL = shortBE ? shortEntry : shortSL

if shortBE

if runnerStopMode == "Structure trail" and not na(lastSwingHigh) and lastSwingHigh < shortEntry

dynShortSL := math.min(dynShortSL, lastSwingHigh)

if runnerStopMode == "ATR trail"

trailSLs = close + atrTrailMult * atrTrail

dynShortSL := math.min(dynShortSL, trailSLs)

strategy.exit("Short Exit", "Short", stop = dynShortSL, limit = shortTP2)

//━━━━━━━━━━━━━━━━━━━

// 9. EXIT LOGIC – HYBRID MODE

//━━━━━━━━━━━━━━━━━━━

// LONG – Hybrid: Scalp + Runner

if isHybrid

// Scalp leg: full TP at TP1

if strategy.opentrades > 0

strategy.exit("LScalp TP", "LongScalp", stop = longRunSL, limit = longRunTP1)

// Runner leg

if strategy.position_size > 0 and not na(longRunEntry)

if not longRunBE and high >= longRunTP1

longRunBE := true

float dynLongRunSL = longRunBE ? longRunEntry : longRunSL

if longRunBE

if runnerStopMode == "Structure trail" and not na(lastSwingLow) and lastSwingLow > longRunEntry

dynLongRunSL := math.max(dynLongRunSL, lastSwingLow)

if runnerStopMode == "ATR trail"

trailRunSL = close - atrTrailMult * atrTrail

dynLongRunSL := math.max(dynLongRunSL, trailRunSL)

strategy.exit("LRun TP", "LongRun", stop = dynLongRunSL, limit = longRunTP2)

// SHORT – Hybrid: Scalp + Runner

if isHybrid

if strategy.opentrades > 0

strategy.exit("SScalp TP", "ShortScalp", stop = shortRunSL, limit = shortRunTP1)

if strategy.position_size < 0 and not na(shortRunEntry)

if not shortRunBE and low <= shortRunTP1

shortRunBE := true

float dynShortRunSL = shortRunBE ? shortRunEntry : shortRunSL

if shortRunBE

if runnerStopMode == "Structure trail" and not na(lastSwingHigh) and lastSwingHigh < shortRunEntry

dynShortRunSL := math.min(dynShortRunSL, lastSwingHigh)

if runnerStopMode == "ATR trail"

trailRunSLs = close + atrTrailMult * atrTrail

dynShortRunSL := math.min(dynShortRunSL, trailRunSLs)

strategy.exit("SRun TP", "ShortRun", stop = dynShortRunSL, limit = shortRunTP2)

//━━━━━━━━━━━━━━━━━━━

// 10. RESET STATE WHEN FLAT

//━━━━━━━━━━━━━━━━━━━

if strategy.position_size == 0

longEntry := na

shortEntry := na

longBE := false

shortBE := false

longRunEntry := na

shortRunEntry := na

longRunBE := false

shortRunBE := false

//━━━━━━━━━━━━━━━━━━━

// 11. VISUAL ENTRY MARKERS

//━━━━━━━━━━━━━━━━━━━

plotshape(longSignal, title = "Long Signal", style = shape.triangleup,

location = location.belowbar, color = color.lime, size = size.tiny, text = "L")

plotshape(shortSignal, title = "Short Signal", style = shape.triangledown,

location = location.abovebar, color = color.red, size = size.tiny, text = "S")

Ashok 07 Dec 25 updated scriptTried to fix the bugs in previous script. Even now improvements are needed, but for now it looks reasonably profiting.

Adaptive Alligator - Asymmetric MH (Entry Only)

Adaptive Alligator – Asymmetric Mexican Hat (Entry Only)

This strategy combines adaptive cycle detection (wavelet + autocorrelation), directional entropy, and a Mexican Hat filter to generate highly selective LONG entry signals. Exits are based solely on the Alligator structure. The system is designed to detect asymmetric, strong, and accelerating bullish phases while filtering out market noise.

1. Adaptive Cycle Detection: The strategy analyzes the median price using wavelet decomposition (Haar, Daubechies D4/D6, Symlet 4), wavelet detail energy, and autocorrelation. It also incorporates the ratio of short-term to long-term ATR volatility. Based on these components, it computes a dominant_cycle value, which dynamically controls the lengths of the Alligator lines (Jaw, Teeth, Lips). This adaptive behavior allows the Alligator to speed up during trending phases and slow down during noise or consolidation.

