Length Adaptive MA SuperTrendLength Adaptive MA SuperTrend

Length Adaptive MA SuperTrend is a third-generation evolution of the SuperTrend concept, designed to improve signal accuracy while maintaining high responsiveness across different market conditions. The indicator dynamically adjusts its moving-average length to better match current market activity, allowing it to react quickly in fast markets while remaining stable during slower phases.

This adaptive behavior helps traders and investors visualize trend direction more clearly while reducing unnecessary noise, making the tool suitable for both beginners and advanced users seeking a responsive trend overlay.

🔍 How It Works

The indicator uses a moving average as the foundation for a SuperTrend-style structure, but instead of keeping the moving-average length fixed, it continuously adapts to changing market environments.

The script compares average activity levels across three horizons:

• Long-term period

• Medium-term period (half length)

• Short-term period (square-root length)

Activity is measured using one of three selectable drivers:

• ATR (volatility)

• Volume

• Standard deviation

Whichever period shows the strongest average activity becomes the active length used for calculating the moving-average base. This allows the indicator to automatically shift between faster and slower behavior depending on market conditions.

After selecting the active length, the result is slightly smoothed using the chosen moving-average type to produce a cleaner and more stable trend structure.

ATR-based bands are then applied around the adaptive base, and trend direction changes when price crosses these bands.

⚙️ Key Features

• Adaptive moving-average length selection

• Automatic adjustment between short, medium, and long market conditions

• Multiple smoothing types (SMA, EMA, WMA, HMA, VWMA, DEMA, TEMA, EWMA)

• ATR-based SuperTrend structure

• Trend transition markers

• Optional candle coloring based on active trend

🧩 Inputs Overview

• Moving-average smoothing type

• Base length and price source

• ATR length and multiplier

• Adaptive driver selection (ATR, Volume, or Standard Deviation)

📌 Usage Notes

• Helps visualize prevailing market trends across changing environments.

• Automatically adapts speed for trending and consolidating markets.

• Signals may change intrabar on lower timeframes.

• Best used with confirmation tools and proper risk management.

• Intended as an analytical tool, not financial advice.

Adaptive

Institutional Volume RSI [Adaptive]The Institutional Volume RSI is a next-generation momentum oscillator designed to solve the two biggest problems with standard RSI: Price Deception and Static Thresholds.

Standard RSI uses fixed 70/30 levels to define "Overbought" and "Oversold." This is flawed because in a strong institutional trend, the market can stay "Overbought" for weeks. Selling just because RSI hit 70 is a guaranteed way to lose money.

This tool fixes that.

It replaces static lines with Adaptive Volatility Bands . These bands breathe with the market—expanding during trends and contracting during squeezes—giving you a dynamic, statistically significant view of true momentum.

How It Works

The engine runs on three institutional concepts:

1. Volume-Weighted Source (VWMA) 📊

We calculate RSI based on Volume Weighted Moving Average , not just Close price.

Low Volume Move: RSI ignores it (Fakeout).

High Volume Move: RSI reacts aggressively (True Momentum).

2. Adaptive Volatility Bands 🌊

Instead of fixed lines, we use dynamic bands (similar to Bollinger Bands) applied directly to the RSI.

The Trend Ride: As long as the RSI line stays inside or above the Upper Band, the trend is strong. Do not sell.

The Squeeze: When the bands contract (get tight), it signals that volatility is dead and a massive explosive move is imminent.

3. Dynamic Sentiment Coloring 🎨

Green Line: RSI is above the baseline (Bullish Control).

Red Line: RSI is below the baseline (Bearish Control).

White Dots: These appear when RSI breaks outside the bands, signaling an extreme statistical anomaly (often a climax top or bottom).

The "Elastic Snap" Strategy

Recommended Companion: Hooke's Law: Market Elasticity

This indicator is the perfect "Trigger" for a Mean Reversion system. We recommend pairing it with a Reversal indicator (like Hooke's Law) to create a complete Setup + Trigger system.

The Strategy Rules:

1. The Setup (The Stretch) 📏

Wait for your Reversal Indicator (e.g., Hooke's Law) to identify an overextended market condition (Overbought/Oversold).

Context: The rubber band is stretched tight.

2. The Trigger (The Snap) 🔫

Do not enter blindly! Look at the IV-RSI :

For Shorts: Wait for the RSI line to turn RED . This confirms that momentum has actually rolled over.

For Longs: Wait for the RSI line to turn GREEN . This confirms that buyers have stepped in.

3. The Filter (The Safety) 🛡️

If price hits your Stop Loss level before the IV-RSI changes color, cancel the trade . This prevents you from shorting a strong trend that is simply "melting up" without volume exhaustion.

Settings & Configuration

RSI Length: Default is 14.

Source Type: VWMA (Volume Weighted) is recommended for institutional analysis.

Bands Multiplier: Default is 2.0 (Standard Deviation). Increasing this to 2.5 will make the "White Dot" extremes rarer and more significant.

Disclaimer

Trading involves a high level of risk and is not suitable for all investors. The content provided here is for educational purposes only and does not constitute financial advice. Past performance is not indicative of future results. The author (abgthecoder) is not responsible for any financial losses incurred from the use of this indicator. Always use proper risk management and never trade with money you cannot afford to lose. This tool is provided "as is" with open source code for the benefit of the trading community.

Adaptive AI SuperTrend [AlgoPoint]🚀 Adaptive AI SuperTrend

Adaptive AI SuperTrend is a high-performance trading terminal that redefines trend-following by integrating Machine Learning (ML) principles with advanced market regime detection. Unlike static indicators, this system dynamically recalibrates its internal parameters to match the ever-changing volatility of the financial markets.

Equipped with a custom "Wizard Engine," it filters out market noise during consolidation and identifies high-probability trend continuation points, making it an essential tool for scalpers, day traders, and swing traders alike.

🧠 What Makes it "AI"?

While traditional indicators use fixed rules, Adaptive AI SuperTrend utilizes Algorithmic Intelligence to make real-time decisions:

KNN-Inspired Adaptation: The engine analyzes the last 150 bars of volatility and trend strength to automatically adjust its sensitivity.

Market Regime Intelligence: It distinguishes between "Trending" and "Ranging" states using a sophisticated Squeeze Momentum module, preventing "whipsaws" during low-volume periods.

Self-Backtesting Logic: The indicator continuously calculates its own historical Win-Rate. If the probability of success falls below a certain threshold, it suppresses lower-quality signals.

🛠 Key Features

Dynamic Consolidation Boxes: Automatically identifies and wraps "choppy" price action in professional gray boxes. It waits for 3+ bars of consolidation before marking the zone, helping you spot breakout opportunities early.

Multi-Strategy Aggression:

- Conservative: Filtered signals for long-term trend following.

- Balanced: Optimized for daily volatility.

- Aggressive: High-frequency signals for capturing micro-trends.

Dual-Exit Risk Management:

- ATR TP-SL Mode: Sets mathematical targets based on market volatility with persistent on-screen lines.

- Smart Trailing Mode: Rides the trend to its exhaustion point. Includes intelligent labeling (🎯 TP or 🛑 SL) based on the trade's net profitability.

- RSI Pullback Confirmation: Beyond simple trend flips, it detects "buy the dip" or "sell the rip" opportunities within an existing trend using RSI 50-level crossovers.

📊 Real-Time Analytics Dashboard

The integrated AlgoPoint Dashboard provides a surgical view of the market:

- Market State: Instant "Trending" vs. "Ranging" (Consolidation) detection.

- Trend Strength: ADX-based momentum tracking.

- Strategy Status: Real-time feedback on your active aggression and exit modes.

🎨 Clean Charting & Customization

Built for professional clarity, you have total control over the UI:

Toggle Consolidation Boxes on/off.

Toggle ATR Target Lines and Exit Labels.

Customize background filters and dashboard visibility.

