OPEN-SOURCE SCRIPT

CHAN CRYPTO RS

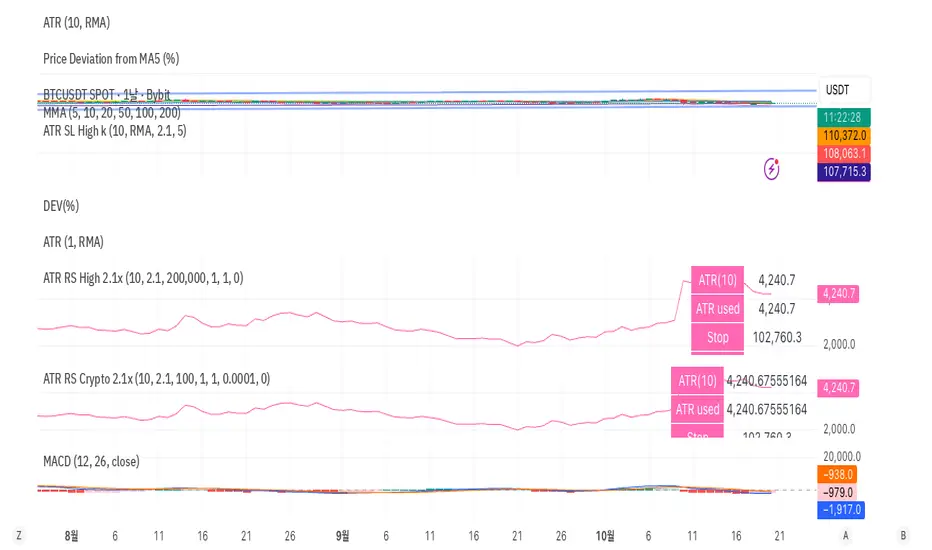

🩷 ATR RS (Crypto / High-based 2.1x, Decimal Safe v2)

This indicator is designed for crypto position sizing and stop calculation using ATR-based risk management. It helps traders automatically determine the stop price, per-unit risk, and optimal position size based on a fixed risk amount in USDT.

🔧 Core Logic

ATR Length (Daily RMA) — calculates the daily Average True Range (ATR) using RMA smoothing.

ATR Multiplier (2.1× default) — defines how far the stop is placed from the daily high.

Stop Price (for Longs) = Daily High − ATR × Multiplier

Per-Unit Risk = (Entry − Stop) × Point Value

Position Size = Risk Amount ÷ Per-Unit Risk

Automatically handles decimal precision for micro-priced crypto assets (e.g., PEPE, SHIB).

Includes safeguards for minimum size and maximum position caps.

💡 Features

Uses Daily ATR without lookahead (no repainting).

Dynamically switches between current and previous ATR for stable results when the daily bar isn’t yet confirmed.

“Snap to tick” ensures stop prices align with the symbol’s tick size.

Table display summarizes ATR, stop price, per-unit risk, total risk, size, and bet amount.

Optional stop label on the chart for visual clarity.

🧮 Output Table

Metric Description

ATR(10) Daily RMA-based ATR

ATR used Chosen ATR (current or previous)

Stop Calculated stop price

Per-unit Risk per coin/unit

Risk Total risk in USDT

Size Optimal position size

Bet Total position value (Entry × Size)

🧠 Ideal For

Crypto traders who use fixed-risk ATR strategies and need precise, decimal-safe position sizing even for ultra-low-priced tokens.

This indicator is designed for crypto position sizing and stop calculation using ATR-based risk management. It helps traders automatically determine the stop price, per-unit risk, and optimal position size based on a fixed risk amount in USDT.

🔧 Core Logic

ATR Length (Daily RMA) — calculates the daily Average True Range (ATR) using RMA smoothing.

ATR Multiplier (2.1× default) — defines how far the stop is placed from the daily high.

Stop Price (for Longs) = Daily High − ATR × Multiplier

Per-Unit Risk = (Entry − Stop) × Point Value

Position Size = Risk Amount ÷ Per-Unit Risk

Automatically handles decimal precision for micro-priced crypto assets (e.g., PEPE, SHIB).

Includes safeguards for minimum size and maximum position caps.

💡 Features

Uses Daily ATR without lookahead (no repainting).

Dynamically switches between current and previous ATR for stable results when the daily bar isn’t yet confirmed.

“Snap to tick” ensures stop prices align with the symbol’s tick size.

Table display summarizes ATR, stop price, per-unit risk, total risk, size, and bet amount.

Optional stop label on the chart for visual clarity.

🧮 Output Table

Metric Description

ATR(10) Daily RMA-based ATR

ATR used Chosen ATR (current or previous)

Stop Calculated stop price

Per-unit Risk per coin/unit

Risk Total risk in USDT

Size Optimal position size

Bet Total position value (Entry × Size)

🧠 Ideal For

Crypto traders who use fixed-risk ATR strategies and need precise, decimal-safe position sizing even for ultra-low-priced tokens.

오픈 소스 스크립트

트레이딩뷰의 진정한 정신에 따라, 이 스크립트의 작성자는 이를 오픈소스로 공개하여 트레이더들이 기능을 검토하고 검증할 수 있도록 했습니다. 작성자에게 찬사를 보냅니다! 이 코드는 무료로 사용할 수 있지만, 코드를 재게시하는 경우 하우스 룰이 적용된다는 점을 기억하세요.

면책사항

해당 정보와 게시물은 금융, 투자, 트레이딩 또는 기타 유형의 조언이나 권장 사항으로 간주되지 않으며, 트레이딩뷰에서 제공하거나 보증하는 것이 아닙니다. 자세한 내용은 이용 약관을 참조하세요.

오픈 소스 스크립트

트레이딩뷰의 진정한 정신에 따라, 이 스크립트의 작성자는 이를 오픈소스로 공개하여 트레이더들이 기능을 검토하고 검증할 수 있도록 했습니다. 작성자에게 찬사를 보냅니다! 이 코드는 무료로 사용할 수 있지만, 코드를 재게시하는 경우 하우스 룰이 적용된다는 점을 기억하세요.

면책사항

해당 정보와 게시물은 금융, 투자, 트레이딩 또는 기타 유형의 조언이나 권장 사항으로 간주되지 않으며, 트레이딩뷰에서 제공하거나 보증하는 것이 아닙니다. 자세한 내용은 이용 약관을 참조하세요.