2. Directional Entropy: Entropy is measured separately for upward and downward movements within the selected lookback window. The entropy difference: e_diff = entropy_down - entropy_up represents the directional bias of the market. When e_diff > 0, the market shows an organized bullish pressure; when < 0, bearish dominance.

3. Mexican Hat Filter: The Mexican Hat (Ricker Wavelet) acts as a second-derivative filter, detecting local maxima in the acceleration of directional entropy. The filtered output (mh_out) is compared against an adaptive noise level computed as SMA(|mh_out|). A signal is considered strong only when: – mh_out exceeds the adaptive noise level, – mh_out is rising relative to the previous bar. This step is critical for eliminating false signals produced by random fluctuations.

4. Entry Logic: A LONG entry requires all three layers: (1) Alligator structure: Lips > Teeth > Jaw. (2) Directional entropy bias: e_diff > 0. (3) A strong, accelerating Mexican Hat signal confirmed by a user-defined number of bars. Once all conditions are satisfied, a buy_final entry is triggered.

5. Exit Logic: Exits are intentionally simple and rely solely on the Alligator: crossunder(lips, teeth) This clean separation ensures precise, adaptive entries and stable, consistent exits.

6. Visual Components: – Alligator lines: Jaw (blue), Teeth (red), Lips (green), plotted with their characteristic offsets. – Background coloring reflects signal strength: dark green (STRONG BUY), lime (acceleration), yellow (weak bias), transparent otherwise. – A dedicated panel displays e_diff (entropy difference), mh_out (Mexican Hat output), and the adaptive noise band.

7. Diagnostic Table: A compact diagnostic dashboard shows: – MH Value, – Noise Level, – MH Acceleration (YES/NO), – Signal Status (STRONG BUY / ACCELERATING / WEAK / BEARISH). It updates on the last bar, making it suitable for live monitoring.

8. Use Case: This strategy is highly selective and ideal as an entry module within trend-following systems. By combining wavelets, entropy, and adaptive noise modeling, it effectively filters out consolidation periods and focuses only on statistically significant bullish transitions. It can be integrated with various exit frameworks such as ATR stops, channel-based exits, range boxes, or trailing logic.

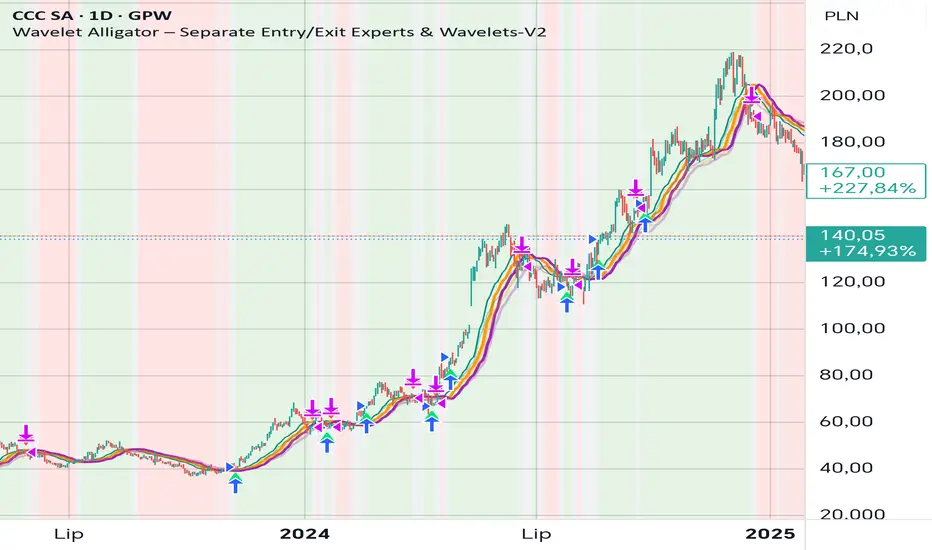

Wavelet Alligator – Separate Entry/Exit Experts & Wavelets-V2

Wavelet Alligator – Strategy Explanation & How to Use

1. Concept Overview

The Wavelet Alligator strategy combines:

- Wavelet transforms (Daubechies, Haar, Symlet, Mexican Hat, Morlet)

- Fractional calculus kernels: Caputo-Fabrizio (CF) and Atangana-Baleanu (AB)

- Three-layer “alligator-like” wavelet smoothing (soft → medium → strong)

- Expert-based entry/exit routing (RAW, CF, AB, or Majority vote)

- Independent wavelets for ENTRY and EXIT

- Main trend defined by AB wavelet ordering

This creates a multi-structure, multi-kernel trend engine capable of capturing extended moves with high signal quality.