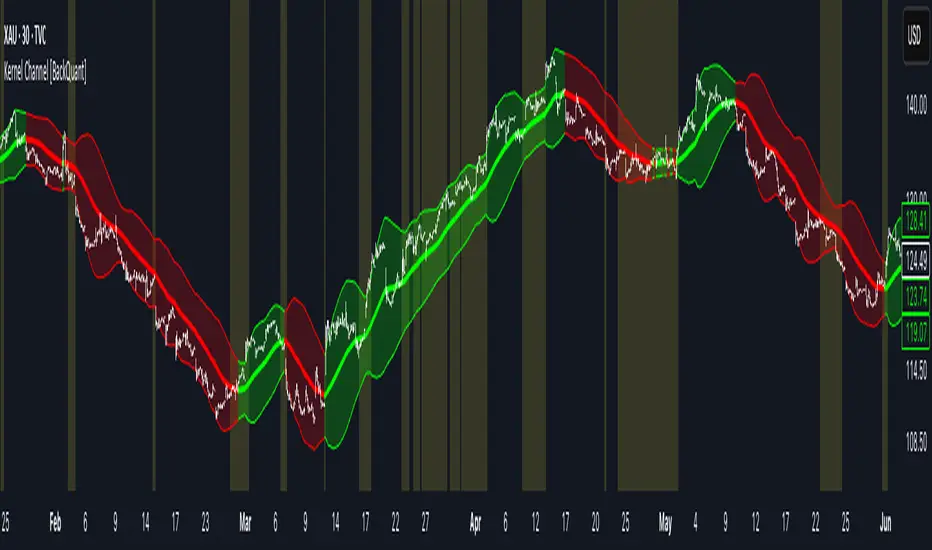

Laguerre Filter [BackQuant]Laguerre Filter

Overview

The Laguerre Filter is a powerful trend-following tool designed to smooth price action while maintaining responsiveness to market changes. It is based on the Laguerre recursive filter, which is a type of signal processing filter that adapts to both the current price dynamics and the underlying trend. The Laguerre Filter can be seen as a method to reduce market noise, enabling traders to more easily identify the strength and direction of trends while minimizing lag.

The Laguerre Filter is well-suited for markets with varying volatility levels, offering a smoother representation of price action without the delay associated with traditional moving averages. By dynamically adjusting to price movements, the Laguerre Filter provides a more adaptive and reliable signal compared to simpler smoothing techniques.

What is the Laguerre Filter?

The Laguerre Filter is derived from the Laguerre polynomial, which is used in signal processing for smooth filtering of data. The Laguerre filter is a recursive filter, meaning that each new value is calculated based on both the current price data and previous values, with a weighting system that allows it to adapt to market conditions. This recursive nature helps reduce the impact of short-term fluctuations, enabling the filter to focus on the underlying trend.

The Laguerre filter uses a feedback mechanism, where the input signal (price data) is smoothed iteratively. This iterative process helps avoid the lag that is typically associated with traditional moving averages while still capturing the overall trend direction.

The filter is designed to have:

Adaptive behavior: It reacts quickly to significant price changes while ignoring minor fluctuations.

Reduced noise: By filtering out random short-term price movements, it provides a clearer view of the underlying trend.

Customizability: Traders can adjust the filter’s sensitivity through user inputs, making it adaptable to different market conditions.

Core Calculation Methodology

The core of the Laguerre Filter lies in its recursive calculation:

Each new value is calculated using the previous value along with the current price input.

The recursive formula is governed by two key parameters: the damping factor (gamma) and the order of the filter (number of Laguerre elements).

The damping factor controls how responsive the filter is to changes in price. A higher gamma value makes the filter smoother but introduces more lag, while a lower gamma value makes it more reactive to price changes but can introduce more noise.

The order defines how many Laguerre elements are used in the calculation. A higher order results in a smoother output but with more delay, while a lower order provides a faster response but less smoothing.

The filter works by weighting previous values with a binomial weighting system, which assigns more weight to recent values and less weight to older values. This creates a dynamic smoothing effect that adapts to price volatility, ensuring that the filter is neither too slow nor too noisy.

Signal Logic and Trend Detection

The Laguerre Filter continuously evaluates the strength and direction of the trend by comparing the current smoothed value to the previous value:

If the current value is greater than the previous value, the trend is considered bullish, and the filter will signal a long condition.

If the current value is less than the previous value, the trend is considered bearish, and the filter will signal a short condition.

The trend detection logic is based on the recursive nature of the filter, which smooths price movements over time. This allows the filter to capture the broader trend while minimizing the influence of short-term price fluctuations.

The trend state is also visually represented by color-coding:

Green color represents an uptrend (bullish condition).

Red color represents a downtrend (bearish condition).

Neutral (white) indicates no clear trend direction.

This color-coding helps traders easily identify the prevailing trend and decide whether to enter or exit trades based on the trend's strength.

Laguerre Filter Behavior and Performance

The performance of the Laguerre Filter can be influenced by several factors:

Gamma (Damping Factor): A higher gamma value results in a smoother filter but increases lag. A lower gamma value allows for a faster response but may introduce more noise, making it more reactive to smaller price changes.

Filter Order: The order determines how many Laguerre elements are used in the filter calculation. A higher order provides more smoothing but increases lag, while a lower order results in a quicker response but less smoothing.

The sweet spot for gamma is typically between 0.7 and 0.85, where the filter offers a good balance between smoothness and responsiveness. The filter order is usually set to 4 for classic Laguerre filtering, but higher orders can be used for more smoothing if needed.

The Laguerre Filter’s performance shines in markets with sustained trends, where the filter can effectively capture and represent the underlying direction without excessive lag. It is particularly useful in volatile markets, as it helps smooth out noise while providing a clear picture of the trend.

Visual Presentation

The Laguerre Filter provides a dynamic, color-coded line that follows the trend direction. This line can be displayed alongside price data to visually highlight the market trend. In addition to the main Laguerre line, several visual enhancements can be applied:

Gradient fill between the price and the Laguerre Filter line, providing a visual cue for bullish or bearish market conditions.

Candle coloring to reflect the current trend, making it easier to spot trend reversals or confirmations directly on the chart.

Background shading to visually highlight areas of strong trend or consolidation.

Edge glow effect that highlights trend boundaries, making it easy to spot key levels of support or resistance.

These visual elements enhance the usability of the Laguerre Filter, allowing traders to quickly assess the market trend and make informed decisions.

Practical Use Cases

1) Trend Following

The Laguerre Filter is ideal for trend-following strategies. By using the filter to identify the prevailing trend, traders can:

Enter long positions when the Laguerre Filter turns bullish (green).

Enter short positions when the Laguerre Filter turns bearish (red).

By aligning trades with the dominant trend, traders can improve their chances of success.

2) Trend Strength Assessment

The Laguerre Filter can also be used to assess the strength of the trend:

A rising Laguerre value indicates a strengthening uptrend.

A falling Laguerre value indicates a strengthening downtrend.

A flattening Laguerre value signals weakening momentum or consolidation.

This information can be used to adjust position sizing or to decide when to enter or exit a trade.

3) Trade Management

The Laguerre Filter can also assist in trade management:

Use the Laguerre line as a trailing stop for long positions in an uptrend.

Scale out of positions as the Laguerre value begins to flatten or reverse.

Use the Laguerre Filter to avoid trades when the market is in consolidation or lacks a clear trend.

Tuning Guidelines

The Laguerre Filter can be adjusted for different market conditions using the following parameters:

Gamma (Damping Factor): Adjust for the desired level of responsiveness versus smoothness. Typical values range from 0.7 to 0.85.

Filter Order: Adjust to control the level of smoothing. The default value of 4 is a good starting point, but higher orders can be used for smoother filters.

Summary

The Laguerre Filter is a versatile and adaptive trend-following indicator that smooths price data and reduces noise, making it easier to identify and follow trends. By using recursive smoothing techniques and adjustable parameters, the Laguerre Filter provides an accurate representation of market conditions with minimal lag. It is especially useful in volatile markets where traditional moving averages may fail to capture the underlying trend. With its color-coded trend detection, gradient fills, and customizable settings, the Laguerre Filter is a powerful tool for traders looking to stay aligned with the prevailing market direction.

Apex Wallet - Adaptive Average Directional Index (ADX) & Trend DOverview The Apex Wallet Average Directional Index (ADX) is an enhanced version of the classic Wilder’s DMI/ADX system, designed to filter market noise and pinpoint trend strength with precision. Unlike standard indicators, this script features an adaptive engine that recalibrates its internal logic based on your specific trading style.

Adaptive Trading Engine The core strength of this script is its three-mode preset system:

Scalping: Fast-response settings (ADX 7) for quick scalp opportunities on low timeframes.

