OPEN-SOURCE SCRIPT

업데이트됨 Band Pass Normalized Suite (BPNS)

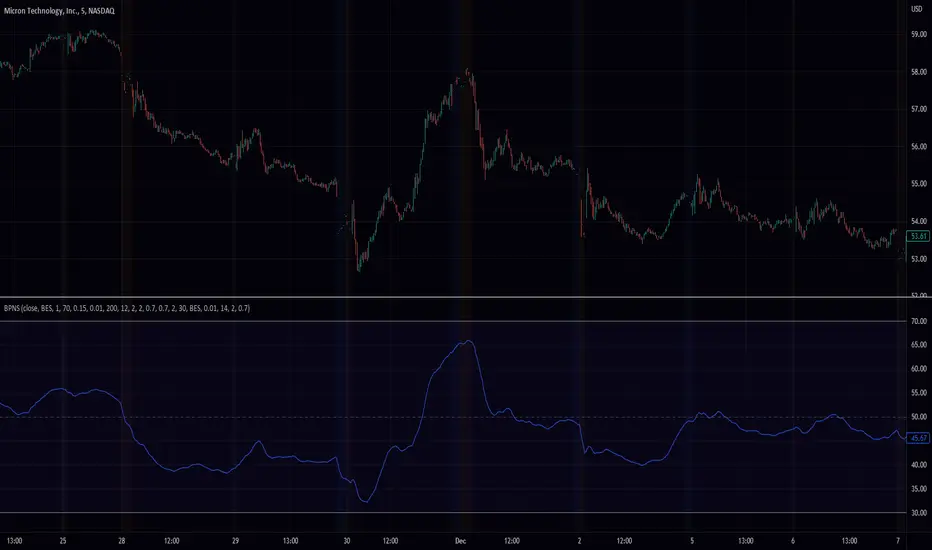

Outlier-Free Normalization and Band Pass Filtering

We present a technique for normalizing and filtering a given time series, source, in order to improve its stationarity and enhance its features. The technique includes two stages: outlier-free normalization and band pass filtering.

Outlier-Free Normalization:

In order to normalize source and reduce the impact of outliers, we first smooth the time series using an exponential moving average with a smoothing factor of alpha. The smoothed time series is then normalized by subtracting the minimum value within a given lookback period, dev_lookback, and dividing the result by the range (maximum - minimum) within the same lookback period. Outliers are detected and excluded from the normalization process by identifying values that are more than outlier_level standard deviations away from the exponentially smoothed average.

Band Pass Filtering:

After normalization, the time series is passed through a band pass filter to remove low and high frequency components. The specifics of the band pass filter implementation are not provided.

Code snippet:

bes(float source = close, float alpha = 0.7) =>

var float smoothed = na

smoothed := na(smoothed) ? source : alpha * source + (1 - alpha) * nz(smoothed[1])

max(source, outlier_level, dev_lookback)=>

var float max = na

src = array.new<float>()

stdev = math.abs((source - bes(source, 0.1))/ta.stdev(source, dev_lookback))

array.push(src, stdev < outlier_level ? source : -1.7976931348623157e+308)

max := math.max(nz(max[1]), array.get(src, 0))

min(source, outlier_level, dev_lookback) =>

var float min = na

src = array.new<float>()

stdev = math.abs((source - bes(source, 0.1))/ta.stdev(source, dev_lookback))

array.push(src, stdev < outlier_level ? source : 1.7976931348623157e+308)

min := math.min(nz(min[1]), array.get(src, 0))

min_max(src, outlier_level, dev_lookback) =>

(src - min(src, outlier_level, dev_lookback))/(max(src, outlier_level, dev_lookback) - min(src, outlier_level, dev_lookback)) * 100

To apply the outlier-free normalization and band pass filter to a given time series, source, the min_max() function can be called with the desired values for outlier_level and dev_lookback as arguments. For example:

normalized_source = min_max(source, 2, 50)

This will apply the outlier-free normalization and band pass filter to source, using an outlier_level of 2 standard deviations and a lookback period of 50 data points for both the normalization and outlier detection steps. The resulting normalized and filtered time series will be stored in normalized_source.

It is important to note that the choice of values for outlier_level and dev_lookback will have a significant impact on the resulting normalized and filtered time series. These values should be chosen carefully based on the characteristics of the input time series and the desired properties of the normalized and filtered output.