2. Wavelet Alligator Structure

Each source (RAW, CF, AB) is transformed into three wavelet layers:

Soft = fastest reaction

Medium = mid smoothing

Strong = trend backbone

Wavelets:

- Daubechies: stable trend

- Haar: fast impulse detection

- Symlet: balanced

- Mexican Hat: curvature and reversal detection

- Morlet: cyclic, oscillatory

3. Entry Logic

Long entry occurs when:

- AB wavelet shows bullish structure (soft > medium > strong, medium rising)

- Selected entry expert approves (RAW / CF / AB / Majority)

- Wavelet condition: soft > strong AND medium crosses above strong

4. Exit Logic

Exit is independent from entry:

- Controlled by chosen exit expert

- Wavelet reversal condition: soft < strong AND medium crosses below strong

- Forced exit when AB trend turns neutral or bearish

5. Background Color (Regime)

- Green: bullish AB regime

- Red: bearish AB regime

- Gray: neutral/transition

6. How to Use

Step 1 – Choose entry wavelet

Daubechies: stable trend

Haar: breakout scalping

Mexican Hat: early reversals

Symlet: balanced

Morlet: cyclic markets

Step 2 – Choose exit wavelet

Mexican Hat: best precision

Daubechies: smooth exits

Haar: aggressive exits

Step 3 – Select entry/exit experts

CF only – fast fractional trend

AB only – stable long-memory trend

RAW only – pure price structure

Majority – safest, noise-filtered

Step 4 – Run the strategy

Entries occur only during AB bullish trend.

Exits occur on wavelet reversal or AB trend failure.

7. Why This Strategy Works

It fuses:

- Fractional calculus (memory)

- Wavelets (shape/curvature)

- Alligator ordering (trend hierarchy)

Result: high-quality entries, strong trend holding, noise-resistant signals.

Fractional Candlestick Long Only Experimental V10Fractional Candlestick Long-Only Strategy – Technical Description

This document provides a professional English description of the "Fractional Candlestick Long Only Experimental V6" strategy using pure CF/AB fractional kernels and wavelet-based filtering.

1. Fractional Candlesticks (CF / AB)

The strategy computes two fractional representations of price using Caputo–Fabrizio (CF) and Atangana–Baleanu (AB) kernels. These provide long-memory filtering without EMA approximations. Both CF and AB versions are applied to O/H/L/C, producing fractional candlesticks and fractional Heikin-Ashi variants.

2. Trend Stack Logic

Trend confirmation is based on a 4-component stack:

- CF close > AB close

- HA_CF close > HA_AB close

- HA_CF bullish

- HA_AB bullish

The user selects how many components must align (4, 3, or any 2).

3. Wavelet Filtering

A wavelet transform (Haar, Daubechies-4, Mexican Hat) is applied to a chosen source (e.g., HA_CF close). The wavelet response is used as:

- entry filter (4 modes)

- exit filter (4 modes)

Wavelet modes: off, confirm, wavelet-only, block adverse signals.

4. Trailing System

Trailing stop uses fractional AB low × buffer, providing long-memory dynamic trailing behavior. A fractional trend channel (CF/AB lows vs HA highs) is also plotted.

5. Exit Framework

Exit options include: stack flip, CF

Crypto Pro Strategy (Entry Model + Risk)Imma try to use this on a prop firm but if you want to use it itss free or im going to try to make it free

BTC 5-MA Multi Cross Strategy By Hardik Prajapati Ai TradelabThis strategy is built around the five most powerful and commonly used moving averages in crypto trading — 5, 20, 50, 100, and 200-period SMAs (Simple Moving Averages) — applied on a 1-hour Bitcoin chart.

Core Idea:

The strategy aims to identify strong bullish trends by confirming when the price action crosses above all key moving averages. This alignment of multiple MAs indicates momentum shift and helps filter out false breakouts.