Day-Trading: Balanced settings (ADX 14) optimized for intraday sessions.

Swing-Trading: High-filter settings (ADX 21) designed to capture major market waves.

Visual Intelligence & Labels To ensure clarity, the script features a dynamic labeling system directly on the ADX line:

Trend Strength Zones: Clear horizontal markers for "Consolidation," "Trending," and "Extremely Strong" phases.

Real-time Status Labels: The ADX line changes color and displays its current state (Bullish, Bearish, or Consolidation) directly on the chart.

Optimized UI: No sidebar panels to clutter your view; all essential information is integrated into the oscillator window.

How to Use:

Select your Trading Mode in the settings.

Monitor the ADX color: Green indicates a strong bullish trend, Red indicates a strong bearish trend, and White/Orange signals consolidation.

Use the labels to confirm if the market is currently in a high-conviction trend phase or sideways range.

Adaptive RSI [BOSWaves]Adaptive RSI - Percentile-Based Momentum Detection with Dynamic Regime Thresholds

Overview

Adaptive RSI is a self-calibrating momentum oscillator that identifies overbought and oversold conditions through historical percentile analysis, constructing dynamic threshold boundaries that adjust to evolving market volatility and momentum characteristics.

Instead of relying on traditional fixed RSI levels (30/70 or 20/80) or static overbought/oversold zones, regime detection, threshold placement, and signal generation are determined through rolling percentile calculation, smoothed momentum measurement, and divergence pattern recognition.

This creates adaptive boundaries that reflect actual momentum distribution rather than arbitrary fixed levels - tightening during low-volatility consolidation periods, widening during trending environments, and incorporating divergence analysis to reveal momentum exhaustion or continuation patterns.

Momentum is therefore evaluated relative to its own historical context rather than universal fixed thresholds.

Conceptual Framework

Adaptive RSI is founded on the principle that meaningful momentum extremes emerge relative to recent price behavior rather than at predetermined numerical levels.

Traditional RSI implementations identify overbought and oversold conditions using fixed thresholds that remain constant regardless of market regime, often generating premature signals in strong trends or missing reversals in range-bound markets. This framework replaces static threshold logic with percentile-driven adaptive boundaries informed by actual momentum distribution.

Three core principles guide the design:

Threshold placement should correspond to historical momentum percentiles, not fixed numerical levels.

Regime detection must adapt to current market volatility and momentum characteristics.

Divergence patterns reveal momentum exhaustion before price reversal becomes visible.

This shifts oscillator analysis from universal fixed levels into adaptive, context-aware regime boundaries.

Theoretical Foundation

The indicator combines smoothed RSI calculation, rolling percentile tracking, adaptive threshold construction, and multi-pattern divergence detection.

A Hull Moving Average (HMA) pre-smooths the price source to reduce noise before RSI computation, which then undergoes optional post-smoothing using configurable moving average types. Confirmed oscillator values populate a rolling historical buffer used for percentile calculation, establishing upper and lower thresholds that adapt to recent momentum distribution. Regime state persists until the oscillator crosses the opposing threshold, preventing whipsaw during consolidation. Pivot detection identifies swing highs and lows in both price and oscillator values, enabling regular divergence pattern recognition through comparative analysis.

Five internal systems operate in tandem:

Smoothed Momentum Engine : Computes HMA-preprocessed RSI with optional post-smoothing using multiple MA methodologies (SMA, EMA, HMA, WMA, DEMA, RMA, LINREG, TEMA).

Historical Buffer Management : Maintains a rolling array of confirmed oscillator values for percentile calculation with configurable lookback depth.

Percentile Threshold Calculation : Determines upper and lower boundaries by extracting specified percentile values from sorted historical distribution.

Persistent Regime Detection : Establishes bullish/bearish/neutral states based on threshold crossings with state persistence between signals.

Divergence Pattern Recognition : Identifies regular bullish and bearish divergences through synchronized pivot analysis of price and oscillator values with configurable range filtering.

This design allows momentum interpretation to adapt to market conditions rather than reacting mechanically to universal thresholds.

How It Works

Adaptive RSI evaluates momentum through a sequence of self-calibrating processes:

Source Pre-Smoothing: Input price undergoes 4-period HMA smoothing to reduce bar-to-bar noise before oscillator calculation.

RSI Calculation: Standard RSI computation applied to smoothed source over configurable length period.

Optional Post-Smoothing: Raw RSI value undergoes additional smoothing using selected MA type and length for cleaner regime detection.

Historical Buffer Population: Confirmed oscillator values accumulate in a rolling array with size limit determined by adaptive lookback parameter.

Percentile Threshold Extraction: Array sorts on each bar to calculate upper percentile (bullish threshold) and lower percentile (bearish threshold) values.

Regime State Persistence: Bullish regime activates when oscillator crosses above upper threshold, bearish regime activates when crossing below lower threshold, neutral regime persists until directional threshold breach.

Pivot Identification: Swing highs and lows detected in both oscillator and price using configurable left/right parameters.

Divergence Pattern Matching: Compares pivot relationships between price and oscillator within min/max bar distance constraints to identify regular bullish (price LL, oscillator HL) and bearish (price HH, oscillator LH) divergences.

Together, these elements form a continuously updating momentum framework anchored in statistical context.

Interpretation

Adaptive RSI should be interpreted as context-aware momentum boundaries:

Bullish Regime (Blue): Activated when oscillator crosses above upper percentile threshold, indicating momentum strength relative to recent distribution favors upside continuation.

Bearish Regime (Red): Established when oscillator crosses below lower percentile threshold, identifying momentum weakness relative to recent distribution favors downside continuation.

Upper Threshold Line (Blue)**: Dynamic resistance level calculated from upper percentile of historical oscillator distribution - adapts higher during trending markets, lower during ranging conditions.

Lower Threshold Line (Red): Dynamic support level calculated from lower percentile of historical oscillator distribution - adapts lower during downtrends, higher during consolidation.

Regime Fill: Gradient coloring between oscillator and baseline (50) visualizes current momentum intensity - stronger color indicates greater distance from neutral.

Extreme Bands (15/85): Upper and lower extreme zones with strength-modulated transparency reveal momentum extremity - darker shading during powerful moves, lighter during moderate momentum.

Divergence Lines: Connect price and oscillator pivots when divergence pattern detected, appearing on both price chart and oscillator pane for confluence identification.

Reversal Markers (✦): Diamond signals appear at 80+ (bearish extreme) and sub-15 (bullish extreme) levels, marking potential exhaustion zones independent of regime state.

Percentile context, divergence confirmation, and regime persistence outweigh isolated oscillator readings.

Signal Logic & Visual Cues

Adaptive RSI presents four primary interaction signals:

Regime Switch - Long : Oscillator crosses above upper percentile threshold after previously being in bearish or neutral regime, suggesting momentum strength shift favoring bullish continuation.

Regime Switch - Short : Oscillator crosses below lower percentile threshold after previously being in bullish or neutral regime, indicating momentum weakness shift favoring bearish continuation.

Regular Bullish Divergence (𝐁𝐮𝐥𝐥) : Price forms lower low while oscillator forms higher low, revealing positive momentum divergence during downtrends - often precedes reversal or consolidation.

Regular Bearish Divergence (𝐁𝐞𝐚𝐫) : Price forms higher high while oscillator forms lower high, revealing negative momentum divergence during uptrends - often precedes reversal or correction.

Alert generation covers regime switches, threshold crossings, and divergence detection for systematic monitoring.

Strategy Integration

Adaptive RSI fits within momentum-informed and mean-reversion trading approaches:

Adaptive Regime Following : Use threshold crossings as primary trend inception signals where momentum confirms directional breakouts within statistical context.

Divergence-Based Reversals : Enter counter-trend positions when divergence patterns appear at extreme oscillator levels (above 80 or below 20) for high-probability mean-reversion setups.

Threshold-Aware Scaling : Recognize that tighter percentile spreads (e.g., 45/50) generate more signals suitable for ranging markets, while wider spreads (e.g., 30/70) filter for stronger trend confirmation.

Extreme Zone Confluence : Combine reversal markers (✦) with divergence signals for maximum-conviction exhaustion entries.

Multi-Timeframe Regime Alignment : Apply higher-timeframe regime context to filter lower-timeframe entries, taking only setups aligned with dominant momentum direction.