In conclusion, the outlier-free normalization and band pass filtering technique presented here provides a useful tool for preprocessing time series data and improving its stationarity and feature content. The flexibility of the method, through the choice of outlier_level and dev_lookback values, allows it to be tailored to the specific characteristics of the input time series.

We present a technique for normalizing and filtering a given time series, source, in order to improve its stationarity and enhance its features. The technique includes two stages: outlier-free normalization and band pass filtering.

Outlier-Free Normalization:

In order to normalize source and reduce the impact of outliers, we first smooth the time series using an exponential moving average with a smoothing factor of alpha. The smoothed time series is then normalized by subtracting the minimum value within a given lookback period, dev_lookback, and dividing the result by the range (maximum - minimum) within the same lookback period. Outliers are detected and excluded from the normalization process by identifying values that are more than outlier_level standard deviations away from the exponentially smoothed average.

Band Pass Filtering:

After normalization, the time series is passed through a band pass filter to remove low and high frequency components. The specifics of the band pass filter implementation are not provided.

Code snippet:

bes(float source = close, float alpha = 0.7) =>

var float smoothed = na

smoothed := na(smoothed) ? source : alpha * source + (1 - alpha) * nz(smoothed[1])

max(source, outlier_level, dev_lookback)=>

var float max = na

src = array.new<float>()

stdev = math.abs((source - bes(source, 0.1))/ta.stdev(source, dev_lookback))

array.push(src, stdev < outlier_level ? source : -1.7976931348623157e+308)

max := math.max(nz(max[1]), array.get(src, 0))

min(source, outlier_level, dev_lookback) =>

var float min = na

src = array.new<float>()

stdev = math.abs((source - bes(source, 0.1))/ta.stdev(source, dev_lookback))

array.push(src, stdev < outlier_level ? source : 1.7976931348623157e+308)

min := math.min(nz(min[1]), array.get(src, 0))

min_max(src, outlier_level, dev_lookback) =>

(src - min(src, outlier_level, dev_lookback))/(max(src, outlier_level, dev_lookback) - min(src, outlier_level, dev_lookback)) * 100

To apply the outlier-free normalization and band pass filter to a given time series, source, the min_max() function can be called with the desired values for outlier_level and dev_lookback as arguments. For example:

normalized_source = min_max(source, 2, 50)

This will apply the outlier-free normalization and band pass filter to source, using an outlier_level of 2 standard deviations and a lookback period of 50 data points for both the normalization and outlier detection steps. The resulting normalized and filtered time series will be stored in normalized_source.

It is important to note that the choice of values for outlier_level and dev_lookback will have a significant impact on the resulting normalized and filtered time series. These values should be chosen carefully based on the characteristics of the input time series and the desired properties of the normalized and filtered output.

In conclusion, the outlier-free normalization and band pass filtering technique presented here provides a useful tool for preprocessing time series data and improving its stationarity and feature content. The flexibility of the method, through the choice of outlier_level and dev_lookback values, allows it to be tailored to the specific characteristics of the input time series.

릴리즈 노트

chart fix오픈 소스 스크립트

트레이딩뷰의 진정한 정신에 따라, 이 스크립트의 작성자는 이를 오픈소스로 공개하여 트레이더들이 기능을 검토하고 검증할 수 있도록 했습니다. 작성자에게 찬사를 보냅니다! 이 코드는 무료로 사용할 수 있지만, 코드를 재게시하는 경우 하우스 룰이 적용된다는 점을 기억하세요.

면책사항

해당 정보와 게시물은 금융, 투자, 트레이딩 또는 기타 유형의 조언이나 권장 사항으로 간주되지 않으며, 트레이딩뷰에서 제공하거나 보증하는 것이 아닙니다. 자세한 내용은 이용 약관을 참조하세요.

오픈 소스 스크립트

트레이딩뷰의 진정한 정신에 따라, 이 스크립트의 작성자는 이를 오픈소스로 공개하여 트레이더들이 기능을 검토하고 검증할 수 있도록 했습니다. 작성자에게 찬사를 보냅니다! 이 코드는 무료로 사용할 수 있지만, 코드를 재게시하는 경우 하우스 룰이 적용된다는 점을 기억하세요.

면책사항

해당 정보와 게시물은 금융, 투자, 트레이딩 또는 기타 유형의 조언이나 권장 사항으로 간주되지 않으며, 트레이딩뷰에서 제공하거나 보증하는 것이 아닙니다. 자세한 내용은 이용 약관을 참조하세요.