OPEN-SOURCE SCRIPT

Black Scholes Model [racer8]

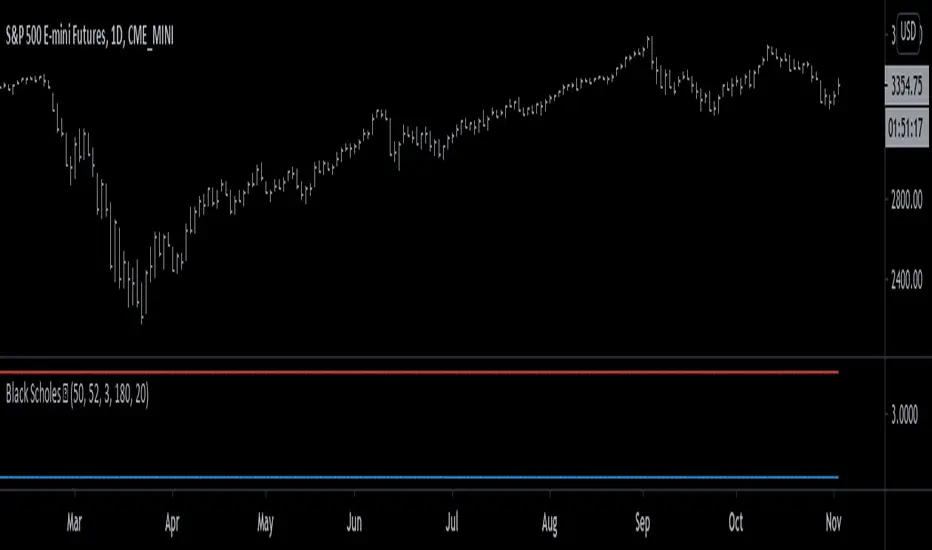

This is the Black Scholes Model. This indicator tells you the prices of both a call option & a put option.

Input variables are spot price, strike price, risk free rate %, days to maturity, and implied volatility %.

This indicator was made generally for educational purposes.

By using this indicator, you will develop a better understanding of how options are priced.

This indicator was made to be as simple as possible so that the user can easily understand it.

I recreated the Black Scholes Model because there is very little scripts on TV that are based on the Black Scholes Model.

I am aware that are Black Scholes Model (BSM) scripts already on TV, but mine is not the same. Correct me if I'm wrong, but I don't think there is a BSM script out there yet that relies on the exact same inputs that mine does.

Why use this indicator?

If you don't already have your own IV indicator...

You can use this indicator to approximate the value of implied volatility %.

You already know every input variable except IV%, and you know the call & put option prices.

So put in the numbers for each input and put a random number between 0 to 100 into the IV% input to get the options prices.

Adjust that random number for IV% until the output (options prices) matches correctly with what you already know they are to be.

This is called the trial and error method.

On the other hand, if you already know all input variables including IV%. Then you can use this indicator to find the call & put options prices directly.

Hope this helps. Enjoy 🙂

Input variables are spot price, strike price, risk free rate %, days to maturity, and implied volatility %.

This indicator was made generally for educational purposes.

By using this indicator, you will develop a better understanding of how options are priced.

This indicator was made to be as simple as possible so that the user can easily understand it.

I recreated the Black Scholes Model because there is very little scripts on TV that are based on the Black Scholes Model.

I am aware that are Black Scholes Model (BSM) scripts already on TV, but mine is not the same. Correct me if I'm wrong, but I don't think there is a BSM script out there yet that relies on the exact same inputs that mine does.

Why use this indicator?

If you don't already have your own IV indicator...

You can use this indicator to approximate the value of implied volatility %.

You already know every input variable except IV%, and you know the call & put option prices.

So put in the numbers for each input and put a random number between 0 to 100 into the IV% input to get the options prices.

Adjust that random number for IV% until the output (options prices) matches correctly with what you already know they are to be.

This is called the trial and error method.

On the other hand, if you already know all input variables including IV%. Then you can use this indicator to find the call & put options prices directly.

Hope this helps. Enjoy 🙂

오픈 소스 스크립트

트레이딩뷰의 진정한 정신에 따라, 이 스크립트의 작성자는 이를 오픈소스로 공개하여 트레이더들이 기능을 검토하고 검증할 수 있도록 했습니다. 작성자에게 찬사를 보냅니다! 이 코드는 무료로 사용할 수 있지만, 코드를 재게시하는 경우 하우스 룰이 적용된다는 점을 기억하세요.

면책사항

해당 정보와 게시물은 금융, 투자, 트레이딩 또는 기타 유형의 조언이나 권장 사항으로 간주되지 않으며, 트레이딩뷰에서 제공하거나 보증하는 것이 아닙니다. 자세한 내용은 이용 약관을 참조하세요.

오픈 소스 스크립트

트레이딩뷰의 진정한 정신에 따라, 이 스크립트의 작성자는 이를 오픈소스로 공개하여 트레이더들이 기능을 검토하고 검증할 수 있도록 했습니다. 작성자에게 찬사를 보냅니다! 이 코드는 무료로 사용할 수 있지만, 코드를 재게시하는 경우 하우스 룰이 적용된다는 점을 기억하세요.

면책사항

해당 정보와 게시물은 금융, 투자, 트레이딩 또는 기타 유형의 조언이나 권장 사항으로 간주되지 않으며, 트레이딩뷰에서 제공하거나 보증하는 것이 아닙니다. 자세한 내용은 이용 약관을 참조하세요.