Smoothing Optimization : Increase smoothing length in choppy markets to reduce false signals, decrease in trending markets for faster response.

Technical Implementation Details

Core Engine : HMA-preprocessed RSI with configurable smoothing (SMA, HMA, EMA, WMA, DEMA, RMA, LINREG, TEMA)

Adaptive Model : Rolling percentile calculation over confirmed oscillator values with size-limited historical buffer

Threshold Construction : Linear interpolation percentile extraction from sorted distribution array

Regime Detection : State-persistent threshold crossing logic with confirmed bar validation

Divergence Engine : Pivot-based pattern matching with range filtering and duplicate prevention

Visualization : Gradient-filled regime zones, adaptive threshold lines, strength-modulated extreme bands, dual-pane divergence lines

Performance Profile : Optimized for real-time execution with efficient array management and minimal computational overhead

Optimal Application Parameters

Timeframe Guidance:

1 - 5 min : Micro-structure momentum detection for scalping and intraday reversals

15 - 60 min : Intraday regime identification with divergence-validated turning points

4H - Daily : Swing and position-level momentum analysis with macro divergence context

Suggested Baseline Configuration:

RSI Length : 18

Source : Close

Smooth Oscillator : Enabled

Smoothing Length : 20

Smoothing Type : SMA

Adaptive Lookback : 1000

Upper Percentile : 50

Lower Percentile : 45

Divergence Pivot Left : 15

Divergence Pivot Right : 15

Min Pivot Distance : 5

Max Pivot Distance : 60

These suggested parameters should be used as a baseline; their effectiveness depends on the asset's volatility profile, momentum characteristics, and preferred signal frequency, so fine-tuning is expected for optimal performance.

Parameter Calibration Notes

Use the following adjustments to refine behavior without altering the core logic:

Too many whipsaw signals : Widen percentile spread (e.g., 40/60 instead of 45/50) to demand stronger momentum confirmation, or increase "Smoothing Length" to filter noise.

Missing legitimate regime changes : Tighten percentile spread (e.g., 48/52 instead of 45/50) for earlier detection, or decrease "Smoothing Length" for faster response.

Oscillator too choppy : Increase "Smoothing Length" for cleaner readings, or switch "Smoothing Type" to RMA/TEMA for heavier smoothing.

Thresholds not adapting properly : Reduce "Adaptive Lookback" to emphasize recent behavior (500-800 bars), or increase it for more stable thresholds (1500-2000 bars).

Too many divergence signals : Increase "Pivot Left/Right" values to demand stronger swing confirmation, or widen "Min Pivot Distance" to space out detections.

Missing significant divergences : Decrease "Pivot Left/Right" for faster pivot detection, or increase "Max Pivot Distance" to compare more distant swings.

Prefer different momentum sensitivity : Adjust "RSI Length" - lower values (10-14) for aggressive response, higher values (21-28) for smoother trend confirmation.

Divergences appearing too late : Reduce "Pivot Right" parameter to detect divergences closer to current price action.

Adjustments should be incremental and evaluated across multiple session types rather than isolated market conditions.

Performance Characteristics

High Effectiveness:

Markets with mean-reverting characteristics and consistent momentum cycles

Instruments where momentum extremes reliably precede reversals or consolidations

Ranging environments where percentile-based thresholds adapt to volatility contraction

Divergence-driven strategies targeting momentum exhaustion before price confirmation

Reduced Effectiveness:

Extremely strong trending markets where oscillator remains persistently extreme

Low-liquidity environments with erratic momentum readings

News-driven or gapped markets where momentum disconnects from price temporarily

Markets with regime shifts faster than adaptive lookback can recalibrate

Integration Guidelines

Confluence : Combine with BOSWaves structure, volume analysis, or traditional support/resistance

Threshold Respect : Trust signals that occur after clean threshold crossings with sustained momentum

Divergence Context : Prioritize divergences appearing at extreme oscillator levels (80+/15-) over those in neutral zones

Regime Awareness : Consider whether current market regime matches historical momentum patterns used for calibration

Multi-Pattern Confirmation : Seek divergence patterns coinciding with reversal markers or threshold rejections for maximum conviction

Disclaimer

Adaptive RSI is a professional-grade momentum and divergence analysis tool. It uses percentile-based threshold calculation that adapts to recent market behavior but cannot predict future regime shifts or guarantee reversal timing. Results depend on market conditions, parameter selection, lookback period appropriateness, and disciplined execution. BOSWaves recommends deploying this indicator within a broader analytical framework that incorporates price structure, volume context, and comprehensive risk management.

Multi Cycles Slope-Fit System MLMulti Cycles Predictive System : A Slope-Adaptive Ensemble

Executive Summary:

The MCPS-Slope (Multi Cycles Slope-Fit System) represents a paradigm shift from static technical analysis to adaptive, probabilistic market modeling. Unlike traditional indicators that rely on a single algorithm with fixed settings, this system deploys a "Mixture of Experts" (MoE) ensemble comprising 13 distinct cycle and trend algorithms.

Using a Gradient-Based Memory (GBM) learning engine, the system dynamically solves the "Cycle Mode" problem by real-time weighting. It aggressively curve-fits the Slope of component cycles to the Slope of the price action, rewarding algorithms that successfully predict direction while suppressing those that fail.

This is a non-repainting, adaptive oscillator designed to identify market regimes, pinpoint high-probability reversals via OB/OS logic, and visualize the aggregate consensus of advanced signal processing mathematics.

1. The Core Philosophy: Why "Slope" Matters:

In technical analysis, most traders focus on Levels (Price is above X) or Values (RSI is at 70). However, the primary driver of price action is Momentum, which is mathematically defined as the Rate of Change, or the Slope.

This script introduces a novel approach: Slope Fitting.

Instead of asking "Is the cycle high or low?", this system asks: "Is the trajectory (Slope) of this cycle matching the trajectory of the price?"

The Dual-Functionality of the Normalized Oscillator

The final output is a normalized oscillator bounded between -1.0 and +1.0. This structure serves two critical functions simultaneously:

Directional Bias (The Slope):

When the Combined Cycle line is rising (Positive Slope), the aggregate consensus of the 13 algorithms suggests bullish momentum. When falling (Negative Slope), it suggests bearish momentum. The script measures how well these slopes correlate with price action over a rolling lookback window to assign confidence weights.

Overbought / Oversold (OB/OS) Identification:

Because the output is mathematically clipped and normalized:

Approaching +1.0 (Overbought): Indicates that the top-weighted algorithms have reached their theoretical maximum amplitude. This is a statistical extreme, often preceding a mean reversion or trend exhaustion.

Approaching -1.0 (Oversold): Indicates the aggregate cycle has reached maximum bearish extension, signaling a potential accumulation zone.

Zero Line (0.0): The equilibrium point. A cross of the Zero Line is the most traditional signal of a trend shift.

2. The "Mixture of Experts" (MoE) Architecture:

Markets are dynamic. Sometimes they trend (Trend Following works), sometimes they chop (Mean Reversion works), and sometimes they cycle cleanly (Signal Processing works). No single indicator works in all regimes.

This system solves that problem by running 13 Algorithms simultaneously and voting on the outcome.

The 13 "Experts" Inside the Code:

All algorithms have been engineered to be Non-Repainting.

Ehlers Bandpass Filter: Extracts cycle components within a specific frequency bandwidth.

Schaff Trend Cycle: A double-smoothed stochastic of the MACD, excellent for cycle turning points.

Fisher Transform: Normalizes prices into a Gaussian distribution to pinpoint turning points.

Zero-Lag EMA (ZLEMA): Reduces lag to track price changes faster than standard MAs.

Coppock Curve: A momentum indicator originally designed for long-term market bottoms.

Detrended Price Oscillator (DPO): Removes trend to isolate short-term cycles.

MESA Adaptive (Sine Wave): Uses Phase accumulation to detect cycle turns.

Goertzel Algorithm: Uses Digital Signal Processing (DSP) to detect the magnitude of specific frequencies.

Hilbert Transform: Measures the instantaneous position of the cycle.

Autocorrelation: measures the correlation of the current price series with a lagged version of itself.

SSA (Simplified): Singular Spectrum Analysis approximation (Lag-compensated, non-repainting).

Wavelet (Simplified): Decomposes price into approximation and detail coefficients.

EMD (Simplified): Empirical Mode Decomposition approximation using envelope theory.