⸻

⚙️ How It Works:

1. Calculates 5 Moving Averages:

• 5 MA → Short-term momentum (fastest signal)

• 20 MA → Near-term trend confirmation

• 50 MA → Mid-term trend filter

• 100 MA → Long-term trend foundation

• 200 MA → Macro-trend direction (strongest support/resistance)

2. Buy Condition (Entry):

• A Buy is triggered when:

• The price crosses above the 5 MA, and

• The closing price remains above all other MAs (20, 50, 100, 200)

This signals that momentum is aligned across all time horizons — a strong uptrend confirmation.

3. Sell Condition (Exit):

• The position is closed when price crosses below the 20 MA, showing weakness in short-term momentum.

4. Visual Signals:

• 🟢 BUY triangle below candles → Entry signal

• 🔴 SELL triangle above candles → Exit signal

• Colored MAs plotted for trend clarity.

⸻

📈 Recommended Usage:

• Chart: BTC/USDT

• Timeframe: 1 Hour

• Type: Trend-following crossover strategy

• Ideal for: Identifying major breakout moves and confirming trend reversals.

⸻

⚠️ Notes:

• This script is meant for educational and backtesting purposes only.

• Always apply additional confirmation tools (like RSI, Volume, or VIX-style filters) before live trading.

• Works best during trending markets; may produce whipsaws in sideways zones.

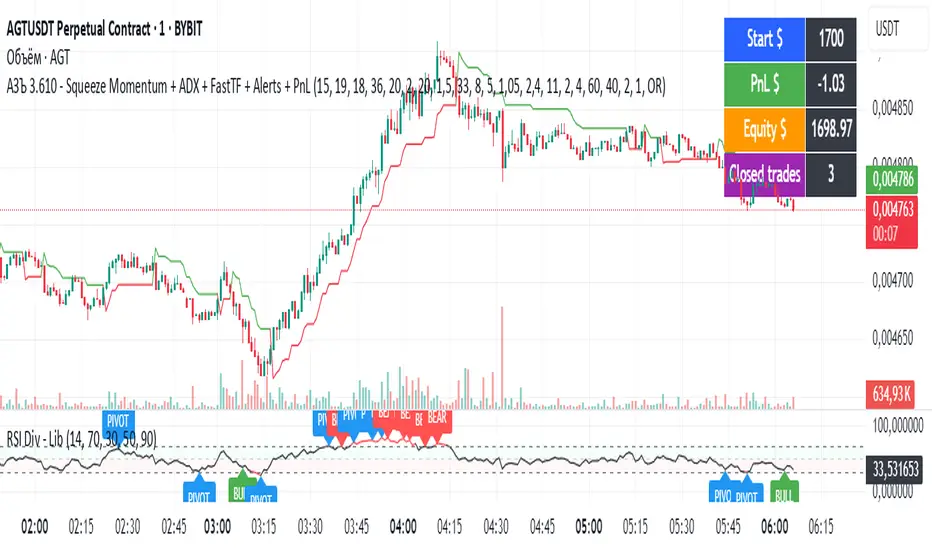

АЗЪ 3.610 - Squeeze Momentum + ADX + FastTF + Alerts + PnLStrata genius squeeze momentum + tester + adx +fast tf

US100 Liquidity Precision StrategyScalping strategy 5-10 point sl / 17 points tp

Automatic BE

Consistent money over time

ARSI – (VWAP & ATR) 3QKRAKThe ARSI Long & Short – Dynamic Risk Sizing (VWAP & ATR) indicator combines three core components—an adjusted RSI oscillator (ARSI), Volume‐Weighted Average Price (VWAP), and Average True Range (ATR)—so that entry/exit signals and position sizing are always tailored to current market conditions. ARSI, plotted from 0 to 100 with clearly marked overbought and oversold zones, is the primary signal driver: when ARSI falls below the lower threshold it indicates an excessive sell‐off and flags a long opportunity, whereas a break above the upper threshold signals overextended gains and foreshadows a short. A midpoint line at 50 can serve as an early exit or reduction signal when crossed against your position.

VWAP, showing the volume‐weighted average price over the chosen period, acts as a trend filter—long trades are only taken when price sits above VWAP, and shorts only when it’s below—ensuring each trade aligns with the prevailing market momentum. ATR measures current volatility and is used both to set safe stop‐loss levels and to dynamically size each position. In practice, this means positions automatically shrink in high‐volatility environments and grow in quieter markets, all while risking a fixed percentage of your capital.