3. The Adaptive "GBM" Learning Engine

This is the "Machine Learning" component of the script. It does not use pre-trained weights; it learns live on your chart.

How it works:

Fitting Window: On every bar, the system looks back 20 days (configurable).

Slope Correlation: It calculates the correlation between the Slope of each of the 13 algorithms and the Slope of the Price.

Directional Bonus: It checks if the algorithm is pointing in the same direction as the price.

Weight Optimization:

Algorithms that match the price direction and correlation receive a higher "Fit Score."

Algorithms that diverge from price action are penalized.

A "Softmax" style temperature function and memory decay allow the weights to shift smoothly but aggressively.

The Result: If the market enters a clean sine-wave cycle, the Ehlers and Goertzel weights will spike. If the market explodes into a linear trend, ZLEMA and Schaff will take over, suppressing the cycle indicators that would otherwise call for a premature top.

4. How to Read the Interface:

The visual interface is designed for maximum information density without clutter.

The Dashboard (Bottom Left - GBM Stats)

Combined Fit: A percentage score (0-100%). High values (>70%) mean the system is "Locked In" and tracking price accurately. Low values suggest market chaos/noise.

Entropy: A measure of disorder. High entropy means the algorithms disagree (Neutral/Chop). Low entropy means the algorithms are unanimous (Strong Trend).

Top 1 / Top 3 Weight: Shows how concentrated the decision is. If Top 1 Weight is 50%, one algorithm is dominating the decision.

The Matrix (Bottom Right - Weight Table)

This table lifts the hood on the engine.

Fit Score: How well this specific algo is performing right now.

Corr/Dir: Raw correlation and Direction Match stats.

Weight: The actual percentage influence this algorithm has on the final line.

Cycle: The current value of that specific algorithm.

Regime: Identifies if the consensus is Bullish, Bearish, or Neutral.

The Chart Overlay

The Line: The Gradient-Colored line is the Weighted Ensemble Prediction.

Green: Bullish Slope.

Red: Bearish Slope.

Triangles: Zero-Cross signals (Bullish/Bearish).

"STRONG" Labels: Appears when the cycle sustains a value above +0.5 or below -0.5, indicating strong momentum.

Background Color: Changes subtly to reflect the aggregate Regime (Strong Up, Bullish, Neutral, Bearish, Strong Down).

5. Trading Strategies:

A. The Slope Reversal (OB/OS Fade)

Concept: Catching tops and bottoms using the -1/+1 normalization.

Signal: Wait for the Combined Cycle to reach extreme values (>0.8 or <-0.8).

Trigger: The entry is taken not when it hits the level, but when the Slope flips.

Short: Cycle hits +0.9, color turns from Green to Red (Slope becomes negative).

Long: Cycle hits -0.9, color turns from Red to Green (Slope becomes positive).

B. The Zero-Line Trend Join

Concept: Joining an established trend after a correction.

Signal: Price is trending, but the Cycle pulls back to the Zero line.

Trigger: A "Triangle" signal appears as the cycle crosses Zero in the direction of the higher timeframe trend.

C. Divergence Analysis

Concept: Using the "Fit Score" to identify weak moves.

Signal: Price makes a Higher High, but the Combined Cycle makes a Lower High.

Confirmation: Check the GBM Stats table. If "Combined Fit" is dropping while price is rising, the trend is decoupling from the cycle logic. This is a high-probability reversal warning.

6. Technical Configuration:

Fitting Window (Default: 20): The number of bars the ML engine looks back to judge algorithm performance. Lower (10-15) for scalping/quick adaptation. Higher (30-50) for swing trading and stability.

GBM Learning Rate (Default: 0.25): Controls how fast weights change.

High (>0.3): The system reacts instantly to new behaviors but may be "jumpy."

Low (<0.15): The system is very smooth but may lag in regime changes.

Max Single Weight (Default: 0.55): Prevents one single algorithm from completely hijacking the system, ensuring an ensemble effect remains.

Slope Lookback: The period over which the slope (velocity) is calculated.

7. Disclaimer & Notes:

Repainting: This indicator utilizes closed bar data for calculations and employs non-repainting approximations of SSA, EMD, and Wavelets. It does not repaint historical signals.

Calculations: The "ML" label refers to the adaptive weighting algorithm (Gradient-based optimization), not a neural network black box.

Risk: No indicator guarantees future performance. The "Fit Score" is a backward-looking metric of recent performance; market regimes can shift instantly. Always use proper risk management.

Author's Note

The MCPS-Slope was built to solve the frustration of "indicator shopping." Instead of switching between an RSI, a MACD, and a Stochastic depending on the day, this system mathematically determines which one is working best right now and presents you with a single, synthesized data stream.

If you find this tool useful, please leave a Boost and a Comment below!

Adaptive Log Trend Zones + Retest SignalsAdaptive Log Trend Zones + Retest Signals

Adaptive Log Trend Zones is a trend-following overlay built to identify high-probability breakout retests in strong market conditions. It combines logarithmic regression , volatility-adaptive behavior , and ATR-based trend zones to help traders stay aligned with dominant momentum while avoiding chop.

🔹 Core Features

Logarithmic Regression Midline

Uses linear regression on log price to better handle exponential market moves

Produces smoother, more realistic trend structure on higher timeframes

Volatility-Adaptive Lookback

Automatically expands or contracts the regression length based on ATR volatility

Reacts faster in high volatility, smoother in consolidation

Dynamic Trend Zones

Upper and lower bands are ATR-adjusted and trend-colored

Optional future projection for visual trend guidance

Breakout → Retest Signal Logic

Detects clean breakouts beyond the trend zone

Waits for a controlled pullback (retest) before signaling

Signals only trigger when trend strength is confirmed

Trend Quality Filter

Internal regime detection filters out low-quality, sideways conditions

Uses slope strength and volatility compression to validate entries

🔹 Signals

BUY : Bullish breakout followed by a valid retest in a trending regime

SELL : Bearish breakout followed by a valid retest in a trending regime

Signals are designed for trend continuation , not mean reversion.

🔹 Best Use Cases

Crypto, Forex, and Index markets

Higher timeframes (15m+ recommended)

Trend continuation and pullback strategies

⚠️ Notes

This indicator is not a standalone trading system . Always use proper risk management and confirm signals with structure, volume, or higher-timeframe context.

Designed for traders who prefer structure, patience, and momentum alignment.

Volatility Trend Score [BackQuant]Volatility Trend Score

Overview

Volatility Trend Score is a trend-strength and regime-evaluation indicator built to measure directional persistence, not just direction. Most trend tools answer “up or down” using slope, crossovers, or a single condition. This indicator answers a more useful question for real trading: “How consistently is trend structure holding up once volatility is accounted for?”

It does this by building a volatility-scaled trailing structure (ATR-based) and then scoring how that structure evolves over a configurable lookback range. The output is a continuous score that rises when trend is persistent and decays when price action becomes noisy, mean-reverting, or unstable.

What it is measuring (the real goal)

This indicator is not trying to predict reversals. It is trying to quantify whether the market is behaving like a trend market or a chop market. It focuses on:

Persistence: does structure keep pushing in one direction bar after bar?

Stability: are pullbacks being absorbed without breaking the trailing structure?

Regime: is the market trending strongly enough to justify directional bias?

If you already have entries from other systems, this becomes a high-quality trend filter and trade management layer.

Core idea

At its foundation, the indicator combines two parts:

A volatility-adjusted trailing level derived from ATR and a user-defined factor.

A rolling persistence score that compares the current trail to prior trail values over a configurable loop window.

The trailing structure adapts to volatility and enforces one-sided movement, while the scoring logic converts that behavior into a numeric measure of trend quality.

Inputs and what they actually control

Average True Range Period (calc_p)

Defines the ATR window used to estimate volatility. A higher value smooths the volatility estimate and makes the trailing structure less reactive.

Factor (atr_factor)

Scales the ATR band size. Higher values widen the trailing band, filtering more noise, reducing flip frequency, and generally producing slower but more stable regimes.

For Loop Start/End (start/end)

Defines the comparison window used to build the score. It effectively sets how many historical trail values the current trail is compared against.

Shorter ranges produce a faster, more responsive score.

Longer ranges produce a slower, more “confidence-based” score that only climbs when trend persistence is sustained.

Long/Short Thresholds (thresL/thresS)

Convert a continuous score into regime thresholds.

Long threshold is a “trend quality requirement” for bullish bias.

Short threshold is used as a deterioration / breakdown trigger via crossunder logic.

Volatility-adjusted trailing structure

The trailing line is built from ATR bands around price:

up = close + ATR * factor

dn = close - ATR * factor

Then a trailing value is maintained with one-sided ratcheting behavior:

If dn rises above the previous trail, the trail steps up (ratchets upward).

If up drops below the previous trail, the trail steps down (ratchets downward).

This “ratchet” behavior is important. It prevents the trail from oscillating with small countertrend moves, forcing the trail to represent meaningful structure rather than micro-noise. On-chart, this trail often behaves like dynamic support/resistance in trends.

Why the trail is a better base than raw price

Price itself is noisy, and volatility changes the meaning of “big move” vs “small move.” By anchoring structure to ATR:

A move is interpreted relative to current volatility, not in absolute points.

High-volatility chop is less likely to be misread as a trend.

Trend structure is normalized across assets and timeframes more reliably.

This is why the score remains usable even when switching from low-vol assets to high-vol crypto pairs.

Trend scoring logic

The score is built by repeatedly comparing the current trailing value to trailing values from prior bars across a loop window:

If current trail > trail , add +1

If current trail < trail , add -1

This is a persistence test, not a momentum calculation. In a strong trend, the trail should generally keep stepping in the trend direction, so current values will be greater than many past values (bullish) or lower than many past values (bearish). In chop, the trail fails to progress meaningfully, so the score compresses, oscillates, or bleeds out.

How to interpret the score

Think of the score as a “trend conviction meter”:

High positive values: bullish persistence, structure is advancing consistently.

Low positive values: bullish bias may exist, but trend quality is weak or unstable.

Near zero: indecision, range behavior, or frequent structure challenges.

Negative values: bearish dominance or sustained deterioration in structure.

The speed of score change matters too:

Fast expansion suggests a fresh regime gaining traction.

Slow grind suggests mature trend continuation.

Rapid compression often signals consolidation, exhaustion, or a transition phase.

Signals and regime transitions

This script uses two different styles of conditions (important detail):

Long condition: score > long threshold (state-based, persistent while true).

Short condition: crossunder(score, short threshold) (event-based trigger).

That means:

Long bias can remain active as long as score stays above the long threshold.

Short regime flips are triggered at the moment the score breaks down through the short threshold.

On the chart, long/short shapes are only plotted when the regime flips (first bar of the change), not on every bar, using:

Long shape when signal becomes 1 and previous signal was -1

Short shape when signal becomes -1 and previous signal was 1

This keeps signals clean and avoids spam, making it usable for alerts and regime tagging.

Visual presentation

The indicator is designed to work both as a panel oscillator and as an on-chart overlay:

Score plot (oscillator): color reflects active regime state.

Optional trail on price: volatility-scaled structure line on chart.

Optional threshold reference lines: clear regime boundaries.

Optional candle coloring: makes regime obvious without reading the panel.

Optional background shading: useful for quick scanning and backtesting visually.

You can use only the score, only the trail, or both together depending on your workflow.

Practical use cases

1) Trend filter for systems

Use the score as a regime gate:

Allow long entries only when score is above the long threshold.

Avoid longs when score compresses toward zero or loses the threshold.

Treat the short threshold break as “trend is no longer healthy.”

This often improves system expectancy by reducing exposure during low-conviction conditions.

2) Trend quality grading

Instead of treating all uptrends as equal:

Higher score = higher persistence, better continuation odds.

Score plateau = trend losing pressure, continuation becomes less reliable.

Score decay while price rises = trend is getting weaker under the hood.

This is useful for position sizing or deciding whether to add to winners.

3) Trade management and exits

Two complementary tools exist here:

Trail line can act as a dynamic stop reference or structure invalidation level.

Score behavior can be used to scale out when persistence fades (before a full flip).

Many traders use the trail for “hard structure” and the score for “soft deterioration.”

4) Breakout confirmation vs fakeouts

A breakout that immediately fails to build score is often low quality.

Healthy breakouts usually come with score expansion as structure advances.

Fakeouts often revert quickly, score fails to climb, and regime stays unstable.

Tuning guidelines

These are general behaviors you can expect when adjusting settings:

Higher ATR period and factor: slower regimes, fewer flips, cleaner structure.

Lower ATR period and factor: faster reaction, more sensitivity, more noise risk.

Longer loop range: score becomes more “confidence-based,” slower to change.

Shorter loop range: score becomes more “tactical,” faster but more jittery.

A good way to tune is to pick the trail behavior first (ATR period and factor), then tune the score window (loop) to match how quickly you want “trend conviction” to build.

Market behavior focus

Volatility Trend Score is most valuable in markets where volatility shifts frequently and fake trends are common, especially crypto. It is designed to:

Stay out of low-quality chop where most indicators whipsaw.

Quantify when volatility is being expressed directionally (constructive trend).

Provide a clean regime framework for filtering, alignment, and management.

Summary

Volatility Trend Score converts volatility-adjusted structure into a quantified measure of trend persistence. By combining an ATR-based trailing mechanism with a rolling comparison score, it provides a more reliable read on trend quality than single-condition indicators. It is best used as a regime filter, a trend strength gauge, and a trade management layer, helping you stay aligned with strong directional phases while avoiding low-conviction envir

Apex Adaptive Trend Navigator [Pineify]Apex Adaptive Trend Navigator

The Apex Adaptive Trend Navigator is a comprehensive trend-following indicator that combines adaptive moving average technology, dynamic volatility bands, and market structure analysis into a single, cohesive trading tool. Designed for traders who want to identify trend direction with precision while filtering out market noise, this indicator adapts its sensitivity based on real-time market efficiency calculations.

Key Features

Adaptive Moving Average with efficiency-based smoothing factor

Dynamic ATR-based volatility bands that expand and contract with market conditions

Market Structure detection including BOS (Break of Structure) and CHoCH (Change of Character)

Real-time performance dashboard displaying trend status and efficiency metrics

Color-coded cloud visualization for intuitive trend identification

How It Works

The core of this indicator is built on an Adaptive Moving Average that uses a unique efficiency-based calculation method inspired by the Kaufman Adaptive Moving Average (KAMA) and TRAMA concepts. The efficiency ratio measures the directional movement of price relative to total price movement over the lookback period:

Efficiency = |Price Change over N periods| / Sum of |Individual Bar Changes|

This ratio ranges from 0 to 1, where values closer to 1 indicate a strong trending market with minimal noise, and values closer to 0 indicate choppy, sideways conditions. The smoothing factor is then squared to penalize noisy markets more aggressively, causing the adaptive line to flatten during consolidation and respond quickly during strong trends.

The Dynamic Volatility Bands are calculated using the Average True Range (ATR) multiplied by a user-defined factor. These bands create a channel around the adaptive moving average, helping traders visualize the current volatility regime and potential support/resistance zones.

Trading Ideas and Insights

When price stays above the adaptive line with the bullish cloud forming, consider this a confirmation of uptrend strength

The efficiency percentage in the dashboard indicates trend quality - higher values suggest more reliable trends

Watch for price interactions with the upper and lower bands as potential reversal or continuation zones

A flat adaptive line indicates consolidation - wait for a clear directional break before entering trades

How Multiple Indicators Work Together

This indicator integrates three complementary analytical approaches:

The Adaptive Moving Average serves as the trend backbone, providing a dynamic centerline that automatically adjusts to market conditions. Unlike fixed-period moving averages, it reduces lag during trends while minimizing whipsaws during ranging markets.

The ATR Volatility Bands work in conjunction with the adaptive MA to create a volatility envelope. When the adaptive line is trending and price remains within the cloud (between the MA and outer band), this confirms trend strength. Price breaking through the opposite band may signal exhaustion or reversal.

The Market Structure Analysis using swing point detection adds a Smart Money Concepts (SMC) layer. BOS signals indicate trend continuation when price breaks previous swing highs in uptrends or swing lows in downtrends. CHoCH signals warn of potential reversals when the structure shifts against the prevailing trend.