Everything appears on a single chart: the ARSI pane below the price window with its reference levels; VWAP overlaid on the price; and the ATR‐based stop‐loss distances graphically displayed. Traders thus get a comprehensive, at-a-glance view of entries, exits, trend confirmation, and exactly how large a position they can safely take. The indicator runs in real time, removing the need for manual parameter calculations and letting you focus on strategic decision-making.

Gold Pro StrategyHere’s the strategy description in a chat format:

---

**Gold (XAU/USD) Trend-Following Strategy**

This **trend-following strategy** is designed for trading gold (XAU/USD) by combining moving averages, MACD momentum indicators, and RSI filters to capture sustained trends while managing volatility risks. The strategy uses volatility-adjusted stops to protect gains and prevent overexposure during erratic price movements. The aim is to take advantage of trending markets by confirming momentum and ensuring entries are not made at extreme levels.

---

**Key Components**

1. **Trend Identification**

- **50 vs 200 EMA Crossover**

- **Bullish Trend:** 50 EMA crosses above 200 EMA, and the price closes above the 200 EMA

- **Bearish Trend:** 50 EMA crosses below 200 EMA, and the price closes below the 200 EMA

2. **Momentum Confirmation**

- **MACD (12,26,9)**

- **Buy Signal:** MACD line crosses above the signal line

- **Sell Signal:** MACD line crosses below the signal line

- **RSI (14 Period)**

- **Bullish Zone:** RSI between 50-70 to avoid overbought conditions

- **Bearish Zone:** RSI between 30-50 to avoid oversold conditions

3. **Entry Criteria**

- **Long Entry:** Bullish trend, MACD bullish crossover, and RSI between 50-70

- **Short Entry:** Bearish trend, MACD bearish crossover, and RSI between 30-50

4. **Exit & Risk Management**

- **ATR Trailing Stops (14 Period):**

- Initial Stop: 3x ATR from entry price

- Trailing Stop: Adjusts to lock in profits as price moves favorably

- **Position Sizing:** 100% of equity per trade (high-risk strategy)

---

**Key Logic Flow**

1. **Trend Filter:** Use the 50/200 EMA relationship to define the market's direction

2. **Momentum Confirmation:** Confirm trend momentum with MACD crossovers

3. **RSI Validation:** Ensure RSI is within non-extreme ranges before entering trades

4. **Volatility-Based Risk Management:** Use ATR stops to manage market volatility

---

**Visual Cues**

- **Blue Line:** 50 EMA

- **Red Line:** 200 EMA

- **Green Triangles:** Long entry signals

- **Red Triangles:** Short entry signals

---

**Strengths**

- **Clear Trend Focus:** Avoids counter-trend trades

- **RSI Filter:** Prevents entering overbought or oversold conditions

- **ATR Stops:** Adapts to gold’s inherent volatility

- **Simple Rules:** Easy to follow with minimal inputs

---

**Weaknesses & Risks**

- **Infrequent Signals:** 50/200 EMA crossovers are rare

- **Potential Missed Opportunities:** Strict RSI criteria may miss some valid trends

- **Aggressive Position Sizing:** 100% equity allocation can lead to large drawdowns

- **No Profit Targets:** Relies on trailing stops rather than defined exit targets

---

**Performance Profile**

| Metric | Expected Range |

|----------------------|---------------------|

| Annual Trades | 4-8 |

| Win Rate | 55-65% |

| Max Drawdown | 25-35% |

| Profit Factor | 1.8-2.5 |

---

**Optimization Recommendations**

1. **Increase Trade Frequency**

Adjust the EMAs to shorter periods:

- `emaFastLen = input.int(30, "Fast EMA")`

- `emaSlowLen = input.int(150, "Slow EMA")`

2. **Relax RSI Filters**

Adjust the RSI range to:

- `rsiBullish = rsi > 45 and rsi < 75`

- `rsiBearish = rsi < 55 and rsi > 25`

3. **Add Profit Targets**

Introduce a profit target at 1.5% above entry:

```pine

strategy.exit("Long Exit", "Long",

stop=longStopPrice,

profit=close*1.015, // 1.5% target

trail_offset=trailOffset)

```

4. **Reduce Position Sizing**

Risk a smaller percentage per trade:

- `default_qty_value=25`

---

**Best Use Case**

This strategy excels in **strong trending markets** such as gold rallies during economic or geopolitical crises. However, during sideways or choppy market conditions, the strategy might require manual intervention to avoid false signals. Additionally, integrating fundamental analysis—like monitoring USD weakness or geopolitical risks—can enhance its effectiveness.

---

This strategy offers a balanced approach for trading gold, combining trend-following principles with risk management tailored to the volatility of the market.

TrendGuard Scalper: SSL + Hama Candle with Consolidation ZonesThis TradingView script brings a powerful scalping strategy that combines the SSL Channel and Hama Candles indicators with a special twist—consolidation detection. Designed for traders looking for consistency in various markets like crypto, forex, and stocks, this strategy highlights clear trend signals, risk management, and helps filter out risky trades during consolidation periods.

Why Use This Strategy?

Clear Trend Detection:

With the SSL Channel, you’ll know exactly when the market is in an uptrend (green) or downtrend (red), giving you straightforward entry points.

Short-Term Trend Precision with Hama Candles:

By calculating unique EMAs for open, high, low, and close, the Hama Candles show the strength and direction of short-term trends. Combined with the Hama Line, it gives you a solid confirmation on whether the trend is strong or about to reverse, allowing for precise entries and exits.

Avoiding Choppy Markets:

Thanks to ATR-based consolidation detection, this strategy identifies low-volatility periods where the market is “choppy” and less predictable. During these times, a yellow background appears on the chart, warning you to hold off on trades, reducing the likelihood of entering losing trades.

Built-In Risk Management:

With adjustable Take Profit and Stop Loss levels based on price movements, you can set and forget your trades, with a safety net if the market turns against you. The strategy automatically closes positions if the price returns to the Hama Candle, keeping your risk low.

How It Works:

Long Position: When both the SSL and Hama indicators show a green trend, and the price is above the Hama Candles, the strategy opens a long position. Take Profit triggers at your chosen risk-to-reward ratio, while Stop Loss protects you just below the Hama Line.

Short Position: When both indicators align in red and the price is below the Hama Candles, the strategy opens a short. Similar to longs, Stop Loss is set just above the Hama Line, and Take Profit is at your defined level.

Start Trading Confidently

Test this strategy with different settings and discover how it can perform across various assets. Whether you're trading Bitcoin, forex pairs, or stocks, this system has the flexibility and robustness to help you spot profitable trends and avoid risky zones. Try it today on a 30-minute timeframe to see how it aligns with your trading goals, and let the consolidation detection guide you away from false signals.

Happy trading, and may the trends be with you! 📈

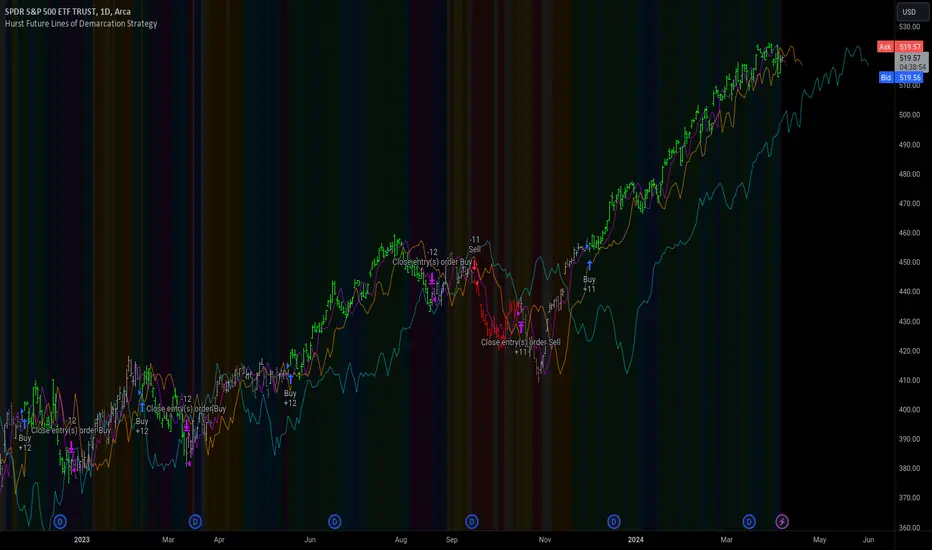

Hurst Future Lines of Demarcation StrategyJ. M. Hurst introduced a concept in technical analysis known as the Future Line of Demarcation (FLD), which serves as a forward-looking tool by incorporating a simple yet profound line into future projections on a financial chart. Specifically, the FLD is constructed by offsetting the price half a cycle ahead into the future on the time axis, relative to the Hurst Cycle of interest. For instance, in the context of a 40 Day Cycle, the FLD would be represented by shifting the current price data 20 days forward on the chart, offering an idea of future price movement anticipations.