Unique Aspects

The squared efficiency factor creates a non-linear response that dramatically reduces noise sensitivity

Cloud fills only appear on the trend side, providing clear visual distinction between bullish and bearish regimes

The integrated dashboard eliminates the need to switch between multiple indicators for trend assessment

Pivot-based swing detection ensures accurate market structure identification

How to Use

Add the indicator to your chart and adjust the Lookback Period based on your trading timeframe (shorter for scalping, longer for swing trading)

Monitor the cloud color - green clouds indicate bullish conditions, red clouds indicate bearish conditions

Use the efficiency reading in the dashboard to gauge trend reliability before entering positions

Consider entries when price pulls back to the adaptive line during strong trends (high efficiency)

Use the volatility bands as dynamic take-profit or stop-loss reference levels

Customization

Lookback Period : Controls the sensitivity of trend detection and swing point identification (default: 20)

Volatility Multiplier : Adjusts the width of the ATR bands (default: 2.0)

Show Market Structure : Toggle visibility of BOS and CHoCH labels

Show Performance Dashboard : Toggle the trend status table

Color Settings : Customize bullish, bearish, and neutral colors to match your chart theme

Conclusion

The Apex Adaptive Trend Navigator offers traders a sophisticated yet intuitive approach to trend analysis. By combining adaptive smoothing technology with volatility measurement and market structure concepts, it provides multiple layers of confirmation for trading decisions. Whether you are a day trader seeking quick trend identification or a swing trader looking for reliable trend-following signals, this indicator adapts to your market conditions and trading style. The efficiency-based calculations ensure you always know not just the trend direction, but also the quality and reliability of that trend.

ML-Inspired Adaptive Momentum Strategy (TradingView v6)This strategy demonstrates an adaptive momentum approach using volatility-normalized trend strength. It is designed for educational and analytical purposes and uses deterministic, fully transparent logic compatible with Pine Script v6.

ML-Inspired Concept (Educational Context)

Pine Script cannot train or execute real machine-learning models.

Instead, this strategy demonstrates ML-style thinking by:

Converting price data into features

Normalizing features to account for volatility differences

Producing a bounded confidence score

Applying thresholds for decision making

This is not predictive AI and does not claim forecasting capability.

Strategy Logic

EMA is used to measure directional bias

EMA slope represents momentum change

ATR normalizes the slope (feature scaling)

A clamped score between −1 and +1 is generated

Trades trigger only when the score exceeds defined thresholds

Risk & Execution

Position size capped at 5% equity

Commission and slippage included for realistic testing

Signals are calculated on closed bars only

Purpose

This script is intended to help traders explore adaptive momentum concepts and understand how feature normalization can be applied in systematic trading strategies.

Adaptive Strength Overlay (MTF) [BackQuant]Adaptive Strength Overlay (MTF)

A multi-timeframe RSI strength visualizer that projects oscillator “pressure” directly onto price using adaptive gradient fills between percent bands. Built to make strength, exhaustion, and regime context readable at a glance, without needing to stare at a separate oscillator panel.

Mean-Reversion mode example

What this indicator does

This indicator converts RSI strength into a chart overlay that reacts to momentum and extremes, then visualizes it as colored “pressure zones” around price.

Instead of plotting RSI in a sub-window, it:

Builds 1 to 3 symmetric percent bands above and below price.

Computes RSI strength on up to 3 different timeframes (MTF).

Smooths RSI with your selected moving average type.

Maps RSI values into discrete transparency “buckets”.

Fills between the bands with a gradient whose opacity reflects strength or exhaustion.

Displays a compact RSI table for all enabled timeframes.

Provides alert conditions for extremes and midline shifts on each timeframe.

The result is an overlay that looks like a dynamic envelope. When strength rises, the envelope “lights up” in the direction of the move. When strength becomes stretched, the outer zones become visually prominent.

Core idea: “Strength as an overlay”

RSI is normally interpreted in a separate oscillator panel. That makes context-switching slow:

You check price action.

You look down at RSI.

You mentally translate RSI into risk or trend bias.

This script removes that translation step by projecting strength directly onto the price area, using band fills as a visual language:

More visible fill = stronger strength or more extreme condition (depending on mode).

Less visible fill = weak strength or neutral state.

Two operating modes

1) Trend mode

Trend mode emphasizes strength aligned with direction:

When RSI is strong on the upside, upper bands become more visible.

When RSI is strong on the downside, lower bands become more visible.

Neutral RSI fades, so the chart de-clutters during chop.

Use Trend mode when:

You want a clean trend-following overlay.

You want to quickly see which timeframe(s) are powering the move.

You want to filter entries to moments when strength confirms direction.

2) Mean-Reversion mode

Mean-Reversion mode flips the emphasis to highlight exhaustion against the move :

Upper extremes become a “potential exhaustion” cue.

Lower extremes become a “potential exhaustion” cue.

The overlay is tuned to make stretched conditions obvious.

This is not an automatic “short overbought / long oversold” system. It is a visualization mode that makes “extended” conditions stand out faster, especially when multiple timeframes align.

How the bands work (Percent Bands)

The indicator constructs up to three symmetric envelopes around price:

Band 1: percent1 scaled by scale

Band 2: percent2 scaled by scale (optional)

Band 3: percent3 scaled by scale (optional)

The percent bands are simple deviations from the selected price source:

Upper = price * (1 + (percent * scaling)/100)

Lower = price * (1 - (percent * scaling)/100)

Why this matters:

It anchors “strength visualization” to meaningful price distance.

It makes the overlay comparable across assets because it’s percent-based.

It gives you a consistent spatial frame for reading momentum versus extension.

Multi-timeframe engine (MTF)

The script runs the same strength calculation on up to three timeframes:

Timeframe 1 uses the chart timeframe by default (empty string input).

Timeframe 2 is optional and defaults to Daily.

Timeframe 3 is optional and defaults to Weekly.

Each timeframe has:

Its own RSI period (len, len2, len3).

Its own smoothing length (slen, slen2, slen3).

The same smoothing type selection (EMA, HMA, etc).

This creates a layered view:

TF1 often reflects tactical pressure (entries/exits).

TF2 reflects structural pressure (swing context).

TF3 reflects macro bias (regime context).

When multiple timeframes agree, the fills stack and the overlay becomes visually louder. When they disagree, the overlay looks mixed or muted, which is exactly the point.

Smoothing options (why so many)

Raw RSI can be noisy. This script lets you smooth RSI with multiple MA types, which changes how “responsive” the overlay feels:

EMA/RMA smooth without lagging as hard as SMA.

HMA responds faster but can be twitchy.

LINREG can feel more “structural”.

ALMA and T3/TEMA provide heavier smoothing profiles with different lag characteristics.

This isn’t cosmetic. Your smoothing choice affects:

How early the overlay “lights up” in Trend mode.

How long extremes remain highlighted in Mean-Reversion mode.

How often fills flicker in chop.

Strength mapping (the transparency buckets)

Instead of mapping RSI to a continuous color scale, the script uses a discrete transparency ladder. That creates a clean, readable visual that avoids constant flickering.

The logic assigns two transparency values per timeframe:

Upper-side transparency responds to lower RSI zones (weak upside strength).

Lower-side transparency responds to higher RSI zones (strong upside strength).

Then the script uses those transparencies differently depending on mode:

Trend mode shows “strength aligned with direction”.

Mean-Reversion mode swaps the emphasis so “extremes” stand out as potential stretch.

You can think of it as:

Trend mode highlights continuation strength.

Mean-Reversion mode highlights potential exhaustion.

Fill stacking (how the overlay is built)

The overlay uses layered fills:

Fill from price to Band 1

Fill from Band 1 to Band 2 (if enabled)

Fill from Band 2 to Band 3 (if enabled)

Upper side uses the negative color (typically red) and lower side uses the positive color (typically green), because upper bands represent “above price” space and lower bands represent “below price” space. The intensity is controlled by the computed transparency per timeframe and selected mode.

Important behavior:

Disabling Band 2 or Band 3 can change how the stacked fills look, because you are removing fill segments.

If you want a clean look, run only Band 1.

If you want a “regime heat” look, run Bands 1–3 with higher scaling.

Table (MTF RSI dashboard)

A compact table prints RSI values for each configured timeframe:

Row labels show TF.

Values show the smoothed RSI output that drives the overlay.

Use it for quick confirmation:

If overlay looks strong but table RSI is neutral, your band settings might be too tight.