The utility of FLDs extends into three critical areas of insight, which form the backbone of the FLD Trading Strategy:

A price crossing the FLD signifies the confirmation of either a peak or trough formation, indicating pivotal moments in price action.

Such crossings also help determine precise price targets for the upcoming peak or trough, aligned with the cycle of examination.

Additionally, the occurrence of a peak in the FLD itself signals a probable zone where the price might experience a trough, helping to anticipate of future price movements.

These insights by Hurst in his "Cycles Trading Course" during the 1970s, are instrumental for traders aiming to determine entry and exit points, and to forecast potential price movements within the market.

To use the FLD Trading Strategy, for example when focusing on the 40 Day Cycle, a trader should primarily concentrate on the interplay between three Hurst Cycles:

The 20 Day FLD (Signal) - Half the length of the Trade Cycle

The 40 Day FLD (Trade) - The Cycle you want to trade

The 80 Day FLD (Trend) - Twice the length of the Trade Cycle

Traders can gauge trend or consolidation by watching for two critical patterns:

Cascading patterns, characterized by several FLDs running parallel with a consistent separation, typically emerge during pronounced market trends, indicating strong directional momentum.

Consolidation patterns, on the other hand, occur when multiple FLDs intersect and navigate within the same price bandwidth, often reversing direction to traverse this range multiple times. This tangled scenario results in the formation of Pause Zones, areas where price momentum is likely to temporarily stall or where the emergence of a significant trend might be delayed.

This simple FLD indicator provides 3 FLDs with optional source input and smoothing, A-through-H FLD interaction background, adjustable “Close the Trade” triggers, and a simple strategy for backtesting it all.

The A-through-H FLD interactions are a framework designed to classify the different types of price movements as they intersect with or diverge from the Future Line of Demarcation (FLD). Each interaction (designated A through H by color) represents a specific phase or characteristic within the cycle, and understanding these can help traders anticipate future price movements and make informed decisions.

The adjustable “Close the Trade” triggers are for setting the crossover/under that determines the trade exits. The options include: Price, Signal FLD, Trade FLD, or Trend FLD. For example, a trader may want to exit trades only when price finally crosses the Trade FLD line.

Shoutouts & Credits for all the raw code, helpful information, ideas & collaboration, conversations together, introductions, indicator feedback, and genuine/selfless help:

🏆 @TerryPascoe

🏅 @Hpotter

👏 @parisboy

DZ Strategy ICTThe script presented is a trading strategy called "Breaker Block Strategy with Price Channel". This strategy uses multiple time frames (1 minute, 5 minutes, 15 minutes, 1 hour, and 4 hours) to detect support and resistance areas on the chart.

The strategy uses parameters such as length, deviations, multiplier, Fibonacci level, move lag and volume threshold for each time frame. These parameters are adjustable by the user.

The script then calculates support and resistance levels using the simple moving average (SMA) and standard deviation (STDEV) of closing prices for each time frame.

It also detects "Breaker Blocks" based on price movement from support and resistance levels, as well as trade volume. A Breaker Block occurs when there is a significant breakout of a support or resistance level with high volume.

Buy and sell signals are generated based on the presence of a Breaker Block and price movement from support and resistance levels. When a buy signal is generated, a buy order is placed, and when a sell signal is generated, a sell order is placed.

The script also plots price channels for each time frame, representing resistance and support levels.

Profit limit levels are set for each time range, indicating that the price levels assigned to positions should be closed with a profit. Stop-loss levels are also set to limit losses in the event of canceled price movements.

In summary, this trading strategy uses a combination of Breaker Block detection, support and resistance levels, price channels and profit limit levels to generate buy and sell signals and manage positions on different time ranges.

[D] Dudu 95 Strategy Template ver.1.1.Hello Guys! Nice to meet you all!

This is my Second script after changing My Profile Name!

I updated my strategy template before - I added some filter conditions (EMA, ADX, DMI).

If there's something to update, I will update this script!

Thank you!

-----

I made this based on the open source strategies by jason5480, kevinmck100, myncrypto.

Thank you All!

### Filter

1. Can Choose whether to use filter.

2. Filters Based on ATR, EMA, ADX, and DMI are ready to use.

### StopLoss

1. Can Choose Stop Loss Type: Percent, ATR, Previous Low / High.

2. Can Chosse inputs of each Stop Loss Type.

### Take Profit

1. Can set Risk Reward Ratio for Take Profit.

- To simplify backtest, I erased all other options except RR Ratio.

- You can add Take Profit Logic by adding options in the code.

2. Can set Take Profit Quantity.

### Risk Manangement

1. Can choose whether to use Risk Manangement Logic.

- This controls the Quantity of the Entry.

- e.g. If you want to take 3% risk per trade and stop loss price is 6% below the long entry price,

then 50% of your equity will be used for trade.

2. Can choose How much risk you would take per trade.

### Plot

1. Added Labels to check the data of entry / exit positions.

2. Changed and Added color different from the original one. (green: #02732A, red: #D92332, yellow: #F2E313)

[fpemehd] Strategy TemplateHello Guys! Nice to meet you all!

This is my fourth script!

This is the Strategy Template for traders who wants to make their own strategy.

I made this based on the open source strategies by jason5480, kevinmck100, myncrypto. Thank you All!

### StopLoss

1. Can Choose Stop Loss Type: Percent, ATR, Previous Low / High.

2. Can Chosse inputs of each Stop Loss Type.

### Take Profit

1. Can set Risk Reward Ratio for Take Profit.

- To simplify backtest, I erased all other options except RR Ratio.

- You can add Take Profit Logic by adding options in the code.

2. Can set Take Profit Quantity.

### Risk Manangement

1. Can choose whether to use Risk Manangement Logic.

- This controls the Quantity of the Entry.

- e.g. If you want to take 3% risk per trade and stop loss price is 6% below the long entry price,

then 50% of your equity will be used for trade.

2. Can choose How much risk you would take per trade.

### Plot

1. Added Labels to check the data of entry / exit positions.

2. Changed and Added color different from the original one. (green: #02732A, red: #D92332, yellow: #F2E313)

[Strategy Alert Webhook Demo] Buy One Sell One Buy One Sell One

Two Options to send Alert Order via Webhook

1. Order fill events with `alert_message` on strategy.close(), strategy.entry(), strategy.exit() and strategy.order()

NOTE: Need to fill the Alert Creation box with `{{strategy.order.alert_message}}`

2. Send Alert through `alert()`

BEST Strategy Template w/ Custom SL/TP Size - EducationalHello traders

I'm getting this question at least once per week: "how to define a custom exit quantity for my stop loss and a different one for my take profit"

Instead of answering every day the same question in my DMs, I've decided to publish an educational strategy template script using this

Features

- Select to use or not the SL and/or TP

- Define how many pips/USD the SL/TP should be set at from the entry

- Define what quantity percentage you want to close at SL and/or at TP (lines 301 to 320 in the code)

- Classical custom trailing stop where the SL is moved to breakeven once the TP is hit

- Get real-time backtesting stats based on the options you've selected

Update

You might not know it yet but from last week (or maybe the week before), the qty/qty_percent from the strategy.exit function refers now to the initial position size (and not the remaining position size like before)

For example:

strategy.exit("EX1", qty_percent = 50, stop = constant)

strategy.exit("EX2", qty_percent = 20, stop = constant)

What happened before

After "EX1" reaches SL levels, "EX2" exits 20% from the % of the remaining position size.

If the initial position size = 100 contracts

EX1 exits 50 contracts

EX2 exits 20% of 50 contracts = 10 contracts

What's happening now

After "EX1" reaches SL levels, "EX2" exits 20% from the % of the original position size.

If the initial position size = 100 contracts

EX1 exits 50 contracts

EX2 exits 20 (20% of 100 contracts) contracts

I think this is an improvement and I really enjoy this new behavior.

See you in a few days with another post :)

ALL THE BEST

Dave