If TF3 RSI is extreme while TF1 is neutral, you are likely in a macro stretched regime with local consolidation.

Alerts (built-in)

Alerts are provided for each timeframe separately, covering:

Entering upper extreme (cross above 70)

Exiting upper extreme (cross below 70)

Entering lower extreme (cross below 30)

Exiting lower extreme (cross above 30)

Bullish midline cross (cross above 50)

Bearish midline cross (cross below 50)

This enables workflows like:

Notify when TF2 enters extreme, then wait for TF1 mean-reversion confirmation.

Notify when TF3 crosses midline, then only take TF1 trend setups in that direction.

How to use it (practical reads)

Trend mode reads

Strong continuation: TF1 and TF2 fills become clearly visible on the same side.

Healthy pullback: TF1 fades but TF2 stays visible, suggesting underlying structure remains strong.

Chop warning: fills alternate or remain mostly invisible, indicating neutral strength.

Mean-Reversion mode reads

Exhaustion zones: outer fills become prominent near the extremes, signaling stretched conditions.

Compression after extreme: fill fades while price stabilizes, suggesting “cooling off” rather than immediate reversal.

Multi-TF stretch: TF2 and TF3 extremes together often mark higher significance zones.

Recommended setup presets

Preset A: Clean trend overlay

Mode: Trend

Bands: only Band 1

Scale: 1–2

Smoothing: EMA, moderate slen (6–10)

TF2: Daily on intraday charts

Preset B: Regime and exhaustion mapper

Mode: Mean-Reversion

Bands: Bands 1–3

Scale: 2–4

Smoothing: T3 or RMA, slightly higher slen

TF2: Daily, TF3: Weekly

Limitations

This is a strength visualization tool, not a full entry/exit system.

Percent bands are not volatility-adjusted, they are distance frames. In very high vol conditions, you may need higher band percentages or higher scaling.

MTF values update on their own timeframe closes, so higher timeframes will step rather than update every bar.

Options Gamma Flip Zones [BackQuant]Options Gamma Flip Zones

A market-structure style “gamma flip” mapper that builds adaptive strike-like zones, scores how price interacts with them, then promotes the strongest candidates into confirmed flip zones. Designed to highlight pinning, failed breaks, and rotational behavior without needing live options chain data.

What this indicator does

This script identifies price levels that behave like “strike magnets” during conditions that resemble options pinning, then draws dynamic zones around those levels.

Instead of assuming every round number matters, it:

Creates a strike ladder (auto or manual step).

Applies a regime filter that looks for “pin-friendly” market conditions.

Tracks and scores repeated interactions with the level.

Upgrades a zone from candidate to confirmed when enough evidence accumulates.

Invalidates zones when price achieves sustained acceptance away from them.

The output is a set of shaded boxes (zones) centered on strike-like levels, with text readouts that show the current state of each zone.

Key concept: “Gamma proxy”

A true gamma flip requires options positioning data. This indicator does not use options chain gamma.

Instead, it uses a proxy approach:

When markets have elevated volatility relative to their recent baseline AND trend strength is weak, price often behaves “sticky” around key levels.

In those conditions, repeated touches and failed escapes around a level behave similarly to pinning around strikes.

So this tool is best read as:

“Where would a strike-like magnet likely exist right now, based on price behavior and regime conditions?”

How zones are created

Zones only start forming when the script detects a pin-friendly regime.

1) Strike Ladder (level selection)

Auto Strike Step selects a step size based on current price magnitude (bigger price, bigger step).

Manual Strike Step lets you force a fixed increment.

The current “active level” is the nearest rounded level to price.

Major Level Every optionally marks major ladder levels (multiples of step).

2) Band construction (zone thickness)

Each zone is a symmetric band around the level, using one of two modes:

ATR mode scales thickness with volatility.

Percent mode scales thickness as a fraction of price.

This matters because “pin behavior” is not a single tick. It’s a region where price repeatedly probes and rejects.

Regime filter (when the script is allowed to believe in pinning)

A zone is only eligible to form and strengthen when Pin Regime is active. Pin Regime is a conjunction of:

1) IV proxy (ATR z-score)

Uses ATR as a volatility proxy.

Converts ATR% into a z-score relative to a long lookback.

IV Proxy Threshold controls how elevated volatility must be before the script considers pinning likely.

2) Weak trend requirement

The script also requires price action to be non-trending:

EMA spread must be small (fast vs slow EMA not diverging strongly).

ADX must be below a ceiling, confirming weak directional trend strength.

Interpretation:

High “IV proxy” + weak trend is where pin-like behavior is most common.

If trend is strong, zones are less meaningful because price is more likely to accept away from levels.

Flip confirmation logic (what upgrades a zone)

A zone is not “confirmed” just because price is near it once. The script builds conviction via evidence accumulation.

Evidence types:

Touches : price comes close to the level within tolerance.

Failed escapes : price pushes outside the band but closes back inside (rejection).

Acceptance run : consecutive closes outside the band, suggesting price is accepting away from the zone.

Protections:

Touch Cooldown prevents counting the same micro-chop as multiple touches.

Acceptance Bars defines what “real acceptance” means, so the zone does not get invalidated by one noisy bar.

A zone becomes confirmed when:

Touches meet the “evidence” requirement.

Failed escapes meet the “rejection” requirement.

The regime filter still says the market is pin-friendly.

That is important, it avoids promoting levels that only worked briefly in a trending tape.

Zone scoring and lifecycle

Each zone maintains a score that evolves over time. Think of score as “how much this level has recently behaved like a magnet.”

Score dynamics:

Decay per bar : score fades over time if price stops respecting the zone.

+ per touch : repeated proximity increases score.

+ per failed escape : rejections add stronger reinforcement.

- per acceptance bar : sustained trading outside reduces score.

Min score to draw : prevents clutter from weak, low-confidence zones.

Invalidation:

If the score becomes very weak AND price achieves sustained acceptance away from the zone, the zone is deleted.

This keeps the chart clean and ensures zones represent current market behavior, not ancient levels.

How to read the plot on chart

1) Zone fill and border

Each zone is drawn as a box extended to the right.

Fill opacity adapts to zone strength, strong zones are visually more prominent.

Border color encodes the current directional context and special events.

2) Bullish vs bearish coloring

A zone is colored bullish when price is currently trading above the zone’s mid-level.

A zone is colored bearish when price is currently trading below it.

This is not a trade signal by itself, it is a state cue for “which side is in control around the level.”

3) Failed escape highlighting

If price attempts to break above the band and fails, the border temporarily highlights as a failed up escape.

If price attempts to break below the band and fails, the border temporarily highlights as a failed down escape.

These are the moments where pin behavior is most visible:

Break attempt.

Immediate rejection.

Return to the band.

4) Midline (optional)

The zone midline is the strike-like level itself.

It is dotted to distinguish it from price structure lines.

5) Optional strike ladder overlay

When enabled, the script draws major and minor ladder lines near current price.

Major levels are thicker and less transparent.

This is a visualization aid for “where the algorithm is rounding,” not a prediction tool.

On-chart text readout (what the box text means)

Each box prints a compact state summary, designed for fast scanning:

Γ CANDIDATE means the zone is being tracked but not yet validated.

Γ FLIP (PROXY) means the zone has met confirmation requirements.

BULL/BEAR indicates which side price is on relative to the mid-level.

L prints the level value.

T is touch count, repeated proximity events.

F is fail count, rejected escape attempts.

IVz is the volatility proxy z-score at the moment.

ADX is the trend strength context.

Practical use cases

1) Pinning and range trading context

Confirmed zones often act like gravity wells in sideways or rotational regimes.

When price repeatedly fails to escape, fading outer edges can be reasonable context for mean reversion workflows.

2) Breakout validation

If price achieves acceptance outside the band for multiple bars, that is stronger breakout context than a single wick.

Zones that invalidate cleanly can mark transitions from pinning to directional move.

3) Time your “do nothing” periods

When Pin Regime is active and a zone is confirmed, the tape often becomes sticky and inefficient for trend chasing.

This helps avoid taking trend entries into a pin environment.

Alerts

Standalone alertconditions are included:

Zone Confirmed : a candidate becomes confirmed.

Zone Touch : price touches an active zone within tolerance.

Zone Invalidated : the zone loses relevance and is removed.

Tuning guidelines

Sensitivity vs quality